Embed Size (px)

Citation preview

ABC Islamic Bank (E.C.)

INTERIM CONDENSED CONSOLIDATED

FINANCIAL STATEMENTS

30 June 2020 (REVIEWED)

A member firm of Ernst & Young Global Limited

Ernst & Young — Middle East P.O. Box 140 East Tower — 10th floor Bahrain World Trade Center Manama Kingdom of Bahrain

Tel: +973 1753 5455 Fax: +973 1753 5405 [email protected] www.ey.com/mena C.R. no. 29977-1

REPORT ON REVIEW OF INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS TO THE BOARD OF DIRECTORS OF ABC ISLAMIC BANK (E.C.) Introduction

We have reviewed the accompanying interim consolidated statement of financial position of ABC Islamic Bank (E.C.) ["the Bank"] and its subsidiary [together "the Group"] as of 30 June 2020, and the related interim consolidated statement of income, cash flows, changes in owners' equity and sources and uses of Zakah and charity funds for the six month period then ended and explanatory notes. The Board of Directors are responsible for the preparation and presentation of these interim condensed consolidated financial statements in accordance with the basis of preparation and accounting policies as set out in note 2. Our responsibility is to express a conclusion on these interim condensed consolidated financial statements based on our review. Scope of Review

We conducted our review in accordance with International Standards on Review Engagements 2410, "Review of Interim Financial Information Performed by the Independent Auditor of the Entity". A review of interim financial information consists of making inquiries, primarily of persons responsible for financial and accounting matters, and applying analytical and other review procedures. A review is substantially less in scope than an audit conducted in accordance with International Standards on Auditing and consequently does not enable us to obtain assurance that we would become aware of all significant matters that might be identified in an audit. Accordingly, we do not express an audit opinion. Conclusion

Based on our review, nothing has come to our attention that causes us to believe that the accompanying interim condensed consolidated financial statements are not prepared, in all material respects, in accordance with the accounting policies disclosed in note 2 of the interim condensed consolidated financial statements.

13 August 2020 Manama, Kingdom of Bahrain

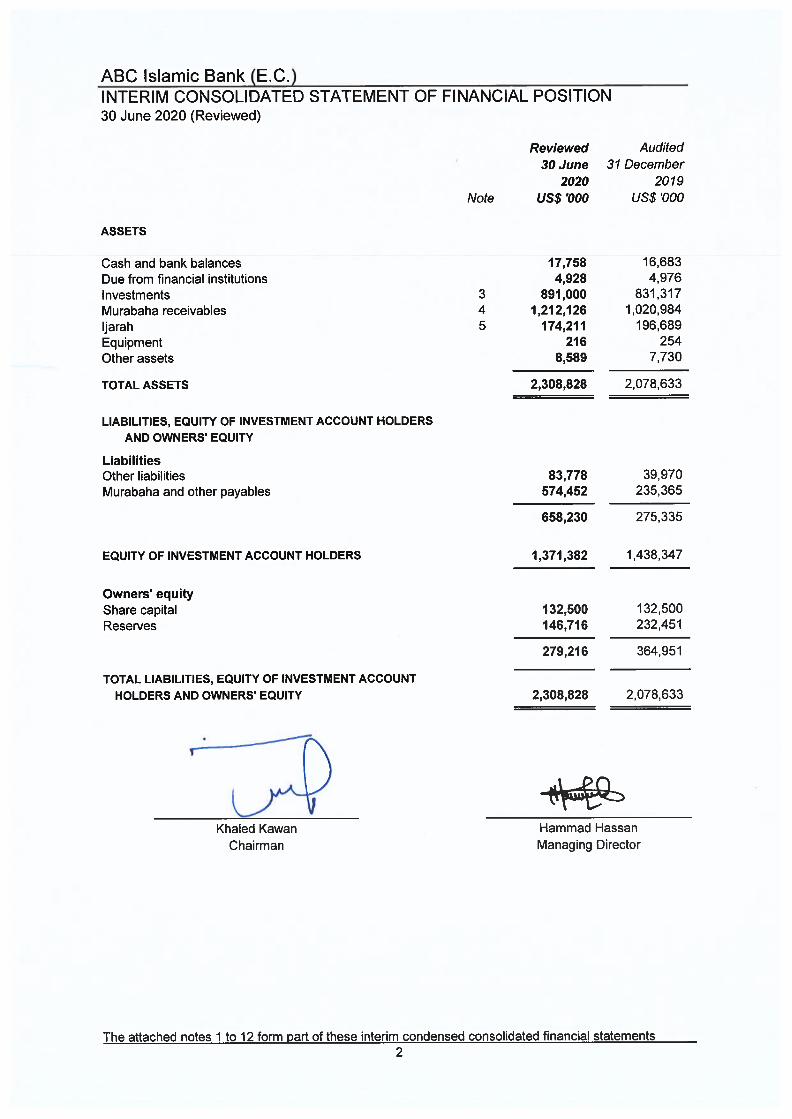

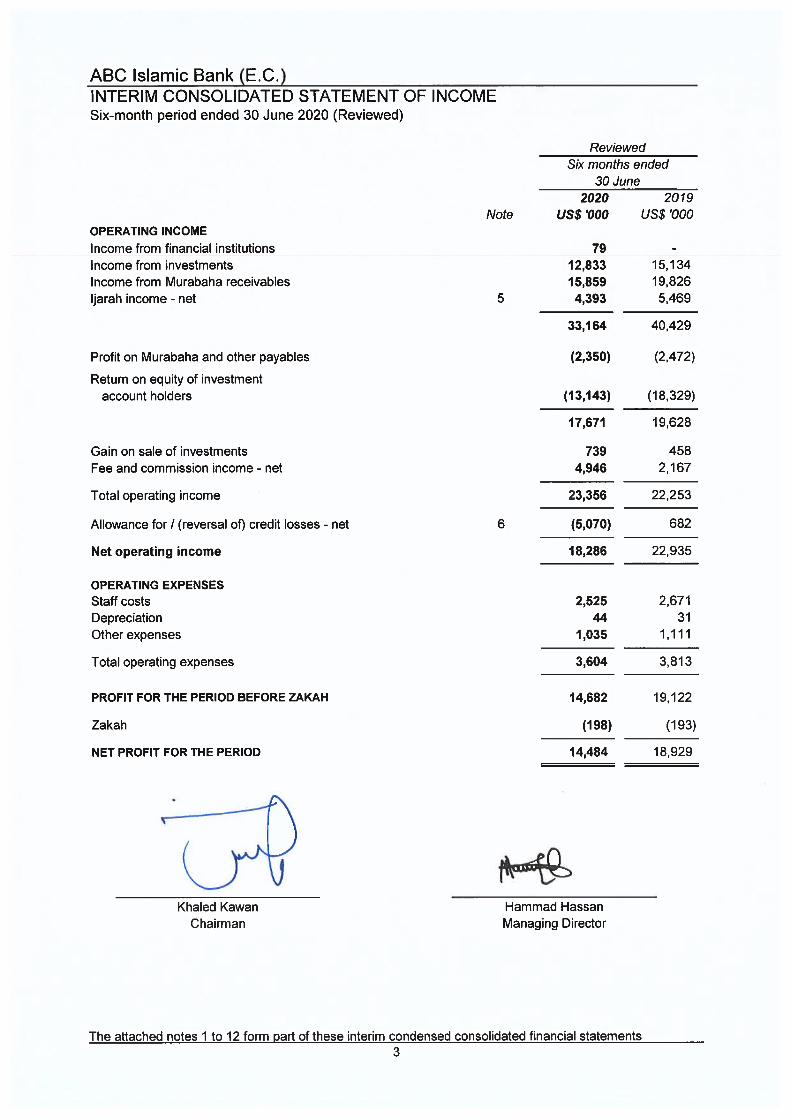

ABC Islamic Bank (E.C.)INTERIM CONSOLIDATED STATEMENT OF CASH FLOWSSix-month period ended 30 June 2020 (Reviewed)

2020 2019

Note US$ '000 US$ '000

OPERATING ACTIVITIES

Net profit for the period 14,484 18,929

Adjustments for:

Depreciation 44 31

Gain on sale of investments (739) (458)

Allowance for credit losses - net 6 5,070 (682)

Operating profit before changes in operating assets and liabilities 18,859 17,820

Murabaha receivables (188,088) (3,321)

