Embed Size (px)

Citation preview

A Comprehensive Overview of the Icelandic Fish Industry

______

A Background Report for a Value Chain Analysis of International Fish Trade and Food Security with an Impact of the Small Scale-Sector

______

Dr. Ögmundur Knútsson Hreiðar Þór Valtýsson

Hörður SævaldssonHelgi GestssonBjarni Eiríksson

The Fisheries Research Science Centre of The University of Akureyri2011

Fisheries Science Centre of The University of Akureyri 2011

ForewordThis report was prepared for the project Value-Chain Analysis of International Fish Trade and Food Security with an Impact Assessment of the Small-Scale Sector, a FAO project supported financially by the Norwegian Agency for Development Cooperation (NORAD).

This report did not receive any financial support and is therefore a direct contribution of the Fisheries Research Science Centre of the University of Akureyri to the project.

The University of Akureyri and its Fisheries Science Research Centre has been a co-operating partner of the United Nations University – Fisheries Training Program (UNU-FTP) since 1999. The main tasks during that time have been to manage the UNU-FTP Company Management and Marketing of Seafood Products course, to supervise UNU-FTP fellows in their writings of their final projects and work with UNU-FTP in organizing and implementing short training courses in developing countries.

The Fisheries Science Centre of the University of Akureyri is hoping that this report can serve as a stepping-stone for further international research projects.

The majority of the information that is presented in this report is converted from www.fisheries.is an information portal about Icelandic Fisheries that was funded by Icelandic government and edited by The Fisheries Science Centre of the University of Akureyri.

Fisheries Science Centre of The University of Akureyri 2011

1 Introduction..............................................................................................................1

2 Fisheries Control and Management.........................................................................1

2.1 The Icelandic exclusive economic zone 12.2 The Quota System 22.3 Individual Transferable Quota (ITQ)2

3 The Fisheries............................................................................................................4

3.1 Total Catch 43.1.1 Structure of the fishing sector....................................................................6

3.1.2 Fishing Gear...............................................................................................8

3.2 Fishing Grounds 93.2.1 Foreign Fleets.............................................................................................9

3.2.2 Global Comparison..................................................................................10

3.3 Aquaculture 114 Fish markets...........................................................................................................12

4.1 Market price vs. price in direct sales 135 Processing Sector...................................................................................................14

Structure of the processing sector 155.1 Processing methods 17

5.1.1 Fresh.........................................................................................................17

5.1.2 Frozen.......................................................................................................18

5.1.3 Salted........................................................................................................18

5.1.4 Dried.........................................................................................................18

5.1.5 Fish Meal And Oil....................................................................................19

6 Markets and export sector......................................................................................19

6.1.1......................................................................................................................20

6.1.2 Europe......................................................................................................20

6.1.3 Asia..........................................................................................................21

6.1.4 America....................................................................................................22

6.1.5 Africa.......................................................................................................23

6.1.6 Oceania.....................................................................................................24

6.2 Structure of the marketing sector 257 Economy................................................................................................................26

7.1 Financial Performance 278 Summary................................................................................................................28

9 References..............................................................................................................30

Fisheries Science Centre of The University of Akureyri 2011

List of Figures

Figure 1. Relative catch and catch value in 2008 for the 9 most important species in the Icelandic fisheries. Source: Statistics Iceland..................................................5

Figure 2. Total catch by major species since 1900 in Icelandic waters and catch of Icelandic vessels in other waters. Source: ICES....................................................6

Figure 3. Changes in the Icelandic fleet from 1992 to 2007. Source: Statistics Iceland.................................................................................................................................7

Figure 4. Total catch of Icelandic boats by major fishing gear since 1992. Source: Statistics Iceland, weight reports...........................................................................8

Figure 5. Iceland and surrounding waters, 200 mile EEZ shown. Map: Google earth..9

Figure 6. Foreign catches in Icelandic waters since 1900, official statistics are not available for all nations until 1906. Source: ICES...............................................10

Figure 7. Total fishery catch of the 16 countries with the highest catch in 2007. Source: FAO........................................................................................................10

Figure 8.Total aquaculture production in Iceland by fish species. Source: Directorate of Fisheries...........................................................................................................11

Figure 9. Total export of Icelandic aquaculture products in volume (left axis) and value (right axis, ISK million at current prize). Source: Statistics Iceland..........12

Figure 10 Relative share of the main species on the Icelandic fish markets. Source. Statistics Iceland..................................................................................................13

Figure 11 Fish market vs. direct sales prices. All prices in €. Source; Statistics Iceland and authors´ calculations......................................................................................14

Figure 12 Export value by processing methods since 1840. Source. Statistics Iceland..............................................................................................................................15

Figure 13 The Number of Icelandic processing companies. Source: Statistics Iceland...............................................................................................................................16

Figure 14 Icelandic export value of fish by processing methods in 2009. Source: Statistics Iceland..................................................................................................17

Figure 15 Icelandic seafood export value by continents in 2009. Source: Statistics Iceland..................................................................................................................19

Figure 16 Icelandic seafood export value for 8 major countries in 2009. Source: Statistics Iceland..................................................................................................20

Figure 17. Icelandic seafood export value by major countries in Europe in 2009. Source: Statistics Iceland.....................................................................................20

Figure 18. Icelandic seafood export value by major countries in Asia in 2009. Source: Statistics Iceland..................................................................................................22

Figure 19. Icelandic seafood export value by major countries in America in 2009. Source: Statistics Iceland.....................................................................................23

Figure 20. Icelandic seafood export value by major countries in Africa in 2009. Source: Statistics Iceland.....................................................................................24

Figure 21. Icelandic seafood export value by major countries in Oceania in 2009. Source: Statistics Iceland.....................................................................................24

Figure 22. Growth of GDP in Iceland since 1945; annual percent changes. Source: Statistics Iceland..................................................................................................26

Figure 23 Average value of the Icelandic króna (right) and net profit in the fishing industry (left). Source: Statistics Iceland.............................................................28

2

Fisheries Science Centre of The University of Akureyri 2011

1 IntroductionFrom the earliest settlements, the fish and the sea have been of major importance for Iceland. It would have been difficult for people to live in Iceland had it not been not for the food supplies that came from the sea (Kristjánsson, 1980). Up until the 19th

century, fishing was supplemented by farming and was practised in rowing boats owned by farmers and mainly operated seasonally according to farming conditions. This form of fishing started as “home fishing” operated from the farms. Later came the establishment of fishing stations closer to the best fishing grounds. In the fishing season, farm workers moved from their farm to the fishing station and stayed there over the season which lasted from the end of January to the beginning of May, during the spawning migrations of cod. This continued until the latter part of the 19th century.

It is surprising how late the Icelandic fish industry started to develop and that the development began because of pressure and influence from foreigners (Snævarr, 1993). The development of the Icelandic fishing industry commenced in 1783 when the Danish King supported experiments in the operation of decked boats in Iceland. It was not until the beginning of the 19th century that Icelanders started to operate their own decked boats in any numbers. From that point on it is possible to talk about an independent fishing industry, operating on a full year basis in Iceland.

Jónsson (1984) split the development of the fishing industry into five periods: 1) rowing boats, 2) sail boats, 3) motorboats and trawlers, 4) innovation trawlers and Swedish boats, and finally 5) the stern trawlers. In addition to those five periods one period is added, processing trawlers, which have been developing over the past two decades or so. It is interesting to see that until the beginning of the 20 th century the majority of improvements and innovations in the Icelandic fishing sector occurred through activities of foreign companies or individuals. It was not until the third decade of the 20th century that Icelanders took the fish industry into their own hands (Snævarr, 1993).

2 Fisheries Control and ManagementFishing management and control can be divided into three important periods: (1) when the Icelandic government increased the Icelandic fisheries’ limits during the period 1952-75, (2) in 1983 when quotas were placed on the catches of the most important species and (3) in 1990, when quotas were put on all species and boats and individual transferable quotas were introduced on all major species.

2.1 The Icelandic exclusive economic zoneAn extension of the fisheries’ jurisdiction started in 1952 when the limits were extended from 3 to 4 miles and from 4 to 12 miles in 1958. In 1972 the Icelandic government decided, unilaterally, to extend the jurisdiction from 12 to 50 miles and again in 1975 from 50 to 200 miles. These extensions were made because of a rapid decline in fish stocks and over-fishing in the fishing grounds around Iceland. Between 1950 and 1974 foreign fishing vessels caught an average of 360,000 tons of demersal species in the sea around Iceland, which is similar to the total demersal catch of the Icelandic fleet (Jónsson, 1984). This foreign fleet was mainly from Britain (about 60%) and West Germany (30%) (Bjarnason, 1996). After each of the four extensions,

1

Fisheries Science Centre of The University of Akureyri 2011

Britain imposed a landing ban on Icelandic ships; West Germany imposed this after the last two extensions. The third conflict in 1972 also had an effect on the Icelandic fish industry; Protocol 6 in the EEC agreement meant that, without reaching a satisfactory agreement with EEC countries, Iceland would not enjoy specific reductions on import duties on fish to EEC countries. This sanction lasted from 1972 to 1976 when Iceland reached an agreement with regard to the 200 mile limit. Since 1976 fishing by foreign ships in Icelandic waters has been very limited and does not play an important role in the total catch.

