Embed Size (px)

Citation preview

28NOV200902355264

Offering memorandum

Grupo Posadas, S.A.B. de C.V.$200,000,000$9.250% Senior Notes Due 2015Interest Payable January 15 and July 15Issue Price: 99.023%

We are offering $200,000,000 aggregate principal amount of our 9.250% Senior Notes due 2015.

The notes will mature on January 15, 2015. We will pay interest on the notes on January 15 and July 15,commencing on July 15, 2010. The notes will bear interest at a rate equal to 9.250% per annum.

We may redeem the notes, in whole or in part, at a redemption price based on a ‘‘make-whole’’ premium.Until January 15, 2013, we may redeem up to 35% of the notes with the net proceeds of qualified equityofferings (as defined under ‘‘Description of the Notes’’). If we undergo a change of control or sell certain ofour assets, we may be required to offer to purchase notes from holders.

The notes will be our senior unsecured obligations and will rank equally with all of our other unsecuredsenior indebtedness, except for our obligations that are preferred by statute, and senior to all of oursubordinated indebtedness. The notes will be unconditionally guaranteed by certain of our existing andfuture wholly-owned direct and indirect subsidiaries. The guarantees will be the senior unsecured obligationsof the guarantors and will rank equally with all of the guarantors’ other senior unsecured indebtedness,except for their obligations that are preferred by statute, and senior to all of the guarantors’ subordinatedindebtedness. The notes and the guarantees will be effectively subordinated in right of payment to all of ourand the guarantors’ secured indebtedness, and the notes and the guarantees will also be effectivelysubordinated in right of payment to all liabilities, including trade payables, of our subsidiaries that are notguarantors.

We have applied to list the notes on the official list of the Luxembourg Stock Exchange and to trade on theEuro MTF Market. However, we cannot assure you that the listing application will be approved. This offeringcircular constitutes a prospectus for the purpose of Luxembourg law dated July 10, 2005 on Prospectuses forSecurities.

Investing in the notes involves risks that are described in the ‘‘Risk Factors’’ section beginning on page 13 ofthis offering memorandum.

The notes have not been registered under the Securities Act of 1933, as amended (the ‘‘Securities Act’’), orthe securities laws of any other jurisdiction. We are offering the notes only to qualified institutional buyersunder Rule 144A promulgated under the Securities Act and to persons outside the United States underRegulation S promulgated under the Securities Act. See ‘‘Transfer Restrictions.’’

THE NOTES HAVE NOT BEEN AND WILL NOT BE REGISTERED WITH THE REGISTRO NACIONAL DE VALORES(NATIONAL SECURITIES REGISTRY) MAINTAINED BY COMISION NACIONAL BANCARIA Y DE VALORES (NATIONALBANKING AND SECURITIES COMMISSION), OR CNBV, AND MAY NOT BE OFFERED OR SOLD PUBLICLY, OROTHERWISE BE THE SUBJECT OF BROKERAGE ACTIVITIES IN MEXICO, EXCEPT PURSUANT TO THE PRIVATEPLACEMENT EXEMPTION SET FORTH UNDER ARTICLE 8 OF THE LEY DEL MERCADO DE VALORES (MEXICANSECURITIES MARKET LAW). AS REQUIRED UNDER THE MEXICAN SECURITIES MARKET LAW, WE WILL NOTIFY THECNBV OF THE OFFERING OF THE NOTES OUTSIDE OF MEXICO. SUCH NOTICE WILL BE DELIVERED TO THE CNBV TOCOMPLY WITH A LEGAL REQUIREMENT AND FOR INFORMATION PURPOSES ONLY, AND THE DELIVERY TO ANDTHE RECEIPT BY THE CNBV OF SUCH NOTICE DOES NOT IMPLY ANY CERTIFICATION AS TO THE INVESTMENTQUALITY OF THE NOTES OR OF OUR SOLVENCY, LIQUIDITY OR CREDIT QUALITY OR THE ACCURACY ORCOMPLETENESS OF THE INFORMATION SET FORTH HEREIN. THE INFORMATION CONTAINED IN THIS OFFERINGMEMORANDUM IS SOLELY THE RESPONSIBILITY OF GRUPO POSADAS, S.A.B. DE C.V. AND HAS NOT BEENREVIEWED OR AUTHORIZED BY THE CNBV. IN MAKING AN INVESTMENT DECISION, ALL INVESTORS, INCLUDINGANY MEXICAN INVESTORS WHO MAY ACQUIRE NOTES FROM TIME TO TIME, MUST RELY ON THEIR OWN REVIEWAND EXAMINATION OF GRUPO POSADAS, S.A.B. DE C.V.

Delivery of the notes has been made to investors in book-entry form through The Depository Trust Companyon January 15, 2010.

Sole book-running manager

J.P. MorganFebruary 5, 2010

14

4

4

4 Other

13 2

6010

71

This map shows the number and brand of our hotels in the countries in which we operate as of September 30, 2009.

Source: Grupo Posadas

i

You should rely only on the information contained in this offering memorandum. We have not, and the initial purchaser has not, authorized any other person to provide you with different information. If any person provides you with different or inconsistent information, you should not rely on it. We are not, and the initial purchaser is not, making an offer to sell, or seeking offers to buy, the notes in any jurisdiction where the offer or sale is not permitted. This offering memorandum does not constitute an offer to sell, or a solicitation of an offer to buy, any notes by any person in any jurisdiction in which it is unlawful for such person to make such an offer or solicitation. You should assume that the information contained in this offering memorandum is accurate only as of any date on the front of this offering memorandum. Our business, financial condition, results of operations and prospects may have changed since that date.

