Embed Size (px)

Citation preview

Islamic bonds and real-estate securitization.

The Italian perspective for

issuing a sukuk

Turin 19 october 2015

Enrico Giustiniani

Supervisor of Islamic Finance Working Group

AIAF - Italian Association of Financial Analysts Societies

2nd TURIN ISLAMIC ECONOMIC FORUM (TIEF 2015)

1

2

AIAF - Associazione Italiana degli Analisti Finanziari (Italian Association of Financial Analysts Societies) was founded in 1971 as a non-profit association and in 1972 joined EFFAS (The European Federation of Financial Analysts Societies). The total AIAF members are now about 1.000. Objectives To support and develop the financial analysts' profession in Italy, to take care of its professional qualification and to promote the acknowledgment of its function. To promote the study and the analysis of the financial market in order to contribute to its development and efficiency, acting as a spokesman of the members' demands and opinions. Activities Training Course for the Financial Analysts' Education, certified by EFFAS. About 250 meetings, each year, with the Italian listed Companies for presentation and discussions on annual and mid-year reports, new quotations and special operations. a quarterly magazine was produced, called "Rivista AIAF". To all issues are enclosed technical supplements called "Quaderni AIAF", produced by the study's Commissions.

3

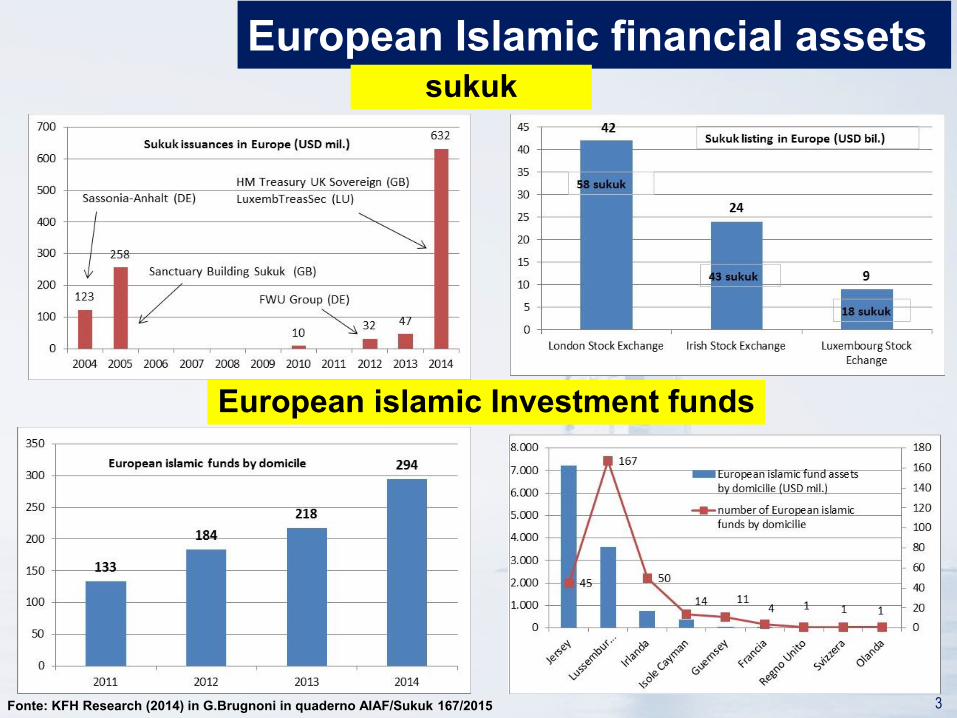

European Islamic financial assets

Fonte: KFH Research (2014) in G.Brugnoni in quaderno AIAF/Sukuk 167/2015

sukuk

European islamic Investment funds

4

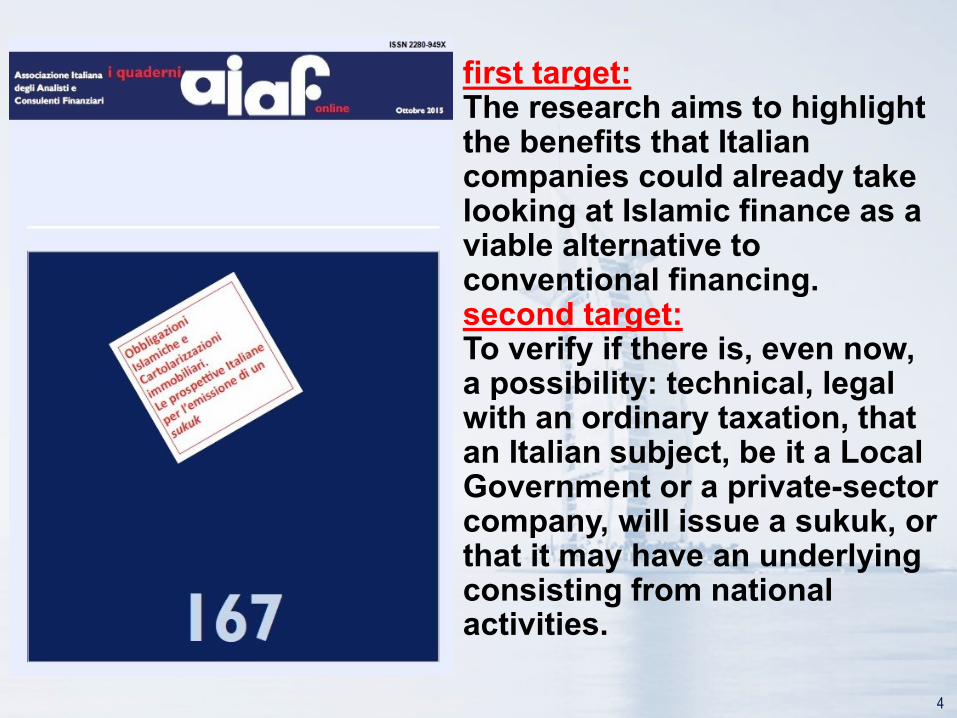

