Embed Size (px)

Citation preview

Construction fraud in Canada—Understand it, prevent it, detect it

A Grant Thornton white paper for construction and real estate companies

For businesses or individuals involved in residential or commercial construction, it’s critical to understand the severity of fraud, the most common types of fraud schemes and what you can do to prevent and detect them within your business.

Table of Contents

3 Construction fraud is pervasive

4 Evidence of fraud isn’t hard to uncover

5 Who is committing construction fraud and how?

7 What can you do? Stay vigilant and take control

8 Preserve business, uphold your reputation and avoid financial loss

9 Action is key to keeping fraud outside your risk perimeter

10 Appendix

11 About us

3

This paper examines construction fraud in Canada and the factors that facilitate it. We also look at 10 common fraud schemes and provide practical advice on fighting them.

Construction numbers remain strong in Canada, particularly in Toronto where “there are about 148 skyscrapers and high-rises under construction, far more than any other city in North America,” with “400 planned developments marketing their condos across the Greater Toronto Area.”3 Given the investment dollars involved and the potential for loss on multiple fronts—from money to reputation to legal action—the industry needs to stand up and take action.

For any businesses or individuals involved in residential or commercial construction—including construction firms, construction lawyers, real estate companies, property development companies, property management companies and real estate investors—understanding the severity of the issue, the most common types of fraud schemes out there and what you can do to prevent and detect them within your business is critical.

3 Nicholas Johnson, the Globe and Mail. “Toronto’s moving on up . . . and up.” February 19, 2012. Accessed at http://www.canada.com/news/Slain+mobster+exported+construction+fraud/5762200/story.html on October 24, 2012.

From government projects to corporate developments to individual home builds, cases of fraudulent activity in the construction industry are abundant. In many cases, rather than the stereotype of construction companies defrauding individuals or the public, it is the companies themselves losing money to fraud perpetrated by employees, contractors, subcontractors and venture partners. These frauds include diverted funds, materials misuse, padded bills, charging for unperformed work, hidden cost overruns and more.

In a recent global study, the Association of Certified Fraud Examiners (ACFE) ranked real estate and construction fraud as the second and third most costly frauds in terms of median loss, with billing fraud the number one scheme.1 In a similar study focused on Canada, the average loss for all fraud cases was higher than the global average, and this held true in construction, where it was $628,500.2

1 The Association of Certified Fraud Examiners. Report to the Nations on Occupational Fraud and Abuse: 2012 Global Fraud Study, p. 29-30. Accessed at http://www.acfe.com/uploadedFiles/ACFE_Website/Content/rttn/2012-report-to-nations.pdf on October 24, 2012.

2 The Association of Certified Fraud Examiners. Detecting Occupational Fraud in Canada: A Study of its Victims and Perpetrators, p.17. Accessed at http://www.acfe.com/uploadedFiles/ACFE_Website/Content/documents/rttn-canadian.pdf on October 24, 2012.

The many faces of fraud: The family business Two sons purchase their father’s construction business without reviewing the current staff and suppliers, relying on their father’s previous decisions. Taking advantage of their inexperience, an individual in the procurement department sets up a fictitious supplier. Then he purchases raw materials through an approved supplier, only to sell those materials back to the construction company—through his fictitious supply company—at a significantly inflated cost.

Construction fraud is pervasive

4

Evidence of fraud isn’t hard to uncover

estimating the amount of workers or materials needed for large-scale construction projects.”4

In a current high-profile Toronto case, a manager of multiple properties is alleged to have used falsified contracts and board documents to borrow close to $20 million

4 Paul Cherry, the Montreal Gazette. “Slain mobster ‘exported construction fraud.’” November 28, 2011. Accessed at http://www.canada.com/news/Slain+mobster+exported+construction+fraud/5762200/story.html on October 22, 2012.

for supposed repairs, maintenance and other development expenses without the condo boards’ knowledge, which he then allegedly funnelled into personal accounts.5

The growing prevalence of construction fraud is not a myth or the product of hype—it’s happening and the stakes are high. The question is, what can your company do about it?

5 “Property manager bilked $20M in condo fraud, victims claim.” The Toronto Star. Accessed at http://www.thestar.com/news/gta/article/1054140--property-manager-bilked-20m-in-condo-fraud-victims-claim on October 24, 2012.