This offering memorandum has been prepared by us solely for use in connection with the placement of the notes. We and the initial purchaser reserve the right to reject any offer to purchase for any reason.

TABLE OF CONTENTS ENFORCEMENT OF CIVIL LIABILITIES ................................................................................................... iii WHERE YOU CAN FIND MORE INFORMATION...................................................................................... iii PRESENTATION OF FINANCIAL AND OPERATING INFORMATION ..................................................... iv FORWARD-LOOKING STATEMENTS...................................................................................................... vii SUMMARY...................................................................................................................................................1 SUMMARY OF THE OFFERING.................................................................................................................7 SUMMARY CONSOLIDATED FINANCIAL AND OPERATING INFORMATION ......................................10 RISK FACTORS.........................................................................................................................................13 EXCHANGE RATES..................................................................................................................................34 USE OF PROCEEDS.................................................................................................................................35 CAPITALIZATION ......................................................................................................................................36 SELECTED FINANCIAL AND OPERATING INFORMATION...................................................................37 MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF

OPERATIONS...............................................................................................................................40 BUSINESS .................................................................................................................................................66 MANAGEMENT .........................................................................................................................................87 PRINCIPAL SHAREHOLDERS .................................................................................................................93 RELATED PARTY TRANSACTIONS ........................................................................................................94 DESCRIPTION OF OTHER INDEBTEDNESS..........................................................................................95 DESCRIPTION OF THE NOTES...............................................................................................................99 BOOK-ENTRY; DELIVERY AND FORM .................................................................................................139 TAXATION ...............................................................................................................................................143 PLAN OF DISTRIBUTION .......................................................................................................................148 TRANSFER RESTRICTIONS..................................................................................................................151 LEGAL MATTERS ...................................................................................................................................153 INDEPENDENT AUDITORS....................................................................................................................154 GENERAL LISTING INFORMATION.......................................................................................................155 INDEX TO CONSOLIDATED FINANCIAL STATEMENTS ......................................................................F-1 APPENDIX A – SUMMARY OF CERTAIN DIFFERENCES BETWEEN MEXICAN FRS AND U.S.

GAAP................................................................................................................................................. A-1

_____________________

Neither the Securities and Exchange Commission, or SEC, any state securities commission nor any other regulatory authority has approved or disapproved the notes; nor have any of the foregoing authorities passed upon or endorsed the merits of this offering or the accuracy or adequacy of this offering memorandum. Any representation to the contrary is a criminal offense.

ii

The initial purchaser makes no representation or warranty, express or implied, as to the accuracy or completeness of the information contained in this offering memorandum. Nothing contained in this offering memorandum is, or shall be relied upon as, a promise or representation by the initial purchaser as to the past or future. We have furnished the information contained in this offering memorandum. The initial purchaser has not independently verified any of the information contained herein (financial, legal or otherwise) and assumes no responsibility for the accuracy or completeness of any such information.

The notes are subject to restrictions on transferability and resale and may not be transferred or resold except as permitted under the Securities Act and the applicable securities laws of any state or other jurisdiction pursuant to registration or exemption therefrom. As a prospective purchaser, you should be aware that you may be required to bear the financial risks of this investment for an indefinite period of time. Please refer to the sections in this offering memorandum entitled “Plan of Distribution” and “Transfer Restrictions.”

In making an investment decision, prospective investors must rely on their own examination of our business and the terms of the offering, including the merits and risks involved. Prospective investors should not construe anything in this offering memorandum, as legal, business or tax advice. Each prospective investor should consult its own advisors as needed to make its investment decision and to determine whether it is legally permitted to purchase the securities under applicable legal investment or similar laws or regulations.

In this offering memorandum, we rely on and refer to information and statistics regarding our industry and the economic condition of the countries where we operate. We have obtained this data from either our internal studies or publicly available sources such as independent industry publications and government sources. Although we believe that these publicly available sources are reliable, we have not independently verified and do not guarantee the accuracy and completeness of this information.

This offering memorandum contains summaries believed to be accurate with respect to certain documents, but reference is made to the actual documents for complete information. All such summaries are qualified in their entirety by such reference. Copies of documents referred to herein will be made available to prospective investors upon request to us or the initial purchaser.

We accept responsibility for the information contained in this offering circular. To the best of our knowledge and belief (and we have taken all reasonable care to ensure that), the information contained in this offering circular is in accordance with the facts and does not omit any material information. You should assume that the information contained in this offering circular is accurate only as of the date on the front cover of this offering circular.

