Embed Size (px)

Citation preview

Harlingen ConsolidatedIndependent School

District

STUDENT ACTIVITY FUND ACCOUNTING

PROCEDURES MANUAL

Update #15: September 2018-August 2019

By: HCISD Accounting Department

Board of Trustees: 2018-2019

President: Greg Powers

Vice President: Dr. Nolan Perez

Secretary: Eladio Jaimez

Member: Dr. Bobby Muniz

Member: Gerry Fleuriet

Member: Javier Deleon

Member: Dr. Belinda Reiniger

Superintendent’s Senior Team

Dr. Arturo J. Cavazos – Superintendent

Mr. Julio Cavazos – Chief Financial Officer

Dr. Alicia Noyola – Chief Academic Officer

Mr. Shane Strubhart – Director of Public Relations/Community Engagement

Mr. Oscar Tapia - Asst. Superintendent for District Operations

Mrs. Debbie Scogin- Asst. Superintendent for Human Services

Mr. Joseph Villarreal – Asst. Superintendent for Secondary Education

Mrs. Loranda Romero – Asst. Superintendent for Elementary Education

Mrs. Veronica Kortan – Administrator for Organizational Development

Mrs. Dalia M. Garcia – Director of Accountability/Assessment

Mr. Randy Cretors – Director of Athletics

Mr. Ronnie Rios – Director of Music Programs

PREFACE

This manual is designed to provide a set of standardized accounting guidelines and procedures for the administration of the Harlingen Consolidated Independent School District Activity Funds.

Principals, financial secretaries and clerks, sponsors and other personnel involved in the handling of Activity Funds are responsible for following the guidelines and procedures prescribed in this manual.

This manual supersedes all prior publications regulating the administration of Activity Funds.

Please contact the Director of Accounting at 430-9732 for any questions regarding Student Activity.

TABLE OF CONTENTS

SECTION

1 General Information……………………………………………………………….1

2 Basic Records……………………………………………………………….….4

3 Banking Practices and Procedures…………………………………………………………….…6

4 Issuing Receipts…………………………………………………………………..8

5 Deposit of Funds…………………………………………………………….…..….10

6 Returned Checks and Redeposits………………………………………………………….…...12

7 Disbursements……………………………………………………….....13

8 Petty Cash……………………………………………………………………...18

9 Fixed Assets…………………………………………………………………..19

10 Purchasing Policies and Procedures……………………………………………………….…….20

11 Vending Machines…………………………………………………………………21

12 State, Local Sales and Federal Excise Taxes……………………………………………………………………23

13 Investments……………………………………………………………...29

14 Transfer of Funds Between Activity Accounts………………………………………………………………….31

15 Guidelines for Principals on PTA and Booster Club Activities………….............................................................................32

16 Other Related Issues…………………………………………………………….……….33

17 Code of Ethics……………………………………………………………………..36

APPENDIX Activity Fund Forms………………………………….………….38

SECTION 1. GENERAL INFORMATION

1.1 PURPOSE OF ACTIVITY FUNDS

The Activity Fund is designed to account for funds held by a school in a trustee capacity or as an agent for students, club organizations of the campus, teachers and the general administration of the school. These funds are used to promote the general welfare of each school and the educational development and morale of all students. Each campus is responsible for the accounting function for all of their activity funds. Each campus must comply with the guidelines and procedures required by this manual.

Campus Activity Funds- FUND 461

Campus Activity Funds consist of monies raised at a particular campus which are managed by the Principal or other campus administrator. Campus Activity Funds are accounted for by the district as Campus Funds in compliance with the TEA Financial Accountability System Resource Guide. Campus accounts must be spent to promote the general welfare of the school and the educational development of students. Principals may use these funds to supplement their budgeted district funds. Campus funds should NOT be spent to benefit any individual or non-student group.

Student Activity Funds- FUND 865

Student Activity Funds consist of money that is received and held by the school as trustee. Individual student groups raise these funds and that group controls their disbursements as long as the decisions regarding the use of funds do not conflict with Board policy and/or legal regulations or restrictions. Student activity funds are accounted for by the district as Agency Funds in compliance with the TEA Financial Accountability System Resource Guide. The basic purpose for the collection or raising and expending of activity funds must be for the direct benefit of the students or for the general educational curriculum of the District. Fund raising activities shall in general contribute to the educational experience of students and shall not conflict with the instructional program.

1

Student activity money shall be expended to benefit a bona fide student group that contributed to its accumulation. A bona fide student group is one that has been properly approved by the campus principal and consists of elected student officers and a faculty sponsor. A roster of newly elected officers is to be furnished to the principal and the campus financial clerk immediately after being elected to office. Clubs that do not elect officers and/or hold regular activities for an entire school year will be considered inactive and any balances will be transferred to other accounts at the discretion of the principal. Organizations that do not have approved officers will not be allowed to conduct any fund raising activities. Funds derived from the student body as a whole shall be expended in a manner benefiting all students. Student activity funds shall be managed in accordance with sound business practices, including budgetary and accounting procedures.

Campus and Student Activity

Fund Definitions

Campus Activity Funds

Funds are raised locally at the

school or donated to the school.

The funds belong to the campus.

The money must be expended to

benefit the student body and have a

public purpose in the realm of

education. The sponsor or principal

decides upon the use of the funds.

Funds are deposited and disbursed

in 461 fund accounts.

The campus qualifies for two tax-free

sales days per CALENDAR year.

The campus principal must approve

disbursements.

All fundraisers, cash collection and

disbursements are subject to HCISD

2

procedures and regulations.

Upon dissolution of the club/activity,

any remaining funds will be

transferred to the general fund.

Student Activity Funds

Funds are generated by specific

student groups, not by the district or

campus.

Funds are held in trust for the

student group. The money does not

belong to the campus.

The student group must be

recognized by the school and have

elected officers (not participatory

captains). The group must hold

meetings and take minutes. Minutes

must be approved by the group and

signed by the club president.

Funds deposited and disbursed are

included in 865 fund accounts.

The group qualifies for two tax-free

sales days per CALENDAR year.

Disbursements are authorized by

club action. Meeting minutes

authorizing the disbursement must

3

be attached to the request for

payment and retained by the campus

secretary/bookkeeper. The minutes

must be signed by the club President

or secretary.

All fundraisers, cash collection and

disbursements are subject to HCISD

procedures and regulations.

The group should indicate their wish

for the use of any funds left after the

student group disbands.

4

1.2 RESPONSIBILITY FOR ACTIVITY FUNDS

The school principal is responsible for the proper collection, disbursement and control of all activity fund monies. This responsibility includes:

1. Providing for the safekeeping of monies.

2. Proper accounting and administration of fund transactions.

3. Expenditure of funds in compliance with applicable state laws, and local board policy administrative guidelines.

4. Adequate training and supervision of all personnel designated by the principal to administer activity funds

The principal is not responsible for funds collected, disbursed and controlled by parent or booster organizations. These parent and booster organizations’ funds are not to be accounted for in the school’s Activity Fund. See Section 15 for more information on PTA and Booster Clubs.

1.3 AUDIT OF ACTIVITY FUNDS

Activity Funds are audited periodically by the District's Internal Auditor. In addition, an audit is to be performed whenever there is a change in principal or financial clerk. The principal may request in writing a special audit if a situation or event warrants it.

1.4 RETENTION OF RECORDS

5

All records should be kept current and in good order for a period of five years and available for audit at any time.

6

SECTION 2 BASIC RECORDS

2.1 ACTIVITY FUND CASH RECEIPTS

Activity Fund Cash Receipts are the means of accurately recording cash received and provide support for each bank deposit. Only pre-numbered cash receipt books provided by the District are to be used. Other types of receipt books are not authorized.

See attached sample of HCISD cash receipt. Attachment #1.

Please receipt all cash and checks received, including reimbursements from the HCISD Business Office. Checks should be endorsed on the back immediately upon receipt.

2.2 REQUEST FOR CHECK (CHECK REQUEST FORM)

Please use the revised Check Request Form when a Student Activity Fund check needs to be requested. This form is now available on Excel.

See Attachment #2.

2.3 PRE-NUMBERED CHECKS

Pre-numbered checks are used to disburse all funds from the Activity Fund checking account. These checks are obtained directly from the bank as needed (no more than two-year supply at a time). Checks must be printed with the school Activity Fund name. When ordering additional checks, new check numbers should begin with the number succeeding the last check number in the old checkbook.

7

2.4 BANK DEPOSIT SLIPS

Deposit slips, once validated by the bank, serve as a record for the specific date that receipts were credited for the bank account. Deposit slips are obtained from the bank as needed and must be printed with the school's Activity Fund account name.

2.5 FUND RAISING APPLICATION

A Fund Raising Application must be processed before a fund-raising activity is started. This informs the Principal of all fundraising activities occurring for the campus. The Financial Recap found at the bottom of the Fundraising Application should be completed at the end of the fundraiser to report the final sales and expenses. This helps the organization and campus keep track of their fundraisers’ profitability and/or losses.

