Embed Size (px)

DESCRIPTION

Achievement of high economic growth is the basic principles of present economic policy. In achieving the objectives, the banking sector plays an important role. The banking sectors channel resources through deposit mobilization and providing credit for different business venture

Citation preview

IntroductionAchievement of high economic growth is the basic principles of present economic policy. In achieving the objectives, the banking sector plays an important role. The banking sectors channel resources through deposit mobilization and providing credit for different business venture. The successful running of a bank business depends upon how effectively the credit management recovered the funds. The Bangladesh Commerce Bank Limited is new banking operation in a sound manner. BCBLi is always ready to maintain the highest quality services by upgrading Banking technology prudence in manage and applying high standard of business ethics through its established commitment and heritage. Objectives of a private institution like BCBL are to maximize profit through optimum utilization of resources by providing best customer’s service.To ensure the safety of depositor and give them different types of credit facilities, Consumer Credit Scheme (CCS) is one of such kind of credit facility, which helps limited income people to purchase any household effects, including car, computer, air conditioner, motorcycle and other consumer durable. The scheme has been generating huge profit for the Bank. But the recovery rate is not up to the mark as BCBL tries to recover. If the management of Bangla Bazar Branch becomes successful to increase the recovery rate of this scheme, it can be the highest profitable sector for the Branch. This research reveals how BCBL can decrease the defaulting rate.The profit of a commercial bank depends primarily on the utilization of its fund. But Bank cannot lend its fund fully. As per Banking Company Act 1991 every banking company has to maintain a specified minimum (presently 16%) of the total of its demand and time liabilities in the form

of cash and approved securities with Bangladesh Bank. This percentage or ratio is termed Statutory Liquid Ratio. Further every scheduled bank has to maintain with Bangladesh Bank an average daily balance, the amount of which has not to be less than a particular percentage (presently 4%) of the total of its demand and time liabilities. As such Commercial Bank generally goes for short-term finance although a small portion of its total deposit is invested as long term lending.

ProlegomenonModern banks play an important part in promoting economic development of a country. Banks provide necessary funds for executing various programmers underway in the process of economic development. They collect savings of large masses of people scattered through out the country, which in the absence of banks would have remained idle and unproductive. These scattered amounts are collected, pooled together and made available to commerce and industry for meeting the requirements. Economy of Bangladesh is in the group of world’s most underdeveloped economies. One of the reasons may be its underdeveloped banking system. Government as well as different international organizations have also identified that underdeveloped banking system more causes some obstacles to the process of economic development. So they have highly recommended for reforming financial sector. Since 1990, Bangladesh Government has taken a lot of financial sector reform measurements for making financial sector as well as banking sector transparent, formulation and implementations of these reform activities has also been participated by different international organization like World Bank, IMF etc.In 1996, World Bank published ‘Bangladesh: Agenda for action’ in which it has suggested a lot of recommendations for economic development of our country. These recommendations include special presentation for reforming banking sector. Rationality of the Study

Proper economic growth of a country largely depends on sound and proper industrialization. A huge amount of fund is required for the sound industrialization. Various Private and Public banks invest their funds in the form of credit. The BCBL also invests or lends its fund in this regard. The BCBL has several types of credit facilities. The profitability of a bank largely depends on appropriate credit approval procedure. The credit approval process involves various type of risk. When a bank lends money to the investor, it has to consider the related risks of the lending. So a proper credit approval policy and monitoring technique is essential.For the knowledge of banking system, the students of Business Studies must acquire the knowledge of lending process. It is the core to a bank. Bank earns profit by financing various sectors of business in the form of credit. Hence credit approval and monitoring technique is very important for the bank and the economy also. So the researcher selects this specific topic for the study.

ObjectivesPrime objective

To know how the Bank fixes its prices for Loan and Advances.

Secondary objectives

The secondary objectives were:

To analyze the present policies and practices of credit management in BCBL

To find out the Strength and weakness of Bangla Baser Branch in BCBL

To deliver greater suggestion measures for the improvementMethodology

The nature and type of this study is exclusively an observatory1 and exploratory2 research. The method involved an intensive study of books; journals and banks survey to gauge the theoretical aspects of commercial bank operation. A commercial bank operation has been observed directly aiming to conduit the theories and practices thereby. Research Types

i) Observatory ResearchA 15 weeks direct observation and participation in BCBL operations has been done by the researcher. During the participatory work in bank, the internee has ideas and collected relevant information from different desks. The methodological procedure follows different stages, which were described briefly as below:

Sources of data

Information used in the report collects from both primary and secondary sources. Primary data collected mainly through the writer’s observation of the approval process and monitoring techniques, informal interviews of executives, officers and employees of The Bangladesh Commerce Bank Limited. Sources of information for writing this report were:

Personal experience gained by visiting different desks. Study of old files. Different circulars sent by Head Office of Bangladesh Commerce

Bank and Bangladesh Bank. Annual Report Publications on Credit Management

Sampling method

1 Observation is the only method available to gather certain types of information. Observation is the full range of monitoring behavioral and non behavioral activities and conditions

3. Exploratory studies tend towards loose structure with the objective of discovering future research task. The immediate purpose of exploration is usually to develop hypotheses or questions for further research.2

Probability sampling has been done for the research purpose. This was done for the convenience of the study and to meet the available time in my hand. The bankers surveyed by interview.

Analysis techniquesThis was a descriptive report mainly aiming to depict the credit approval process and monitoring techniques of the BCBL. The data gathered from both primary and secondary sources arranged orderly to get a clear picture of The Bangladesh Commerce Bank’s credit management policy regarding lending process and monitoring. The study included both qualitative and quantitative analysis of loan approval process and monitoring tools. Based on the observational information writer also tries evaluate and analyze the problems involved in various phases of the credit approval process and monitoring techniques. After receiving the necessary data, it has been placed in the data instrument sheet. As per the guideline in the questionnaire manual, collected data have been analyzed by using different statistical technique. Results of the data analysis have been used to prove the specific objectives to draw a conclusion. ii) Exploratory Research A pricing Loans model has been developed as part of the exploratory research. The loan-pricing model assumes that the rate of interest charged on any loan includes three components:

1) The cost to the lender of raising adequate funds to lend. The lender’s non-funds operating costs.

2) Necessary compensation paid to the lender for the degree of default risk inherent in a loan request.

3) The desired profit margin on each loan that provides the lending institutions stockholders with an adequate return on their capital.

The model finally developed considering three factors, such as

Price of Loans3 = Cost of Capital fund4 + Risk Premium5 + Expected Profit6

Scope and Limitations of the Study

Scope The Bangladesh Commerce bank Limited is one of the leading banks in Bangladesh. The scope of the study is limited to the Bangla Bazar Branch only. The portion of the report covers the organizational structure, background, functions and the performance of the bank in broad spectrum. The Credit management portion covered in the Project part of the report. Besides credit management, the report was mainly highlight on few delicate aspects like Service charge, Foreign Currency Exchange rate, Credit worthiness of customer (character, capacity, condition, cash, collateral and control), forced credit and Industry analysis. LimitationsTime was a big factor to have adequate knowledge to make a complete report. My internship period was just for 03 (three) months. On the way of my study, I have faced the following problems that may be terms as the limitations/shortcomings of the study.

Budgeted times for the StudyThe first obstruct is time itself. Due to the time limit, the scope and dimension of the study has been curtailed. Bangladesh Commerce Bank Limited is a big organization. It is very tough to deal with this Bank within this short time. On the other hand due to short time I will not become able to conduct with all the customers who have taken the loan. The respondents are scared with different places. Due to the short time it

3 Pricing Loans is the lender wants to charge a high enough interest rate to ensure that each loan will be profitable and compensate the lending institution fully for the risks involved4 The cost of capital is an expected return that the provider of capital plans to earn on their investment.5 The risk premium can be the expected rate of return above the risk-free interest rate.6 Profit is the difference between the income of the business and all its costs/expenses.

will not possible me to do random sampling and conduct with the respondent by going everywhere.

Data InsufficiencyIt is very difficult to collect data from such a big organization. But for better interpretation I collected some information from the Head office. Because of some divisional and confidential problem, are not to get enough information. So for better interpretation I didn’t get sufficient data.

Lack of RecordsSufficient books, publications, facts and figures were not available. These constraints narrowed the scope of accurate analysis. If these limitations have not been there, the report would have been more useful and attractive.

BANK PROFILE

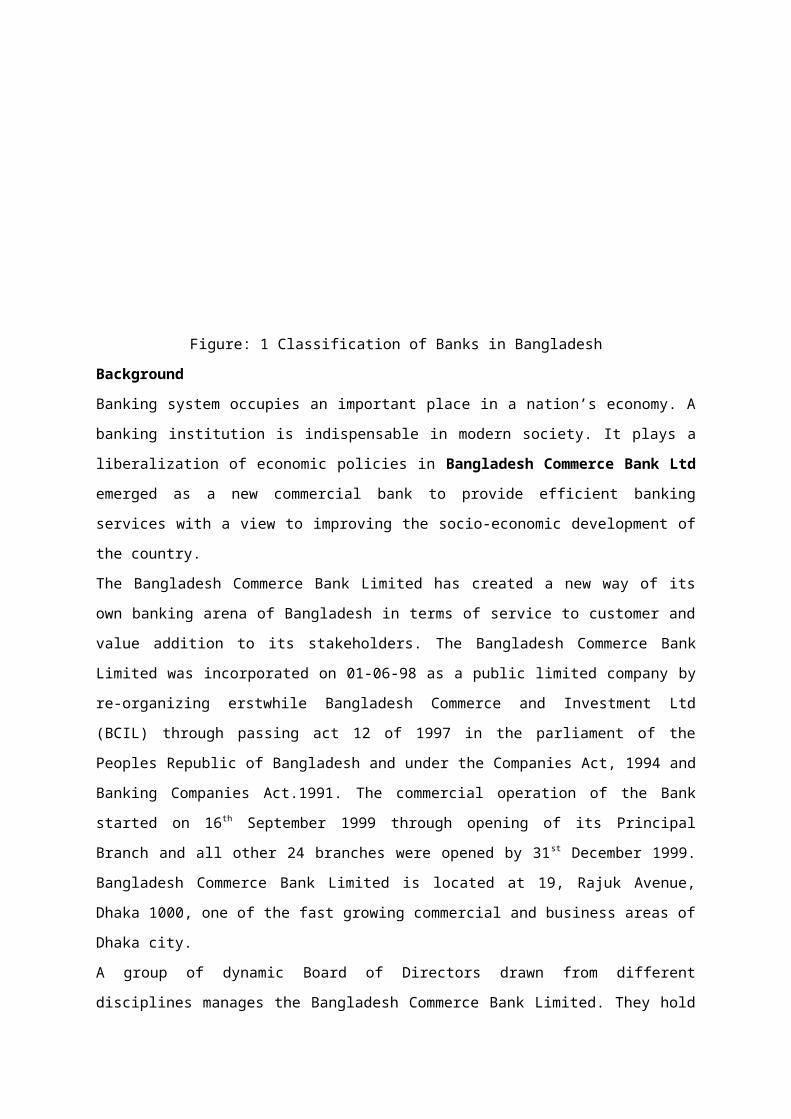

The prosperity of a country depends upon its economic activities like any other sphere of modern socio-economic activities; banking is a powerful medium of bringing about socio-economic changes of a developing country. Agriculture, commerce and industry provide the bulk of a country’s wealth. Without adequate banking facility these three cannot flourish. For a rapid economic growth a fully developed banking system is highly essential. A suitably developed banking system can provide the necessary boost for the economic uplift of the country. The whole economy of a country is link up with its banking system.Banks in Bangladesh can be classifying into the following categories:

BANKS

BANGLADESH

BANK (central bank of

the country)

COMMERCIAL

BANKS

SPECILIZED

BANKS AND

CREDIT AGENCIE

S

BANGLADESH

SAMABAYA BANK

LTD.

