Embed Size (px)

Citation preview

Rowing the New Wave Game-changing Rules for Indian Real Estate

June | 2014

On Point

Rowing the New Wave2

Pessimistic attitude of investors • FDIinflowsintherealestateindustrydecreasedsignificantlybyalmost16%

• Declineintheservicesectorgrowthratecauseddecreaseinrealestatedemand

• Pilingrealestateinventorycausedcorrectionofrealtyprices

Difficult times for the economy - start of the global financial crisis (GFC)• CreditcrisisduetosubprimecrisisandglobalbankingleadersweredeclaringbankruptcyintheUnitedStates

• SqueezeofcreditflowinIndia-withdrawalofforeignfundsfromequitymarkets

• GDPgrowthratedroppedto6.7%• Servicesectorgrowthratedroppedto8.2%whileindustrialsectorgrowthratedroppedto5%

eCON

OMY

REal

Est

atE

sentiments improved • Officespaceabsorptionincreased• OfficespacerentincreasedinDelhi,MumbaiandBangalore

• Increaseinresidentialpricescauseddeclineinabsorptionofunits

Optimism continued• GDPgrowthrateincreasedfurtherto9.3%

• Servicesectorreboundedstrongly• Creditsituationimprovedtheindustrialsector,whichgrewto9.5%

eCON

OMY

REal

Est

atE

State of the Economy - Past, Present and Future

Investment sentiments remained low• Investmentinlandsloweddrastically,ascomparedwith2008

• Officeandretailrentsslumped• Residentialsalesimprovedbecauseofcorrectedpricesandlaunchofaffordableprojects

Indian economy showed resilience but not real estate• GDPgrowthrecoveredandwasat8.6%• Capitalmarketsgraduallystrengthened• TheReserveBankofIndia(RBI)raisedinterestratetocontrolrisinginflation

eCON

OMY

REal

Est

atE

Huge optimism in real estate and construction industries• PhenomenalgrowthinFDIflows-FDIintherealestateindustryincreasedthreetimes

• Consistentincreaseintheservicesectorimprovedrealestatedemand

• Availabilityofcapitalandpositivebusinesssentimentsdroveinvestmentsinrealestate

strong growth and high investment sentiments• AnnualaverageGDPgrowthrateinfiveyearswasabove8%

• Servicesectorgrowthratewasat10.8%,andindustrialsectorgrowthratewasat8%

• Strongforeigndirectinvestment(FDI)andforeigninstitutionalinvestment(FII)flows

• Stockmarketwassurging-BSESensexabove20,000points

eCON

OMY

REal

Est

atE

Pre-2008 20092008 2010

Legend:MarketSentiment

FavourableNeutralUnfavourable

Rowing the New Wave 3

sentiments dampened because of credit crunch • FDIflowsinrealestatesloweddown• Officespaceabsorptiondroppedsignificantlyandnationalaveragevacancyroseto17.3%

• Therewasaspurinnewlaunchesintheresidentialsector,andabsorptionrateimproved

Uncertainty in global economy continued to dampen growth• GDPgrowthratedroppedfurtherto5%• Indiafacedheatfromglobalcredit-ratingagencies(CRAs)becauseofhighcurrentaccountdeficit

• TheRBIreducedinterestratestoimproveliquidityandpromotegrowth

• Rupeedepreciateddrasticallyagainstdollar

eCON

OMY

REal

Est

atE Game-changing economic reforms to boost

investments • Economicreformsaretheneedofthehourtobringbacktheeconomyonthegrowthtrack

• Theplantocontrolfoodinflationbyimprovingsupplycangraduallyhelpinsofteninginterestratesandbringingbackliquidityinthemarkettosurgegrowthinthemedium-to-longterm.Thiswillhelptherealestateindustry-whichisstrugglingwithliquiditycrunch-toalargeextent

• Goodsandservicestax(GST)willbeanotherstrongfactorinstreamliningthetaxationprocessandmakingithassle-freefordevelopers

New wave of optimism • Thenewgovernmentbeingformedbyfullmajorityhasbroughtinanewwaveofoptimisminthecountry

• Thestockmarkethaswitnessedanewpeak,andrupeehasstrengthenedagainstdollar

• NewdevelopmentpoliciesthatarelikelytoimproveinvestmentsentimentsinIndiaarebeingplanned

• ImprovingeconomicsentimentsarelikelytoimproveIndia’screditrating,andthisisseentoboostinvestmentsinthecountry

• ThenewgovernmentplanstoincreasetheGDPgrowthratetoabove5%

eCON

OMY

REal

Est

atE

Cautious investment sentiments• FDIinrealestateremainedslow• Officespaceleasingstabilisedandrentalrecoverybegan,althoughstillfarfrompeak

• Residentialabsorptionandlaunchesremainedslow

Indian economy saw the slowest growth • GDPgrowthdroppedfurtherto4.7%• Investmentsentimentsdroppedsignificantly• FDIinflowswereweak• Servicesectorimproved,butindustrialsectorremainedweak

eCON

OMY

REal

Est

atE

Global economy again uncertain because of the Eurozone crisis• SovereigncrisisinEurozoneagaincausedslowdownincapitalflows

• Weakenedcreditsituationaffectedindustrialproduction• GDPgrowthratedroppedsignificantlyto6.2%

eCON

OMY

Recovery continued • Officespaceabsorptionincreased• Increaseinofficerentssloweddown• AbsorptionrateofresidentialunitsimprovedmarginallyRE

al E

stat

E

2011 20132012 2014 - 2017

Rowing the New Wave4

Policies - Setting New Rules to Open New Opportunities for the Real Estate Industry

sEZ act, 2005

UndertheprovisionsoftheSpecialEconomicZones(SEZ)Act,2005,severalzonesinIndiahavebeennotifiedasSEZs.TheSEZshavebeenpromotedbyprovidingtaxholidays-foraplethoraoftaxesincludingincometax,salestax,customsduty,minimumalternatetax(MAT),dividenddistributiontax(DDT)andothers-fordevelopersandoccupiers,withtheobjective

tocreateemployment,promoteexportsanddevelopinfrastructure.TheincentivesledtoseveralSEZsbeingdevelopedacrossIndia.Thisacthasprovidedthemuch-neededimpetustotheITindustryandhasdriventhedevelopmentofITinfrastructureacrossseveralcitiesinIndia.

FDI Policy in Real estate and Relaxations

FDIofupto100%forthefirstcategoryispermittedundertheautomaticrouteintownships,housing,built-upinfrastructureandconstructiondevelopmentprojects(whichwouldinclude,butisnotrestrictedto,housing,commercialpremises,hotels,resorts,hospitals,educationalinstitutions,recreationalfacilitiesandcity-levelandregional-levelinfrastructure).Thepolicies

arebeingrelaxedprogressivelytoattractinterestfrominvestorsandprovidethemwithaprofitableexitstrategyinthefuture.

Inaddition,thegovernmenteasednormsforinvestmentsbyforeigncompaniesactiveinIndiathroughjointventures(JV)in2010.Foreigncompanieswillnolongerhavetoseekano-objectioncertificate(NOC)fromtheirIndianpartnertoinvestinthesectorwheretheJVoperates.Also,theminimumsizeforhousingestatesbuiltwithforeigncapitalwasloweredfrom100to25acrestoattractforeigninvestments.

Concerningretailrealestate,FDIisnowallowedupto100%insingle-brandretailproducts.TheobjectiveofthispolicyhasbeentoenhancethecompetitivenessofIndianenterprisesthroughaccesstoglobaldesigns,betterpracticesandtechnology.Additionally,100%FDIispermittedviatheautomaticrouteincash-and-carrywholesaletrading.Thisisaimedatimprovingthedistributioninfrastructurebetweenmanufacturersandretailers.ThenewgovernmenthaskepttherelaxationofFDIinmultibrandretailcurrentlyonholdtosafeguardtheinterestsofsmalltradersandfarmers.

land acquisition, Rehabilitation and Resettlement act, 2013

TheLandAcquisition,RehabilitationandResettlementActtriedtoensuremaximumprotectionforlandowners,whoareoftenindividualsandattimesnotfullyawareofthefutureconsequencesofdisowningtheirland.ThisActhasthepotentialtounlockallthelandthathasbeenlockedforseveralyearsbecauseoflackofwaysandmeansthatensurefaircompensation.

WhiletheActhadtheobjectiveofbalancingtheinterestsoflandownersandlandacquirers,thefinaldraftofthepolicydidnotreallydeliveronthisfront.TheclausesthatappearintheActnotonlyensurethatlandcostsgoupfortheacquirer,butalsorenderstheacquisitionprocessmorecomplexandtime-consuming.Thisisevidentintheclausespertainingtoobtainingmandatoryconsentof80%oftheowners,futureincrementalgainsfromlandtransactionstobesharedbythelandownersanddifferentresettlementproceduresfordifferentsectionsofthepopulation(suchasscheduledcastes/tribes).

Rowing the New Wave 5

Real estate (Regulation and Development) Bill, 2013

TheRealEstate(RegulationandDevelopment)Bill,2013,whichtheUnionCabinetapprovedafteralonghiatusinJune2013,willbeagame-changerforpropertybuyersandtherealestateindustryasawhole.Thebillislikelytobringinthemuch-neededtransparencyintheindustry.Thiscanencourageinvestmentsintheindustrythroughmechanismssuchas

realestateinvestmenttrusts(REITs)andrealestatemutualfunds(REMFs).

Theaimofthebillistocreatearealestateregulatorthatwillactasawatchdogforthehousingsector,withaviewtoprotecttheinterestofconsumerswhilecreatinganalternativeredressmechanismforanydisputesthatmayarise.However,thebillcurrentlyhasitsownsetofchallengeswaitingforitsstakeholders.Implementationofthisbillislikelytodelaytheprojects,asputtingalltheapprovalsinplacebeforelaunchingaprojecttakeampletimefordevelopers.Thedelay,inturn,willalsoincreasethecostoftheproject.However,effectiveimplementationofthebill,alongwithstreamliningapprovalprocesses,canbearealgame-changerfortheindustry.

Repealing - Urban land Ceiling (ULC) Act, 1976

TheUrbanLandCeiling(ULC)Act,1976gavethestategovernmenttherighttoacquireanddisposeofexcessland(asspecifiedintheAct)fromindividualsandentities,therebyservingthecommongood.However,theActcausedshortsupplyofland,makinglandpricesunaffordable.ManyIndianstateshaverepealedthisActundertheJawaharlalNehruNational

UrbanRenewalMission(JnNURM).However,ifallstatesrepealthisAct,landcanbemadeaffordableandavailablefordevelopment.

Repealing - Rent Control Act

TheRentControlLegislationhasbeeninexistenceforalmostacenturyinIndia.Thecommonintentofeverystateenactingthelegislationistoprotecttenantsfromforcefulevictionandunfairrentalhikes.Inanattempttoprotecttenants,thisActhasinfactcreatedunfavourabletermsforlandlords,therebymakingtheentiremodelofrentalhousingunviableandinefficient.

