Embed Size (px)

Citation preview

3Q16 Results - Investor Presentation

PETKİM PETROCHEMICAL HOLDING CORPORATION

07 November 2016

2

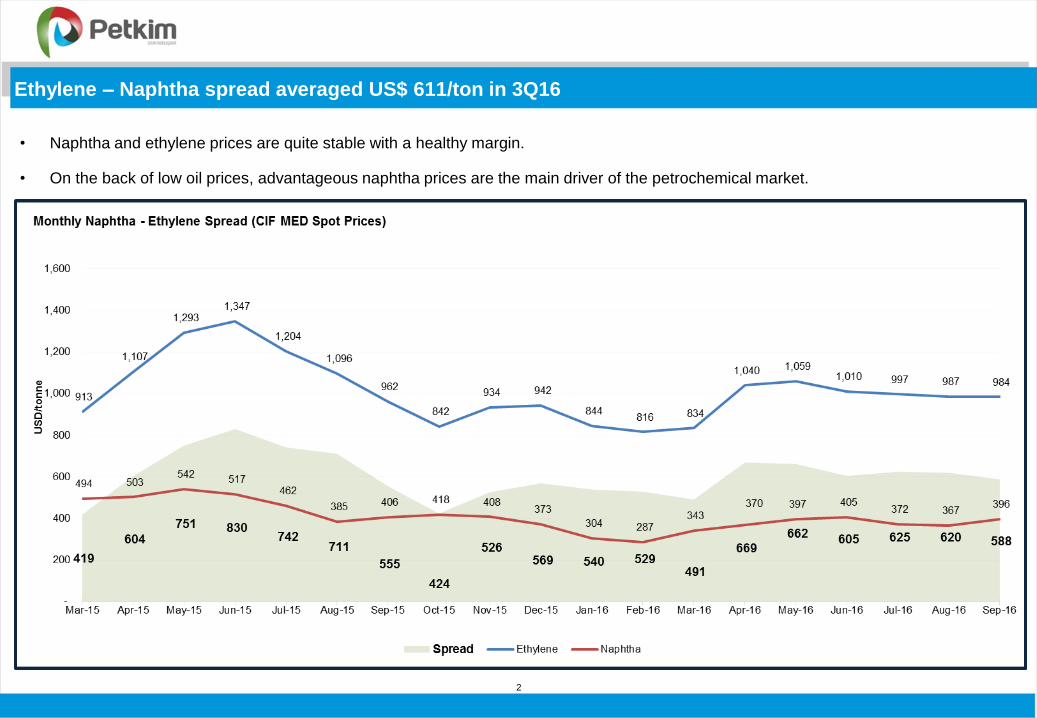

Ethylene – Naphtha spread averaged US$ 611/ton in 3Q16

• Naphtha and ethylene prices are quite stable with a healthy margin.

• On the back of low oil prices, advantageous naphtha prices are the main driver of the petrochemical market.

3

PLATT’s Index averaged US$ 881per ton in 3Q16

• PLATT’s index increased to $881 per ton in 3Q16 from $852per ton in 2Q16.

• Healthy demand in the 3rd quarter is reflected to the product prices.

4

• Feedstock vs. Product Prices in 3Q16

• Due to an unplanned shut down in ethylene unit, CUR and

production volumes were lower than expected. However, on the

back of high demand on Petrochemical industry, deficit in supply

can not be covered with higher production from other facilities.

Thus increases prices.

• Despite low production volumes, Petkim reached high

operational profit level with high margins.

• In terms of margins Petkim was quite successful to utilise global

petrochemical market conditions.

• Maximum production and fast sales strategy that started with

2015 still prevails.

• Depreciation of TL favors Petkim’s operational performance

both due to USD denominated revenue and 15% TL

denominated COGS. Additionally, fluctuations in USD/TRY

currency with expectation of further depreciation of TL

strengthens market position of Petkim against importers.

Costs and Operational Efficiency in 3Q16

5

6

• PETKIM 3Q16– In 3Q16 Petkim recorded TL 975mn sales via 365kton volume

3Q16 Revenue: TL 969mn

3Q16 Export Sales: TL 252mn 3Q16 Volume: 365k ton

• PETKIM 2Q16 Income Statement

7

TL mn 3Q15 3Q16

Sales 3.375,1 3.253,5 Cost of sales (2.814,0) (2.585,1)

Gross Profit 561,1 668,4 Gross profit % 16,6% 20,5%

Marketing and sales expenses (22,0) (31,2) General admin. Expenses (86,0) (103,1) R&D Expenses (8,4) (9,7)

Operating profit 444,8 524,3 Other income / (expenses) (38,2) 47,5 Financial income 351,5 195,0 Financial expense (312,0) (174,3)

