Embed Size (px)

Citation preview

1

550.448Financial Engineering and

Structured Products

Week of April 14, 2014Advanced CMO Liability Structures &

Markov Chains for Loan Level, Delinquency-Based Deal Analysis

1.1 1.2

Assignment

Readings Review website Documents on MBS & CMOs RBSGC (8, 10, (11)) and Fabozzi Chapter 24, CMO BoA Agency CMO Structures and SSB CMO CF Structures JPM Agency CMOs (BBG Screens) Fabozzi Chapter 38, Valuation of MBS JPM MBS Primer

R&R Chapter 16

1.3

Assignment

Last day of Class – Wednesday, April 30th

Final Exam Tuesday, May 13, 2pm-5pm Whitehead 304

1.4

Project for PMB

Objective: Explore extensions & variations to PMB Identify PMB opportunity for Trigger or Reserve Fund

(Chapter 7) and Implement Alternatively, Choose one of the VBA automations and

give a presentation on the approach with an example Model Builder 10.2, 10.3 or 10.4, only

First Deliverable due April 7: Project Proposal Content: Identify Group members Identify problem to be addressed

2

1.5

Project for PMB

Presentations due week of April 28 include: Presentation Hardcopy/Summary Content Statement of Situation/Problem/Context Opportunity – “what we are going to do is enhance (implement,

etc.) with the objective of showing (demonstrating, etc.) …” Describe what you did and what you found Show by an example

1.6

Plan for This Week

Advanced CMO Structures Valuation & Relative Value Analysis Investor Types/Preferences The Markov Chain Approach Basic Model Loan Level Analysis Delinquency-Based Approach to Transaction Analysis

Final Take Home Final Presentations

1.7

CMO Structures

Basic Tranche Types Sequential PAC Variations Z-Bonds & Accretion Direction (VADMS) IO/PO

Interest Structuring Floater Inverse Floater

1.8

CMO Structures

Sequential Window for principal return ‘Strip-down” of coupon 4.0x6.0 vs. 6.0x6.0 Tranche Coupon x Collateral Coupon Have same principal payment characteristics 4x6 has longer duration (8.8 vs. 3 OAD) and trades under PAR

Analysis of Sequential Tranches Bifurcate between Short Duration: investors seek yield to fill a short duration need;

must consider impact of extension if yields fall; compare to short agencies, ABS, etc., and,

Long Duration: similar to collateral; compare on OAS and total rate of return

Premium vs. Discount as with callable agency bonds

3

1.9

CMO Structures

Sequential

1.10

CMO Structures

Sequential (and the collateral matters) Current Coupon Collateral

Discount Collateral (longer dur & less neg convexity)

1.11

CMO Structures

PAC Corporate Bond with a sinking fund Scheduled return of principal – “guaranteed” by

companion – described using PAC window 6.5-year average life PAC w/band 110-250

1.12

CMO Structures

PAC When companions are exhausted, PAC bond

becomes a Sequential PAC w/no band left

Cheaper to equivalent Sequential on OAS

4

1.13

CMO Structures

PAC PACs are analyzed relative to sequential classes Market range-bound? Implied vs. Actual Volatility and where headed? Is CF stability cheap via PACs?

Standard analysis is via OAS, yield and total return vs. other MBS or agency

PAC 2 Like a PAC, tighter bands, between PACs and

companions (quasi stable companion) Companion (Support)

1.14

CMO Structures

Companion (Support) Variable CF depends on what is being supported Real value can only be determined w/OAS Usually higher yielding – takes most of the optionality Though structure prevents yield from falling below nominal

level even in a rising environment

1.15

CMO Structures

Accrual or Z Bonds Accrual Phase – interest not paid, added to principal During Accrual Phase – interest can be added to a

chosen tranche(s) to pay down principal Payment Phase – Principal & Interest paid off the

accreted principal: becomes a current pay Used to reduce extension risk in “directed” tranches OAD of Z can be highly variable as it has a long

period as a zero coupon bond – vs. a Treasury zero Jump Z becomes payer if prepays go above a stated

level – a discount bond could become very valuable (usually, in “sticky” form – sticky Jump Z) 1.16

CMO Structures

Accrual or Z Bonds

5

1.17

CMO Structures

Accrual or Z Bonds

Discontinuity in principal payments as Z becomes a payer 1.18

CMO Structures

Accrual or Z Bonds

Contrast to standard sequential from before:

Durations of A, B, C are shorter, less convexity, & w/lower option cost due to extension risk reduction Due to Z accretion: independent of prepayment rates

1.19

CMO Structures

Accretion-Directed (VADM) Z Tranche interest is directed to principal of VADM Very Stable Cash Flows (for VADM) – market willing

to pay-up for VADMs Sequential-only w/Z vs. Sequential, VADM, & Z At slow 100 PSA, no extension for VADM, but sequential

extends – source of principal is Z (even at 0 PSA) Absolute extension protection Some potential to shorten under extreme environments

1.20

CMO Structures

VADM

6

1.21

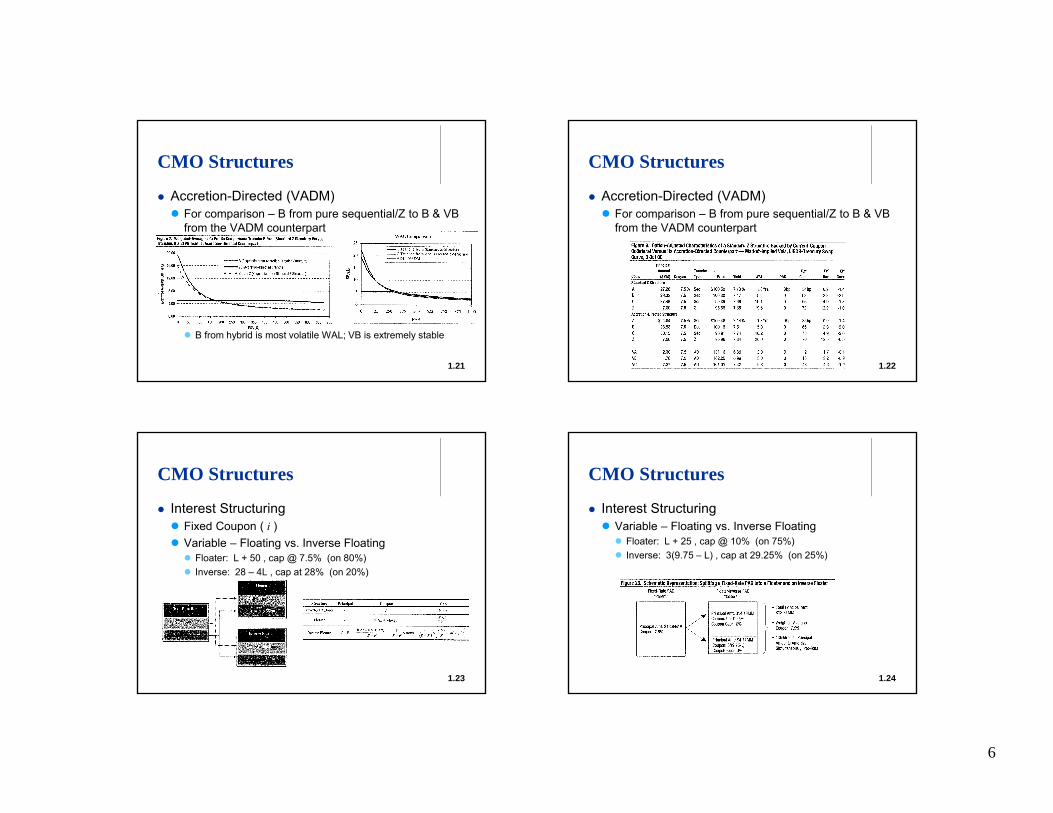

CMO Structures

Accretion-Directed (VADM) For comparison – B from pure sequential/Z to B & VB

from the VADM counterpart

B from hybrid is most volatile WAL; VB is extremely stable

1.22

CMO Structures

Accretion-Directed (VADM) For comparison – B from pure sequential/Z to B & VB

from the VADM counterpart

1.23

CMO Structures

Interest Structuring Fixed Coupon ( i ) Variable – Floating vs. Inverse Floating Floater: L + 50 , cap @ 7.5% (on 80%) Inverse: 28 – 4L , cap at 28% (on 20%)

1.24

CMO Structures

Interest Structuring Variable – Floating vs. Inverse Floating Floater: L + 25 , cap @ 10% (on 75%) Inverse: 3(9.75 – L) , cap at 29.25% (on 25%)

