Embed Size (px)

Citation preview

4th Quarter 2013 ResultsFebruary 20th , 2014

Disclaimer

Forward-Looking Statements

This presentation contains forward-looking statements within the meaning of applicablefederal securities laws. Such statements are based upon current expectations thatinvolve risks and uncertainties. Any statements contained herein that are not statementsof historical fact may be deemed to be forward-looking statements. For example, wordssuch as “may,” “will,” “should,” “estimates,” “intends,” and similar expressions areintended to identify forward-looking statements. Actual results and the timing of certainevents may differ significantly from the results discussed or implied in the forward-lookingstatements. Among the factors that might cause or contribute to such a discrepancyinclude, but are not limited to the risk factors described in the Company’s RegistrationStatement filed with the Securities and Exchange Commission, particularly thosedescribing variations on charter rates and their effect on the Company’s revenues, netincome and prof i tabi l i ty as wel l as the value of the Company’s f leet .

Stealthgas Top Handy LPG Owner

Top LPG Owners Ranked by Number of Vessels

Leading owner of Handysize LPG vessels

Maintain a modern fleet. Average age of current LPG fleet 12 years and will come down to 10.2

after the new buildings will be delivered in 2015.

Maintain moderate leverage with net debt to cap around 55-60%.

Maintain a visible revenue stream: 74% voyage days fixed for 2014, 41% for 2015

Maintain cost efficient operations with the lowest breakeven operating cost in the industry