2.2 The Quota SystemThe next aspect of fishing control that is worth mentioning is the quota system. It was introduced in 1983, with quotas on important species, either in the form of quantities or limitations regarding the number of days that ships could fish each year. Before 1983 a quota system had been introduced in the herring fisheries in 1975 and in 1980 this was extended to the fishing of capelin. The main pressure for introducing the quota system was declining fish stocks; first the collapse of the herring stock and later on the foreseeable collapse of the capelin stock unless preventive measures were adopted. The same can be said about the demersal species before 1983 when the stock had been declining due to over-fishing. Hannesson (1994) has pointed out that the ownership of quotas involves the right to catch the fish but does not entail ownership of the fish stock. Thus, it is claimed that the quota does not mean the ownership of the fish but rather the right to catch the fish.

From the beginning of the quota system, the quota has been bound to the fishing vessels. In the first years, two main systems were active. First there were quantity quotas where the fishing vessels were assigned certain quantities that they could catch. Then there was the fishing effort system that allowed the vessels to fish for a certain number of days during the year. Later the fishing effort system was abolished for all vessels except for boats under 10 tons that could choose between the two systems. In 1995 the Fisheries Management Act was slightly modified so it would also cover boats under 10 tons, which before had been exempt from the quantity quota (Fisheries Association of Iceland, 1996). A separate small boat quota system (isl. krókaaflamarkskerfi) is still available for boats less than 15 GT. These are only allowed to fish with handlines or longlines. These boats get quotas for all the major demersal species and can freely transfer the quota within this system. However to prevent consolidation of fishing rights these quotas cannot be transferred to the common quota system.

In 2009 new system was introduces for small boat called costal fishing (isl. strandveiði). In 2010 total 6000 thousand tones are allocated for coastal fishing one open access base from May to August. Coastal fishing is limited to small boats that are outside the quota system with two handlines and maximum 650 kg catch per day.

By the 1990 Act the fishing year was set from Sept 1 to Aug 31 in the following year but previously it had been based on the calendar year. This was an effort to channel fishing of the groundfish stocks away from the summer months, when quality suffers more quickly and many regular factory workers are on vacation.

2

Fisheries Science Centre of The University of Akureyri 2011

2.3 Individual Transferable Quota (ITQ)The law in relation to fishing was amended in 1990 in order to make the quota system more effective rather than responding to declining fish stocks or over-fishing as almost all law concerning the quota had previously attempted. According to Fisheries Management Act No 38/1990 no one can catch fish inside the Icelandic economic zone without permission from the Ministry of Fisheries, and licences are allocated for one year at a time. Due to this law, all major fisheries inside the Icelandic economic zone operate according to a uniform system with transferable quotas in all species and fisheries. Hence, nearly all fishing vessels have individual transferable quotas (ITQ), allowing ship owners to buy or sell quotas between ships. As has been pointed out earlier, the ITQ grants the right to catch the fish but not the ownership of the fish stock. In that way, the ITQ permits the owners of the fishing vessel to sell the right to catch the fish. However, there are limitations to the transferability of the ITQ that could affect the structure of the fisheries sectors. Firstly it is exclusively owners of fishing vessels with a valid fishing licence that can hold quotas. Secondly, the holders of quotas must catch at least 50% of their quotas every second year to maintain the quota shares. There is also a requirement that within the year, the net transfer of quota from any vessel must not exceed 50%. The third restriction is the geographical restriction to the ITQ system where the local authorities and respective fisheries unions in local geographical regions can block the transfer of annual quotas between regions. On the other hand, annual vessel quotas are freely transferable between fishing vessels within the same region. Runólfsson and Árnason (1996) point out that it is rare in practice, that transfers of quotas between geographical regions are blocked.

In the beginning, the annual quota was issued by the Ministry of Fisheries free of charge. In 1990 this changed in such a way that now the Ministry collects fees for the annual quota to cover the cost of monitoring and enforcing the ITQ system (Runólfsson & Árnason, 1996). The fee only covers a very small amount compared to the price of the quotas on the market.

The Icelandic Parliament passed a new chapter in the Fisheries Management Act in the spring session 2002. This includes a levy on fishing rights allocation and is payable by fishing companies. Fishing rights for the Icelandic fleet within and outside the EEZ have been levied from Sept 1 2004.

The fishing fee each year is based on the total value of landed catch in the period May 1 (previous year) to April 30 (current year) from which major running costs and fishermen's salaries are deducted. Salaries are calculated as being 39.8% of the landed catch value in the period. The cost of oil for the fleet as a whole is calculated on the basis of average cost in 2000 and linked to later changes on the world market. Other running costs are also index linked to the average cost in 2000. From this figure of net landed value, 9.5% will be the total resource fee when fully applied. The total fee is further divided by the corresponding landed volume (landings in cod-equivalents) and this ratio then becomes the resource fee per allocated cod equivalent in the ensuing fishing year. As a preliminary measure, the fee was 6% from September 1 2004, but gradually increased to 9.5% by Sept.1 2009.

In order to prevent undue consolidation of fishing rights by a few fishing companies certain upper limits have been set for the holding of quota shares in major fishable stocks by a fishing company or a group of companies closely linked by ownership.

3

Fisheries Science Centre of The University of Akureyri 2011

The Icelandic fisheries management system has many supporting measures designed for specific fisheries. There are extensive nursery areas permanently closed for fishing. Spawning areas of cod are closed for a few weeks in late winter during the spawning period and the Marine Research Institute has the right of immediate, temporary closure of areas with excess juveniles. There is a 12 mile limit for large trawlers in most areas and there are several selectivity measures, such as a mesh size of 135 mm or equivalent. A sorting grid is mandatory to avoid by-catch of juvenile fish in the shrimp fisheries and devices for excluding juveniles in the groundfish fisheries are also mandatory in certain areas.

The catch rule for cod is also a very important landmark in the precautionary approach to cod stock management. This rule, based on scientific recommendations, was adopted by a government decision and became effective in 1995. It states that the annual TAC for cod is to be set at 25% of the fishable biomass. This implies that the TAC is automatically set after the annual stock assessment. Following the recommendations of the Marine Research Institute, the government decided in July 2007 that the TAC for cod in the fishing year 2007/08 should be set at 20% of the fishable biomass.

There are requirements that small fish, i.e. cod and saithe less than 50 cm and redfish shorter than 33 cm must be kept separate in the catch and must not exceed 10% of the cod, saithe, haddock and redfish catch, the equivalent numbers for haddock are 41 cm and 25%. In compensation, and since this fish has rather low value, it does not count fully in calculations of the vessels' used quota.

There are also strict requirements for the keeping of logbooks on-board all fishing vessels and they must be made available for fishery inspectors. Furthermore, the logbooks are important for scientific assessment purposes.

3 The FisheriesIn the second half of last century, the Icelandic fleet has been constantly modernized for improved efficiency, comfort of the crew and safer working conditions. Fishing gear has also been revolutionized, even though the basic principles of catching fish by hook, gillnet, purse seine or trawl are still the same. Handlines are now worked by computerized jigging reels and the trawl works both for the demersal and the midwater fisheries. Gear devices for improved selectivity of catch have been developed and are increasingly required in many of the fisheries. The captain has the use of the latest instruments for locating his catch and regulating its intake on board.

Few boats use only one gear or target one species. For example, purse seiners catch capelin during part of the year, herring in other seasons and sometimes trawl for shrimp during other parts of the year. Many of the smaller shrimp boats switch seasonally between Danish seine, gillnet, shrimp trawl and longline. Large trawlers fish for cod in one season, Greenland halibut in another, redfish the third and then go for cod or shrimp in distant waters.

Fisheries in Icelandic waters are now characterized by the most sophisticated technological equipment available in this field. This applies to navigational techniques and fish-detection instruments as well as the development of more effective fishing gear. The most significant development in recent years is the increasing size of midwater trawls and, with increasing engine power has improved

4

Fisheries Science Centre of The University of Akureyri 2011

the ability to fish deeper. There have also been substantial improvements with respect to technological aspects of other gears such as bottom trawl, longline, and handline.

3.1 Total CatchTotal catches in Icelandic waters increased from roughly 200,000 tonnes prior to the First World War, to about 700,000 tonnes between the wars. After the Second World War, the catches of demersal species stabilized around this level but total catches increased to 1.5 million tonnes because of the herring fisheries. Then the herring stocks collapsed and the total catches declined again. Production increased again in the late 1970s and has since then fluctuated between 1 and 2 million tonnes annually. These fluctuations are explained by the volatile changes in the size of the capelin stock, which makes up roughly half of the total recent catch.

