Embed Size (px)

Citation preview

30 September 2010

The Manager

Company Announcements Office

Australian Securities Exchange

Annual Report and Completion of Inventory Review

Kresta Holdings Limited is pleased to release its Annual Report for the year ended 30 June 2010.

The Company’s net profit after tax for the year ended 30 June 2010 was $2,697,000 compared to

$3,658,000 for the year ended 30 June 2009. The profit for the year was affected by the inventory

write down announced on 14 September 2010.

The Board has completed its review into the carrying value of inventory and has received an

independent review of the inventory. Following that review, the Board resolved to write down the

carrying value of inventory by an additional $5.8 million as at 30 June 2010, in addition to the $1.5

million which had been provided prior to the review.

Yours faithfully

Kresta Holdings Limited

Ian N Trahar

Non-Executive Chairman

For

per

sona

l use

onl

y

Kresta Holdings Limited

Annual financial report for the year ended 30 June 2010

Kresta

For

per

sona

l use

onl

y

KRESTA HOLDINGS LIMITED—ANNUAL REPORT

Chairman’s Report

Chairman’s Report

The 2009/2010 financial year resulted in a solid operating cash flow performance as your Company

responded positively to the recovery from the global financial crisis and the wind back of the Federal

Government‟s stimulus package.

Group revenue for the year rose to $123 million compared to $117 million for the prior period.

Unfortunately the Company‟s strong cash flow performance was adversely impacted at the net profit

line where after significant investigation and external assessment the Board resolved to reduce the

value of inventory by $5.8 million on top of the $1.5 million already provided against the inventory

prior to the review.

Whilst this one off non-cash charge was extremely annoying the underlying cash flow strength of the

Company has enabled your Board to maintain the final dividend of 1.5 cents per share bringing the

full year dividend to 3.5 cents per share fully franked.

My fellow directors join me in thanking our staff for their diligent and continued efforts throughout the

year.

Ian N Trahar Chairman Perth 30 September 2010

For

per

sona

l use

onl

y

KRESTA HOLDINGS LIMITED—ANNUAL REPORT

Corporate Information

ABN 26 008 675 803

Directors Ian Norman Trahar (Chairman)

Trent Josiah Bartlett

Peter Hatfull

Company Secretary & Chief Financial Officer Thye Tan

Registered Office 389 Victoria Road

Malaga WA 6090

Telephone: (08) 9249 0777

Share Register Computershare Investor Services Pty Ltd

Level 2, Reserve Bank Building

45 St Georges Terrace

Perth WA 6000

Telephone: (08) 9323 2000

Kresta Holdings Limited shares are listed on the Australian Securities Exchange.

ASX Code: KRS

Bankers Australia and New Zealand Banking Group Limited

Commonwealth Bank of Australia Ltd

Auditors Ernst & Young

The Ernst & Young Building

11 Mounts Bay Road

Perth WA 6000

Internet Address www.kresta.com.au

For

per

sona

l use

onl

y

KRESTA HOLDINGS LIMITED – ANNUAL REPORT

Contents

Directors‟ report ......................................................................................................................................................... 1 Corporate governance statement ............................................................................................................................ 13 Income statement .................................................................................................................................................... 16 Statement of comprehensive income ....................................................................................................................... 17 Statement of financial position ................................................................................................................................. 18 Statement of changes in equity................................................................................................................................ 19 Statement of cash flows .......................................................................................................................................... 20 Notes to the financial statements 1. Corporate information ......................................................................................................................................... 21 2. Summary of significant accounting policies ......................................................................................................... 21 3. Revenues and expenses .................................................................................................................................... 33 4. Income tax .......................................................................................................................................................... 34 5. Earnings per share ............................................................................................................................................. 35 6. Dividends paid and proposed ............................................................................................................................. 36 7. Cash and cash equivalents ................................................................................................................................. 37 8. Trade and other receivables (current) ................................................................................................................. 38 9. Inventories ......................................................................................................................................................... 39 10. Parent entity information .................................................................................................................................... 39 11. Property, plant and equipment ........................................................................................................................... 41 12. Intangible assets and goodwill ........................................................................................................................... 42 13. Share-based payment plans .............................................................................................................................. 44 14. Trade and other payables (current) ................................................................................................................... 45 15. Interest-bearing loans and borrowings ............................................................................................................... 45 16. Provisions .......................................................................................................................................................... 47 17. Contributed equity and reserves ........................................................................................................................ 48 18. Government grants ............................................................................................................................................ 49 19. Financial risk management objectives and policies ............................................................................................ 50 20. Commitments .................................................................................................................................................... 55 21. Related party disclosures .................................................................................................................................. 56 22. Key management personnel .............................................................................................................................. 57 23. Business combination ........................................................................................................................................ 59 24. Events after the balance sheet date ................................................................................................................... 60 25. Auditor‟s remuneration....................................................................................................................................... 60 26. Operating segments .......................................................................................................................................... 60 27. Derivative financial instruments ........................................................................................................................ 61 Directors‟ declaration ............................................................................................................................................... 63 Auditor‟s Report....................................................................................................................................................... 64 ASX Additional Information ...................................................................................................................................... 66

For

per

sona

l use

onl

y

KRESTA HOLDINGS LIMITED—ANNUAL REPORT

Directors’ Report

1

Your directors submit their report for the year ended 30 June 2010. DIRECTORS The names and details of the Company‟s directors in office during the financial year and until the date of this report are as follows. Directors were in office for this entire period unless otherwise stated. Names, qualifications, experience and special responsibilities Neil Fearis, LL.B (Hons) MAICD, F FIN (Non-executive Chairman) – retired 31 December 2009 Mr Fearis is a commercial lawyer with 33 years‟ experience. During the past seven years, Mr Fearis has also served as a director of the following other listed companies - Carnarvon Petroleum Ltd, Perseus Mining Ltd and Liberty Resources Limited (resigned 2008). He also served on the audit and remuneration committees of the Group. Tass Zorbas (Managing Director) – retired 6 September 2010 Mr Zorbas has been involved in the window treatment industry for approximately 35 year and was instrumental in pioneering the marketing and manufacturing of vertical blinds in Australia. Trent Bartlett, Grad Dip Bus, Grad Cert E-Commerce, FAICD (Non-executive Director) Mr Bartlett is the Chief Executive Officer of Capricorn Society Ltd. Mr Bartlett joined Kresta Holdings Limited as a non-executive director in 2003 and has had considerable retail experience in senior management roles with Coles Myer, Aherns and David Jones before joining Capricorn Society Ltd. He also serves on the audit and remuneration committees of the Group. Peter Johnston, FCPA, FCIS (Non-executive Director) – retired 23 June 2010 Mr Johnston is an accountant by profession with a long career in the corporate sector and was the Company Secretary of Wesfarmers Limited until his retirement in 2001. Mr Johnston has served as a director of the ASX-Listed Bunnings Warehouse Property Trust since 2005. He also served on the audit and remuneration committees of the Group. Peter Hatfull, MAICD (Non-executive Director) – appointed 14

July 2009

Mr Hatfull is qualified as a Chartered Accountant and has over 30 years‟ experience in a range of senior executive positions with Australian and international companies. He has an extensive skill-set with listed companies in the areas of corporate governance, business optimization, capital raising and company restructuring. Mr Hatfull is currently a director of mining services company Barminco Pty Ltd and is a corporate advisor of and director of a range of private companies. He also serves on the audit and remuneration committees of the Group. Ian Trahar, B.Ec, MBA, MAICD (Non-executive Chairman) – appointed 23 February 2010 Mr Trahar joined the board as a non-executive director on 23 February 2010. Mr Trahar has a consumer products and finance background and is a member of the Australian Institute of Company Directors. He has served as a director and Chairman of CO2 Group Limited for the past eight year. He also serves on the audit and remuneration committees of the Group. COMPANY SECRETARY & CHIEF FINANCIAL OFFICER Thye Tan, FCPA Mr Tan is a fellow of CPA Australia and has worked in various senior commercial and financial positions at Wesfarmers Ltd, Bunnings Ltd, Schlumberger and ERG Ltd. Mr Tan also holds a Graduate Diploma in Chartered Secretaries and Administrators.