Profit before tax 446,1 592,5 Income tax (8,0) (112,5) Deferred tax 65,1 35,5

Net Profit / (loss) 503,2 515,4 Net profit % 14,9% 15,8%

Severance (13,0) 2,7 Depreciation 84,8 81,7

EBITDA 516,5 608,7 EBITDA % 15,3% 18,7%

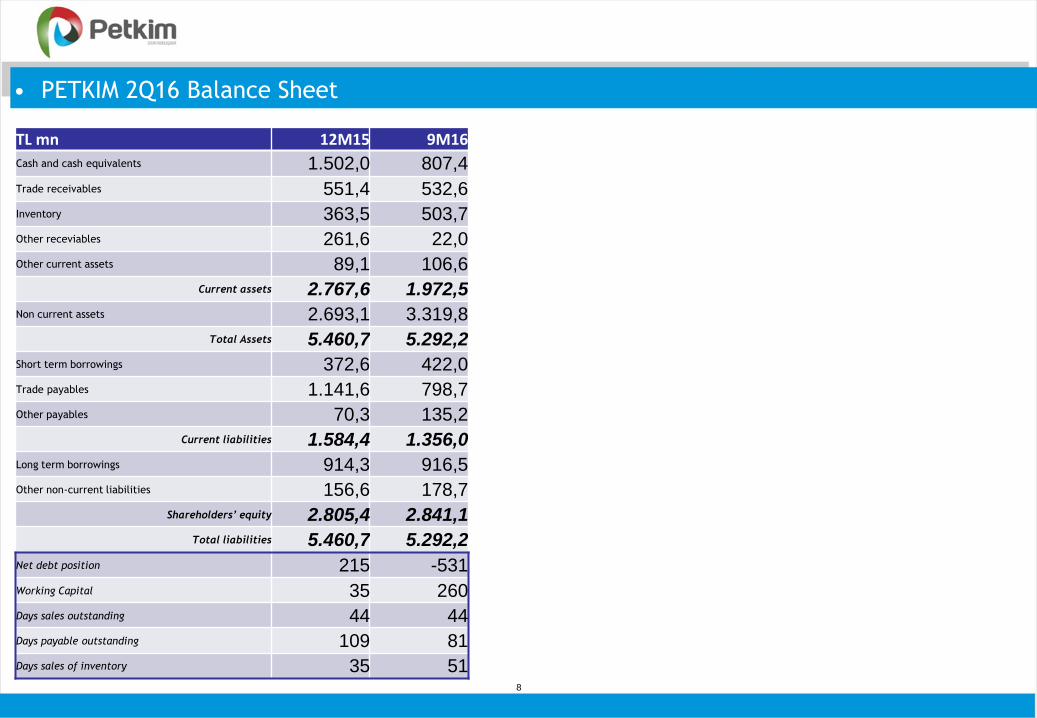

• PETKIM 2Q16 Balance Sheet

8

TL mn 12M15 9M16

Cash and cash equivalents 1.502,0 807,4

Trade receivables 551,4 532,6

Inventory 363,5 503,7

Other receviables 261,6 22,0

Other current assets 89,1 106,6

Current assets 2.767,6 1.972,5

Non current assets 2.693,1 3.319,8

Total Assets 5.460,7 5.292,2

Short term borrowings 372,6 422,0

Trade payables 1.141,6 798,7

Other payables 70,3 135,2

Current liabilities 1.584,4 1.356,0

Long term borrowings 914,3 916,5

Other non-current liabilities 156,6 178,7

Shareholders’ equity 2.805,4 2.841,1

Total liabilities 5.460,7 5.292,2

Net debt position 215 -531

Working Capital 35 260

Days sales outstanding 44 44

Days payable outstanding 109 81

Days sales of inventory 35 51

PETKIM – Debottlenecking Investments are completed as of November 2014

In addition to c.50% capacity increase, PETKİM will

also benefit on energy cost.

Capacity (tons /year) : 105,000

Project finance (E/D ratio) : 100% Debt

Investment amount : US$ 20mn

Ethylene Capacity Increase PTA Capacity Increase

9

With the completion of the project ethylene

production capacity increased by 13%

Capacity (tons /year) : 588,000

Project finance (E/D ratio) : 20:80

Investment amount : US$ 118mn

PETLIM – Goldman Sachs has purchased 30% stake in Petlim for a total consideration of US$ 250mn

• PETLIM Port Project has 1.5 million TEU container handling capacity, 42

hectare main port area, 8 hectare off-dock service area terminal port.

• APMT and Petkim’s 70% subsidiary PETLIM has a revenue sharing

agreement for the 28 years (+4 years option) of the operational period.

• Our partner in port operations, APMT (group company of Maersk Group)

paid US$ 25mn in July 2013, as the first installment of US$ 65mn upfront

fees for the Operation Rights.

• The infrastructure investment is carried out by Petlim. Petlim’s part of

investment is US$ 276mn, of which around US$ 70mn will be equity and

the remaining will be financed by project financing.

• Goldman Sachs has purchased 30% stake in Petlim for a total

consideration of US$ 250mn

• First phase of the project is completed.

10

Petkim - Wind Power Plant

• Petkim is setting up a wind power plant with a total capacity of 51MW

at the Petkim Peninsula

• The WPP is planned to generate 200GWh electricity per annum.

• PETKİM signed an agreement with ALSTOM RENOVABLES ESPAÑA S.L.U

and ALSTOM Power ve Ulaşım A.Ş (Alstom Türkiye) consortium on

28/03/2014 amounting to €55 million which will be covering a full range

of basic and detailed engineering study, material procurement,

construction, electric work and installation and commissioning.

