Embed Size (px)

Citation preview

7/31/2019 34580182 Personal Financial Planning

http://slidepdf.com/reader/full/34580182-personal-financial-planning 1/28

Personal financial planning: an

opportunity for Indian banks

Presented by:

Ajay Panwar 08FN008Akshay Patil 08FN010

Ameesh Sharma 08FN011Sorubh Janmeja 08HR094

7/31/2019 34580182 Personal Financial Planning

http://slidepdf.com/reader/full/34580182-personal-financial-planning 2/28

Personal Financial

Planning

7/31/2019 34580182 Personal Financial Planning

http://slidepdf.com/reader/full/34580182-personal-financial-planning 3/28

Definition

A process of determining an individual·sfinancial goals, purposes in life and life·spriorities.

Then after considering his resources, riskprofile and current life style, to detail a

balanced and realistic plan to meet thosegoals.

It is the process of developing a personal

roadmap for your financial well being .

7/31/2019 34580182 Personal Financial Planning

http://slidepdf.com/reader/full/34580182-personal-financial-planning 4/28

Definition contd«

The inputs to the financial planning process are, ² Your finances, i.e., your income, assets and liabilities ² Your goals, i.e., your current and future financial needs ² Your appetite for risk

The output of the financial planning process is apersonal financial plan that tells you how to use your money to achieve your goals, keeping in mind

inflation, real returns and taxes.In short, financial planning is the process of systematically planning your finances towardsachieving your short-term and long-term life goals.

7/31/2019 34580182 Personal Financial Planning

http://slidepdf.com/reader/full/34580182-personal-financial-planning 5/28

Scope

Risk management and insurance planning: managingcash flow risk through sound risk management andinsurance techniques.

Investment and planning issues: planning, creatingand managing capital accumulation to generate futurecapital and cash flows.Retirement planning: insuring financial independence

at retirement taking into consideration increased costof living and improved lifestyle.Tax planning: reduction in tax liabilities and freeingup cash flows.

7/31/2019 34580182 Personal Financial Planning

http://slidepdf.com/reader/full/34580182-personal-financial-planning 6/28

Scope contd«

Estate planning: planning for creation, accumulation,conservation and distribution of assets.

Cash flow and liability management: maintaining andenhancing cash flows through debt and lifestylemanagement. Most important tool for short and longterm planning.

Education planning for kids and other familymembers.

Relationship management: moving beyond pureproduct selling. Understanding needs of thecustomer.

7/31/2019 34580182 Personal Financial Planning

http://slidepdf.com/reader/full/34580182-personal-financial-planning 7/28

Objectives

Financial independence of an individual

Provision for family to maintain same living

standard in event of disability or deathMinimising incidence of taxes

Providing for children·s education,

improvement events like marriage and other family functions

Investing the savings in most efficientmanner to maximise returns

7/31/2019 34580182 Personal Financial Planning

http://slidepdf.com/reader/full/34580182-personal-financial-planning 8/28

Objectives contd«

Repaying mortgage and other debt

Maintaining the same standard of living after retirement

Staying ahead of inflation

Preserving estate for legal heirs

7/31/2019 34580182 Personal Financial Planning

http://slidepdf.com/reader/full/34580182-personal-financial-planning 9/28

Key elements

1. Age. For example, an older individual typicallyfavours fixed income, safe investments.

2. Marital Status. For instance, a married persondesires sufficient life insurance to protect the family.

3. Family status. For instance, children will need acollege education.

4. Risk preferences. For instance, a risk averse person

will favour Government Securities.5. Investment preferences. For example, if an

individual wants growth, stocks having capitalappreciation potential be selected.