For

per

sona

l use

onl

y

KRESTA HOLDINGS LIMITED—ANNUAL REPORT

Directors’ Report continued

2

Interests in the shares and options of the company As at the date of this report, the interests of the directors in the shares of Kresta Holdings Limited were: Number of

Ordinary Shares

TJ Bartlett

5,000

I Trahar

27,890,068

DIVIDENDS Cents $‟000 Final dividends recommended for 2010 on:

Ordinary shares 1.5 2,162 Dividends paid in the year: Interim of the year

Ordinary shares 2.0 2,864 Final dividends for 2009 shown as recommended in the 2009 financial report:

Ordinary shares 1.0 1,432

For

per

sona

l use

onl

y

KRESTA HOLDINGS LIMITED—ANNUAL REPORT

Directors’ Report continued

3

CORPORATE INFORMATION Corporate structure Kresta Holdings Limited is a company limited by shares that is incorporated and domiciled in Australia. Kresta Holdings Limited has prepared a consolidated financial report incorporating the following entities that it controlled during the financial year: Kresta Holdings Limited (parent) Kresta Blinds (Holdings) Pty Ltd Kresta Blinds Ltd Kresta Blinds International Pty Ltd Kedena Holdings Pty Ltd Sharatan Pty Ltd Blind Wholesalers, Distributors and Manufacturers Pty Ltd Finmar Pty Ltd Mardo Australia Pty Ltd Mardo International Pty Ltd Twighlight Sun Pty Ltd Sandelle Pty Ltd Curtain Wonderland Pty Ltd

Principal activities The principal activities during the year of entities within the consolidated entity were the manufacture, distribution and retailing of window treatments and components. There have been no significant changes in the nature of those activities during the year. Employees The consolidated entity employed 907 employees as at 30 June 2010 (2009: 954 employees). OPERATING AND FINANCIAL REVIEW Group overview The Kresta Group has been a leading manufacturer and retailer of window furnishings for over 34 years and is renowned for pioneering the manufacture and marketing of vertical blinds in Australia. Although the Group‟s business activities are predominately centred in Western Australia, the Group has a significant chain of outlets located throughout Australia and New Zealand. During the financial year ended 30 June 2010, the Group acquired the Ace of Shades business based in Victoria. This business has been a well regarded and profitable supplier of external blinds and awnings in Melbourne for the last 17 years. This purchase will provide the Group with an immediate profitable entry point into the Victorian market for outdoor products and will allow the Group to expand this service throughout Australia and New Zealand and to complement the Group‟s existing range of indoor products. The Group also rolled out 2 new stores and relocated and/or refurbished 6 others as part of its ongoing business strategy to improve customer service and expand coverage to include geographical areas where the company does not have a retail presence. Although new stores and refurbishments as a general rule require time to contribute a satisfactory return, the investment made this financial year is expected to have a positive impact on Kresta‟s financial performance in the next 12 to 18 months. The Board of directors and management will continue to pursue this policy of expanding coverage in the forthcoming year in locations where the demographics support new store developments. Kresta operates several manufacturing plants involving textile weaving, the fabrication of timber, fabric and aluminium venetian blinds, curtains and vertical blinds. The manufacturing operations continue to be a major part of the Group‟s core activities. At the same time, the Group currently sources many finished product lines from overseas manufacturers and this policy will be continued, provided these imported “boxed products” can be manufactured off-shore at competitive prices and delivery time to customers is not compromised. In February 2010 the Group commissioned an independent valuer to value the land and buildings owned by the Group and this valuation has shown a significant increase in value compared to the current book value as noted in Note 11 of the Financial Report. The Group‟s strong sales results have been positively impacted by the successful introduction of a range of innovative product ranges, together with the recent acquisitions performing at or above expectations. Several new product lines have been introduced during the year ended 30 June 2010 to meet customer expectations and Kresta will continue to keep abreast with latest trends in window treatments and blinds to maintain its strong market position. A number of new products are being developed for launch in the 2010/11 financial year to maintain the Group‟s position as a leading supplier. In this regard, Kresta has maintained its market share and continues to be an industry leader through product innovation and range. Performance indicators The Board has adopted a number of financial and operational key performance indicators (KPIs) to monitor the Group‟s core activities. These KPIs are regularly reviewed by management to gauge the performance of operations and ensure that the measures adopted continue to be relevant in the changing economic environment in which the Group operates.

For

per

sona

l use

onl

y

KRESTA HOLDINGS LIMITED—ANNUAL REPORT

Directors’ Report continued

4

OPERATING AND FINANCIAL REVIEW continued Operating results for the year The Group‟s earnings before interest and tax of $4,895,000 for the year ended 30 June 2010 was 23 per cent lower than the previous year of $6,329,000. The decrease was mainly due to the inventory write down to net realisable value (please see notes 3(g) and 9). Summarised operating results are as follows: 2010 Sales Results $‟000 $‟000

Consolidated entity sales and profit before income tax expense 122,630 3,921 Shareholder returns Management is pleased with the results of the Group especially after coming through a turbulent 2009 and the impact of the global financial crisis and a continued global uncertainty which impacted on consumer spending and high unemployment.

2010 2009 2008 2007

Basic earnings per share (cents) 1.88 2.68 3.22 3.00

Investments for future performance The Group continues to direct significant resources into product development and remains committed to constant improvements in the products that are manufactured and marketed by its businesses. Kresta is the holder of a number of patents and registered designs which have resulted from this ongoing strategy. The Group remains committed to providing staff with access to appropriate training and development. Management has also been charged with responsibility to focus on executive succession planning and the development of internal candidates for promotion to senior positions in the Group as these opportunities present themselves. Management is also focused on the enhancement of the Group‟s information technology systems, recognizing the need to constantly upgrade and improve inventory management and reporting capabilities. A software package (particularly tailored to support the window treatment business), has been selected and is currently under evaluation for introduction in the 2010/11 financial year. Capital structure The Group had a capital gearing ratio of 10% at year end (2009: 21%). Liquidity and funding At year end, the Group had credit facilities (inclusive of bank guarantee) totalling $14,433,827 (2009: $17,200,000). At year end, credit facilities unused were $3,376,188 (2009: $2,457,000). In November 2009, the Group has cancelled the temporary overdraft facility of $3,000,000 entered in February 2009 and negotiated an increase of $1,000,000 to the existing $2,000,000 overdraft facility and a temporary overdraft facility of $1,000,000 for a period of seven months from April to October 2010. This additional credit facility has not been utilized due to the success of the Group‟s focus on the reduction of inventories and debtors and the improvement in overall liquidity. Share issues during the year One million shares were issued from the conversion of options for the year ended 30 June 2010. (refer Share Options) SIGNIFICANT CHANGES IN THE STATE OF AFFAIRS There have been no significant changes in the state of affairs during the financial year and up to the date of this report. SIGNIFICANT EVENTS AFTER THE BALANCE DATE On 19 August 2010, the directors of Kresta Holdings Limited announced a final dividend on ordinary shares in respect of the 2010 financial year. The total amount of the dividend is $2,162,378 which represents a fully franked dividend of 1.5 cents per share. The dividend has not been provided for in the 30 June 2010 financial statements. LIKELY DEVELOPMENTS AND EXPECTED RESULTS It is the Kresta Board‟s view that the general economy and the retail trading environment remains patchy, particularly with the risk of global uncertainty, but the directors are confident that as a result of the success of the range of initiatives undertaken to date, coupled with the growth related strategies now in place, will ensure the Group is well positioned to continue to achieve sustained and profitable growth moving forward. The Group will also continue to focus on its strategy of conserving a strong cash position and controlling costs.