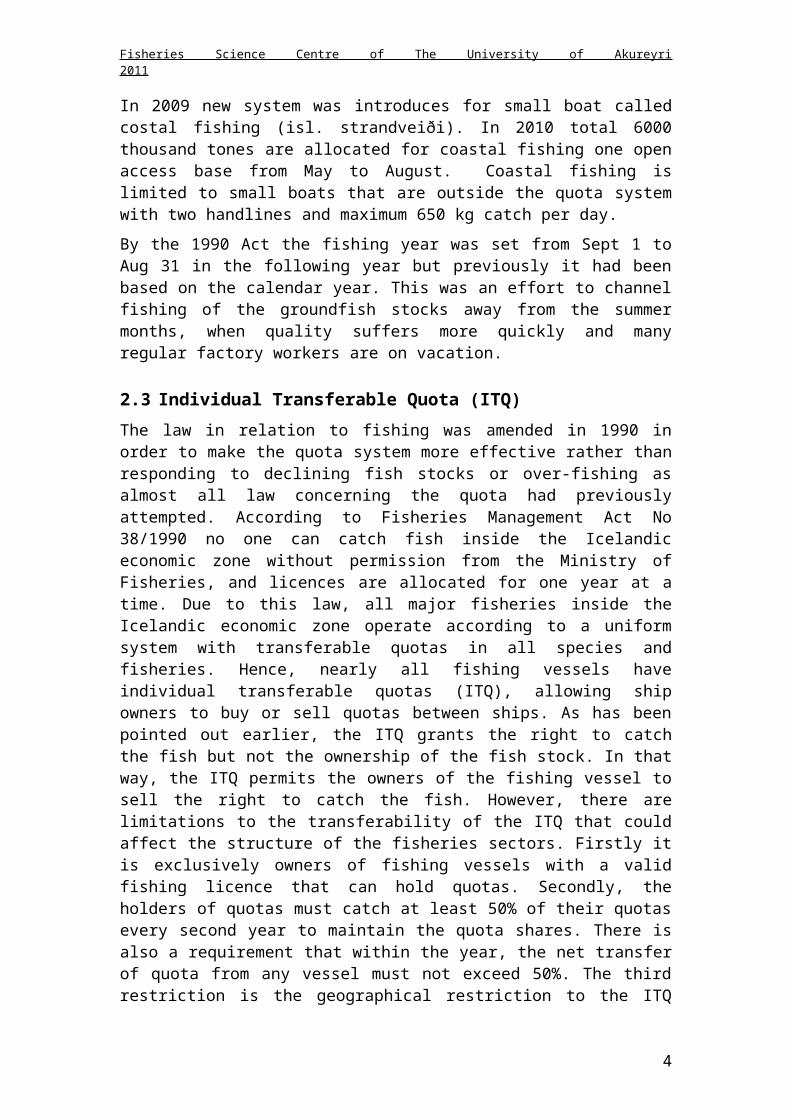

However, high quantity is not the same as high value. Most of the capelin is processed into meal and oil that is of relative low value. The highest value is in the cod catches and only two species, cod and haddock make up more than half the total value of catches in Icelandic waters, although they are combined only about 20% of the total catch (Figure 1).

Figure 1. Relative catch and catch value in 2008 for the 9 most important species in the Icelandic fisheries. Source: Statistics Iceland.

Cod has always been the most important fish in Iceland, accounting for more than half of total demersal catch until the early 1980s (Figure 2). The first Icelandic owned trawler started operating in 1905. At that time the total demersal catch by Icelandic vessels was 53 thousand tonnes but the foreign catches about 130 thousand tonnes after the rapid increase in numbers of foreign trawlers in Icelandic waters. By 1925, 40 Icelandic trawlers were operating, and the total demersal catch had increased almost fourfold to 202 thousand tonnes and the foreign catches were only slightly higher. Catches by the Icelandic fleet decreased during the Great Depression, but increased rapidly during and after WWII, to a peak of 405,000 t in 1960. After the extension of the EEZ to 200 miles, the number of Icelandic trawlers, that were mostly state of the art stern trawlers, increased rapidly to more than 100 vessels. Catches also

5

Fisheries Science Centre of The University of Akureyri 2011

increased; first catches of cod, then until this day followed by other species. However, with the recent decreasing TAC for cod, the relative importance of other species has been rising and in 2006 the cod was only about 36% of the total catch, down from 52% twenty years earlier and 69% forty years earlier.

Figure 2. Total catch by major species since 1900 in Icelandic waters and catch of Icelandic vessels in other waters. Source: ICES

The herring fisheries have also been historically very important for Iceland. They were especially prominent in the 1960s, when nearly 590 thousand tonnes were caught. The herring stocks collapsed in 1967, and catches remained low for a long time. The herring stocks have, however, recovered fully now and catches in Icelandic waters have been around 100 thousand tonnes within the Icelandic EEZ since 1988. After the herring stocks collapsed, the Icelandic purse seiners turned their attention to the capelin, which had been largely ignored before. This fishery increased rapidly to around 1 million tonnes annually. The capelin stock size can, however, fluctuate wildly, since it is short lived and dies after first spawning. Landings from pelagic fisheries are now usually more than half of the total annual catch in Icelandic waters.

Catches of the demersal species are fairly evenly spread over the year, but are still highest during the spring. This is when some major species, most importantly the cod concentrate for the spawning migrations. This used to be the main fishing season. However the fisheries for the pelagic species are highly seasonal. The pelagic fleet is mainly fishing for capelin during its spawning migrations in late winter, then it switches over to blue whiting and then Atlantic-Scandian herring or recently Atlantic mackerel in the summer and Icelandic summer spawning herring in early winter.

3.1.1 Structure of the fishing sector

The Icelandic motor fishing fleet has traditionally been split into 3 groups; trawlers, decked boats, and undecked boats. The decked boat category is by far the most diverse as it ranges from small boats (smaller than many undecked boats) to large purse-seiners and multipurpose vessels. However, the separation of decked boats and trawlers is not very clear since many decked boats can also operate trawls. Many of the decked boats are also structurally similar to stern trawlers, and some of the old

6

Fisheries Science Centre of The University of Akureyri 2011

side trawlers were converted to purse-seiners, which put them into the decked boat class. This classification is in fact a kind of an anachronism from the times when trawlers were much larger than all the other boats. This started to change around 1960 when large purse-seiners began operating. However, Icelandic data sources still separate the boats into these classes.

Of the 40 large and medium sized fisheries companies in the early 1990s, only around half have survived today. The effect of the consolidation on the size and on the number of fishing vessels was great as can be seen in figure 3. The number of large trawlers sank by 44% and the number of vessels with 96% of the catch decreased by 2/3 between 1992 and 2007 (Figure 3). But it is worth noting that the number of small vessels has risen in that period by one-third. This reduction of the fleet resulted in a 33% reduction in manpower employed at sea (Knútsson, Klemenson, & Gestsson, 2008).

0

200

400

600

800

1000

1200

1400

1600

1800

2000

1992 1999 2001 2002 2003 2004 2005 2006 2007

Total number of vessels

Number of small vessels

Number of traw lers

Number of vessels w ith 96% of quota/catch

Figure 3. Changes in the Icelandic fleet from 1992 to 2007. Source: Statistics Iceland.

Simultaneously, as an integral part of the consolidation, a large scale concentration of quota holdings took place. In 2007, the 50 largest quota owners had 82% of the total quota in all species but 60% in 1995. The quota concentration is most pronounced in the class of 5 and 10 largest quota owners as the 5 largest have 34% of the quota in 2007 but 17% in 1995. The same development of concentration can be seen among the 10 largest as they had 51% of the quota in 2007 but only 26% in 1995 (Statistics Iceland, 2008). These consolidation and rationalisation measures have resulted in eliminating the largest part of the overcapacity of the fleet although it is to be assumed that overcapacity is still prevailing in the fleet of small vessels.

The large scale consolidation of the fisheries companies in the last 8-10 years is probably the most important effect of the changes in the macro-environment of the fisheries sector. Undoubtedly, the implementation of the ITQ system contributed largely and facilitated this consolidation. But other influences had their impacts, mainly the surge of the larger fisheries to be publicly listed companies, mainly in the years 1997-2002, which aided greatly the necessary financing of M&A. For a long time, the size of the fishing fleet had been considerably over the optimal capacity. To decrease the overcapacity became increasingly urgent as the TACs of the most important demersal species were reduced. This was even more important as the

7

Fisheries Science Centre of The University of Akureyri 2011

financial performance of the demersal fleet was totally unacceptable. Of the 20 publicly listed fisheries companies (all but three were vertically integrated companies) in 1999, only nine have survived. The rest were merged with other companies (Einarsson, 2003, pp. 41-52).

The total number of fishing vessels at the end of the year 2010 was 1,625. Trawlers counted 57 of these with a combined size of 65,087 GT, decked vessels were 761 with a combined size of 83,457 GT and undecked boats were 807 with a combined size of 3,857 GT. The number of boats in all categories declined from previous year excepting number of undeck boat that increased by 51 in number from 2009 and the total size by 242 GT. In 2009 about 42% of the total catch value was landed by trawlers, just over 1% by the small undecked boats and 57% by other vessels of varying sizes and capacities. These numbers only apply to boats that have licenses to fish in Icelandic waters (Statistics Iceland, 2010).

3.1.2 Fishing Gear

The Icelandic fishing fleet is technologically advanced and uses a variety of fishing techniques and gears. The range of fishing gears include handline, longline, gillnet, bottom trawl and Danish seine for groundfish and flatfish. Purse seine and pelagic (or midwater) trawl for pelagics and various types of dredges and trawls for invertebrates.

Purse seines and quite recently, pelagic trawls catch the highest amounts as they are fishing for a few but very abundant pelagic fish species. This catch is usually around 2/3 of the total catch. However, this is not reflected in the value of the catch as the value of pelagics is low compared with groundfish. The fishing gear that catches the highest value is the bottom trawl with 40%-50% of the value of the total catch. The second most valuable catch is from longlines. With the exception of lobster, fisheries for invertebrates are quite low in both value and catch amount. However, valuable scallop and especially shrimp fisheries have recently collapsed or declined due to environmental factors (Figure 4).