first target: The research aims to highlight the benefits that Italian companies could already take looking at Islamic finance as a viable alternative to conventional financing. second target: To verify if there is, even now, a possibility: technical, legal with an ordinary taxation, that an Italian subject, be it a Local Government or a private-sector company, will issue a sukuk, or that it may have an underlying consisting from national activities.

Ijara (lease) is a contract according to which a party purchases and leases out equipment

required by the client for a rental fee. The duration of the rental and the fee are agreed in

advance and ownership of the asset remains with the lessor.

•The assets purchased by the SPV is funded by the issuance of sukuk (trust certificates)

which represents beneficial ownership in the assets and the lease

•Originator received cash proceeds

•SPV rents property to the Originator for specified period

•SPV collects rentals

•SPV passed the rentals to investors – periodic distribution/coupon

At maturity: SPV sells the property to the Originator at an agreed price, and Originator

pays cash to SPV

•SPV simultaneously pay investors cash for sukuk redemption much usufruct from it as

possible.

Sukuk al-Ijara

5

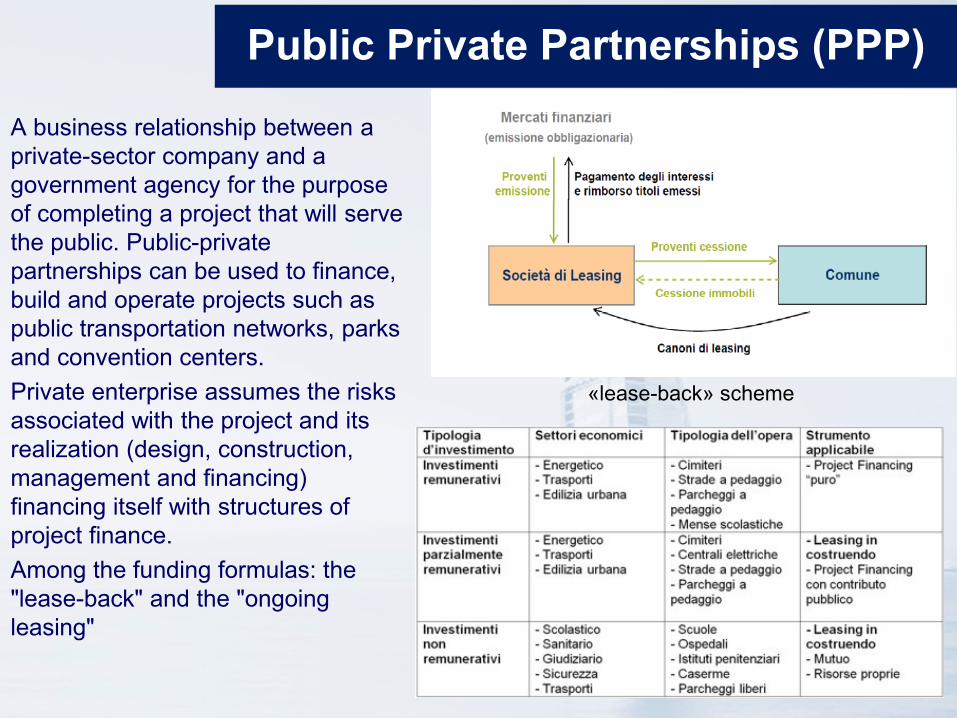

A business relationship between a

private-sector company and a

government agency for the purpose

of completing a project that will serve

the public. Public-private

partnerships can be used to finance,

build and operate projects such as

public transportation networks, parks

and convention centers.