For

per

sona

l use

onl

y

KRESTA HOLDINGS LIMITED—ANNUAL REPORT

Directors’ Report continued

5

ENVIRONMENTAL REGULATION AND PERFORMANCE The consolidated entity holds licences issued by the relevant environmental protection authorities. These licences specify limits to, and regulate the management of, discharges to the air and water run-off associated with the manufacturing operations. There have been no significant known breaches of the consolidated entity‟s licence conditions or any environmental regulations to which it is subject to. SHARE OPTIONS Unissued shares As at the date of this report, there were no unissued shares under options. Shares issued as a result of the exercise of options During the financial year, executives have exercised options to acquire 1,000,000 fully paid ordinary shares in Kresta Holdings Limited at a weighted average exercise price of $0.285 per share. INDEMNIFICATION AND INSURANCE OF DIRECTORS AND OFFICERS During the financial year, the Company has paid premiums in respect of a contract insuring all the directors and officers of Kresta Holdings Limited and its controlled entities against legal costs incurred in defending proceedings for conduct involving: a) a wilful breach of duty; or b) a contravention of sections 182 or 183 of the Corporations Act 2001, as permitted by section 199B of the Corporations Act 2001. The total amount of insurance contract premiums paid was $10,875. DIRECTORS’ MEETINGS The number of meetings of directors (including meetings of committees of directors) held during the year and the number of meetings attended by each director was as follows:

Directors’ Meetings Meetings of Committees

Audit Remuneration Number of meetings held:

7 1 1 Number of meetings attended:

TJ Bartlett

7 1 1 NC Fearis

4 1 1 T Zorbas

7 - - P Johnston

6 1 1 P Hatfull

6 1 1 I Trahar

2 - -

For

per

sona

l use

onl

y

KRESTA HOLDINGS LIMITED—ANNUAL REPORT

Directors’ Report continued

6

Committee membership As at the date of this report, the Company had an Audit Committee and a Remuneration Committee. Members acting on the committees of the Board during the year were: Audit Remuneration

TJ Bartlett (Chairman) I Trahar* (New Chairman)

NC Fearis (retired 31 December 2009) P Johnston (retired 23 June 2010)

P Johnston (retired 23 June 2010) TJ Bartlett

P Hatfull P Hatfull

I Trahar* NC Fearis (Chairman) (retired 31 December 2009)

* I Trahar was appointed to the Audit and Remuneration Committees on 24 June 2010. ROUNDING The amounts contained in this report and in the financial report have been rounded to the nearest $1,000 (where rounding is applicable) under the option available to the Company under ASIC Class Order 98/0100. The Company is an entity to which the Class Order applies.

For

per

sona

l use

onl

y

KRESTA HOLDINGS LIMITED—ANNUAL REPORT

Directors’ Report continued

7

REMUNERATION REPORT (audited) This Remuneration Report outlines the director and executive remuneration arrangements of the Company and the Group in accordance with the requirements of the Corporation Act 2001 and its Regulations. For the purpose of this report, Key Management Personnel (KMP) of the Group are defined as those persons having authority and responsibility for planning, directing and controlling the major activities of the Company and the Group, directly or indirectly, including any director (whether executive or otherwise) of the parent Company, and includes the executives in the parent and the Group receiving the highest remuneration. Details of key management personnel (including the two highest paid executives of the Company and the Group)

(i) Directors NC Fearis Chairman (Non-Executive) (retired 31 December 2009) T Zorbas Managing Director (retired 6 September 2010) TJ Bartlett Director (Non-Executive) P Johnston Director (Non-Executive) (retired 23 June 2010) P Hatfull Director (Non-Executive) (appointed 14 July 2009) I Trahar Chairman (Non-Executive) (appointed 23 February 2010)

(ii) Executives T Tan Company Secretary and Chief Financial Officer J Fulton General Manager – Sales and Marketing

Remuneration philosophy The performance of the Company depends upon the quality of its directors and executives. To prosper, the Company must attract, motivate and retain highly skilled directors and executives. To this end, the Company embodies the following principles in its remuneration framework: - Provide competitive rewards to attract high calibre executives; - Link executive rewards to shareholder value; and - Establish appropriate, demanding performance hurdles for variable executive remuneration. Remuneration Committee The Remuneration Committee of the Board of Directors is responsible for determining and reviewing compensation arrangements for the directors, the managing director and executives. The Remuneration Committee assesses the appropriateness of the nature and amount of emoluments of such executives on a periodic basis by reference to relevant employment market conditions with the overall objective of ensuring maximum stakeholder benefit from the retention of a high quality board and executive team. Such executives are given the opportunity to receive their base emolument in a variety of forms including cash and fringe benefits such as motor vehicles and expense payment plans. It is intended that the manner of payment chosen will be optimal for the recipient without creating undue cost for the Company. To assist in achieving these objectives, the Remuneration Committee links the nature and amount of each executive‟s and director‟s emolument to the Group‟s financial and operational performance. All variable remuneration needs to be approved by the Remuneration Committee. Remuneration structure In accordance with best practice corporate governance, the structure of non-executive director and executive remuneration is separate and distinct. Non-executive director remuneration

Objective The Board seeks to set aggregate remuneration at a level which provides the Company with the ability to attract and retain directors of the highest calibre, whilst incurring a cost which is acceptable to the shareholders. Structure Each non-executive director receives a fee for being a director of the Company and the fees and payments reflect the demands which are made on, and the responsibilities of, the directors. No additional fee is paid for membership of Board committees.

Executive remuneration

Objective The Group aims to reward executives with a level and mix of remuneration commensurate with their position and responsibilities within the Company and so as to:

For

per

sona

l use

onl

y

KRESTA HOLDINGS LIMITED—ANNUAL REPORT

Directors’ Report continued

8

REMUNERATION REPORT (audited) continued

reward executives for company, business unit and individual performance against targets set by reference to appropriate benchmarks;

align the interests of executives with those of shareholders;

link reward with the strategic goals and performance of the Group; and

ensure total remuneration is competitive by market standards. Structure In consultation with external remuneration consultants, the remuneration committee has structured an executive remuneration framework that is market competitive and complimentary to the reward strategy of the organisation. Remuneration consists of the following key elements:

Fixed Remuneration;

Variable Remuneration; - Short Term Incentive (STI); and - Long Term Incentive (LTI).

The proportion of fixed remuneration and variable remuneration (potential short term and long term incentives) is established for each executive by the remuneration committee. The Group has no policy on executives and directors entering into contracts to hedge their exposure to options or shares granted as part of their remuneration package.

Fixed Remuneration

Objective The level of fixed remuneration is set so as to provide a base level of remuneration which is both appropriate to the position and is competitive in the market.

Fixed remuneration is reviewed annually by the remuneration committee and the process consists of a review of company, business unit and individual performance, relevant comparative remuneration externally and internally and, where appropriate, external advice on policies and practices. As noted above, the committee has access to external advice independent of management. Structure Executive directors and executives are given the opportunity to receive their fixed (primary) remuneration in a variety of forms including cash and fringe benefits such as motor vehicles. It is intended that the manner of payment chosen will be optimal for the recipient without creating undue cost for the Group. Variable remuneration – short term incentive (STI)

Objective The objective of the STI program is to link the achievement of the Group‟s operational targets with the remuneration received by the executives charged with meeting those targets. The total potential STI available is set at a level so as to provide sufficient incentive to the executive to achieve the operational targets and such that the cost to the Group is reasonable in the circumstances. Structure Actual STI payments granted to each executive depend on the extent to which specific operating targets set at the beginning of the financial year are met. The operational targets consist of a number of key performance indicators (KPIs) covering both financial and non-financial measures of performance. Typically included are measures such as budgeted contribution to net profit after tax, customer service, product management and risk management. These measures were chosen as they represent the key drivers for the short term success of the business and provide a framework for delivering long term value. On an annual basis, after consideration of performance against KPIs, an overall performance rating for the Group is approved by the remuneration committee. The aggregate of annual STI payments available for executives across the Group is subject to the approval of the remuneration committee. Payments made are usually delivered as a cash bonus and at the discretion of the remuneration committee. STI Bonus for 2010 financial year (2009: $115,000) 100% of the STI cash bonus of $97,750 relating to the 2008/9 financial year was accrued and vested to executives and was paid in the 2010 financial year. There were no forfeitures. Bonus payments were made at the discretion of the remuneration committee.

Variable remuneration – long term incentive (LTI)

Objective The objective of the LTI plan is to reward executives in a manner which aligns this element of remuneration with the creation of shareholder wealth. As such, LTI grants are only made to executive directors and executives who are able to influence the generation of shareholder wealth and thus have a direct impact on the Group‟s performance against the relevant long term performance hurdle.