NATIONALIZED

COMMERCIAL BANKS

FOREIGN BANKS PRIVATE

BANKS

BANGLADESH SHILPA

RING SANGSTHA

BANGLADESH KRISHI BANK

BANGLADESH SHILPA BANK

CENTRAL CO-OPERATIVE

BANK

PRIMARY CO-OPERATIVE

CREDIT SOCIETES

Figure: 1 Classification of Banks in BangladeshBackgroundBanking system occupies an important place in a nation’s economy. A banking institution is indispensable in modern society. It plays a liberalization of economic policies in Bangladesh Commerce Bank Ltd emerged as a new commercial bank to provide efficient banking services with a view to improving the socio-economic development of the country.The Bangladesh Commerce Bank Limited has created a new way of its own banking arena of Bangladesh in terms of service to customer and value addition to its stakeholders. The Bangladesh Commerce Bank Limited was incorporated on 01-06-98 as a public limited company by re-organizing erstwhile Bangladesh Commerce and Investment Ltd (BCIL) through passing act 12 of 1997 in the parliament of the Peoples Republic of Bangladesh and under the Companies Act, 1994

and Banking Companies Act.1991. The commercial operation of the Bank started on 16th September 1999 through opening of its Principal Branch and all other 24 branches were opened by 31st December 1999. Bangladesh Commerce Bank Limited is located at 19, Rajuk Avenue, Dhaka 1000, one of the fast growing commercial and business areas of Dhaka city.A group of dynamic Board of Directors drawn from different disciplines manages the Bangladesh Commerce Bank Limited. They hold very respectable positions in the society and are from highly successful group of Businesses and Industries in Bangladesh. The Bank has a very competent Management Team who has long experience in domestic and international Banking. The Bank

upholds and strictly abides by good corporate governance practices and is subject to the regulatory supervision of Bangladesh Bank.Authorized Capital: BDT 2000.00 MillionPaid up Capital: BDT 920.00 MillionMission and Vision of BCBLMission:

To be the most caring and customer friendly provider of financial services, creating opportunities for more people in more places.

To ensure stability and sound growth while enhancing the value of shareholders investment

To aggressively adopt technology at all levels of operation to improve efficiency and reduce cost per transaction

To ensure a high level of transparency and ethical standards in all business transacted by the bank

To be socially responsible and strive to uplift the quality of the life by making effective contribution to national development

Vision:The Bangladesh Commerce Bank has a dream-to carve out a name for our esteemed organization as a symbol of corporate exception that would stand out in the crowed as a “bank par excellence”.Management Team

The Board consists of 11 (eleven) Directors. The members of the Board of

Directors of the Bank hold very respectable positions in the society. They are

from highly successful group of Business and Industries in Bangladesh. Each

member of the Board of Directors plays a significant role in the socio-economic

domain of the country.

Offices Automation

Basic accounting system of the bank branches has been fully computerized to minimize cost and risk to optimize benefits and increase overall efficiency for improved services. The bank is capable of generating the relevant financial statements at the end of the day. The Bank is taking action to become

a member of ATM Network. The web page www.bcblbd.com can be accessed round the clock for appropriate information.Bank Financial Telecommunication: SWIFT is a member owned co-operative, which provides a fast and accurate communication network for financial transactions such as Letters of Credit, Fund transfer etc. In 2002, by becoming a member of SWIFT, the bank has opened up possibilities for uninterrupted connectivity with over 5,700 user institutions in 150 countries around the world.Products and Services of the Bank

The motto of The Bangladesh Commerce Bank is ‘Service First’. The BCBL’s

goal is to be the most caring and customer-friendly provider of financial

services creating opportunities for more people in more places. Bangladesh

Commerce Bank always undertakes a continuous mission to develop new and

improved services for its valued customers.

Some of BCBL’s popular products & services have given bellow:

Financing of small and medium Industries Financing of Trade Financing of Import & Export Micro Credit and Micro Enterprise Scheme Credit Scheme for Women entrepreneurs Consumers Credit Scheme Special Credit Scheme for Service holder Special Savings Scheme

Deposit Products: Monthly Savings Scheme (MSS) Monthly Income Scheme (MIS) Lakhpoti Deposit Scheme (LDS) Millionaire Deposit Scheme (MDS) Kotipoti Deposit Scheme (KDS) Marriage Deposit Scheme (MDS) Education Savings Scheme (ESS) Double Benefit Scheme (DGDS) Triple Benefit Scheme (TGDS)

Lending Products: Consumer Credit Scheme Loan Ag. Trust Receipt Secured Overdraft Cash Credit Personal Loan Other Commercial Lending such as: Cash Credit, PAD, LIM, LTR

Services:

Treasury Service

Evening Banking Service

Remittance Service

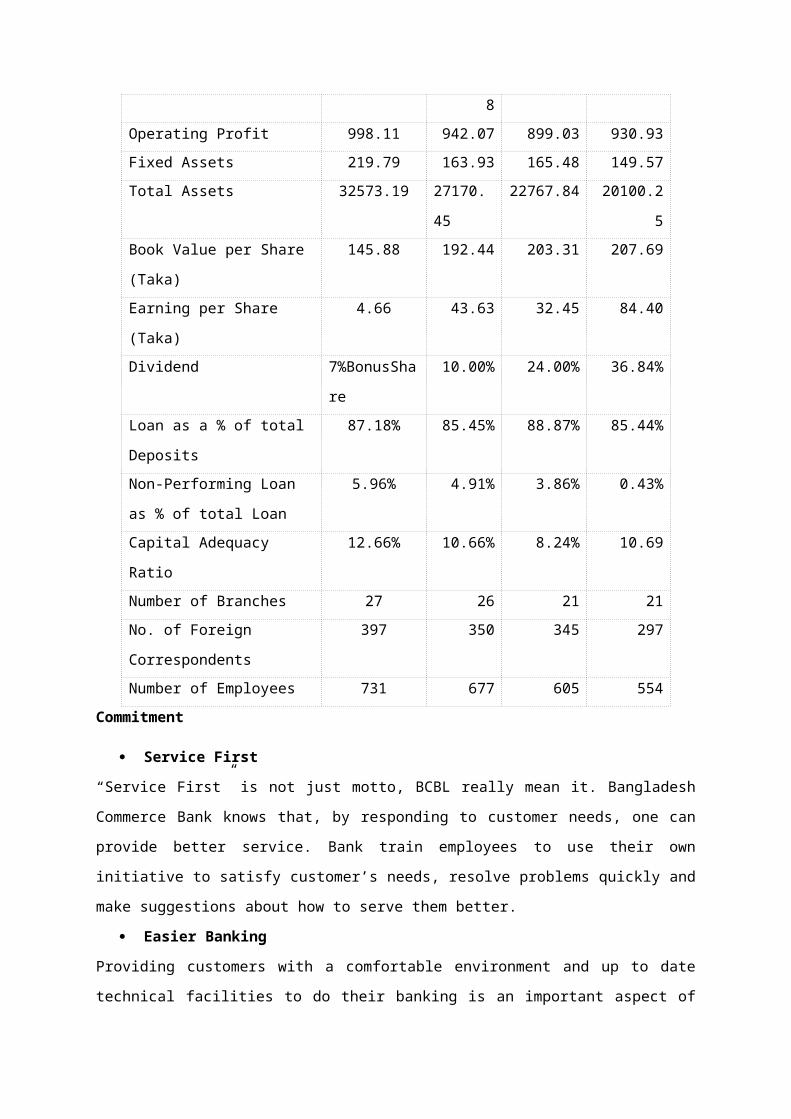

Financial Performance of the BCBL

Business Growth and Operating ResultDeposit numerous challenges on the frontline of banking, The Bangladesh Commerce Bank Ltd ended with an impressive progress in almost all key areas of banking business during 2007. During the year, Bank retained its upward trend and recorded an operating profit of Tk.998.11 million compared to 942.07 million in 2006 registering a growth of 5.95%. An amount of Tk.451.40million has earmarked as tax contribution to national exchequer. Earning Per Share (EPS) increased to Tk.4.66 in 2007.Capital Funds:

The Authorized Capital of the Bank remained unchanged Tk.2000 million and Paid-up Capital at Tk.1689.99 million as on 31 December 2008. Statutory Reserve Fund of the Bank stood at Tk.646.79million, Retained Earnings Tk.125.57million and General Provision for unclassified Loans and Advances at Tk.267.13million. After taking all considerable components for determining Capital Adequacy Ratio (CAR), total capital funds stood at Tk.2792.33 million as on December 31, 2008.Deposits:

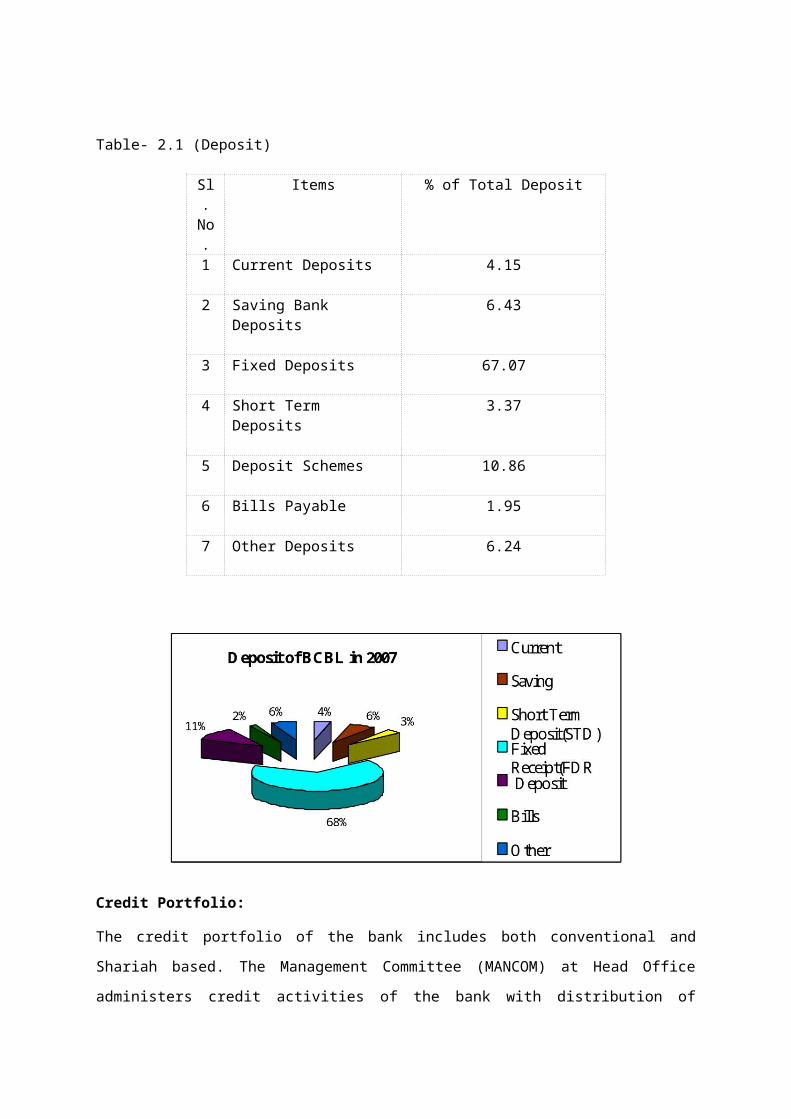

Deposits have well recognized as the blood of financial institutions especially banks. Inevitably they constitute the very foundation of a bank. In pursuit of deposit mobilization, the bank was most successful during 2008 with a record level of deposit balance of Tk.27114.47 million from 24199.01 million in 2007 producing a growth of 12.05%.

Deposit mix at the end of Year 2008 is as follows:

Table- 2.1 (Deposit)

Sl.No.

Items % of Total Deposit

1 Current Deposits 4.15

2 Saving Bank Deposits 6.43

3 Fixed Deposits 67.07

4 Short Term Deposits 3.37

5 Deposit Schemes 10.86

6 Bills Payable 1.95

7 Other Deposits 6.24

Credit Portfolio:

The credit portfolio of the bank includes both conventional and Shariah based. The Management Committee (MANCOM) at Head Office administers credit activities of the bank with distribution of distinct responsibilities as regards assessment of risks, lending decisions and monitoring functions.