RepealofthisActcouldunleashalotofredevelopmentactivity,ashasbeenwitnessedinmanymajorcitiesallovertheworld.Thisisnotonlynecessarytomeetthegrowingunmetdemandforhousinginkeylocationsofdenselypopulatedcities;itwouldalsohaveaveryfavourableeffectonemploymentgenerationwithincreasedconstructionactivity.

The Direct Tax Code (DTC) - Deferred

TheGovernmentofIndiahasdeferredtheimplementationoftheDirectTaxCode(DTC)from2014to2015,whichgivesofficeoccupiersmoretimetocapitaliseontheirexpansiondecisionswhilecarefullynegotiatingwithdevelopers.ThedelayintheimplementationoftheDTChasresultedinagoodportionoftheofficespacedemandforITSEZsspillingoverfrom2013

to2014.WiththedemandforITSEZstoremainhealthyinthenext12–18months,weexpectthedevelopersofITSEZstofocusonexecutionandcompletionofprojectsforthedurationtoensureareadysupplytomatchtheimmediatelyupcomingdemand.

BPLR to Base Rate System by RBI in 2010

TheRBIhasintroducedanewregulatorysysteminplaceoftheexistingbenchmarkprimelendingrate(BPLR)forbanksthatoffercommercialloansin2010.Thisnewbaseratesystem,whichsetsafloorforinterestratesthatbanksarenotallowedtolendbelow,isexpectedtoenhancetransparencyandhelpsmallerborrowersinraisingfunds.TheBPLRsystem,which

wasinitiallystartedtobringintransparency,ledwaytogiveloansatsub-BPLRrates.ThiswasnotservingBLPR’soriginalpurpose.Therefore,thereplacementofBPLRbroughtintherequiredtransparency.Althoughbankscanchoosetheirbaserate,theycannotdisburseloansbelowthebaserate.Thissystemwillhelptheborrowersevaluatetheirloancostinabetterway.

Goods and Services Tax to be introduced

TheGoodsandServicesTaxisexpectedtoreplacealltheindirecttaxesleviedbystateandcentralgovernmentinIndia.ThistaxislikelytobeintroducedinIndia.Thistaxisexpectedtolowerthetaxasitisexpectedtobroadenthetaxbase.Thisislikelytomaketaxationhasslefreewhichwillbeanadvantagetodevelopers.

Rowing the New Wave6

TheneedforbetterinfrastructureispressingwithIndia’srapidurbanizationandburgeoningmiddleclass.Some590millionpeople-377millionin2011-willliveincitiesby2030,andcouldaccountfor70percentofIndianGDP,accordingtoaMcKinseyreport.Inaddition,therapidgrowthoftheIndianeconomyinpasthasplacedincreasingstressonphysicalinfrastructurei.e.electricity,railways,roads,ports,irrigation,watersupplyandsanitation,allofwhichsufferfromdeficitintermsofcapacitiesaswellasefficiencies.TheinfrastructuresectorinIndiahasevolvedfrompurelyGovernmentfundedprojectstonewerbusinessmodelsinvolvingpartialorcompleteownershipoftheprivatesector.Meanwhile,intherecentpast,theinfrastructuresectorwasinastateofflux,withthesectorbeinghitbyslowdownintheeconomyandstrainbeingfacedbyvariousinfrastructuredevelopers.Goingahead,thesectorispoisedtobouncebackwithnewopportunities.Butgrowthoftheinfrastructuresectorisdependentonsolvingsomekeychallengesrelatedtoreducingregulatoryuncertainty,developingappropriatefinancingmechanismsandensuringefficientprojectmanagement.Andahighinclusivegrowthforthecountrycouldonlybeachievedifthisinfrastructuredeficitisovercomewithinvestmentopportunitycomesinplacetosupporthighergrowth.

Infrastructure

Delhi Mumbai Investment Corridor (DMIC)

Dedicated Freight Corridor (DFC) sanctioned part

Dedicated Freight Corridor (DFC) proposed part

Delhi NCR

Ludhiana

Kolkata

Hyderabad

Vijayawada

Chennai

Rowing the New Wave 7

Dedicated Freight Corridor (DFC)• EasternCorridor(sanctioned)-Ludhiana-Kolkata,1,805km• WesternCorridor(sanctioned)-1,515km,Mumbai(J.N.Port)toDadri

• ExpectedSpeed:100-120+kmperhour• Providesgreatscopeforlogisticsandwarehousingrealestateatimportantnodes

Delhi Mumbai Investment Corridor (DMIC)• 1,483-kmlength• 200-sq-kmsizedinvestmentregion• Sixmega-investmentregions• INR175billioninvestmentapprovedinfirstphase,whileestimatedtotalpojectcostisINR5.5trillion

• About50%priceappreciationinthelasttwoyears

Infrastructure that has changed the game

• GujaratInternationalFinanceTec-City(GIFT)-aninternationalfinancecityon986acresofland,builtatacostINR700billion

• BusRapidTransitSystem(BRTS)-Whenfullycompletedin2015,itwillcover115kmandwillhavecostINR15billion

• YamunaExpressway-Asix-lane(extendabletoeightlanes),165-km-longexpresswayconnectingGreaterNoidawithAgra,builtatacostofINR130billion

• DelhiMetro-AmetrosystemservingDelhi,Gurgaon,NoidaandGhaziabadwithanetworkofsixlines,plusanAirportExpressline,withatotallengthof190km

• KolkataMetro-Thenetworkconsistsofoneoperationalline(NorthSouthMetro)andthreeunderconstruction,withfurtherlinesinvariousstagesofplanning

• KolkataBusRapidTransitSystem-BeginningatUltadanga,theroutewillcover15.5kmalongtheEMBypass

• ChennaiMetroRail-Underconstruction,theprojectconsistsoftwocorridorscoveringalengthof87km

• OuterRingRoad-A62-km-longcorridordevelopedalongtheperipheryoftheChennaiMetropolitanArea

• PuneMetro-Theproposed82-km-longmetrorailprojectisexpectedtocommencein2018.• PuneRingRoad-ThetenderfortheDPRoftheproposed170-kmRingRoadthatwillconnectthefringeareasofPuneandPimpriChinchwadislikelytobeissuedinJune

• NammaMetro-PhaseIcoversadistanceof42km,whilePhaseIIcovers115km• TheBangalore-MysoreInfrastructureCorridor(BMIC)-AlsocalledNICERoadwithalengthof111km,ithasbeenproposedthatthecorridorisupgradedfromfourtosixlanesbetweenBangaloreandMysore

• MumbaiMetro-FirstphasefromVersovatoGhatkoparwillbeoperationalbyend-2014.Theentireprojectwillhavealengthof146km,builtatacostofINR360billion

• MumbaiMonorail-Thecompletenetworkof135kmandeightlineswillcostINR202billion• EasternFreeway-The16.8-km-longhighwaybetweenSouthMumbaiandGhatkoparwascompletedin2013atacostofINR15billion

• HyderabadMetroRail-PhaseIcoversadistanceof71km,whilePhaseIIcovers80km;thethreephaseswillcostINR170billion

• RegionalRingRoad-A290-kmringroadconnectingthedistrictsaroundthecityandlinkingnationalhighwaysNH4,NH7,NH9andNH202

Delhi Mumbai Investment Corridor (DMIC)

Dedicated Freight Corridor (DFC) sanctioned part

Dedicated Freight Corridor (DFC) proposed part

Rowing the New Wave8

Impact of Infrastructure Development on Real Estate

Infrastructuredevelopmentshavedirectimpactonpropertyvalues.Especiallytransportinfrastructurepositioninghasseriousimpactsonpeople,communitiesandpropertyvalues.Residentialandcommercialpropertieslocatedclosetotransportationinfrastructuretendtocommandapremium-ithasbeencommonforrealestatepricestoappreciateintandemwiththedevelopmentofinfrastructure.Thegeneralrulebeing-thebettertheinfrastructure,thebetterthepropertyvalue.ManycitiesinIndiahavewitnessedthebenefitsofinfrastructureprojectdevelopmentssuchasmetrorailways,peripheralringroads,andbusrapidtransitsystems(BRTS)onthebackofthefuturegrowthpotentialoftheseprojects.Theygenerallywitnesssuddeninfluxofrealestatedevelopmentandriseinpropertyvaluesaroundtheinfrastructureproject.Inaddition,priceincreasesduringtheyearswhenaninfrastructureisbeingbuilthavebeencatalyticallyfunctionaltominimisegapsbetweenpricesontheperipheryandinthecentreofthecity.

Ifwetakeacloserlook,upcominginfrastructureprojectsgenerally

Case Study: Mumbai Metro Railway

MumbaiwitnessedthecommissioningoftheVersova-Andheri-Ghatkopar(VAG)corridoroftheMumbaiMetroinJune2014.ThisPublicPrivatePartnershipinitiativeoftheMumbaiMetropolitanRegionDevelopmentAuthorityhasequityparticipationfromRelianceInfrastructureandVeoliaTransport.Themetroconnectivityreducestraveltimeto21minutesfromthecurrent90minutesbetweenVersovaandGhatkoparwithimprovedEast-Westconnectivity.Theareasthatbenefitfromthemetroconnectivityhavealreadyseenapriceappreciationof400%overthepasteightyears,andthistrendissettocontinuewiththelaunchofthelink.

leadtothedevelopmentofnewresidentialhubs.And,iflandpricesinsuchlocationsarenothighthenitcreatesimmensepotentialforaffordableandbudgethousingwhicheventuallygetscrowdedandmakeswayforhighpricedresidentialunits.Normally,landacquisitionandconsolidationarebasedonpreliminarynewsregardinginfrastructureprojects.However,commercialprojectsshowaslightlyskewedbehaviour.Theytrulygathermomentumwheninfrastructureprojectshavemovedfromthedrawingboardtotheexecutionphase.

Meanwhile,thecompletionoflargeinfrastructureprojects,suchastheDMICandDFC,willbeexpeditedinthecomingyears.This,inturn,wouldmeanthedevelopmentofmanynewcitiesacrossthebeltoftheseprojects.Thesemassiveon-goinginfrastructureprojectswillalsoleadtoahugedemandforwarehousespace,therebygivingasignificantboosttowarehousing-relatedandlogistics-relatedrealestatedemand.OncetheDMICandDFCarecompleted,thegrowthofrealestateinIndia’shinterlandsthatwillbeconnectedbythesecorridorswillbeexponential.