Ijarah 20,720 17,871

Other assets (860) 1,134

Murabaha and other payables 339,087 (57,443)

Other liabilities 44,408 21,227

Equity of Investment account holders (66,965) -

Net cash flows from / (used in) operating activities 167,161 (2,712)

INVESTING ACTIVITIES

Purchase of investments (209,404) (70,127)

Proceeds from redemption / sale of investments 143,324 99,609

Purchase of equipment (6) (315)

Net cash (used in) / flows from investing activities (66,086) 29,167

FINANCING ACTIVITY

Dividend paid to the shareholder (100,000) (24,000)

Cash used in financing activity (100,000) (24,000)

NET CHANGE IN CASH AND CASH EQUIVALENTS 1,075 2,455

Cash and cash equivalents at the beginning of the period 16,683 5,454

CASH AND CASH EQUIVALENTS AT THE END OF THE PERIOD 17,758 7,909

Reviewed

Six months ended

30 June

Changes in:

The attached notes 1 to 12 form part of these interim condensed consolidated financial statements____________________________________________________________________________________

4

ABC Islamic Bank (E.C.)INTERIM CONSOLIDATED STATEMENT OF CHANGES IN OWNERS' EQUITYSix-month period ended 30 June 2020 (Reviewed)

Investments Total

Share Statutory fair value Retained Total Owners'

capital reserve reserve earnings reserves equity

US$ '000 US$ '000 US$ '000 US$ '000 US$ '000 US$ '000

1 January 2020 132,500 31,348 1,087 200,016 232,451 364,951

Net profit for the period - - - 14,484 14,484 14,484

Cumulative changes in fair value - - (219) - (219) (219)

Dividend Paid - - - (100,000) (100,000) (100,000)

At 30 June 2020 (Reviewed) 132,500 31,348 868 114,500 146,716 279,216

At 1 January 2019 132,500 27,613 1,306 190,406 219,325 351,825

Net profit for the period - - - 18,929 18,929 18,929

Cumulative changes in fair value - - (153) - (153) (153)

Dividend Paid - - - (24,000) (24,000) (24,000)

At 30 June 2019 (Reviewed) 132,500 27,613 1,153 185,335 214,101 346,601

Reserves

The attached notes 1 to 12 form part of these interim condensed consolidated financial statements________________________________________________________________________________________

5

ABC Islamic Bank (E.C.)

Six-month period ended 30 June 2020 (Reviewed)

2020 2019

US$ '000 US$ '000

Sources of Zakah and charity funds

Balance at 1 January 514 580

Charity 22 23

Zakah due from the Bank 198 193

Total sources of Zakah and charity funds 734 796

Uses of Zakah and charity funds

Zakah and charity paid to the poor and needy (334) (482)

Undistributed Zakah and charity

funds at end of the period 400 314

INTERIM CONSOLIDATED STATEMENT OF SOURCES AND USES OF

ZAKAH AND CHARITY FUNDS

Reviewed

Six months ended

30 June

The attached notes 1 to 12 form part of these interim condensed consolidated financial statements____________________________________________________________________________________

6

ABC Islamic Bank (E.C.)

30 June 2020 (Reviewed)

1 INCORPORATION AND ACTIVITIES

Nature of Date of Country of Amount and

Name business incorporation incorporation % of holding

ABC Clearing Islamic Investment 30 November Cayman US$ 2,000

Company Company Islands 100% management

shares

2 BASIS OF PREPARATION AND SIGNIFICANT ACCOUNTING POLICIES

2.1 Accounting convention

2.2 Basis of preparation

(a)

1993

NOTES TO THE INTERIM CONDENSED CONSOLIDATED FINANCIAL

STATEMENTS

ABC Islamic Bank (E.C.) [the Bank] is an exempt joint stock company incorporated in the Kingdom of

Bahrain on 10 December 1985 and registered with the Ministry of Industry, Commerce and Tourism

under commercial registration number 16864. The Bank and its subsidiary [together the Group] operate

under a wholesale banking license issued by the Central Bank of Bahrain [the CBB] and are engaged in

financial trading in accordance with the teachings of Islam (Shari’a). The postal address of the Bank’s

registered office is P O Box 2808, Manama, Kingdom of Bahrain.

Arab Banking Corporation (B.S.C.) [ABC (B.S.C.)], which operates under a wholesale banking license

issued by the CBB, holds 100% of the share capital of the Bank.

The Bank’s Shari’a Supervisory Board is entrusted with the responsibility to ensure the Group’s

adherence to Shari’a rules and principles in its transactions and activities.

The ownership in the subsidiary of the Bank as at 30 June 2020 is as follows:

The interim condensed consolidated financial statements were authorised for issue by a resolution of the

Board of Directors on 13 August 2020.

The Bank operates only in the Kingdom of Bahrain and does not have any branches.

The interim condensed consolidated financial statements are prepared under the historical cost

convention as modified for measurement at fair value of "equity type instruments carried at fair value

through equity" and Tabdeel.

The interim condensed consolidated financial statements have been presented in United States Dollars

[US$], being the functional currency of the Bank. All values are rounded to the nearest thousand (US$

'000) unless otherwise stated.

The interim condensed consolidated financial statements of the Group have been prepared in

accordance with applicable rules and regulations issued by the Central Bank of Bahrain (“CBB”)

including the recently issued CBB circulars on regulatory concessionary measures in response to

COVID-19. These rules and regulations, in particular CBB circular OG/226/2020 dated 21 June 2020,

require the adoption of all Financial Accounting Standards (“FAS”) issued by the Accounting and

Auditing Organisation of Islamic Financial Institutions (AAOIFI) with two exceptions which are set out

below. In accordance with the AAOIFI framework, for matters not covered by FAS, the Group uses the

requirements of the relevant International Financial Reporting Standards (“IFRS”) issued by the

International Accounting Standards Board (“IASB”). This framework is referred to as “FAS issued by

AAOIFI”.

The two exceptions mentioned above are as follows:

recognition of modification losses on financial assets arising from payment holidays provided to

customers impacted by COVID-19 without charging additional profit, in equity instead of profit or

loss as required by FAS issued by AAOIFI. Any other modification gain or loss on financial

assets are recognised in accordance with the requirements of FAS issued by AAOIFI. Refer note

2.2.2 for further details;

____________________________________________________________________________________

7

ABC Islamic Bank (E.C.)

30 June 2020 (Reviewed)

NOTES TO THE INTERIM CONDENSED CONSOLIDATED FINANCIAL

STATEMENTS

2 BASIS OF PREPARATION AND SIGNIFICANT ACCOUNTING POLICIES (continued)

2.2 Basis of preparation (continued)

(b)

2.2.1 COVID - 19

2.2.2 GOVERNMENT GRANTS

Government grants are recognised where there is reasonable assurance that the grant will be received

and all attached conditions will be complied with. When the grant relates to an expense item, it is

recognised as income on a systematic basis over the periods that the related costs, for which it is

intended to compensate, are expensed. When the grant relates to an asset, it is recognised as income

in equal amounts over the expected useful life of the related asset.

When the Group receives grants of non-monetary assets, the asset and the grant are recorded at

nominal amounts and released to profit or loss over the expected useful life of the asset, based on the

pattern of consumption of the benefits of the underlying asset by equal annual instalments.

COVID-19 pandemic has spread across various geographies globally, causing disruption to business

and economic activities. COVID-19 has brought about uncertainties in the global economic environment.

The fiscal and monetary authorities, both domestic and international, have announced various support

measures across the globe to counter possible adverse implications. In addition, the Group’s operations

are mainly based in economies that are relatively more dependent on the price of crude oil and natural

gas. During the first half of 2020, oil prices have witnessed unprecedented volatility and the reduction in

prices is expected to have medium to long term adverse consequences on these economies.

The interim condensed consolidated financial statements do not contain all information and disclosures

required in the annual consolidated financial statements, and should be read in conjunction with the

annual consolidated financial statements as at 31 December 2019. In addition, results for the six months

period ended 30 June 2020 are not necessarily indicative of the results that may be expected for the

financial year ending 31 December 2020.