Figure 4. Total catch of Icelandic boats by major fishing gear since 1992. Source: Statistics Iceland, weight reports

8

Fisheries Science Centre of The University of Akureyri 2011

3.2 Fishing GroundsIceland's exclusive fisheries zone has an area of 760,000 square kilometres, seven times the area of Iceland itself (Figure 5). Some of the largest fish stocks in the North Atlantic are found in Icelandic waters, including the cod stock, which is Iceland's most important stock, and the capelin stock, which is generally the largest in size. Other large stocks migrate in and out of Icelandic waters, including the Atlanto-Scandian herring stock, blue whiting and Atlantic mackerel, while still others are mostly close to the 200-mile limit, such as the oceanic redfish stock.

Figure 5. Iceland and surrounding waters, 200 mile EEZ shown. Map: Google earth.

Looking at Iceland's northerly position on the map, one would expect the ocean around it to be icy cold, so that very little production of phytoplankton could take place to become the basis for the food chain. One would expect the ocean to be rather lifeless. The fact is, however, quite the contrary because the ocean around Iceland is teeming with life. The explanation lies in the system of ocean currents around the country. As the warm North Atlantic drift approaching from the southwest meets the polar current from the north, a huge upwelling of nutrients takes place from the deeper layers to the surface. The nutrients feed microscopic life in the surface layers, notably phytoplankton and zooplankton and thus the ocean's entire food web. The North Atlantic drift warms the ocean south of Iceland and flows north along the west coast and east along the north coast. It meets the polar current off the north and west coasts and also in the southeast.

3.2.1 Foreign Fleets

The first references to distant water fisheries in Icelandic waters are those of English boats fishing for cod in 1412. They became quite numerous in the 15th century but declined in numbers after that. After the decline of the English Fleet, boats from the Netherlands became the most numerous distant water fleet in Icelandic waters later replaced by French boats from Brittany and Flanders from the early 19th century, until the return of the British fleet, now with trawlers in the late 19 th century. During the 20th century until the extension of the EEZ to 200 miles the British fleet was the largest foreign fleet in Icelandic waters (Figure 6).

9

Fisheries Science Centre of The University of Akureyri 2011

Figure 6. Foreign catches in Icelandic waters since 1900, official statistics are not available for all nations until 1906. Source: ICES

The current distant water fleets fishing in Icelandic waters are: Norwegian and Faroese longliners fishing for groundfish; Norwegian, Faroese and Greenlandic purse-seiners fishing for capelin and herring; and Greenlandic and European Union trawlers fishing for redfish. Furthermore, Russian and European herring boats and Faroese boats fishing for blue whiting are allowed to fish up to a certain amount in Icelandic waters depending on annual agreements on the trans-boundary stocks.

3.2.2 Global Comparison

Few nations in the world are as dependent on fisheries as Iceland if one considers the size of population. Although Iceland is among the smallest nations of the world, with a population of slightly more than 300 thousand people, it is nevertheless among the world’s largest fishing nations (Figure 7).

Figure 7. Total fishery catch of the 16 countries with the highest catch in 2007. Source: FAO.

10

Fisheries Science Centre of The University of Akureyri 2011

In 2007, Iceland ranked 16th on a global scale. This is around average for Iceland, as it has been ranking from the 10th to the 21st high place since 1950.

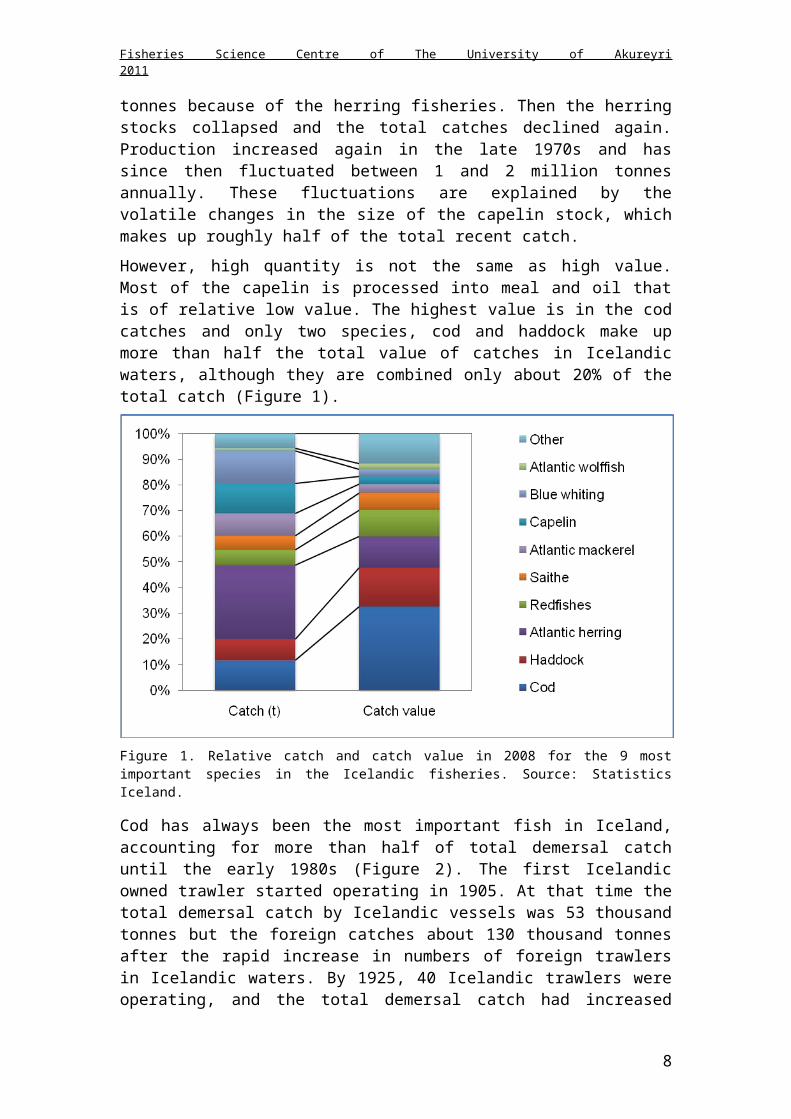

3.3 AquacultureAlthough Iceland is one of the leading fishing nations in the world, the same does not apply for aquaculture. Real commercial sized aquaculture began only around 1985 with first attempts at salmon (Salmo salar) farming (Gunnarsson, 2011a). In 1990, after a large- scale build-up, the production reached about 3,000 t and was at that level for more than 10 years. The salmon farming in Iceland did therefore not grow to anywhere near the same levels as the Norwegian salmon farming, conducted at similar latitudes. The second phase of salmon farming began in 2004 when production was doubled. This subsequently collapsed in 2007 and salmon farming has been on a very low scale since (Figure 8). However, one salmon farming sector is thriving, selective breeding and exporting of eggs and juveniles.

Figure 8.Total aquaculture production in Iceland by fish species. Source: Directorate of Fisheries

The development of Arctic char (Salvelinus alpinus) farming has developed quite differently. Faming began at about the same time as salmon farming but was on a very low scale. The growth has subsequently been slow but steady so in the recent years there has been more Arctic char production in Iceland than for all other aquaculture species together. Furthermore Iceland is the largest producer of Arctic char in the world. Arctic char farming can therefore be classified as a success. It has to be mentioned that that along with increased production a strong marketing campaign was conducted to boost sales and prises.

Iceland has experimented in cod farming since 1992 (Gunnarsson, 2011). The growth of this sector has been slow but steady. On-growing of wild caught fish has proven to be feasible and most of the production is from on-growing. Farmed juveniles are also produced in experimental stations, but have not yet proven to be economically feasible on a large scale.

Several other species have been experimented with, but most are minor in comparison with the species above. Some success has been reached with Atlantic halibut farming,

11

Fisheries Science Centre of The University of Akureyri 2011

but production tonnage values are low since it is mostly exported for on-growing as small juveniles. Other species still at experimental stages or grown on very small scale are turbot (Scopthalmus maximus), blue mussel (Mytilus edulis), tilapia (Oreochromis niloticus), and rainbow trout (Oncorhynchus gairdneri).

The highest annual aquaculture production year was 2006, with about 5,000 t exported and about 2,000 million ISK in value (Figure 9). This dropped the subsequent year, due to sharply reduced salmon production, but has grown again to previous levels partly due to successful marketing of Arctic char and partly because of favourable exchange rate for the ISK. The largest marked for Icelandic aquaculture products are the United States, where large part of the Arctic char products are exported. Halibut juveniles are mostly exported for on-growing to Norway and salmon eggs and juveniles to Chile (Gunnarsson, 2011).