Picture above is presented for only representative purposes

11

STAR Refinery

• STAR Refinery will have 10 million tons /year crude oil refining capacity.

• Petkim signed a 20-year off-take agreement with STAR Rafineri A.Ş to offtake

270,000 tonnes mixed-xylene and 1,600,000 tonnes naphtha annually.

• Naphtha price will be set as the Platts’ FOB MED spot market price plus

US$ 6 margin per tonne and mixed-xylene price will be based on ICIS’s

Rotterdam Paraxylene Spot Price multiplied by 0.74.

• It is expected that PETKIM’s feedstock cost will be reduced US$ 30 per

tonne as a result of this agreement. The offtake pricing terms in the

agreement are in line with the market prices.

• Other than the logistics cost savings, as a result of the synergies

created by the refinery and the petrochemicals integration, there will

be significant cost benefits for Petkim including quality standardization

and stabilization, and the reduction in inventory costs.

• The aggregate investment amount will reach US$ 5.7bn.

• On May 30th 2014, US$ 3,290 million project finance portion of the STAR

Refinery investment has been signed with a number of 23 local and

international financial institutions including Export Credit Agencies (ECAs),

commercial banks and development banks.

• US$ 2,690 million of the project finance has a maturity of 18 years with 4 years

grace period, while the remaining US$ 600 million has a maturity of 15 years

with 4 years grace period.

12

Naphtha

Ethylene

Propylene

Aromatics

Ethylene Plant

LDPE

(337.000 ton/year)

HDPE

(96.000ton/year)

MEG

(89.000ton/year)

VCM

PVC

(150.000ton/year)

PP

(144.000 ton/year)

Bag, greenhouse covers, film, cable, toys, pipes, bottles, hose,

packaging

Construction and water pipes, packaging film, toys, bottles,

soft drink crates, barrels

Polyster fiber, polyester film, antifreeze

Pipe, window shades, cable, bottles, building

materials, packaging film, floor tiles, serum bags

ACN

(90.000 ton/year)

Knitting yarn, ropes, tablecloths, napkins, doormats,

hoses, radiator pipes, fishing nets, brushes

Textile fibers, artificial wool, ABS resins (acrylonitrile

butadiene)

Benzene

(144.000 ton/year)

Toluen

(16.000 ton/year)

PA

(49.000 ton/year)

P-X

(92.000 ton/year)

PTA

(105.000 ton/year)

Detergent, solvents, explosives, pharmaceuticals,

cosmetics, parts of white goods

Polyester fiber, polyester resin, films, plasticizers,

synthetic chemicals

Polyester industry

LPG

(320.000 ton/year) C4

(140.000ton/year)

C5 Mixtures

(80.000 ton/year)

Appendix 1. Petrochemical Complex Flow Chart

13

Appendix 2. PETKIM’s Ownership Structure

Petkim Stock Performance

Closing Price as of 30 September 2016 (TRY/Share) TL 4.55

Market Cap (TRY mn) TL 6,825

Free Float (%) 47,6

State Oil Company of Azerbaijan

Republic

SOCAR Turkey Energy

SOCAR Turkey

Petrochemicals

ISE Ticker: PETKM

Free Float : 43.7%

Petlim Port

87%

100%

51%

1.32%

43.7%

70%

SOCAR Turkey Yatırım A.Ş.

(RHAŞ 60%)

(MED 40%)

Refinery Holding

(RHAŞ)

100%

STAR Refinery

100%

14

Goldman Sachs

Goldman Sachs 30%

We welcome your questions, comments and suggestions. Our corporate headquarters office address is:

Petkim Petrochemical Holding Corp. PO. Box.12

Aliağa, 35800 İzmir/ TURKEY

To contact us with respect to shareholding relations for individual and corporate investors, please call directly or send an e-mail to:

Also, please visit our web site at www.petkim.com.tr for further information and queries.

Semih ATALAY

SOCAR Turkey Investor Relations Manager

Direct: +90212 305 0142

Erdem ÜNLÜER

SOCAR Turkey Investor Relations Supervisor

Direct: +90212 305 0018

Mustafa Çağatay

Corporate Governance and IR Coordinator

Phone: +90 (232) 616 12 40 ext.2501

Email: [email protected]

Investor Relations

This presentation is confidential and does not constitute or form part of, and should not be construed as, an offer or invitation to subscribe for, underwrite

or otherwise acquire, any securities of Petkim Petrokimya Holding A.Ş. (the “Company”) or any member of its group nor should it or any part of it form the

basis of, or be relied on in connection with, any contract to purchase or subscribe for any securities of the Company or any member of its group nor shall it

or any part of it form the basis of or be relied on in connection with any contract, investment decision or commitment whatsoever. This presentation has

been made to you solely for your information and background and is subject to amendment. This presentation (or any part of it) may not be reproduced or

redistributed, passed on, or the contents otherwise divulged, directly or indirectly, to any other person (excluding the relevant person’s professional

advisers) or published in whole or in part for any purpose without the prior written consent of the Company.

Disclaimer