Government assistance amounting to USD 248 thousand is recorded in profit or loss during the current

period as the Bank had no modification losses to be recorded in equity (in line with note 2.2 (a)). The

amount was recorded as a deduction from related expenses in the interim consolidated statement of

income.

recognition of financial assistance received from the government and/ or regulators in response

to its COVID-19 support measures that meets the government grant requirement, in equity,

instead of profit or loss. This will only be to the extent of any modification loss recorded in equity

as a result of (a) above, and the balance amount to be recognized in profit or loss. Any other

financial assistance is recognised in accordance with the relevant requirements of FAS issued by

AAOIFI. Refer note 2.2.2 for further details.

FAS issued by AAOIFI alongwith the two exceptions is above referred to as “FAS issued by AAOIFI as

modified by the CBB” and has been applied retrospectively along with the changes in accounting policies

due to adoption of new FAS as discussed in note 2.3 and did not result in any change to the financial

information reported for the comparative period. The interim condensed consolidated financial

statements of the Group have been prepared in accordance with the guidance provided by International

Accounting Standard 34 – ‘Interim Financial Reporting’ using FAS issued by AAOIFI as modified by the

CBB framework.

These two exceptions did not require any adjustment to the financial information included in the interim

condensed consolidated financial statements.

____________________________________________________________________________________

8

ABC Islamic Bank (E.C.)

30 June 2020 (Reviewed)

2 BASIS OF PREPARATION AND SIGNIFICANT ACCOUNTING POLICIES (continued)

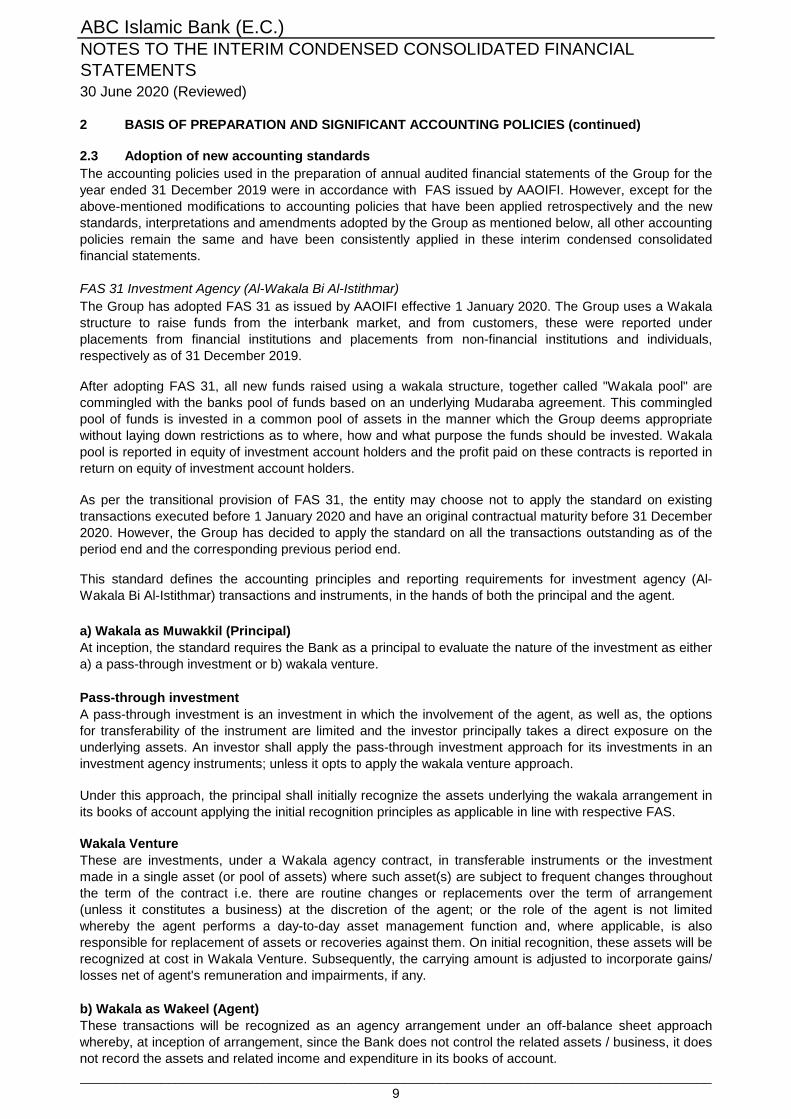

2.3 Adoption of new accounting standards

FAS 31 Investment Agency (Al-Wakala Bi Al-Istithmar)

a) Wakala as Muwakkil (Principal)

Pass-through investment

Wakala Venture

b) Wakala as Wakeel (Agent)

This standard defines the accounting principles and reporting requirements for investment agency (Al-

Wakala Bi Al-Istithmar) transactions and instruments, in the hands of both the principal and the agent.

NOTES TO THE INTERIM CONDENSED CONSOLIDATED FINANCIAL

STATEMENTS

At inception, the standard requires the Bank as a principal to evaluate the nature of the investment as either

a) a pass-through investment or b) wakala venture.

A pass-through investment is an investment in which the involvement of the agent, as well as, the options

for transferability of the instrument are limited and the investor principally takes a direct exposure on the

underlying assets. An investor shall apply the pass-through investment approach for its investments in an

investment agency instruments; unless it opts to apply the wakala venture approach.

Under this approach, the principal shall initially recognize the assets underlying the wakala arrangement in

its books of account applying the initial recognition principles as applicable in line with respective FAS.

These are investments, under a Wakala agency contract, in transferable instruments or the investment

made in a single asset (or pool of assets) where such asset(s) are subject to frequent changes throughout

the term of the contract i.e. there are routine changes or replacements over the term of arrangement

(unless it constitutes a business) at the discretion of the agent; or the role of the agent is not limited

whereby the agent performs a day-to-day asset management function and, where applicable, is also

responsible for replacement of assets or recoveries against them. On initial recognition, these assets will be

recognized at cost in Wakala Venture. Subsequently, the carrying amount is adjusted to incorporate gains/

losses net of agent's remuneration and impairments, if any.

These transactions will be recognized as an agency arrangement under an off-balance sheet approach

whereby, at inception of arrangement, since the Bank does not control the related assets / business, it does

not record the assets and related income and expenditure in its books of account.

The Group has adopted FAS 31 as issued by AAOIFI effective 1 January 2020. The Group uses a Wakala

structure to raise funds from the interbank market, and from customers, these were reported under

placements from financial institutions and placements from non-financial institutions and individuals,

respectively as of 31 December 2019.

After adopting FAS 31, all new funds raised using a wakala structure, together called "Wakala pool" are

commingled with the banks pool of funds based on an underlying Mudaraba agreement. This commingled

pool of funds is invested in a common pool of assets in the manner which the Group deems appropriate

without laying down restrictions as to where, how and what purpose the funds should be invested. Wakala

pool is reported in equity of investment account holders and the profit paid on these contracts is reported in

return on equity of investment account holders.

As per the transitional provision of FAS 31, the entity may choose not to apply the standard on existing

transactions executed before 1 January 2020 and have an original contractual maturity before 31 December

2020. However, the Group has decided to apply the standard on all the transactions outstanding as of the

period end and the corresponding previous period end.

The accounting policies used in the preparation of annual audited financial statements of the Group for the

year ended 31 December 2019 were in accordance with FAS issued by AAOIFI. However, except for the

above-mentioned modifications to accounting policies that have been applied retrospectively and the new

standards, interpretations and amendments adopted by the Group as mentioned below, all other accounting

policies remain the same and have been consistently applied in these interim condensed consolidated

financial statements.

______________________________________________________________________________________

9

ABC Islamic Bank (E.C.)

30 June 2020 (Reviewed)

NOTES TO THE INTERIM CONDENSED CONSOLIDATED FINANCIAL

STATEMENTS

2 BASIS OF PREPARATION AND SIGNIFICANT ACCOUNTING POLICIES (continued)

2.3 Adoption of new accounting standards (continued)

b) Wakala as Wakeel (Agent) (continued)

c) Multi level arrangements

3 INVESTMENTS

At 30 June 2020 (Reviewed) Fair value

Amortised through

cost equity Total

US$ '000 US$ '000 US$ '000

Debt type

Quoted investments

Sukuk 905,142 - 905,142

Equity type

Quoted investments

Equity shares - 2,412 2,412

905,142 2,412 907,554

Allowance for credit losses - net (16,554) - (16,554)

888,588 2,412 891,000

At 31 December 2019 (Audited) Fair value

Amortised through

cost equity Total

US$ '000 US$ '000 US$ '000

Debt type

Quoted investments

Sukuk 838,323 - 838,323

Equity type

Quoted investments

Equity shares - 2,631 2,631

838,323 2,631 840,954

Allowance for credit losses - net (9,637) - (9,637)

828,686 2,631 831,317

From agent perspective, a multi-level investment arrangement is maintained, whereby the Bank invests

funds under the investment agency into unrestricted investment arrangements, under a separate Mudaraba

contract which is accounted for accordingly based on the relevant accounting standard.