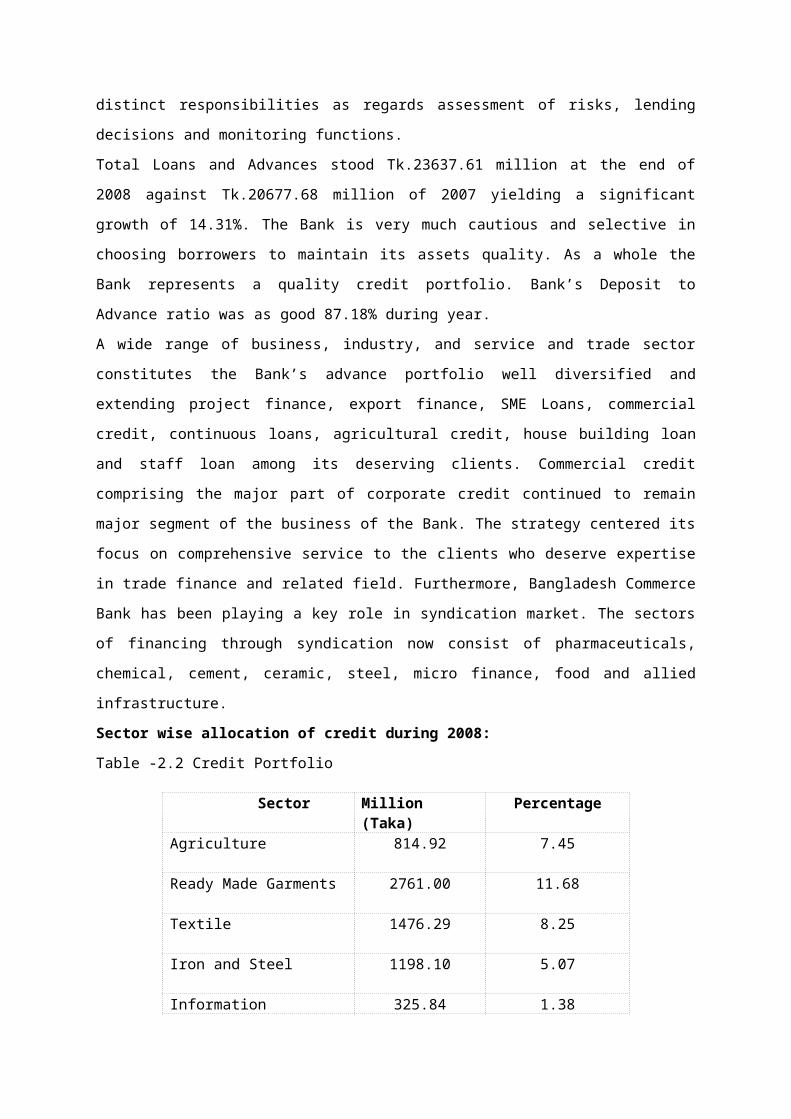

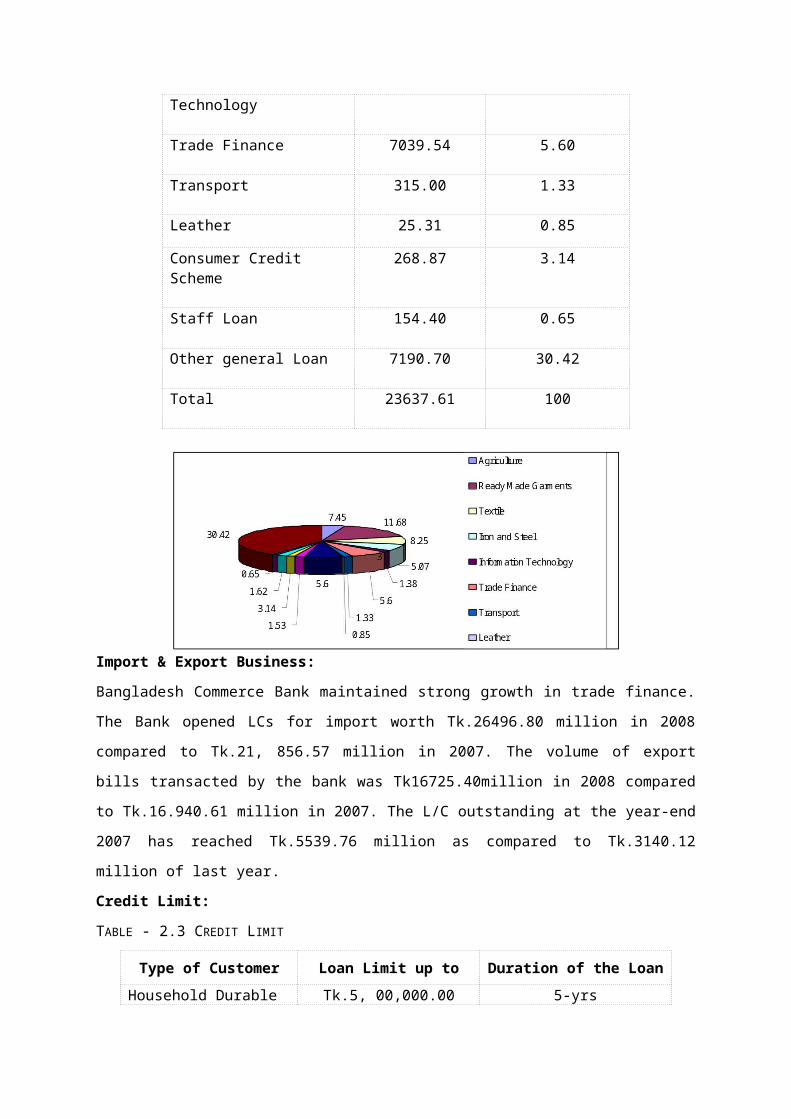

Total Loans and Advances stood Tk.23637.61 million at the end of 2008 against Tk.20677.68 million of 2007 yielding a significant growth of 14.31%. The Bank is very much cautious and selective in choosing borrowers to maintain its assets quality. As a whole the Bank represents a quality credit portfolio. Bank’s Deposit to Advance ratio was as good 87.18% during year.A wide range of business, industry, and service and trade sector constitutes the Bank’s advance portfolio well diversified and extending project finance, export finance, SME Loans, commercial credit, continuous loans, agricultural credit, house building loan and staff loan among its deserving clients. Commercial credit comprising the major part of corporate credit continued to remain major segment of the business of the Bank. The strategy centered its focus on comprehensive service to the clients who deserve expertise in trade finance and related field. Furthermore, Bangladesh Commerce Bank has been playing a key role in syndication market. The sectors of financing through syndication now consist of pharmaceuticals, chemical, cement, ceramic, steel, micro finance, food and allied infrastructure.Sector wise allocation of credit during 2008:Table -2.2 Credit Portfolio

Sector Million (Taka)

Percentage

Agriculture 814.92 7.45

Ready Made Garments 2761.00 11.68

Textile 1476.29 8.25

Iron and Steel 1198.10 5.07

Information Technology

325.84 1.38

Trade Finance 7039.54 5.60

Transport 315.00 1.33

Leather 25.31 0.85

Consumer Credit Scheme

268.87 3.14

Staff Loan 154.40 0.65

Other general Loan 7190.70 30.42

Total 23637.61 100

Import & Export Business:Bangladesh Commerce Bank maintained strong growth in trade finance. The Bank opened LCs for import worth Tk.26496.80 million in 2008 compared to Tk.21, 856.57 million in 2007. The volume of export bills transacted by the bank was Tk16725.40million in 2008 compared to Tk.16.940.61 million in 2007. The L/C outstanding at the year-end 2007 has reached Tk.5539.76 million as compared to Tk.3140.12 million of last year. Credit Limit:TABLE - 2.3 CREDIT LIMIT

Type of Customer Loan Limit up to Duration of the LoanHousehold Durable Loan Tk.5, 00,000.00 5-yrs

Car Loan Tk.40, 00,000.00 5-yrsDoctors Loan Tk.10, 00,000.00 5-yrsAdvance Against Salary Tk.3, 00,000.00 2-yrs

Any Purpose Loan Tk.1, 50,000.00 2-yrsEducation Loan Tk.3, 00,000.00 2-yrsTravel Loan Tk.2, 00,000.00 3-yrsHospitalization Loan Tk.5, 00,000.00 2-yrs

Performance of the bank at a glance:

Table -2.4 Performance of the bank (Tk. In

Million)Particulars 2008 2007 2006 2005Authorized Capital 2000.00 2000.00 2000.00 2000.00

Paid-Up Capital 1689.99 845.00 557.55 557.55Reserve Fund 649.79 543.76 403.85 301.08

Total Capital Funds 2792.33 1855.58 1318.99 1312.63

Deposits 27114.4 24199.01

20290.47 18005.20

Advances 23637.61 20677.68

18032.50 15383.93

Investment in Govt. Securities

3461.45 2392.01 2240.78 2750.00

Foreign Trade Business 43222.20 38797.18

34108.50 34108.50

Foreign Remittance 1620.60 940.10 1427.40 1408.00Income 4186.33 3622.05 2863.86 2395.45Expenditure 3188.22 2679.98 1964.83 1464.52Operating Profit 998.11 942.07 899.03 930.93Fixed Assets 219.79 163.93 165.48 149.57Total Assets 32573.19 27170.4

522767.84 20100.2

5Book Value per Share (Taka)

145.88 192.44 203.31 207.69

Earning per Share (Taka)

4.66 43.63 32.45 84.40

Dividend 7%BonusShare

10.00% 24.00% 36.84%

Loan as a % of total Deposits

87.18% 85.45% 88.87% 85.44%

Non-Performing Loan as % of total Loan

5.96% 4.91% 3.86% 0.43%

Capital Adequacy Ratio 12.66% 10.66% 8.24% 10.69Number of Branches 27 26 21 21No. of Foreign Correspondents

397 350 345 297

Number of Employees 731 677 605 554Commitment

Service First

“Service First” is not just motto, BCBL really mean it. Bangladesh Commerce Bank knows that, by responding to customer needs, one can provide better service. Bank train employees to use their own initiative to satisfy customer’s needs, resolve problems quickly and make suggestions about how to serve them better.

Easier BankingProviding customers with a comfortable environment and up to date technical facilities to do their banking is an important aspect of the customer service at Bangladesh Commerce Bank. Goal is to make banking easier through one to one communications.

Better RelationshipBangladesh Commerce Bank views banking to be a long-term relationship with customers. The business they transact with Bank help to understand their goals and expectations and bank respond proactively to their financial needs.

Ensured ConfidentialityAt Bangladesh Commerce Bank, great care has taken customers, to make sure that all banking transactions have done in a confidential & Professional manner.FORMS OF ADVANCESWhat is Advance?

Credit is an arrangement whereby bank acting at the request and on the instructions of a customer or on its own behalf to make a payment to or to the order of a third party or is to accept and pay bills of exchange drawn by the beneficiary. In an economy banks play the role of an intermediary that channel funds from the surplus economic units to the deficit economic units. The bank’s mission is to actively participate in the growth and expansion of our national economy by providing credit to borrowers in most efficient way of delivery and at a competitive price.Bank can lend up-to 84% of the total amount of its total time and demand liabilities. The rest 16% is kept as Statutory Liquidity Reserve (SLR) with Bangladesh Bank. But in practice banks do not lend the whole 84% and a certain portion is set aside to meet up the day-to-day banking operations and also meet up the liquidity requirement of the depositors. Bank can lend up-to 15% of its core capital without the approval of Bangladesh Bank but above that level approval from Bangladesh Bank is required.Credit is continuous process. Recovery of one credit gives rise to another credit. In this process of revolving of funds, bank earns income in the form of interest. A bank can invest its fund in many ways. Bank makes loans and advances to

traders, businessmen, and industrialists. Moreover nature of credit may differ in terms of security requirement, disbursement provision, terms and conditions etc.In the banking arena, many types of financial facilities are extended to the clients with the expectation of getting the same returned along with interest. This “provided purchasing power” can be termed as loan, credit or advance. These three terms have similarities as well as some differences.Advance

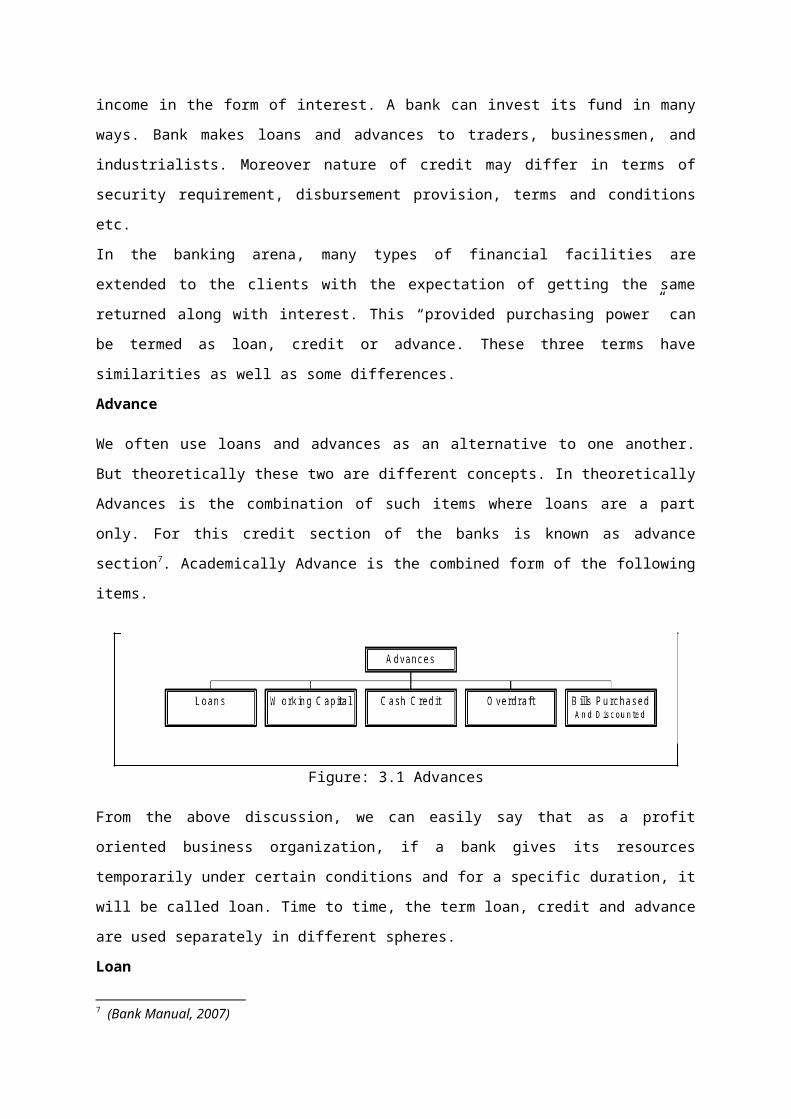

We often use loans and advances as an alternative to one another. But theoretically these two are different concepts. In theoretically Advances is the combination of such items where loans are a part only. For this credit section of the banks is known as advance section7. Academically Advance is the combined form of the following items.