7/31/2019 34580182 Personal Financial Planning

http://slidepdf.com/reader/full/34580182-personal-financial-planning 10/28

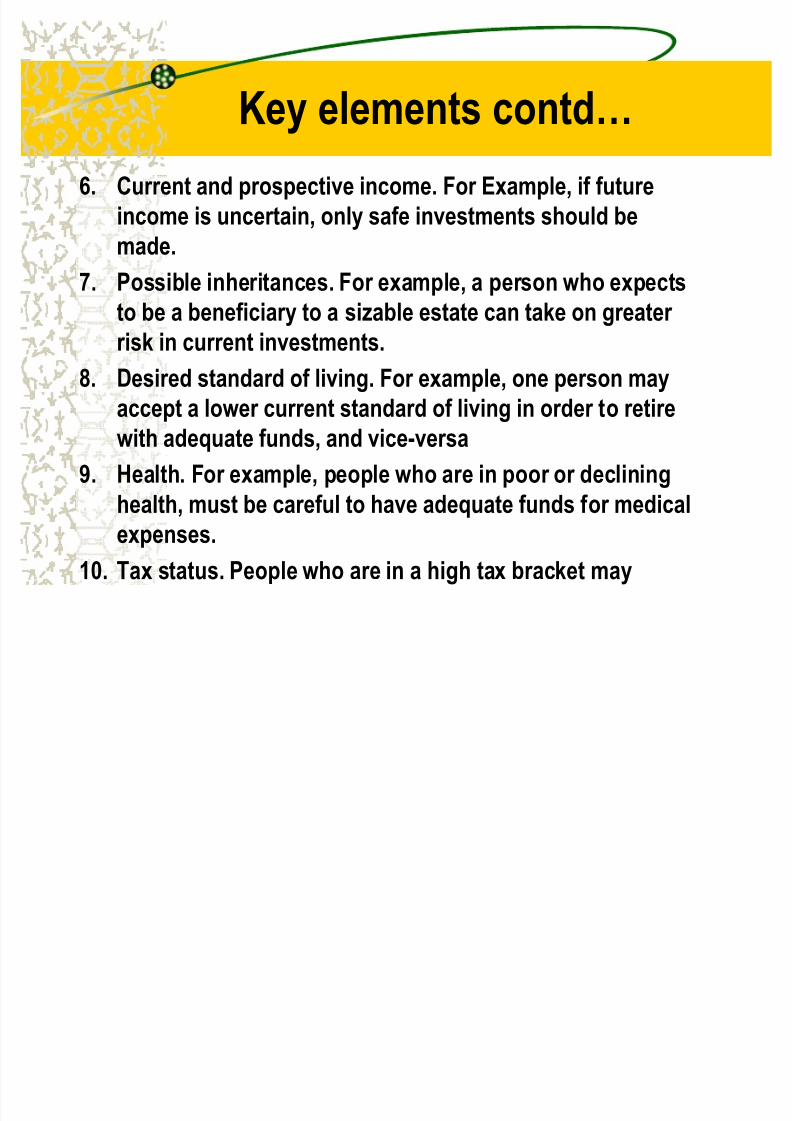

Key elements contd«

6. Current and prospective income. For Example, if futureincome is uncertain, only safe investments should bemade.

7. Possible inheritances. For example, a person who expectsto be a beneficiary to a sizable estate can take on greater risk in current investments.

8. Desired standard of living. For example, one person may

accept a lower current standard of living in order to retirewith adequate funds, and vice-versa

9. Health. For example, people who are in poor or declininghealth, must be careful to have adequate funds for medicalexpenses.

10. Tax status. People who are in a high tax bracket may

7/31/2019 34580182 Personal Financial Planning

http://slidepdf.com/reader/full/34580182-personal-financial-planning 11/28

Process

1. Setting goals with the client

2. Gathering relevant information on the client

3. Analyzing the information

4. Constructing a financial plan

5. Implementing the strategies in the plan6. Monitoring implementation and reviewing

the plan.

7/31/2019 34580182 Personal Financial Planning

http://slidepdf.com/reader/full/34580182-personal-financial-planning 12/28

Importance and Benefits

Helps monitor cash flows and reducesunnecessary expenditure.

Enables maintenance of an optimum balancebetween income and expenses.

Helps boost savings and create wealth.

Helps reduce tax liability.

Maximizes returns from investments.

7/31/2019 34580182 Personal Financial Planning

http://slidepdf.com/reader/full/34580182-personal-financial-planning 13/28

Importance and Benefits contd«

Creates wealth and ensures better wealthmanagement to achieve life goals.

Financially secures retirement life.

Reviews insurance needs and therefore alsoensures that dependents are financially

secure in the unfortunate event of death or disability.

Lastly, it also ensures that a will is made.

7/31/2019 34580182 Personal Financial Planning

http://slidepdf.com/reader/full/34580182-personal-financial-planning 14/28

Importance and Benefits contd«

7/31/2019 34580182 Personal Financial Planning

http://slidepdf.com/reader/full/34580182-personal-financial-planning 15/28

Requirements

A detailed net worth account containing,

² Income data: income details of earning members

and family as a whole.