Private enterprise assumes the risks

associated with the project and its

realization (design, construction,

management and financing)

financing itself with structures of

project finance.

Among the funding formulas: the

"lease-back" and the "ongoing

leasing"

Public Private Partnerships (PPP)

6

«lease-back» scheme

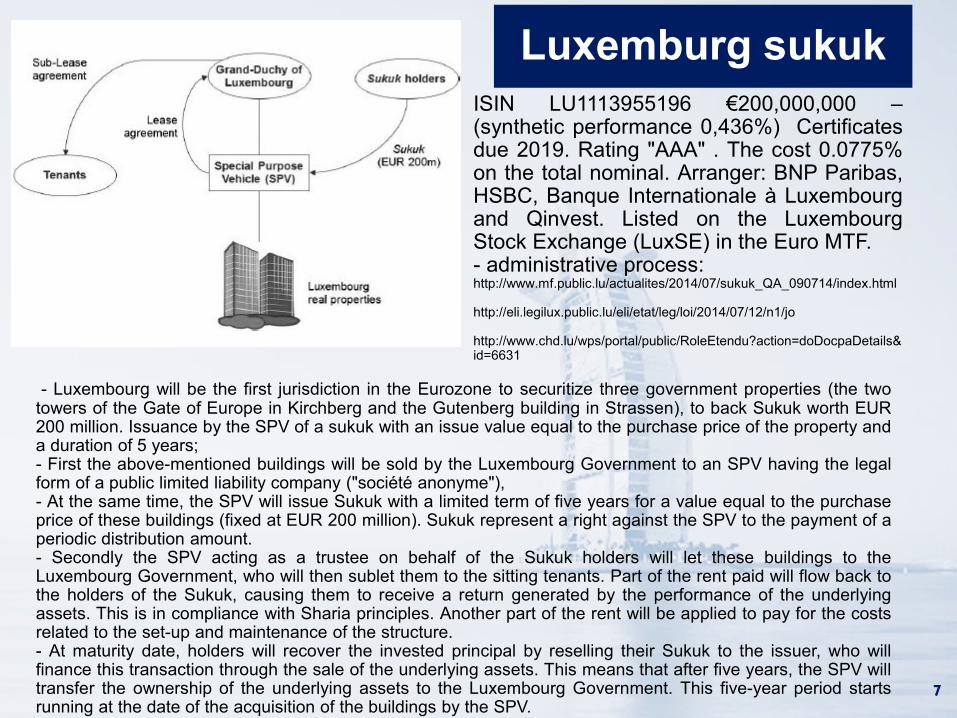

Luxemburg sukuk

7

ISIN LU1113955196 €200,000,000 – (synthetic performance 0,436%) Certificates due 2019. Rating "AAA" . The cost 0.0775% on the total nominal. Arranger: BNP Paribas, HSBC, Banque Internationale à Luxembourg and Qinvest. Listed on the Luxembourg Stock Exchange (LuxSE) in the Euro MTF. - administrative process: http://www.mf.public.lu/actualites/2014/07/sukuk_QA_090714/index.html http://eli.legilux.public.lu/eli/etat/leg/loi/2014/07/12/n1/jo http://www.chd.lu/wps/portal/public/RoleEtendu?action=doDocpaDetails&id=6631

- Luxembourg will be the first jurisdiction in the Eurozone to securitize three government properties (the two towers of the Gate of Europe in Kirchberg and the Gutenberg building in Strassen), to back Sukuk worth EUR 200 million. Issuance by the SPV of a sukuk with an issue value equal to the purchase price of the property and a duration of 5 years; - First the above-mentioned buildings will be sold by the Luxembourg Government to an SPV having the legal form of a public limited liability company ("société anonyme"), - At the same time, the SPV will issue Sukuk with a limited term of five years for a value equal to the purchase price of these buildings (fixed at EUR 200 million). Sukuk represent a right against the SPV to the payment of a periodic distribution amount. - Secondly the SPV acting as a trustee on behalf of the Sukuk holders will let these buildings to the Luxembourg Government, who will then sublet them to the sitting tenants. Part of the rent paid will flow back to the holders of the Sukuk, causing them to receive a return generated by the performance of the underlying assets. This is in compliance with Sharia principles. Another part of the rent will be applied to pay for the costs related to the set-up and maintenance of the structure. - At maturity date, holders will recover the invested principal by reselling their Sukuk to the issuer, who will finance this transaction through the sale of the underlying assets. This means that after five years, the SPV will transfer the ownership of the underlying assets to the Luxembourg Government. This five-year period starts running at the date of the acquisition of the buildings by the SPV.