7

1.25

CMO Structures

Interest Structuring

1.26

CMO Structures

Interest Structuring

1.27

CMO Structures

Interest Structuring

1.28

CMO Structures

Interest Structuring Inverse IO

8

1.29

Valuation

Collateral Cash Flow Contingencies – prepays & defaults Prepayment Models Embedded Options

Term Structure Modeling & Interest Rate Models Embedded Option & Volatility

The Present Value of the Contingent Cash Flow Comparing the PV to Market Pricing and Option

Adjusted Spread (OAS)

1.30

Valuation Many Different Types of Spreads (JPM)

Basic: static yield spread over a single point on the curve “I” : spread to Treasury “N” : spread to swaps

Intermediate: zero volatility yield curve spread “Z” : spread to Treasury curve “E” : spread to Libor/swap curve

Advanced OAS : option-adjusted spread LIBOR OAS Treasury OAS M B S

1.31

Valuation Yield analysis in the MBS market (JPM) Static Spread (Yield Spread): standard measure of incremental

return over a single benchmark Treasury Compares MBS to single point on the yield curve, usually to the

interpolated point closest to the Weighted Average Life of the MBS But MBS does not return principal in one lump sum but over many

periods. A better assumption would include multiple data points on the yield curve. Z Spread takes this another step further.

Z Spread (Yield Curve Spread) : discounts each monthly MBS cash flow by the monthly forward rates derived from the current yield curve More accurate for securities that return principal over many periods

as opposed to bullets Still a static measure since it assumes that interest rates and MBS

cash flows remain constant 1.32

Valuation (E: LIBOR/Swap)

9

1.33

Valuation OAS Calculation To incorporate prepayment volatility in the valuation of MBS, we

can calculate a theoretical price for a given OAS1. Hundreds of hypothetical interest rate paths are simulated2. On each interest rate path the prepayment model is used to predict

prepayment speeds and thus, MBS cash flows3. For each path, the present value of the projected cash flows are

calculated using a specified spread, s, which is added to the forward rates

4. Value of MBS = Average value of PV(s) over all simulated interest rate paths = AVGPV(s) where s is OAS

To find OAS given market price:1. Start with an initial estimate for OAS2. Calculate AVGPV(s) adjusting OAS until AVGPV(s) = market price

Investor Types and ABS

Banks Buyers of Pass-Through & CMOs, Agency & non-Agency Like pass-through liquidity, not duration extension risk & mismatch

of liabilities – hence, CMOs or z-supported front sequential Shorter CMOs, 5-years or less Floaters are popular for some banks

Usually, hold to maturity

GSEs (FNMA, FHLMC, FHLBs) Responsible for orderly market for MBS investor Hold mortgages (MBS) vs. loans for liquidity TRR, relative value buyers (buy cheap/sell rich) Some CMOs (PACs); match-off against debt issue 1.34

Investor Types and ABS

Money Managers Measured vs. benchmark indexes MBS indexes usually hold only pass-through MBS CMOs & anything other than pass-through MBS are “out of index” bet Compare on relative value (OAS) to pass-through MBS

Liquidity is important to manage flows and index changes Insurance Companies Buy most types of pass-through MBS/CMOs across curve P&C buy shorter PACs – 2-year sequential Life Ins buy longer w/structure & match long liabilities Variable Annuity Mangers are like money managers

1.35

Investor Types and ABS

Pension Funds Like money managers, but have duration benchmarks Constraints on credit risk from pension law

Long duration CMOs tranches to offset long term liabilities Hedge Funds Retail/Regional CMOs & high yielding derivative tranches: sell to smaller

trust accounts and retail investors – like PAR bonds Non-US Investors (Central Banks in Asia: huge!) Yield pick-up w/o credit give-up or liquidity Vs. Treasury or Agency debt 1.36

10

A Finite State Markov Process for Structured Finance

Consider the n-state Markov process where, x , economic agents (obligors), are allowed to occupy a predefined set of nstates: x(t), t=1,2,…,T; x ϵ [1,2,…,n] The states will correspond to recognized delinquency states

The Markov process may be specified by matrices of conditional, time-dependant transition probabilities

A series of consecutive states ruled by a sequence of transition matrices, P(t), will be referred to as a Markov chain

1.38

111 12

21 22 2

1 2

( )(t) ( )(t) ( ) ( )

( )(t) ( ) ( )