See Attachment # 13.

2.6 MONTHLY BANK STATEMENTS

The bank statement is the official bank record reflecting all transactions affecting the cash balance on deposit during the preceding month. When properly reconciled, the statement serves as official support for the cash balance indicated in the Activity Fund records. A bank statement should be received and reconciled for all accounts including checking and investments.

The campus’ bank statement should be downloaded by the campus secretary from the online bank website by the 2nd day of every month. Bank

8

reconciliations should be completed and sent to the Business Office by the 15th of each month along with the monthly student activity report and sales tax report. Principals must review, sign and date the bank reconciliation.

PLEASE NOTE if we do NOT receive your reports by the 15 th of each month then our office will go out to your campus to obtain them.

2.7 GENERAL LEDGER – Accounting data entry

The Expenditure Ledger for Activity Funds is maintained on the Campus’s central computer system. All campuses are required to use the District furnished activity software to maintain their student activity ledgers. Daily input is highly recommended. Weekly input is required. All checks, deposits and receipts should be entered regularly to ensure having accurate balances. The Reconciliation report summarizes all transactions of the Activity Fund during the month.

2.8 Preparation of Records

All records must be completed in ink or printed from Excel or Word.

NO EXCEPTIONS.

9

SECTION 3 BANKING PRACTICES AND PROCEDURES

3.1 BANK ACCOUNTS

A. Each school shall have only one checking account which shall be entitled "(Name of School) Activity Fund." This account title must be imprinted on all Activity Fund checks and deposit slips. All monies received will be deposited into this account, and all disbursements will be made by a check drawn on this account.

B. Only activity fund transactions may be directed through the Activity Fund bank account. Transactions controlled by an outside organization such as the PTA or booster club, must be handled through the groups' own bank account.

C. Principals are encouraged to invest surplus funds whenever possible to generate additional funds. Options available include:

(Discuss with Administrator for Business Services before doing this)

1. Savings and/or money market accounts

2. Certificates of deposit

3. District sponsored investment program - (See Section 13 for procedures.)

3.2 CHECK SIGNATURE

A. Each bank account can have up to two (2) authorized check signers, one of which must be the principal.

10

B. Each check must be manually signed.

C. Under no circumstances shall checks be pre-signed. No signatures shall be affixed until the check has been filled out in its entirety.

D. If an authorized check signer changes at any time throughout the year, then all authorized signers must sign again with the new authorized check signer.

3.3 BANK RECONCILIATION

A. One of the most important aspects of the financial secretary’s job is the prompt reconciliation of the Activity Fund bank account. It is the principal's responsibility to see that the financial secretary has adequate time to complete the bank reconciliation on time each month.

B. Upon receipt, the bank statement is reconciled to the checkbook and General Ledger. A copy of the reconciliation should be forwarded to the Business Office by the 15th of each month along with a monthly report and sales tax report.

C. Any stale dated checks over 90 days should have a stop pay and void issued and then removed from the Outstanding Check Register. This helps maintain a cleaner check register.

11

SECTION 4 ISSUING RECEIPTS

4.1 GENERAL RECEIPTING PROCEDURES

A. All cash and check collections must be recorded (in triplicate) by the

person receiving the money. See Attachment #1 (NO EXECPTIONS) (See section 6 for re-deposits):

1. Original (white) to person submitting the money.

2. Posting copy for Accounting (yellow)

3. Permanent copy (pink) retained in the receipt book.

B. The receipt must be completed in its entirety:

1. Date

2. Amount

3. The individual or firm submitting the money. A receipt may not be issued to more than one person.

4. An explanation of the purpose for which the money was received.

5. Write down if monies are for General fund 461, or if it’s an agency, list name.

12

6. The breakdown of total received in cash and in checks (all checks must be endorsed at the time of acceptance).

7. The signature of the person receiving the money. The signature must be manual; signature stamps are forbidden.

C. An actual cash count should be made by the person signing the receipt in the presence of the person turning in the money, whenever possible.

D. Post dated checks cannot be accepted from any source.

E. No Out of State or Temporary checks should be accepted from any source.

F. Under no circumstances shall a cash receipt be altered. If an error occurs, VOID the original receipt and all duplicates and issue a new receipt. The original of the voided receipt must be attached to the copies and retained for audit purposes.

G. Please make sure that all checks accepted include the maker’s phone number and the home address is local in case there is a problem with the check, i.e. NSF.

4.2 RECEIPT OF MONEY BY PERSONS OTHER THAN THE CASH RECEIPT CLERK

A. The cash receipt clerk is responsible for maintaining an adequate supply of Cash Deposit Forms (See Attachment 3) and Cash Sub-Receipts.

This includes ALL cash and checks, including vending machine revenue, and HCISD Business Office reimbursements and refunds.

13

B. A distribution record must be kept of all Cash Sub-Receipts issued to teachers, sponsors and other individuals approved by the principal to collect funds.

C. Money may be collected by an authorized individual other than the Cash Receipt Clerk (teachers, librarian, clerks, etc., but only as approved by the principal) for such items as books, student fees, fund raising activities, etc. In such instances, the individual collecting the monies must account for the monies collected as follows:

1. Cash Deposit Form (Attachment # 3) must be completed with all information provided.

2. If a teacher collects monies from students, then the Tabulation of Monies/Name of Students Form ( Attachment #3a ) should also be prepared and turned in.

3. In some cases, the authorized individual may issue Cash Sub-Receipts to payers for monies collected. The permanent copy (pink) should be stapled to a Cash Deposit Form with only the summary and total information completed.

4. Collections shall be submitted to the Cash Receipt Clerk daily. A deposit report will be required daily or whenever the aggregate amount of such collections exceeds $50.00.

5. The original completed Cash Deposit Form (s) and the attached yellow copy of Cash Sub-Receipts, if used, shall be sent with monies collected to the Cash Receipt Clerk who will count the funds in the presence of the depositor and prepare an Activity Fund Cash Receipt once the deposit total is verified. The Cash Receipt Clerk should also sign the Cash Deposit Form.

14

6. The Cash Receipt Clerk should keep for audit purposes the original Cash Deposit Form on file for 5 years with attached Cash Sub-Receipts, if applicable

7. Individual sponsors/collectors should also keep verified copies of the Cash Deposit Form collected for 5 years for audit purposes.

15

SECTION 5 DEPOSIT OF FUNDS

5.1 GENERAL OPERATING PROCEDURES

A. Deposits must be made daily .

B. Undeposited receipts at the close of the school week (normally Friday except in the case of holidays) should be kept to a minimum.

C. All checks held for deposit shall be endorsed as follows:

For Deposit Only

(Name of School) Activity Fund

Account Number

All checks should be endorsed at the time they are receipted or accepted.

D. All cash receipts supporting cash deposits shall be deposited in numerical sequence.

E. All monies on hand at the end of the school year should be deposited prior to closing the books for the year.

5.2 PROCEDURES FOR PREPARATION OF BANK DEPOSITS

A. A bank deposit slip shall be prepared in a triplicate NCR deposit and shall include the following:

16

1. The date and amount of the deposit

2. The cash receipt number(s) issued that make up the deposit.

3. A listing of each check in the deposit (or a tape) and:

The original copy of the deposit slip is retained by the bank and returned with the monthly bank statement.

The yellow copy is validated by the bank and returned at the time of the deposit.

The pink copy stays in the deposit book.

The Cash Receipt Clerk should verify the validated amount at the time she receives the bank bag from the armored car company.

C. The sum of the amounts of the supporting cash receipts must agree with the amount of the deposit slip.

D. For procedures on handling returned checks, redeposits and deposit corrections, see Section 6 of this manual.

5.3 CASHING OF CHECKS

A. The practice of cashing personal and/or payroll checks is not allowed. The district is not in the banking business. There is no exception to this rule.

17

SECTION 6 RETURNED CHECKS AND REDEPOSITS

6.1 RETURNED CHECKS

Occasionally, a check which had been previously deposited is returned by the bank for a variety of reasons. A check may be returned for improper signature, insufficient funds, or account closed. When a check is returned by the bank, it will be automatically forwarded to the District’s NSF collection company, Envision Payment Solutions.

A. Envision Payment Solutions will handle all collection issues on returned checks. A monthly report will be made available online so you can review which checks have been returned, if any.

B. The collection of funds will be returned to the Bank Account on the 1st or 15th of the month depending on when it was submitted (not collected).

C. All communications with the payer should be made from Envision only. If you receive any calls from a parent, or payer, please refer them to Envision Payment Solutions at 1.877.290.5460.

D. No checks shall be accepted from a party who has not redeemed a previously returned check through Envision. These individuals must be placed on the Do Not Accept Checks List.

E. Retain all bank memorandums and reports from Envision in the school files.

F. If an NSF check is collected by the organization or vendor, such as Cherrydale, they are responsible for the collection process NOT the campus.

18

G. If you need to contact Envision then please use this designated line for us at 1.800.618.1110 and refer to our Client # HC27.

