Embed Size (px)

Citation preview

M I N I S T R Y O F I N T E R N AT I O N A L T R A D E A N D

I N D U S T R Y 2 0 1 2

MALAYSIA – ASEAN’S MULTINATIONAL MARKETPLACE

_

2

9

M

A

Y

2

0

1

2

_

_

S

H

A

N

G

R

I

L

A

H

O

T

E

L

_

_

K

U

A

L

A

L

U

M

P

U

R

_

1

MINISTRY OF INTERNATIONAL TRADE AND INDUSTRY 2012

CONTENTS

ASEAN in the Global Economic

Environment

Malaysia’s Economic Strength

Malaysia - ASEAN’s Multinational

Marketplace

2

ASEAN IN THE

GLOBAL

ECONOMIC

ENVIRONMENT

3

MINISTRY OF INTERNATIONAL TRADE AND INDUSTRY 2012

INDICATORS UNIT 2011

Total land area km2 4,435,670Total population million 606.93

Gross domestic product at current prices

US$ billion 2,153#

GDP growth percent 4.9#

Gross domestic product per capita at current prices

US$ 3547.4#

Merchandise trade US$ billion 2,045.7*

Export US$ billion 1,070.9*

Import US$ billion 974.8

Export of Services US$ billion 216.9 *

Foreign direct investments inflow US$ billion 76.2

Source : ASEAN Secretariat , DOSM and IHS Global Insight

#IMF Database

*2010 figures

**Exclude Brunei, Lao PDR and Myanmar

ASEAN ECONOMIC INDICATORS

4

MINISTRY OF INTERNATIONAL TRADE AND INDUSTRY 2012

ASEAN

$2,153b

China

$6,516b

Japan

$5,822b

India

$1,704b

Australia

and New

Zealand

$1,601b

ROK

$1,126b

Source : ASEAN Secretariat

Note: Figures are 2011 GDP

EU

$17,452b

USA

$15,227b

5

ASEAN IN THE GLOBAL ECONOMY

MINISTRY OF INTERNATIONAL TRADE AND INDUSTRY 2012

ASEAN COMMUNITY 2015

6

MINISTRY OF INTERNATIONAL TRADE AND INDUSTRY 2012

Single Market and Production

Base

Equitable Economic

Development

Competitive Economic Region

Integration into the Global Economy

4 Main Pillars

MAIN COMPONENTS OF AEC

7

MINISTRY OF INTERNATIONAL TRADE AND INDUSTRY 2012

AEC KEY PRIORITIES

AEC initiatives are on track and member states are committed

towards achieving AEC in 2015

Enhancing physical & non-physical connectivity – Aviation,

maritime & land transport , telecommunication and ICT

Integration of the goods, services and investments

Enhancing trade facilitation – operationalization of the ASEAN

Single Window

Elimination of non-tariff barriers

Promoting inclusive and sustainable growth – SME development

Enhancing regional economic partnership with dialogue partners –

ASEAN+FTAs

8

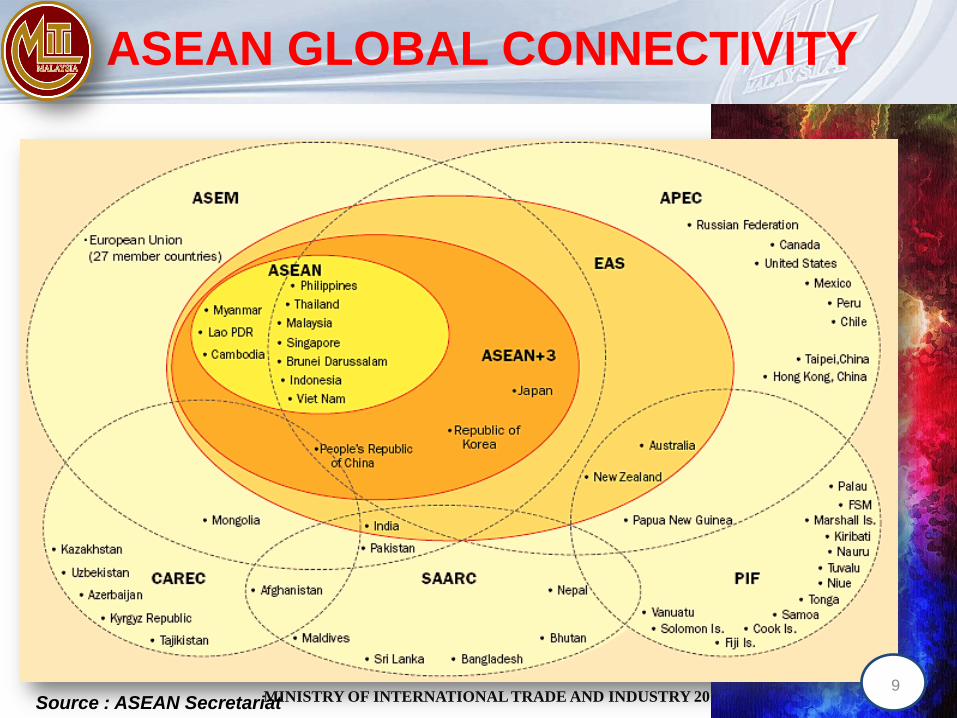

MINISTRY OF INTERNATIONAL TRADE AND INDUSTRY 2012Source : ASEAN Secretariat9

ASEAN GLOBAL CONNECTIVITY

MINISTRY OF INTERNATIONAL TRADE AND INDUSTRY 2012

Source : ASEAN Secretariat , IMF Database, DOSM and IHS Global Insight

10

ASEAN ECONOMY: SNAPSHOT

MINISTRY OF INTERNATIONAL TRADE AND INDUSTRY 2012

Intra-ASEAN

16.13%

Australia

2.32%

Canada

2.16%