* Including 4 tankers

Fleet Development

Current fleet of 38 LPG vessels, 3 product tankers and 1 aframax tanker

Contracted 17 eco-type LPG vessels

Investments in modern vessels and newbuilding LPG carriers

3

6

3

50

55

60

3

37 37 3740 42 42 42 43 44 46 47

50

56591 1

21

3

25

30

35

40

45

FY

2011

FY

2012

Q1

2013

Q2

2013

Q3

2013

Q4

2013

Q1

2014

Q2

2014

Q3

2014

Q4

2014

Q1

2015

Q2

2015

Q3

2015

Q4

2015

2013 Q4 Income Statement

In US$ 000, except per share amounts

Q4 2012 Q4 2013 12M 2012 12M 2013

Net Revenues $30,586 $32,033 $119,213 $121,482

Voyage Costs 3,855 3,319 12,703 14,302

Running Costs 7,734 10,009 30,592 36,523

Drydocking Costs 22 704 2,067 3,160

Operating Income 9,845 7,681 39,291 29,110

4

Net Income 7,759 5,532 28,958 21,217

Net Income, adjusted

6,740 5,205 24,209 18,668

EBITDA 18,190 16,166 71,516 62,618

EPS 0.38 0.17 1.41 0.75

EPS, adjusted 0.33 0.16 1.18 0.66

Number of Shares, diluted

20,552,568 32,052,568 20,552,568 28,271,746

Balance Sheet

December 31, December 31,

2012 2013

Cash and Cash Equivalents incl. restricted 42,273,000 86,218,517

Current Assets excl. cash 6,649,752 8,040,162

Advances for vessels under construction 19,321,045 70,577,435

Vessels, net 634,634,671 677,022,902

Other assets 1,519,908 3,199,349

Total Assets 713,039,031 850,984,743

5

Total Assets 713,039,031 850,984,743

Current portion of long term debt 35,787,544 72,874,472

Current Liabilities 20,021,170 21,702,603

Long Term Debt 309,564,768 279,994,150

Other Liabilities 5,632,107 3,714,599

Stockholders' Equity 342,033,442 472,594,443

Total Liabilities and Stockholders Equity 713,039,031 850,984,743

2013 Q4 Operating Highlights

Fleet Data Q4 2012 Q4 2013 12M 2012 12M 2013

Average number of vessels in fleet 37 42 36.9 39.4

Period end number of vessels in fleet 37 42 37 42

Total calendar days for fleet 3,404 3,864 13,494 14,399

Total voyage days for fleet 3,401 3,820 13,342 14,196

Fleet utilization 99.90% 98.90% 98.90% 98.60%

Total charter days for fleet 2,817 3,365 11,531 11,896

Total spot market days for fleet 584 455 1,811 2,300

* Assuming no vessels on Bareboat Charter

6

Fleet operational utilization 95.50% 94.90% 95.40% 92.30%

Average Daily Results (in $) Q4 2012 Q4 2013 12M 2012 12M 2013

Time Charter Equivalent – TCE 9,532 9,193 9,699 9,083

Vessel Operating Expenses 3,889 4097 4056 4255

Management Fees 325 338 320 334

General & Administrative Expenses 202 239 210 196

Total Vessel Operating Expenses 4091 4336 4266 4451

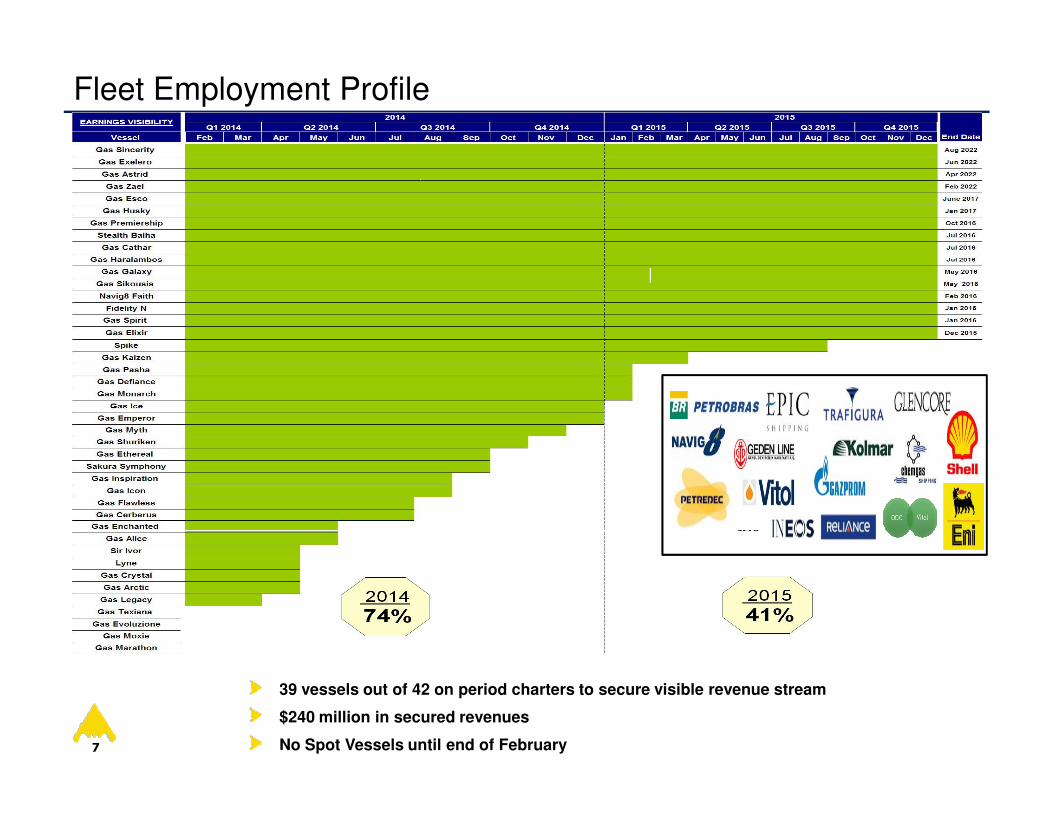

Fleet Employment Profile

7

39 vessels out of 42 on period charters to secure visible revenue stream

$240 million in secured revenues

No Spot Vessels until end of February

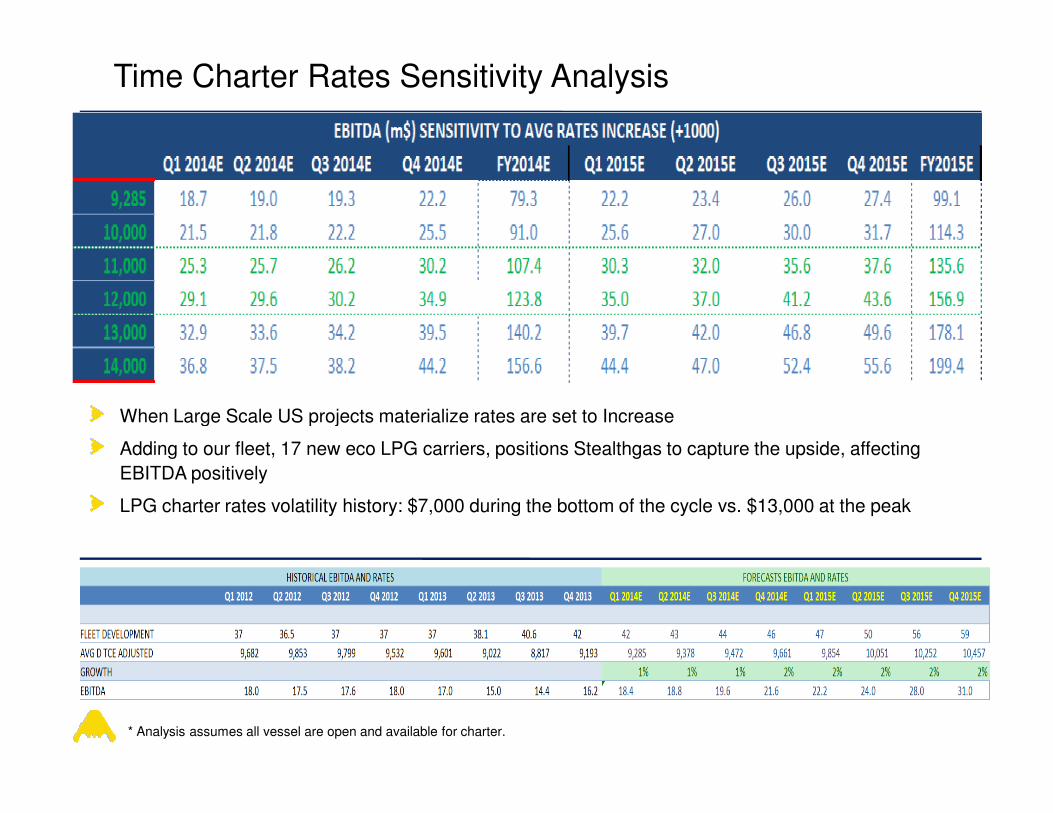

Time Charter Rates Sensitivity Analysis

When Large Scale US projects materialize rates are set to IncreaseWhen Large Scale US projects materialize rates are set to Increase

Adding to our fleet, 17 new eco LPG carriers, positions Stealthgas to capture the upside, affecting

EBITDA positively

LPG charter rates volatility history: $7,000 during the bottom of the cycle vs. $13,000 at the peak

