Embed Size (px)

DESCRIPTION

good

Citation preview

CHAPTER 6

ISLAMIC BANKING IN

MALAYSIA

1 snurazani/2011

OBJECTIVES

By end of this chapter student must be able to:

1. Interpret the Islamic Banking concept

2. Explain the need for Islamic Banking in the

financial system

3. Describe the Islamic financial instrument the are

available in Malaysia

4. Compare Islamic banking system to conventional

banking system

5. Explain the implementation of Islamic banking in

Malaysia

snurazani/2011 2

What is Islamic banking?

According to OIC – Organization of the Islamic Conference

define the Islamic Banking as the company which

carries Islamic banking business.

Islamic banking business is banking activities based on

Islamic law (Shariah). It follows the Shariah, called fiqh

muamalat (Islamic rules on transactions).

The rules and practices of fiqh muamalat came from the

Quran and the Sunnah, and other secondary sources of Islamic

law such as opinions collectively agreed among Shariah

scholars (ijma’), analogy (qiyas) and personal reasoning

(ijtihad).

3 snurazani/2011

snurazani/2011 4

GENERAL OBJECTIVE

snurazani/2011 5

To implement the

economic and

financial principles

of Islam in the

banking industry.

To spread

economic

prosperity within

the framework of

Islam.

To create an efficient, progressive

and comprehensive Islamic financial

system that contributes significantly

to the effectiveness and efficiency of

the Malaysian financial sector while

meeting the economic needs of the

nation.

1 2

3

Islamic banking in Malaysia

In Malaysia, the Islamic banking system exists side by

side with the conventional banking system.

In 1993, commercial banks, merchant banks and finance

companies begun to offer Islamic banking products and

services under the Islamic Banking Scheme (IBS banks).

The IBS banks have to separate the funds and activities of

the Islamic banking transactions from the non-Islamic

banking business (conventional banking).

6 snurazani/2011

Islamic banking in Malaysia

Islamic banking in Malaysia began in September

1963 when Perbadanan Wang Simpanan Bakal-Bakal

Haji (PWSBH) was established.

PWSBH was set up as an institution for Muslims to save for

their Hajj (pilgrimage to Mecca) expenses. In 1969, PWSBH

merged with Pejabat Urusan Haji to form Lembaga Urusan

dan Tabung Haji (now known as Lembaga Tabung Haji).

The purpose of the Pilgrims Management and Fund Board ,

to promote and accumulate savings from the Muslims and

coordinate all aspects of pilgrimage activities undertaken by

members.

7 snurazani/2011

ISLAMIC BANKING IN MALAYSIA

The first Islamic bank in Malaysia was established in

1983.

Commercial banks, merchant banks and finance

companies were allowed to offer Islamic banking products

and services under the Islamic Banking Scheme (IBS).

These institutions are required to separate the funds and

activities of Islamic banking transactions from that of the

conventional banking business to ensure that there would

not be any co-mingling of funds.

In 1983, Bank Islam Malaysia Berhad (BIMB) was

established.

Objective: To provide banking facilities and services to

Malaysians in accordance to Islamic Commercial Law 8 snurazani/2011

• You can identify an Islamic bank or an IBS bank from the logo

below:

• The legal basis for the introduction of banking products along

Islamic principles is the Islamic Banking Act 1983, which came

into effect on 7 April 1983.

• to supervise and regulate Islamic banks similar to the case of other

licensed banks.

All banking institutions that provide Islamic banking products and services in banking logo as shown above. Malaysia are required to display the

Islamic

9 snurazani/2011

Malaysia advocates dual banking, in effect there are 3

categories of banking

1. Conventional banking

2. Full-fledged Islamic banks

3. Conventional banks operating Islamic banking windows

under the Islamic banking scheme (IBS)