Figure: 3.1 Advances

From the above discussion, we can easily say that as a profit oriented business organization, if a bank gives its resources temporarily under certain conditions and for a specific duration, it will be called loan. Time to time, the term loan, credit and advance are used separately in different spheres.LoanBanks can provide loan in different ways. Loans can be in cash or in non-cash form. If any client takes advantage from bank by using the bank’s goodwill through making a contract, this will be treaded as “goodwill loan” of the bank. L/C, traveler’s checks, and traveler’s notes are the “goodwill loan” of a bank. Loans can be defined as, “the lending of a sum of money of a lender to a borrower to be repaid with a certain amount of interest”8. Loans are, “formal agreement between a bank and borrower to provide a fixed amount of credit for a specified period.”9 Credit7 (Bank Manual, 2007)8 Dictionary of Banking & Finance.9 Timothy W Koch.

The word "Credit" is derived from the Latin word "credo" meaning, "I believe". The term credit may be defined broadly or narrowly. Speaking broadly, credit is finance made available by one party (lender, seller or shareholder/owner) to another (borrower, buyer, corporate or non-corporate firm). More generally the term credit is used narrowly for debt finance. Credit is simply the opposite of debt. Debt is the obligation to make future payments. Credit is the claim to receive these payments. Both are created in the same act of borrowing and lending.In a credit economy, that is economy with borrowing and lending, each spending unit can be placed in any one of the three categories: deficit spenders, surplus spenders, and balance spenders, as it total expenditure is greater than, less than, or equal to its total receipts respectively. The chief function of credit is to relax the constraint of balanced budgets.Types of AdvancesAdvances by commercial banks are made in different forms such as loans, cash credits, overdrafts, bills purchased, bills discounted etc. These are generally short-term advances. Commercial banks do not sanction advances on a long-term basis beyond a small proportion of their demand and time liabilities. Advances may be granted against tangible security or in special deserving cases on an unsecured/ clean basis.LoansIn a loan account, the entire amount is paid to the debtor at one time, either in cash or by transfer to his current account10. No subsequent debit is ordinarily allowed except by way of interest, incidental charges, insurance premiums, expenses incurred for the protection of the security etc. sometimes, repayment is provided for by installment without allowing the demand character of the loan to be affected in any way. Interest is charged on the debit balance, usually with quarterly rests unless there is an arrangement to the contrary. No checkbook is issued. The security may be personal or in the form of shares, debentures, Government paper, immovable property, fixed deposit receipts, life insurance policies, goods etc.Overdraft

Overdrafts are those drawings, which are allowed by the banker in excess of the balance in the account up to a specified amount for definite period as, arranged

10 Deviation from this practice is being made in the case of some loans, say, agricultural loans and the amount may be disbursed to the borrower in convenient installments, as and when he may need funds.

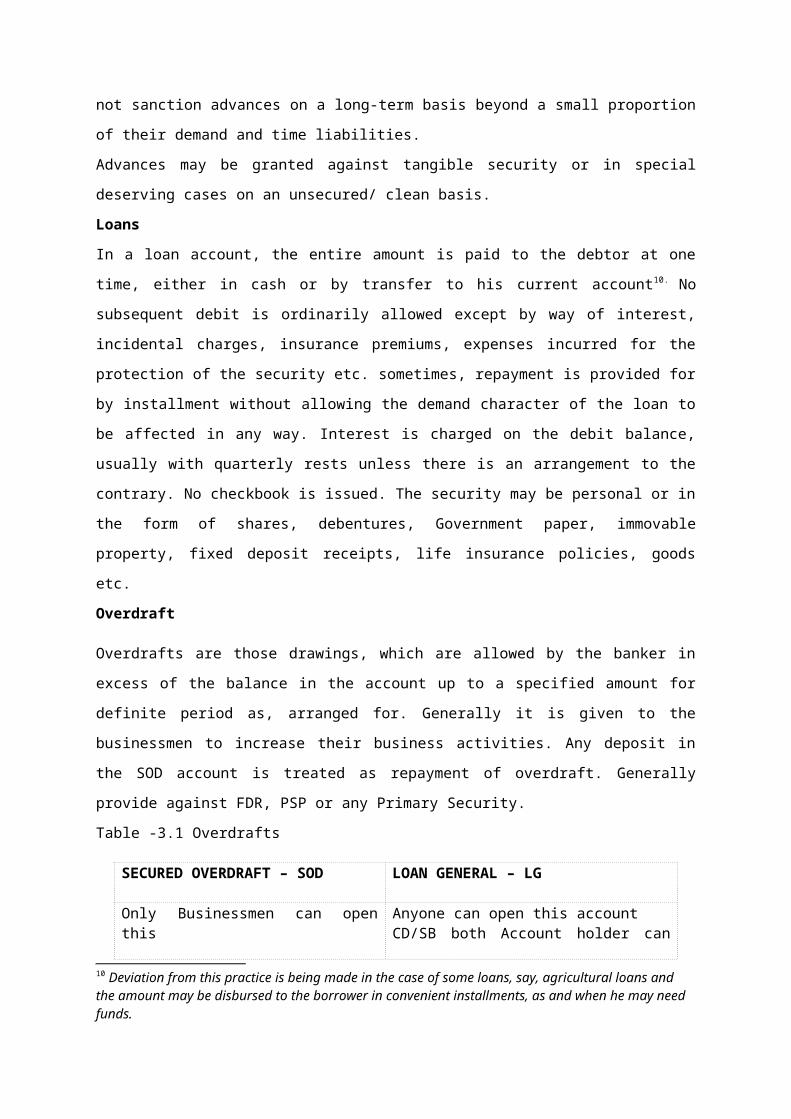

for. Generally it is given to the businessmen to increase their business activities. Any deposit in the SOD account is treated as repayment of overdraft. Generally provide against FDR, PSP or any Primary Security.Table -3.1 Overdrafts

SECURED OVERDRAFT – SOD LOAN GENERAL – LG

Only Businessmen can open thisOnly CD Account Holder can openInterest rate is 14.00%Interest starts from the date of first withdrawal

Anyone can open this accountCD/SB both Account holder can openInterest rate is 15.00%Interest starts from the date of sanction of the overdraft

Cash Credit: Working Capital Management

Cash credit account is basically a current account, however a little difference exists, between them. The former is intended to be an account with credit balance and the latter an account for drawing of advances. Operation of cash credit is same as that of overdraft11. The purpose of cash credit is to meet working capital needs of traders, farmers, and industrialists. The principal advantages of a cash credit account to a borrower are that, unlike the party borrowing on a fixed loan basis, he may operate the account within the stipulated limit as and when required, and can save interest by reducing the debit balance whenever he is a position to do so. Cash credits are against personal security. If there is good turnover both in the account and in the goods, and there are no adverse factors, a cash credit limit is allowed to continue for years together. Of course, a periodical review would be necessary. Inland Bills Purchased - IBPBank purchase two types of Inland Bill – Clean Bill and Documentary BillClean Bills are those, which require no document for payment like Checks, Demand Draft, Pay Order, Telex Transfer, and Mail Transfer etc.Documentary Bills are those, which require related documents for payments like bill of exchange, Railway Receipt, Chalan, and Invoice etc. Before granting a limit, the banker satisfies himself as to the creditworthiness of the drawer. Sometimes banks verify the financial standing of the drawees of the bills, particularly when the bills are drawn from time to time on the same drawees and /or the amounts are large.Sometimes, overdraft or cash credit limits are allowed against the security of bills. A suitable Margin is usually maintained.

11.Hasem, Abul; What the Banker Does, 2/E; p-53-54.

Bills Discounted

Usance bills, maturing within 90 days or so after date or sight, are discounted by banks for approved parties. The difference between the present worth and the amount of the bill is represents earnings of the banker for the period for which the bill is to run. In banking terminology this item of income is called “Discount”.Discounting of issuance bills/ promissory notes constitutes a clean advance against two or more signatures of independent parties, one that of the endorser, and the other that of the drawer / maker. Hire –purchase and Leasing Finance

Banks entertain advances to parties who finance hire purchase business relating to transport vehicles, machinery and durable consumer goods e.g. refrigerators, radiograms etc. Banks have also started lending to leasing companies. They have been recently permitted to establish subsidiary companies undertaking leasing business.Temporary Overdrafts

An un-interrupted temporary overdraft facility allowed by a bank extending over a period of time, says a few years, and though without execution of documents, is tantamount to a contract between customer and the bank. A contract is implied from the conduct of the parties. The bank cannot therefore unilaterally terminate the facility without giving the account-holder due notice in this regard.12

Clean Advances

Traditionally, clean (unsecured) advances were granted for short periods after taking into consideration the net liquid resources of the borrowers. Since there was no security to fall back upon, only such parties were considered eligible as would, at short notice, be expected to adjust the amount. Credit, Capital and Capacity had, therefore, to be carefully assessed before such facilities were allowed. Clean advances are generally spread over a number of parties and are sometimes required to be reinforced by suitable guarantees. Term Loans

12 Indian Overseas Bank vs. N.D. Govindlal Patel, A.L.R.1980,Gujarat, p-158

Since some time, bankers have started lending large amounts for fairly long periods to industries and agriculture on the security of fixed assets on “term-loan” basis. Such loans are repayable by installment over a number of years ranging from 3 to 10 and sometimes more. Bridge Loan

Usually term loans are sanctioned by financial institution such as State Finance Corporations, ICICI and IDBI etc. Sometimes when these institutions are unable to disburse the loans already sanctioned either for what of completion of documentation formalities or, as in the case of some State Finance Corporations, for what of resources, it is customary for them to commercial bank to extend what are known as ‘bridge loans’ for temporary periods as a stop gap arrangement.Participation / Syndicated Loans

The size of industrial units is expanding rapidly as requirements for finance. Where the amount of an advance is Large, no bank could afford or would like to sanction the entire limit singly, in such cases two or more banks agree to advance jointly to one borrower in certain agreed proportions against a common security. In such cases the borrower is one, the security is common and the lending banks are more than one. Such loans called participation loans or consortium finance.Types of LoansTable-3.2 Types of Loans

Types of Loans Characteristics

Industrial Loans

It is given at equal monthly installmentInterest rate is 15.00%Grace Period is allowed depending on types of projectTo facilitate the industrial growth this is given

Transport Loans

This is given to accelerate the transport facility nationwideInterest rate is 15.00%It is given at equal monthly installmentOthers conditions are almost same as the Industrial Loans

House Building Loans

This Loan is give for the construction of dwelling house.It is given at equal monthly installmentInterest rate is 15.00%This Loan is not given frequently.

Others Loan – Including agricultural Loan

Agricultural loan is given from this branch of Premier Bank at the rate of 12.00-14.00%.

Every Bank has to send a quarterly CIB Report to the Bangladesh Bank for amounts due up to TK.50, 000/- mentioning the name of the borrower and the purpose for which loan has been sanctioned and a monthly statement for the amount due more 1 crore Taka. Bangladesh Bank provides CL (Classification Form) to every bank for preparing this report. Bank preserves following provisions for continuous, forced, and term loan:

For unclassified loan 1%. For SME Loan 5% For substandard loan 20% For doubtful loan 50% For bad loan 100%

Staff Loan

STAFF HOUSE BUILDING LOAN – SHBL The branch manager is getting this facility. Repayment is adjusted from his monthly salary. Repayment is made at equal monthly installment.