The adoption of the above accounting standard did not have a material impact on the Bank’s assets.

The Bank performed an impact assessment for the implementation of FAS 31 and concluded that:

The agency remuneration, including fixed and variable components thereof, will be recognized on an

accrual basis i.e. when the relevant services are provided. Any expenses, including losses reimbursable will

be recognized when due.

The Bank maintains multi-level investment arrangements to invest funds received under “Wakala “to invest

as “Mudaraba” in its financing and investment assets.

From the principal perspective, the Bank opted to use Wakala venture approach instead of a pass-through

approach given the difficulties for the principal to identify in which assets the funds are invested in, and

hence, the investment is accounted for applying the equity method of accounting.

______________________________________________________________________________________

10

ABC Islamic Bank (E.C.)

30 June 2020 (Reviewed)

NOTES TO THE INTERIM CONDENSED CONSOLIDATED FINANCIAL

STATEMENTS

3 INVESTMENTS (continued)

Stage 1 Stage 2 Stage 3 Total

US$ '000 US$ '000 US$ '000 US$ '000

Sukuk 881,665 - 23,477 905,142

ECL Allowance (1,709) - (14,845) (16,554)

879,956 - 8,632 888,588

Stage 1 Stage 2 Stage 3 Total

US$ '000 US$ '000 US$ '000 US$ '000

Sukuk 829,823 - 8,500 838,323

ECL Allowance (1,137) - (8,500) (9,637)

828,686 - - 828,686

Stage 1 Stage 2 Stage 3 Total

US$ '000 US$ '000 US$ '000 US$ '000

As at 1 January 2020 1,137 - 8,500 9,637

Net transfer between stages (55) - 55 -

Charge for the period - net 627 - 6,290 6,917

As 310 June 2020 1,709 - 14,845 16,554

Stage 1 Stage 2 Stage 3 Total

US$ '000 US$ '000 US$ '000 US$ '000

As at 1 January 2019 1,211 188 8,500 9,899

Net transfer between stages (204) 204 - -

(Write back) / Charge for the period - net (317) 702 - 385

As 30 June 2019 690 1,094 8,500 10,284

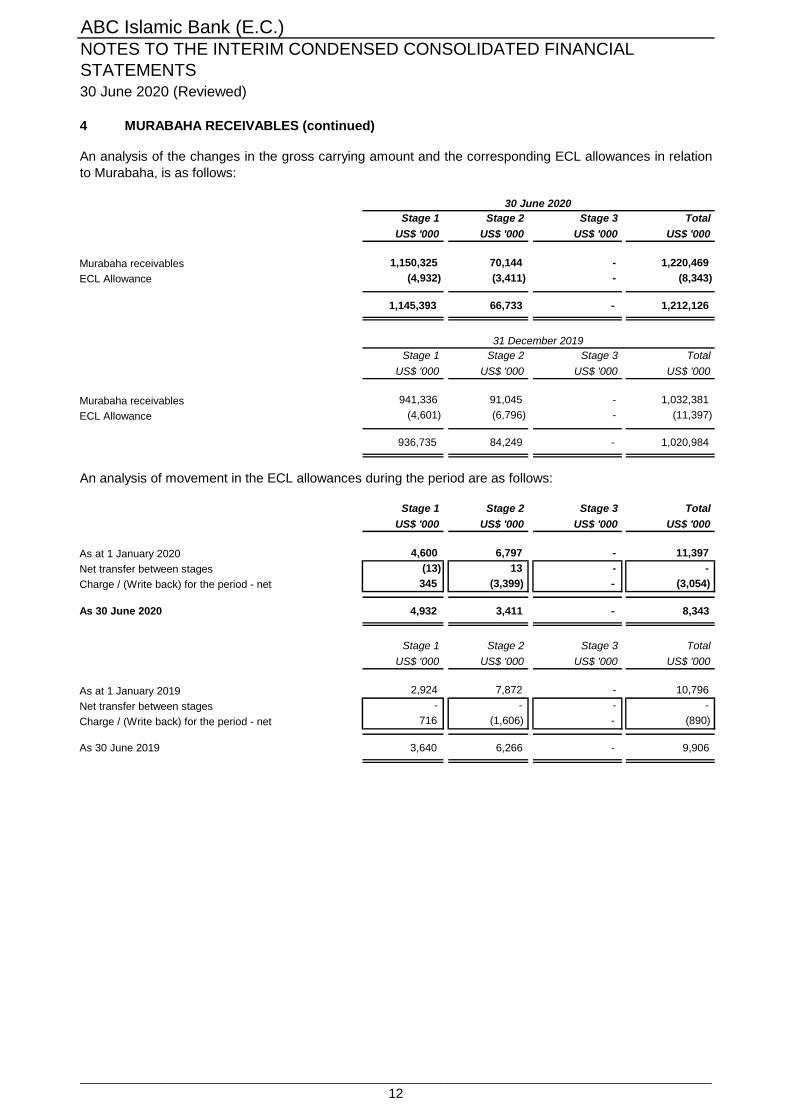

4 MURABAHA RECEIVABLES

Reviewed Audited

30 June 31 December

2020 2019

US$ '000 US$ '000

International Commodity Murabaha 528,800 137,648

Murabaha receivables 697,128 899,985

Deferred profits (5,459) (5,252)

Allowance for credit losses - net (8,343) (11,397)

1,212,126 1,020,984

Sukuk with a carrying value of US$ 230,942 were pledged against Murabaha payables (31 December 2019:

nil).

An analysis of movement in the ECL allowances during the period are as follows:

30 June 2020

31 December 2019

The fair value of the Sukuk carried at amortised cost as at 30 June 2020 is US$ 846,907 thousand (31

December 2019: US$ 837,698 thousand).

The Group considers the promise made by the purchase orderer in the Murabaha contract as obligatory.

______________________________________________________________________________________

11

ABC Islamic Bank (E.C.)

30 June 2020 (Reviewed)

NOTES TO THE INTERIM CONDENSED CONSOLIDATED FINANCIAL

STATEMENTS

4 MURABAHA RECEIVABLES (continued)

Stage 1 Stage 2 Stage 3 Total

US$ '000 US$ '000 US$ '000 US$ '000

Murabaha receivables 1,150,325 70,144 - 1,220,469

ECL Allowance (4,932) (3,411) - (8,343)

1,145,393 66,733 - 1,212,126

Stage 1 Stage 2 Stage 3 Total

US$ '000 US$ '000 US$ '000 US$ '000

Murabaha receivables 941,336 91,045 - 1,032,381

ECL Allowance (4,601) (6,796) - (11,397)

936,735 84,249 - 1,020,984

Stage 1 Stage 2 Stage 3 Total

US$ '000 US$ '000 US$ '000 US$ '000

As at 1 January 2020 4,600 6,797 - 11,397

Net transfer between stages (13) 13 - -

Charge / (Write back) for the period - net 345 (3,399) - (3,054)

As 30 June 2020 4,932 3,411 - 8,343

Stage 1 Stage 2 Stage 3 Total

US$ '000 US$ '000 US$ '000 US$ '000

As at 1 January 2019 2,924 7,872 - 10,796

Net transfer between stages - - - -

Charge / (Write back) for the period - net 716 (1,606) - (890)

As 30 June 2019 3,640 6,266 - 9,906

An analysis of the changes in the gross carrying amount and the corresponding ECL allowances in relation

to Murabaha, is as follows:

An analysis of movement in the ECL allowances during the period are as follows:

30 June 2020

31 December 2019

______________________________________________________________________________________

12

ABC Islamic Bank (E.C.)