SECTION 7 DISBURSEMENTS

7.1 GENERAL POLICIES

A. All expenditures shall be paid by check from the Activity Fund checking account.

19

B. Income received from a specific group (student and faculty) should be expended for that group. The principal shall ensure that expenditures from these accounts are written for the intended purpose of the group and should not divert for other uses.

C. All checks issued should be supported with proper documentation.

D. No expenditure of funds shall be approved by the principal unless sufficient funds are available in the appropriate activity account. Thus, NO check shall be drawn on any account with a NEGATIVE balance unless sufficient funds are available in the appropriate fund account, or unless funds are anticipated within the week in the appropriate activity fund account.

E. It is imperative that you check your cash balances before issuing a check to ensure you are not overdrawn in that pertinent activity account.

F. Tips and Gratuities are NOT allowed. The only exception to this rule is for a “Service Charge” that is already included on the ticket. An example is a service charge for a table of 6 or more people.

G. Food purchases for staff only will be coded to object code 6497000 under Fund 461. This object code helps us keep track on how much the District spends on food for staff.

a. Food purchases should be limited to in-services, staff meetings and staff appreciation. Limit per person is $10.00. Items NOT allowed are food for baby showers, birthday cakes, or food for any individual. Allowable food purchases should be for the betterment of the campus’ total benefit and morale.

b. Other refreshments for Parents and the Parent Center are to be charged to Function 61, object 6499000.

c. Student snacks and student banquets should be charged to object code 6499000.

H. Reimbursements to staff for items purchased through a personal credit card will be limited to $100 AND MUST be pre-approved by the Principal before making the purchase. Please use Attachment #18 to document this process.

20

7.2 REQUEST FOR CHECK

A. A completed Check Request Form (Attachment #2) shall be the authority for the issuance of an Activity Fund check. It must be completed by the club sponsor prior to issuance of a check. This form is now on Excel and can be saved onto your desktop.

B. A completed Check Request Form shall include:

1. The payee

2. Date

3. Amount

4. A brief description of the reason

5. Fund 461 account number or the agency’s name to be charged

6. Approved signature of the Sponsor

7. Approved signature of club treasurer or student group leader.

8. Check number (when approved)

C. The Check Request Form shall be attached to the supporting documentation and kept on file for audit purposes. Every Check Request Form MUST have proper supporting documentation. It shall include:

1. Vendors' original invoices. Periodic statements are not adequate supporting documentation.

21

2. Sales slip or itemized cash register tapes from teachers or other employees who request reimbursement for items purchased from their own funds. Credit card statements and customer copy of charge slips are not adequate supporting documentation.

3. Other supporting documentation may include letters, announcements and renewal notices when invoices are not provided by the vendor together with a properly completed purchase form (Attachment #5).

D. Request for check forms for advances may be completed without supporting documentation. However, permanent documentation must be attached later in support of the advance payment. Also indicate on the Request for Check form the receipt number, if monies are returned which have not been spent.

E. Any Travel Advances (Hotel and conference fees ONLY) made through Fund 461Student Activity MUST be approved by the CFO prior to the check requisition. If NOT approved, the student activity will NOT be reimbursed for this travel advance. Mileage and meals are NOT allowed to be advanced.

F. All invoices shall be checked to ascertain that sales tax has or has not been properly charged since most purchases made by schools are tax exempt. (See Section 12 on Sales Tax.) If a teacher/sponsor submits a receipt for reimbursement that includes sales tax, deduct sales tax portion before reimbursing. Teachers and sponsors should be aware that they can obtain a sales tax exempt certificate from the principal’s office before they make purchase.

7.3 ISSUANCE OF CHECKS

A. No expenditure of funds shall be approved by the principal unless sufficient funds are available in the appropriate activity account. Thus, no check shall be drawn on any account with a negative balance

22

unless funds are anticipated at a later date in the appropriate activity fund account.

B. All payments shall be made by pre-numbered Activity Fund checks.

C. All Activity Fund checks must be manually signed by an authorized check signer.

D. Payments must always be made to a specific person, company or organization. Checks shall NEVER be made payable to "cash."

E. Under no circumstances shall checks be pre-signed by an authorized check signer.

F. All checks must be completed in ink

F. "VOID" checks shall have the signature area cutoff and stapled to the appropriate check stub

G. Invoices must be paid within 30 days of receipt

7.4 ADVANCE PAYMENTS

A. Advance payment (Attachment #10) may sometimes be requested for necessary expenses to be incurred by clubs or other student groups engaged in out-of-town travel. (Fund 865 only – Fund 461 needs pre-approval from CFO)

23

B. The Check Request Form shall indicate that the check is for a travel advance.

C. Upon completion of the activity, the sponsor shall return any unused funds to the Cash Receipt Clerk for issuance of a receipt. All supporting documentation and the receipt for unused funds shall be attached to the original Check Request form.

D. The settlement of all advances shall be completed no later than fifteen (15) days after the completion of the activity for which the advance was made, except in cases deemed necessary by the principal. In all cases settlement should be attained prior to the end of the school year.

7.5 PAYMENTS TO NON-EMPLOYEES FOR CONTRACTED SERVICES

A. Payments for services performed by individuals not employed by the District may be made directly from the Activity Fund.

B. For employment of non-district personnel as a consultant/instructor the Contract for Consultant Services - Activity Fund (Attachment #4) should be completed prior to the services being rendered. The form should be attached to the Request for Check form. The following approvals are required for the employment of a consultant/instructor based on the total cost:

COST APPROVAL REQUIRED

Less than $1,000 Building Principal

24

$1,000 - $10,000 CFO

Greater than $10,000 Superintendent

NOTE: A background check should be performed prior to contracting an individual AND should be done once a year for each contractor. Submit the signed Contract for Consultant Services to Human Resources/Risk Management to perform background check. Human Resources will then fax the approved form to your office.

C. Campus will insure to have a properly executed W-9 form (See Attachment # 14) for each and every consultant contract. A complete listing of all vendors/contractors denoting paid amounts hired by the campus will be provided to the Business Office prior to Christmas break of each year. This information will be used to prepare IRS 1099 forms by the Business Office. The listing should include name, address, social security number and amount paid.

D. This listing should be sent to the Business Office for issuance of a 1099 form as required by Section 6041 of the Internal Revenue Code prior to December “Christmas” Break of each year.

7.6 MEMBERSHIP FEES

Activity Fund monies (school accounts) may not be used for individual membership dues in a professional organization; however, monies can be used for campus membership/dues as approved by the Directors for Elementary and Secondary Education. School membership dues are allowable expenditures from the Activity Funds.

25

7.7 TRAVEL EXPENSES

Activity Fund monies may be used for travel expenses in accordance with the District’s procedures for district travel. Hotel and conference fees are the only expenses allowed. No advances for meals and/or mileage is allowed. A Travel Request form must be completed in advance and submitted to the CFO for approval . The budget account to be charged should read "Activity Funds."

26

SECTION 8 PETTY CASH

8.1 GENERAL POLICIES

A. NO PETTY CASH WILL BE MAINTAINED AT THE CAMPUSES

27

SECTION 9 FIXED ASSETS

9.1 DEFINITION

Fixed assets are purchased or donated items that are tangible in nature, have a life longer than one year, have a unit value of $5,000.00 or more, and/or may be reasonably identified and controlled through a physical inventory system.

The following items will need to be barcoded because of insurance requirement:

1. A/V Equipment <$500 - - Multi-media projectors, televisions, camcorders, PAs, sound systems, digital cameras, projectors, palm pilots, graphing calculators, DVD players, stereo equipment, TV’s, iPods, MP3 players and any other items deemed by campus principals

See Attachment #15 for “Assets Less than $500.00” worksheet.

2. Furniture >$500 - - Fireproof files & safes, custom made credenzas, shelves

3. Technology-Related Equipment >$500 - - Computers, monitors, printers,scanners, fax machines, digital cameras, software>$500 that becomes

District property4. Misc Equipment >$500 - - ID cameras, band instruments, science

equipment

9.2 PURCHASE FROM ACTIVITY FUNDS

28

Activity fund purchases of fixed assets are required to be added to the campus inventory. The campus must forward the pertinent information to the Business Office (equipment type, brand, model, location, vendor name, serial number, acquired date and cost) (See Attachment # 7, Transfer of Equipment). The Business Office will send the Fixed Asset Clerk to tag the item and record it in the Campus fixed asset subsidiary.