Rowing the New Wave 9

On the cards: Proposed Infrastructure

Proposed Indian experiment of ‘Smart Cities’

Thecreationof100‘smartcities’islikelytobeagame-changerforthenextgenerationofIndianinfrastructuredevelopment.Thegeneralcharacteristicsofthese‘smartcities’include:

• Utilisationofnetworkedinfrastructure,includingbusiness,housing,leisureandlifestyleservices,aswellasinformationandcommunicationinfrastructure(ICT)toimproveeconomicandpoliticalefficiencyenablesocial,culturalandurbandevelopment

• Applicationofstrategytoincreaselocalprosperityandcompetitiveness

• Socialinclusionofvariousurbanresidentsinpublicservicesandemphasisoncitizenparticipationinco-designingwhilefocusingonsocial,environmentalandeconomicsustainability

Railways

OneoftheprominentschemesinthissectorcouldbethelaunchoftheDiamondQuadrilateralproject,ahigh-speedtrainnetwork(bullettrain).Othersincludetouristrailsandresearchanddevelopment(R&D)centresforindigenousrailways

airports

Modernisationofexistingandoperationalairportsaswellasbuildingnewones,especiallythoseconnectingsmallertownsandalltourismcircuits,arelikelytotakeplace

Ports and Waterways

Modernisationofexistingportsanddevelopmentofnewones,andthenlinkingthemtogether,aswellasdevelopmentofwaterwaysforpassengerandcargotransportarealsoonthecards

Roads and Transport System

Apublictransportsystemthatreducesdependenceonpersonalvehiclesandcost,timetotravelandecologicalcostcouldbethefuture,alongwiththeconstructionandexpansionofnewhighways

Rowing the New Wave10

Capital flows - The Vital Fluid of Indian Real Estate

Investing in Indian Real Estate

Investinginrealestatehasbecomeincreasinglypopularoverthelastfewdecadesandacommoninvestmentvehicle.Realestateisconsideredtobeoneofthesoundestinvestmentoptionsinmaturedcountries,andnotwithoutreason.Subsequently,inIndiancontext,therealestatemarkethasplentyofopportunitiesformakingbiggainsamidthechangingsocioeconomicconditionsandfluctuatinggoldandstockmarketvalues.Althoughmanycomplexitiessurroundedthebuyingandowningofrealestateinthecountryand2013wasmiredinchallengessuchassubduedsales,pilesofunsoldinventoriesandbuildersfacingcashcrunchwiththechangeingovernment,Indiaislikelytowitnessaninfrastructuralboom,providingrealestatewithanadvantageousedgeasaninvestmentvehicle.Thenewpoliticalenvironmentislikelytomakepolicyreformswhichwillbringtheeconomybacktothegrowthtrack,therebyimprovingtheinvestmentsentimentsinrealestateintheshort-to-mediumterm.

However,itisimportanttomentionthatcautionshouldbeexercisedatallcostwhileinvestinginrealestate,consideringmanyfacetsincludingpossiblecapitalappreciationduringtheprojectlifecycleandstudyingthereputationofthedevelopersfordeliverywithinstipulatedtimeaswellaslegalissuesrelatedtotheproject.

Positive aspects of Real Estate Investment

MORe CHOICe ThereisawidearrayofchoicesforinvestinginrealestateacrossIndia.Itcanbeland,commercial/residentialspaceoranythingthat

generatesinterest.

LeSS RISk INvOLveD Investorsarelesslikelytoendupwithalossbyinvestinginrealestate.Realestateisrelativelyfreefromdrasticfluctuationsandrarelylosesvalue.Ontheotherhand,factorssuchassurroundingdevelopments,i.e.,anewroad,canincreasethevalueofreal

estatemanytimes.

A SOLID INveSTMeNT Thebestthingaboutinvestinginrealestateisthatthereismore

appreciationwiththepassageoftime.

PROFITABILITY Investmentchurnsupprofitinmanywaysasreturns,including

appreciation,resaleandrents.

Rowing the New Wave 11

FDI in Indian Real estate

AccordingtotheDepartmentofIndustrialPolicyandPromotion(DIPP)data,FDIintotheconstructionsector-townships,housingandbuilt-upinfrastructure-declinedtoaboutUSD1.3billionovertheApril2013toFebruary2014periodfromUSD3.1billionintheApril2012toMarch2013period.ThisisprimarilybecauseinvestmentsentimentsinIndiadroppedsignificantlygiventhepre-electionpoliticaluncertaintyandunveilingofscams.Meanwhile,fromApril2000toFebruary2014,acumulativeFDIofUSD23.1billion-11%ofthetotalinflows-hascomeintotherealestatesector.Although,atpresent,100%FDIispermittedthroughtheautomaticrouteinthesector-whichcoverstownships,housing,commercialpremises,hotels,resorts,hospitals,educationalinstitutionsandrecreationalfacilities,aswellascity-levelandregional-levelbuilt-upinfrastructure,theFDIinflowwasreducedoveracoupleofyearsastherealestatesectorhavebeenbattlingdecliningsalesandhighinventory,alongwithcashcrunchandpiled-updebt.

Now,aftertheelectionresult,FDIinIndianrealestateisexpectedtogetalift,resultinginamplificationoffundflowsandstrengtheningofthebatteredIndianrupee.Withaclearmajoritytriumph,theincumbentgovernmentwillenjoyunwaveringstabilityatthecentre,

Permission Status of FDI in Indian Real estate and Infrastructure

Sharp fall in FDI in Real estate & Infrastructure in India

7000

6000

5000

4000

3000

2000

1000

1,652

3,922

4,829

5,787

1,663

3,141

1,332

FY 08FY07 FY 09 FY 10 FY 11 FY 12 FY130

USDmn

whichwillinturnencourageinvestors’sentimentswithregardtotherealestatemarket.GlobalinvestorsarenowmarkedlyoptimisticabouttheIndianeconomy,whichisexpectedtowitnessincreaseinforeigninvestmentinflows-bothviaFDIandFII-inthecurrentfinancialyear,ascomparedtoUSD29billionduringFY2013–2014.

ExistingAirports-beyond74%

AtomicMinerals

Incaseofjointventureortechnologycollaborationagreementinthesamefield

Greenfieldairports

Construction&maintenanceofinfrastructurelikeports,harbors,roadsandhighways

Powergeneration,transmissionanddistributionandtrading(Notatomicenergy)

Massrapidtransportsystems

Townships,housing,built-upinfrastructureandconstruction-developmentproject

Freely PermittedPermission Required

Source: DIPP, India

Rowing the New Wave12

key Steps towards Reducing Opaqueness

Improving Transparency: Facilitating Better Investment Scene

India’simprovingtransparencywouldlikelyactpositivelyforforeigncorporatesandinvestors.Everytwoyears,JLLreleasestheGlobalRealEstateTransparencyIndex,whichincludes97marketsworldwide.Auniquesurveythatcovers83differentfactorsacross 13transparencytopics(mentionedbelow),theindexprovidesaholisticscorethatindicatesimprovementordeteriorationinanycountry’stransparencylevel.Theindexaimstohelprealestateinvestors,corporateoccupiers,retailersandhoteloperatorsunderstandimportantdifferenceswhentransacting,owningandoperatinginforeignmarkets.Itisalsoahelpfulgaugeforgovernmentsandindustryorganisationswhoareinterestedinimprovingtransparencyintheirhomemarkets.Thelastpublishedindexin2012showedthatIndiaimproveditsoveralltransparencyratingalongwithstabilityinranksofTierIIcitiesandincrementinranksofTierIIIcities,comparedwith2010.Althoughthecountryisstillunderasemi-transparentstage,theimprovementisencouraging.

However,India’sgovernmentandregulatoryauthoritiesareworkingtoimprovetheinvestmentclimatethroughmarkettransparency-albeitataslowpace-whiletherelaxationofFDIlaws,animprovementintheavailabilityofdataandthestrengtheningofregulationsintherealestatesectoraresomeoftheotherinitiatives.

• DirectPropertyIndices

• ListedRealEstateSecuritiesIndices

• UnlistedFundIndices

• Valuations

• MarketFundamentalsData

• FinancialDisclosure

• CorporateGovernance

• Regulation

• LandandPropertyRegistration

• EminentDomain

• DebtRegulation

• SalesTransactions

• OccupierServices

13 Transparency Topics

• TheRealEstateRegulationBillisregardedasakeypolicythatwilllikelyimproveIndia’stransparencyscore

• WiththeincreaseinmultinationaloccupiersinIndia,theclarityofcontractsinoccupierservicesisexpectedtoimprovefurther

• AsbothinternationalandnationaldevelopersinIndiaarepenetratingdeepintothecities,transparencyscoresareexpectedtoimprovefurther

• Introductionofthegeneralanti-avoidancerule(GAAR)andthecomputerisationoflandrecords(CLR),alongwithstrengtheningofrealestateregulations,areexpectedtoimprovetransparencyintheapplicationoftaxandbuildingcodesandtheavailabilityoftitlerecords

• In2014,India’sTierIcitiesarelikelytobeclosetotransparentwiththeavailabilityofmoreaccuratedataonreturnsandmarketfundamentals.TierIIandTierIIIcitieswillcontinuetobelowerdownthesemi-transparenttier,albeitwithhighertransparencyscores

• Theavailabilityoftimeseriesdataonmarketfundamentals,suchasdemand,supplyandrealestatepricesfortheoffice,retailandresidentialsectors,isexpectedtoimprove.IndicesonrealestatereturnswillimprovewiththeincreaseinthenumberoflistedrealestatecompaniesandinstitutionalinvestorsinIndia

Rowing the New Wave 13

Real estate Investment Trust (ReIT)

Theglobalcommercialrealestatesectorwitnessedashiftfromtheprivatesectortopublicmarketsoverthepasttwodecades,whiletheIndianrealestateindustrybegantoseekadditionalsourcesoffundsoverthesameperiod,asthiscapital-intensivesectorfacedsevereconstraintsintermsofadequateandstructuredfinancingoptions.Asaresult,thesuccessstoryofglobalREITsiscompellingenoughtoencouragetheimplementationofasimilarregimeinIndia,withrequisiteadjustments.REITshaveproventobeanattractiveinvestmentoptionforretailinvestorsaswellasforinvestors’long-termpoolsofcapitalsuchaspensionfundsandinsurancecompaniesthatpreferaregularincomestream.REITshaveotheradvantages:

• Bringinincreasedtransparencybyadoptingbettercorporategovernance,disclosureandfinancialtransparency

• Deliverregularinformationexchangeandavailabilityinthepublicdomainwithhigherprofessionalism

• Equityfinancingwouldimprovethedebt-equitybalanceinthemarket• Provideavehicleforaddressingnonperformingassets• Givecommoninvestorsahugeopportunitytoshareinthegainsofthisassetclass

REITsarelikelytoprovideinvestorswithanavenuethatislessriskywithinvestinginincome-generatingpropertiesthaninvestinginunder-constructionproperties.Theywillalsoprovideanincomesourceinthe