² Asset data: information on savings account,personal residence, other real estate, jewelry etc.

² Liability data: information on home loan, autoloan, personal loan etc.

7/31/2019 34580182 Personal Financial Planning

http://slidepdf.com/reader/full/34580182-personal-financial-planning 16/28

Requirements contd«

Insurance information: information regarding the amountof information required. List of all the current insurancepolicies like,

² Health insurance policy ² Property insurance ² Auto insurance

Savings and investment planning ² Level of risk tolerance

² Diversification of portfolioEstate planning: taking out an inventory out of the assetsand making a will or establishing a trust. Aims atminimizing tax liabilities.

7/31/2019 34580182 Personal Financial Planning

http://slidepdf.com/reader/full/34580182-personal-financial-planning 17/28

Financial Education and Credit

CounsellingCredit counselling is a process of offeringeducation to consumers about how to avoidincurring debts that cannot be repaid. It servesthe following purposes: ² It examines ways to solve the current financial

problems ² By educating about the costs of misusing a credit, it

improves financial management ² It encourages distressed people to access the formal

financial system ² Empowers consumers to be better positioned to take

responsibility for their own well-being

7/31/2019 34580182 Personal Financial Planning

http://slidepdf.com/reader/full/34580182-personal-financial-planning 18/28

Financial literacy

Financial literacy of an individual is his ability toknow, monitor and effectively use financial resourcesfor the benefit of his economic security.

Certain recommendations on principles and goodpractices for financial literacy and awareness havebeen developed: ² Governments and all concerned stakeholders should

promote unbiased, fair and co-ordinated financialeducation

² It should start at school, for people to be educated asearly as possible

² It should be a part of good governance in financialinstitutions

7/31/2019 34580182 Personal Financial Planning

http://slidepdf.com/reader/full/34580182-personal-financial-planning 19/28

Financial literacy contd«

² It should be clearly distinguished from commercial advice;codes for conduct for the staff of financial institutions shouldbe developed

² Programs should focus on important life planning aspects,such as basic saving, debt, insurance and pension ² Programs should be oriented towards financial capacity

building and appropriately targeted on specific groups, andshould be made as personalised as possible

² Future retires should be made aware of the need to assess the

financial adequacy of their current public and private pensionschemes ² National campaigns, specific websites, free information

services, and warning systems on high risk issues for financial consumers should be promoted

7/31/2019 34580182 Personal Financial Planning

http://slidepdf.com/reader/full/34580182-personal-financial-planning 20/28

Opportunity for Indian banks

7/31/2019 34580182 Personal Financial Planning

http://slidepdf.com/reader/full/34580182-personal-financial-planning 21/28

Potentials in India

Changing Demographic Profile:

Source: Ministry of Home Affairs, Government of India

< 14 years34%

15 - 35 years35%

35 - 49 years

17%

> 50 years14%

7/31/2019 34580182 Personal Financial Planning

http://slidepdf.com/reader/full/34580182-personal-financial-planning 22/28

Potentials in India

Household Savings Pattern:

7/31/2019 34580182 Personal Financial Planning

http://slidepdf.com/reader/full/34580182-personal-financial-planning 23/28

Potentials in India

Retail Market Size:

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

1999-00 2000-01 2001-02 2002-03

Housing finance Car finance Credit card spend

Commercial vehicle finance 2-wheeler finance Personal loans

Consumer durable finance

7.39.4

12.9

16.5

CAGR of 31%

Annual disbursement (US$ billion)

7/31/2019 34580182 Personal Financial Planning

http://slidepdf.com/reader/full/34580182-personal-financial-planning 24/28

Potentials in India

Financial Services Potential:14.2%

12.1%

9.0%

5.2%

2.9% 2.7% 2.2%

0.0%2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

UnitedKingdom

SouthKorea

UnitedStates

Malaysia Thailand India China

Life insurance General insurance

Premium as a % of GDP

7/31/2019 34580182 Personal Financial Planning

http://slidepdf.com/reader/full/34580182-personal-financial-planning 25/28

Potentials in India

Investment opportunity across all segments in thebanking and financial services sector. ² Low penetration in the pension market makes it a lucrative

business segment. ² Foreign banks likely to be allowed to acquire local banks after

March 2009 when the next stage of banking reforms isproposed.

Foreign banks gaining prominence and popularity inIndia.Pension fund industry in India grew at a CAGR of 122.44%from 1999-00 to 2006-07.Rural and semi-urban India is expected to account for 58.33% of the insurance sector by 2010.