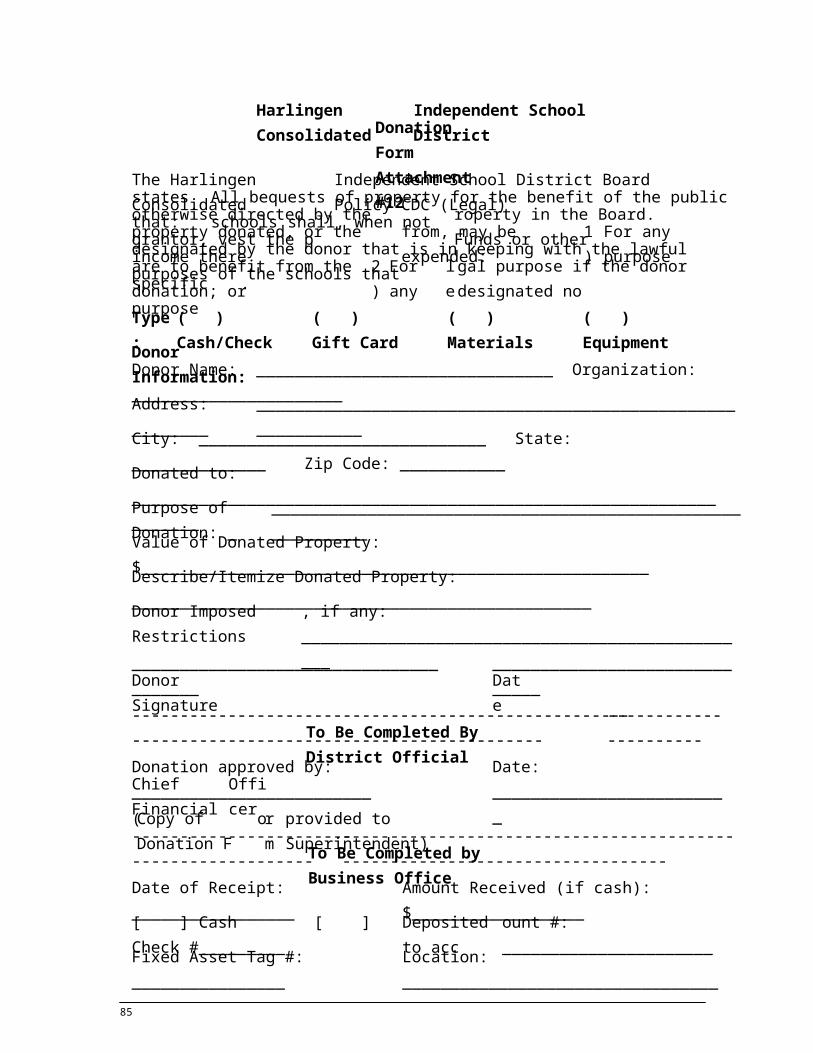

9.3 DONATIONS

A. Donated fixed assets and monetary donations must be submitted to the CFO for approval. Send pertinent information to the Business Office (Attachment # 12 – Donation Form).

B. Donated fixed assets must be added to the campus fixed asset subsidiary. All information pertaining to the donated asset must be sent to the Business Office for tagging and processing into our Fixed Asset System if warranted.

29

SECTION 10 PURCHASING POLICIES AND PROCEDURES

10.1 PURCHASES FROM ACTIVITY FUNDS

A. The school principal is fully responsible for all purchases and commitments requiring the present or future disbursement of Activity Fund monies. Teachers must have a commitment from the school principal before making any purchases in the name of the school.

B. Personal property purchases made with Activity Funds must comply with

Competitive bidding requirements.

10.2 COMPETITIVE BIDDING REQUIREMENTS

The guidelines presented below serve as an introduction to making purchases through the Activity Fund. The Purchasing Manual must be consulted, and those policies and procedures followed when applicable to the purchase(s) being contemplated. Use existing purchasing guidelines established for budgeted accounts when considering any and all purchases.

A. Purchases under $1,000 may be implemented in the most expedient manner available to the principal provided the purchase is from a “vendor of record”. If a vendor of record does not exist for the type of items required, then the principal may proceed.

B. Purchases from $1,000 to $10,000:

Formal Request for Quotations secured from three (3) or more competitors recorded on Quote Tabulation (Attachment #8) filed with other Activity Fund records. If a vendor of record exists it is not necessary to secure three written quotes. Campus must denote on all paperwork the respective bid number. A written explanation by the principal must be attached to the quotes when the lowest quote(s) is not accepted or when the vendor of record is not used.

30

Please continue to ensure this bidding procedure is followed on all purchases ranging from $1,000 to $10,000.

C. Purchases of $10,000 or more must comply with the provisions of the Texas Education Code, Section 44.031, shall be referred to the District Purchasing Department. As soon as the price is determined, the school shall issue a check payable to Harlingen Consolidated Independent School District and forward it to the Business Office. A cash receipt will be transmitted to the Purchasing Department authorizing preparation of a requisition and a purchase order. The merchandise will be delivered and payment made to the vendor from the Accounts Payable Department.

Upon request the HCISD Purchasing Department will assist in quote, bid and contracting processes.

SECTION 11 VENDING MACHINES

11.1 GENERAL POLICY

Revenue from vending machines situated in all areas of the school, whether school-serviced or vendor-serviced, shall be controlled by the school principal and processed through the Activity Fund. The principal must approve the placement of vending machines and all product(s) to be sold.

Revenue from vending machines should be used for educational development for the campus and should NOT be used for items such as birthday cakes, birthday cards, floral arrangements for funerals or get-well gifts.

11.2 SCHOOL-SERVICED VENDING MACHINES

31

A. All transactions involving funds generated by vending machines shall be entered into the Campus Activity Fund Accounts (Fund 461) established for this purpose. For example, receipts and disbursements for soft drinks, other vending machine sales, etc. should be handled through a separate soft drink or vending machine account, such as: Soft Drinks Faculty Lounge, Soft Drinks - Boys Gym, Vending Machine - Students.

B. Profits resulting from vending machine sales may be transferred, at the option of the principal, to accounts related to the supporters/payers from whom the profits were generated or other accounts for student related purposes (refer to Section 14 for procedures).

C. This method of entitling the individual Activity Fund Accounts should relate directly to the location of the machines and the intended purpose of the profits.

D. A perpetual inventory must be maintained on all vending machine items

which should report the beginning inventory, purchases, sales and ending inventory.

11.3 VENDOR-SERVICED MACHINES

A school may contract with a firm whereby the non-beverage vendor agrees to service the machine and collect the money. The school then receives a periodic commission check from the vendor. The school is not required to establish an Activity Fund account for each vending machine operator under this type of arrangement. Vending machines profits (i.e., the commission checks) may be placed directly into the account related to the location of the machine or to the intended purpose of profits from the machine.

32

11.4 GENERAL OPERATING PROCEDURES

A. For elementary schools revenue from vending machines must be collected and receipted weekly or when the amount exceeds $30.00. Money cannot remain in the building over weekends or holidays. For secondary schools, revenue from vending machines must be collected and receipted daily or when the amount collected exceeds $30.00.

B. The principal is responsible for providing the maximum available security for vending machine inventories.

C. Funds shall be disbursed from the individual vending machine account only for the purchase of vending machine supplies, maintenance of the machine (s) and rental, if any, of the machine(s).

D. Any balance justly due for vending machine supplies shall be paid in full upon receipt of each monthly statement.

E. The balance in each vending machine account should be reviewed periodically to determine if a transfer of funds from profits from the account is warranted.

F. Vending machine profits which have been transferred to any related account(s) may be expended for any expenditure generally permissible from that account.

G. Schools must comply with the FMNV guidelines.

H. Secretaries should monitor the Commission checks monthly to ensure that they are reasonable in dollar amount. These should arrive on a

33

monthly basis. Please let the Business Office know if you are not receiving these checks on a timely basis, or if the commission amount appears incorrect.

I. Purchases made from these funds should be used for educational purposes only and NOT for items that will benefit one individual. Items that are not allowed include birthday gifts and cards, flower arrangements for hospital stays or funerals, baby showers, etc.

34

SECTION 12 STATE, LOCAL SALES AND FEDERAL EXCISE TAXES

12.1 TAXABLE STATUS OF PURCHASES

Ruling No. 95-0 from the State Comptroller, effective October 1, 1969 states:

"The sale, lease or rental of tangible property directly to, or for storage, use or other consumption of tangible personal property directly by an educational organization. . . . , which property is necessary to its function as such, and paid for by the organization is exempted from the computation of (state and local sales) taxes."

Provisions under Article 21-023 of the Federal Statutes provide tax exemption to the School District.

In accordance with these rulings:

A. TAX FREE PURCHASES

All items purchased by a public school, school district or non-private school for the schools own use qualify for an exemption from sales tax if the items purchased relate to the educational process. The school, school district or authorized agent should provide the seller with a Texas Sales Tax Exemption Certificate (Attachment #9) to be valid the certificate must state that the merchandise being purchased is for the organization’s own use in providing education, is being made in the name of the organization, and that payment shall be made from the organization’s own funds.

Purchases for their own use by individuals, even though connected with a school or school organization, are NOT exempt from the tax.

35

Examples – cheerleaders purchasing their own uniforms, band members purchasing their own instruments and athletic teams purchasing their own jackets.

B. EXEMPT SCHOOL ITEMS

Public and non-profit private schools and school-related organizations do not need to collect sales tax on the following:

Ad sales – In yearbooks, athletic programs, newspapers and posters.