For

per

sona

l use

onl

y

KRESTA HOLDINGS LIMITED—ANNUAL REPORT

Directors’ Report continued

9

REMUNERATION REPORT (audited) continued Structure LTI grants to executive directors and executives are delivered in the form of options. The share options generally vest over varying periods and are not usually subject to a performance hurdle as these options are issued to executives as a form of retention bonus and incentive to contribute to the creation of shareholder wealth. They usually have a life from the date of grant of five years, and are exercisable at specific dates and proportions set at the time of granting the options. Group performance The table below shows the performance of the Company (as measured by the Company‟s Return on Shareholders‟ Fund (ROSF) for the last five years for the period ended 30 June.

Employment contracts

Executives Mr Tan and Mr Fulton are employed under written contracts. The current contracts commenced on 16 May 2005. Under the terms of the present contracts:

Mr Tan and Mr Fulton may resign from their positions and thus terminate these contracts by giving 12 months‟ written notice. On resignation, any unvested options will be forfeited.

The Company may terminate the employment agreement by providing 12 months‟ written notice or provide payment in lieu of the notice period (based on the total remuneration). On termination on notice by the Company, any options that have vested or will vest during the notice period can be exercised within a period of two years. After which, the options will be forfeited.

The Company may terminate the contract at any time without notice if serious misconduct has occurred. Where termination with cause occurs, the executives are only entitled to that portion of remuneration which is fixed, and only up to the date of termination. On termination with cause, any unvested options will immediately be forfeited.

2010 2009 2008 2007 2006

ROSF 12% 15% 21% 20% 19%

For

per

sona

l use

onl

y

KRESTA HOLDINGS LIMITED—ANNUAL REPORT

Directors’ Report continued

10

REMUNERATION REPORT (audited) continued Details of the nature and amount of each element of the compensation of each key management personnel are as follows: Table 1: Remuneration for the years ended 30 June 2010 and 30 June 2009

Short -Term

Post

Employment

Share-based

Payment

Salary &

fees Cash bonus

Non-monetary benefits

Super- annuation Options# Total

Performance related

Option related

$ $ $ $ $ $ % %

NC Fearis 2010 37,500 - - - - 37,500 - -

2009 75,000 - - - - 75,000 - -

T Zorbas 2010 518,066 55,250 62,031 51,599 - 686,946 8.0 -

2009 463,643 65,000 52,676 47,578 - 628,897 10.3 -

P Johnston 2010 52,499 - - 4,725 - 57,224 - -

2009 55,000 - - 4,950 - 59,950 - -

TJ Bartlett 2010 45,833 - - 4,125 - 49,958 - -

2009 55,000 - - 4,950 - 59,950 - -

P Hatfull 2010 43,911 - - 3,952 - 47,863 - -

T Tan 2010 254,145 25,500 26,192 25,168 - 331,005 7.7 -

2009 225,354 30,000 23,090 22,982 2,488 303,914 10.7 0.8

J Fulton 2010 181,195 17,000 69,846 17,838 - 285,879 5.9 -

2009 156,760 20,000 65,168 15,909 - 257,837 7.7 -

# These are not benefits paid but a fair value measurement of the options granted using the Binomial Option-Pricing model. Options were granted as equity compensation benefits under the long-term incentive plan to certain key management personnel as disclosed above. The options were issued free of charge. Each option entitles the holder to subscribe for one fully paid ordinary share in the entity at an exercise price equal to the market price of the shares on the date of grant of the option. The contractual life of each option granted is five years. There are no cash settlement alternatives.

There were no options granted during the financial year to key management personnel and the Board of Directors.

For

per

sona

l use

onl

y

KRESTA HOLDINGS LIMITED—ANNUAL REPORT

Directors’ Report continued

11

REMUNERATION REPORT (audited) continued

Table 2: Shares issued on exercise of compensation options 30 June 2010

Shares Issued No.

Paid per share (note 13) $

Executives T Tan

1,000,000

0.285

For

per

sona

l use

onl

y

KRESTA HOLDINGS LIMITED—ANNUAL REPORT

Directors’ Report continued

12

AUDITOR’S INDEPENDENCE AND NON-AUDIT SERVICES

The directors received the following declaration from the auditor of Kresta Holdings Limited.

NON-AUDIT SERVICES The following non-audit services were provided by the entity‟s auditor, Ernst & Young. The directors are satisfied that the provision of non-audit services is compatible with the general standard of independence for auditors imposed by the Corporations Act 2001. The nature and scope of each type of non-audit service provided means that auditor independence was not compromised. Ernst & Young received or are due to receive the following amounts for the provision of non-audit services: $ Special audits required for government grants 5,923 Assurance related and due diligence services 78,337 84,260

Signed in accordance with a resolution of the directors.

I Trahar Chairman 30 September 2010

For

per

sona

l use

onl

y

KRESTA HOLDINGS LIMITED—ANNUAL REPORT

Corporate Governance Statement

13

The Board of Directors of Kresta Holdings Limited is responsible for establishing the corporate governance framework of the Group having regard to the ASX Corporate Governance Council (CGC) published guidelines as well as its corporate governance principles and recommendations. The Board guides and monitors the business and affairs of Kresta Holdings Limited on behalf of the shareholders by whom they are elected and to whom they are accountable.

Kresta Holdings Limited‟s Corporate Governance Statement is structured with reference to the Corporate Governance Council‟s principles and recommendations, which are as follows:

Principle 1. Lay solid foundations for management and oversight Principle 2. Structure the board to add value Principle 3. Promote ethical and responsible decision making Principle 4. Safeguard integrity in financial reporting Principle 5. Make timely and balanced disclosure Principle 6. Respect the rights of shareholders Principle 7. Recognise and manage risk Principle 8. Remunerate fairly and responsibly

Kresta Holdings Limited‟s corporate governance practices were in place throughout the year ended 30 June 2010 and were compliant with the Council‟s best practice recommendations, except for there being no separate nomination committee. To ensure the Board is well equipped to discharge its responsibilities, it has established guidelines for the nomination and selection of directors and for the operation of the Board.

Structure of the Board The structure of the Board is determined in accordance with the following policies and guidelines:

The Board should comprise at least three directors and should maintain a majority of non-executive directors.

The Chairman must be a non-executive director.

The Board should comprise directors with an appropriate range of qualifications and expertise; and

The Board shall meet at least once every two months. The directors in office at the date of this statement are:

Name Position Term in Office Independent

I Trahar Chairman, Non-Executive Director 4 months Yes

TJ Bartlett Non-Executive Director 6 years Yes

P Hatfull Non-Executive Director 1 year Yes

Audit Committee The Board has established an Audit Committee. It is the Board‟s responsibility to ensure that an effective internal control framework exists within the entity. This includes internal controls to deal with both the effectiveness and efficiency of significant business processes, including the safeguarding of assets, the maintenance of proper accounting records, and the reliability of financial information. The Board has delegated responsibility for the establishment and maintenance of a framework of internal controls and ethical standards for the management of the consolidated entity to the Audit Committee. The committee also provides the Board with additional assurance regarding the reliability of financial information for inclusion in the financial reports. All members of the Audit Committee are non-executive directors. The members of the Audit Committee during the year were:

Independent Executive

NC Fearis – retired 31 December 2009 Yes No

TJ Bartlett (Chairman) Yes No

P Johnston – retired 23 June 2010 Yes No

P Hatfull Yes No

I Trahar Yes No

For

per

sona

l use

onl

y

KRESTA HOLDINGS LIMITED—ANNUAL REPORT

Corporate Governance Statement continued

14

Nomination Committee The Board is responsible for selecting candidates for the position of director. There is no separate Nomination Committee. Remuneration Committee The Board is responsible for determining and reviewing compensation arrangements for the directors themselves, the managing director and executives. The Board has established a remuneration committee, comprising three non-executive directors. Members of the remuneration committee throughout the year were:

Independent Executive NC Fearis (Chairman) – retired 31 December 2009 Yes No TJ Bartlett Yes No P Johnston – retired 23 June 2010 Yes No P Hatfull Yes No I Trahar Yes No

Board responsibilities As the Board acts on behalf of and is accountable to the shareholders, it seeks to identify the expectations of the shareholders, as well as other regulatory and ethical expectations and obligations. In addition, the Board is responsible for identifying areas of significant business risk and ensuring arrangements are in place to adequately manage those risks. The Board seeks to discharge these responsibilities in a number of ways.