Usa singapore UK India

System REIT S-REIT UK-REIT -

Date Established 1960 1999 2007 Atthedraftstage(October2013)

listed/Unlisted Both Both OnlyListed OnlyListed

Closed-end or Open-end Closed-End Closed-End Closed-End Closed-End

Fund vehicle Corporation,Trust Corporation,Trust Corporation Corporation

Investment in Real Estate Atleast75% Atleast70% Atleast75% Atleast90%

Minimum Number of stockholders

100 None 100 PublicfloatfortheREITunitsshallbeaminimumof25%atalltimes

REIt Income Notlessthan75%fromrentsormortgageinterest

Notmorethan10%ofitsrevenuefromsourcesotherthanrentsormortgageinterest

Atleast75%ofgrossincomefromrentsormortgageinterest

Atleast75%ofgrossincomefromrentsormortgageinterest

Distribution of REIt Income Atleast90% Atleast90% Atleast90% Atleast90%

Conduit Structure Passthrough Passthrough Taxexempt Notyetfinalised

formofrents,which,inturn,couldbeagoodhedgeagainstinflation.Moreover,beingamoreliquidinstrumentamongthecurrentrangeofpropertyinvestmentvehicles,REITsholdthepotentialofimprovinganinvestor’sinvestmentprofilethroughdiversificationoftheinvestmentbaseandtheincreasingstabilityoftheincomesource.Furthermore,notonlytaxbenefitsbutclarityontaxationisevenmoreimportant.ThereasonREITsaresuccessfulinothercountriesisthatonlytheendinvestorortheunitholderistaxed.Inaddition,whenREITsareintroducedforthefirsttimeinIndia,theyneedsomeincentivesandtaxbreaks-whichcouldbeonetimeorforastipulatedperiod-togivetheinitialpush.Oncetheindustrymatures,thenthegovernmentcanthinkofremovingorreducingthetaxincentives.

ThereleaseofdraftregulationsforsettingupREITsinIndiaisaneffortbythemarketregulator,theSecuritiesandExchangeBoardofIndia(SEBI),tobringahigherlevelofmaturitytotheIndianrealestatesector.ItisexpectedthatwiththeopeningofthesectortoREITs,therewillbeincreasedcapitalinflowsfromoverseasmarkets.TheintroductionofREITsisgoingtoprovideatimelyopportunityforbothinvestorsandtherealestateindustrytodevelopamatureandtransparentmarket.Overaperiodoftime,itwillalsohelpindevelopingapricediscoverymechanismforthecommercialpropertymarketinselectcities.

Rowing the New Wave14

Office Market - Superimposing the Growth of India

State of Office Market in India

TheservicesectoristhebackboneoftheIndianeconomy,contributing

tomorethan58%oftheGDP.Itisalsothekeydriveroftheoffice

spaceleasingmarketinIndia.Theloomingeurocrisisanduncertain

globaleconomicconditionssloweddownbusinessoutsourcingin

India,leadingtoslowdowninofficespacedemandin2012.These

conditionsledtosignificantdropinnetabsorptionofofficespacein

Indiaduringthesameperiod.However,in2013,theservicesector

stabilised,contributedbythemoderategrowthoftheinformation

technology/informationtechnology-enabledservices(IT/ITES)industry

andthestablegrowthofotherservicesindustryinIndia.Theyear2013

wasmoderatelygoodfortheIT/ITESindustry,whichwitnesseda7%

y-o-ygrowthaspertheNationalAssociationofSoftwareandServices

Companies(NASSCOM)estimate.Thissectoraloneaccountedfor

8.2%ofIndia’sGDP.Recruitmentsinthissectorgrewby32%y-o-y

duringthesameperiod.Inaddition,otherservicesectorssuchas

finance,insurance,businessservicesandrealestatealsowitnessed

stablegrowthin2013.Therefore,thesefactorskepttheofficespace

demandstabledespitethesloweconomicgrowthinIndia.Mumbaiand

Bangalorewerethetwocitiesthatwitnessedmaximumdemandfrom

officeoccupiersin2013andcontributedtomostofthenetabsorption.

OfficespacedemandremainedstrongeveninNCR-Delhiwheremost

oftheleaseswerepre-commitmentinofficespacesthatwereunder

construction.Apartfromthesethreeprimecities,Punealsowitnessed

healthydemandforofficespacein2013.

TheNASSCOMestimatesthecurrentFY2013-2014toberelatively

morepositivefortheIT/ITESsector.Italsoestimatesthat,duringthe

sameperiod,exportrevenueswillgrowby12-14%-owingtosustained

economicrecoveryintheUnitedStatesandEurope-anddomestic

revenueswillgrowby13-15%,owingtoincreasedspendingbythe

governmentandthebanking,financialservicesandinsurance(BFSI)

sector.Meanwhile,officespacedemandisexpectedtoimproveor

remainstablein2014.Thepositivegrowthsignshownbythenew

governmentislikelytoimproveinvestmentsentimentsandbusiness

climateinIndia.Thiscanencouragecompaniestoexpandtheir

operationsfurtherinthecountry.Fence-sittingoccupierswhowere

waitingfortheelectionresultscantakepositivedecisionsthisyear.

MumbaiandBangalorearelikelytocontinuetobethemostpreferred

citiesbyofficeoccupiers.

Supplyconditionsremainedstableover2013,andthisisexpected

tocontinuein2014.Thesuddenburstofoptimismbroughtbythe

electionresultsislikelytosupportdeveloperstocontinuebuilding.

Source: JLL Research and ReIS, 1Q14

60

50

40

30

20

10

20102009 2011 2012 2013

FORECAST

2014 20150Ne

wCo

mpletion

/NetAb

sorption(inmillio

nssq

ft)

42.0

40.5 44

.437.0

30.9

21.6

30.4

26.8

33.3

26.8

8.522.8

3.027.8

27.0

17.1

18.4

NewCompletion NetAbsorption CBDSupplySBDSupply PBDSupply

Demand and supply of office space across major seven cities in India

Rowing the New Wave 15

Capitalmarketsareexpectedtoimprove,andthismaybringinthe

much-neededimpetusfordeveloperstocompletetheirprojects.

Developerscanleverageonthestableofficespacedemand,whichis

likelytocomebykeepingtheirbuildingsreadyforoccupancy.

Intermsoffinancialindicators,theofficesectorenteredapreliminary

growthphasewithagradualincreaseinrentsinend-2013.Average

capitalvaluesintheofficesectorinIndiawerestill25%lowerthan

theirmostrecentpeaksseeninmid-2008.Ontheotherhand,capital

valuesintheresidentialsectorhadsurpassedtheirpreviouspeakby

end-2011.In2013,selectsubmarketsinMumbai,PuneandChennai

witnessedmoderategrowthinrents,whilethecitiesofBangaloreand

NCR-Delhiwitnessednegligiblerentalgrowth.AmongtheTierIIcities,

Hyderabadsawnegligiblegrowth,whereasinKolkata,rentalvalues

remainedstableinmostsubmarketsamidthedownwardpressure

DECLINE SLOWING

Rental Value Index

2008 2009 2010 2011 2012 2013 1Q14 1Q14

Bangalore -0.9% -17.7% 3.3% 10.8% 5.3% -0.6% 0.3% 99.5

Mumbai City -3.6% -34.3% 0.8% 1.1% 0.8% 0.5% 0.1% 62.1

Delhi City -3.8% -41.6% 2.2% 3.2% 1.3% 0.0% 0.0% 59.2

Mumbai Suburbs -7.0% -34.3% 0.0% 7.4% 1.1% 2.1% 0.6% 68.3

Gurgaon (Prime) 1.6% -31.1% 2.8% 11.8% 5.7% 5.0% 0.9% 80.9

Gurgaon (Off Prime) -15.0% -38.2% -2.4% 9.8% 4.4% 2.1% 0.0% 66.7

Noida -3.2% -16.6% -9.0% 3.3% 2.7% 3.6% 0.0% 77.7

Chennai -0.6% -22.4% 0.0% 6.4% 4.9% 4.4% 0.2% 93.2

Pune -5.1% -20.7% 0.0% 3.4% 7.3% 6.8% 2.3% 83.9

Hyderabad 3.1% -14.0% 0.0% 4.1% 5.1% 1.1% 0.0% 80.1

Kolkata 9.3% -27.4% 0.0% 5.7% 8.2% -0.3% 0.0% 82.6

RENTSDECLINING RENTS RECOVERING

Mumbai City includes CBD, SBD Central, BkC and SBD North. Mumbai Suburbs includes eastern and Western Suburbs. Delhi City includes -CBD & SBD of Delhi.

Source: JLL Research and ReIS, 1Q14

Office rental value Index

createdbyslowabsorptioninthecity.RentalvaluesinChennai

remainedlargelystablewithstabledemand.However,increased

demandandrelativelylowvacancylevelssupportedrentalgrowthinthe

SBDandSBDOldMahabalipuramRoad(OMR)submarketsinChennai.

Rowing the New Wave16

Changing Occupier Profiles in India

Share of leasing activity by occupier type across India

2009 2010 2011 2012 2013

100%

80%

60%

40%

20%

0%

ProfessionalServices

ConsultancyBusiness

Telecom,Healthcare-Biotech,RealEstate &Constructionandotherindustries

BFSI

Miscellaneous

IT&ITES

Manufacturing/Industrial

23%

22%

23%

25%

5%

34%

26%

11%

18%

8%

39%

29%

8%

18%

4%

46%

18%

16%

13%

5%

34%

14%

13%

10%4%

24%

Meanwhile,thepost-GFCandsovereigncrisisinEurozonemadetheBFSIindustryverycautious.BFSIcompaniesconsolidatedtheiroperationsandreducedexpansionplans.Asaresult,theirshareinofficespaceleasinggraduallydroppedfrom23%in2009to14%in2013.MumbaiandPuneremainedastheirmostpreferredcitiesin2013.Thetelecom,healthcare,biotech,realestate,constructionandotherindustriesalsofollowedthesamepatternastheBFSIindustries,seeingtheirsharedropfrom25%in2009to13%in2013.PuneandHyderabadreducedtheirdependencyontheIT/ITESindustry.Hyderabadhasbeenthefirstchoiceforhealthcare,biotech,telecomandconstructioncompanies,whichhavecollectivelytakenupmorethan25%ofthetotalspaceleasedinthecity.

Interestingly,themanufacturingsector-whichpassedthroughchoppywatersacoupleoftimesduringthelastfiveyears-continuedtoleaseofficespaceinastablepattern.Manufacturingcompaniesincreasedtheirsharefrom22%in2009to24%in2014.Bangalore,whichisconsideredasthesiliconhubofIndia,interestinglyturnedouttobetheleaderinofficespaceleasingbymanufacturingfirms.Anotherindustrythatincreaseditsshareinofficespaceleasingconsistentlyoverthelastfiveyearswasbusinessconsultingcompanies.NCR-DelhiwasthemostpreferredcitybybusinessconsultingfirmsinIndiatosetuptheiroperations.