Admission – Athletic, dances, dance performances, drama and musical performances

Admission – Summer camps, clinics, workshops and project graduation

Admission – Banquet fees

Admission – Bids, prom, homecoming

Admission – Tournament fees, academic competition fees

Cosmetology services – Except for products sold to customers which are deemed taxable

Discount/Entertainment cards and books

Facility rentals for school groups

Food items sold during fundraisers

Whole cakes and pies

Labor- Automotive, upholstery classes (NOTE: Auto parts are taxable)

Magazine subscriptions greater than six

36

months

Parking permits

Services – Car wash, cleaning

C. EXEMPT FOOD SALES

The sales tax is not collected on meals and food products, including candy and soft drinks, served in an elementary or secondary school during the regular school day by a school, student organization or PTA subject to agreement with school authorities.

This exemption from the sales tax applies to guests, employees, or teachers served in a school cafeteria or teacher's lounge during the regular school day.

The sale of food, including candy and soft drinks, is exempt from sales tax when sold by an organization associated with a public or non-profit private elementary or secondary school (4-H clubs, Future Farmers of America, Future Homemakers, etc.) If:

1. The sale is part of a fund-raising drive sponsored by the organization; and

2. All net proceeds from the sale go to the organization for its exclusive use.

D. SCHOOL SPONSORED TRIPS

37

Meals purchased by the school for athletic teams, bands, etc. on authorized school trips are exempt from sales tax if the school contracts for meals. The school must pay for the meals and provide the eating establishment with an exemption certificate.

Individual members of the athletic team, band, etc. may not claim exemption from the sales tax on the meals they purchase while on a school-authorized trip.

An exemption may also be claimed by the school from the Hotel Occupancy Tax if the school contracts and pays for the accommodations and provides the hotel with a completed Hotel Occupancy Tax Exemption Certificate.

Teachers, coaches, etc., MAY NOT claim exemption from sales tax on individual purchases while on school business even though they are reimbursed by the school for expenses.

E. TAXABLE SALES

1. Supplies and Publications

Public and non-profit private schools and school-related organizations must collect the sales tax on the following:

Agenda books Magazines – subscriptions less than six months

Agricultural sales Magazines – when sold individually

Art – supplies and works of art

Musical supplies – recorders and reeds

38

Artistic – CDs, tapes and videos

Parts – career & technology classes (Not to include products used in cosmetology)

Athletic – equipment and uniforms

Parts – upholstery

Auction items sold PE – uniforms, supplies

Automotive – parts and supplies

Pennants

Band – equipment, supplies, patches, badges, uniform sales or rentals

Pictures- school, group (if school is the seller)

Book covers Plants – holiday greenery and poinsettas

Books – workbooks, vocabulary, library, author (if the school is the seller)

Rentals – equipment of any kind

Brochure items Rentals – uniforms of any kind, towels

Calculators Repairs to tangible personal property (i.e. computer repair, house remodeling)

Calendars Rings and other school jewelry

Candles Rummage, yard and garage sales

Car – painting, pin striping Safety supplies

Clothing – school, club, class, spirit

School publications – athletic programs, posters

Computer – supplies, mouse pads

School publications – brochures

39

Cosmetology products sold to customers

School publications – magazines (unless > six month subscription)

Cups – glass, plastic, paper School publications – newsletters, newspapers (generally are not sold though)

Decals School publications – reading books

Directories – student and faculty

School publications – sheet music and hymnals

Drafting – supplies School publications – yearbooks

Family and consumer science – supplies and sewing kits

School store – all items (except food)

Fees – copies, printing, laminating

Science – science kits, boards, supplies

Flowers – roses, carnations, arrangements

Spirit items

Greeting cards Stadium seats

Handicrafts Stationary

Horticulture items Supplies – any sold to students

Hygiene supplies Uniforms – any type to include PE, dance team, drill team, cheerleaders, athletic, club shirts

Identification cards – when they are sold to entire student body (not just the fine for a lost ID card)

Vending – pencils and other non-edible supplies when the school services the machine

Locks – sales and rentals Woodworking crafts – entire

40

sale to include parts and labor

Lumber Yard signs

Merchandise, tangible personal property

2. Sales by Teachers and Students

Teachers and students MUST COLLECT the sales tax on merchandise other than food products they sell.

If the school assumes responsibility for the activity and/or sales, the school is responsible for insuring the tax is paid. The school may purchase items tax free and must collect the tax when the items are sold.

3. Band boosters are required to pay sales tax when purchasing taxable items and to collect sales tax when selling taxable items.

4. There are no Tax Exempt numbers. Exemption certificates DO NOT require numbers.

F. TAX – FREE DAYS

Each school district, each school and each bona fide chapter of each school (student group) is allowed to have 2, one-day tax-free sales each calendar year. During these tax-free sales, the organization may sell any taxable item tax-free.

A bona fide chapter is a group that must be organized for some business or activity other than instruction or a participatory group. Essentially, any

41

student group that is recognized by the school and is organized by electing officers (not just participatory captains), holding meetings, and conducting business are bona fide chapters of the school and each group may have 2 one-day, tax-free sales in a calendar year.

For example:

The school district qualifies for a tax-free day.

The school-wide fundraiser qualifies for a tax-free day.

The Basketball Club qualifies, but the basketball team does not.

The Cheerleader Club qualifies, but not the cheerleader team.

The Debate Club qualifies, but debate teams and classes do not.

The French Club qualifies, but the French classes do not.

The Senior Class qualifies, but not one particular class that has seniors in it.

One-day means 24 consecutive hours; the delivery should be made on a single day. Generally, title passes to the purchaser when the item is given to the purchaser. In the case of pre-ordered and pre-paid sales, title can transfer as soon as the seller (school) receives the order. Therefore, the date the items are delivered by the vendor to the seller is designated as the one-day for the purpose of the tax-free sales. However, persons buying from surplus stock on subsequent dates after the tax-free day owe tax on the items.

When the school or school group receives a commission, the tax-free day sale provisions cannot apply because the sale is the vendor’s sale, not the school’s sale. The school group would collect and remit tax to the vendor, and the vendor would report the sale and remit tax to the Comptroller’s office.

G. TOLL FREE NUMBER & WEBSITE

42

The State Comptroller's office maintains a toll-free tax information number for a quick response to any state tax questions you may have. You can reach the Comptroller's Office from anywhere in Texas by dialing: 1-800-252-5555.

Or you can also inquire on a sales tax issue at http://cpastar2.cpa.state.tx.us/ by typing in your topic or question.

12.2 REMITTANCE OF SALES TAXES

A. All sales tax collected by the school and the corresponding Sales Report shall be remitted by the 15th of each month by all campuses to the Business Office, unless contractual agreements with a vendor stipulate that such taxes should be remitted to the vendor. (Attachment #6)

PLEASE REMEMBER THIS REPORT MUST BE IN BY THE 15TH OF THE MONTH IN ORDER TO SUBMIT TO THE COMPTROLLER’S OFFICE ON TIME.

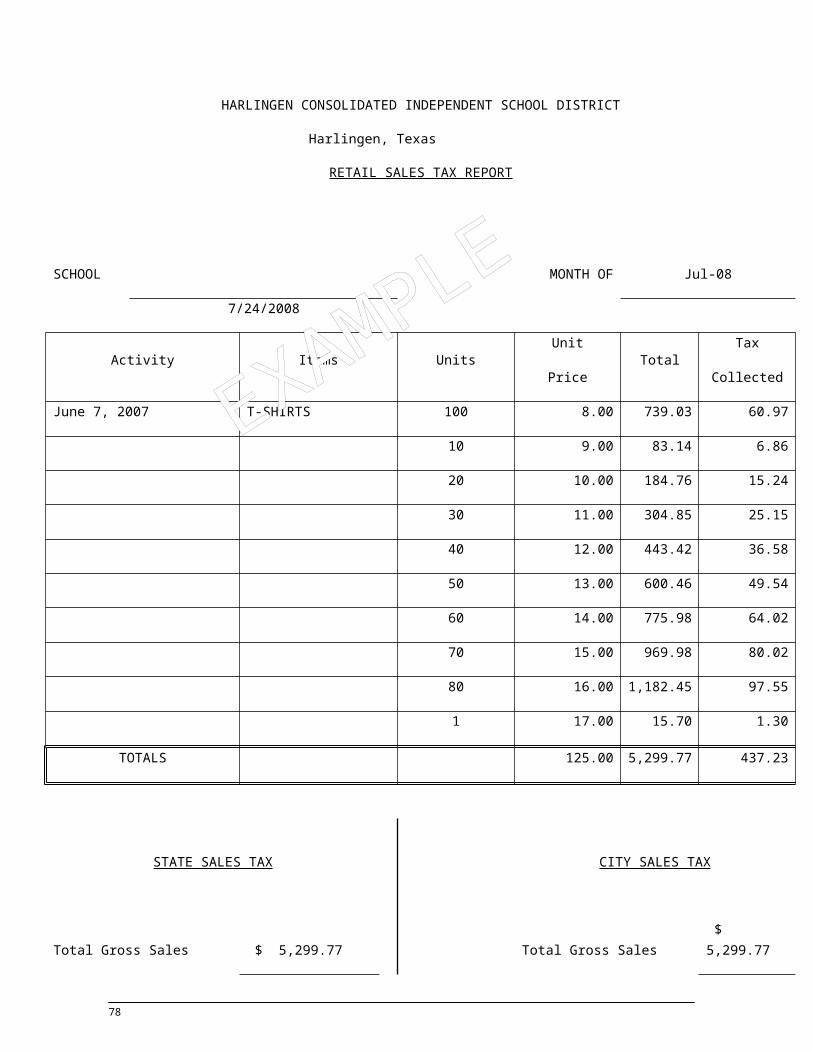

B. Please note that the Sales Tax Report now includes a new column to calculate the amount of tax that should be collected for items sold at a set price, such as a t-shirt sold at $17 in which $15.70 is the actual shirt price and $1.30 is the sales tax collected on this sale.