30 June 2020 (Reviewed)

NOTES TO THE INTERIM CONDENSED CONSOLIDATED FINANCIAL

STATEMENTS

5 IJARAH

Reviewed Audited

30 June 31 December

2020 2019

US$ '000 US$ '000

Ijarah Muntahia Bittamleek

Cost:

At 1 January 435,682 396,499

Additions - 39,183

Disposals - -

At the end of the period/year 435,682 435,682

Depreciation:

At 1 January 237,548 188,507

Provided for the period/year 6,516 49,041

Relating to disposals for the period/year 13,958 -

At the end of the period/year 258,022 237,548

Net book value:

At the end of the period/year 177,660 198,134

Ijarah receivables 893 1,139

Allowance for credit losses - net (4,342) (2,584)

Total Ijarah 174,211 196,689

Stage 1 Stage 2 Stage 3 Total

US$ '000 US$ '000 US$ '000 US$ '000

Ijarah 161,798 16,755 - 178,553

ECL Allowance (1,864) (2,478) - (4,342)

159,934 14,277 - 174,211

Stage 1 Stage 2 Stage 3 Total

US$ '000 US$ '000 US$ '000 US$ '000

Ijarah 182,517 16,756 - 199,273

ECL Allowance (1,345) (1,239) - (2,584)

181,172 15,517 - 196,689

In Ijarah Muntahia Bittamleek, the legal title of the leased asset passes to the lessee at the end of the Ijarah

term provided that all Ijarah instalments are settled and the lessee purchases the asset.

30 June 2020

An analysis of the changes in the gross carrying amount and the corresponding ECL allowances in relation

to Ijarah, is as follows:

31 December 2019

______________________________________________________________________________________

13

ABC Islamic Bank (E.C.)

30 June 2020 (Reviewed)

NOTES TO THE INTERIM CONDENSED CONSOLIDATED FINANCIAL

STATEMENTS

5 IJARAH (continued)

Stage 1 Stage 2 Stage 3 Total

US$ '000 US$ '000 US$ '000 US$ '000

As at 1 January 2020 1,345 1,239 - 2,584

Net transfer between stages - - - -

Charge for the period - net 519 1,239 - 1,758

As 30 June 2020 1,864 2,478 - 4,342

Stage 1 Stage 2 Stage 3 Total

US$ '000 US$ '000 US$ '000 US$ '000

As at 1 January 2019 408 - - 408

Net transfer between stages (41) 41 - -

(Write back) / Charge for the period - net (9) 162 - 153

As 30 June 2019 358 203 - 561

30 June 30 June

2020 2019

US$ '000 US$ '000

Ijarah income – gross 10,909 30,403

Depreciation provided during the period (6,516) (24,934)

Ijarah income – net 4,393 5,469

6 ALLOWANCE FOR / (REVERSAL OF) CREDIT LOSSES - NET

30 June 30 June

2020 2019

US$ '000 US$ '000

Due from financial institutions 48 -

Investments 6,917 385

Murabaha receivables (3,054) (890)

Ijarah 1,758 153

Other assets 1 8

Other liabilities (600) (338)

5,070 (682)

7 SEGMENTAL INFORMATION

Reviewed six months ended

Reviewed six months ended

There are no impaired Ijarahs as at 30 June 2020 (31 December 2019: nil).

An analysis of movement in the ECL allowances during the period is as follows:

The activities of the Group are performed on an integrated basis. Therefore, any segmentation of operating

income, expenses, assets and liabilities is not relevant. As such, operating income, expenses, assets and

liabilities are not segmented.

The Group has physical operations and offices solely in the Kingdom of Bahrain and, as such, no

geographical segment information is presented.

Details of Ijarah income are as follows:

______________________________________________________________________________________

14

ABC Islamic Bank (E.C.)

30 June 2020 (Reviewed)

NOTES TO THE INTERIM CONDENSED CONSOLIDATED FINANCIAL

STATEMENTS

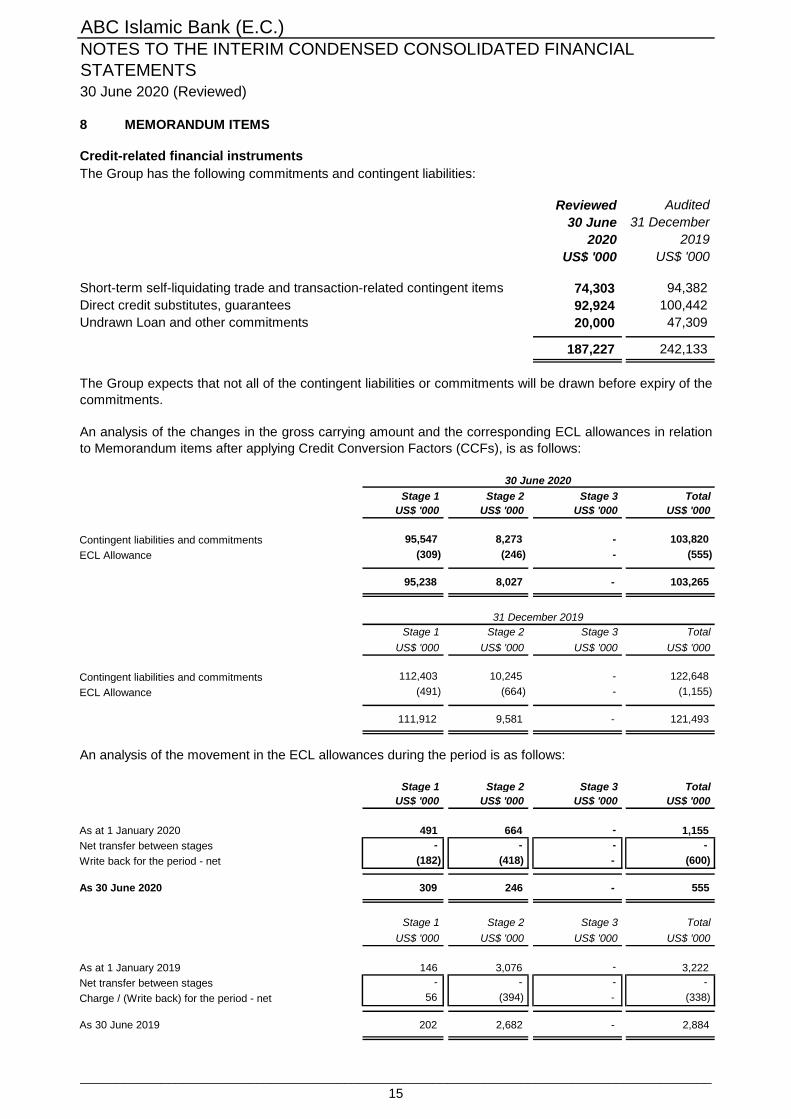

8 MEMORANDUM ITEMS

Credit-related financial instruments

Reviewed Audited

30 June 31 December

2020 2019

US$ '000 US$ '000

Short-term self-liquidating trade and transaction-related contingent items 74,303 94,382

Direct credit substitutes, guarantees 92,924 100,442

Undrawn Loan and other commitments 20,000 47,309

187,227 242,133

Stage 1 Stage 2 Stage 3 Total

US$ '000 US$ '000 US$ '000 US$ '000

Contingent liabilities and commitments 95,547 8,273 - 103,820

ECL Allowance (309) (246) - (555)

95,238 8,027 - 103,265

Stage 1 Stage 2 Stage 3 Total

US$ '000 US$ '000 US$ '000 US$ '000

Contingent liabilities and commitments 112,403 10,245 - 122,648

ECL Allowance (491) (664) - (1,155)

111,912 9,581 - 121,493

Stage 1 Stage 2 Stage 3 Total

US$ '000 US$ '000 US$ '000 US$ '000

As at 1 January 2020 491 664 - 1,155

Net transfer between stages - - - -

Write back for the period - net (182) (418) - (600)

As 30 June 2020 309 246 - 555

Stage 1 Stage 2 Stage 3 Total

US$ '000 US$ '000 US$ '000 US$ '000

As at 1 January 2019 146 3,076 - 3,222

Net transfer between stages - - - -

Charge / (Write back) for the period - net 56 (394) - (338)

As 30 June 2019 202 2,682 - 2,884

The Group has the following commitments and contingent liabilities:

30 June 2020

31 December 2019

An analysis of the movement in the ECL allowances during the period is as follows:

The Group expects that not all of the contingent liabilities or commitments will be drawn before expiry of the

commitments.

An analysis of the changes in the gross carrying amount and the corresponding ECL allowances in relation

to Memorandum items after applying Credit Conversion Factors (CCFs), is as follows:

______________________________________________________________________________________

15

ABC Islamic Bank (E.C.)