Overthelastfiveyears,officespaceoccupierprofilesinIndiahaveseenaseaofchange.AlthoughtheIT/ITESindustrycontinuestoremaintheleaderinleasingofficespacesinIndia,thelastfiveyearssawagradualincreaseintheshareofofficespacetake-upbymanufacturingfirms.Duringthesameperiod,therewasagradualdecreaseintheshareofofficespacetake-upbytheBFSIindustry.Thisisadirectimplicationoftheperformanceofthesesectorsintheturbulenteconomicconditionofthenation.Meanwhile,theIT/ITESindustrywitnessedaslowdownduringtheGFC.PosttheGFC,thisindustryslowlyrevivedgrowthastheUSandUKeconomiesrecoveredandwitnessedstrengtheneddomesticdemandforIT/ITESservices.TheshareofIT/ITEScompaniesintotalspaceleasedacrossIndiawas46%in2010andfellto34%in2013.ThisindicatesanothertrendthatIT/ITEScompanieshaveadoptedstrategiesofefficientusageofspacestoreduceexpansionofoperationsastheybecomecautiousabouttheirrealestateexpenditure.Amongthecities,Mumbai,Pune,KolkataandNCR-DelhistrengthenedtheirshareofIT/ITESleasedspace,whereasBangalore’ssharedropped.

Source: JLL Research and ReIS, 1Q14

Rowing the New Wave 17

FLeXI DeSkS Smartoccupancyorflexidesksareastrategythatallowsmaximumworkspaceefficiencyorreductionofunusedrealestatespacesordesks.Insuchoffices,therearenofixeddesksorspacesfortheemployees.Theofficespacehasanoptimumnumberofdesksbasedonaverageoccupancyoftheoffice,andeveryday,employeesareallottedadeskwhentheylogintotheofficeanduntiltheylogout.Thisarrangementdoesnotallowdeskstoremainunusedwhenthe

employeeisoutofofficepremisesforclientmeetingsorotherofficialworks.Thisarrangementalsoimprovesnetworkinginofficeandupgradestheenergyefficiencyoftheofficepremises.ThisisalreadybeingusedinothercountriesandisslowlygaininggroundinIndia.TheJLLMumbaiofficehasalreadyadoptedthisstrategy,whichiscalledtheWorkSmartprogramme.

TheWorkSmartconceptworksthisway:Anemployeewouldlogintothesystemass/heentersthe‘cubicle-less’officeinthemorningandreceivesthecodeforhis/herworkdeskforthatday,takechargeofthedeskphoneandlaptoppointandworkthereuntils/helogsoffintheevening.S/hewouldhavealockersomewhereintheofficeforkeepinghis/herbelongingsand,withthissystem,wouldhavetoadapttoapaperlesswayofworking-awayofworkingthatcreatesnowastepaperbutleavesadeskcleanontopandunderneath.OnekeyachievementofthisprogrammeisthatthisarrangementhasallowedtheJLLMumbaiofficetosave30%onrealestatecosts.

Corporate Real estate Dynamics- Occupiers’ Needs Giving Way to New Occupancy Strategies

PosttheGFC,officeoccupiershavefocusedoncostcuttingandcostefficiency,alongwithgrowth.Realestateexpenditureisoneofthekeyexpensesthatanoccupierhastobear.Undersuchcircumstances,occupiersstartedadoptinginnovativestrategiestomanagerealestatecosts.Theseinnovationsandcreativestrategiescameupasnewtrendsinofficeoccupancyoverthelastfewyears.Threeofthesetrendsarediscussedbelow:

GReeN BUILDINGS GreenfootprintisincreasingconsistentlyinIndia.TheincreasingawarenessaboutsustainabilityandrisingenergycostsaredrivingthedevelopmentofgreenbuildingsinIndia.Currently,thegrowthofgreenbuildingsinthecountryismorevisibleinthecommercialsectorthaninotherrealestatesectors.Thisisprimarilyledbymultinationalanddomesticoccupierswhowanttoproactivelydemonstratetheircorporatesocialresponsibility(CSR)stewardshipandalsofocus

onsavingenergycosts.Asidefromoccupiers,manydevelopersinIndiaarealsoadoptinggreendesigntechnologiesinconstructingnewofficebuildings.ChennaiandMumbaiaretheleadingcitiesinthedevelopmentofgreenofficebuildingsinIndia.

SMART BUILDINGS Risingenergy,waterandotherresourcecostshavedriventheriseofsmartorintelligentbuildingsinIndia.SmartbuildingsarealsousedinIndiaforthesafetyandsecurityoftheinhabitantsofthebuildings.Thesebuildingsaredevisedwithcomputer-aidedbuildingmanagementsystemsthatcanallowmanagingthebuildingsremotely.Developers,occupiersandfacilitymanagershaveeffectivelyadoptedthebuildingmanagementsystemsinsmart

buildingsacrossthecountryinalltypesofbuildings,suchasoffice,retail,residentialandhotelprojects.Fromsmallbuildingmanagementsystemstohighlysensitiveandadvancedmanagementsystems,Indiahaswitnessedgrowthofintelligentbuildingmanagementsystemsinallsegments.CompaniessuchasCisco,Cognizant,HSBC,IBM,InfosysMicrosoftandWipro,amongothers,haveadoptedbuildingmanagementsystemsintheircampusfacilitiesinIndia.Inaddition,manyotherstand-aloneofficebuildingsinIndiahavealsoadoptedintegratedbuildingmanagementsystemsintheirbuildings.OlympiaTechParkandTIDELParkinChennai;TechnopolisinKolkata;andCMCBuildingandGodrejBhavaninMumbaiaresomeofthesmartofficebuildingsinIndia.

Rowing the New Wave18

Retail Real Estate - Reinvigorating Growth

Retail Industry: Advantage India

Favourabledemographics,ayoungandworkingpopulation,risingincomelevels,urbanisationandgrowingbrandorientationarehelpingconsumerisminIndiawitnessunprecedentedgrowth.Subsequently,accordingtoarecentreportbyErnst&Young(EY)andtheRetailersAssociationofIndia(RAI),India’sretailmarket,whichin2013wasestimatedatUSD520billion,isexpectedtogrowatacompoundannualgrowthrate(CAGR)of13%toreacharoundUSD950billionby2018.Meanwhile,thereportalsostatesthatorganisedretailpenetrationisexpectedtoclockannualgrowthof19–20%toreach10%by2018.PenetrationinTierIIandTierIIIcities,animprovementinbusinessmodelsandoperations,aswellasmovementfromunorganisedtoorganisedtradewouldlikelyplayanintegralroleindrivingthisgrowth.

Source: eY and RAI, 2014

2013

7.5%Us$ 520 bn

201810%Us$ 950 bn

Size of Indian Retail Industry

Rowing the New Wave 19

Retail Real estate in India: Benchmarking With Other Retail Cities of Asia Pacific

South-EastAsia,inparticular,continuestomaturerapidlywiththecompletionofnewretailspaceandincreasinglysophisticatedconsumers,spurringthearrivalofnewretailersfromoverseas.Domesticconsumptionishealthyinmostpartsoftheregion,albeit

Thefalteringtrendsofhighervacancyrates

• AmongtheemergingretailcitiesofAsia,Indiancitiessufferfromthehighestvacancyrates - Largebuilt-upofaverageandpoor- grademallsisthemainculprit - Consumersandretailersincreasingly prefermallsthataremanagedwell

• Retailershavemovedtosuperior-grademallsupontheiravailability,thusvacatingspacereluctantlytakenupearlier,owingtoanabsenceofsuperiormalls

• ExistingstockinIndianTierIcitiesislesserthaninTierIIcitiesofChina

• PrimecitiesinsmallermarketssuchasThailandandthePhilippineshavestockscomparablewithIndianTierIcities

• RentsinIndianTierIcitiesarecomparablewithotheremergingcitiesintheAsiaPacificregion

• RetailpenetrationinIndiaisgovernedbytheavailabilityofrelevantsupply

• ShenzhenandHangzhouinChinaandMumbaiandDelhiinIndiaofferlargeconcentrationsofhigh-net-worthindividuals(HNWI)butalimitedstockofqualityretailspace

Hyderabad

60Indiahasproportionatelylessersupplydespitebeingalargemarket

Orgnise

dReta

ilstoc

kandFutu

re

Supply(millionsq

ft)

80

100

40

20

0

Source: JLL Research and ReIS, 1Q14

Source: JLL Research and ReIS, 1Q14

Mumb

ai

Hefei

Pune

Chen

nai

Changsha

Shenyang

Bangalo

re

Bangkok

Kolka

ta

Hangzou

Jakarta

Shenzhen

Chengdu

NCRDe

lhi

Manila

RetailStock(Asof2013)FutureSupply(during2014-2016)

Hyderabad

1500

Rentalsareincomparionwithmature

citiesofAPAC

PrimeR

etailR

ents(USD

/sqm/year)

2000

2500

1000

500

0

Mumb

ai

Pune

Chen

nai

Bangalo

re

Bangkok

Kolka

ta

Hangzou

Jakarta

Shenzhen

NCRDe

lhi

Manila

RetailStock(Asof2013)FutureSupply(during2014-2016)

Shenyang

Chengdu

cloudedtoacertainextentbylargerglobaleconomicuncertainty.Asaresult,Indiawillcontinuetoseegoodretailactivity,evenatthegivenfactthatitwillseelessersupplydespitebeingalargemarket.cloudedtoacertainextentbylargerglobaleconomicuncertainty.Asaresult,

Rowing the New Wave20

Indiawillcontinuetoseegoodretailactivity,evengiventhatitwillseeRetail Realty: Demand Supply Dynamics in India

DrivenbythiseconomicgrowthandfactorsfavourabletotheIndianconsumer,therealestatesectorhasshownexemplarygrowth,growingfromlessthan1millionsqftofmallspacein2001.TheIndianorganisedretailsectorhasalsowitnessedamanifoldincrease.However,onthebackofeconomicupsanddownsandirrelevantsupply,theperformanceoftheretailindustryhaswitnessedswings,withseveralchangesinabsorptionlevelsandvacancyratesovertheyears.