Figure 9. Total export of Icelandic aquaculture products in volume (left axis) and value (right axis, ISK million at current prize). Source: Statistics Iceland

4 Fish marketsA great enabler of the structural changes in the Icelandic fish industry was the establishment of fish markets in Iceland. The first fish markets started in 1987 when the official price regulation on wet fish was partially uplifted. The turnover in volume increased rapidly from 22 thousand tonnes at the beginning up to the maximum of 115 thousand tonnes in 1996. In the last 8 years or from year 2000 the yearly average turnover has been around 100 thousand tonnes or about one-fifth of the demersal catch every year. Cod and haddock has always been the most prominent species at the auction markets, in 2001 cod was 44% (18% of total landed cod) of the auctioned volume and haddock 14% (35% of landed haddock). The composition of species has changed in recent years as the availability of cod has gone down due to lower TAC and risen in haddock. In 2007 the volume of cod had fallen to 28% (16% of total catch of cod) of the total of traded volume but haddock was up to 29% (26% of the catch) (Reiknistofa fiskmarkaða, 2008). The emergence of fish markets in Iceland has had a profound impact on availability of fish for the non-vertically integrated fish processors. Fish markets have also strengthened the market power of the fishermen as

12

Fisheries Science Centre of The University of Akureyri 2011

market based price formation has resulted in higher prices for them (Einarsson, 2003, pp. 41-52). It is evident from the rapid growth of the fish markets in the first four years of operation, that it was a great need for a market-based exchange of fish. In the first four years, the traded volume increased from 22.000 tons to 95.000 tonnes and in the first five years the volume came up to 100.000 tons. In the last 20 years the volume has been on average 100.000 tons slightly falling since 2000. The composition of species on the fish markets has seen considerable changes in recent years. Cod has been the most important specie on the markets both in volume and in value, but has in the last 10 years its importance decreased from nearly half of the total volume in 2000-2002 to around one-third in 2009 (Figure 10). The importance of haddock has in the same time increased from one-fifth to one-third of the total supply in volume terms.

0%

10%

20%

30%

40%

50%

Cod Haddock Saithe Catfish Other species

Relative share of the main species on the fish markets

2000-2009 2000-2004 2005-2009

Figure 10 Relative share of the main species on the Icelandic fish markets. Source. Statistics Iceland

This indicates that haddock has to some extent replaced or substituted cod as the general supply of haddock has greatly increased in recent years due to much larger TAC in haddock at the same time that the TAC of cod was cut drastically. Besides that, haddock is a natural near-substitute for cod on the main consumer markets. Other species have kept their share relatively unchanged in the last 10 years.

4.1 Market price vs. price in direct salesFrom the beginning of the fish markets in Iceland there has been a significant difference in prices between the domestic fish market prices and the price of fish in direct sales (internal transfer pricing sales). This should not come as a surprise as the price formation is fundamentally different between these two allocations. On one hand is basically an internal pricing, regulated by the semi-official Bureau of Ex-vessel Fish Prices, where the set-price is changed according to changes in the market price sometimes with a considerable delay. This price is not used in any transactions other than calculating the vessel crews´ wages (based on a share system). It is to

13

Fisheries Science Centre of The University of Akureyri 2011

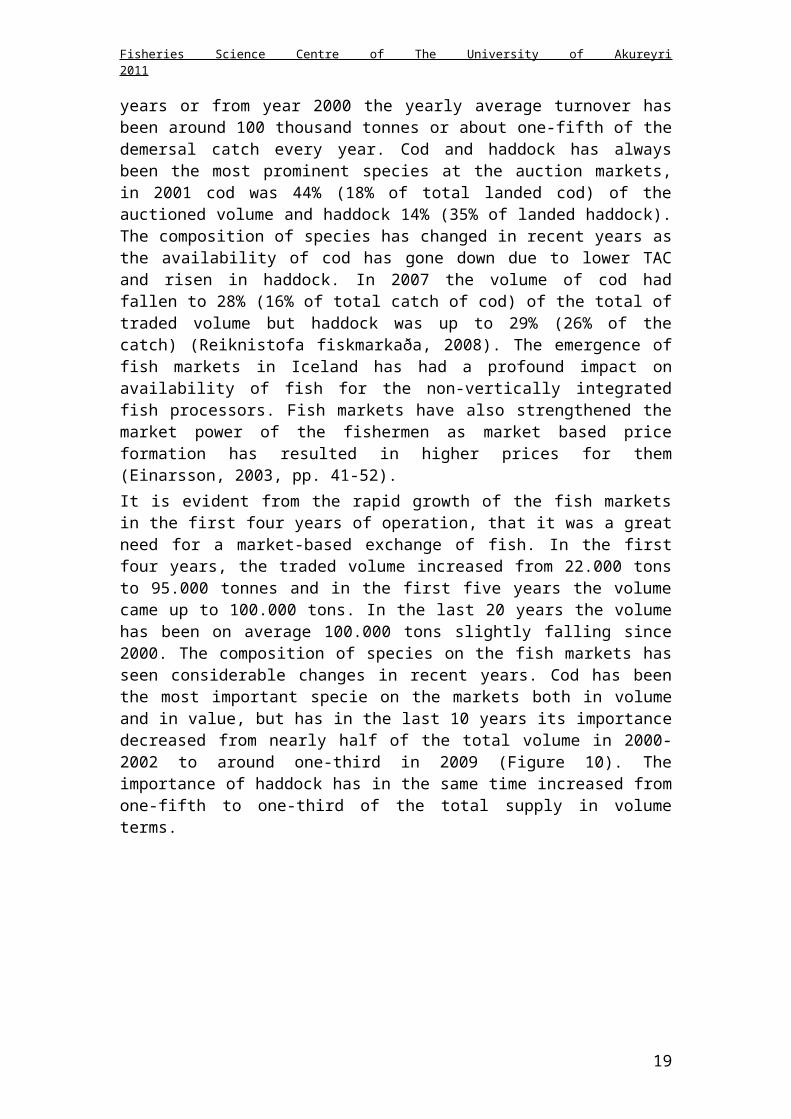

assume that important cost factors are not included such as direct or indirect costs of quota (leasing or buying). Other cost factors like handling, grading, logistics and other services are included in the fish market price but not in the direct sales price. It is also to assume that buyers on the fish markets are ready to pay higher price for fish in the right quantity and quality according to their stringiest demand. To what extent these differences can explain the price difference is hard to say but in general it is evident that it is not straight forward to compare these prices as they are decided in a fundamentally different way (Figure 11).

20%

30%

40%

50%

60%

70%

0,5

1,0

1,5

2,0

2,5

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Fish market price vs. directs sales price in €

Price diff. (r-axis) Direct sales (l-axis) Fish market price (l-axis)

Figure 11 Fish market vs. direct sales prices. All prices in €. Source; Statistics Iceland and authors´ calculations

It can be argued on ground of economic theory that the auction as a method of exchange does affect the relative power of the buyers and sellers. In the case of the auction mechanism, it is obvious the number of buyers is much greater than in other mechanism of exchange and this will tilt the price setting to the favour of the sellers overview see (Trondsen, 2001). In other words, the auction price will generally tend to be higher than a contractual price or the internal price used by the VICs (sale and purchasing of landings within the same organization).

5 Processing SectorIn the past, the main aim of most processing methods was to expand the lifetime of the fish products so it could be kept edible under the primitive conditions of that time. Salting and drying were basically the only methods available for this but both involved considerable risk. Salt was expensive and drying depended on favourable weather conditions.

Developments in fish processing have principally followed the development of the fishing sector. Fish processing was connected with the boat owners, usually farmers, who processed their own catch. With the emergence of bigger boats and independent boat owners (who were not farmers), operation on a whole year basis started around the middle of the 19th century. From this time on it is possible to talk about a

14

Fisheries Science Centre of The University of Akureyri 2011

significant fishing industry in Iceland, both in terms of fishing and production. However, it was not until around 1930 that individual processing companies appeared that were not bound to the operation of fishing vessels (Jónsson, 1984). From that time onwards an independent fish processing industry has become a reality, although the link between fishing and processing is obvious. Today, most of the processing companies operate their own fishing vessels to secure supplies for their production.