30 June 2020 (Reviewed)

NOTES TO THE INTERIM CONDENSED CONSOLIDATED FINANCIAL

STATEMENTS

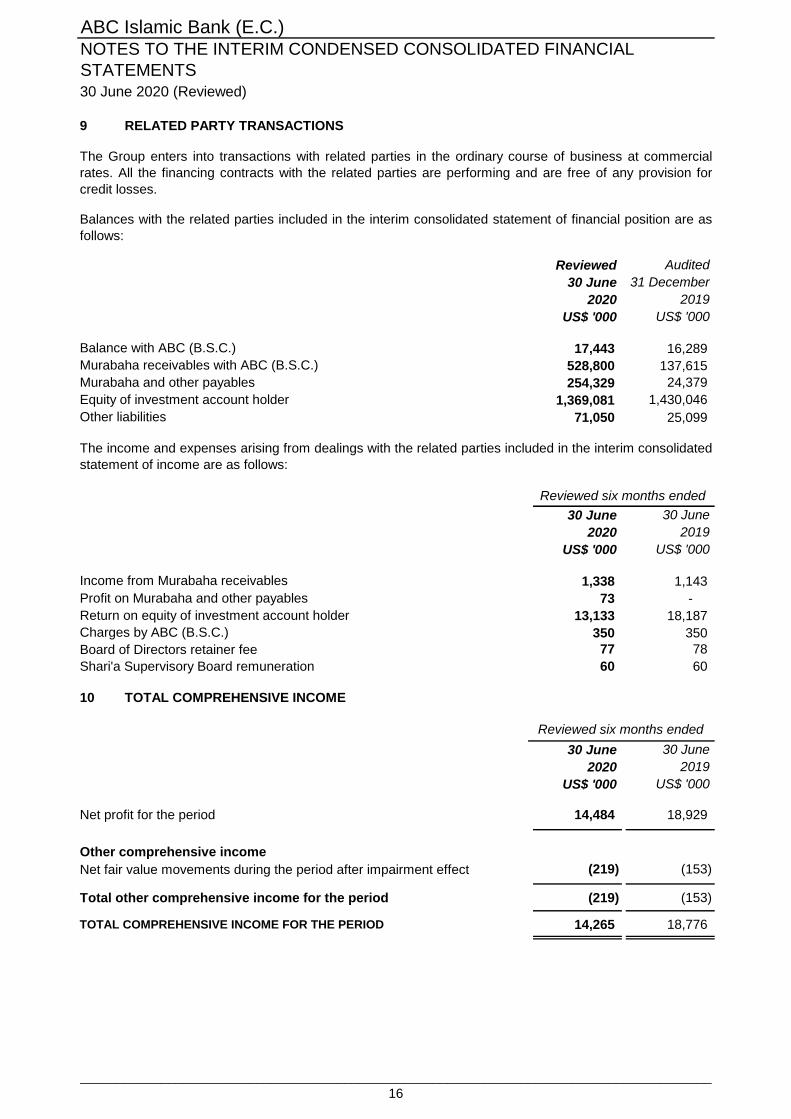

9 RELATED PARTY TRANSACTIONS

Reviewed Audited

30 June 31 December

2020 2019

US$ '000 US$ '000

Balance with ABC (B.S.C.) 17,443 16,289

Murabaha receivables with ABC (B.S.C.) 528,800 137,615

Murabaha and other payables 254,329 24,379

Equity of investment account holder 1,369,081 1,430,046

Other liabilities 71,050 25,099

30 June 30 June

2020 2019

US$ '000 US$ '000

Income from Murabaha receivables 1,338 1,143

Profit on Murabaha and other payables 73 -

Return on equity of investment account holder 13,133 18,187

Charges by ABC (B.S.C.) 350 350

Board of Directors retainer fee 77 78

Shari'a Supervisory Board remuneration 60 60

10 TOTAL COMPREHENSIVE INCOME

30 June 30 June

2020 2019

US$ '000 US$ '000

Net profit for the period 14,484 18,929

Other comprehensive income

Net fair value movements during the period after impairment effect (219) (153)

Total other comprehensive income for the period (219) (153)

TOTAL COMPREHENSIVE INCOME FOR THE PERIOD 14,265 18,776

Balances with the related parties included in the interim consolidated statement of financial position are as

follows:

The income and expenses arising from dealings with the related parties included in the interim consolidated

statement of income are as follows:

Reviewed six months ended

Reviewed six months ended

The Group enters into transactions with related parties in the ordinary course of business at commercial

rates. All the financing contracts with the related parties are performing and are free of any provision for

credit losses.

______________________________________________________________________________________

16

ABC Islamic Bank (E.C.)

30 June 2020 (Reviewed)

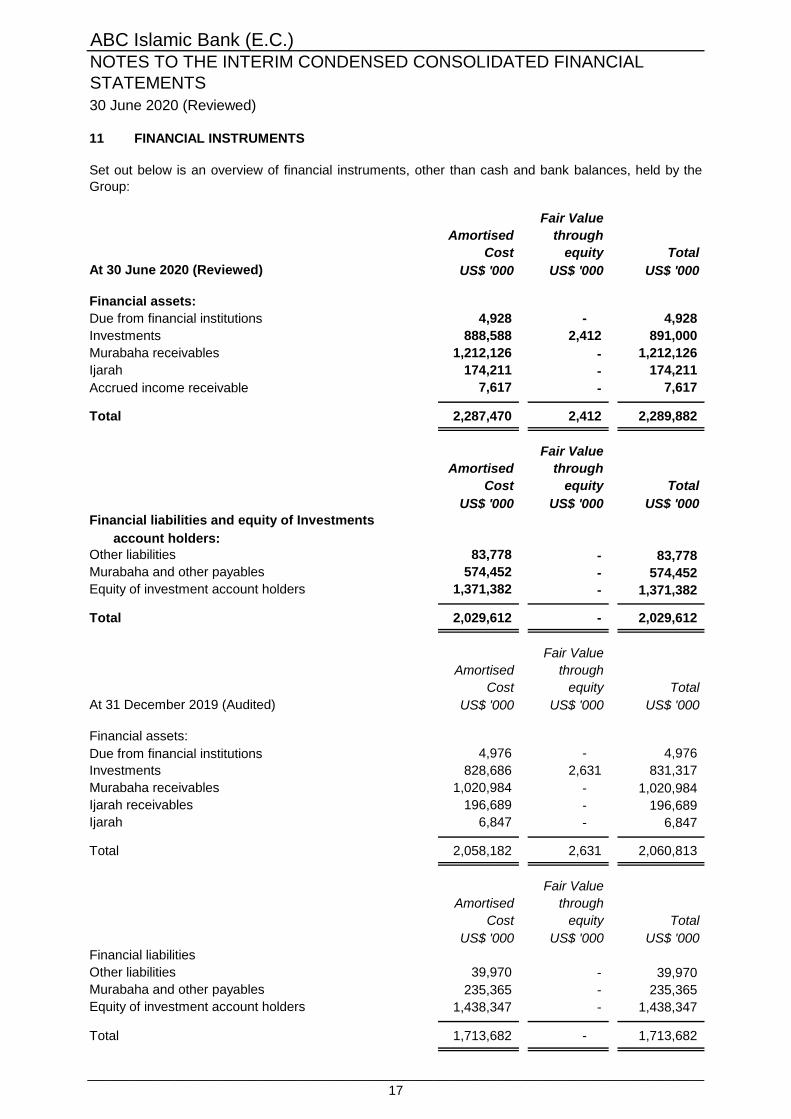

11 FINANCIAL INSTRUMENTS

Fair Value

Amortised through

Cost equity Total

At 30 June 2020 (Reviewed) US$ '000 US$ '000 US$ '000

Financial assets:

Due from financial institutions 4,928 - 4,928

Investments 888,588 2,412 891,000

Murabaha receivables 1,212,126 - 1,212,126

Ijarah 174,211 - 174,211

Accrued income receivable 7,617 - 7,617

Total 2,287,470 2,412 2,289,882

Fair Value

Amortised through

Cost equity Total

US$ '000 US$ '000 US$ '000

Financial liabilities and equity of Investments

account holders:

Other liabilities 83,778 - 83,778

Murabaha and other payables 574,452 - 574,452

Equity of investment account holders 1,371,382 - 1,371,382

Total 2,029,612 - 2,029,612

Fair Value

Amortised through

Cost equity Total

At 31 December 2019 (Audited) US$ '000 US$ '000 US$ '000

Financial assets:

Due from financial institutions 4,976 - 4,976

Investments 828,686 2,631 831,317

Murabaha receivables 1,020,984 - 1,020,984

Ijarah receivables 196,689 - 196,689

Ijarah 6,847 - 6,847

Total 2,058,182 2,631 2,060,813

Fair Value

Amortised through

Cost equity Total

US$ '000 US$ '000 US$ '000

Financial liabilities

Other liabilities 39,970 - 39,970

Murabaha and other payables 235,365 - 235,365

Equity of investment account holders 1,438,347 - 1,438,347

Total 1,713,682 - 1,713,682

NOTES TO THE INTERIM CONDENSED CONSOLIDATED FINANCIAL

STATEMENTS

Set out below is an overview of financial instruments, other than cash and bank balances, held by the

Group:

____________________________________________________________________________________

17

ABC Islamic Bank (E.C.)