The responsibility for the operation and administration of the consolidated entity is delegated by the Board to the Managing Director and the executive team. The Board is responsible for setting the strategic direction of the Company, establishing goals for management and monitoring the achievement of those goals. The Managing Director is responsible to the Board for the day to day management of the Company.

The Board is responsible for ensuring that management‟s objectives and activities are aligned with the expectations and risks identified by the Board.

Managing Director and Chief Financial Officer declaration Consistent with ASX Principle 4, the company‟s financial report preparation and approval process for the financial year ended 30 June 2010, involved both the Managing Director and Chief Financial Officer providing a written statement to the Board that, to the best of their knowledge and belief, the Company‟s financial report presents a true and fair view, in all material respects, of the Company‟s financial condition and operating results and is in accordance with applicable accounting standards. Independence declaration In respect of financial years commencing on or after 1 July 2004, the Corporate Law Economic Reform Programme (Audit Reform and Corporate Disclosure) Act 2004 (“CLERP 9”) amendments to the Corporations Act 2001 require external auditors to make an annual independence declaration, addressed to the Board, declaring that the auditors have maintained their independence in accordance with CLERP 9 amendments and the rules of the professional accounting bodies. Ernst & Young has provided such a declaration to the Board for the financial year ended 30 June 2010. Attendance of external auditors at Annual General Meeting Consistent with ASX Principle 6 and CLERP 9, Ernst & Young attend, and are available to answer questions at, the Company‟s annual general meeting relating to the conduct of the audit and preparation of the audit report. Shareholders may submit questions for the external auditors to the Company Secretary no later than five business days before an annual general meeting. Risk identification and management Consistent with ASX Principle 7, the Company is committed to the identification, monitoring and management of risks associated with its business activities and has embedded in its management and reporting systems a number of risk management controls. These include:

guidelines and limits for approval of capital expenditure and investments;

a group compliance programme supported by approved guidelines and standards covering such key areas as safety, the environment, legal liability, risk identification, quantification and reporting and financial controls;

a comprehensive annual insurance programme;

annual budgeting and monthly reporting systems for all operations which enable the monitoring of progress against performance targets and the evaluation of trends; and

directors‟ financial due diligence questionnaires to management.

Management is ultimately responsible to the Board for the Group‟s system of internal control and risk management. The Audit Committee assists the Board in monitoring this role.

For

per

sona

l use

onl

y

KRESTA HOLDINGS LIMITED—ANNUAL REPORT

Corporate Governance Statement continued

15

In accordance with ASX Principle 7, the Managing Director and Chief Financial Officer have provided the Board with a written statement that:

the statement given with respect to the integrity of the financial statements (referred to under the heading “Financial Reporting”) was founded on a sound system of risk management and internal compliance and control which implements the policies adopted by the Board; and

the Company‟s risk management and internal compliance and control system was operating efficiently and effectively in all material respects.

Continuous disclosure The Company understands and respects that timely disclosure of price sensitive information is central to the efficient operation of the Australian Securities Exchange‟s securities market and has adopted a comprehensive policy covering announcements to the Australian Securities Exchange, prevention of elective or inadvertent disclosure, conduct of investor and analysts briefings, media communications, commenting on expected earnings, communication black-out periods and review of briefings and communications. The Company‟s continuous disclosure policy is consistent with ASX Principle 5. Communication to shareholders The Board of Directors aims to ensure that the shareholders, on whose behalf they act, are informed of all information necessary to assess the performance of the directors. Information is communicated to the shareholders through:

the annual report which is distributed to all shareholders;

the annual general meeting and other meetings called to obtain approval for Board action as appropriate; and

continuous disclosure notices and periodic filings lodged with the ASX.

For

per

sona

l use

onl

y

KRESTA HOLDINGS LIMITED—ANNUAL REPORT

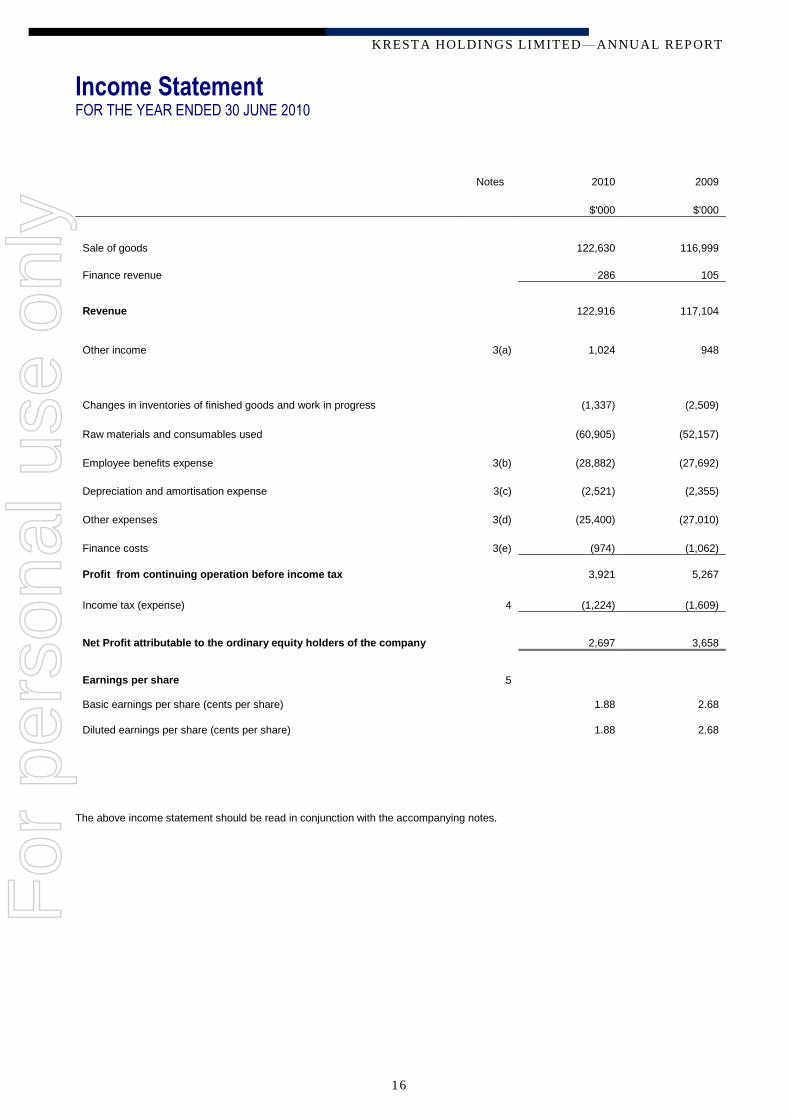

Income Statement FOR THE YEAR ENDED 30 JUNE 2010

16

Notes 2010 2009

$'000 $'000

Sale of goods 122,630 116,999

Finance revenue 286 105

Revenue 122,916 117,104

Other income 3(a) 1,024 948

Changes in inventories of finished goods and work in progress (1,337) (2,509)

Raw materials and consumables used (60,905) (52,157)

Employee benefits expense 3(b) (28,882) (27,692)

Depreciation and amortisation expense 3(c) (2,521) (2,355)

Other expenses 3(d) (25,400) (27,010)

Finance costs 3(e) (974) (1,062)

Profit from continuing operation before income tax 3,921 5,267

Income tax (expense) 4 (1,224) (1,609)

Net Profit attributable to the ordinary equity holders of the company 2,697 3,658

Earnings per share 5

Basic earnings per share (cents per share) 1.88 2.68

Diluted earnings per share (cents per share) 1.88 2.68

The above income statement should be read in conjunction with the accompanying notes.