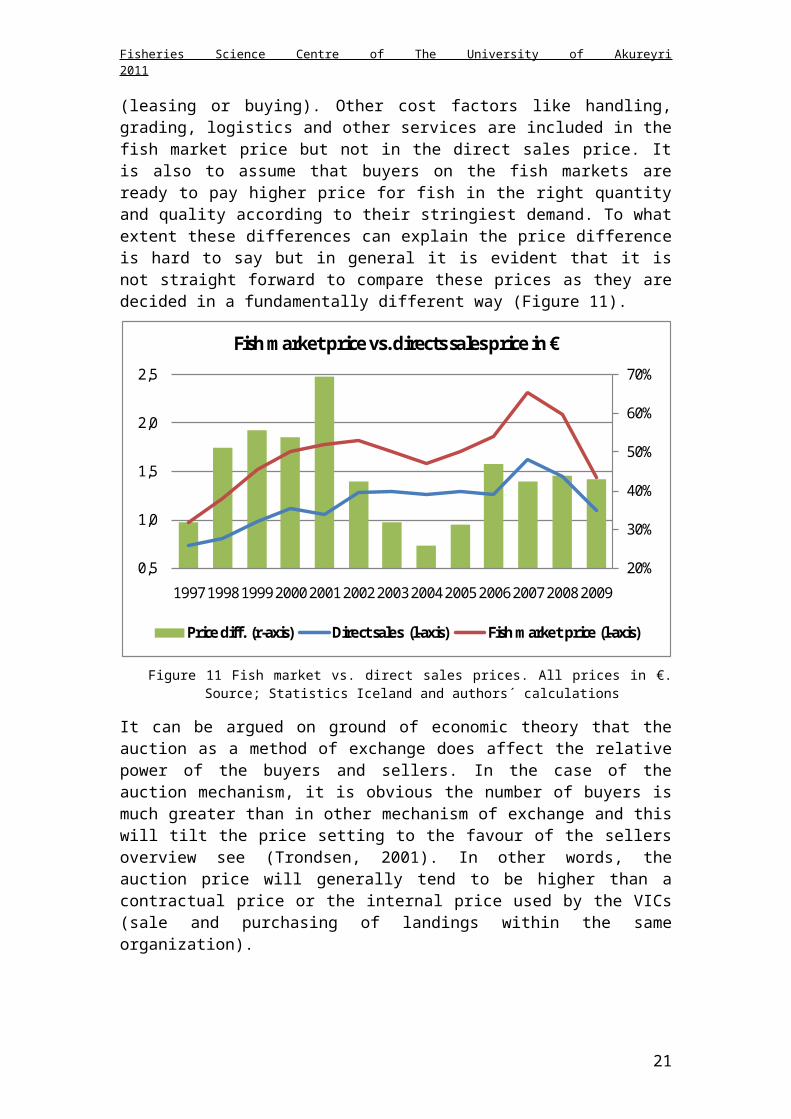

The oldest fish processing method in Iceland was to dry the fish to make the so-called stockfish. In the middle of the 19th century salting took over as the main processing method, until the closing of the main market in Spain during the Civil War in the mid 1930s. After that, sales of fresh unprocessed fish increased considerably, especially to Britain during the Second World War.

Figure 12 Export value by processing methods since 1840. Source. Statistics Iceland

Between 1930 and 1950 freezing took over as the main processing method in the industry, and has kept that position ever since although fresh processed fish have increased its portion again in the last decade (Figure 12).

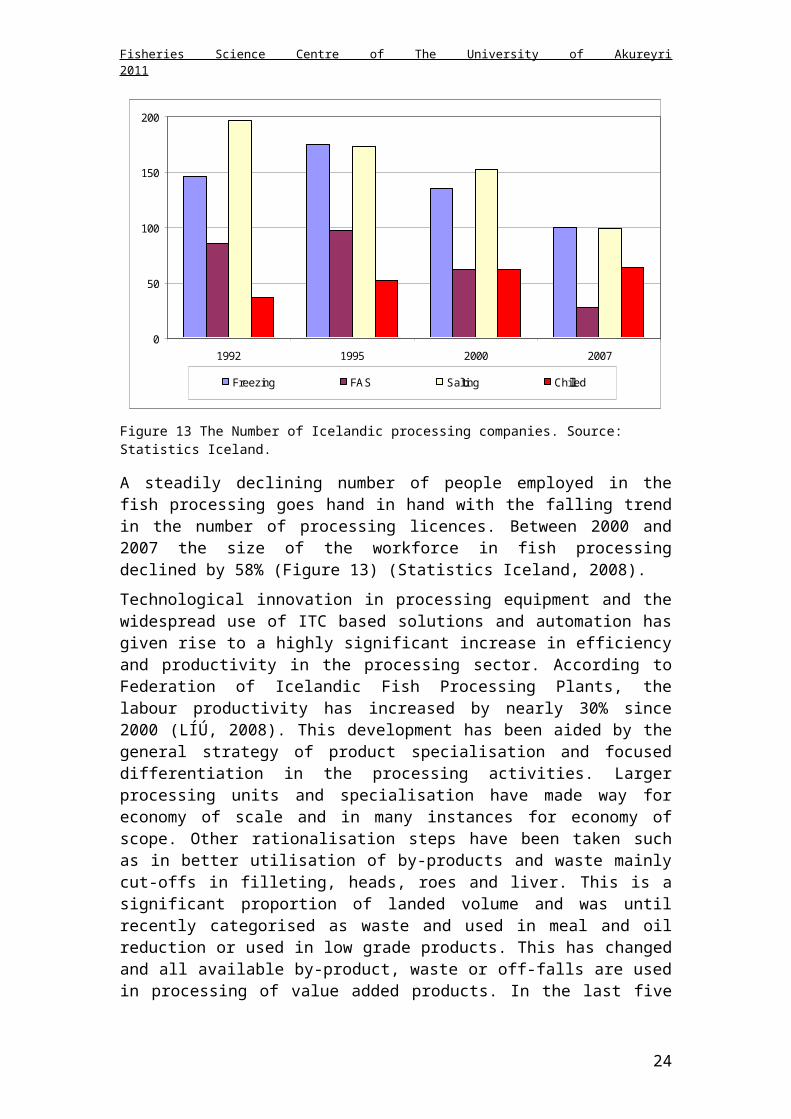

Structure of the processing sectorThe consolidation within the fisheries sector did not only affect the size of the fleet and concentration of the quota ownership, but also had the same effect on the processing sector. The most illustrious way is to look at the development of the official processing licences. In the beginning of ´90s there were slightly over 400 licences active but in 2007 the total number of processing licences had gone down by 32% The largest decrease in processing licences is in freezing at sea (FAS) due to a much lower number of operators and the large increase in processing capacity on each vessel. The exemption from the general trend of decreasing number of processors is the growing number of producers of chilled fish products as can be seen in from figure 14.

15

Fisheries Science Centre of The University of Akureyri 2011

0

50

100

150

200

1992 1995 2000 2007

Freezing FAS Salting Chilled

Figure 13 The Number of Icelandic processing companies. Source: Statistics Iceland.

A steadily declining number of people employed in the fish processing goes hand in hand with the falling trend in the number of processing licences. Between 2000 and 2007 the size of the workforce in fish processing declined by 58% (Figure 13) (Statistics Iceland, 2008).

Technological innovation in processing equipment and the widespread use of ITC based solutions and automation has given rise to a highly significant increase in efficiency and productivity in the processing sector. According to Federation of Icelandic Fish Processing Plants, the labour productivity has increased by nearly 30% since 2000 (LÍÚ, 2008). This development has been aided by the general strategy of product specialisation and focused differentiation in the processing activities. Larger processing units and specialisation have made way for economy of scale and in many instances for economy of scope. Other rationalisation steps have been taken such as in better utilisation of by-products and waste mainly cut-offs in filleting, heads, roes and liver. This is a significant proportion of landed volume and was until recently categorised as waste and used in meal and oil reduction or used in low grade products. This has changed and all available by-product, waste or off-falls are used in processing of value added products. In the last five years the processed amount of by-products account for 8-10% of landed volume of cod, haddock and saithe. This has contributed heavily to higher productivity of input and higher average product margin (Knútsson et al., 2008)

Traditionally, nearly all demersal wet fish was allocated to freezing, salting or iced whole for export. This changed with the emergence of freezing trawlers in the 1980s. Since mid 1990s, around one-third of wet fish has been frozen at sea but land based freezing fell from 45% in 1990 to about 30% on average (Knútsson & Gestsson, 2006). These changes in processing of demersal fish in Iceland occur in the allocation to salting that was increased temporally to 25% in 1996-2000 but has fallen to 16% in the recent years. The only significant change since mid 1990s has been the rapid and parallel increase in allocation to chilled products to 12% in 2007. Since 2005, around quarter of wet fish has been allocated to chilled and iced fish products. Chilled

16

Fisheries Science Centre of The University of Akureyri 2011

products are now the second most important category of processed demersals in Iceland or 26% in value in 2007 (Statistics Iceland, 2008).

5.1 Processing methodsProcessing methods for fish in Iceland can in the simplest terms be split into eight main groups: 1) frozen, 2) fresh (processed) 3) fresh (whole), 4) salted, 5) meal, 6) oil, 7) dried, and 8) other (canned, pickled, smoked etc.,). As can been seen in figure 15 frozen products are the most valuable followed by fresh whole fish and fresh processed. The increase in value from 2008 can mainly be traced to changes in the currency rate of the Icelandic króna (ISK) (Figure 14).

Figure 14 Icelandic export value of fish by processing methods in 2009. Source: Statistics Iceland.

5.1.1 Fresh

Fresh products have always been a significant part of the Icelandic processing sector and have in fact increased in relative value recently. In previous decades fresh fish export was mainly from trawlers that landed the catch in markets in Europe instead of directly in Iceland. This has changed significantly in two respects. Fresh whole fish is rarely landed directly in Europe these days. Instead the catch landed in Iceland, transferred directly to cargo ships that transport it to markets in Europe where it is processed further. A significant part of the flatfish, catfish and haddock catch is disposed in this way.

More modern and efficient transport methods by ship or air, coupled with increased fish prices have also made it possible to export fillets and other processed products directly to markets in Europe by air or ship. These are among the highest paying customers of Icelandic fish products, appreciating the high quality of the fresh caught fish and guaranteed supply. The main species exported in this way are catfish, monkfish, haddock and cod (Matís, 2011a).

The markets for fresh products are primarily in Western Europe as it is conveniently close. A significant proportion of the Arctic char production is also air freighted to North America.

17

Fisheries Science Centre of The University of Akureyri 2011

5.1.2 Frozen

Land based freezing began in Iceland around 1930 and became the most important processing sector after the Second World War with around 50% of the export value. Although production of fresh products has increased lately the frozen products will likely continue to dominate the export market as storing and logistics of quick frozen products is easier in most respects. Continuous improvements in handling and storing have also contributed to its continuing success (Matís, 2011b).