30 June 2020 (Reviewed)

NOTES TO THE INTERIM CONDENSED CONSOLIDATED FINANCIAL

STATEMENTS

11 FINANCIAL INSTRUMENTS (continued)

Carrying Fair Carrying Fair

amount value amount value

US$ '000 US$ '000 US$ '000 US$ '000

Financial assets:

Investments 888,588 846,907 826,686 837,698

Fair value hierarchy

Except for the following, the fair value of financial instruments which are carried at amortised cost are

not materially different from their carrying value:

Fair value is the amount for which an asset could be exchanged or a liability settled between

knowledgeable and willing parties in an arm’s length transaction.

Fair values of quoted securities are derived from quoted market prices in active markets, if available. For

unquoted securities, fair value is estimated using appropriate valuation techniques. Such techniques

may include using recent arm’s length market transactions; reference to the current fair value of another

instrument that is substantially the same; discounted cash flow analysis or other valuation models.

Fair values of financial instruments not carried at fair value

30 June 2020 31 December 2019

The Group uses the following hierarchy for determining and disclosing the fair value of financial

instruments by valuation technique:

Level 1: quoted (unadjusted) prices in active markets for identical assets or liabilities;

Level 2: other techniques for which all inputs which have a significant effect on the recorded fair value

are observable, either directly or indirectly; and

Level 3: techniques which use inputs which have a significant effect on the recorded fair value that are

not based on observable market data.

All investments of the Group are classified under level 1 of the fair value hierarchy.

____________________________________________________________________________________

18

ABC Islamic Bank (E.C.)

30 June 2020 (Reviewed)

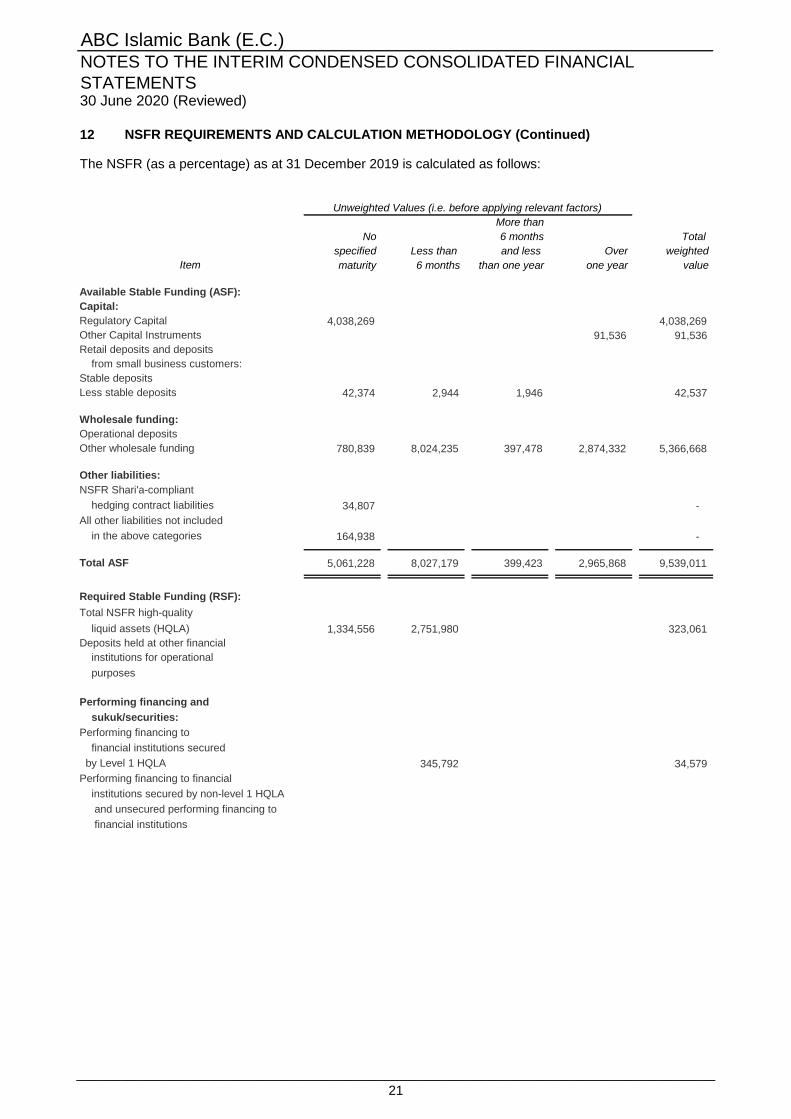

12 NSFR REQUIREMENTS AND CALCULATION METHODOLOGY

More than

No 6 months Total

specified Less than and less Over weighted

maturity 6 months than one year one year value

3,876,364 - - - 3,876,364

- - - 40,712 40,712

- - - - -

- - - - -

- - - - -

57,677 2,524 2,298 - 56,248

- - - - -

- - - - -

- - - - -

1,114,127 7,584,907 947,369 2,744,455 5,515,427

- - - - -

- - - - -

- - - - -

245,694 - - - -

- - - - -

299,640 - - - -

5,593,502 7,587,431 949,667 2,785,167 9,488,751

3,902,599 1,498,531 - - 304,657

- - - - -

- - - - -

- - - - -

- - - - -

- - - - -

- - - - -

- - - - -

- - - - -

- 21,260 - - 2,126

- - - - -

- - - - -

- - - - -

- - - - -

- - - - -

Performing financing to financial

institutions secured by non-level 1 HQLA

and unsecured performing financing to

financial institutions

purposes

Performing financing and

sukuk/securities:

Performing financing to

financial institutions secured

by Level 1 HQLA

Total NSFR high-quality

liquid assets (HQLA)

Deposits held at other financial

institutions for operational

NSFR Shari'a-compliant

hedging contract liabilities

All other liabilities not included

in the above categories

Total ASF

Required Stable Funding (RSF):

Other liabilities:

Available Stable Funding (ASF):

Capital:

Regulatory Capital

Other Capital Instruments

Retail deposits and deposits

from small business customers:

Stable deposits

Less stable deposits

Wholesale funding:

Operational deposits

Other wholesale funding

Item

NOTES TO THE INTERIM CONDENSED CONSOLIDATED FINANCIAL

STATEMENTS

The Net Stable Funding Ratio ('NSFR') is calculated in accordance with the Liquidity Risk Management

Module guidelines, issued by the CBB and is effective from 2019. The minimum NSFR ratio as per CBB is

100%. The Group's consolidated NSFR ratio as of 30 June 2020 is 111.9%.

The NSFR (as a percentage) must be calculated as follows:

Unweighted Values (i.e. before applying relevant factors)

_______________________________________________________________________________________

19

ABC Islamic Bank (E.C.)