Fonte: A.Salvi, F. Petrucci, P.G. Conforti di Lorenzo in quaderno AIAF/Sukuk 167/2015

Investitore/Sottoscrittore

Pagamento

dei Sukuk

Pagamenti

periodici

dell’interes

se a tasso

fisso

(Proventi

dei canoni)

SPV

Property

management

Emissione Sukuk

Costruttore Contratto

PPP

Lo

cazio

ne

(lease-b

ack

)

Can

on

i Ente pubblico

Vendita beni

Opera

pubblica

Diagram of a potential Public sukuk

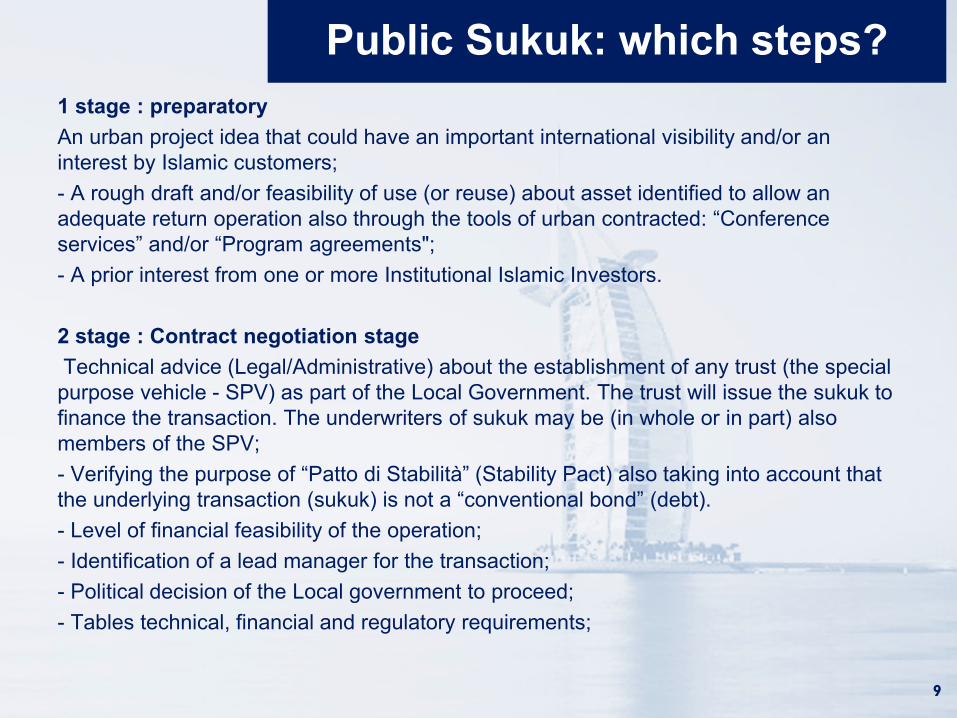

Public Sukuk: which steps?

9

1 stage : preparatory

An urban project idea that could have an important international visibility and/or an

interest by Islamic customers;

- A rough draft and/or feasibility of use (or reuse) about asset identified to allow an

adequate return operation also through the tools of urban contracted: “Conference

services” and/or “Program agreements";

- A prior interest from one or more Institutional Islamic Investors.

2 stage : Contract negotiation stage

Technical advice (Legal/Administrative) about the establishment of any trust (the special

purpose vehicle - SPV) as part of the Local Government. The trust will issue the sukuk to

finance the transaction. The underwriters of sukuk may be (in whole or in part) also

members of the SPV;

- Verifying the purpose of “Patto di Stabilità” (Stability Pact) also taking into account that

the underlying transaction (sukuk) is not a “conventional bond” (debt).

- Level of financial feasibility of the operation;

- Identification of a lead manager for the transaction;

- Political decision of the Local government to proceed;

- Tables technical, financial and regulatory requirements;

Public Sukuk: which steps?

10

3 stage: first Istitutional stage

- Approval by the executive local Government the preliminary project and its financing;

- Inclusion into the “Programma triennale delle opere pubbliche” («Three-year program of public

works) to be carried out during the following three years, attached to the budget;

- Approval the Program schedule by local Government;

- Administrative process for the realization of Public work.

4 stage: Contractual framework

- The SPV established, build (or by others) the Public work following the urban project or it rents

the property, in any case by getting the necessary funds to repay and reward (by the rents) the

capital obtained through sukuk.