The catch is both frozen in land based factories all around the country and at sea on highly automated freezing trawlers. A significant part of the cod, saithe, haddock and redfish catch is frozen at sea and almost all the Greenland halibut. Recently the pelagic fleet has been modernized with larger and more powerful boats which has made is possible to process and freeze a large part of the herring and mackerel catch at sea.

Land based freezing plants process all possible types of fish and invertebrates but the bulk is from cod, saithe and haddock. Currently most of the invertebrate catch is also processed in land based freezing plants.

Markets for frozen products are all around the world as the storage method does not set limits to shelf life during transport as opposed to the fresh products. Frozen at sea products from Greenland halibut, redfish and capelin are especially popular in the Far East but traditional markets for codfishes (both frozen at sea and on land) are in Western Europe and North America. Shrimp is primarily exported to the UK and nephrops lobster to Spain.

5.1.3 Salted

Salting became the most important methods in Iceland to preserve the fish in the 18 th

century and was until the Second World War more than 60% of the export value of fish products from Iceland. The most important products at that time were bacalao (salted cod) for Mediterranean markets and salted herring for Northern and Eastern European markets. During the war most of the catch was sold fresh to the UK but after the war freezing had taken over as the most important preserving method for the Icelandic catch. However, important markets for salted cod were retained, primarily in Spain and Portugal contribution to about 20% of the export value of marine products in recent years. In these countries the bacalao from Icelandic is of high esteem and used in many traditional dishes. Smaller markets for bacalao are also in other catholic countries such as Italy, France and Latin America. Currently a significant part of the cod, saithe, ling and tusk catch is salted in saltfish plants all around the country (Matís, 2011c).

Salted herring was quite an important export product until the collapse of the herring stocks around 1968. However, after the stocks were rebuilt only a small percentage has been salted, most of the catch is frozen at sea or processed into oil and meal.

5.1.4 Dried

Drying is the oldest method of preserving fish in Iceland and was for centuries the only method for storing fish for export. The fish was air dried on racks or simply on exposed rocks. This gives a storage life for years. This is still commonly used, although modern methods use geothermal heat to dry it faster.

18

Fisheries Science Centre of The University of Akureyri 2011

There are two main markets for dried products, quite far apart. Dried cod, haddock or catfish are a popular and healthy snack in Iceland. Dried codfishes are also popular dishes in West Africa and as a consequence Nigeria is one of the largest importers of Icelandic fish products.

5.1.5 Fish Meal And Oil

During the latter part of the 19th century oil from Greenland shark was one of the most important export product from Iceland. This marked declined during the early 20 th

century due to cheaper and more easily available crude oil. The second phase of fish oil production began in the interwar period when fish meal factories began operating, mainly processing herring at that time. Currently fish meal is primarily produced from the abundant pelagic species, such as herring, capelin and blue whiting as well as from offals from groundfish fisheries. The total value of fish meal and oil is around 10% of total fish exports. The amount reduced has declined considerably in recent years due to lower quotas but very high international prices for fish meal and oil have kept the total value of this product level.

Fish meal and oil is primarily used as feed for domestic animals and fish feed in aquaculture. As a consequence the largest buyer of meal and oil from Iceland is Norway, where it is used to feed salmon.

6 Markets and export sectorThe Icelandic seafood industry currently exports products for about 209 billion Icelandic krónur (ISK), roughly equal to 1.7 billion US dollars or 1.2 billion Euros in 2009 (Figure 15). As can be seen from figure 16 the majority are exported to Europe.

Figure 15 Icelandic seafood export value by continents in 2009. Source: Statistics Iceland.

A considerable share is also exported to other European countries, America, Asia and Africa. Icelandic products are known for their high quality and have a tradition on these markets.

19

Fisheries Science Centre of The University of Akureyri 2011

The most important export countries are the United Kingdom, Norway and Spain. A considerable share is also exported to other European countries (Figure 16).

Figure 16 Icelandic seafood export value for 8 major countries in 2009. Source: Statistics Iceland.

It is interesting to see that Nigeria is bigger in import in value that USA that once was the most important markets for Icelandic fish.

6.1.1

6.1.2 Europe

Export of seafood to Europe has been increasing the past few years; the aggregate Icelandic seafood export originated to Europe grew from 77% in 2002 to 83% in 2009. The current export value to Europe is around 172 billion ISK (EUR 1.0 billion / USD 1.4 billion) (Figure 17).

Figure 17. Icelandic seafood export value by major countries in Europe in 2009. Source: Statistics Iceland.

20

Fisheries Science Centre of The University of Akureyri 2011

Besides UK’s status as the largest importer of Icelandic fish, Spain has a very strong tradition of consumption of salted cod; the bacalao. The same applies to Portugal and to a lesser extent to other Southern European countries, where salted fish from Iceland is considered a delicacy.

Western European coastal states, such as the Netherlands, Germany, France and Denmark have through history also been important markets for Icelandic seafood products, mainly fresh or frozen.

The bulk of the export to Europe consists of demersal species and their proportion has grown quite fast in the past few years. A large and rather stable part of this export, however, is comprised of pelagic species, such as capelin and herring, and a significant but declining ratio originates from invertebrates; mainly northern shrimp and nephrops lobster.

Flatfishes, such as plaice and lemon sole, are popular in many western European countries, especially in the UK, the Netherlands and Denmark.

Interesting markets for pelagic species exist throughout Europe. Many European countries have gone through their ”herring periods”, and have subsequently learnt to appreciate this fish and developed their own ways of pickling, salting or smoking the herring. A particularly large market for herring products exists in the Eastern European countries. These markets declined considerably after the collapse of the former Soviet Union. Recently, but have been increasing again lately; either as whole frozen (capelin) or frozen fillets (herring).

Markets for fishmeal products from the pelagic species are primarily in Norway, the UK and Denmark. The meal is included in feeds for land animals as well as for aquaculture feeds; the market for fish oil is mainly in Norway.

Most of the exports to Europe are frozen; either on board the processing vessel or in processing plants ashore. The fundamental markets for frozen products have been; The UK with cod and haddock (for the traditional British dish; fish and chips) and Germany with frozen redfish and saithe. These markets have been remarkably stable through history, including recent years.

6.1.3 Asia

The Asian market has been largely stable recently after a prolonged period of increase in the 1990s; the market is relatively new for Icelandic seafood products. In recent years, the export value has been around 8 to 15 billion ISK, or EUR 85 to 95 million. This is around 7% of the aggregate Icelandic export value of seafood products. The current export value to Asia is around 14.8 billion ISK (EUR 85 million / USD 117 million) (Figure 18).

21

Fisheries Science Centre of The University of Akureyri 2011

Figure 18. Icelandic seafood export value by major countries in Asia in 2009. Source: Statistics Iceland.

The largest single market in Asia has always been Japan, but China has been rising in importance lately. Exports to Taiwan have also increased considerably, while South Korea has declined.

Products exported to Asia are diverse, as this part of the world is known to appreciate and experiment with exotic food from the ocean. Products from demersal species have the largest share, but a large proportion of the exports are also flatfishes and pelagic species. There used to be an extensive market in Japan for large quality whole frozen shrimp, but this has declined with falling shrimp catches in Icelandic waters.

6.1.4 America

North America has, since the end of World War II, been a major market for seafood products from Iceland. However, In recent years the importance of this market has declined considerably, or from around 15% of Iceland’s total marine exports to 5% in 2009. The current export value to America is around 10.6 billion ISK (EUR 61 million / USD 83 million) (Figure 19).

22

Fisheries Science Centre of The University of Akureyri 2011

Figure 19. Icelandic seafood export value by major countries in America in 2009. Source: Statistics Iceland.

The marked for frozen fillets in the USA was developed in the early 1940s, and from that time onwards, the Icelandic processing industry was restructured. It changed, to a large extent, from the traditional salting of demersal products to freezing them. Freezing began in the interwar period but was on a low scale until the fishing industry was modernized after the Second World War. Also, conflicts with European nations over the gradual extension of the Icelandic EEZ contributed greatly to the increasing importance of the American market.

The largest share of exports to America goes to the United States. The majority of products exported to America, originate from demersal species; historically, mainly cod. Over the last few years, the export of cod products has declined considerably, whereas cod status has largely been replaced by haddock and saithe. Some capelin where also exported to America but it is negligible now.

6.1.5 Africa

Somewhat surprisingly, a longstanding and traditional market for Icelandic fish products exists in Africa; Nigeria being almost the sole importer. The value of exports to Nigeria has, in fact, increased in the last years from about 3.1 billion ISK (EUR 35 million) to the current level of 10.2 billion ISK (EUR 59 million / USD 80 million), making Nigeria one of the 10 largest buyers of Icelandic seafood products. Currently about 5% of Iceland’s aggregate seafood exports goes to Nigeria (Figure 20).

Nigerians have for a long time, although occasionally interrupted by civil unrest, been avid buyers of Icelandic stockfish; dried cod. In recent years, exports of dried products from other codfishes such as haddock and saithe have increased as well. The general growth in exports to Nigeria in recent years can largely be explained by these two aforementioned species.

23

Fisheries Science Centre of The University of Akureyri 2011

Figure 20. Icelandic seafood export value by major countries in Africa in 2009. Source: Statistics Iceland.