7/31/2019 34580182 Personal Financial Planning

http://slidepdf.com/reader/full/34580182-personal-financial-planning 26/28

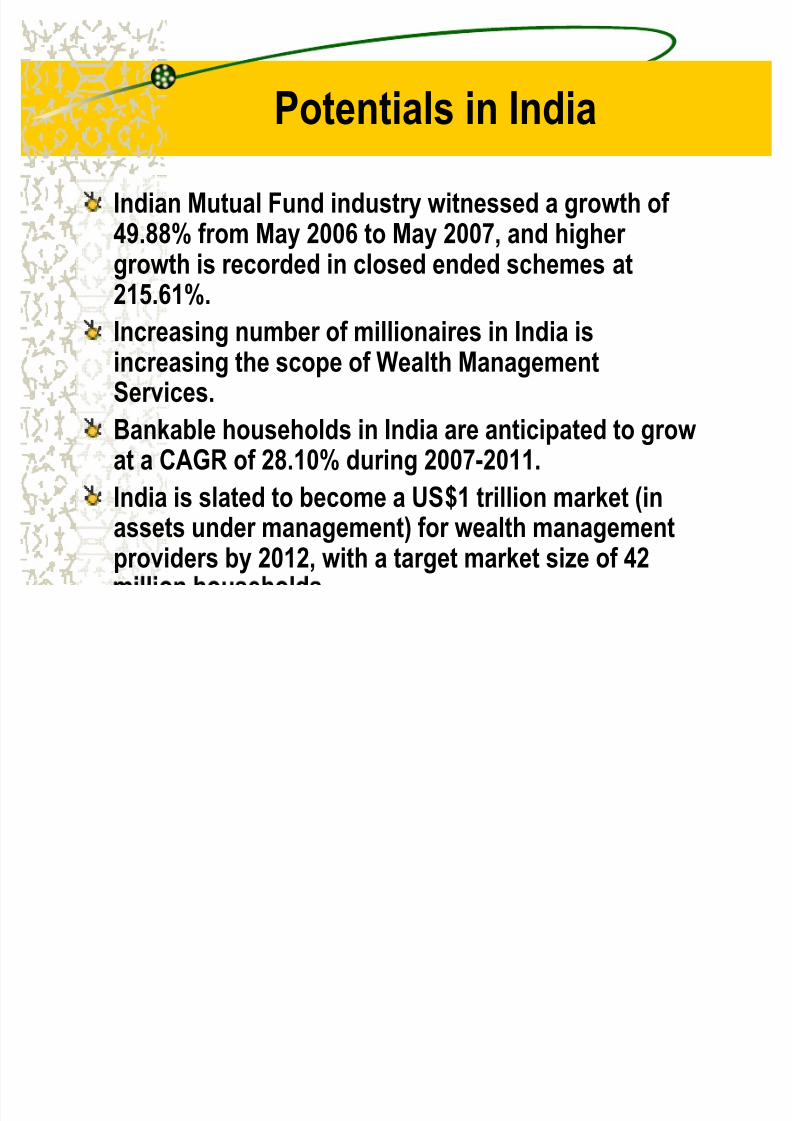

Potentials in India

Indian Mutual Fund industry witnessed a growth of 49.88% from May 2006 to May 2007, and higher growth is recorded in closed ended schemes at215.61%.

Increasing number of millionaires in India isincreasing the scope of Wealth ManagementServices.

Bankable households in India are anticipated to growat a CAGR of 28.10% during 2007-2011.

India is slated to become a US$1 trillion market (inassets under management) for wealth management

providers by 2012, with a target market size of 42

7/31/2019 34580182 Personal Financial Planning

http://slidepdf.com/reader/full/34580182-personal-financial-planning 27/28

Joint efforts of IIBF and FPSB India are likely to producemany qualified and certified financial planners in thebanking industry.

The increasing complexity of financial products will result inan increasing need for personal financial planners.

Offering of Personal Financial Planning advice to customerswill lead to a win-win situation for both banks as well as

their customers.This opens up new opportunities for MBA students.

Business Graduates can build their careers in personalfinancial planning, income tax and estateplanning, retirementplanning, law, investments, insurance, employee benefits

7/31/2019 34580182 Personal Financial Planning

http://slidepdf.com/reader/full/34580182-personal-financial-planning 28/28

Thank you