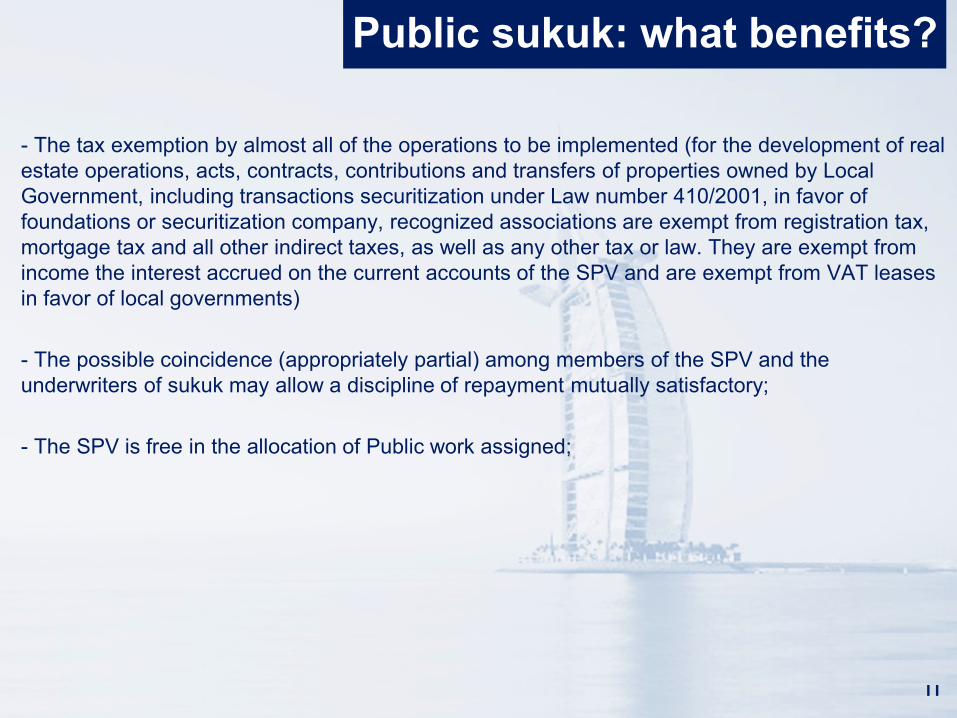

Public sukuk: what benefits?

11

- The tax exemption by almost all of the operations to be implemented (for the development of real

estate operations, acts, contracts, contributions and transfers of properties owned by Local

Government, including transactions securitization under Law number 410/2001, in favor of

foundations or securitization company, recognized associations are exempt from registration tax,

mortgage tax and all other indirect taxes, as well as any other tax or law. They are exempt from

income the interest accrued on the current accounts of the SPV and are exempt from VAT leases

in favor of local governments)

- The possible coincidence (appropriately partial) among members of the SPV and the

underwriters of sukuk may allow a discipline of repayment mutually satisfactory;

- The SPV is free in the allocation of Public work assigned;

Piemonte Region Palace

12

An international project that could have been funded through a sukuk: the new building of the “Piemonte Region” in the district of “Nizza Millefonti” in Turin. Approved approximately 240 million euro to “ATI Coopsette” (spread Euribor + 1.485%) with the formula: "ongoing leasing." The works will be financed with the recovery of rent payable, the sale of urban rights and some buildings. The resources will help to pay the leasing (Art. 160bis Law 163/06) in twenty-year (determinazione 1355 Reg. Piemonte del 30.12.2010)