30 June 2020 (Reviewed)

NOTES TO THE INTERIM CONDENSED CONSOLIDATED FINANCIAL

STATEMENTS

12 NSFR REQUIREMENTS AND CALCULATION METHODOLOGY (continued)

More than

No 6 months Total

specified Less than and less Over weighted

maturity 6 months than one year one year value

- - - - -

- - - - -

- - - - -

- - - - -

- - - - -

- - - - -

- - - - -

- - - - -

- - - - -

- 1,899,846 547,644 2,711,078 3,489,579

- - - - -

- - - - -

- - - - -

- - - - -

- - - - -

- - - - -

- - - - -

- - - - -

- - - - -

- 151,463 135,042 1,620,301 1,520,508

- - - - -

- - - - -

- - - - -

- - - - -

- - - - -

- - - - -

- - - - -

- - - - -

- - - - -

49,139 - - - -

- - - - -

- - - - -

49,139 - - - 49,138

- - - - -

- 1,307,721 713,461 2,426,390 2,993,893

- 962,517 614,353 890,216 123,354

4,000,877 5,841,338 2,010,500 7,647,985 8,483,255

- - - - 111.9%

Total RSF

NSFR (%)

The above ratio is reported at Domestic Liquidity Group (DLG). ie, at aggregate level for Bank ABC Parent

and ABC Islamic Bank.

NSFR Shari'a-compliant hedging

contract liabilities before

deduction of variation margin posted

All other assets not included in

the above categories

OBS items

hedging assets

HQLA, including exchange-

traded equities

Other assets:

Physical traded commodities,

including gold

Assets posted as initial margin for

Shari'a-compliant hedging

contracts contracts and

contributions to default funds of CCPs

NSFR Shari'a-compliant

default and do not qualify as

central banks and PSEs,

of which:

With a risk weight of less than or

equal to 35% as per the CBB

Capital Adequacy Ratio guidelines

Performing residential

mortgages, of which:

With a risk weight of less than or

equal to 35% under the CBB

Capital Adequacy Ratio Guidelines

Securities/sukuk that are not in

financing to sovereigns,

Item

Performing financing to non-

financial corporate clients,

financing to retail and small

business customers, and

Unweighted Values (i.e. before applying relevant factors)

_______________________________________________________________________________________

20

ABC Islamic Bank (E.C.)

30 June 2020 (Reviewed)

12 NSFR REQUIREMENTS AND CALCULATION METHODOLOGY (Continued)

More than

No 6 months Total

specified Less than and less Over weighted

maturity 6 months than one year one year value

4,038,269 4,038,269

91,536 91,536

42,374 2,944 1,946 42,537

780,839 8,024,235 397,478 2,874,332 5,366,668

34,807 -

164,938 -

5,061,228 8,027,179 399,423 2,965,868 9,539,011

1,334,556 2,751,980 323,061

345,792 34,579

Available Stable Funding (ASF):

NOTES TO THE INTERIM CONDENSED CONSOLIDATED FINANCIAL

STATEMENTS

The NSFR (as a percentage) as at 31 December 2019 is calculated as follows:

Unweighted Values (i.e. before applying relevant factors)

Item

NSFR Shari'a-compliant

Capital:

Regulatory Capital

Other Capital Instruments

Retail deposits and deposits

from small business customers:

Stable deposits

Less stable deposits

Wholesale funding:

Operational deposits

Other wholesale funding

Other liabilities:

purposes

hedging contract liabilities

All other liabilities not included

in the above categories

Total ASF

Required Stable Funding (RSF):

Total NSFR high-quality

liquid assets (HQLA)

Deposits held at other financial

institutions for operational

Performing financing and

sukuk/securities:

Performing financing to

financial institutions secured

by Level 1 HQLA

Performing financing to financial

institutions secured by non-level 1 HQLA

and unsecured performing financing to

financial institutions

_______________________________________________________________________________________

21

ABC Islamic Bank (E.C.)

30 June 2020 (Reviewed)

NOTES TO THE INTERIM CONDENSED CONSOLIDATED FINANCIAL

STATEMENTS

12 NSFR REQUIREMENTS AND CALCULATION METHODOLOGY (continued)

More than

No 6 months Total

specified Less than and less Over weighted

maturity 6 months than one year one year value

215,717 4,116,142 965,131 3,360,714 5,465,261

246,520 75,838 1,151,131 1,139,640

6,961 6,961

21,040 1,862,176 1,872,697

1,273,447 320,760 1,268,849 143,153

1,557,235 8,754,922 1,361,728 7,642,871 8,985,353

106.2%

Unweighted Values (i.e. before applying relevant factors)

Item

central banks and PSEs,

Performing financing to non-

financial corporate clients,

financing to retail and small

business customers, and

financing to sovereigns,

HQLA, including exchange-

of which:

With a risk weight of less than or

equal to 35% as per the CBB

Capital Adequacy Ratio guidelines

Performing residential

mortgages, of which:

With a risk weight of less than or

equal to 35% under the CBB

Capital Adequacy Ratio Guidelines

Securities/sukuk that are not in

default and do not qualify as

NSFR Shari'a-compliant hedging

traded equities

Other assets:

Physical traded commodities,

including gold

Assets posted as initial margin for

Shari'a-compliant hedging

contracts and

contributions to default funds of CCPs

NSFR Shari'a-compliant

hedging assets

NSFR (%)

The above ratio is reported at Domestic Liquidity Group (DLG). ie, at aggregate level for Bank ABC Parent

and ABC Islamic Bank.

contract liabilities before

deduction of variation margin posted

All other assets not included in

the above categories

OBS items

Total RSF

_______________________________________________________________________________________

22

ABC Islamic Bank (E.C.)SUPPLEMENTARY FINANCIAL INFORMATION At 30 June 2020 (Unreviewed)

(The attached financial information do not form part of the

interim condensed consolidated financial statements)

ABC Islamic Bank (E.C.)INTERIM SUPPLEMENTARY FINANCIAL INFORMATION30 June 2020 (Unreviewed)

"IMPACT OF NOVEL CORONAVIRUS ("Covid-19")

•

•

•

•

•

The above interim supplementary information has been provided in accordance with the CBB letter

OG/259/2020 dated 14 July 2020.

Since the Covid-19 situation is uncertain and evolving, the above information is based on the best

judgement of the management of condition that existed as at 30 June 2020 and may change due to

events happening afterwards. Further, this information does not represent full comprehensive

assessment of Covid-19 impact on the Group. This should not be considered as an indication of the

results for the entire year.

US$ millions

On 11 March 2020, the spread of the Covid-19 around the world was declared a pandemic by the World

Health Organisation. Many countries, including the Kingdom of Bahrain and other countries, have

implemented restrictions aimed at limiting the rate of its spread which have had immediate impact on

people, businesses and economies. To the extent the Covid-19 pandemic continues to adversely affect

the global economy and adversely affects the business, results of operations or financial condition, it

may also have the effect of increasing the likelihood and/or magnitude of other risks.

In response to the economic and market conditions resulting from the Covid-19 pandemic,

governments, and regulatory authorities, including central banks, have acted to provide fiscal and

monetary stimuli to support the global economy. The Central Bank of Bahrain ("CBB") and other

government entities have supported among other things the following:

The Bank activated its business continuity plan and other risk management practices to manage the

potential impact of the business disruption due to Covid-19 outbreak, on its operations and financial

performance.

The financial impact for the period ended 30 June 2020 mainly arose from spike in the ECL.

The Bank recorded an ECL charge of US$ 5.1 million, out of which US$ 1 million, relating to Stage 1

and Stage 2, was predominantly due to factors impacted by Covid19.

implemented programs to promote liquidity including profit free repurchase agreements;

required banks to provide 6-month payment holidays to eligible customers without charging

additional profit;

announced programs for supporting businesses by providing direct government assistance;

clarified supervisory expectations regarding loan modifications due to Covid-19 related non-

payment; and

clarified expectations for certain bank regulations related to counterparty credit risk, the

current expected credit loss accounting standard and capital adequacy regulatory treatment.

The Bank has also provided payment holidays to certain customers with outstanding exposure

amounting to US$ 154 million as of 30 June 2020. These payment holidays have been provided as part

of its support to impacted customers, however, this did not result in any modification loss.

Item

ECL: Stage1/Stage2

Government Grant

Consolidated Statement of Profit

or Loss

-1

0.25

Further, government assistance amounting to US$ 248 thousand has been recorded in the interim

consolidated statement of profit or loss for the period ended 30 June 2020.

In summary the financial impact of the financial statements is given below:

____________________________________________________________________________________

24

![ABC BANK GROUP - PwC€¦ · ABC BANK GROUP International ... 1 Consolidated ... [Adjusted] At 1 January 2016 Profit / (loss) for the year Other comprehensive income 31](https://img.dokumen.tips/doc/110x75/5ac1e2db7f8b9a4e7c8d9a46/abc-bank-group-pwc-abc-bank-group-international-1-consolidated-adjusted.jpg)