For

per

sona

l use

onl

y

KRESTA HOLDINGS LIMITED—ANNUAL REPORT

Statement of comprehensive income FOR THE YEAR ENDED 30 JUNE 2010

17

2010 2009

$'000 $'000

Profit for the period 2,697 3,658

Other comprehensive income

Net foreign currency translation differences (77) (37)

Other comprehensive income for the period, net of tax (77) (37)

Total comprehensive income for the period 2,620 3,621

Total comprehensive income attributable to the ordinary equity holders of the company 2,620 3,621

For

per

sona

l use

onl

y

KRESTA HOLDINGS LIMITED—ANNUAL REPORT

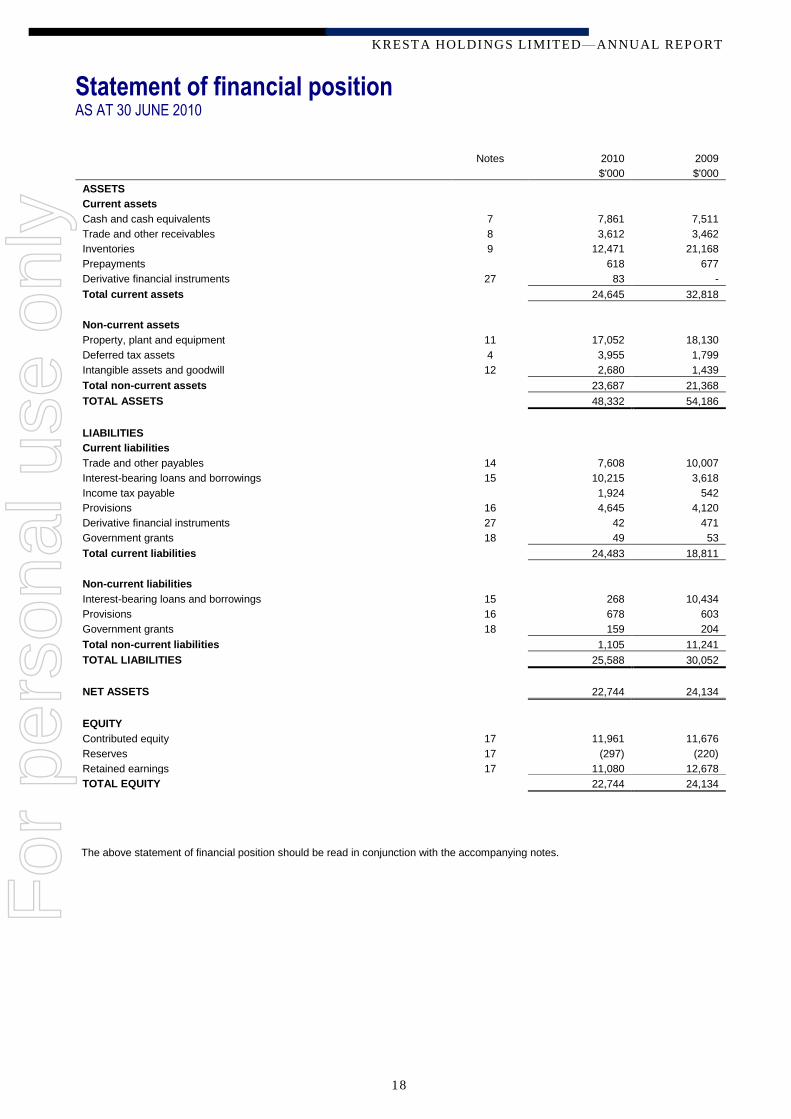

Statement of financial position AS AT 30 JUNE 2010

18

Notes 2010 2009

$'000 $'000

ASSETS

Current assets

Cash and cash equivalents 7 7,861 7,511

Trade and other receivables 8 3,612 3,462

Inventories 9 12,471 21,168

Prepayments 618 677

Derivative financial instruments 27 83 -

Total current assets 24,645 32,818

Non-current assets

Property, plant and equipment 11 17,052 18,130

Deferred tax assets 4 3,955 1,799

Intangible assets and goodwill 12 2,680 1,439

Total non-current assets 23,687 21,368

TOTAL ASSETS 48,332 54,186

LIABILITIES

Current liabilities

Trade and other payables 14 7,608 10,007

Interest-bearing loans and borrowings 15 10,215 3,618

Income tax payable 1,924 542

Provisions 16 4,645 4,120

Derivative financial instruments 27 42 471

Government grants 18 49 53

Total current liabilities 24,483 18,811

Non-current liabilities

Interest-bearing loans and borrowings 15 268 10,434

Provisions 16 678 603

Government grants 18 159 204

Total non-current liabilities 1,105 11,241

TOTAL LIABILITIES 25,588 30,052

NET ASSETS 22,744 24,134

EQUITY

Contributed equity 17 11,961 11,676

Reserves 17 (297) (220)

Retained earnings 17 11,080 12,678

TOTAL EQUITY 22,744 24,134

The above statement of financial position should be read in conjunction with the accompanying notes.

For

per

sona

l use

onl

y

KRESTA HOLDINGS LIMITED—ANNUAL REPORT

Statement of changes in equity FOR THE YEAR ENDED 30 JUNE 2010

19

Ordinary Foreign Employee Retained Total

shares currency equity earnings

translation benefits

reserve reserve

CONSOLIDATED $'000 $'000 $‟000 $'000 $'000

At 1 July 2009 11,676 (268) 48 12,678 24,134 Profit for the period - - - 2,697 2,697

Other comprehensive income - (77) - - (77)

Total comprehensive income for the period - (77) - 2,697 2,620

Transactions with owners in their capacity as owners

Dividends paid - - - (4,295) (4,295)

Share issued 285 - - - 285

At 30 June 2010 11,961 (345) 48 11,080 22,744

At 1 July 2008 10,679 (230) 46 10,351 20,846 Profit for the period - -

- 3,658 3,658

Other comprehensive income 1 (38)

-

- (37)

Total comprehensive income for the period 1 (38)

- 3,658 3,621

Transactions with owners in their capacity as owners

Share issued 1,000 - - - 1,000

Transaction costs on share issue (4) - - - (4)

Share-based payment - - 2 - 2

Dividends paid - - - (1,331) (1,331)

At 30 June 2009 11,676 (268) 48 12,678 24,134

The above statement of changes in equity should be read in conjunction with the accompanying notes.

For

per

sona

l use

onl

y

KRESTA HOLDINGS LIMITED—ANNUAL REPORT

Statement of cash flows FOR THE YEAR ENDED 30 JUNE 2010

20

Notes 2010 2009

$'000 $'000

Cash flows from operating activities

Receipts from customers 131,605 125,238

Payments to suppliers and employees (118,353) (113,416)

Receipt of government grants 475 457

Interest received 286 105

Interest paid (974) (1,062)

Income tax (paid)/received (1,999) (2,498)

Net cash flows from operating activities 7 11,040 8,824

Cash flows from investing activities

Proceeds from sale of property, plant and equipment 64 50

Purchase of property, plant and equipment (1,486) (5,011)

Acquisition of investment 23 (1,687) -

Net cash flows (used in) investing activities (3,109) (4,961)

Cash flows from financing activities

Proceeds from issue of shares - 1,000

Transaction costs on issue of shares - (4)

Options exercised 285 -

Equity dividend paid (4,295) (3,328)

Proceeds from borrowings 1,024 1,602

Repayment of borrowings (2,793) (3,011)

Net cash flows (used in) financing activities (5,779) (3,741)

Net increase in cash and cash equivalents 2,152 122

Net foreign exchange differences (1) 32

Cash and cash equivalents at beginning of period 5,710 5,556

Cash and cash equivalents at end of period 7 7,861 5,710

The above cash flow statement should be read in conjunction with the accompanying notes.F

or p

erso

nal u

se o

nly

KRESTA HOLDINGS LIMITED—ANNUAL REPORT

Notes to the Financial Statements FOR THE YEAR ENDED 30 JUNE 2010

21

1. CORPORATE INFORMATION

The financial report of Kresta Holdings Limited (the Company) for the year ended 30 June 2010 was authorised for issue in accordance with a resolution of the directors on 30 September 2010. Kresta Holdings Limited is a company limited by shares incorporated in Australia whose shares are publicly traded on the Australian Stock Exchange. The nature of the operations and principal activities of the Group are described in the Directors‟ Report.

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

a) Basis of preparation The financial report is a general-purpose financial report, which has been prepared in accordance with the requirements

of the Corporations Act 2001, Australian Accounting Standards and other authoritative pronouncements of the Australian Accounting Standards Board. The financial report has also been prepared on a historical cost basis except for derivative financial instruments, which have been measured at fair value.