* Analysis assumes all vessel are open and available for charter.

What is LPG? StealthGas Seaborne Trade Model

Natural Gas (LNG) Production (~60%)10% is LPG

Commercial/Residential (52%)

Industrial (9%)

StealthGas hub and spoke model

LPG is the World’s Most Multi-Purpose Energy: accessible, environmentally friendly, available supply, less expensive than other fuel sources

9

Crude Oil Refining (~40%)3% is LPG

Engine Fuel (8%)

Refinery (6%)

Other(2%)

VLGCs transport LPG on longhaul trade vs StealthGas does regional trade and transports LPG/Petchem

Currently ~60% of our ships trade in the Far East, ~30% in Europe and ~10% in the Gulf of Mexico / Caribbean

U.S. Shale Gas - The Game Changer

U.S. Net Exports of LPG 2013 -2017E

• EIA projects that the U.S. will continue to be a net exporter of LPG through 2017, mainly because of continued increases in natural gas and oil production.

10

Incremental demand for LPGs should largely originate in Asia, tied to the buildout of new PDH plants and ethylene plant expansions in China, and overall economic growth in the region

The United States will likely compete with the Middle East for market share to meet the growing LPG import requirements of the Far East.

Global LPG Trade

Large Scale U.S. Export Projects Increase Average Sailing Distances

Source: Clarkson, GHS

Limited LPG Fleet Growth

2

% Undersupplied Market Estimates (cb.m)

11

Our niche LPG shipping segments remains undersupplied

Future deliveries will be absorbed by the LPG Seaborne demand in the market

2

Source: Clarkson Research Services Limited, IHS Global insight, Danish Ship Finance, Jefferies Estimates

Limited Handy LPG Fleet Growth

Orderbook as % of Fleet

2

Age Profile

12

Our niche LPG shipping segments remains smaller than other sector

More than 26% of the 1,000 – 12,999 cbm fleet is 26+ years old

Small orderbook and strong demand dynamics support stable charter rates

2

Source: Banchero Costa, Clarksons Research Services amd Barlcays Research estimates

$0

$500

$1,000

$1,500

$2,000

$2,500

'00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13

5k CBM Pressurized (Trading East) Tanker Earnings Dry Bulk Earnings

LPG Timecharter Rates Historically Less Volatile

($ Thousands / Month)

2

Limited LPG Fleet Growth Has Led to Greater Charter Rate Stability

'00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13

13

LPG time charter rates have remained far more stable than those of peer sectors

LPG time charter rates have remained far more stable than those of peer sectors

The small orderbook and strong demand dynamics support stable charter rates and high utilization

LPG charter rates volatility history: $7,000 during the bottom of the cycle vs $13,000 at the peak

Average all inclusive Breakeven is at ~$6,000

Source: Clarksons Research Services

Q & AQ & A

Appendix – Listed Companies Comparables

Contacts

Weekly LPG Market Report updated every Monday

Comprehensive Investor Relations Information

Visit our Website at: www.stealthgas.com

Company Contact:Stavros PapantonopoulosFinance ManagerStealthGas Inc.011-30-210-6250-001E-mail: [email protected]