China

3.76%

EU-27

22.42%

India

3.39%

Japan

11.02%

New

Zealand

0.12%

Korea

4.95%

USA

11.27%

Rest of the

World

22.46%

Source : ASEAN Secretariat11

SOURCES OF FDI TO ASEAN

12

12

Malaysia is strategically located in the most vibrant economicregion:

MALAYSIA – GATEWAY TO

REGIONAL MARKET

12

PREFERENTIAL MARKET ACCESS

13

13

Foreign companies based in Malaysia can enjoy preferential market access via Free Trade Agreements concluded by Malaysia:

Potential market of 600 million

Combined GDP of USD2.0 trillion, as of 2011

Already zero tariffs for 99% of products

ASEAN Economic Community and Single market by 2015

13

LAO PDR

PREFERENTIAL MARKET ACCESS

14

14

Potential market of 3.3 billionTariff reduction and elimination mostly by 2016

REGIONAL / BILATERAL FTAS

Other Potential Markets

China ChileKoreaJapan India Australia New Zealand

TPP EU Turkey

Potential market of 1.08 billion

14

BUSINESS

OPPORTUNITIES

FOR

MULTINATIONALS

IN MALAYSIA

1515

ACCESS TO HUGE MARKETS

AFTA ACFTA AKFTA AJCEP AIFTA AANZFTA

Market

Size

(million)

599 1,939 647 726 1,814 625

Econ size

(US$,

trillion)

1.9 7.7 2.9 7.3 3.4 3.2

Total

Trade

(US$,

billion)

519.8 751.8 618.4 726.4 575.2 582.6

Duty

phase out

date*

(A6+DP)

2010 2012 2012 2026 2019 2020

*For products in Normal Track

ACCESS TO HUGE MARKETS

1616

17

INVESTMENT IN SERVICES 2011

17

• 2011 GDP: 58.6 % is contributed by Services sector

GDP

• 2011 increase by 75.5 % compared to 2010.

• Domestic investment : RM48.2 million

• Foreign investment : RM4.1 billion

Investment in Services

• Approved projects : 3,597

• Expected to create about 43,784 employment

Projects

M I N I S T R Y O F I N T E R N AT I O N A L T R A D E A N D

I N D U S T R Y 2 0 1 2

STATUS OF LIBERALISATION OF SERVICES

SECTORS

2012 SERVICES LIBERALISATION

No of Sectors Implemented In Progress

17 9 8

Implemented

Telecommunications – ASP

Tech & Vocational Schools

Tech & Vocational Schools – Special

Needs

Private Hospitals

Departmental & Specialty Stores

Incineration Services

Accounting (incl audit)/Taxation

Skills Training Centres

Courier Services

In Progress

Legal Services

Telecommunications (NSP & NFP)

Private Universities

International Schools

Medical Specialists

Dental Specialists

Architects

Engineers

18

Electronics & Electrical

Industries :

Machinery &

Equipment:

• High-technology based products

using

wireless & convergence

technology

• Mobile application

• Solar wafer / cells / modules

• Semiconductors

• Automated equipment for semiconductor,

solar, medical & automotive industries

• Process machinery for food & beverages

and oil & gas

• Packaging machinery

Automotive Components :