STAFF LOAN AGAINST PROVIDENT FUND – SPF 10% of basic is contributed by employee in every month 10% of basic is also contributed to the PF by the Bank Repayment is adjusted from their monthly salary Staffs can take loan against PF

Classification of Bank Loans

Bank is an institution which is engaged in the business of money and loan. The more loans a bank can provide the better and beneficial for the bank it will be. The loan should be provided to the appropriate users and they must be monitored in order to ensure the repayment of principal along with interest as and when become due. Loans can be of different types according to the terms, users and security.

In the following chart, the classifications of loans are depicted:

Loan

Based on Users Based on tern Based on security

Unsecured (NoIndividual Industry Businessmen Farmer Landless collateral)

Consumption Working Capital Non-crop

Fully-secured (with Housing loan Crop loan Collateral Export/Import Education/Medical Farming Party Securitized & others Equipments

Short-term

Working capital Fixed capital Loan Loan Medium-term

Distribution Long-term

One term Installment Poultry Housing Loan Medical

Fig: 3.2 Types of loanThe types of loans are discussed below:Classifications based on users:Individual Loan:

i) Consumer Loan: Banks provide loans for durable goods/ applications and commodities like-loans for Freeze, TV, Computer, Car, Furniture etc.

ii) Housing Loan: This includes loans given to the fixed or low-income people for housing purposes. This loan is usually intermediate and or long-term.

iii) Education/Medical and Other Loans: Some of the banks also provide loans to the people of the society in order to meet their educational or medical needs after being sure about the repayment.

Industry Loan:i) Working Capital Loan: This type of loan is given to the business/

industry to provide capital required for purchasing raw materials, paying wages and fuel expenses etc.

ii) Fixed Capital Loan: Huge amount of capital is required for procurement and replacement of machinery/ equipments for the industrial organizations.

Loans for Business Personsi) Working Capital Loan: For maintaining day-to-day transactions,

businesspersons need a great deal of working capital. By providing working capital loans, banks help to solve this working capital necessity of the businesspersons.

ii) Export-Import Loan: Banks also help in export-import firms/ companies by issuing L/C, bill of exchange, discounting, direct loans etc.

Loans of Farmersi) Crop Loan: For buying seeds, cows and fertilizers, farmers need

money. They borrow the money from the bank in order to meet he expenses required.

ii) Non-Crop Loan: Farmers also need money for poultry, fisheries, agro-business, agro-processing and other purposes. In this case, socialized/ commercial banks provide small/medium loans to farmers.

iii) Farming Equipment Loan: To purchase farming equipments, banks also provide loans to farmers. Farming equipments may include- power tiller, tractors, machinery for irrigations, etc.

Loans for Landless People:

People are having no land or lands of less than 0.5 acre of land may be called landless people. The different types of loans that are usually provided to landless people are given below:

i) Small Business Loans: Banks may provide loans to landless people to establish income generating micro-enterprises, small businesses, poultry firms or fisheries. The purpose of banks is to help landless people to overcome financial distress as well as to build up some capital for future investment.

ii) Housing Loan: Bank may provide housing loans to those who have small price of land but don’t have any resource to erect a house just to protect them from rains and sun shines besides earning social status and protection from thieves.

iii) Medical Loan: Loans may be given to landless people also for medical purposes.

Classification based on Term/ Periodicity:According to classification by Term/ periodicity, loans can be of three types: i) Short-Term Loans: This loan is sanctioned for less than one year. These

can be of two types: a. Loans provided for immediate use & payable on demand b. Loans payable on short notice. ii) Medium Term: Usually, loans with the maturity of 1 to 5 years are called

midterm loans. However, commercial banks give medium loans of maturity of 1-3 years.

iii) Loan term: Loans with the maturity of more than 5 years are called long-term loans.

Classification Based On Security:i) Unsecured Loan: Banks, often, provides loan without any type of

collateral to the reliable persons or institution as clients having profound goodwill, excellent track record or sometimes to the very poor clients.

ii) Fully Secured Loans: If the loan is given by taking the security/collateral of the amount exceeding the amount of loan or just equal to the amount of loan, it is called “fully secured loans”.

iii) Partly Secured Loans: If the amount of loan is not fully secured, rather partial amount of collateral is provided to cover the loan sanctioned; it is called “Partly Secured Loan”.

Advances against Balances in SB, CD A/C and Term Deposit ReceiptPrecautionary Measures:Subject to the credit restrictions imposed, adopt the following precautionary measures in allowing advances against balances lying in the Savings Bank and/or Current Deposit Accounts of the parties:

The account is not in the name of a Minor. Make a note of it at the top of the account in the computer.

Right of set off when balance ear-marked in another Account of the borrower: While allowing advance to the customer against a credit balance earmarked/liened in another accounts kept by him in his own name and in the same rights, whether at the same Branch or at some other Branch of the Bank, take a letter of authority from the account-holder to combine the two accounts (one having a credit balance and the other a debit balance), at any time without notice, and to return checks which, as a result of the Bank having taken such an action, would overdraw the combined account. He should also agree not to close the account and withdraw the balance, pending adjustment of the advance.Right of appropriation-Balance earmarked in the Account of a third party:Where the advance is allowed against credit balance, ear-marked/lined in the account of a third party. whether at the same Branch or at some other Branch of the Bank, take an irrevocable letter of authority from that third party, authorizing the Bank to appropriate the credit balance lying in their account to the extent of the debit balance appearing in the account of the borrower, at any time, without any reference to them. This being an irrevocable letter of authority, they should agree neither to close the account pending adjustment of the advance allowed at their instance, nor to issue checks which would reduce that balance.The signature of the account holder in whose account a credit balance is ear-marked is verified on the irrevocable letter of authority given by him.The third party account is not in the name of a Minor.Confirmation having earmarked the credit balance maintained with other Branch of the Bank. In case, advance is allowed against credit balance, maintained with other Branch of the Bank, obtain a confirmation letter from

that Branch to the effect that they have earmarked the credit balance in question and shall not close the account and honor checks, which will reduce the balance, until they receive clearance from the Branch allowing the advance.Advances Against Life Insurance Polices and SharesProposals for advance from known and respectable clients only should be entertained. The Insurance Policy is an endowment policy. The borrower has an insurable interest in the life of the insured, if the policy does not stand in his own name. Ensure that the policy is properly stamped. The policy does not bear any restrictive of qualifying conditions likely to affect its value as a security. The advance should be restricted to 90 percent of the surrender value to cover interest etc. The surrender value of the policy is ascertained from the Insurance Company/Corporation (policies for less than three years have no surrender value).Take a legal assignment by deed duly stamped at the customer’s expenses and obtain the policy at the same time. The policy is assigned to the Bank by the assured and the assignment is sent to the Insurance Company/Corporation at its principal place of business in Bangladesh for registration and return. There should be provided power for the banker to surrender the policy for cash or otherwise to deal with or dispose of if as the banker may consider necessary fit in the event of failure on the part of the borrower in payment of the dues on due date or on demand being made by the Bank. All persons interested in the policy must join in the assignment. The assignment should be attested by witness. If there is previous assignment, such previous assignees have to reassign the policy in favor of the insured and if this is not done, all such previous assignee should join the assignment in favor of the Bank and all other loan documents. Along with the assignment, a notice in duplicate is also sent to the Insurance Company duly signed by the assignor and the Bank notifying the assignment and requesting them to disclose the surrender value of the policy along with any prior charges registered there against. They should also be requested to return to the Bank, a copy of the notice bearing the Company’s/Corporation’s acknowledgement.An undertaking is obtained from the assured that he shall keep on paying the premium punctually, and produces the receipts to the Bank, and shall not do anything which might cause the policy to be void.After the loan is repaid the Bank reassigns the policy back to the borrower. The form of reassignment is as follows:

Advance may be allowed against shares of various companies quoted on the Stock Exchange against required margin, and subject to credit restrictions imposed from time to time.The Branch should obtain a letter of lien from the borrower/holder in respect of all such shares which stand in his name, or which have been sent to the various companies for registration, in his name.Shares standing in the name of third parties should not, as a rule, be taken as security unless accompanied by proper letter from such third party agreeing to the shares being pledged to the Bank and giving up his own right in favor of the borrower with blank Transfer Deed.Where advance has been allowed to the borrower at the specific request of a third party against shares owned by them, the letter of lien shall be obtained from third party and not from the borrower.In the event of transferring the shares in the name of the Bank with the approval of the Head Office, Branches shall take special notice of any declaration of Dividend, Bonus Shares or any offer of Right Shares made by the companies concerned. They shall also ensure that all such Dividends and Bonus Shares are duly received by them.The dividend is credited to the account of the borrowers and the bonus shares are kept along with other shares of the borrowers.The case of an offer of Right Shares, Branches shall send intimation to the borrowers concerned enquiring from them if they were interested to acquire them for the value mentioned on the Letter of Rights, which should immediately be deposited by them with the Bank. If the borrowers do not deposit the money from their own resources or make any alternate arrangement in that behalf, the Letter of Rights may be renounced with the permission of the Head Office and sold, and the sale proceeds should be credited to the borrower’s account under intimation to him.Advances (Loans, Overdrafts& Cash Credits) Against Pledge of Goods/StocksAdvance facility may be extended against security of Pledge of goods/stock (raw materials as well as finished product). In this case, the client surrenders the physical possession of the goods under Bank’s effective control. The ownership of the goods is, however, retained with the client. The pledge of the goods creates an implied lien in favor of the Bank on the concerned goods and if necessitated, Bank can sell the goods for adjustment of the advances by giving

proper notice to the borrower. Sometimes collateral securities are also obtained if the Bank deems it necessary. While allowing credit facility against pledge of goods/stocks, the following points will be considered subject to restrictions imposed by Bangladesh Bank from time to time.Advances (Loans, Overdrafts& Cash Credits) Against Hypothecation of Good/StocksAdvance may be sanctioned to a client against primary security of hypothecation of raw materials and/or finished products. Under this arrangement, the borrower by signing a letter of hypothecation duly stamped creates a charge against the goods for an amount of debt but neither the ownership nor the possession of the same is passed on to the Bank. Only a right or interest on the goods is created in favor of the Bank, but the borrower binds himself to give possession of the goods to the Bank when called upon to do so. Hence, in order to secure the advance, Bank normally insists on the borrowers to provide suitable collateral security. While allowing credit facility against hypothecation of goods/stocks the following points shall be considered subject to restrictions imposed from time to time:

The facility is to be allowed only to the trustworthy having undoubted standing and credit worthiness.

The goods are readily sellable and have constant and effective demand in the market.

Banks only for working capital and not for capital investment allow hypothecation advance.

The goods are not subject to rapid deterioration due to storage for short or long duration.

The borrower has an absolute title in goods. The goods are not encumbered and/or hypothecated to any other Bank. The prices of the goods are steady. In case agricultural crops, the crops should be of current season and the

advance is adjustable before the crops of next season comes in the market. A declaration to be obtained from the borrower that he shall not charge the goods hypothecated to another person/Bank without prior consent of the Bank.

Careful valuation of the goods and its quantity has to be made. The selling price of goods is to be ascertained from the market. The goods are to insured covering all risks under Bank mortgage clause.

Stock report duly signed by the borrower is to be obtained in Bank’s printed preformed at least once in a month but while releasing funds, up to date position of the stocks should be obtained. In the event of default, the Bank would be free to stop further drawings.

Fixation of margin, valuation of commodity and drawing power of a borrower are to be done carefully in the manner as advised under advances against pledge of goods/stocks.

Advances (Loans) Against Hypothecation of Transportation, Capital Machinery etcPoints for General Consideration:Banks allow advances against power driven Vehicle and subject to Credit restrictions as applied from time to time.The following points are considered before selecting a proposed borrower:

The customer is trustworthy and has got fair relation with the Bank. The constituent is preferably a transport operator. He has adequate experience in transport business. The value of the vehicle Projected cash flow vis-à-vis size of repayment installments This is a medium term loan This is generally allowed under Hire-Purchase or Lease Financing.

PRICING CONSUMER AND REAL ESTATE LOANS

Pricing Consumer and Real Estate Loans

A financial institution prices every consumer loan by setting an interest rate, maturity and terms of repayment that both the lender and customer find comfortable. While many consumer loans are short term, stretching over a few weeks or months, long-term loans to purchase automobiles, home applications and new homes may stretch from one or two years all the 25 or 30 years. Competition among consumer credit suppliers is also a power factor shaping consumer loan rates. Where banks face intense competition for consumer loans, interest rates tend to be driven down closer to loan production costs.