NOTICE TO NEW HAMPSHIRE RESIDENTS

NEITHER THE FACT THAT A REGISTRATION STATEMENT OR AN APPLICATION FOR A LICENSE HAS BEEN FILED UNDER CHAPTER 421-B OF THE NEW HAMPSHIRE REVISED STATUTES ANNOTATED (THE “RSA”) WITH THE STATE OF NEW HAMPSHIRE NOR THE FACT THAT A SECURITY IS EFFECTIVELY REGISTERED OR A PERSON IS LICENSED IN THE STATE OF NEW HAMPSHIRE CONSTITUTES A FINDING BY THE SECRETARY OF STATE THAT ANY DOCUMENT FILED UNDER CHAPTER 421-B OF THE RSA IS TRUE, COMPLETE AND NOT MISLEADING. NEITHER ANY SUCH FACT NOR THE FACT THAT AN EXEMPTION OR EXCEPTION IS AVAILABLE FOR A SECURITY OR A TRANSACTION MEANS THAT THE SECRETARY OF STATE HAS PASSED IN ANY WAY UPON THE MERITS OR QUALIFICATIONS OF, OR RECOMMENDED OR GIVEN APPROVAL TO, ANY PERSON, SECURITY OR TRANSACTION. IT IS UNLAWFUL TO MAKE, OR CAUSE TO BE MADE, TO ANY PROSPECTIVE PURCHASER, CUSTOMER OR CLIENT ANY REPRESENTATION INCONSISTENT WITH THE PROVISIONS OF THIS PARAGRAPH.

____________________

iii

ENFORCEMENT OF CIVIL LIABILITIES

Grupo Posadas S.A.B. de C.V., or Posadas, is a sociedad anónima bursátil de capital variable (listed corporation with variable capital) organized under the laws of the United Mexican States, or Mexico. All of our directors and substantially all of our officers and certain of the experts named herein are non-U.S. residents, and all or a significant portion of the assets of those persons may be, and the most significant portion of our assets are, located outside the United States. As a result, it may not be possible for investors to effect service of process within the United States upon those persons or to enforce against them or against us in U.S. courts judgments predicated upon civil liability provisions of the U.S. federal or state securities laws. We have been advised by our Mexican counsel, Romo, Paillés y Guzmán, S.C., that there is doubt as to the enforceability, in original actions in Mexican courts, of liabilities predicated solely on the U.S. federal securities laws and as to the enforceability in Mexican courts of judgments of U.S. courts obtained in actions predicated upon the civil liability provisions of the U.S. federal securities laws.

WHERE YOU CAN FIND MORE INFORMATION

So long as any notes remain outstanding, we will make available, upon request, to any holder and any prospective purchaser of notes the information required pursuant to Rule 144(A)(d)(4)(i) under the Securities Act, during any period in which we are not subject to Section 13 or 15(d) of the U.S. Securities Exchange Act of 1934, as amended, or the Exchange Act.

You may obtain a copy of the indenture that governs the notes by requesting it in writing or by telephone at the address and phone number below.

Grupo Posadas, S.A.B. de C.V.

Attention: Corporate Finance Department Paseo de la Reforma No. 155

Colonia Lomas de Chapultepec 11000, México, D.F.

México Telephone number: (52 55) 5326 6757

We have applied to list the notes on the Official List of the Luxembourg Stock Exchange and to trade the notes on the Euro MTF Market. See “General Listing Information.” We will comply with any undertakings assumed or undertaken by us from time to time to the Euro MTF Market in connection with the notes, and we will furnish to them all such information as the rules of the Luxembourg Stock Exchange may require in connection with the listing of the notes.

Our principal executive offices are located at Paseo de la Reforma 155, Colonia Lomas de Chapultepec, Mexico City, Mexico 11000, and our telephone number is (52 55) 5326-6700. Additional information about our company and our operations can be found at our website at http://www.posadas.com. Information available on our website is not a part of, nor is it incorporated by reference into, this offering memorandum.

iv

PRESENTATION OF FINANCIAL AND OPERATING INFORMATION

Grupo Posadas, S.A.B. de C.V. is a corporation with variable capital organized under the laws of Mexico and is a holding company that conducts a substantial amount of business through subsidiaries. In this offering memorandum, except when indicated or the context otherwise requires, the words “Posadas,” “Grupo Posadas,” “we,” “us,” “our” and “ours” refer to Grupo Posadas, S.A.B. de C.V. together with its consolidated subsidiaries.

For purposes of this offering memorandum, we refer to hotels we operate in which we have an equity interest of 50% or greater as our “owned hotels,” hotels we operate in which we have a leasehold interest as our “leased hotels” and hotels we operate for unrelated third parties (i.e., hotels in which we do not have an equity interest of 50% or greater or a leaseholder interest) as our “managed hotels.”

We have entered into management contracts with all of the hotels that we operate, pursuant to which we receive management and other fees. Fees we receive from our owned and leased hotels are paid to us on substantially the same basis as fees we receive from unrelated third parties with respect to our managed hotels. In order to account for all of the revenues generated by our hotel management business, we do not eliminate from our consolidated statements of operations revenues generated by the fees that our owned and leased hotels pay to us. Our consolidated operating income is not affected by this treatment because the expenses relating to the fees paid by our owned and leased hotels are also not eliminated. Other significant intercompany balances are eliminated in consolidation. For additional information relating to the consolidation of our financial statements and the methods of intercompany elimination employed in such consolidation, see note 2(c) to our audited financial statements and to our unaudited interim financial statements, included herein.

Financial information

This offering memorandum includes our audited consolidated financial statements as of December 31, 2008 and 2007 and for each of the three years in the period ended December 31, 2008, and our unaudited condensed consolidated interim financial statements as of and for the nine months ended September 30, 2009 and 2008.