In relation to Islamic banking, there have been arguments

in support of both full-fledged Islamic banking as well as

Islamic banking windows

ISLAMIC BANKING IN MALAYSIA

Islamic banking windows

Refers to conventional banks that offer Islamic banking

products and services using their existing infrastructure,

including staff and branches

Full-fledged Islamic bank

Refers to a bank dedicated to only offering Islamic banking

products/services

In Malaysia, a number of these banks are set up as a subsidiary

to conventional banks

Operations and management are clearly separated between

the subsidiary Islamic bank and the parent conventional bank

ISLAMIC BANKING IN MALAYSIA

Full-Fledged Islamic Banks in Malaysia

Local 1. Bank Islam Malaysia Berhad

2. Bank Muamalat Malaysia Berhad

3. RHB Islamic Bank Berhad

4. Commerce Tijari Bank Berhad

5. Hong Leong Islamic Bank Berhad

6. Affin Islamic Bank Berhad

7. EONCAP Islamic Bank Berhad

Foreign 1. Kuwait Finance House (Malaysia) Berhad

2. Consortium led by Qatar Islamic Bank

3. Al-Rajhi Banking & Investment Corp

Islamic banking windows in Malaysia

Commercial Banks

1. Alliance Bank Malaysia Berhad

2. AmBank (M) Berhad

3. Citibank Berhad

4. HSBC Bank Malaysia Berhad

5. Malayan Banking Berhad

6. OCBC Bank (Malaysia) Berhad

7. Public Bank Berhad

8. Southern Bank Berhad

9. Standard Chartered Bank Malaysia Berhad

Merchant Banks

1. Affin Merchant Bank Berhad

2. Alliance Merchant Bank Berhad

3. AmMerchant Bank Berhad

4. Commerce International Merchant Bankers Berhad

Islamic banking windows in Malaysia

Discount Houses 1. Abrar Discounts Berhad

2. Amanah Short Deposits Berhad

3. CIMB Discount House Berhad

4. KAF Discounts Berhad

5. Malaysia Discount Berhad

6. Mayban Discount Berhad

Development Financial Institutions (DFI) Offering

Islamic Banking Services

1. Bank Kerjasama Rakyat Malaysia Berhad

2. Bank Simpanan Nasional

3. Bank Pembangunan Malaysia Berhad

4. Bank Pertanian Malaysia

5. Bank Perusahaan Kecil & Sederhana Malaysia Berhad

LIBERALISATION in IBF:

Islamic finance is an ethical and equitable mode of

finance.

Islamic finance encompasses a wide range of products

comparable to mainstream banking products

Government liberalization allows foreign entity to own

local Islamic banks up to 70%, provided the paid up capital

is increased to USD1 bil – this will scale up operations

and expand into global markets

Malaysia:

5 full fledged Islamic banks (2 locals and 3 GCCs)

12 Islamic subsidiary (9 local and 3 foreign)

snurazani/2011 15

GOVERNANCE BODIES

Local

Bank Negara Malaysia

Securities Commission

International level

IFSB - Islamic Financial Services Board (IFSB)

AAOIFI - The Accounting and Auditing

Organisation for Islamic Financial Institutions

snurazani/2011 16

WHY ISLAMIC BANKING?

snurazani/2011 17

No human effort is completely value-free

• Human value are derived from human worldview

• There can be errors, loopholes, injustice

Islamic worldview is different from the Western worldview

• Principals and practices of conventional banking and finance inconsistent with the Islamic Worldview

Islam provide a comprehensive solution, its prescriptions encompasses all aspects of life-shumul

• A specific discipline must be addressed with a larger context – holistic approach – Islamic Worldview

• Islamic banking – “Banks for All”, not limited to Muslim/Malays. Build on competitiveness, innovative financial solutions and excellent service delivery.

18

WHY ISLAMIC BANKING?