• Transmission, brake, airbag,

and steering systems ,

automotive

seats & radiators

INVESTMENT OPPORTUNITIES IN MALAYSIA

(Manufacturing & Commodities)

19

Palm Oil Industry :

• Oleochemicals

• Palm-based nutraceuticals,

constituents of palm oil/palm

kernel oil & palm biomass

• Palm-based food products –

specialty animal fat replacer,

mayonnaise & salad dressing

Food Processsing Industry :

• Processed meat & seafood

• Beverages, food ingredients,

dairy products &

confectionary

Resourced-based industries :• Food & Agro based

• Value-added products

from natural resources

Petrochemical Industry : • Alpha-olefins & fatty alcohols,

propylene oxide & caprolactam

• Renewable & biodegradable

materials

20

INVESTMENT OPPORTUNITIES IN MALAYSIA

(Manufacturing & Commodities)

Hotel & Tourism Projects :• Hotels, tourist projects &

recreational camps

• Expansion, modernization

& renovation

INVESTMENT OPPORTUNITIES IN

MALAYSIA

(Services)

21

ICT Industry :

• Computer & computer

peripherals

• Telecommunications

• Photonics, optoelectronics,

optical fibres & cables

Engineering Services :

• Moulds and dies

• Machining, heat treatment

& surface engineering

M I N I S T R Y O F I N T E R N AT I O N A L T R A D E A N D

I N D U S T R Y 2 0 1 2

• Regional Establishments

• Logistics

• Tourism

• Environmental Management

• Healthcare Travel (Medical Tourism)

INVESTMENT OPPORTUNITIES IN THE

SERVICES SECTOR

22

M I N I S T R Y O F I N T E R N AT I O N A L T R A D E A N D

I N D U S T R Y 2 0 1 2

• Manufacturing• Departmental

stores

• Management consultancy• Islamic fund management• Tourism & travel related services