Shorter-term cash loans may be unsecured, but longer-term loans like purchasing automobiles and other consumer durables are nearly always secured by the assets purchased.The Interest Rate Attached to Nonresidential Consumer Loans

Most consumer loans, like most business loans, are priced off some base or cost

rate, with a profit margin and compensation for risk added. Such as the Cost-

plus Model:

Loan rate Paid by the Consumer

=Marginal cost of raising loan able fund to lend to the borrower

+Non funds operating cost

+Premium for term -risk of consumer default

+Premium for term- risk with a longer term loan

+Desired profit Margin

Banks use a wide variety of methods to determine the actual loan rates they will offer to their household customers. The most popular methods for calculating consumer loan rates include The Annual Percentage Rate (APR), The Simple Interest Method, The Discount Rate, and The Add-On Rate Method. The Annual Percentage Rate (APR)

The APR13 is the internal rate of return that equates total payments with the amount of the loan. It takes into account how fast the loan is being repaid and how much credit the consumer will actually have use of during the life of the loan.The Simple Interest Method

The Simple Interest approach, like the APR, also adjusts for the length of time a borrower actually has of the credit for which he or she is paying. If the customer is paying off a loan gradually, the simple interest approach first determines the declining loan balance, and that reduced balance is than used to determine the amount of interest owed.

Interest owed = Principal X Rate X Time

13 The Truth-in-Lending Act, passed in the United States in 1968

The Discount Rate Method:

While most consumer loans allow the customer to pay off the interest owed, as well as the principal, gradually over the life of a loan, the discount rate method requires the customer to pay interest up front. Under this approach, interest is deduced first, and the customer receives the loan amount less any interest owed.5.2.4 The Add-On Loan Rate Method:

One of the oldest rate calculation methods is known simply as the add-on method because any interest owed is added to the principal amount of the loan before customer is total what the required installment payments will be.

Effective Interest owed Loan rate = Average loan amount year

5.3 Compensating Balance Requirements

Many banks require that consumer-borrowing money from them keep a certain percentage of the loan amount in a deposit account. This so-called compensating deposit balance requirement raises the effective cost of a consumer loan because the borrower does not have use of the full amount of the loan. Instead, the borrower only has use of the loan amount minus the required deposit balance. The effective interest return to the bank then rises above the loan rate quoted to the borrower.

Effective loan Amount of interest owed on the loan Rate with compensating = Balance Total amount borrowed less compensating balance Required required

Use of Variable Rates on Consumer Loans

The majority of installment and lump sum payment loans to families and individuals are made with fixed interest rates rather than with floating

rates that change with credit market conditions. However, due to the volatility of interest rates a greater number of floating-rate consumer loans have appeared. When floating-rate consumer loans are issued, their contract rates are most often tied to either the prime (commercial) at loan rate or to U.S. Treasury bill rates in what is often called base rate pricing.

Floating prime-based Consumer loan rate

= Prime or base rate

+ Risk premium

Interest Rates on Home Mortgage Loans

The trend toward more flexible loan rates is particularly evident in home mortgage lending where most lenders offer both fixed-rate mortgage (FRMS) and adjustable- rate mortgages (ARMS). In the case of an adjustable-rate loan, bank loan officers must be especially careful in deciding whether a borrowing customer has sufficient budgetary flexibility to be able to adjust to variable loan payments, particularly if it seems likely that market interest rates may rise significantly over the life of the loan. Practices Observation The management of the branch always tries to provide quality service to customers. As a result, they have got a huge number of deposits accounts14 in this Branch. The BCBL (Bangla Bazar) Branch started on 16 September 1999 with three functional departments as following. 1) The general Banking department 2) The Credit division and 3) The Foreign Exchange department The General Banking Division deals the day-to-day transactions. This is the busiest department among all three departments. The Credit Division distributes loans, and monitors credit recovery related activities. The foreign Exchange Division deals their different activities with the help of Head Office.Products and Services of the Branch:In the Respective Branch of BCBL is always conscious of the changing needs of the customers and strives to develop new and improved services for its valued customers. Bank offers various Deposits and Lending Products, and Services to 14 Total Deposit: 2141187820 in 2008

meet all kinds of financial needs of customers. The Branch offers following products and services:

Table- 6.1 Products descriptionLiability Products

Saving Account Monthly Profit Scheme

Current Account Monthly Saving Scheme

STD Account Double Benefit Scheme

Foreign Currency

Account

Triple Benefit Scheme

Fixed Deposit Receipt

(FDR)

Education Savings Scheme

Lacpati Deposit Scheme Bills payable

Millionaire Deposit

Scheme

Marriage Deposit Scheme

Crorepati Deposit

Scheme

Table- 6.2 ProductsLending Products

i

Consumer Credit Scheme

Personal Loan

Loan Ag. Trust

Receipt

Secured Overdraft

Cash Credit Payment Ag. Document

Table- 6.3 Services description

ServicesTreasury

Remittance

Evening Banking

The branch has Fifteen (15s) Liability Products shown in table-6.1, Six (06) Lending Products shown in table-6.2 and three (3) Services shown in Table-6.3. One special feature of this bank is paying interest to the Savings & Corporate Savings Accounts on daily balance basis.

Deposit DescriptionDeposits are well recognized as the blood of financial institutions especially banks. Inevitably they constitute the very foundation of a bank. In pursuit of deposit mobilization the branch the most successful during 2007 with a record level of deposit balance of Tk.2141.27 million from 1832.43 million in 2006.

Table- 6.4 Deposit details (Demand)Demand Deposit

accountsMillion

(TK)% of total

TK

Current Account 43.45 14.6

Saving Account 1078.59 29

Short Term Deposit (STD)

200.43 10.1

Education Savings Scheme

2.12 0.3

Sundry Deposits 1333.25 31

Bills Payable 672.99 15

Total 7750.09 100

Table- 6.5 Deposit details (Time)Time Deposit accounts Million (TK) % of total

TKMonthly Saving Scheme

46.91 25

Monthly Income Scheme

99.93 53

Double Benefit Scheme42.46 22

Total 189.30 100

Time Deposit

25%

53%

22%

Monthly SavingScheme

Monthly IncomeScheme

Double BenefitScheme

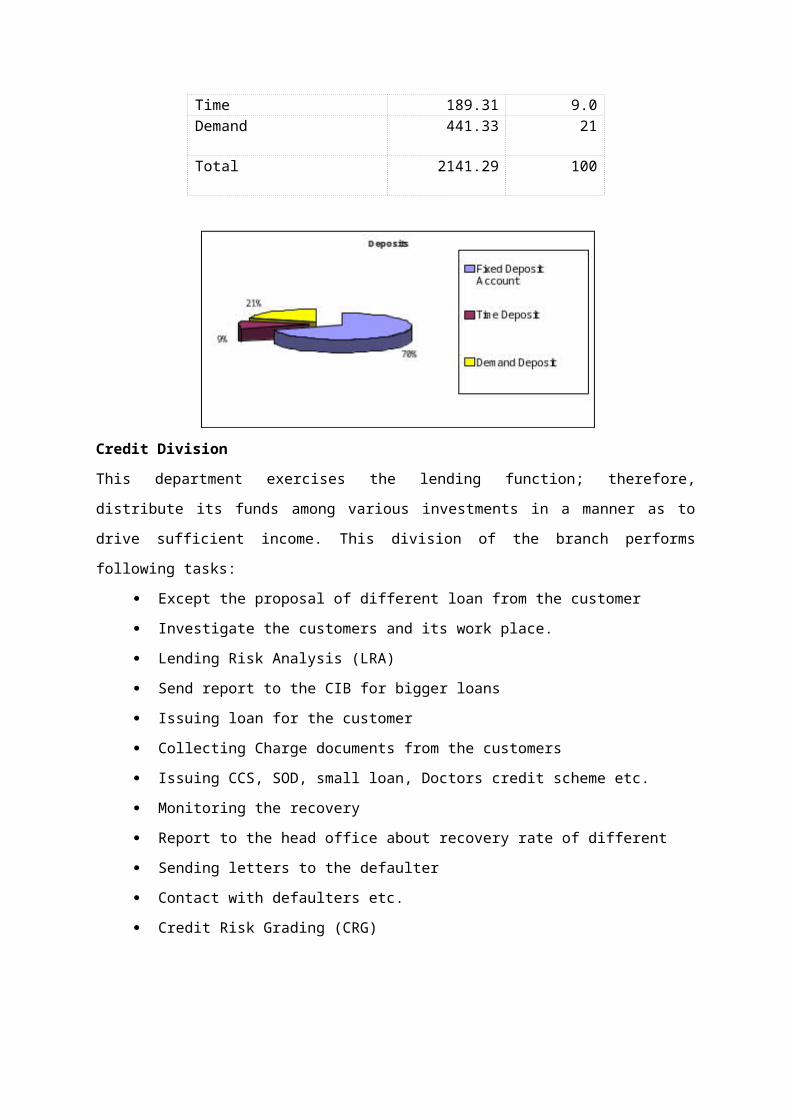

Table- 6.6 Deposit detailsDeposits Million (TK) % of total

TKFixed Deposit Receipt (FDR)

1510.65 70

Time 189.31 9.0Demand 441.33 21

Total 2141.29 100

Credit DivisionThis department exercises the lending function; therefore, distribute its funds among various investments in a manner as to drive sufficient income. This division of the branch performs following tasks:

Except the proposal of different loan from the customer Investigate the customers and its work place. Lending Risk Analysis (LRA) Send report to the CIB for bigger loans Issuing loan for the customer Collecting Charge documents from the customers Issuing CCS, SOD, small loan, Doctors credit scheme etc. Monitoring the recovery Report to the head office about recovery rate of different Sending letters to the defaulter Contact with defaulters etc. Credit Risk Grading (CRG)

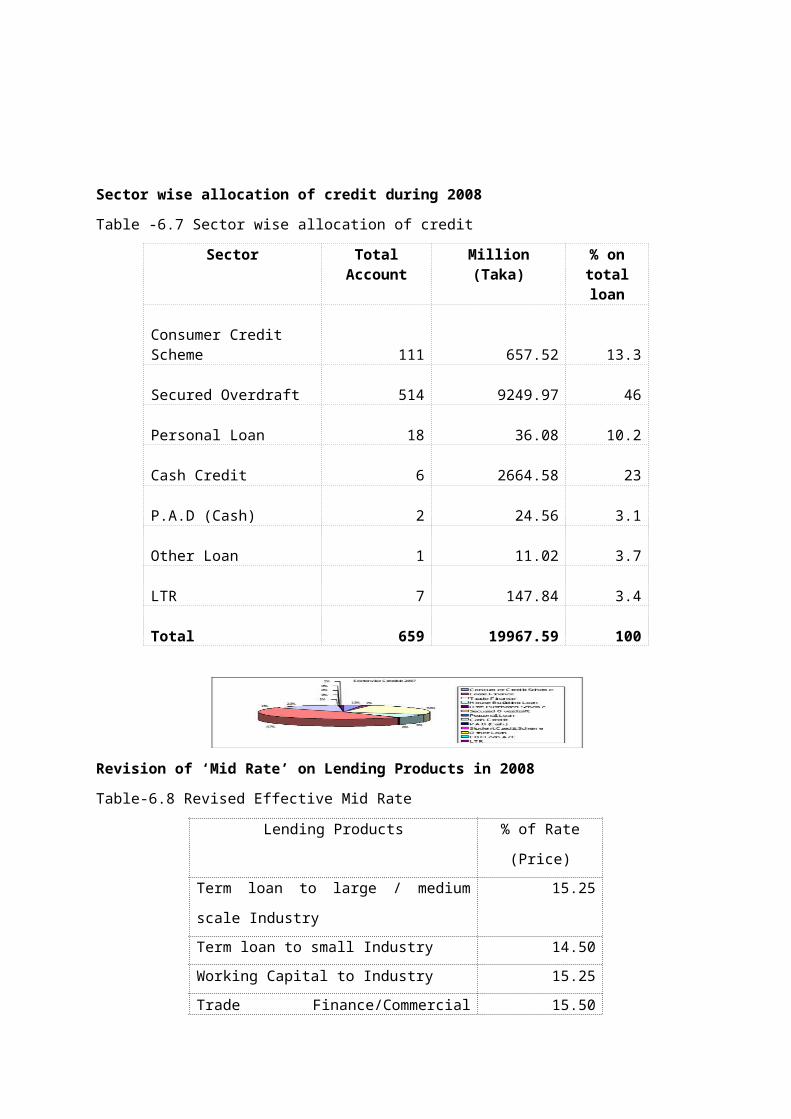

Sector wise allocation of credit during 2008Table -6.7 Sector wise allocation of credit

Sector Total Account

Million (Taka) % on total loan

Consumer Credit Scheme 111 657.52 13.3

Secured Overdraft 514 9249.97 46

Personal Loan 18 36.08 10.2

Cash Credit 6 2664.58 23

P.A.D (Cash) 2 24.56 3.1

Other Loan 1 11.02 3.7

LTR 7 147.84 3.4

Total 659 19967.59 100

Revision of ‘Mid Rate’ on Lending Products in 2008Table-6.8 Revised Effective Mid Rate

Lending Products % of Rate (Price)

Term loan to large / medium scale Industry

15.25

Term loan to small Industry 14.50Working Capital to Industry 15.25Trade Finance/Commercial Lending 15.50Credit to Nationalized Bank Financial Institutions (NBFIs)

15.50

Others 15.50SME 11Agriculture ((SC-1)15 and (SC-2)16 11.50 / 10

Export 7.0Consumer Credit 18Credit Card (Per Month) 2.50

Terms/ Conditions1. The effective Mid Rates on lending are mentioned in table 6.4.