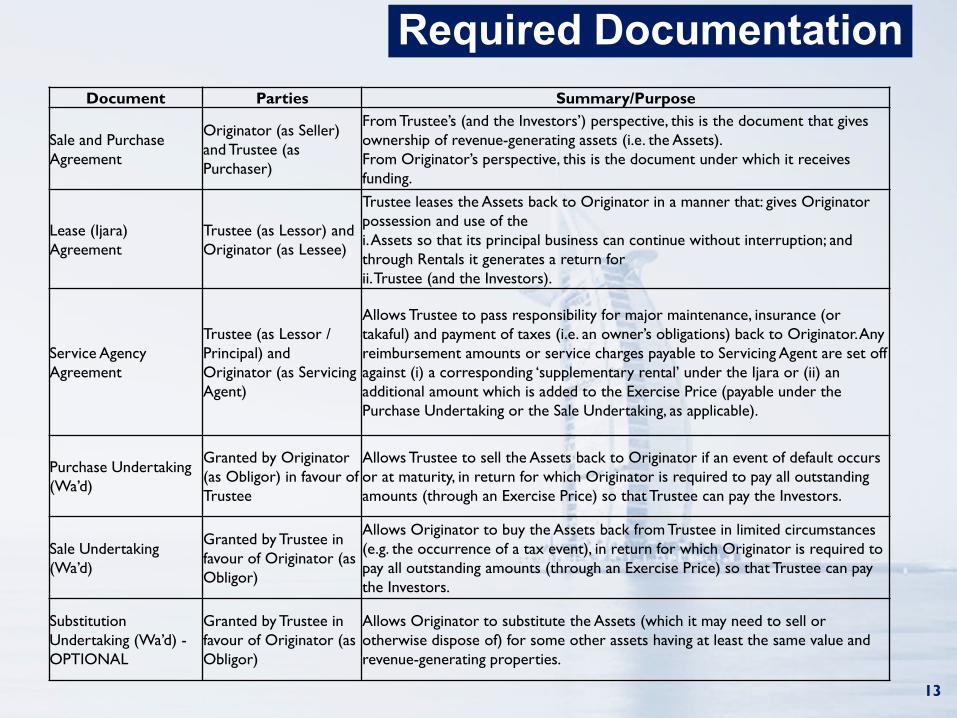

Required Documentation

13

Document Parties Summary/Purpose

Sale and Purchase

Agreement

Originator (as Seller)

and Trustee (as

Purchaser)

From Trustee’s (and the Investors’) perspective, this is the document that gives

ownership of revenue-generating assets (i.e. the Assets).

From Originator’s perspective, this is the document under which it receives

funding.

Lease (Ijara)

Agreement

Trustee (as Lessor) and

Originator (as Lessee)

Trustee leases the Assets back to Originator in a manner that: gives Originator

possession and use of the

i. Assets so that its principal business can continue without interruption; and

through Rentals it generates a return for

ii. Trustee (and the Investors).

Service Agency

Agreement

Trustee (as Lessor /

Principal) and

Originator (as Servicing

Agent)

Allows Trustee to pass responsibility for major maintenance, insurance (or

takaful) and payment of taxes (i.e. an owner’s obligations) back to Originator. Any

reimbursement amounts or service charges payable to Servicing Agent are set off

against (i) a corresponding ‘supplementary rental’ under the Ijara or (ii) an

additional amount which is added to the Exercise Price (payable under the

Purchase Undertaking or the Sale Undertaking, as applicable).

Purchase Undertaking

(Wa’d)

Granted by Originator

(as Obligor) in favour of

Trustee

Allows Trustee to sell the Assets back to Originator if an event of default occurs

or at maturity, in return for which Originator is required to pay all outstanding

amounts (through an Exercise Price) so that Trustee can pay the Investors.

Sale Undertaking

(Wa’d)

Granted by Trustee in

favour of Originator (as

Obligor)

Allows Originator to buy the Assets back from Trustee in limited circumstances

(e.g. the occurrence of a tax event), in return for which Originator is required to

pay all outstanding amounts (through an Exercise Price) so that Trustee can pay

the Investors.

Substitution

Undertaking (Wa’d) -

OPTIONAL

Granted by Trustee in

favour of Originator (as

Obligor)

Allows Originator to substitute the Assets (which it may need to sell or

otherwise dispose of) for some other assets having at least the same value and

revenue-generating properties.

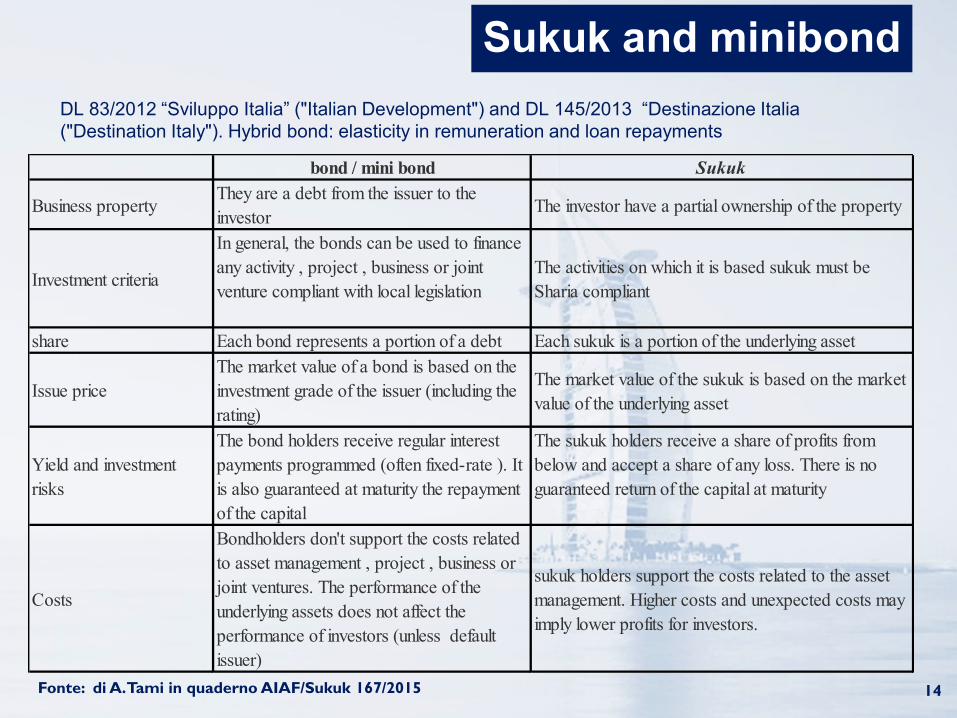

Sukuk and minibond

14

DL 83/2012 “Sviluppo Italia” ("Italian Development") and DL 145/2013 “Destinazione Italia