Foreign Equity

INVESTMENT POLICIES

23

M I N I S T R Y O F I N T E R N AT I O N A L T R A D E A N D

I N D U S T R Y 2 0 1 2

Pioneer Status

Income tax exemption ranging from 70% or 100% for a period

of 5 or 10 years

Investment Tax Allowance

60% or 100% on qualifying capital expenditure for 5 years

Reinvestment Allowance

60% on qualifying capital expenditure for 15 consecutive years

Import Duty & Sales Tax Exemption

For raw materials/components and Machinery and Equipment

Incentives

MAJOR INCENTIVES PROVIDED

24

M I N I S T R Y O F I N T E R N AT I O N A L T R A D E A N D

I N D U S T R Y 2 0 1 2

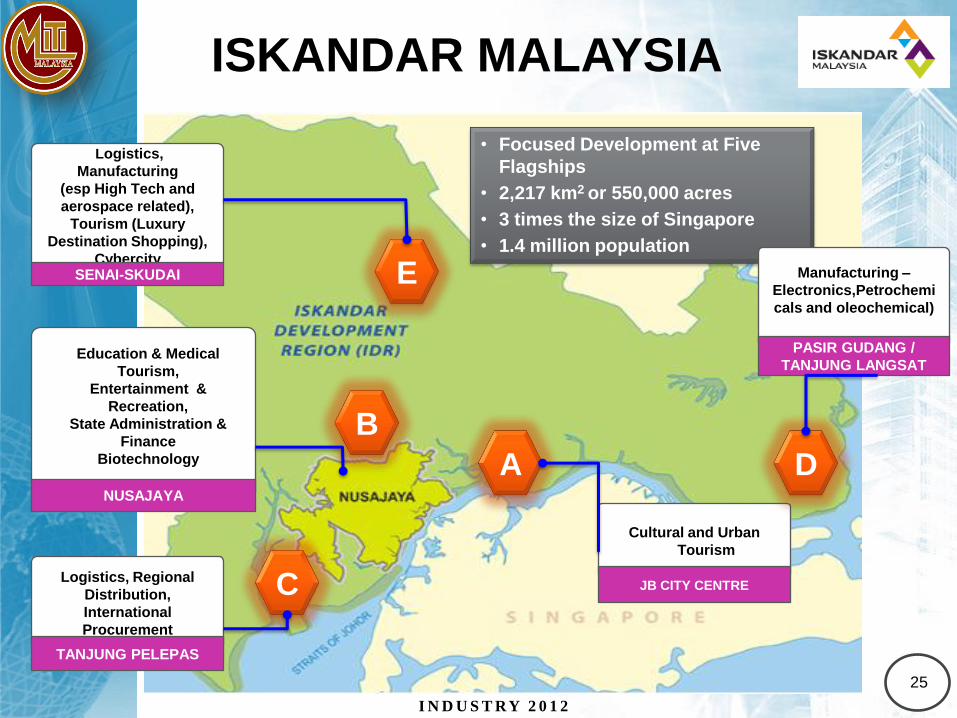

ISKANDAR MALAYSIA

Logistics,

Manufacturing

(esp High Tech and

aerospace related),

Tourism (Luxury

Destination Shopping),

CybercitySENAI-SKUDAI

Education & Medical

Tourism,

Entertainment &

Recreation,

State Administration &

Finance

Biotechnology

NUSAJAYA

Cultural and Urban

Tourism

JB CITY CENTRELogistics, Regional

Distribution,

International

Procurement

TANJUNG PELEPAS

• Focused Development at Five

Flagships

• 2,217 km2 or 550,000 acres

• 3 times the size of Singapore

• 1.4 million population

Manufacturing –

Electronics,Petrochemi

cals and oleochemical)

PASIR GUDANG /

TANJUNG LANGSAT

E

DA

B

C

2525

Projects Sector

Puteri Harbour, Nusajaya Leisure

Johor Premium Outlets, Kulaijaya Premium retail

Regency Specialist Hospital Healthcare

Pinewood Iskandar Malaysia Studios Creative

Management Development Institute

of Singapore (MDIS)

(EduCity)

Education

Raffles University

(EduCity)Education

Raffles American School

(Nusajaya, EduCity)Education

Excelsior International School

(Bandar Seri Alam)Education

Legoland Theme Park

Technocom Systems E&E

Bahru Stainless Sdn Bhd Manufacturing

ISKANDAR MALAYSIA

26

M I N I S T R Y O F I N T E R N AT I O N A L T R A D E A N D

I N D U S T R Y 2 0 1 2

27

Investment Opportunities :-

Agriculture,

Manufacturing

Tourism & Healthcare

Education & Human capital

Social Development

Area of Coverage : 17,816 sq kmInvestment Opportunities :-

Tourism

Oil, Gas & Petrochemical

Manufacturing

Agriculture

Education

Area of Coverage :

66,736 sq km

Investment Opportunities :-

Tourism

Logistics

Agriculture

Manufacturing

Area of Coverage : 73,997 sq km

Investment Opportunities :-

Aluminum Industry

Glass Industries

Steel Industries

Oil-based Industry

Palm Oil Industry

Area of coverage : 70,709 sq km

REGIONAL ECONOMIC CORRIDORS IN

MALAYSIA

27

M I N I S T R Y O F I N T E R N AT I O N A L T R A D E A N D

I N D U S T R Y 2 0 1 2

MSC MALAYSIA STATUS COMPANIES

Clusters Awarded* Operational**

Info Tech 2,195 1,622

Creative

Multimedia334 249

Shared Services

Outsourcing239 202

Institute of

Higher Learning

& Incubators

114 106

GRAND TOTAL 2,882 2,179

*All companies granted the MSC Malaysia

status

**Companies which are still active and

conducting MSC Malaysia approved activities

28

29

KEY NOTABLE ADDITIONS IN RECENT YEARS:

FOCUS HAS BEEN ON HIGH VALUE ACTIVITIES

1,500 man Global Development Center

3rd global location for monitoring and

data processing

Global Finance & IT Center

Global IT Center

Global Innovation Center

Regional Shared

Services Center

Nearshore Shared Services

Delivery Center

10,000 man Customer

Mgmt. Center

Regional Outsourcing

Center

4,000 man Global Campus

for IT, HR, Legal, Finance and

Technology Solutions.

R&D Center

Regional Support Center

Regional IT

Outsourcing Center

5,000 man

Software Devt.

Center

Regional Oil Gas

Data Processing

Center

MINISTRY OF INTERNATIONAL TRADE AND INDUSTRY 2012

8000 FOREIGN COMPANIES AND 400 MNC

IN MALAYSIA

30

MINISTRY OF INTERNATIONAL TRADE AND INDUSTRY 2012

8000 FOREIGN COMPANIES AND 400 MNC

IN MALAYSIA

31

MINISTRY OF INTERNATIONAL TRADE AND INDUSTRY 2012

ASEAN COMPANIES IN MALAYSIA

32

PT Rajawali (Hotel)

Thai Summit Autoparts

FPT Viet Nam

MALAYSIA IN ASEAN

3333

MINISTRY OF INTERNATIONAL TRADE AND INDUSTRY 2012

WHY MALAYSIA ?