Media scrutiny of construction fraud cases has increased because the issue is real and demonstrable. Jeffrey Robinson, an organized crime expert, estimates that “the five major Mafia families in New York take a five percent share of all construction projects in the city,” mostly using the technique of “over-

5

• construction joint ventures, when one unscrupulous partner takes advantage of the business arrangement without the other partner’s knowledge.

The many faces of fraud: Joint ventures Two business partners order and pay for raw materials for their joint project. However, one of the business partners, without the other’s knowledge, uses the material for a secondary project being conducted solely by his own business.

• lack of internal controls, proper monitoring/oversight and a transparent paper trail, which make fraud both easy to perpetrate and difficult to trace;

• increased opportunity for collusion and non-arm’s length transactions as supply chains become larger, more complex and more difficult to manage;

• vaguely worded contracts that allow contract manipulation or misinterpretation;

• the use of large amounts of undocumented cash in transactions, which is difficult to track and trace;

• cost-based contracting approaches, which facilitate the substitution of materials or labour without a commensurate change in costs;

• not ensuring scope is defined before the price is set, leading to cost overruns, bill padding, etc.; and

Before taking action to prevent fraud, it’s critical to understand the “who,” “how” and “why” behind fraudulent activities. Construction fraud can be perpetrated by a variety of individuals up and down the chain of supply and service, the most common being employees, property managers, general contractors, employees of joint venture partners, subcontractors, suppliers and consultants. Personal factors remain the major fraud drivers. Basic greed or stress from financial or emotional issues can drive fraudsters to act or make them vulnerable to external criminal pressures and influences.

It’s important to remember, however, that failure and catastrophe do not define the fraud-friendly environment. Successful projects and profitable relationships are just as susceptible to fraud as unsuccessful projects. So what factors facilitate construction fraud particularly? There are many, including

• economic pressure from factors such as risk of customer or supplier bankruptcy, price volatility, low profit and tight bank credit;

Who is committing construction fraud and how?

6

To prevent and detect fraudulent activity, you should be aware of the most common schemes6:

1 Non-payment of subcontractors and material suppliers by delaying lien waivers, falsifying lien waivers or using project cash receipts to pay bills for other projects.

2 Billing for unperformed work by overstating the units of production accomplished or the labour and equipment actually used.

3 Manipulating the schedule of values and contingency accounts. This can be done in several ways, including

• failing to update schedule of values (SOV) line items as buyouts or changes are made,

• charging phony bills received from shell companies,

• failing to associate subcontractors or vendors with specific SOV line items,

• hiding cost overruns during the project, and

• using a contingency to cover non-reimbursable costs.

4 Diverting lump-sum cost to time and material cost by initially budgeting expenses as a lump-sum then billing for time and materials related to change orders.

5 Substituting or removing material, including using lower-grade material that requires subsequent repairing or replacing or that leads to a structural or system failure, and taking material from the work site for personal use.

6 The Association of Certified Fraud Examiners. Report to the Nations on Occupational Fraud and Abuse: 2012 Global Fraud Study, p. 29-30. Accessed at http://www.acfe.com/uploadedFiles/ACFE_Website/Content/rttn/2012-report-to-nations.pdf on October 24, 2012.

6 Change order manipulation, including altering work scope, removing scope descriptions, adding charges, omitting design specifications in the original scope of work and improper price reductions for work substitution.

7 Falsifying payment applications by covering up the purchase of personal items or funneling money to a phantom company controlled by an employee; other examples include inflating invoices beyond actual costs by using profit or mark-up formulas.

8 Subcontractor collusion, including bid rigging, bribes, kickbacks, false or inflated change orders, undervalued deductive change orders or phantom subcontractors.

9 Diverting purchases and stealing equipment/tools by billing for equipment or tools for the jobsite which are then used for other subcontractor projects or personal use, or billing for tools not required by job specifications.

10 False representations, which could involve using undocumented workers; falsifying minority content reports, test results or insurance certificates; noncompliance with environmental regulations; and misrepresentation of small business status.

The many faces of fraud: Contractor scamAn apartment building is renovating common areas and suites. A review of invoices from vendors for a specific time period identifies numerous anomalies. For example, a vendor had billed to have the south wall painted in one unit seven times within a short period. The giveaway is the consecutive invoice numbers.