The financial report is presented in Australian dollars and all values are rounded to the nearest thousand dollars ($‟000)

unless otherwise stated under the option available to the Company under ASIC Class Order 98/0100. The Company is an entity to which the Class Order applies.

b) Compliance with IFRS

The financial report complies with Australian Accounting Standard and International Financial Reporting Standards (IFRS) as issued by the International Accounting Standards Board.

c) New accounting standards and interpretations

Changes in accounting policy and disclosures Since 1 July 2009, the Group has adopted all the Standards and Interpretations, mandatory for annual periods beginning on or after 1 July 2009 including the following. Adoption of these Standards and Interpretations did not have any effect on the financial position or performance of the Group.

AASB 101 Presentation of Financial Statements (revised). The revised Standard separates owner and non-owner changes in equity and requires a statement of comprehensive income to be prepared which discloses all changes in equity during a period resulting from non-owner transactions. The Group has elected to present comprehensive income using the two statement approach.

AASB 8 Operating Segments. The Standard requires a management approach to be used for segment reporting and replaces the requirement to determine primary and secondary reporting segments of the Group. This approach identifies operating segments by reference to internal reports that are evaluated regularly by the chief operating decision maker in deciding how to allocate resources and in assessing performance. The adoption of the Standard did not have any effect on the financial position or performance of the Group and resulted in the same operating segment as reported in the Annual Financial Report for the year ended 30 June 2009.

AASB 3 Business Combinations (revised). The revised Standard introduces a number of changes to accounting for business combination, including the requirement to expense transaction costs, accounting for non controlling interests and the recognition of contingent consideration at fair value. The Group adopted this revised Standard as of 1 July 2009 and has amended its accounting policy accordingly.

Accounting standards and interpretations issued but not yet effective Applicable Australian Accounting Standards and Interpretations that have recently been issued or amended but are not yet effective have not been adopted by the Group for the annual reporting period ended 30 June 2010. These are outlined in the table below.

Reference

Title

Summary

Impact on Group financial report

Application

date for Group*

AASB 2009-5 Further Amendments to Australian Accounting Standards arising from the Annual Improvements Project

The amendments to some Standards result in accounting changes for presentation, recognition or measurement purposes, while some amendments that relate to terminology and

The Group is in the process to determine the extent of the impact of the amendments, if any.

1 July 2010 For

per

sona

l use

onl

y

KRESTA HOLDINGS LIMITED—ANNUAL REPORT

Notes to the Financial Statements FOR THE YEAR ENDED 30 JUNE 2010

22

Reference

Title

Summary

Impact on Group financial report

Application

date for Group*

editorial changes.

AASB 2009-8 Amendments to Australian Accounting Standards – Group Cash-settled Share-based Payment Transactions [AASB 2]

The amendments clarify the accounting for group cash-settled share-based payment transactions in the separate or individual financial statements of the entity receiving the goods or services when the entity has no obligation to settle the share-based payment transaction.

The Group is in the process to determine the extent of the impact of the amendments, if any

1 July 2010

AASB 9 and AASB 2009-11

Financial instruments and amendments to Australian Accounting Standards arising from AASB 9

The revised Standard includes requirements for the classification and measurement of financial assets resulting from the first part of Phase 1 of the IASB‟s project to replace IAS 39 Financial Instruments: Recognition and Measurement (AASB 139 Financial Instruments: Recognition and Measurement). These requirements improve and simplify the approach for classification and measurement of financial assets.

The potential effect of this Standard is yet to be fully determined. However, it is not expected that the revised Standard will significantly affect the Group‟s financial position.

1 July 2013

AASB 2009-12

Amendments to Australian Accounting Standards

This amendment makes numerous editorial changes to a range of Australian Accounting Standards and Interpretations.

No change to accounting policy required. Therefore no impact.

July 2011

AASB 2010-3 Amendments to Australian Accounting Standards arising from the Annual Improvements Project [AASB 3, AASB 7, AASB 121, AASB 128, AASB 131, AASB 132 & AASB 139]

Limits the scope of the measurement choices of non-controlling interest at proportionate share of net assets in the event of liquidation. Other components of NCI are measured at fair value. Requires an entity (in a business combination) to account for the replacements of the acquiree‟s share-based payment transactions. Clarifies that contingent consideration from a business combination that occurred before the effective date of AASB 3 Revised is not restated. Eliminates the requirement to restate financial statements for a reporting period when significant influence or joint control is lost and the reporting entity accounts for the remaining investment under AASB 139. This includes the effect on

The Group is in the process to determine the extent of the impact of the amendments, if any

1 July 2010

For

per

sona

l use

onl

y

KRESTA HOLDINGS LIMITED—ANNUAL REPORT

Notes to the Financial Statements FOR THE YEAR ENDED 30 JUNE 2010

23

Reference

Title

Summary

Impact on Group financial report

Application

date for Group*

accumulated foreign exchange differences on such investments.

AASB 2010-4 Further Amendments to Australian Accounting Standards arising from the Annual Improvements Project [AASB 1, AASB 7, AASB 101, AASB 134 and Interpretation 13]

Emphasis the interaction between quantitative and qualitative AASB 7 disclosures and the nature and extent of risks associated with financial instruments. Clarifies that an entity will present an analysis of other comprehensive income for each component of equity, either in the statement of changes in equity or in the notes to the financial statements. Provides guidance to illustrate how to apply disclosure principles in AASB 134 for significant events and transactions.

The potential effect of this Standard is yet to be fully determined. However, it is not expected that the revised Standard will significantly affect the Group‟s financial position.

1 January 2011

For

per

sona

l use

onl

y

KRESTA HOLDINGS LIMITED—ANNUAL REPORT

Notes to the Financial Statements continued FOR THE YEAR ENDED 30 JUNE 2010

24

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES continued d) Basis of consolidation

The consolidated financial statements comprise the financial statements of Kresta Holdings Limited and its subsidiaries as at and for the period ended 30 June each year (the Group). Subsidiaries are all those entities over which the Group has the power to govern the financial and operating policies so as to obtain benefits from their activities. The existence and effect of potential voting rights that are currently exercisable or convertible are considered when assessing whether a group controls another entity. The financial statements of subsidiaries are prepared for the same reporting period as the parent company, using consistent accounting policies. In preparing the consolidated financial statements, all intercompany balances and transactions, income and expenses and profit and losses resulting from intra-group transactions have been eliminated in full. Subsidiaries are fully consolidated from the date on which control is obtained by the Group and cease to be consolidated from the date on which control is transferred out of the Group. Investments in subsidiaries are accounted for at cost in the parent entity less any impairment charges. Dividends received from subsidiaries are recorded as a component of other revenues in the parent entity and do not impact the recorded cost of the investment. The acquisition of subsidiaries is accounted for using the acquisition method of accounting. The acquisition method of accounting involves recognising at acquisition date, separately from goodwill, the identifiable assets acquired, the liabilities assumed and any non-controlling interest in the acquiree. The identifiable assets acquired and liabilities assumed are measured at their acquisition date fair values (see note (e)). The difference between the above items and the fair value of the consideration (including the fair value of any pre-existing investment in the acquiree) is goodwill or a discount on acquisition.

e) Business combination - refer to note 23 Subsequent to 1 July 2009 Business combinations are accounted for using the acquisition method. The consideration transferred in a business

combination shall be measured at fair value, which shall be calculated as the sum of the acquisition date fair values of assets transferred by the acquirer, the liabilities incurred by the acquirer to former owners of the acquiree and the equity issued by the acquirer, and the amount of any non-controlling interest in the acquiree. For each business combination, the acquirer measures the non-controlling interest in the acquiree either at fair value or at the proportionate share of the acquiree‟s identifiable net assets. Acquisition-related costs are expensed as incurred.

When the Group acquires a business, it assesses the financial assets and liabilities assumed for appropriate classification and

designation in accordance with the contractual terms, economic conditions, the Group‟s operating or accounting policies and other pertinent conditions as at the acquisition date. This includes the separation of embedded derivatives in host contracts by the acquiree.