Our consolidated financial statements have been prepared in accordance with Mexican Financial Reporting Standards, or Mexican FRS (individually referred to as Normas de Información Financiera, or NIFs), issued by the Consejo Mexicano para la Investigación y Desarrollo de Normas de Información Financiera (Mexican Board for Research and Development of Financial Information Standards), or CINIF, which differ in certain significant respects from accounting principles generally accepted in the United States of America, or U.S. GAAP. For a description of certain significant differences between Mexican FRS and U.S. GAAP, see “Appendix A — Summary of Certain Differences Between Mexican FRS and U.S. GAAP.”

We have not prepared a reconciliation of our consolidated financial statements and related footnotes between Mexican FRS and U.S. GAAP and have not quantified such differences. Accordingly, no assurance is given that the description of certain significant differences between Mexican FRS and U.S. GAAP in Appendix A discusses all material differences between our financial information as prepared in accordance with Mexican FRS as opposed to U.S. GAAP. In making an investment decision, investors must rely upon their own examination of Posadas, the terms of the offering and the financial statements and other information included herein. Potential investors should consult their own advisors for an understanding of the differences between Mexican FRS and U.S. GAAP and how those differences might affect the financial information herein.

Effects of inflation

Pursuant to Bulletin B-10, “Recognition of the Effects of Inflation on Financial Information” issued by the CINIF, through 2007, our consolidated financial statements were reported in constant period-end pesos to adjust for the inter-period effects of inflation. The presentation of financial information in currency units of the most recently ended period, or constant currency units, was intended to eliminate the distorting effect of inflation on the financial statements and to permit comparisons across periods in comparable monetary units.

v

In 2007, NIF B-10, “Effects of Inflation” was issued, and became effective on January 1, 2008. This new NIF ceases the recognition of the comprehensive effects of inflation on financial information unless the economic environment in which the entity operates qualifies as inflationary. An environment is considered inflationary if the cumulative inflation rate in the relevant jurisdiction equals or exceeds 26% over the three preceding years. Because of the relatively low level of Mexican inflation in recent years, we have not recognized inflation for our Mexican entities in the financial information beginning January 1, 2008 presented in this offering memorandum. Accordingly, unless otherwise noted, all financial information through December 31, 2007 has been restated in constant pesos as of such date and all other information beginning January 1, 2008 is stated in nominal pesos, considering that non-monetary assets and stockholders’ equity accounts include inflationary effects recognized through December 31, 2007.

The rates of inflation in Mexico, as measured by changes in the Índice Nacional de Precios al Consumidor (Mexican national consumer price index), or INPC, published by Banco de México, were 6.53% for 2008, 3.8% for 2007 and 4.1% for 2006.

Rounding

Certain figures included in this offering memorandum and in our financial statements have been rounded for ease of presentation. Percentage figures included in this offering memorandum have not in all cases been calculated on the basis of such rounded figures but on the basis of such amounts prior to rounding. For this reason, percentage amounts in this offering memorandum may vary from those obtained by performing the same calculations using the figures in our financial statements. Certain numerical figures shown as totals in certain tables may not be an arithmetic aggregation of the figures that preceded them due to rounding.

EBITDA

This offering memorandum also includes our EBITDA, or earnings before interest, taxes and depreciation and amortization, which we calculate by adding depreciation and amortization to our consolidated operating income as determined in accordance with Mexican FRS. EBITDA is not a measure recognized under Mexican FRS or under U.S. GAAP, does not have a standardized meaning and may not be comparable to similarly titled measures provided by other companies either in Mexico or in other jurisdictions. In addition, we have not calculated EBITDA in accordance with the guidelines adopted by the SEC on presentation of non-GAAP financial measures. Moreover, our manner of calculating EBITDA in this offering memorandum may not be the same as the way in which we will calculate EBITDA for purposes of compliance with the covenants set forth in the Indenture governing the Notes. We disclose EBITDA because we use it as a measure of our consolidated operating performance. EBITDA should not be considered in isolation or as a substitute for net income or loss or as an indicator of operating performance or cash flow or as a measure of liquidity or our ability to service debt obligations.

Currency information

We publish our financial statements in pesos. Unless otherwise specified or the context otherwise requires, references in this offering memorandum to “pesos” or “Ps.” are to Mexican pesos as of December 31, 2007 for annual periods ended on or prior to such date, and to nominal Mexican pesos thereafter, except for those entities that operate in inflationary environments, as defined by Mexican FRS, and thus continue to recognize the effects of inflation in their financial statements. Also, unless otherwise specified or the context otherwise requires, we present pesos in this offering memorandum in thousands of pesos. Unless otherwise specified or the context otherwise requires, references in this offering memorandum to “U.S. dollars,” “$” or “U.S.$” are to United States dollars, all references to “reais”, “reals” or “R$”, are to Brazilian reais, all references to “P$” are to Argentine pesos and all references to “Ch$” are to Chilean pesos.