34

Trainable & Educated

Labour Force

Political & Economic Stability

Well Developed

Infrastructure

Pro-business Government

Liberal Investment

PoliciesQuality of Life

MINISTRY OF INTERNATIONAL TRADE AND INDUSTRY 2012

1st

In Getting Credit For Business

– World Bank’s Doing Business 2012 Report

3rd

Attractive Location For Outsourcing Destinations

– A.T. Kearney Global Services Location Index 2011

10th

For FDI Confidence Index 2012 (18th

in 2011)

– A.T Kearney

4th

For Investor Protection

– World Economic Forum 2012, Global Competitiveness Report

21st

Global Competitiveness In 2011 (24th

in 2010 )

– World Economic Forum

18th

For Ease Of Doing Business (21st

in 2011)

– World Bank’s Doing Business 2012 Report

MALAYSIA’S INTERNATIONAL RANKING

35

36

MALAYSIAN COMPANIES IN

ASEAN

MALAYSIA COMPANIES IN ASEAN

COUNTRIES NO. OF

MALAYSIAN

COMPANIES *

AREAS

Brunei Darussalam 32 Finance Services, Airlines, Construction

Cambodia 66 Accounting and Audit, Banking, Garment,

Indonesia 105 Banking, Oil Palm Plantation, Telecommunication and

Engineering

Lao PDR 18 Financial Services and Hotel

Myanmar 20 Hotel, Oil and Gas, Manufacturing

Philippines 45 Machinery and Equipment, Electrical and Electronics, IT and

Hotel

Singapore 139 Banking, Logistics, Manufacturing, Hospitality Services,

Electrical and Electronics

Thailand 154 Garments, Automotive, Agriculture (Rubber) and Electric and

Electronics, Banking and Insurance

Viet Nam 25 Properties and Construction and Glassware

TOTAL 604Source: MIDA

*The list of number of companies is not exhaustive

37

MINISTRY OF INTERNATIONAL TRADE AND INDUSTRY 2012

MITI AND AGENCIES

Ministry of International Trade

and Industry Malaysia

38

MINISTRY OF INTERNATIONAL TRADE AND INDUSTRY 2012

Establishment of National Committee on

Investment (NCI)

MIDA as Central Coordinating Agency for

Investment Promotion

New role in Promoting Services Sectors

39

MINISTRY OF INTERNATIONAL TRADE AND INDUSTRY 2012

"1Malaysia Promotion" in

Muscat, Oman, 29 April

2012

Trade and Investment Promotion in

Myanmar, 24-25 February 2012

Exchange documents for China-

Malaysia Industrial Park in Qinzhou

of China, April 2012

40

MINISTRY OF INTERNATIONAL TRADE AND INDUSTRY 2012

THE WAY FORWARD

Malaysia’s Transformation Agenda remains a Key Priority. Connecting Malaysia with the Regional Caucus, example ASEAN,

TPP, and other FTAso implementation of Malaysia-Australia FTA (MAFTA)o Conclusion of ASEAN-India Agreements on Services and

Investments by December 2012o Realisation of a Regional Comprehensive Economic

Partnership (RCEP) involving ASEAN and the 6 DialoguePartners (China, Japan, Korea, Australia, New Zealand andIndia) – potential market of 3.3 billion people with 44% shareof global trade: Preparatory work has commenced; 4 Working Groups established – Trade in Goods,

Investments, Services and Rules of Origin; Drafttemplate of Agreement being discussed; and

Possible commencement of negotiations on Trade inGoods Agreement in 2013.

41

MINISTRY OF INTERNATIONAL TRADE AND INDUSTRY 2012

THE WAY FORWARD

High value-added industry and high-value jobs

Aligning with Best Practices and Standards

Enhancing Transparency in the Rule MakingProcess in the Government through OnlinePublic Engagement for Introduction of New orReview of Existing Government Rules andPolicies

42

MINISTRY OF INTERNATIONAL TRADE AND INDUSTRY 2012

THE WAY FORWARD

Deeper integration in ASEAN through the implementation of ASEANEconomic Community 2015 –

Malaysia on track – 80.8 % of measures implemented as at March2012 (ASEAN’s average 75.6%)

Further improvements to be made in 2013 and 2015 on Malaysia’sexisting commitments in 96 services sub-sectors in ASEANFramework Agreement in Services (AFAS).

Liberalisation of 16 new services sectors by Malaysia under AFAS tobe made in 2013 and another 16 in 2015;

Real-estate services;

Tourism and related services;

Transport related services; and

Logistics.

43

THANK YOU

44