7 7

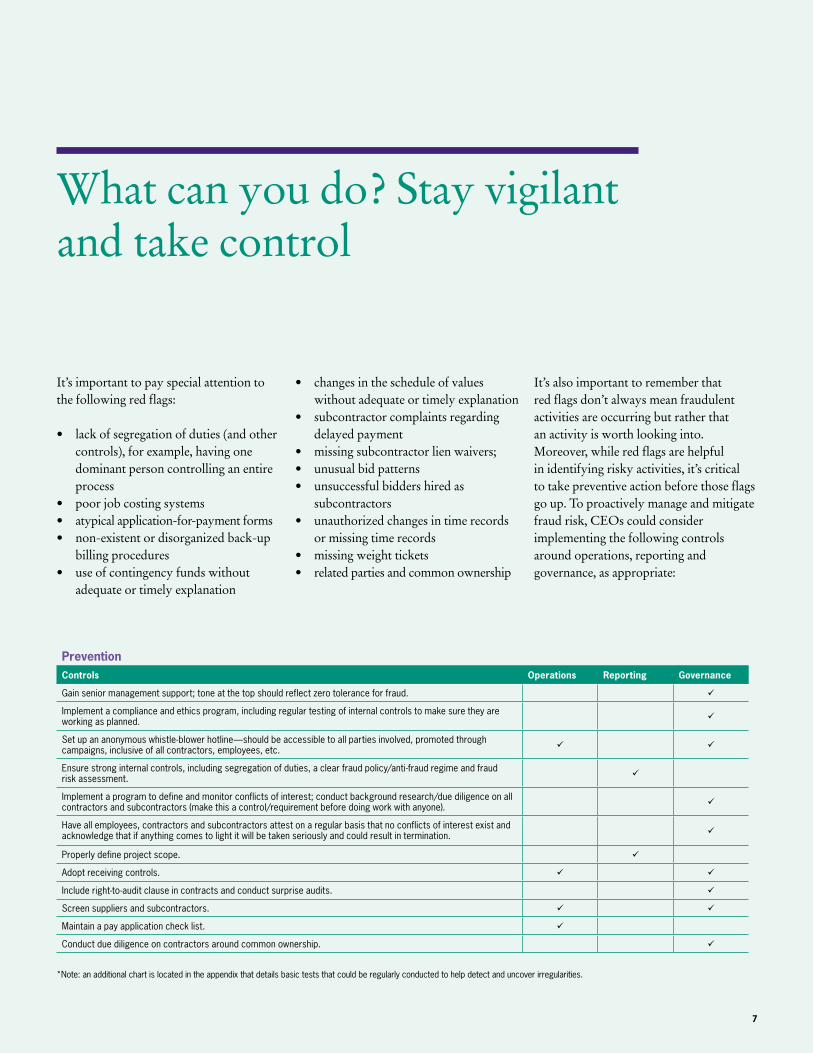

It’s also important to remember that red flags don’t always mean fraudulent activities are occurring but rather that an activity is worth looking into. Moreover, while red flags are helpful in identifying risky activities, it’s critical to take preventive action before those flags go up. To proactively manage and mitigate fraud risk, CEOs could consider implementing the following controls around operations, reporting and governance, as appropriate:

• changes in the schedule of values without adequate or timely explanation

• subcontractor complaints regarding delayed payment

• missing subcontractor lien waivers;• unusual bid patterns• unsuccessful bidders hired as

subcontractors• unauthorized changes in time records

or missing time records• missing weight tickets• related parties and common ownership

It’s important to pay special attention to the following red flags:

• lack of segregation of duties (and other controls), for example, having one dominant person controlling an entire process

• poor job costing systems• atypical application-for-payment forms• non-existent or disorganized back-up

billing procedures• use of contingency funds without

adequate or timely explanation

PreventionControls Operations Reporting Governance

Gain senior management support; tone at the top should reflect zero tolerance for fraud.

Implement a compliance and ethics program, including regular testing of internal controls to make sure they are working as planned.

Set up an anonymous whistle-blower hotline—should be accessible to all parties involved, promoted through campaigns, inclusive of all contractors, employees, etc.

Ensure strong internal controls, including segregation of duties, a clear fraud policy/anti-fraud regime and fraud risk assessment.

Implement a program to define and monitor conflicts of interest; conduct background research/due diligence on all contractors and subcontractors (make this a control/requirement before doing work with anyone).