Retail Realty in the Past: key Pointers

• Afterdisplayinginherentgrowthduring2003-2008,retailrealestatewitnessedaslowerpaceofgrowthaftertheGFC

• Themarketbouncedbackin2011withtheadditionofalargeamountofspace

• Themarketwitnessedaslowadditionofnewsupplyin2012and2013

70.6 millionsqft

organisedretailstockinmajorsevencitiesat1Q14

18.4% vacancyinorganisedretailstockinmajorsevencitiesatend-

1Q14

5.1 millionsqft

netabsorptionin 2013

5.7 millionsqft

newsupplyaddedin2013

key Challenges in the Retail Real Estate sector

• Lackofsophisticatedretailplanning

• Inmostcities,itisdifficulttofindsuitablepropertiesincentrallocationsforretailbecauseoffragmentedprivateholdings,infrequentauctioningoflargeplotsofgovernment-ownedvacantlandandlitigationdisputesamongowners

Thecomingyearsarelikelytohavenearlystablemovementwithmoderatesupplyfromthedevelopersamidexpansionrequirementofretailers.However,lukewarmdemandformallspacenotinfavourablelocationmightaffectthevacancyrate.

Completion NetAbsorption VacancyRate

(‘000sqm) (VacancyRate)

1,500 30%

1,250 25%

1,000 20%

750 15%

500 10%

250 5%

2009 2010 2011 2012 20132013 2014 20150 0%

Forcast

Supply and demand of organised retail space in India in top seven cities

Source: JLL Research and ReIS, 1Q14

Rowing the New Wave 21

Major Concerns for the Retail Real estate Sector in India

• Polarisation in demand in Indian retail real estate - InTierIcitiessuchasMumbaiandNCR-Delhi,vacancyratesvaryhugelyacrossmallsthatareingoodlocations,backedupbyasustainableconsumercommunityandover-ambitiousprojectslaunchedinpoorlocationswithalackofinfrastructureandsupportingconsumerpotential.Evenwithexpectedcorrectioninsupplyinthelongterm,thismismatchinvacancylevelsisexpectedtochangelittle.

• Bigger malls versus smaller malls - Largeshoppingmallsthatmostlyhavearangeofstoresalongsidecinemasandentertainmentarcadesinoneplacearebetteratbecoming‘destinations’inacity.However,securingalargelandparcelisdifficultincitycentres.Therefore,attimes,inbiggercities,largeshoppingmallstendtobelocatedinotherprimeareas.However,insmallercities,largeshoppingmallstendtobethemaincityattraction,i.e.,,LuluMallinKochi.Subsequently,smallermallsareeasytoimplementwhilevisitorcomfortandstorevarietyarethebiggestdownsideswhencomparedwithtypicallarge-sizedmalls.Inaddition,smallcentres,especiallythoselocatedinanofficeorcondominium,havealimitedcatchment.

• absence of clear demarcation of use and strata sales - Itisevidentthattheideaofretailcumofficespaceisbeingusedevennow,asdevelopersdivideexistinglargefloorplatesintosmallerofficespaces.However,mixed-usedevelopmentsintegratingdifferentuseswithinthesamestructurecouldactasasolutionwithcleardemarcationandidentificationofuse.Apartfromthis,stratasalesarehurtingamall’sattractiveness,withthebrand-mixandretailers’presencegettingahit.

Retail Real estate as a Long-term Business

Amidtheconcernsofventuringintoretailsector,thereisenoughpotentialintheIndianretailrealtytoperformasamajorassetclassforinvestment,asthepaceofgrowthislikelytowitnessnorthwardmovementinthecomingyears.Themajorpotentialoftheretailrealtysectorhasremaineduntapped,unlikeinothermajorAsiancitieswhereitisalreadybeingusedasawealth-generatingassetwhenproperlylookedupon.

30%

35%

2000150010005000

25%

20%

15%

10%

5%

0%

Vacancy

Stock(in‘000sqm)

MumbaiPrimeCityMumbaiPrimeOthersMumbaiSuburbs

DelhiNCRPrimeCityDelhiNCRPrimeOthersDelhiNCRSuburbs

Source: JLL Research and ReIS, 1Q14

Polarisation in demand in NCR-Delhi and Mumbai

However,thisrealestatesegmentiscomplexwhencomparedwithotherassetclassessuchascommercialandresidentialrealestate.Investorsinretailrealtyneedtoevaluatemanyfactors,includingdemandforretailspaceinthelocation,expectedreturnoninvestment(ROI),pastperformanceofretailersandfutureexpectations,changingpatternofconsumerspendingandshiftingcommercialtrendswithe-tailing,aswellasthelocalrulesandregulationsmanagingtheretailleases.

Rowing the New Wave22

the Retailer

Retailersarethedeterminingfactorbehindaninvestor’sROIthroughrentorminimumguaranteeorrevenueshare,oracombination.Theamountofsalesaretailercanexpectinanareaonthebackofconsumers’spendinghabitsanddisposableincomesisthemotivationfor

leasingspace

the Developer

Developersareanothercriticallink.Aninvestorchoosingmallsthatare

managedbyaprofessionalagencyoradeveloper,ascomparedwithstrata-salemalls,offsetsriskbyhavingcaptive

demandforresidentialandretailspaceandofferslong-termstability

ROI and Revenue Model

Therevenuemodelhasevolvedoverthepastfewyears,withagradualshiftfromonlyrenttominimumguaranteeorsharingrevenue.Retailersarenowpayingabaserentalongwithashareoftherevenue.Thisallowsretailerstobringdownfixedcostsandpasssome

businessrisktotheowner

Case Study: CRCT

CapitaMallTrustholds122.7millionunitsinCapitaRetailChinaTrust(CRCT)-approximatelya15%stake-asat31December2013.ThetotalassetsizeofCRCTwasapproximatelyUSD2.2billionasatend-2013.

• CRCTisthefirstandonlyChinashoppingmallthatisREIT-listedinSingapore,withaportfoliooftenincome-producingmalls• Acrosstheportfolio,CRCTachievedastrongrentreversionof13.8%andoperatedatahighoccupancyrateof98.2%• CRCThasageographicallydiversifiedportfolioofmallsinsixcities-Beijing,Shanghai,Zhengzhou,Hohhot,WuhuandWuhan

Allthemallsintheportfolioarepositionedasone-stopfamily-orientedshopping,diningandentertainmentdestinationsforthesizeablepopulationcatchmentareasinwhichtheyarelocated.Theyareaccessibleviamajortransportationroutesoraccesspoints.Asignificantportionoftheproperties’tenanciesconsistsofmajorinternationalanddomesticretailers,suchasWalmart,CarrefourandtheBeijingHualianGroup,undermasterleasesorlong-termleases,whichprovideCRCTunitholderswithstableandsustainablereturns.Theanchortenantsarecomplementedbypopularspecialitybrands,suchasUniqlo,Zara,VEROMODA,Sephora,Watsons,KFC,PizzaHutandBreadTalk.

Mixed-use Development: Another Solution for Retail Real estate Growth

Whilemanyretailmallsacrossthecountry-fromsmallstripstomegamalls-sufferfromdouble-digitvacancyrates,designing,owningormanagingamixed-usefacilitymeansthereisanopportunityformultiplechallenges.However,italsoopensthedoortomultipleopportunities,whichinclude:

• Efficientuseoflandresources• Reductioninthelong-termmaintenancecostsofindividualbuildings• Brighteningofcommunitieswithopportunitiesforbuildingandenergyefficiencyaswellassustainability

key Challenges in Mixed-use Developments

• Ontheflipside,shopsinmixed-useprojectsinmanycaseshavelimitedscopeforretailactivity(stationeryshops,chemists,florists,smallrestaurantsandsoforth)

• Additionalproblemsthatariseinvolvetrash,badodour,trafficandnoisetransferringfromoneuseofthebuilding(abustlingrestaurantorstore)toanother(apartments)

• Parkingisanothercommonissuethatarisesinmixed-usefacilities

Case Studies: Mapletree Mixed-use Projects

• Future Cityisa200,000sqmmixed-usedevelopmentinthehistoricalcityofXi’aninShaanxiProvince.ItcomprisesapartmentsinfourexclusiveresidentialtowersandVivoCityXi’an,Mapletree’sfirstoverseasVivoCitymall.VivoCityisalifestyleshoppingmallofferingdiverseshopping,diningandentertainmentoptions.

• Nanhai Business City isbeingdevelopedasanintegratedoffice,residentialandleisuredevelopmentlocatedbetweenthetwobustlingcitiesofFoshanandGuangzhou.Thisplanned42hectaresmixed-usedevelopmentcomprisesretail,residential,officeandhotelcomponents.

Rowing the New Wave 23

FDI in Retail: e-commerce a Game-changer

E-commerceinIndiahaswitnessedstronggrowth,increasingfromUSD3.8billionin2009toUSD12.6billionin2013,whilethee-tailingsharewithintheretailindustrywasabout16%in2012,accordingtoareportbytheInternetandMobileAssociationofIndia(IAMAI)andtheIndianMarketResearchBureau(IMRB).AlthoughFDIpoliciesinIndiarestricte-commercecompaniesfromofferingservicesdirectlytoretailconsumersand100%FDIisallowedonlyinbusiness-to-businesse-commerce,thee-commerceindustryisopentotheproposalforupto51%automaticrouteforFDIinbusiness-to-consumere-commerce.FDIine-commercecouldgiverisetoaparadigmofinvestmentintheretailsectorofIndiawhilethegovernmentisagainstFDIinmultibrandretail.

Growth in E-commerce and Development of associated Industries

The future of retail real estate investment could be decided based on the following pointers:

• Venturingintolocationswithfavourableresidentialcatchmentsandbetterlong-termretailpotential• Selectingthecorrectstrategyforoperationsandgrowth• Churningofnewandinnovativeideasforpotentialretaildevelopment• Understandingtheneedsandwantsoftheconsumer

Thesefactors,whencombined,canmakerealestateusedfortheretailindustryagreatsourceofinvestmentopportunity

FDIine-commercecouldbringcapitalforinfrastructuredevelopment,actingasanimpetustothemanufacturingsector.Inaddition,itwouldprovideoptionsforincreasedoutreachandadoptionofglobalbestpracticesinIndia.Ontheotherhand,theincreaseinFDIcouldactagainstsmall-timebrick-and-mortarstoresandIndia-basedlargee-tailingorganisations.Apartfromthis,intheend,growthine-commercehasaspillovereffectonassociatedindustriessuchaslogistics,onlineadvertising,mediaandIT/ITES.