C. Please note that this also includes Sales Reports with $0 sales. You may fax these to the Business Office at 430.9594

D. If you have any questions as to what is taxable or non-taxable, please call the Internal Auditor or the Accounting Department for assistance.

43

SECTION 13: INVESTMENTS

13.1 GENERAL POLICIES

A. The principal is responsible for managing activity funds to insure that the maximum available cash be invested when appropriate.

B. If the principal wishes to invest some idle monies, the principal must obtain the approval of the Budget Director before entering into any agreements with an investment company.

1. The principal is the authorized signer for all investment accounts. The financial institution shall assign the district's tax payer identification number (74-6001053) and the Activity Fund name to each account.

C. Principals are encouraged to invest funds through the Business Office (see 13.4).

13.2 DEPOSITS AND WITHDRAWALS - OPERATING PROCEDURE

A. All transactions shall be entered into a separate "investment" account in the general ledger. This account shall be a cash account (461X-11XX)

B. Investment purchases or increases to investment accounts may be handled as follows:

1. Request the bank to transfer the amount to be invested from the checking account to the investment account if both accounts are with the same financial institution.

44

OR

2. Prepare a check, as per Section 7, with the financial institution as payee.

C. Investment withdrawals are to be handled as follows:

1. The financial institution may transfer the funds from the investment account to the checking account if both accounts are with the same financial institution.

2. The financial institution shall prepare a check payable to the activity fund. A cash receipt shall be issued and the check deposited, as per Section 4 and 5.

13.3 INVESTMENT INTEREST

Interest income received on investments shall be credited to the general fund of each campus. These monies shall be used for the benefit of all students, since interest were earned with their monies.

13.4 PROCEDURES FOR INVESTMENT OF ACTIVITY FUNDS WITH THE DISTRICT

1. Before investing any monies, consult with the Budget Director.

45

46

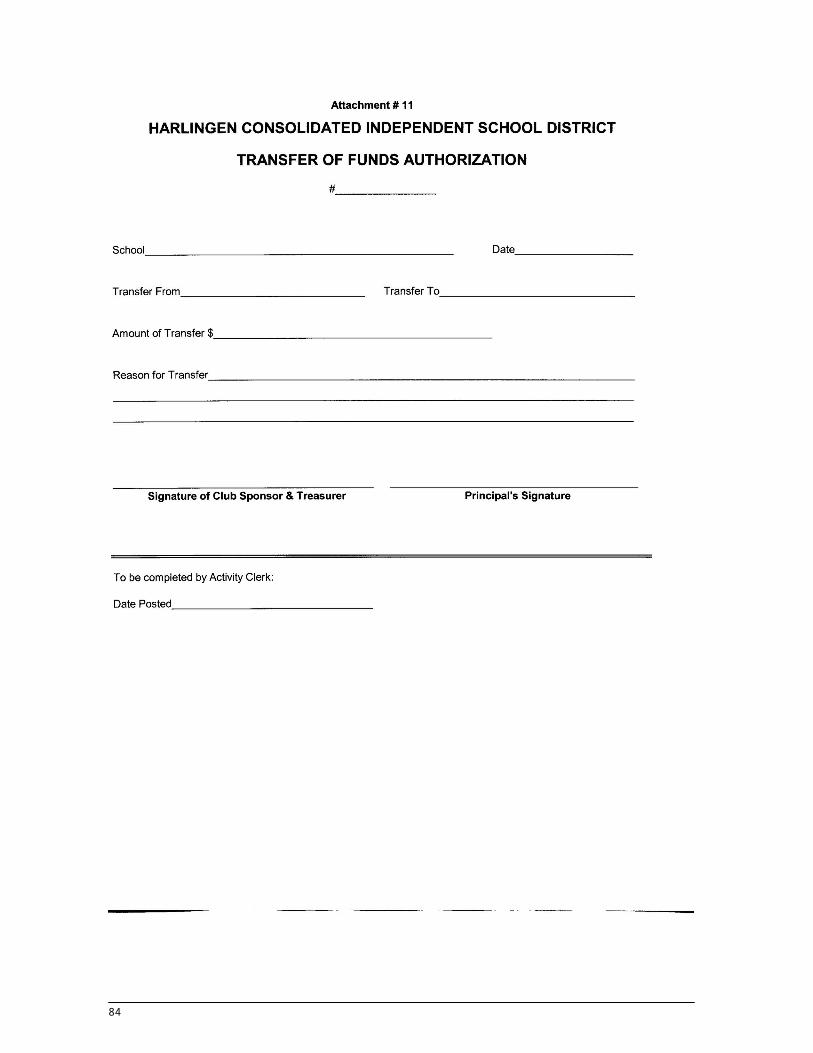

SECTION 14: TRANSFER OF FUNDS BETWEEN ACTIVITY ACCOUNTS

14.1 GENERAL POLICIES

A. Some activity accounts are established for the single purpose of isolating transactions for a specific activity, collection, solicitation, etc., thereby enabling the profitability of the activity to be determined; a Picture Account and Candy Sale Account would be two (2) examples. Net proceeds remaining in such an account must be transferred to the account approved on a Transfer of Funds Authorization Form (Attachment #11). For example, if pictures were taken to provide funds for new library books, then the net proceeds (balance in the Picture Account after all expenses paid to the studio, etc) should be transferred to the Library Account on a Transfer Authorization Form

B Some activity accounts are expected to be revenue producing by the very nature of the accounts. Receipts almost always exceed possible expenditures and the balance in such an account will increase indefinitely unless some disposition is made of the excess revenue; vending machine accounts are an example. As detailed in Section 9.2, vending machine revenue should be transferred, at the option of the principal, to accounts related to the supporters/payers from whom the profits were generated or other account for student related purposes.

C. Occasionally a club will compensate another school organization for goods purchased or services performed. This may occur when a club purchases advertising in the yearbook, newspaper, etc.

D. Likewise, a club may desire to make a voluntary donation or contribution to partially defray the expenses incurred by another club in directing a certain activity. In such cases, the contribution shall be effected by an internal transfer of funds.

47

E. Transfers require the approval in writing of the principal and club sponsors or account custodians when the transfer involves accounts with delegated responsibilities.

14.2 DOCUMENTATION OF TRANSFERS

A. Each transfer shall be initiated by the preparation of Transfer of Funds Authorization Form disclosing both the amount of and the reason for the transfer.

B. The Principal will review and sign off on the Transfer request form. It should then be emailed to the Accounting Clerk or Accountant at the Business Office for them to process. The Accounting Clerk or Accountant will also prepare the necessary journal entries.

C. All copies of the Transfer of Funds Authorization Forms shall be maintained with the School Activity Fund Records.

15.0 GUIDELINES FOR PRINCIPALS ON PTA AND BOOSTER CLUB ACTIVITIES

1. A listing of all officers with address and phone numbers must be kept by campus and kept on file.

2. A copy of the organization’s by-laws must be kept at the office.

3. Please forward a listing of all booster clubs doing business with your school to the business office.

4. A representative of the District must be present at all meetings.

48

5. Copy of all board meeting minutes must be maintained at the principal’s office.

6. A Treasurer’s report must be presented at each regular meeting.

7. Copy of Treasurer’s report along with a copy of the bank statement must be maintained by the campus principal.

8. Campus administrator must approve all fundraising activities that are scheduled by PTA/Booster Club.

9. These records must be maintained at the campus and will be subject to audit by our Internal Auditor.

49

16.0 OTHER RELATED ISSUES

A. Budgets – Campuses must submit their Fund 461 activity fund budget to the Business Office along with their regular local budget in April.

B. Account Coding-Staff should review account codes every year to ensure proper coding to expenditures. Note: Post only income collected from sales into the revenue account R5755. Cost of goods sold should be posted to Function Code 36, object code 6343000.

C. The school district will not reimburse individuals for any sales taxes paid on any purchase. Employees should obtain a sales tax exemption certificate prior to the purchase.

D. Always count monies in presence of person giving you the monies.

E. Remit HELP program monies to Business Office by the 10 th of each month. Please EMAIL a copy of the Monthly Roster/Fee Summary when sending your check. This is needed to reconcile your account.