N

N

N N NN

p tp p tp p t p t

P tp p t p t

A Finite State Markov Process for Structured Finance

Types of Markov states The recurrent state, i , is characterized by the two conditions

and includes the current and delinquent states of an obligation The absorbing state, i , is one for which the condition , pii = 1 , holds

and is typical of prepayment and default states of an obligation

In many cases it is necessary to compute the unconditional probability d(t+1) of the Markov process, an n-dimensional vector; these are the probabilities of finding the system in the state i at t , regardless of its state at time t-1 . So and

giving a representation of how the cash flow environment evolves from closing to maturity 1.39

1 and 0ii jip j p

1 2( ) ( ), ( ),..., ( )Tnd t d t d t d t

( 1) ( ) ( ) ( 1) ( 1) ( ) ... (0) (0) (1)... ( )T T T Td t d t P t d t P t P t d P P P t

A Finite State Markov Process for Structured Finance

Stationary Markov Chains For the stationary case, where Pn is called the n-

step transition matrix Markov transition matrices always have unit spectral radius (the norm

of the largest eigenvalue is unity) If there are two or more unit-eigenvalues, the process is called degenerate The alternative, non-degenerate Markov matrices, have distinct eigenvalues

Consider the non-degenerate Markov matrix, as the sequence of matrices converge to a limit where all the rows of Pn become virtually identical; call this limiting matrix P∞ and we label the attainment of this condition equilibrium When a non-degenerate Markov process has been iterated a sufficient number of

times it reaches equilibrium and Irrespective of the initial state we always end up in the limiting case where

1.40

( ) (0)T T nd n d P

n

( ) is the repeated row of Td P

A Finite State Markov Process for Structured Finance

Stationary Markov Chains Consider the non-degenerate Markov matrix, If we would begin with d(0) = d(∞) , we are at a kind of “fixed point” and

Or letting we have that and that v∞ is the unit eigenvector We can practically determine v∞ by taking the first n-1 rows of and

adding a normalizing equation, that the row sum is always one, Solving this nxn non-singular system (via Cramer’s rule) yields this eigenvector

This result applies only to stationary, non-degenerate Markov chains; However, this is the case for the limiting credit rating distribution of a pool of debt

securities from the corresponding rating transition matrix These rating transition matrix suffers from the human side of rating agency

activity – discretion On the other hand, given quantitative, unbiased surveillance of the market this

approach proceeds

1.41

( ) ( )T Td d P ( )d v Tv P v

Tv P v

11

A Finite State Markov Process for Structured Finance

Markov Chains The application of Markov chain population dynamics for a

conservative system (the row sum condition on transition probabilities) demands that we focus on number of obligors in this model We start with obligor transitions, delinquency/default status and then generate

associated cash flows to analyze expected deal performance In building this model, it is the obligor cash flows that establish obligor delinquency

states; and history that build the transition matrices This “delinquency-based approach” (vs. default analysis) has the inevitability of the

measurement-analysis process as its greatest strength

1.42

Synthesizing Markov Chains

So far we have implicitly assumed that Markov transition data were somehow given In practice, issuers with varying degrees of ABS experience will have

to provide them We consider the following situations No data is available Full Data Set is available State inventories alone are available Full set of loan level histories (=> full data set, above)

When No Data is available either that issuer is denied access to securitization markets or a useful proxy is determined – a close competitor or another closely related issuer

1.43

Synthesizing Markov Chains

A Full Data set would include at least twelve months of account wise delinquency transition data: the table

From the number of accounts, Ni,j , with each transition,each month, we can compute the transition probabilities:

With twelve values for each i,j pair we can proceed in two ways Form a 12 monthly-matrix nonstationary Markov process with a 12 month period This works well for seasoned issuers with large portfolios of pronounced stable seasonality Does not work so well for new issuers with unseasoned portfolios

Average the 12 matrices to synthesize a single matrix and superimpose seasonality Use the geometric mean for the probabilities This method leads to smoother results 1.44

ijij

ijj

Np

N

1212

1

avgij ij

i

p p

Synthesizing Markov Chains

There can be distinctions between how these methods compare as the table shows Twelve months of transition probabilities: p1,1 (early stage delinquency transition) & p4,5 (late

stage) ; early has bigger population, late is smaller => higher variance => Can add volatility to the transitions which directly effects required credit enhancement Ignore zero entries Results from data artifacts of smaller portfolios and ambiguous states