E-taIlING

It/ItEs

ONLINe ADveRTISING

MeDIALOGISTICS

Rowing the New Wave24

Residential Real Estate - Steering in the Right Direction

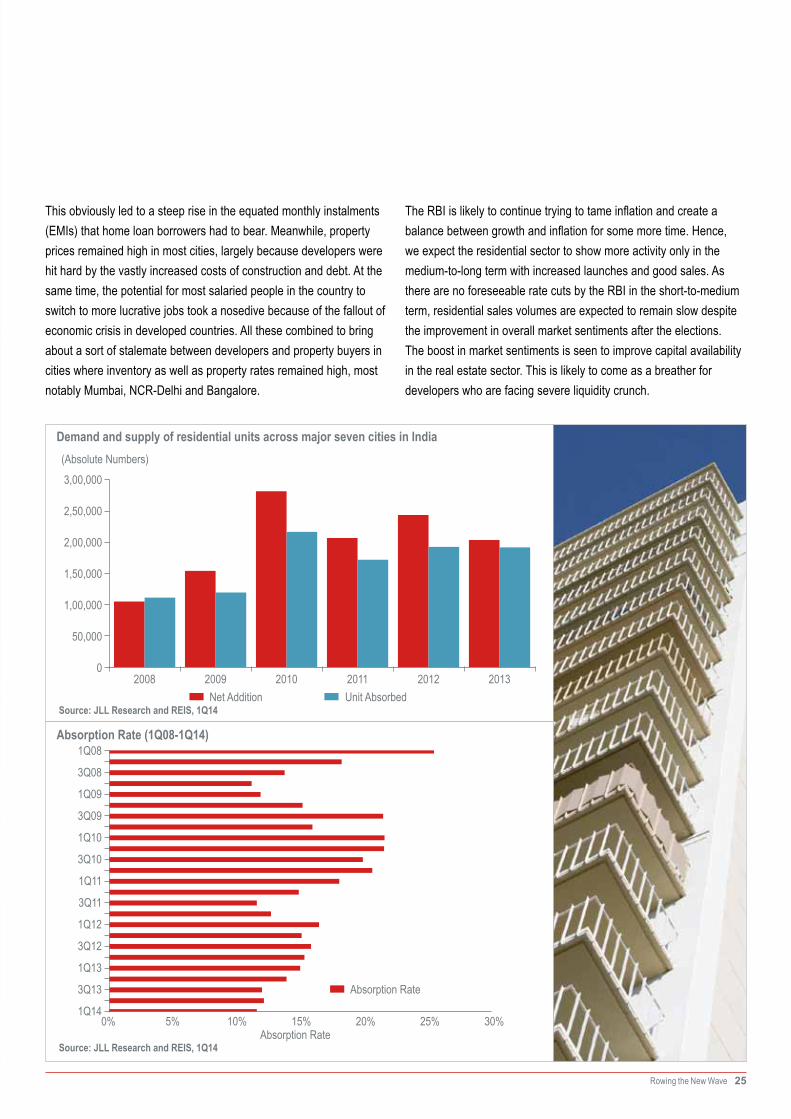

Acountry’seconomicperformancehasdirectrepercussionsonhowitsrealestatemarketbehaves.Thisisespeciallytruefortheresidentialpropertysegment.Moreprosperitymeanshigherfinancialconfidenceamonghomebuyers,andthisleadstoagreaterdemandforhomes.Theoppositeis,ofcourse,equallytrue.

Subsequently,residentialrealestatehasremainedthefocalpointofIndianrealestate,regardlessofthemarketconditions.Consideringthemassivedemandforhomesinthecountry,thisishardlysurprising.However,thedemanddoesnotequalabsorptioninaprice-sensitivecountrysuchasIndia,wherethegreatestrequirementforresidentialpropertiesstemsfromtheEconomicallyWeakerSection(EWS)andmiddle-incomegroup.Thehighdependenceonhomeloansbythesalariedclassunderscoresthepricesensitivityfactorevenfurther.Anditisimportanttomentionthat,ingeneral,2013wasnotagoodyearforIndia’sresidentialrealestatemarket.Thesluggishnesswasmostpronouncedintheprimecities.

Residential Real estate: Demand-Supply Pointers

AftertheGFC,India‘shousingmarketloomedwithslowerdemandduringtheyearsafter2009.However,since2010,theresidentialrealestatesectorhasstartedbouncingbackbasedontheresilienceshownbyIndiaintheinitialaftershockoftheGFC.Itisalsoevidentfromthemorethan15%absorptionrateduring2Q09–2Q11.However,withthesluggishnessoftheeconomy,theresidentialrealestatemarketstartedwitnessingnotonlyalessernumberofnewadditionsin2013butalsoaslowerrateofabsorption.Inaddition,thereweremorereasonsforthegeneralisedslowdowninmostIndiancitiesasinflationledtodecreasedpurchasingpowerandloweredbuyer’sconfidence.Meanwhile,theRBIwentthroughtheceilingwithitsspateofhikesininterestratestocontrolinflation.

Rowing the New Wave 25

Thisobviouslyledtoasteepriseintheequatedmonthlyinstalments(EMIs)thathomeloanborrowershadtobear.Meanwhile,propertypricesremainedhighinmostcities,largelybecausedeveloperswerehithardbythevastlyincreasedcostsofconstructionanddebt.Atthesametime,thepotentialformostsalariedpeopleinthecountrytoswitchtomorelucrativejobstookanosedivebecauseofthefalloutofeconomiccrisisindevelopedcountries.Allthesecombinedtobringaboutasortofstalematebetweendevelopersandpropertybuyersincitieswhereinventoryaswellaspropertyratesremainedhigh,mostnotablyMumbai,NCR-DelhiandBangalore.

(AbsoluteNumbers)3,00,000

2,50,000

2,00,000

1,50,000

1,00,000

50,000

2008 2009 2010 2011 2012 20130

NetAddition UnitAbsorbed

1Q08

3Q08

1Q09

1Q10

1Q11

1Q12

1Q13

3Q09

3Q10

3Q11

3Q12

3Q13

1Q140% 30%25%20%15%10%5%

AbsorptionRate

TheRBIislikelytocontinuetryingtotameinflationandcreateabalancebetweengrowthandinflationforsomemoretime.Hence,weexpecttheresidentialsectortoshowmoreactivityonlyinthemedium-to-longtermwithincreasedlaunchesandgoodsales.AstherearenoforeseeableratecutsbytheRBIintheshort-to-mediumterm,residentialsalesvolumesareexpectedtoremainslowdespitetheimprovementinoverallmarketsentimentsaftertheelections.Theboostinmarketsentimentsisseentoimprovecapitalavailabilityintherealestatesector.Thisislikelytocomeasabreatherfordeveloperswhoarefacingsevereliquiditycrunch.

Absorption Rate (1Q08-1Q14)

Demand and supply of residential units across major seven cities in India

Source: JLL Research and ReIS, 1Q14

Source: JLL Research and ReIS, 1Q14AbsorptionRate

Rowing the New Wave26

80-85%

Navi Mumbai

75-80%

Mumbai

65-70%

Kolkata

60-65%

Gurgaon

25-30%

Noida & Greater Noida

25%

Hyderabad

30%

NCR Delhi

50%

Chennai

50-55%

Bangalore

Rise in Prices of Residential Properties in Last Five YearsProperty prices in most markets have regained strength after the correction triggered by the global inancial crisis of 2008

Figure represent capital value change between April-June 2009 and January-March 2014

Source: JLL

80-85%

thane

60-65%

Pune

Rowing the New Wave 27

Affordable Housing in Indian Context

Withintheattractivepost-electionresidentialrealestatesectorofIndia,affordablehousingappearsasaparticularlylucrativeopportunity.Thepotentialisbolsteredwiththebusinessmodel,asitisinsyncwiththecountry’ssocioeconomicparadigmshiftwiththeriseofthemiddleclassandlower-middleclass.Affordablehousingbecomesakeyissue,especiallyindevelopingnationswheremajorityofthepopulationarenotabletobuyhousesatthemarketprice.

Thedisposableincomeofthepeopleremainstheprimaryfactorindeterminingaffordability.Asaresult,thegovernmenthastheincreasedresponsibilitytocatertotherisingdemandforaffordablehousing.TheIndiangovernmenthastakenvariousmeasurestomeettheincreaseddemandforaffordablehousingalongwithsomedevelopersandtostressonpublic-privatepartnerships(PPP)forthedevelopmentoftheseunits.

INCOMe CATeGORIeS INCOMe LeveL SIZe OF UNIT AFFORDABILITY

EconomicallyWeakerSections(EWS)

<INR150,000perannum Upto300sqft EMItomonthly income-30-40%

LowerIncomeGroup(LIG) INR150,000perannumto INR300,000perannum

300to600sqft EMItomonthly income-30-40%

MiddleIncomeGroup(MIG) INR300,000to INR1,000,000perannum

600to1200sqft Housepricetoannual income-Lessthan5.1X

Definitions of affordable housing in India (as developed by kPMG and CReDAI)

Factors leading to emergence of affordable housing

Source : kPMG

Better cash collection of developers, lower development

costs of affordable projects

Mass appeal of affordable housing evinces strong

response in volumesacquire land with part

paymentImproved finances of residential real estate

developers

start construction, avail construction finance

Launch of projects, collection of customer advances, payment of land dues

acquire land with part payment

Use surplus funds as down payment for

additional land

High leverage among

developersWeak launches muted response

lack of construction

finance

acquire land with part payment

Postponement of project launches

Deleveraging and distressed sales

Befo

re

Crisi

sDu

ring

Crisi

saf

ford

able

Hous

ing

Theweaknessindeveloper’soperatingmodelwhichwascausedbyacashcrunchduringthecrisis,gotsuccessfullyaddressedbyashifttoaffordablehousing

Source : kPMG, Aranca Research

Rowing the New Wave28

New Developments in the affordable Housing sector since 2012

• The Rajiv Rinn Yojna (RRY):ArevisedinterestsubsidyschemeasanadditionalinstrumentforaddressingthehousingneedsoftheEWSandLowerIncomeGroup(LIG)segmentsinurbanareas.Theschemeenvisagestheprovisionofafixedinterestsubsidyof5%(500basispoints)oninterestchargedontheadmissibleloanamounttoEWSandLIGsegmentstoenablethemtobuyorconstructanewhouseorforcarryingoutaddition(i.e.,room,kitchen,toiletorbathroom)totheexistingbuilding

• The Credit Risk Guarantee Fund TrustforLow-incomeHousing(CRGFTLIH)wassetupandregisteredbytheGovernmentofIndia(GoI)on1May2012throughtheMinistryofHousingandUrbanPovertyAlleviation(MoHUPA)

• TheNationalHousingBank(NHB),inassociationwithGenworth,theAsianDevelopmentBank(ADB)andtheInternationalFinanceCorporation(IFC)setupIndia’smaidenmortgageguaranteecompany,theIndiaMortgageGuaranteeCorpPvtLtd(IMGC).ThecompanywasgrantedcertificateofregistrationbytheRBIinApril2013

• INR60billion(INR6,000crore)wasallocatedforruralhousingfundin2013–2014

• TheNHBsetupanurbanhousingfund,andINR20billion(INR2,000crore)wasallocatedinthisregard

the potential market size for affordable housing in India

Source: India Urbanization Affordable Housing Model, Mckinsey Global Institute Analysis

Tier1city UrbanIndia(2010E)

UrbanIndia(2030E)

Tier4cityTier3cityTier2city

In 2010E In 2030E

25 million households

total market size (aggregate of slum and non

slum population

38 million households

5.6

1.8

1.1

8.1

16.6

4.2

0.9

0.4

3.0

8.4

38

SlumPopulation

Non-SlumPopulation

1.5x

Rowing the New Wave 29

New Developments of Precast Technology: Latest for Quality of Construction

Developersandbuildersarenowadoptingprecasttechnologytoavoidlabourshortageandtimedelays,alongwithanaimtodeliverqualityproducts.Themainadvantagesofprecasttechnologyarespeedofconstructionandavalue-for-moneyproduct.Inaddition,itenhancesthequalityofthefinaloutputwiththecreationofabiggercarpetarea.Theuseofsuchtechnologyhelpsinsavingupto64%ofthetimetakenforsimilarprojectsusingnormalconstructionmethodsandtechnology.