("Destination Italy"). Hybrid bond: elasticity in remuneration and loan repayments

Fonte: di A. Tami in quaderno AIAF/Sukuk 167/2015

bond / mini bond Sukuk

Business propertyThey are a debt from the issuer to the

investorThe investor have a partial ownership of the property

Investment criteria

In general, the bonds can be used to finance

any activity , project , business or joint

venture compliant with local legislation

The activities on which it is based sukuk must be

Sharia compliant

share Each bond represents a portion of a debt Each sukuk is a portion of the underlying asset

Issue price

The market value of a bond is based on the

investment grade of the issuer (including the

rating)

The market value of the sukuk is based on the market

value of the underlying asset

Yield and investment

risks

The bond holders receive regular interest

payments programmed (often fixed-rate ). It

is also guaranteed at maturity the repayment

of the capital

The sukuk holders receive a share of profits from

below and accept a share of any loss. There is no

guaranteed return of the capital at maturity

Costs

Bondholders don't support the costs related

to asset management , project , business or

joint ventures. The performance of the

underlying assets does not affect the

performance of investors (unless default

issuer)

sukuk holders support the costs related to the asset

management. Higher costs and unexpected costs may

imply lower profits for investors.

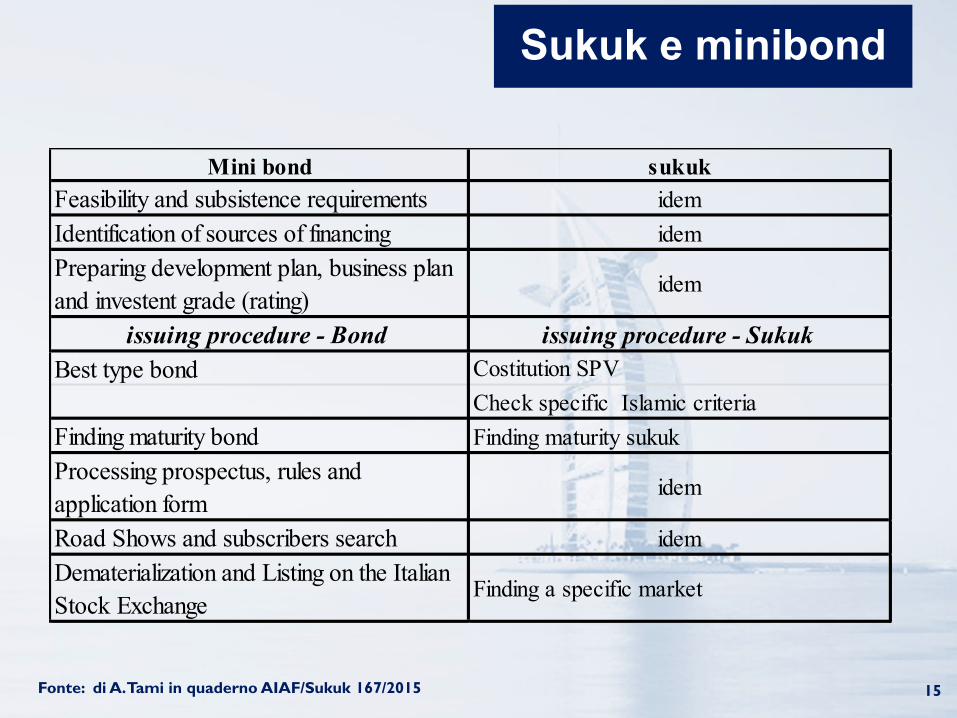

Sukuk e minibond

15 Fonte: di A. Tami in quaderno AIAF/Sukuk 167/2015

Mini bond sukuk

Feasibility and subsistence requirements idem

Identification of sources of financing idem

Preparing development plan, business plan

and investent grade (rating)idem

issuing procedure - Bond issuing procedure - Sukuk

Best type bond Costitution SPV

Check specific Islamic criteria

Finding maturity bond Finding maturity sukuk

Processing prospectus, rules and

application formidem

Road Shows and subscribers search idem

Dematerialization and Listing on the Italian

Stock ExchangeFinding a specific market

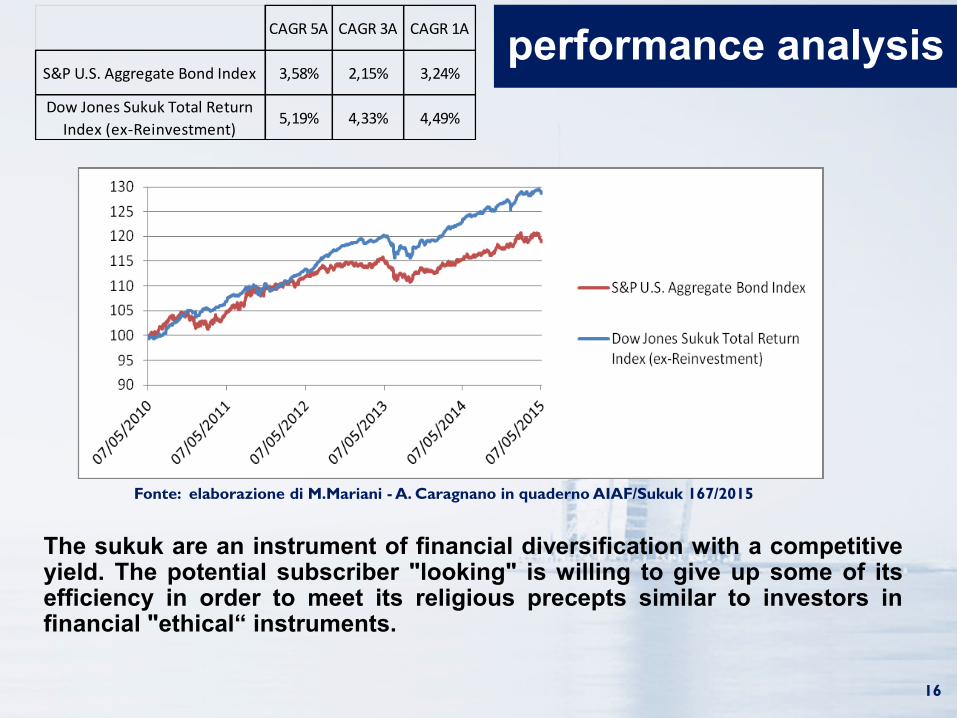

performance analysis

16

Fonte: elaborazione di M.Mariani - A. Caragnano in quaderno AIAF/Sukuk 167/2015

CAGR 5A CAGR 3A CAGR 1A

S&P U.S. Aggregate Bond Index 3,58% 2,15% 3,24%

Dow Jones Sukuk Total Return