1.45

12

Synthesizing Markov Chains

When only State Inventories are available we have a kind of middle ground between the first two cases Instead of a full transition data set (of 12 months) only account inventory of states

are made available in the form of prospectus data on previous deals: table

1.46

Synthesizing Markov Chains

When only State Inventories are available we have a kind of middle ground between the first two cases To round out the full 12-month set of transition probabilities or when the

number of transition probability equations exceeds the number of data points, we need to address an over-determined system

The regularization technique chosen to do this follows: From the transition probabilities, determine an appropriate (objective) functional

to minimize Derive the minimizing Markov transition matrix

To formulate the (over-determined) system, assume the obligor portfolio is static – no account additions and no deletions for reasons other than default or prepayment The account inventory balance for state i can be written as The number of accounts in state i at t equals the number of accounts in i at t-1

adjusted for those that move into or out of state i from t-1 For i=1 and t=1: 1.47

1 1

ti i it t t

S S dS

1 1 2 1 11 0 21 0 1 0 12 0 1 0... ...n

n nS S p S p S p S p S

Synthesizing Markov Chains

When only State Inventories are available we have a kind of middle ground between the first two cases For i=1 and t=1:

Which for all states can be written in matrix format as ( K=PT )

Many entries in K might be set to zero based on “physics” – for example, that the 4th delinquency state will payoff the entire delinquent amount & be current

The regularization to determine K is through linear regression and defining the vector-valued Lagrangian with m data points 1.48

1 1 2 1 11 0 21 0 1 0 12 0 1 0

1 212 1 0 21 0 1 0

1 211 0 21 0 1 0

... ...

(1 ... ) ...

...

nn n

nn n

nn

S S p S p S p S p S

p p S p S p S

p S p S p S

111 21 11 101 1

12 22 2 22 201 1

1 0

1 2

1 10

n

n

n n nnn nn

pp pSS S

p p pSS S

s Ksp p p

S SS

21

1

m

i ii

L s Ks

Synthesizing Markov Chains

When only State Inventories are available we have a kind of middle ground between the first two cases Minimizing L, setting , and proceeding by rows gives

Where uj is the jth row of K ,

So we can get the n solutions for the n rows of K as There can be issues of scale across states – later delinquency states have

relatively low average populations compared to earlier stages – and the elements of the matrix may have value outside [0.1] . There are fixes as the inequality constraints may impose more sophisticated optimizations. Fortunately, “packages” may take care of this.

1.49

0LK

Tj j j j jL q Ru q Ru

1 21 1 11 2

1 22 2 2

1 2

n

nn

nm m m

S S S

S S SR q q q

S S S

1j T T ju R R R q

13

Synthesizing Markov Chains

Bottom line is to “avoid” the continuity method and use transition matrices from reasonable proxy issuers The continuity method can be quite effective, however, just a bit of work to use

properly

1.50

Integrating Delinquencies with Markov Chains

With the credit state transition matrices we have a model to incorporate integrated delinquency-default-prepay analysis in generating cash flows

Procedure proceeds as follows Form the transition matrix representative of servicer’s credit policy,

and with bankruptcy and prepay model parameters

1.51

Integrating Delinquencies with Markov Chains

Procedure proceeds as follows At the end of each collection period, the delinquency

status of an account, l , can be determined from its previous delinquency status For each l, select a uniformly distributed random number and

evaluate state from transition matrix and prior state Establish the account delinquency status and the jth

row of the transition matrix where Define the row-wise cumulative distribution function

Let the new account delinquency status be defined by the condition where

The payment to the trust is set according to the condition of the account as shown next … 1.52

0; 0,1,2,3

jt tj i

iC p j

1( ) | t tl j l jD t j C x C

[0,3]j

0 1 3[ ]t t t tjp p p p 1t

jj

p

1 0tC

Integrating Delinquencies with Markov Chains

……….

1.53

14

Integrating Delinquencies with Markov Chains

Incorporating cumulative defaults amounts to forming the marginal default curve and adjusting the accounts entry into the delinquency process Let be the two leftmost entries in the issuers

base transition matrix Set their new, adjusted values as:

with all others remaining the same This modulation will give rise to the desired cumulative

loss distribution, F(t) SMM and B only apply to current accounts and

therefore apply to the first row1.54

( )( ) F tf t t

000 00

001 01

( ) ( ) ( )

( ) ( ) ( )

p t p t f tp t p t f t

0 000 01( ) and ( )p t p t