If the business combination is achieved in stages, the acquisition date fair value of the acquirer‟s previously held equity interest

in the acquiree is remeasured at fair value as at the acquisition date through profit or loss. Any contingent consideration to be transferred by the acquirer will be recognised at fair value at the acquisition date.

Subsequent changes to the fair value of the contingent consideration which is deemed to be an asset or liability will be recognised in accordance with AASB 139 either in profit or loss in other comprehensive income. If the contingent consideration is classified as equity, it shall not be remeasured.

Prior to 1 July 2009

Business combinations were accounted for using the purchase method. Transaction costs directly attributable to the acquisition formed part of the acquisition costs. The non-controlling interest (formerly known as minority interest) was measured at the proportionate share of the acquiree‟s identifiable assets.

Business combinations achieved in stages were accounted for in separate steps. Any additional interest in the acquiree

acquired did not affect previously recognised goodwill. The goodwill amounts calculated at each step acquisition were accumulated.

When the Group acquired a business, embedded derivatives separated from the host contract by the acquiree were not

reassessed on acquisition unless the business combination resulted in a change in the terms of the contract that significantly modified the cash flows that otherwise would have been required under the contract.

Contingent consideration was recognised if, and only if, the Group had a present obligation, the economic outflow was more

likely than not and a reliable estimate was determinable. Subsequent adjustments to the contingent consideration were adjusted against goodwill.

For

per

sona

l use

onl

y

KRESTA HOLDINGS LIMITED—ANNUAL REPORT

Notes to the Financial Statements continued FOR THE YEAR ENDED 30 JUNE 2010

25

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES continued f) Significant accounting judgements, estimates and assumptions

The preparation of the financial statements requires management to make judgements, estimates and assumptions that affect the reported amounts in the financial statements. In the process of applying the Group‟s accounting policies, management has made the following judgements, apart from those involving estimations, which have the most significant effect on the amounts recognised in the financial statements. (i) Significant accounting judgements

Related parties The Group determines whether the amounts carried as intercompany balances and / or the investment in controlled entities is recoverable at least on an annual basis. The carrying amount of the intercompany balances and / or investment is assessed against the net assets of the controlled entity to determine any impairment. Lease classification Where the Group enters into a lease arrangement the risks and rewards of ownership are assessed. Where they are deemed to pass to the Group the lease is classified as a finance lease. Where the risk and rewards of ownership are deemed to remain with the lessor, the lease is classified as an operating lease.

(ii) Significant accounting estimates and assumptions The carrying amounts of certain assets and liabilities are often determined based on estimates and assumptions of future events. The key estimates and assumptions that have a significant risk of causing a material adjustment to the carrying amounts of certain assets and liabilities within the next annual reporting period are:

Impairment of goodwill The Group determines whether goodwill is impaired at least on an annual basis. This requires an estimation of the recoverable amount of the cash generating units to which the goodwill is allocated. The assumptions used in this estimation of recoverable amount and the carrying amount of goodwill are discussed in note 12. Share based payment The Group measures the cost of equity-settled transactions with employees by reference to the fair value of the equity instruments at the date at which they are granted. The fair value is determined using a Binomial Option-Pricing model. Inventory net realisable value The Group accounts for inventory at the lower of cost or net realisable value. Net realisable value assessments necessitate management‟s best estimate as to the ability of individual inventory items to be sold above cost.

g) Revenue recognition – refer to note 3 Revenue is recognised and measured at the fair value of the consideration received or receivable to the extent that it is probable that the economic benefits will flow to the Group and the revenue can be measured reliably. The following specific recognition criteria must also be met before revenue is recognised. Sale of goods Revenue from sale of goods is recognised when the significant risks and rewards of ownership of the goods have passed to the buyer and the costs incurred or to be incurred in respect of the transaction can be measured reliably. Risks and rewards of ownership are considered passed to the buyer at the time when the goods become available for delivery under a binding sales agreement. Interest revenue Revenue is recognised as the interest accrues using the effective interest method. This is a method of calculating the amortised cost of a financial asset allocating the interest income over the relevant period using the effective interest rate, which is the rate that exactly discounts estimated future cash receipts through the expected life of the financial asset to the net carrying amount of the financial asset.

Dividends Revenue is recognised when the Group‟s right to receive the payment is established.

h) Government grants – refer to note 18

Government grants are recognised in the statement of financial position as a liability when the grant is received. When the grant relates to an expense item, it is recognised as income over the periods necessary to match the grant on a systematic basis to the costs that it is intended to compensate. When the grant relates to an asset, the fair value is credited to a deferred income account and is released to the statement of comprehensive income over the expected useful life of the relevant asset by equal annual instalments.

For

per

sona

l use

onl

y

KRESTA HOLDINGS LIMITED—ANNUAL REPORT

Notes to the Financial Statements continued FOR THE YEAR ENDED 30 JUNE 2010

26

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES continued

i) Leases – refer to note 15

The determination of whether an arrangement is or contains a lease is based on the substance of the arrangement and requires an assessment of whether the fulfilment of the arrangement is dependent on the use of a specific asset or assets and the arrangement conveys a right to use the asset. Group as a lessee Finance leases, which transfer to the Group substantially all the risks and benefits incidental to ownership of the leased item, are capitalised at the inception of the lease at the fair value of the leased asset or, if lower, at the present value of the minimum lease payments. Lease payments are apportioned between the finance charges and reduction of the lease liability so as to achieve a constant rate of interest on the remaining balance of the liability. Finance charges are recognised as an expense in profit or loss. Capitalised leased assets are depreciated over the shorter of the estimated useful life of the asset or the lease term if there is no reasonable certainty that the Group will obtain ownership by the end of the lease term.

Operating lease payments are recognised as an expense in the statement of comprehensive income on a straight-line basis over the lease term. Operating lease incentives are recognized as liability when received and subsequently reduced by allocating lease payments between rental expenses and reduction of the liability.

j) Cash and cash equivalents – refer note 7 Cash and cash equivalents in the statement of financial position comprise cash at bank and cash in hand.

For the purposes of the statement of cash flows, cash and cash equivalents consist of cash and cash equivalents as defined above, net of outstanding bank overdrafts. Bank overdrafts are included within interest-bearing loans and borrowings in current liabilities on the statement of financial position.

k) Trade and other receivables – refer to note 8

Trade receivables, which generally have 30-60 day terms, are recognised and carried at original invoice amount less an allowance for any uncollectible amounts. Collectability of trade receivables is reviewed on an ongoing basis. Debts that are known to be uncollectible are written off when identified. An impairment allowance is recognised when there is objective evidence that the Group will not be able to collect the debts. Failure to collect debts after debt collection procedures and enforcements are considered objective evidence of impairment. The amount of the impairment loss is the carrying amount of the impaired receivables.

l) Inventories – refer to note 9 Inventories including raw materials and finished goods are valued at the lower of cost and net realisable value. Costs incurred in bringing each product to its present location and condition are accounted for as follows: Raw materials – purchase cost on a first in first out basis; and

Finished goods – cost of direct materials, for manufactured finished goods labour and a proportion of manufacturing overheads based on normal operating capacity but excluding borrowing costs. Costs are assigned on the basis of weighted average costs. Net realisable value is the estimated selling price in the ordinary course of business, less estimated costs of completion and the estimated costs necessary to make the sale.

m) Derivative financial instruments – refer to note 27 The Group uses derivative financial instruments such as forward currency contracts and interest rate swaps to manage its risks associated with foreign currency and interest rate fluctuations. Such derivative financial instruments are initially recognised at fair value on the date on which a derivative contract is entered into and are subsequently remeasured to fair value. Derivatives are carried as assets when their fair value is positive and as liabilities when their fair value is negative. As hedge accounting is not applied, any gains or losses arising from changes in the fair value of derivatives are taken directly to profit or loss for the year. The fair value of forward currency contracts is calculated by reference to current forward exchange rates for contracts with similar maturity profiles. The forward currency contracts are usually no longer than 12 months. The fair values of interest rates swaps are determined using a standard pricing methodology with reference to the market rates and terms.

For

per

sona

l use

onl

y

KRESTA HOLDINGS LIMITED—ANNUAL REPORT

Notes to the Financial Statements continued FOR THE YEAR ENDED 30 JUNE 2010

27

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES continued n) Foreign currency translation