Index (ex-Reinvestment)5,19% 4,33% 4,49%

The sukuk are an instrument of financial diversification with a competitive yield. The potential subscriber "looking" is willing to give up some of its efficiency in order to meet its religious precepts similar to investors in financial "ethical“ instruments.

Sukuk are a great alternative to raise funds not only for the Italian

companies, in search of funding diversification sources but also, and

above all, a viable alternative for the local Government authorities in

view of the project finance and securitization of real estate.

The evolution of the Italian legislation sought to promote the use of

hybrid financial instruments by companies, but despite that has not yet

taken a position on the development of Islamic finance in Italy. Sukuk is

to be considered, because of its peculiarity of not being a standardized

instrument, an alternative already viable, both as part of those

businesses oriented towards markets where the dominant religion is

Islam, and for those local Government authorities that, in the operations

of public-private partnerships can, through projects of international

importance, access to a financial channel alternative and qualified.

Conclusions

17

- Enrico Giustiniani coordinatore del gruppo finanza Islamica - AIAF

- Giorgio Carlo Brugnoni Credit Analyst presso Cassa Depositi e Prestiti

- Alessandra Caragnano, cultore della materia in Finanza Aziendale presso

l’Università Lum Jean Monnet

- Raffaele Didonato, statistico, membro della European Financial Management

Association e della Faculty of Actuaries Students' Society

- Paolo Gaspare Conforti Di Lorenzo Avvocato, Studio Legale Delfino e Associati

Willkie Farr & Gallagher LLP

- Lorenzo Lentini, Avvocato, CONSOB

- Massimo Mariani, Professore associato di Finanza Aziendale e Finanza Immobiliare

- Claudio Palandra ingegnere matematico. ALM ed asset allocation strategica per

PosteVita e PosteAssicura

- Fabrizio Petrucci avvocato cassazionista, partner Studio Delfino e Associati Willkie

Farr & Gallagher LLP

- Antonio Salvi Preside della Facoltà di economia dell’Università LUM “Jean Monnet”.

Professore Ordinario di finanza aziendale

- Alessandra Tami professore Associato di Bilancio presso la Scuola di Economia e

Statistica dell’Università degli Studi di Milano – Bicocca

AIAF - Islamic Finance Working Group

18

Thank you for your attention

19