Have all employees, contractors and subcontractors attest on a regular basis that no conflicts of interest exist and acknowledge that if anything comes to light it will be taken seriously and could result in termination.

Properly define project scope.

Adopt receiving controls.

Include right-to-audit clause in contracts and conduct surprise audits.

Screen suppliers and subcontractors.

Maintain a pay application check list.

Conduct due diligence on contractors around common ownership.

*Note: an additional chart is located in the appendix that details basic tests that could be regularly conducted to help detect and uncover irregularities.

What can you do? Stay vigilant and take control

8

The benefits of understanding construction fraud risks, knowing how to mitigate them and taking proactive measures to combat them are many—not only in what you can avoid but in what you can gain. A strong fraud strategy can help you steer clear of penalties for violating industry standards or regulatory requirements, avoid project delays or cancellations, maintain costs at stable and predictable levels, and control reputational risk. And don’t forget that construction fraud can be very dangerous if it involves the use of substandard or unsafe materials. A good fraud prevention program may actually prevent injury or loss of life and the legal calamities those entail. Clear gains include potentially reducing your insurance costs, ensuring a fair competitive process (both when receiving and tendering bids) and enhancing your reputation as a company that can be trusted.

Moreover, by establishing appropriate organizational controls, you can create a corporate culture that has zero tolerance for fraud. Your employees, partners, clients and vendors will be aware of your company’s standards and that you’ve implemented strong, effective measures to combat fraudulent activity to help protect all parties involved.

Establishing a comprehensive anti-fraud program isn’t always easy. Many companies do not have the in-house knowledge and experience to identify and manage risks, develop and maintain internal controls, identify overcharges, and avoid litigation and reputational damages. A professional adviser can help you get your anti-fraud initiative under way, with services that include

• construction cost monitoring and project close-out audits;

• compliance with agreements and definitions;

• contract reviews and interpretation;

• litigation and dispute support;

• fraud investigations;

• fraud risk assessments and other internal control reviews, assessments and recommendations;

• development of fraud policy, code of conduct and other governance documents;

• establishing and monitoring a whistle-blower hotline; and

• background research and due diligence on contractors, subcontractors and employees.

Preserve business, uphold your reputation and avoid financial loss

9

The many faces of fraud: Bait and switch A couple purchases products from a do-it-yourself store to renovate their home. When the product arrives, it is not what they ordered. Post-delivery, the supplier of the product goes bankrupt and opens a new store down the road from the now bankrupt operation. Luckily, the couple paid with their credit card, so they claim the refund with the credit card company.

Given current levels of construction activity and investment in Canada, the construction industry needs to implement proactive, preventive measures. Individuals and organizations need to acquire the tools and know-how to put a fraud prevention and detection plan into action. Unchecked, fraud risks and losses can be substantial. To potentially avoid increased costs, loss of clients, license and permit suspensions, project delays, removal from proposal and tender lists, regulatory enforcement penalties and reputational damage, companies need to understand fraud and the full range of fraud schemes out there. This will help companies position themselves to take appropriate action to prevent and detect fraud and mitigate their risks.

Companies often balk at the idea of implementing a substantive fraud prevention program. Assuring themselves “It won’t happen to me,” they feel they cannot justify the costs. Unfortunately, fraud exists. Not only that, it is becoming more prevalent and sophisticated. Despite this, most companies do not take action to prevent fraud before it happens. Rather, they react, often only after the damage has been done. In fact, most companies with fraud prevention programs and controls in place have already been victims of fraud.

Action is key to keeping fraud outside your risk perimeter

10

Appendix

Once effective fraud controls are in place, the following basic tests could be regularly conducted to help detect and uncover irregularities:

Detection Tests Operations Reporting Governance

Schedule out pay applications

Compare actual costs to budget on a line item basis

Reconcile payments to pay applications

Reconcile pay applications to underlying cost reports

Track changes in the schedule of values

Track changes in the contingency account

Compare change order signature dates to the actual time in which the work was completed

Inventory lien waivers

Make a list of purchased equipment and inventory the remainder

Conduct supplier confirmations

Prove reimbursable charges

Tie subcontractor bill to payment applications

Compare drawing/spec material volumes to claimed actual volumes

Review the subcontractor bid selection process and selection documentation

Further informationThis is dummy text. It is intended to be read but have no meaning. As a simulation of actual copy, using ordinary words with normal letter frequencies, it cannot deceive eye or brain. Dummy settings which use other languages or even gibberish to approximate text have the inherent disadvantage that they distract attention to themselves.