6.1.6 Oceania

Due to distances and small markets in Oceania and strong traditions of their own fisheries, the markets for Icelandic seafood products in Oceania are negligible. The total value has been in the range of 50 to 600 million ISK (EUR 0.6 to 3.5 million), compared to similar amounts in billions in the other markets. Only about 0.1% to 0.3% of total seafood exports from Iceland end up in Oceania, at the other side of the world (Figure 21).

The exports have been exclusively to Australia, except in recent years a significant quantity has been exported to New Zealand. The export is almost exclusively fish oil and roe (salted) from demersal species.

Figure 21. Icelandic seafood export value by major countries in Oceania in 2009. Source: Statistics Iceland.

24

Fisheries Science Centre of The University of Akureyri 2011

6.2 Structure of the marketing sector The exporting of fish products were since the 1930´s regulated by an official export licensing system. The three large producers organisations (Icelandic Freezing Plants (IFPC), Iceland Seafood (IS) and Union of Icelandic Fish Producers (UIFP)), which were producers co-operatives held a quasi monopoly of exporting of frozen and salted products as they had virtually an unlimited export licenses from the authorities. These marketing and sales organisations (MSOs) had the great majority of processors as members of their organisations and by contractual agreements; they were obliged to sell all their products through these organisations. In effect, these three exporting organisations, two in frozen products and one in salted products, exerted a huge power over the harvesting and processing sectors in their heydays. The export licensing system was gradually uplifted from 1987 and the last remains were uplifted in 1993 (Knútsson & Gestsson, 2006).

The decreased fish stock after the 90´s meant that producers often had difficulties in increasing their value creation by just increasing fishing as they often did before. This increasingly put pressure on the MSOs to create the type of relationship where producers have the opportunity to get access to information and knowledge in the network that can support further value creation in their own companies. The role and power of the producers´ organisation dwindled gradually in the later years of the 1990s´ due to the abolishment of export licensing and the establishment of new large fisheries companies. Soon after that the largest vertically integrated fisheries company (Samherji) started exporting their products as well as a number of new marketing and exporting companies sprang up when larger independent producers (i.e. producers sourcing wet fish from fish markets or through direct supplying contracts with vessel owners) did the same. To counter these changes the nature of the producer’s organisations was changed to limited liability companies where the members got shares in accordance to their part in the equity reserves. This tied the producers business to these exporting companies until the three companies were listed on the Icelandic Stock Exchange in 1997 and the shareholders could capitalise their share value on the stock market. Gradually after 2000, the large integrated fisheries companies took over most of their exporting and marketing activities and so did a number of seafood producing companies of frozen and chilled products (Klemenson & Knútsson, 2006). In recent years, a three-tier structure characterises the exporting and marketing activities in Iceland;

1. The two large exporting and marketing companies, Icelandic and Iceland Seafood Internationali (ISI), holding a market share of 35-40% in frozen and salted products

2. The fish processing companies´ own marketing divisions3. Independent marketing companies often in close ties or affiliated with fish

processing plants.

This three-tier structure of marketing and exporting activities is an open and flexible system which allows amble space to find the most profitable market options. It must be noted that although there were severe drawbacks in the market predominance of the large MSOs, they supplied a wide range of services to their members or business partners. There were also benefits and strengths (economy of scale) stemming from the market size of the MSOs and from the wide range of products (economy of scope) they could supply. In many cases the MSOs acted like cartels both at home and on foreign markets.

25

Fisheries Science Centre of The University of Akureyri 2011

7 EconomyOver the course of the 20th century, Iceland was transformed from one of Europe’s poorest economies, with about 2/3 of the labour force employed in agriculture, to a prosperous modern economy employing 2/3 of its labour force in services. For most of the century, economic growth was led by the fisheries. Consequently, swings in the fish catch and export prices of marine products were the leading source of fluctuations in output growth (Figure 22).

Figure 22. Growth of GDP in Iceland since 1945; annual percent changes. Source: Statistics Iceland

Post-World War II economic growth has been both significantly higher and more volatile than in other OECD countries. The average annual growth rate of GDP from 1945 to 2008 was about 4%. Studies have shown that the Icelandic business cycle has been largely independent of the business cycle in other industrialised countries. This can be explained by the natural resource-based export sector and external supply shocks. However, the volatility of growth declined markedly towards the end of the century, which may be attributed to the rising share of the services sector, diversification of exports, more solid economic policies, and increased participation in the global economy (Central Bank of Iceland, 2011).

Historically, agriculture and fisheries has been the mainstay of the economy; sheep farming and cod fisheries as the fundamentals. The importance of fisheries increased considerably during the 20th century, which enabled the nation to develop from a poor agricultural country to a prosperous modern society. The fisheries’ significance and their dominant influence on the economy was, however, vulnerable to fluctuations in fish prices internationally and the condition of domestic fish stocks.

Around the turn of 21st century, the importance of the fishing industry declined considerably, not because of direct fall in fisheries themselves, but rather as the result of a rapid growth in the service and production sectors, such as financial intermediation, software design and aluminium manufacture. Diversification in the economy increased with further development from primary production, a similar process as known to occur in other developed countries. The export of fish products

26

Fisheries Science Centre of The University of Akureyri 2011

still weighs considerably in the nation’s foreign currency earnings, the following are the 2008 numbers; 37% of merchandise exports, roughly 26% of total exports and 8% of GDP.

In 2008 the total catch in Icelandic waters was close to 1.3 million tonnes of fish products worth ISK 171 billion; EUR 1.4 billion in export value. At the same time, the nation’s total population was 319,000 people and the workforce 178,600. The fishing industry employs 4.1% of the total workforce; fishing 2.4% and fish processing 1.7%. Although not visible from the aforementioned numbers, the fishing industry is fundamental for the whole economy and the country’s regional development. Fisheries and fish processing companies constitute the most important source of livelihood in coastal communities, where employment opportunities are often more limited because of less economic diversification.

From 1973 to the late 1980s, the growth of the fishing industry as a whole was substantial; i.e. the internal size of the sector increased. Then the industry remained fairly stable until 2002, when it declined sharply. These changes were largely controlled by the development of the fisheries. Fish processing has, on the other hand, been rather stable since the late 1970s but has also declined in the past few years.

The contribution of the fishing industry to GDP gradually declined over the same period; from a maximum of around 17% in 1978 to 8% in 2008. The fish processing production had turned down, while the fisheries sector remained largely stable at around 8% until the beginning of the 21st century.

The fishing industry is, nevertheless, fundamental to the Icelandic economy. If the whole marine sector had been removed in 2008, the effect would have been considerably stronger than the aforementioned 8% share. This can be explained by the side effects created by industry. Many auxiliary companies have developed around the fishing industry, providing supporting services and products (Sævaldsson & Heiðarsson, 2011).

7.1 Financial PerformanceThe Icelandic fishing industry has been profitable since the early nineties. Figure 24 shows the profitability of the consolidated industry, on average the profit of the industry has been 6.1% of total revenues. Only in 1997 and 1999 did the industry lose money, 1.4% in 1997 and 1.3% in 1999. The figure indicates as well, that the profitability of the industry has been improving in recent years. Every year since 2001 the profit of the fishing industry as a whole has been above 5% of revenues, but between 1993 and 2000 the profitability of the industry was never above 5%. The best years were 2001, when the profit of the industry was 18.1% of revenues, and 2006, when the profit was 16.9%. The reasons for the increased profitability of the industry are mainly twofold, increased productivity and higher prices (Figure 23).

27

Fisheries Science Centre of The University of Akureyri 2011

Figure 23 Average value of the Icelandic króna (right) and net profit in the fishing industry (left). Source: Statistics Iceland

The fluctuations of the Icelandic currency (ISK) explain some of the variation in profitability. When the index is high, the ISK is weak and when it is low, the ISK is strong. The ISK was lowest in 2001 which was the best year ever for the Icelandic fishing industry. On the other hand, 2005, when the ISK was strongest, was the 2nd worst year for the industry since 2001 (Gunnlaugsson, 2011).

8 SummaryThe Icelandic marine sector is still one of the main economic sectors and one of the pillars of export activities in Iceland, but its relative importance has diminished with the ascendancy of aluminium and services. In 2007, fishing and fish processing contributed 42% of total merchandise exports, compared with around 90% in the early 1960s. Likewise, the sector’s contribution to GDP has fallen from around 15% to under 7% over the same period. The marine sector is highly diversified in terms of species, modes of processing, and its export markets.

During the late ´90s and after 2000, the Icelandic fishing industry’s environment was not very favourable with decreasing quotas and more or less negative currency development for the industry. Despite this the profitability of the industry increased after the year 2000. In the period from 1993 to 2000 the profitability for the industry as a whole had fallen from its highest point of the decade in 1995 when it was up at 4.4% to being negative by 1.4% in 1997. In 2001 the profitability margin rose to its highest or to 18.1% but fluctuated and hit a low of 5.1% in 2004 rising steadily after that (Statistics Iceland, 2008). It is interesting to see that at the same time that the fish industry in Iceland is getting more profitable and competitive, but the old MOSs, have been facing increased difficulties as they did not seem to have found their place in the new value chain. This indicates that the industry competitive status is strong and its ability to face the changes in the business environment is high. This can mainly be traced to the quota system supporting a high degree of vertical integration of the industry where for

28

Fisheries Science Centre of The University of Akureyri 2011