15 SC-1: Represents finance in Fertilizer Industry16 SC-2: Represents finance in Agriculture, Plantation, Horticulture etc

2. Interest Rate can be varied by mid-rate 1.5% on case-to-case basis.3. Interest rate spread for loan against FDR, which is 3% above the rates.

Loan Recovery Categorization and the branch’s positionThe procedure for loan classification is given by Bangladesh Bank under BRPD circular no 16, dated 06/12/1998.According to Bangladesh Bank categorization there are four types of loan. If any borrower fails to repay his amount or installment within the specified period then it will fall under the following classification status.

Table -6.9 Loan Recovery CategorizationClassification

Types of Loans Account

Continuous loan

(C/C; O/D)

Demand loan (LIM; PAD; FBP; IBP)

CL in 2008

DL in 2008

Unclassified Less than 6 months

Less than 6 months

- -

Special Mension Account

3 months or more but less than 6 months

3 months or more but less than 6 months

- -

Substandard 6 months or more but less than 9months

6 months or more but less than 9 months

- -

Doubtful 9 months or more but less than 12 months

9 months or more but less than 12 months

1 -

Bad loan 12 months or more

12 months or more

1 -

In the Branch, we can see the Table- 6.4 Loan Recovery Categorization in 2008 that has no Unclassified, SMA, Substandard loan but One Doubtful loan which is Prime Thread Ltd, Amount Tk.166363.64 and12/09 /2006. And One Bad loan that is M/S. Sujana, amount Tk.3919992.54, 2/11/2001.

Table -6.10 Loan Recovery CategorizationClassification

Types of Loans

Term loans to be

overdue after 6 months

Amount in 2007

Term loans to be

overdue after 12 months

Amount in 2007

Unclassified Less than 6 months

- Less than 12 months

-

Special Mension

3 months or more but

- 3 months or more but

-

Account less than 6 months

less than 12 months

Substandard 6 months or more but less than 12 months

- 12 months or more but less than 36 months

1

Doubtful 12 months or more but less than 24 months

2 36months or more but less than 48 months

-

Bad loan 24 months orMore

1 48 months or more

2

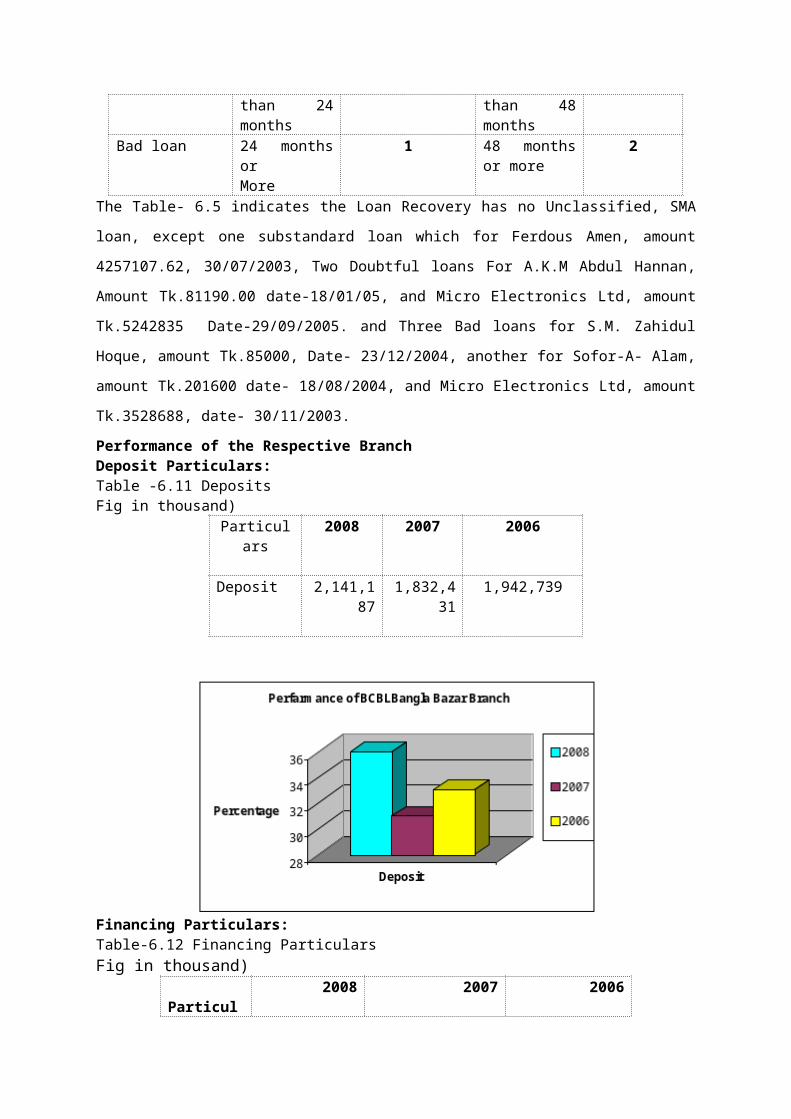

The Table- 6.5 indicates the Loan Recovery has no Unclassified, SMA loan, except one substandard loan which for Ferdous Amen, amount 4257107.62, 30/07/2003, Two Doubtful loans For A.K.M Abdul Hannan, Amount Tk.81190.00 date-18/01/05, and Micro Electronics Ltd, amount Tk.5242835 Date-29/09/2005. and Three Bad loans for S.M. Zahidul Hoque, amount Tk.85000, Date- 23/12/2004, another for Sofor-A- Alam, amount Tk.201600 date- 18/08/2004, and Micro Electronics Ltd, amount Tk.3528688, date- 30/11/2003.Performance of the Respective BranchDeposit Particulars:Table -6.11 Deposits Fig in thousand)

Particulars

2008 2007 2006

Deposit 2,141,187 1,832,431 1,942,739

Financing Particulars:Table-6.12 Financing ParticularsFig in thousand)

Particula2008 2007 2006

rs

Advance 1,996,759 1,649,611 963,112

Export 3,731,584 1,973,083 596,654

Import 2,376,080 1,454,273 1,923,676

Financing Particulars: (income/ expenditure) Table-6.13 Financing ParticularsFig: Thousand)

Particulars

2008 2007 2006

Income 354,355 321,887 262,860

Expenditure

224,984 224,984 172,050

Profit 129,370 120,109 90,810

Ratio Analysis• Ratio Analysis is a method to express the relationship among selected

items of the financial statement data.

• Ratio analysis has used to evaluate a company’s operating performance and financial stability over a period.

• Though the Bangla Bazar branch has no information to do ratio analysis, so have done of the BCBL.

Table – 6.14 Ratio analysesRatio Bangladesh Commerce Bank

LtdIndustry Avg.

Liquidity Ratio 2008 2007 2008

2007

Current ratio

Current Assets (CA)

CurrentLiabilities

(CL)

32353.2

23681.5

2700721630

1.4 1.2 1.5 1.7

Networking Capital ratio

CA-CLCA

8671.732353.

2

537727007

0.27 0.2 0.35 1.7

Leverage Ratio

Debt to total assets ratio

Total debt Total Assets

30107.5

32573.19

2554427171

0.93 0.94 0.94 0.92

Debt equity ratio

Total-Long-Term debtsTotal equity capital

6428.02465.4

39141626

3 2.4 4.7 4.16

Profitability Ratio

Income to total assets

Net income Total assets

78.75632573

368.727170

0.0007

0.01 0.0003

0.013

Net income to equity

Net incomeEquity & retained earnings

78.7562465.4

368.71626

0.03 0.22 0.05 0.16

Earning Profit after 78.756 368.7 4.66 43.63 8.04 31.9

per share taxationAvg number of ordinary

shares

16.89 8.45 4

Investment to capital fund ratio

Investment (Loans & Advance)Capital Fund

23637.61

2792.33

20677.68

1855.58

8.5 11.14 10.06 8.19

Investment to Deposit ratio

Investment (Loans & Advance)Deposit Fund

23637.61

27114.47

20677.68

24199.01

0.8718

0.8545

0.79 0.74

STRENGTH: The bank has 1.4 times more current assets than the current liabilities in

order to meet any liquidity crises. This is a strength of the bank. Although the industry average is higher than PBL, the current ratio of PBL is considerably satisfactory.

WEAKNESS: The income to total assets ratio of BCBL decreased from 1% to 0.07%

during 2007-2008.This reflects the weakness of the bank financial management.

ROE is 3% whereas industry average during the year was 5%. Compare to previous year, it also decline blatantly by 19%

OPPORTUNITY: The net working capital has increased from 20% to 27%, which shows

higher business opportunity for the BCBL. Net income to equity ratio shows that the net income of the bank is

contributing a good amount to the banks equity and retains earning and this was made possible due to good business opportunity of BCBL.

THREAT: The bank has 93% loan capital for funding total assets. Definitely, it is

threat for the bank. The bank has three times more long-term debt than its total equity

capital for which they may require considerable efforts to arrange more funds for the bank.

The bank has investment (Loans and Advances) 8.5 times from the total capital fund it is more risk for bank.

The bank has investment (Loans and Advances) 87.18% of the deposit, but the Industry average has 79%, that is compatible should be around.

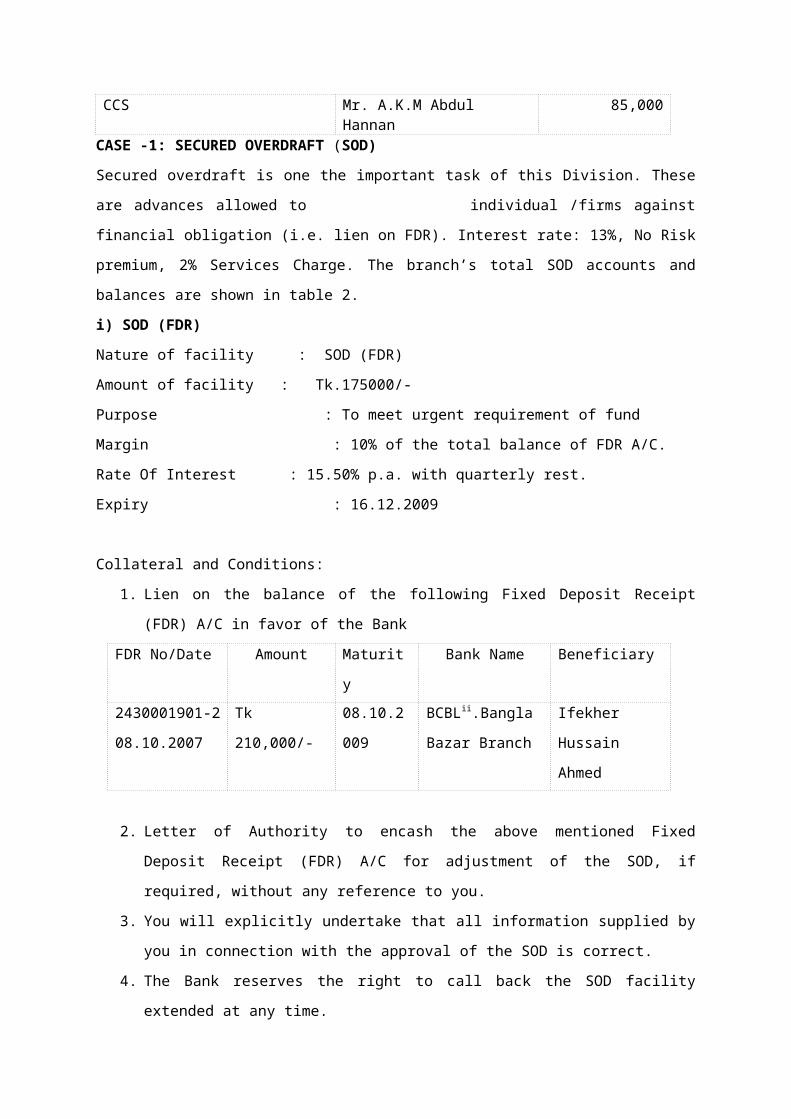

CASES STUDYEIGHT CASES HAVE BEEN PICKED OUT FROM THE BANK BRANCHTypes of Loan Borrowers Amount (TK)SOD (FDR) Ifekher Hussain Ahmed 175000SOD (FO) Khandaker Mujahidul