HELP money must be sent in every month. If a 2nd collection is done after the 10th of the month, please submit that payment before month-end. Your Student Activity HELP balance should be zero at month-end.

F. Please note NO RAFFLES are allowed at campuses.

G. Fundraising activities are not confined to regular school hours but are considered an extension of the school program. When fund-raising activities are in the name of the school, all funds raised become school funds, belonging to the school-sponsored group responsible for raising

50

the money. It is advisable for the school principals to have some sort of annual plan (Calendar) for fund-raising activities. The plan would list the organizations which will engage in fund-raising activities with the intended use of the funds specified.

H. If seeking reimbursement from General Fund it has to be done within 30 days and must include a copy of check and invoices. This Reimbursement will be processed through the Purchasing Department as a requisition to charge your local budget.

I. Each campus must have a listing of each club, printed club officer’s names and their signature(s) and printed club sponsor’s name and their signature(s).

J. Occasionally, we have found that Booster Clubs, PTAs and other associated groups have used the school district’s tax exemption certificate or the employer identification number. By law, these groups must obtain their own tax exemption status and employer identification number independent of the school district.

K. Gift cards are considered compensation by the Internal Revenue Service. If a gift card purchased by Campus/Student Activity funds is provided to an HCISD employee, please provide a listing of these employees, along with their social security numbers, AND the total amount of gift card value. This listing should be sent to Mr. Julio Cavazos, CFO. It should also be included as backup for Reimbursement Payment. If not, Accounts Payable will return it to you until the listing is attached. The total amount of gift cards received will be included on the respective employee’s W-2 form. (Reminder: Gift cards cannot be purchased with HEB or Walmart credit cards.)

L. Please make sure that all library book fines held in your Student Activity Account are submitted to the Business Office at the end of the school year in May. This will leave your library book fines account at zero at the end of the school year.

51

M. Effective August 1, 2011 , any school field trips and/or extracurricular activities requiring a bus driver must provide lunch and/or dinner for the attending bus driver. Therefore, in calculating your meals for these trips a meal must be included for the bus driver along with the sponsor(s) and students.

In requesting meal money, please include the bus driver at the same price rate as the sponsor(s) and students. ($7 per meal for local travel and $8 per meal for travel outside the Valley)

N. Student Activity Recognition Awards Policy:

a. Recognition awards for Teachers, Nurses, Counselors etc. should be de minimus with a value less than $25

b. Gift cards should be $5-10 for teacher recognition awards; they should be instructional related

c. Reimbursement requests from Local funds should be cleared with Purchasing department first; non vendors of record are NOT allowed

d. Gift cards from Student activity and Local funds are allowable but cannot be purchased with an HEB or Walmart credit card (see student activity manual)

O. Crowd Funding

New Fundraiser Option:

Crowdfunding is a new form of electronic fundraising that can be conducted by our teachers here at Harlingen CISD to obtain additional resources for their classrooms. These should be additional resources needed for special classroom projects; and not for normal class supplies since these are already provided by the District.

At this time, there are two different choices 1) GoFundMe and 2) DonorsChoose. This fundraiser is to be used after utilizing all available resources currently available to

52

staff, such as local funds, campus activity funds and PTA resources. The following procedures are required for such a fundraiser:

Prior approval must be obtained from their Campus Principal All transactions must be funneled through their Campus secretary/bookkeeper NO items shall be shipped to the teacher’s house; all items must be received at

the campus through their Campus secretary/bookkeeper Teacher’s email and web address must be affiliated with our District email and

website A project deadline must be set at 45 days or less Ensure donors are aware of any applicable service fees from their online donation Ensure all technology items requested meet our District’s standards and are

approved by our Technology Director Any items received over $5,000 must be identified with our District’s fixed asset

tag All fundraisers must use the Fundraiser Application to document approval and

close-out report

53

17.0 CODE OF ETHICS

As an employee of Harlingen CISD, it is required you comply with our board policy DH – Code of Ethics and Standard Practices. The following is a copy of this board policy. Please make sure to read and understand this policy. If you have any questions on this policy, please feel free to call Mrs. Ledesma, Internal Auditor or Mr. Julio Cavazos, CFO.

CODE OF ETHICS AND STANDARD PRACTICES

FOR TEXAS EDUCATORS

The Texas educator shall comply with standard practices and ethical conduct toward students, professional colleagues, school officials, parents, and members of the community and shall safeguard academic freedom. The Texas educator, in maintaining the dignity of the profession, shall respect and obey the law, demonstrate personal integrity, and exemplify honesty. The Texas educator, in exemplifying ethical relations with colleagues, shall extend just and equitable treatment to all members of the profession. The Texas educator, in accepting a position of public trust, shall measure success by the progress of each student toward realization of his or her potential as an effective citizen. The Texas educator, in fulfilling responsibilities in the community, shall cooperate with parents and others to improve the public schools of the community.

1. Professional Ethical Conduct, Practices, and Performance.

Standard 1.1. The educator shall not knowingly engage in deceptive practices regarding official policies of the school district or educational institution.

Standard 1.2. The educator shall not knowingly misappropriate, divert, or use monies, personnel, property, or equipment committed to his or her charge for personal gain or advantage.

Standard 1.3. The educator shall not submit fraudulent requests for reimbursement, expenses, or pay.

Standard 1.4. The educator shall not use institutional or professional privileges for personal or partisan advantage.

54

Standard 1.5. The educator shall neither accept nor offer gratuities, gifts, or favors that impair professional judgment or to obtain special advantage. This standard shall not restrict the acceptance of gifts or tokens offered and accepted openly from students, parents, or other persons or organizations in recognition or appreciation of service.

Standard 1.6. The educator shall not falsify records, or direct or coerce others to do so.

Standard 1.7. The educator shall comply with state regulations, written local school board policies, and other applicable state and federal laws.

Standard 1.8. The educator shall apply for, accept, offer, or assign a position or a responsibility on the basis of professional qualifications.

2. Ethical Conduct Toward Professional Colleagues.

Standard 2.1. The educator shall not reveal confidential health or personnel information concerning colleagues unless disclosure serves lawful professional purposes or is required by law.

Standard 2.2. The educator shall not harm others by knowingly making false statements about a colleague or the school system.

17.1 Affidavit Disclosing Substantial Conflict of Interest in a Business Entity or in Real Property

In addition to complying with the District’s policy on conflict of interest, see attached policies DBD Legal and DBD Local, the following Affidavit found in this manual as Attachment 17 will be required to be filled out if a school district employee has a substantial interest in a company your campus is using. What is a substantial interest? The Affidavit includes 5 tests that can help you determine if the school district employee holds a substantial amount of interest in the company you are soliciting goods and services. This affidavit must be completed and signed by the school district employee and turned into Mr. Julio Cavazos’ office before any purchasing agreements (P.O. or requisition) is made with the company in question.

55

The school district employee does not have to be at your campus – this applies to any and all school district employees with Harlingen CISD.