Thistechnologyconsistsofcustom-designedprecastconcretecomponentssuchasroofslabs,beams,columnsandwallpanels,amongothers,whichofferflexibilityinshapeandsizewithavarietyofsurfacefinishesandcolours.Thecomponentsaremanufacturedorcastinstrictlycontrolledenvironmentwithstate-of-the-artmachineryerectedonthesitewiththehelpoftowercranesandthenjoinedtoeachotherasperspecification.

New Policy: Real estate (Regulatory and Development) Bill – Reorganising Residential sector in India

TheRealEstate(RegulatoryandDevelopment)Billaimstoinstiltransparencyintoasectorthathasbeensofarunregulatedandhaswitnessedhaphazardgrowth.Althoughinitscurrentformthebillonlycoversnewprojectsofover4,000sqmintheresidentialsector,consumerscanexpectsomeofthebestpracticesinthisindustrytocomeintoforce,includingprotectingtheirinterestsinthetimelinessofprojectcompletion,delayinaccountabilityanddisputeresolution.Oncethebillcomesintoforce,therewillbeastandarddefinitionofcarpetareathroughoutthecountry.Inaddition,itproposesaregulatorineachstateandunionterritory.

Nevertheless,withtheapplicationofthebill,developerswouldbecomemoredependentoncostlierbankandnon-bankingfinancialcompanies(NBFCs)lendingforprojectfunding,astheycannotlaunchaprojectuntilallapprovalshavebeenreceivedfromtherelevantauthorities.Asidefromthis,withthismeasurethatencouragestimelycompletions,thebillislikelytolureinvestorsandenduserswithgreaterfaiththatthepropertywillbedeliveredtothepromisedspecifications.Inaddition,misleadingprojectadvertisementsmayresultinpunitiveactionbythestate.Asaresult,thisbillcouldhelpininculcatingaprofessionalattitudeamongthedevelopercommunity.

Thebillmayhelptoreducemoneylaunderingthroughrealestatebykeepingatraceofthemoneytrailthroughorganisedbrokerage,asitwillbecompulsoryforrealestateagentstohavealicence.Banksandfinancialinstitutionswillnowbecomemoreconfidentinlendingmoneytothissectorbecauseofthelowerriskofmisuseoffunds.Itmighthelptherealestateindustrytowardaparadigmshiftintermsoftransparencyandconsumerfriendliness,increasingIndia’stransparencyscoreandusheringinamorematureIndianrealestatemarket.However,thepossibilityofanincreaseinprojectcostonthebackoftransparencymeasureswithoutasinglewindowclearancemightactasasubduingparametergoingforward

Cost factor Intheory,thecostofconstructionwiththistechnologyismarginallyhigherthantheconventionalmethod,butinpractice,consideringthewastage-controlandspeedofconstructionwithbestofqualityandvirtuallynorepairorreworkingcost.theoverallvalueisthesame.

Investment-friendly Whilemarginsarenotgoingtobeaffectedmuch,thequalityoftheproductwillbeenhancedexponentially,andthedeliveryoftheprojectcanbemadewithinthestipulatedtimeframe.Thegovernmentisalsopromotingthistechnology,and,recently,theDelhiDevelopmentAuthority(DDA)completedaround800unitswiththistechnology.

Rowing the New Wave30

Crystal Gazing into

2014

TheRealEstateRegulatoryBillislikelytobeapproved,anditwillbringinthemuch-neededtransparencyintheIndianreal

estatesector.

TheNASSCOM estimates2014tobe

relativelymorepositive,with IT/ITESexportsrevenuesgrowingby12-14%anddomesticrevenuesgrowingby13-15%.Thisisalsoexpectedtoimprovetheoffice

spacedemandorkeepit stablein2014.

Asdemandforofficespace islikelytoimproveandsupplyconditionsalsoremainstable,

rentalandcapitalvaluerecoveryisontheway.Gurgaon and Pune areforecastwithhighestrentalappreciationbyend-2014.

FDIine-commerce canbeagame-changer.Itcouldbringcapitalfor

infrastructuredevelopment,actingasanimpetustothe

manufacturingsector.

Capital Markets

Office Market

Retail

Residential Market

REItsarelikelytobe allowedin2014.Thiswill

improvethesituationofcreditcrunchinrealestate.

AreportbyEYandthe RAIstatesthatorganisedretailpenetrationisexpectedto

reach10% by 2018

AstheRBIisnotlikely toeaseoutinterestratesintheshortterm,residentialsalesvolumesarelikelytoremain

lowintheshortterm.

Affordablehousing appearsasaparticularlylucrativeopportunityinthe

currenttimes.TheNHBhassetupanurbanhousingfundandallocatedINR20billionin

thisregard.

GDPgrowthrateis estimatedtobeat4.5-4.7%

in2014bytheRBI,WorldBankandtheInternationalMonetaryFund(IMF).However,thenew

governmenthasplanned toincreaseitto 5% or above.

Theinvestmentclimateislikelytoimprovewithastablenewgovernmentatthecentre.RatingagenciesmayimproveIndia’sinvestmentratingin

2014.FDIflowsareexpectedtoimprove.

economy

Rowing the New Wave 31

Author Profile

Sujash BeraAssistantManager,Research&[email protected]+913322273293SujashBeramanagestheResearchandRealEstateIntelligenceService(REIS)offeringsforKolkata.HejoinedJLLin2012andisbasedinKolkata.Hecontributestotopicalwhitepapersandpropertymarketdigestaswellasresearchdeliverablesonthecommercial,retail,residentialandindustrialrealestatemarketsinIndia.

SujashholdsaMaster’sdegreeincityplanningfromIndianInstituteofTechnology,Kharagpurbesidesbeinganarchitect.Hehasfouryearsofexperienceintheindustry.

Trivita Roy AssistantVicePresident,Research&REIS [email protected] +914040409123

TrivitaRoyhasjoinedJLLResearchteamin2007.BasedoutofHyderabad;shecontributestotopicalwhitepapers,propertymarketdigestandresearchdeliverablesonindustrial,commercial,retailandresidentialrealestatemarketsin

India.SheisalsoresponsibleforIndianrealestateintelligenceservice(REIS)

TrivitaistrainedasCityPlannerfromIndianInstituteofTechnologyKharagpurbesidesbeinganarchitectandalsoholdsaDiplomainExecutiveGlobalBusinessManagementfromIndianInstituteofManagementCalcutta.Shehaseightyearsofexperienceinrealestateresearch.

ashutosh Limaye Head,ResearchandREIS [email protected] +919821107054

FormoreinformationaboutResearch

about JLLJLL(NYSE:JLL)isaprofessionalservicesandinvestmentmanagementfirmofferingspecializedrealestateservicestoclientsseekingincreasedvaluebyowning,occupyingandinvestinginrealestate.Withannualfeerevenueof$4billion,JLLhasmorethan200corporateofficesandoperatesin75countriesworldwide.Onbehalfofitsclients,thefirmprovidesmanagementandrealestateoutsourcingservicesforapropertyportfolioof3billionsquarefeetandcompleted$99billioninsales,acquisitionsandfinancetransactionsin2013.Itsinvestmentmanagementbusiness,LaSalleInvestmentManagement,has$48.0billionofrealestateassetsundermanagement.JLListhebrandnameofJonesLangLaSalleIncorporated.

JLLhasover50yearsofexperienceinAsiaPacific,withover27,500employeesoperatingin80officesin15countriesacrosstheregion.Thefirmwasnamed‘BestPropertyConsultancy’insevenAsiaPacificcountriesattheInternationalPropertyAwardsAsiaPacific2014,andwonnineAsiaPacificawardsintheEuromoneyRealEstateAwards2013.www.jll.com/asiapacific.Forfurtherinformation,pleasevisitourwebsite,www.jll.com.

About JLL IndiaJLLisIndia’spremierandlargestprofessionalservicesfirmspecializinginrealestate.Withanextensivegeographicfootprintacross11cities(Ahmedabad,Delhi,Mumbai,Bangalore,Pune,Chennai,Hyderabad,Kolkata,Kochi,ChandigarhandCoimbatore)andastaffstrengthofover6800,thefirmprovidesinvestors,developers,localcorporatesandmultinationalcompanieswithacomprehensiverangeofservicesincludingresearch,analytics,consultancy,transactions,projectanddevelopmentservices,integratedfacilitymanagement,propertyandassetmanagement,sustainability,industrial,capitalmarkets,residential,hotels,healthcare,seniorliving,educationandretailadvisory.

ThefirmwasnamedtheBestPropertyConsultancyinIndia(5StarWinner)attheInternationalPropertyAwards-AsiaPacificfor2012-13.Forfurtherinformation,pleasevisitwww.joneslanglasalle.co.in

JonesLangLaSalle©2014JonesLangLaSalleIP,Inc.Allrightsreserved.Allinformationcontainedhereinisfromsourcesdeemedreliable;however,norepresentationorwarrantyismadetotheaccuracythereof.

Confederation of Indian Industry (CII)TheConfederationofIndianIndustry(CII)workstocreateandsustainanenvironmentconducivetothedevelopmentofIndia,partneringindustry,Government,andcivilsociety,throughadvisoryandconsultativeprocesses.

CIIisanon-government,not-for-profit,industry-ledandindustry-managedorganization,playingaproactiveroleinIndia’sdevelopmentprocess.Foundedin1895,India’spremierbusinessassociationhasover7100members,fromtheprivateaswellaspublicsectors,includingSMEsandMNCs,andanindirectmembershipofover90,000enterprisesfromaround257nationalandregionalsectoralindustrybodies.

With63offices,including9CentresofExcellence,inIndia,and7overseasofficesinAustralia,China,Egypt,France,Singapore,UK,andUSA,aswellasinstitutionalpartnershipswith224counterpartorganizationsin90countries,CIIservesasareferencepointforIndianindustryandtheinternationalbusinesscommunity.Confederation of Indian IndustryTheMantoshSondhiCentre23,InstitutionalArea,LodiRoad,NewDelhi-110003(India)T:911145771000/24629994-7•F:911124626149E:[email protected]•W:www.cii.in