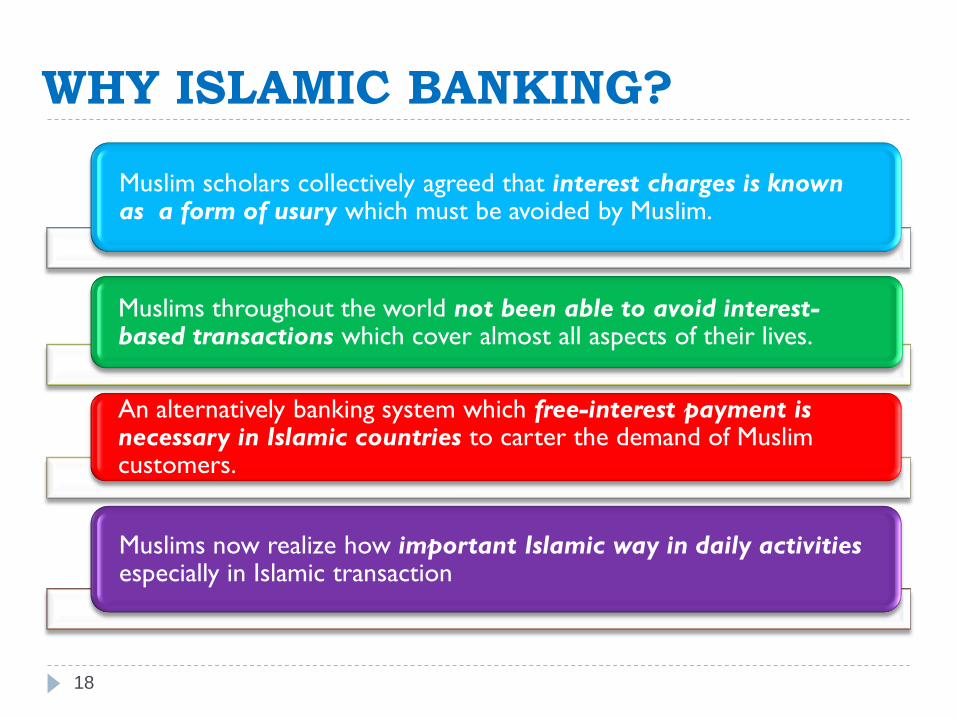

Muslim scholars collectively agreed that interest charges is known as a form of usury which must be avoided by Muslim.

Muslims throughout the world not been able to avoid interest-based transactions which cover almost all aspects of their lives.

An alternatively banking system which free-interest payment is necessary in Islamic countries to carter the demand of Muslim customers.

Muslims now realize how important Islamic way in daily activities especially in Islamic transaction

Shariah Principle prohibitions:

Riba - Interest

Maisir - Gambling

Gharar - Uncertainty

19 snurazani/2011

snurazani/2011 20

Prohibition : RIBA

Riba, interest, or usury is strictly prohibited in Islam.

The literal meaning of the Arabic word riba is increase,

excess, addition or growth

The Shariah meaning ‘premium’ that must be paid by the

borrower to the lender along with the principal amount as a

condition for the loan or for an extension in its maturity.

The Holy Quran has clear instructions regarding business and trading

activities as earnings from trade (Bai) is halal but interest (Riba) based

activities are Haraam.

Banking activities are the part of economic activities and Islam

allows Riba-free banking only.

21 snurazani/2011

Prohibition : RIBA

Riba An-Nasiah:

"That kind of loan where specified repayment

period and an amount in excess of capital is

predetermined." Imam Abu Bakr Hassas Razi

"Every loan that draws profit is one of the forms of

Riba" Sahabi Fazala Bin Obaid

"Every loan that draws more than its actual

amount" Abu Ishaq az Zajjaj

22 snurazani/2011

Prohibition : RIBA

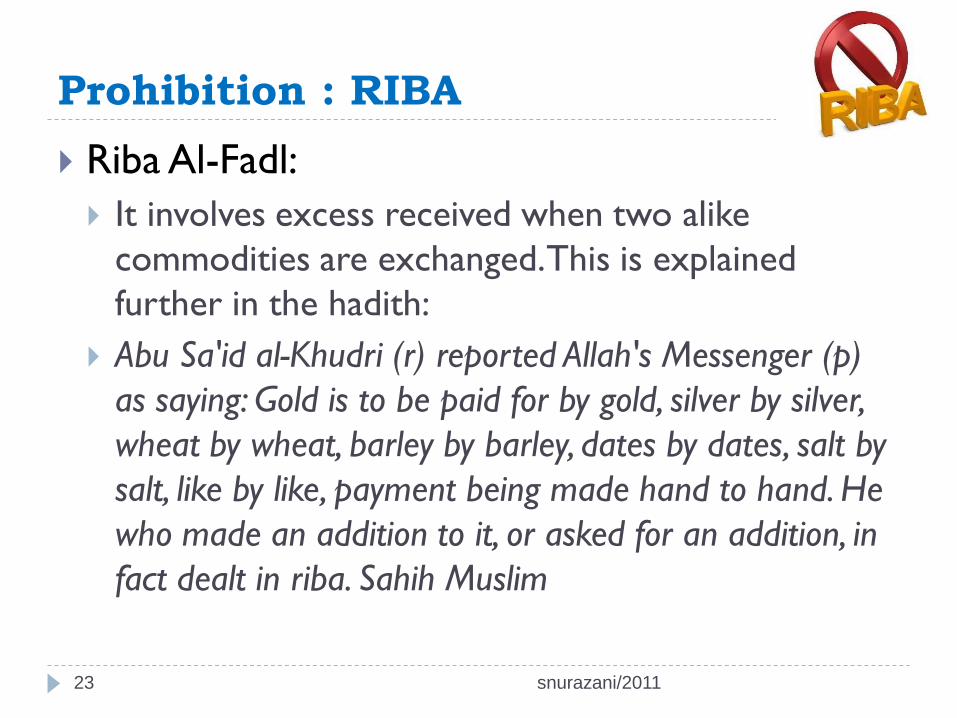

Riba Al-Fadl:

It involves excess received when two alike

commodities are exchanged. This is explained

further in the hadith:

Abu Sa'id al-Khudri (r) reported Allah's Messenger (p)

as saying: Gold is to be paid for by gold, silver by silver,

wheat by wheat, barley by barley, dates by dates, salt by

salt, like by like, payment being made hand to hand. He

who made an addition to it, or asked for an addition, in

fact dealt in riba. Sahih Muslim

23 snurazani/2011

Prohibition : RIBA

Every excess in return of which no reward or equivalent

counter value is paid

A predetermined excess or surplus over and above the loan

received by the creditor conditionally in relation to specified

time period

A forced “increased of value” in “the medium of

exchange” that is loaned.

Quran :

“ they say, trade is like riba, but Allah has permitted trade and

prohibited riba….” 2:275

24 snurazani/2011

Riba and Inflation

Inflation, defined as a continuous rise in prices, can reduce

the value of money. Assume that person X provides a $100

loan to person Y, to be paid back in 12 months time.

However, if prices have increased by 10 per cent during

that time, the value of that $100 will be worth less to the

lender (person X). In such a case, can person X charge an

excess or premium to take into account the loss of value of

money? The Islamic opinion is against the charging of any

premium. Scholars contend that although it is unfortunate

that person X has lost some value, this is not the fault of

person Y (borrower), hence the borrower should not be

burdened with this excess.

snurazani/2011 25

RIBA vs PROFIT

26 snurazani/2011

RATIONALE BEHIND THE PROHIBITION:

1. Element of exploitation in financing consumption

The rich is able to generate more without exerting much

effort

2. Inconsistent with Islam on the perspective of debt

Incurring debt and interest is discouraged

3. Negative effects on “credit society”

Easy availability of credit cultivates a materialistic society

Banks – controller, Customers- enslaved

4. Elements of injustice in financing productive activities

Contract done with unequal counter-value

Injustice to debtor- obligated to pay even no profit or loss

snurazani/2011 27

Prohibition : GHARAR

• Literally: Deceit, fraud, uncertainty, danger, peril, or hazard that

might lead to destruction or loss.

• Technically: Uncertainty and/or ignorance of one/both parties

in a contract over the substance or attributes of the object of

sales, or doubt over its existence and availability at the time of

contract.

• An unknown fact or condition. An element which must be

avoided in Islamic banking dealings as excessive gharar may

make the contract null and void.

– For example:

– Sale of birds in the air

– Sale of fish still in the sea

– Sale of unborn animal

28 snurazani/2011

Prohibition : GHARAR

Rationale for prohibiton of gharar:

Gharar may lead to injustice, exploitation and

enmity among contracting parties.

To ensure full consent and satisfaction of both

parties in a contract Contract will not valid-without full consent.

Contract valid if certainty, full knowledge, full disclosure and

transparency.

29 snurazani/2011

Prohibition : MAISIR

Definition: Easily obtaining something without effort,

acquisition and wealth by chance.

Applies to all activities where a person wins or losses by

mere chance; gambling.

30 snurazani/2011

Prohibition : MAISIR

The main idea behind the prohibition of gambling

(maisir) in Islam is that money should be earned by

way of work and effort example knowledge and

not by mere pure chance.