56

57

58

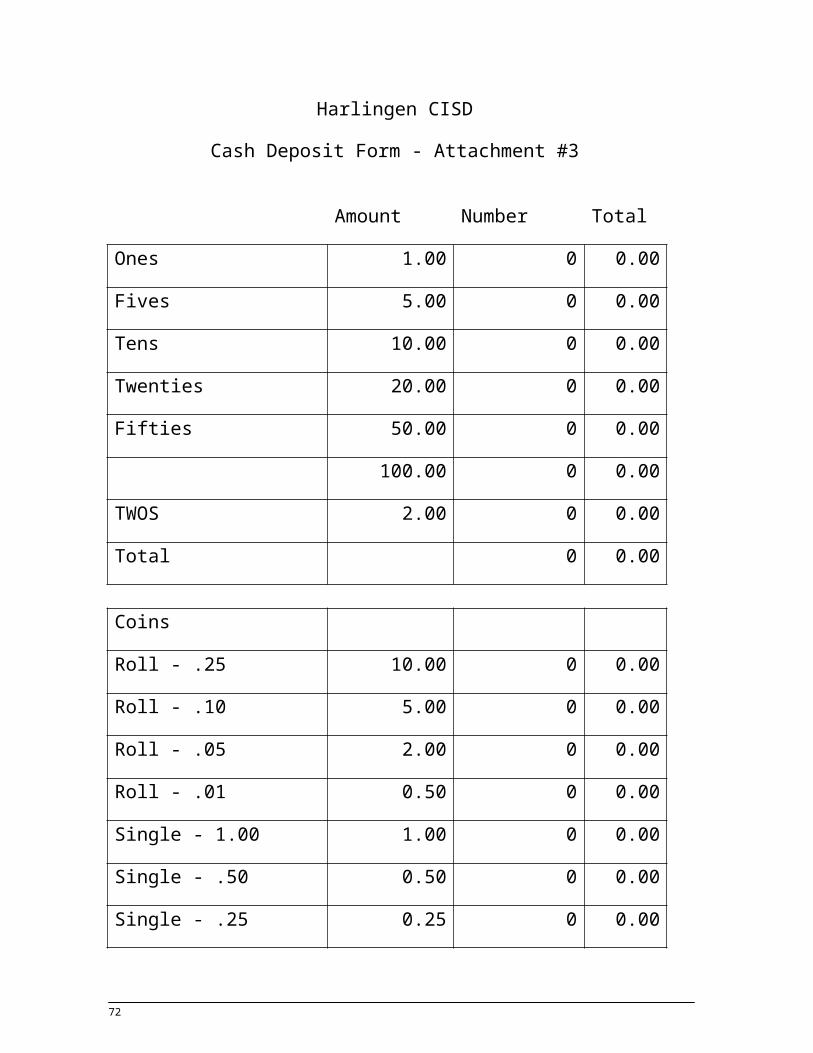

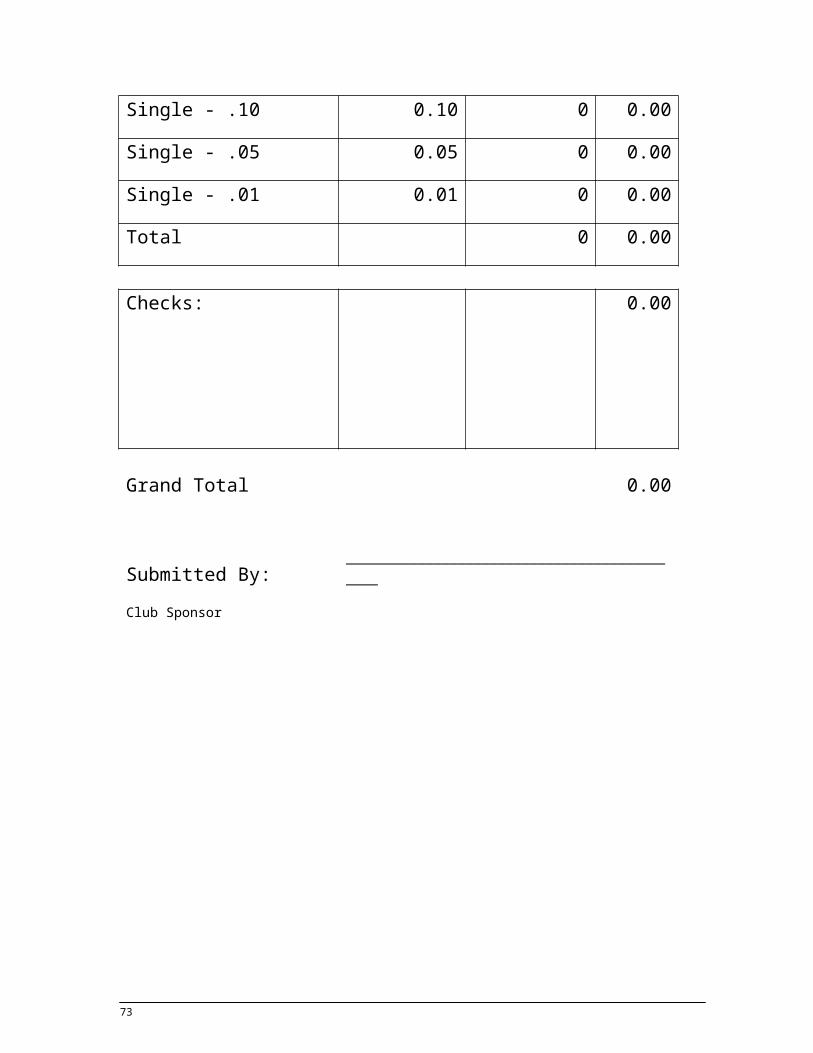

Harlingen CISD

Cash Deposit Form - Attachment #3

Amount Number Total

Ones 1.00 0 0.00

Fives 5.00 0 0.00

Tens 10.00 0 0.00

Twenties 20.00 0 0.00

Fifties 50.00 0 0.00

100.00 0 0.00

TWOS 2.00 0 0.00

Total 0 0.00

Coins

Roll - .25 10.00 0 0.00

Roll - .10 5.00 0 0.00

Roll - .05 2.00 0 0.00

Roll - .01 0.50 0 0.00

Single - 1.00 1.00 0 0.00

Single - .50 0.50 0 0.00

Single - .25 0.25 0 0.00

Single - .10 0.10 0 0.00

Single - .05 0.05 0 0.00

Single - .01 0.01 0 0.00

59

Total 0 0.00

Checks: 0.00

Grand Total 0.00

Submitted By: ____________________________________________

Club Sponsor

60

61

62

63

64

HARLINGEN CONSOLIDATED INDEPENDENT SCHOOL DISTRICT

Harlingen, Texas

RETAIL SALES TAX REPORT

SCHOOL MONTH OF Jul-08

7/24/2008

Activity Items UnitsUnit

TotalTax

Price Collected

June 7, 2007 T-SHIRTS 100 8.00 739.03 60.97

10 9.00 83.14 6.86

20 10.00 184.76 15.24

30 11.00 304.85 25.15

40 12.00 443.42 36.58

50 13.00 600.46 49.54

60 14.00 775.98 64.02

70 15.00 969.98 80.02

80 16.00 1,182.45 97.55

1 17.00 15.70 1.30

TOTALS 125.00 5,299.77 437.23

65

STATE SALES TAX CITY SALES TAX

Total Gross Sales $ 5,299.77 Total Gross Sales $ 5,299.77

Sales Tax .0625 or 6 1/4 % X 0.0625 Sales Tax (2 %) X 0.02

Gross Amount of Tax $ 331.24 Gross Amount of Tax $ 106.00

Discount .005 X Gross Discount .005 X Gross

Amount of Tax X 1.66 Amount of Tax X 0.53

Net Amount of Sales Tax $ 329.58 Net Amount of Sales Tax $ 105.47

(Gross Amount of Tax (Gross Amount of Tax

Less Discount) Less Discount)

make check for: $ 435.04

Limited Sales Tax Permit No.

1-74-6001053-5

OUTLET NUMBER 26

SIGNATURE OF PREPARER

Prepare in duplicate. Original to Business Office: retain duplicate for files

66

67

68

69

70

71

Harlingen Consolidated Independent School District Donation FormAttachment#12

The Harlingen Consolidated Independent School District Board Policy CDC (Legal) states that: All bequests of property for the benefit of the public schools shall, when

not otherwise directed by the grantor, vest the p roperty in the Board. Funds or other property donated, or the income there

from, may be expended: 1) For any purpose designated by the donor that is in keeping with the lawful purposes of the schools that are to benefit from the donation; or 2) For any legal purpose if the donor designated no specific purpose. Type: ( ) Cash/Check ( ) Gift Card ( ) Materials ( ) Equipment Donor Information: Donor Name: _______________________________ Organization: ______________________

Address: _____________________________________________________________________ City: ______________________________ State: ______________ Zip Code: ___________

Donated to: ____________________________________________________________________

Purpose of Donation: ____________________________________________________________ Value of Donated Property: $_____________________________________________________

Describe/Itemize Donated Property: ________________________________________________

Donor Imposed Restrictions, if any: ________________________________________________ _______________________________________ ______________________________ Donor Signature Date -----------------------------------------------------------------------------------------------

----------------------

To Be Completed By District Official

Donation approved by: _________________________ Date: _________________________ Chief Financial Officer (Copy of Donation Form provided to Superintendent) ------------------------------------------

---------------------------------------------------------------------------

To Be Completed by Business Office

Date of Receipt: _________________ Amount Received (if cash): $__________________ [ ] Cash [ ] Check #_________ Deposited to account #: ______________________ Fixed Asset Tag #: ________________ Location: _________________________________

72

73

74

Attachment #15

Campus Name

Assets Less Than $500.00

As of_________________

Date of Name of

Barcode # Serial #Manufacture

r DescriptionPurchas

e Cost Teacher Assigned

75

Total Cost 0

76

77

78

79

80

81

82

83

84

85

Attachment #18

Harlingen CISD

Activity Fund Pre-Authorization FormFor All Personally purchased items to be Reimbursed

Limit is Up to $100

Purpose of Form: Please use this Form to document any pre-authorized purchases with a Sponsor’s personal credit card to be reimbursed at a later time. The Sponsor reimbursement request should be submitted to the Principal within one week.

Date:___________________

Activity Name:_____________________________________

Sponsor Name:____________________________________

Items to be Purchased:___________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________

Total Estimated Cost not to Exceed $100 = ____________________

Exception Applied for $100 Limit: yes_____ Reason:__________________________________________

Reason for Purchase:_______________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________

Items to be Purchased at:________________________________________________________________

Submitted by:__________________________________________________

Pre-Authorization:

86

I have reviewed and approve this Request for the above mentioned items needed from our campus activity funds. The Sponsor will have one week from this form’s date to submit their request for reimbursement.

Principal Signature__________________________________________________________

Date Signed_______________________________________________________________

87