Solely for the convenience of the reader, certain amounts presented in Mexican pesos in this offering memorandum as of and for the year ended December 31, 2008 and the nine months ended September 30, 2009 have been converted into U.S. dollars at specified exchange rates. According to the Mexican FRS, Posadas determines the exchange rate applicable for the end of each period from the conversion rate of the transactions executed by Posadas in the open market prior to the end of the dates

vi

indicated. Unless otherwise indicated, the exchange rate used in converting Mexican pesos into U.S. dollars for amounts presented as of and for the year ended December 31, 2008 and as of and for the nine months ended September 30, 2009 was determined by reference to the exchange rate of Ps.13.5383 per U.S. dollar and Ps.13.4890 per U.S. dollar, respectively. Management does not believe there is a material difference between the rate applied for purposes of our financial reporting and the rates published by the Banco de Mexico in the Federal Official Gazette as the rate for the payment of obligations denominated in non-Mexican currency payable in Mexico. You should not construe our conversions as representations that the Mexican peso amounts actually represent the United States dollar amounts presented, or that they could be converted into U.S. dollars at the rate or at the dates indicated. See “Exchange Rates.”

Industry and market data

Unless otherwise noted, market data and other statistical information used throughout this offering memorandum are based on our estimates, which are derived from our review of internal surveys and independent industry publications, government publications, and reports by market research firms or other published independent sources, including, reports and analyses prepared by Smith Travel Research, the World Tourism Organization and the Secretaría de Turismo (Ministry of Tourism) of the Mexican federal government. Although we believe our sources, including our estimates, are reliable, we have not independently verified the information and cannot guarantee its accuracy or completeness.

vii

FORWARD-LOOKING STATEMENTS

This offering memorandum includes forward-looking statements within the meaning of the U.S. securities laws. These forward-looking statements include, but are not limited to, statements about our future financial position and results of operations, our strategy, plans, objectives, goals and targets, future developments in the markets where we participate or are seeking to participate and other statements contained in this offering memorandum that are not historical facts. In some cases, you can identify forward-looking statements by terminology such as “anticipate,” “believe,” “continue,” “could,” “estimate,” “expect,” “forecast,” “intend,” “may,” “plan,” “potential,” “predict,” “should” or “will” or the negative of such terms or comparable terminology. Such forward-looking statements involve known and unknown risks, uncertainties and other factors, some of which are beyond our control, which may cause our actual results, performance or achievements expressed or implied by such forward-looking statements to differ materially from historical results or those anticipated. Such forward-looking statements are based on numerous assumptions regarding our present and future business strategies and the environment in which we will operate in the future. These risks, uncertainties and other factors include, among other things, those listed under “Risk Factors” as well as those included elsewhere in this offering memorandum and include, but are not limited to:

political and economic factors in Mexico, Brazil, Argentina, Chile and the United States;

supply and demand changes for hotel rooms and vacation club memberships in our markets;

the financial condition of the airline industry and its impact on the lodging industry;

the impact of government regulations, including land use, tax, health, safety and environmental laws;

capital market volatility;

risks related to our business, our strategy, our expectations about growth in demand for our services, our expectations as to our ability to increase the number of hotels and hotel rooms we manage and our business operations, financial condition and results of operations;

statements of our plans, objectives or goals, including our ability to implement our strategy;

the availability of funds to finance growth;

currency fluctuations and inflation in the countries in which we operate;

the impact of natural events, such as earthquakes, hurricanes and floods; and

health pandemics, such as the recent H1N1 influenza outbreak.

These factors could cause our actual results, performance or achievements to differ materially from those in the forward-looking statements.

These forward-looking statements speak only as of the date of this offering memorandum and we undertake no obligation to update our forward-looking statements or risk factors to reflect new information, future events or otherwise. Additional factors affecting our business emerge from time to time and it is not possible for us to predict all of these factors, nor can we assess the impact of all such factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements. Although we believe that the plans, intentions, and expectations reflected in or suggested by such forward-looking statements are reasonable, we can give no assurance that such plans, intentions or expectations will be achieved. In addition, you should not interpret statements regarding past trends or activities as assurances that those trends or activities will continue in the future. While we continually review trends and uncertainties affecting our results of operations and financial condition, we do not intend to update any particular forward-looking statements contained in this offering memorandum.

(This page has been left blank intentionally.)

1

SUMMARY

This summary contains basic information about us and this offering. Because it is a summary, it does not contain all of the information that you should consider before investing. You should read this entire offering memorandum carefully, including the section entitled “Risk Factors” and our financial statements and the notes thereto incorporated by reference herein before making an investment decision.

Overview

We are primarily engaged in the business of operating hotels in several countries in Latin America and our principal operations are located in Mexico and Brazil. According to Hotels magazine, we are the largest Latin American operator of hotels based on number of hotels and number of rooms. We also believe that we are the leading operator of hotels in Mexico based on number of hotels, number of rooms, geographic coverage, revenues and market share. We distinguish ourselves from other operators by offering to hotel owners superior franchise services including, among other things, centralized reservation and marketing resources, revenue-optimization services, data gathering and analysis platforms, robust customer loyalty programs and strong, well-defined brands.

Through our subsidiaries, we operate 110 hotels (including four vacation club resorts) with a total of 19,454 rooms in Mexico, Brazil, Argentina, Chile and the United States (in the State of Texas). In Mexico we operate 94 hotels with a total of 16,487 rooms (including our vacation club units). We also operate 10 hotels in Brazil with a total of 1,899 rooms, two hotels in Argentina with a total of 247 rooms and one hotel in Chile with 142 rooms. In addition, we currently operate three hotels with a total of 679 rooms in Texas. Of the 110 hotels we operate, 33 are owned hotels, 19 are leased hotels and 58 are managed hotels (not including our owned and leased hotels that we also manage). Our hotels are located in a mix of urban and coastal destinations serving both leisure and business travelers and approximately 80% of our rooms are in urban destinations and 20% of our rooms are in coastal destinations. See “Business—Hotel Business” for a description of each of the structures under which we operate our hotel business.