E [email protected] +XX XX XXX XXXX

DownloadsThis guide can also be downloaded fromwww.sample.org

CountryLegal nameNameT +XX XX XXXX XXXXF +XX XX XXXX XXXX

CountryLegal nameNameT +XX XX XXXX XXXXF +XX XX XXXX XXXX

CountryLegal nameNameT +XX XX XXXX XXXXF +XX XX XXXX XXXX

CountryLegal nameNameT +XX XX XXXX XXXXF +XX XX XXXX XXXX

CountryLegal nameNameT +XX XX XXXX XXXXF +XX XX XXXX XXXX

CountryLegal nameNameT +XX XX XXXX XXXXF +XX XX XXXX XXXX

CountryLegal nameNameT +XX XX XXXX XXXXF +XX XX XXXX XXXX

CountryLegal nameNameT +XX XX XXXX XXXXF +XX XX XXXX XXXX

CountryLegal nameNameT +XX XX XXXX XXXXF +XX XX XXXX XXXX

CountryLegal nameNameT +XX XX XXXX XXXXF +XX XX XXXX XXXX

CountryLegal nameNameT +XX XX XXXX XXXXF +XX XX XXXX XXXX

CountryLegal nameNameT +XX XX XXXX XXXXF +XX XX XXXX XXXX

CountryLegal nameNameT +XX XX XXXX XXXXF +XX XX XXXX XXXX

CountryLegal nameNameT +XX XX XXXX XXXXF +XX XX XXXX XXXX

CountryLegal nameNameT +XX XX XXXX XXXXF +XX XX XXXX XXXX

ContactsAbout us

Contributors

David Malamed, CA.IFA, CPA (Illinois), CFE PartnerT +1 416 360 3382E [email protected]

Bo Mocherniak, CA•CBV PartnerNational Construction, Real Estate and Hospitality LeaderT +1 416 360 3050 E [email protected]

Caroline Hillyard, BA, BComm, CA.IFA ManagerT +1 416 607 2716 E [email protected]

Regional contacts

British ColumbiaKelownaKevin Santos, BComm, CAPartnerT +1 250 712 6876 E [email protected]

VancouverDoug Bastin, CMC PartnerGrant Thornton ConsultingT +1 604 443 2149E [email protected]

AlbertaEdmontonBrad Danyluik, CA PartnerT +1 780 401 8211 E [email protected]

CalgaryAlex McInnisPartnerT +1 403 260 2530 E [email protected]

OntarioBo Mocherniak, CA•CBV PartnerT +1 416 360 3050 E [email protected]

New BrunswickPeter Powell, CA PartnerT +1 506 460 8428 E [email protected]

Nova ScotiaKatrina Beach, CA, CPA (IL)PartnerT +1 902 491 7730E [email protected]

Keith MacIntyre, CA PartnerT +1 902 491 7739 E [email protected]

Prince Edward IslandDennis Carver, CA PrincipalT +1 902 566 6316 E [email protected]

Newfoundland and LabradorRob Flynn, CA PartnerT +1 709 634 8236 E [email protected]

Grant Thornton is one of the world’s leading organizations of independent assurance, tax and advisory firms. These firms help dynamic organizations unlock their potential for growth by providing meaningful, actionable advice through a broad range of services. Proactive teams, led by approachable partners in these firms, use insights, experience and instinct to solve complex issues for privately owned, publicly listed and public sector clients. Over 31,000 Grant Thornton people, across 100 countries, are focused on making a difference to clients, colleagues and the communities in which we live and work.

About Grant Thornton in CanadaGrant Thornton LLP is a leading Canadian accounting and advisory firm providing audit, tax and advisory services to private and public organizations. We help dynamic organizations unlock their potential for growth by providing meaningful, actionable advice through a broad range of services. Together with the Quebec firm Raymond Chabot Grant Thornton LLP, Grant Thornton in Canada has approximately 4,000 people in offices across Canada. Grant Thornton LLP is a Canadian member of Grant Thornton International Ltd, whose member firms operate in close to 100 countries worldwide.

Audit • Tax • Advisorywww.GrantThornton.ca

Grant Thornton LLP. A Canadian Member of Grant Thornton International Ltd TL-CRH-02-22-2013