Playing a lottery is one form of gambling.

31 snurazani/2011

Prohibition : MAISIR

Gambling include any activity where a person pays

something of value for the chance to win a prize. When

someone gambles, it will involve three things, namely: Prize: anything of value: money, physical items, software

Consideration: what the person must pay to enter

Pure chance: something that is opposite to the pure skill. For example, chess

requires pure skill and slot machine require pure chance. It seems apparent

that the chance factor is the dividing line between gambling and non-gambling

functions with a consideration.

For example, risking $10,000 (i.e. the consideration) in a joint-venture (JV)

project is not gambling because the outcome of the JV is based on knowledge

and market skills.

32 snurazani/2011

COMPARISON BETWEEN IB AND CB

Sources: http://www.academicjournals.org/AJBM Afr. J. Bus. Manage. 33 snurazani/2011

ISLAMIC BANKING INSTRUMENTS

Mudharabah (perkongsian untung)

Wadiah (simpanan)

Musyarakah (Usaha sama)

Murabahah (Kos tokok)

Ijarah (Sewaan)

Bai’ Bithaman Ajil (Pembayaran Jualan Tertangguh)

Wakalah (Agensi)

Qardhul Hassan (Pinjaman Ihsan)

Bai’ al Inah (Perjanjian Jual dan Beli Balik)

Hibah (Hadiah)

Assalam

Ar Rahn

Al Hiwalah

Al Dayn

36

CONTINUE…

snurazani/2011 37

ADDITIONAL

INFO

snurazani/2011 38

THE ISLAMIC FINANCIAL SERVICES BOARD (IFSB)

The Islamic Financial Services Board (IFSB) is an

international standard-setting organisation that promotes

and enhances the soundness and stability of the Islamic

financial services industry by issuing global prudential

standards and guiding principles for the industry, broadly

defined to include banking, capital markets and insurance

sectors. The IFSB also conducts research and coordinates

initiatives on industry related issues, as well as organises

roundtables, seminars and conferences for regulators and

industry stakeholders.

snurazani/2011 39

• The Association of Islamic Banking Institutions Malaysia (AIBIM) or Persatuan Institusi-Institusi Perbankan Islam Malaysia was established in 1996 as the Association of Interest Free Banking Institutions Malaysia.

• The objective of AIBIM is to promote the establishment of sound Islamic banking systems and practices and also aims at promoting and representing the interests of members and to render where possible such advice or assistance as may be deemed necessary and expedient to members.

• AIBIM promotes education and training in Islamic banking so as to upgrade Islamic banking expertise in Malaysia and in pursuing the above objectives, AIBIM works in co-operation with other similar associations in the country and elsewhere in the world.

• Website: www.aibim.com

40 snurazani/2011

Islamic Banking and Finance Institute Malaysia (IBFIM),

• mandated by the nation’s financial and capital market master plans to develop human talent for the Islamic financial sector, has made a number of achievements since its formation in 2001.

• The institute, whose stakeholders include Bank Negara Malaysia, the Islamic banks and takaful (Islamic insurance) operators, is a vital training institute in Islamic finance, handling about 30% of the Islamic finance sector manpower annually.

• Its management team led by Dr Adnan Alias as its Managing Director and Chief Executive Officer and is also the Shariah advisor to about 60% of the country’s Shariah-based unit trust funds.

• Besides training, IBFIM provides total solutions to its clients through a comprehensive range of inter-related services, which include business consultancy and Shariah advisory in Islamic banking, takaful, Islamic money and capital markets.

• more info : www.ibfim.com

41 snurazani/2011

Accounting and Auditing Organisation for Islamic Financial Institutions

(AAOIFI) is an independent industry body dedicated to the development of

international standards applicable for Islamic financial institutions. The

Bahrain-based organisation started producing standards as early as 1993.

AAOIFI standards have been developed in consultation with leading Sharia

scholars, with several counties adopting them. Although AAOIFI standards

are not binding on members, over the last few years the organisation has

made significant progress in encouraging the widespread adoption of the

standards.

Countries where AAOIFI standards are either mandatory or recommended

include: Bahrain, Malaysia, UAE, Saudi Arabia, Lebanon, Syria, Sudan and

Jordan.

snurazani/2011 42