We also operate a vacation club business through Fiesta Americana Vacation Club, or FAVC. FAVC markets and sells memberships that grant a right to use vacation club resorts that we own and operate in upscale destinations in Mexico including Los Cabos, Cancun, Acapulco and Kohunlich, Mexico, as well as other affiliated properties. In most cases, we provide financing to customers who purchase such memberships. Our vacation club business represented 20.9% and 29.2% of our revenues for the year ended December 31, 2008 and for the nine months ended September 30, 2009, respectively.

In addition, in recent years, we have attempted to market our management skills and technology platform, originally developed to support our hotel operating business, by opening a number of related services businesses: Ampersand manages loyalty programs for diverse related and unrelated businesses; Konexo provides call center and contact services and related customer-contact services for related and unrelated businesses; Conectum offers business process outsourcing services, or shared services, for diverse industries; and GloboGO offers online travel planning services.

Together with the expansion of our hotel operations and vacation club business, we have sought to develop strong brand names and to foster customer recognition of our brand-wide consistency of service. We consider our brands to be one of our main assets. We operate substantially all of our hotels in Mexico under the Fiesta Americana, Fiesta Inn, Live Aqua and One Hotels brand names, while in South America, we operate our hotels under the Caesar Park and Caesar Business brand.

Our Hotel Brands

Fiesta Americana is our flagship brand. We currently operate 18 hotels under this brand. Hotels operating under this brand offer deluxe, large scale, full-service accommodations to the high-end leisure traveler segment in coastal destinations and to the high-end business traveler segment in major urban centers. The Fiesta Americana line includes four hotels under the Fiesta Americana Grand brand. The Fiesta America hotels are upper-scale class hotels, and the Fiesta Americana Grand hotels are luxury class hotels. These hotels compete primarily with other high-end international and

2

Mexican brands. The hotels range from around 150 to over 600 rooms each. The Fiesta Americana and Fiesta Americana Grand brands constitute 27% of our total rooms.

Fiesta Inn hotels are smaller, more moderately priced hotels relative to Fiesta Americana hotels. Fiesta Inn hotels are medium-scale class hotels offering modern, comfortable accommodations and efficient service primarily to the domestic and regional business traveler segment. We currently operate 60 hotels in Mexico under the Fiesta Inn brand and these hotels are typically located in small, mid-size or major urban destinations or suburbs of major urban areas. Fiesta Inn hotels compete primarily with other moderately priced Mexican and international chains, as well as with moderately priced Mexican independent hotel operators. The hotels range from around 100 to over 300 rooms each. The Fiesta Inn brand constitutes 45% of our total rooms.

Live Aqua is a luxury class, lifestyle resort hotel. The Live Aqua concept seeks to build a memorable experience through pampering details – including fine dining, aromatic scents, spirit-renewing sanctuaries and comfortable settings – and superior service. We have one, 371-room Live Aqua hotel which competes with other luxury resorts in the Riviera Maya and Cancun region. The Live Aqua brand constitutes 2% of our total rooms.

One Hotels is an innovative chain of economy class hotels in Mexico that offer guest’s security, confidence and comfort at an affordable cost. The warm atmosphere, efficient service and practical design is ideal for business travelers who desire a convenient location and restful accommodations at an accessible price. One Hotels compete primarily with other economy class Mexican chains and independent hotel operators. We operate 10 hotels under the One Hotels brand and each of the hotels has around 125 rooms. The One Hotels brand constitutes 7% of our total rooms.

Caesar Park and Caesar Park Silver hotels are luxury class, full-service hotels in major urban centers that cater primarily to the high-end business traveler segment. We currently operate three hotels in Brazil and two hotels in Argentina under the Caesar Park brand. Caesar Park hotels compete primarily with other high-end international brands. The hotels range from around 80 to over 200 rooms each. The Caesar Park and Caesar Park Silver brands constitute 4% of our total rooms.

Caesar Business hotels are smaller, moderately priced hotels offering practical lodging and efficient service primarily to the domestic and regional business traveler. We currently operate seven hotels in Brazil and one hotel in Chile under the Caesar Business brand. Caesar Business hotels are medium-scale class hotels that compete primarily with other moderately priced international brands. The hotels range from around 100 to 400 rooms each. The Caesar Business brand constitutes 8% of our total rooms.

We will selectively continue to develop new properties to grow our hotel and vacation club businesses, but we intend to emphasize growth by increasing the number of properties we manage under our brand portfolio. In particular, we plan to expand in Mexico primarily by adding more One Hotels and Fiesta Inn hotels to supply the business traveler segment and in South America by adding more Caesar Business hotels.

Our Other Brands

Fiesta Rewards is our customer loyalty program. Launched in 1989, we were the first hotel company in Mexico to develop a sound customer loyalty program. The point-based program offers a certain numbers of points for every dollar spent on stays and consumption in our hotels and in certain subscriber restaurants, bars and spas, among other places. The points can, in turn, be redeemed for a variety of rewards including, among other things, free hotel stays, airline reservations, car rentals and fashion products.