Hoque.2 84,000

Cash Credit (Hypo) Md. Rafiqul Islam 40,00,000CCS Mr. Akhlaq-Uz-Zaman 5,00,000CCS Mr. A.K.M Abdul Hannan 85,000

CASE -1: SECURED OVERDRAFT (SOD) Secured overdraft is one the important task of this Division. These are advances allowed to individual /firms against financial obligation (i.e. lien on FDR). Interest rate: 13%, No Risk premium, 2% Services Charge. The branch’s total SOD accounts and balances are shown in table 2.i) SOD (FDR)Nature of facility : SOD (FDR) Amount of facility : Tk.175000/-Purpose : To meet urgent requirement of fundMargin : 10% of the total balance of FDR A/C.Rate Of Interest : 15.50% p.a. with quarterly rest.Expiry : 16.12.2009

Collateral and Conditions:1. Lien on the balance of the following Fixed Deposit Receipt (FDR) A/C in

favor of the BankFDR No/Date Amount Maturity Bank Name Beneficiary2430001901-2 08.10.2007

Tk 210,000/-

08.10.2009

BCBLii.Bangla Bazar Branch

Ifekher Hussain Ahmed

2. Letter of Authority to encash the above mentioned Fixed Deposit Receipt (FDR) A/C for adjustment of the SOD, if required, without any reference to you.

3. You will explicitly undertake that all information supplied by you in connection with the approval of the SOD is correct.

4. The Bank reserves the right to call back the SOD facility extended at any time.

5. Without assigning any reason whatsoever and can adjust the SOD by enchasing the above with or without notice to you.

6. All the above terms and condition should be strictly complied with.7. Interest of FDR A/C will not release till adjustment of the loan.

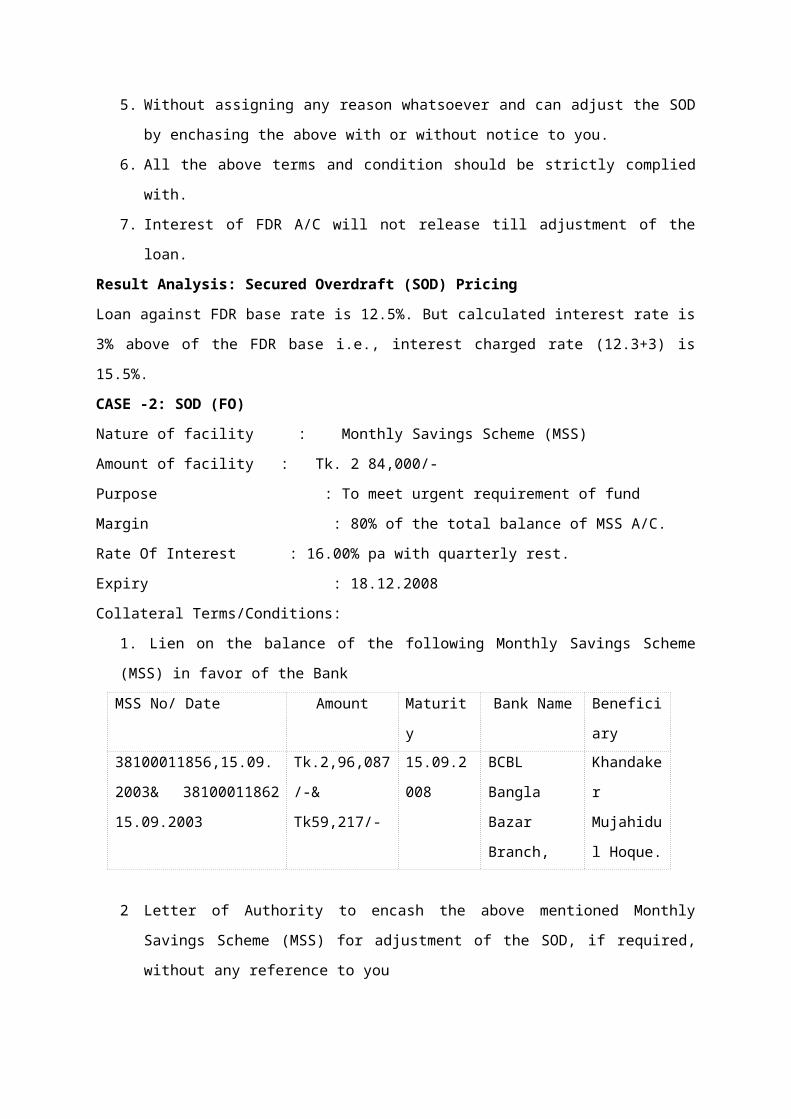

Result Analysis: Secured Overdraft (SOD) PricingLoan against FDR base rate is 12.5%. But calculated interest rate is 3% above of the FDR base i.e., interest charged rate (12.3+3) is 15.5%.CASE -2: SOD (FO)Nature of facility : Monthly Savings Scheme (MSS) Amount of facility : Tk. 2 84,000/-Purpose : To meet urgent requirement of fundMargin : 80% of the total balance of MSS A/C.Rate Of Interest : 16.00% pa with quarterly rest.Expiry : 18.12.2008 Collateral Terms/Conditions:

1. Lien on the balance of the following Monthly Savings Scheme (MSS) in favor of the Bank

MSS No/ Date Amount Maturity Bank Name Beneficiary

38100011856,15.09.2003& 38100011862 15.09.2003

Tk.2,96,087/-& Tk59,217/-

15.09.2008

BCBL Bangla Bazar Branch,

Khandaker Mujahidul Hoque.

2 Letter of Authority to encash the above mentioned Monthly Savings

Scheme (MSS) for adjustment of the SOD, if required, without any reference to you

ii

3 You will explicitly undertake that all information supplied by you in connection with the approval of the SOD is correct.

4 The Bank reserves the right to call back the SOD facility extended at any time.

5 Without assigning any reason whatsoever and can adjust the SOD by enchasing the above with or without notice to you.

6 All the above terms and condition should be strictly complied with.Result Analysis: Secured Overdraft (SOD) PricingLoan against MSS interest rate is 16%.This interest rate calculated by following options:

Financial obligations Loan size Degree of personal relationship

CASE -1: CASH CREDIT (HYPO.) Advances allowed to individual/firm for trading as well as wholesale purpose or to industries to meet up the working capital requirements against hypothecation of goods as primary security fall under this type of lending. It is a continuous credit. It is allowed under the categories (i) “Commercial Lending” when the customer is other than an industry and (ii) “Working Capital” when the customer is an industry. An example of Cash Credit (Hypothetication) is extracted from the respective branch and is shown in table 6.8. Table- 6.8: Case of a Cash Credit (with details terms/conditions)

1 Name of Credit Facility

Cash Credit (Hypo)

2 Amount Tk.40, 00,000 Only

3 Margin 50% on the value of the stock of goods or market price, whichever is lower

4 Rate of Interest 15.50% p.a. at quarterly rest subject to any change that may be made by the Bank from time to time

5 Validity/ Expiry 31.10.2008

6 Repayment From the sale proceeds or customer’s other sources.

7 Purpose For meeting up the working Capital requirement of the business

8 Security i) Hypothecation of stocks of goods in

Business duly issued by a insurance company acceptable to the Bank covering Fire & RSD, Flood & Cyclone, Theft & Burglary etc. However, if the client is unwilling to insure the hypothecation covering Flood & Cyclone, Theft & Burglary through insurance Company, an undertaking to be obtained from the client through Indemnity Bond to the effect that all losses/damages due to Flood & Cyclone, Theft & Burglary will be borne by the client.

ii) Registered Mortgage of 7.65 (2.40+5.25) decimal land along with a five- stored residential building and a three- storied residential building thereon at Bhairab with the following details valuing Tk.81.21 (37.91+43.30) Lac (FSV):

a) 2.40 decimal land with a 05 storied residential building, J.L.324, Khation: 3933, Dag: 9028, Bhairab, Kishoregonj valuing Tk.50.55Lac (market Value) and Tk.37.91 Lac (Forced sales value- FSV) as assessed by enlisted surveyor Bhuiyan Associate and 47.78 Lac & 38.23 Lac (FSV) as assessed by the Branch- Officialsb) 5.25 decimal land with a 03 storied residential J.L.324, Khation: 2925, Dag: 8497, Bhairab, Kishoregonj valuing Tk. 57.74 Lac (market Value) and TK43.30 Lac (Forced sales value- FSV) andTk.56.17 Lac & Tk.44.94 Lac (FSV) as assessed by the Branch- Officials. Both the properties are owned by Md. Rafiqul Islam, proprietor of the concern.

iii) Registered Irrevocable General Power of Attorney to be executed by the mortgagor in favor of the bank enabling the bank to sell the property without intervention of court in case of default

iv) IGPA (duly notarized) to be obtained to sell hypothecated stocks without intervention of the court in case of

defaultv) Personal Guarantee of the proprietor of

the concern along with his spousesvi) Personal Guarantee of mortgagorvii) Post dated check covering the loan

amount.viii) Execution of usual change documents

9 Other Expenditure (if any

Will be borne by the Lessee

Result Analysis: Cash Credit (Hypo.) PricingThe respective branch is not empowered to fix (price) a cash credit interest rate. The interest rate (price of cash credit) is therefore fixed by the Head Office. It should be noted that head office is guided by the central bank (Bangladesh bank) while setting the interest rate for CC. Here in this branch the CC rate is 15.5% and for the concerned case -1 thus the rate (price) is charged so.

CASE -1: CONSUMER CREDIT SCHEMEIt is a special credit scheme of the Bank to finance purchase of consumers’ durable to the fixed income group to raise their standard of living. The loans are allowed on soft terms against personal guarantee and deposit of specified percentage of equity by the customers. The loan is repayable by monthly installment within a fixed period.Table- 6.12 Cases of Consumer Credit Scheme (Details Terms)1 Name of Credit

FacilityConsumer Credit Scheme

2 Amount Tk.5, 00,000 Only

3 Price of the Car Tk12, 75,000/- only

4 Rate of Interest 14.5% p.a. at monthly rest subject to any change that may be made by the Bank from time to time

5 Service Charge 3% Agent commission (with monthly rest) - The management of the may change the rate of interest from to time.

6 Validity/ Expiry 26.11.2013

7 Repayment The loan will be repaid by 60 equal monthly installments of tk12600/=

8 Purpose To Purchase an Unregistered Reconditioned Toyota Corolla X Sedan Car, Chassis # NZE121-3317975, Model Year: 2005, Color: Silver. Dated: 18.11.2008.

9 Equity Participation

Tk.7, 75,000 only (60.78% of total value of the car)

10 Security i) The vehicle will be registered in the joint name of the bank and insurance coverage.

ii) Personal Guarantee of mortgagor

iii) Post dated check covering the loan amount

iv) Execution of usual change documentsResult Analysis: Consumer Credit Scheme PricingConsumer Credit Scheme interest rate (Price) is 14.5% which is computed by following bases:

Principal lease amount = Tk.12, 75,000

Down payment = 60.78% of lease amount =Tk7, 75,000

Remaining due=Tk5, 00,000

Monthly installment payment = Tk.12600 for 60 monthsOther charges = Agent commission =3% monthly restTotal price of the CCS loan Tk.15, 31,000 CCS property cost price 12, 75,000Interest (profit) 256,000Considering total return on current investment the borrower is basically paying 17% rather than the nominal rate as mentioned (price) 14.5%.CASE 2 CONSUMER CREDIT SCHEME

Table- 6.13 Cases of Consumer Credit Scheme (Details Terms)1 Name of Credit

FacilityConsumer Credit Scheme

2 Amount Tk.85, 000 Only