Fiesta Americana Vacation Club is the brand name for our vacation club business. FAVC members receive an annual allocation of points that members can redeem to stay

3

at our FAVC properties, any other hotels that we operate or, through FAVC’s affiliations with Resorts Condominium International, or RCI, and Hilton Hotels Corp., any RCI-affiliated resort or Hilton Grand Vacation Club, or HGVC, resort throughout the world. As of September 30, 2009, FAVC had almost 29,000 members.

We are also developing brand identities around our service businesses, including:

Ampersand operating our loyalty program management business for diverse related and unrelated businesses;

Konexo providing call center and customer care solutions for related and unrelated businesses;

Conectum offering business process outsourcing services, or back office shared services, for diverse industries; and

GloboGO operating our online travel planning portal.

Our Competitive Strengths

Although we operate in a highly competitive environment, we believe that we have developed a number of competitive strengths that position us well in the regions and businesses in which we operate. We believe that the following are the key highlights of our competitive position:

Strong market position. We are a leading hotel operator in Latin America. According to Hotels magazine, we are the largest Latin American operator of hotels based on number of hotels and number of rooms, and we believe we are the leading operator of hotels in Mexico based on number of hotels, number of rooms, geographic coverage, revenues and market share. In addition, we believe that we benefit from strong brand recognition in Mexico and Brazil and we have a reputation for providing high value accommodations in desirable locations.

Diversified portfolio of properties. Our diversified brand portfolio targets various market segments in various geographic locations— including business and leisure travelers in urban destinations in upscale and moderately-priced categories, and groups, conventions and leisure travelers in urban and coastal destinations. Historically, this diversification has enhanced our ability to maintain a stable cash flow in a variety of market conditions while also limiting our exposure to any particular brand, market segment or geographic location.

Our market position, strong reputation and superior brand and hotel management services attract third-party investment. During the last few years we have been able to expand our hotel business mainly through increasing our operation of hotels developed with investment capital provided by third parties. We distinguish ourselves from other operators by offering to hotel owners superior brand and hotel management services including, among other things, centralized reservation and marketing resources, revenue-optimization technology, data gathering and analysis platforms, robust customer loyalty programs and strong, well-positioned brands.

Scale. As the leading hotel operator in Latin America, we have achieved a scale to support our core technology platforms and marketing functions. We also believe that our scale helps to lower our procurement expenses including, for example, insurance, utilities, food and beverages, furniture, fixtures and equipment. As we further increase our room count, we expect that our economies of scale would further improve our operating cost structure.

Loyal customer base. We have created a loyal customer base through our Fiesta Rewards guest loyalty program. As of December 31, 2008, Fiesta Rewards had approximately 2.2 million members and accounted for 19% and 25% of the occupancy in Fiesta Americana and Fiesta Inn hotels, respectively. As of September 30, 2009,

4

members of Fiesta Rewards accounted for 13.8% and 19.8% of the occupancy in Fiesta Americana and Fiesta Inn hotels, respectively.

Investments in technology that seek to enhance profitability. We have invested and continue to invest in technology designed to achieve greater operating efficiencies, enhanced distribution capabilities and profitability. We believe that these investments have made our technology platform comparable to many major international hotel companies and have given us a strong competitive advantage over other Latin American competitors.

New business development and diversification. We have launched several new businesses with distinct competitive advantages by leveraging our strengths: talent, technology, marketing and broad expertise in the tourism and hospitality industry in Latin America for application to customers in the tourism space and in other industries.

Experienced management. Our senior management team is led by Mr. Gastón Azcárraga Andrade, who has been our Chairman and Chief Executive Officer since 1992. We have a well-qualified senior management team with an average of over 15 years of industry experience. We believe that, historically, the turnover among our senior management has been low relative to our competitors, reducing organizational volatility and allowing us consistently to pursue our long-term strategic interests.

Our Business Strategy

Our long term strategic plan is to be the leading hotel operator and a tourism-related services provider in Latin America, while developing and strategically investing in complementary and ancillary businesses that are synergistic with our core business.

We focus on maximizing shareholder value and return on capital by optimizing the use of our talent, real estate, third party management contracts and advanced proprietary operating systems. As part of our portfolio management strategy, we continuously examine our business units’ portfolio to address issues of market dynamics, demand, supply and competition. Several of our key strategies are highlighted below:

Leverage our infrastructure to improve on our previous utilization levels

We believe we have built a solid business infrastructure in recent years, diverse both geographically and by brand, and supported by talented professionals and leading-edge technology. Due to the negative impacts of the global economic crisis and H1N1 influenza outbreak, we believe our infrastructure is currently underutilized. Nevertheless, the recent crisis has allowed us to streamline our operations and improve our cost structure, responsiveness and profitability. We believe we are positioned to increase our utilization levels and operational performance in line with a global economic recovery.

Strengthen our capital structure

We seek to strengthen our capital structure to make us more resilient to industry cycles and to provide us with the flexibility and capacity to take advantage of opportunities that may arise in the future. Furthermore, we intend to focus on strengthening our capital structure through improving our cash flow generation and reprofiling the maturities of our consolidated indebtedness.

Continue to consolidate and expand our hotel network while maintaining limited capital expenditures

An important part of our growth strategy is to continue to benefit from our strong brand recognition, solid reputation, centralized resources and extensive management experience which allow us to enter into additional hotel management contracts and, at the same time, to reduce our investment in owned hotels. Management contracts with hotels owned by third parties, including hotels that we lease from third parties, help improve our profitability by generating revenue streams at a relatively low marginal cost of leveraging our centralized resources and systems and with fairly minimal additional capital

5

investment by us. We believe that based on the above mentioned factors, we are an attractive option for hotel owners who seek profitable investments with a stable revenue stream. In the next 36 months, we plan to commence operating 52 new hotels with approximately 7,233 rooms pursuant to management contracts we are currently negotiating or have already entered into. Approximately 86% of these new hotels in development will be owned by unrelated third parties.

Continue to penetrate the moderately-priced business traveler segment

We have successfully addressed the needs of the domestic and regional business traveler, and our success has allowed us to diversify our operations. We believe the domestic and regional business travel segment continues to be underserved and represents attractive growth opportunities to us going forward. In 1993 we began to serve this segment in Mexico through our Fiesta Inn brand. Building on the success of Fiesta Inn, in 2001 we launched Caesar Business serving the business traveler in South America and, in 2007, we launched One Hotels, an economy class line in Mexico, catering to business travelers. We currently operate 60 Fiesta Inns, eight Caesar Business and ten One Hotels serving this market segment.

We plan to continue expanding our Fiesta Inn brand in the moderately-priced business traveler segment and to expand our One Hotels economy class brand to South America, primarily through third-party owned hotels.

Continue to develop our Fiesta Americana Vacation Club business

Leveraging our brand positioning, we have been able to build a solid and profitable vacation club business. Our solid brand names have helped us significantly increase our customer base while providing our customers a unique experience with unparalleled flexibility. We believe that the vacation club business enhances the profitability of our existing asset base by leveraging synergies stemming from both businesses. We will selectively continue converting, developing and constructing resorts or new vacation club units in appealing destinations.

Enhance the guest experience

We believe the knowledge of our guest’s preferences and patterns grant us a competitive advantage. For more than 20 years, we have consciously invested in customer loyalty programs, such as our Fiesta Rewards program, thereby creating loyal users of our hotels. Several years ago we decided to take the knowledge of our customer one step further. We have built a detailed database that feeds into a proprietary guest experience system, Delphos, which permits us to anticipate each customer's pre-stay, in-stay and post-stay needs, preferences and desires. Delphos allows us to tailor our services to each guest based on experience, thus creating a unique bond.

Develop talent

As we move from a company focused on property ownership towards an organization emphasizing portfolio management, we believe talent becomes one of our most important and visible assets. We believe our ability to identify, train and retain talent is one of our core enterprise strengths.

Focus on strengthening the core capabilities of our service businesses

We have successfully designed and developed specific service businesses, such as Ampersand, Konexo, Conectum and GloboGO, that support our day-to-day operations. We believe these businesses are synergistic to our operations and diversify our revenue stream. We intend to continue strengthening and developing those service businesses through marginal investments. We believe attractive business opportunities exist for the unique services we provide in the countries where we operate.

Continue leveraging our distribution strategy to efficiently capture market share

We believe our distribution platform gives us a competitive advantage because it allows us to seamlessly coordinate all reservation transactions in a dynamic pricing model, inventory and oversell limits that constrain the hotel industry. We believe that our information management platforms are robust and state of the art, and that these platforms allow us to benefit from the dynamic growth of our electronic distribution channels.

6

Realize cost savings and improve operating efficiencies

We are focused on effectively streamlining our operations to take advantage of cost reduction opportunities and to improve our profitability. We have reduced our distribution costs structure by centralizing and consolidating the room inventory data from our entire hotel portfolio into a single proprietary solution called the Central Inventory Posadas (ICP). We have enhanced our profitability through real-time dynamic pricing of our room inventory. We have also achieved similar cost reductions by centralizing and consolidating accounting, payroll, strategic sourcing and receivables processing. We are one of the few hotel operators in Latin America that have developed such systems.

Future growth

While we are currently focused on preserving liquidity, reducing leverage and improving operational performance, we may consider additional investments in the tourism-related industry, including new developments and/or opportunistic acquisitions, when conditions improve and further investments would be prudent. We will only consider investments that would add value to the existing portfolio, diversify our operations by market, geography or customer type, and improve EBITDA generation.

Corporate Headquarters

Our principal executive offices are located at Paseo de la Reforma 155, Colonia Lomas de Chapultepec, Mexico City, Mexico 11000, and our telephone number is (52 55) 5326-6700. Additional information about our company and our operations can be found at our website at http://www.posadas.com. Information available on our website is not a part of, nor is it incorporated by reference into, this offering memorandum.

7

SUMMARY OF THE OFFERING

Issuer................................................... Grupo Posadas, S.A.B. de C.V.

Notes Offered ..................................... U.S.$200,000,000 aggregate principal amount of 9.250% senior notes due January 15, 2015, or the Notes.

Issue Price .......................................... 99.023 % of the principal amount.

Maturity ............................................... January 15, 2015.

Interest Payment Dates ..................... January 15 and July 15 of each year, commencing July 15, 2010.

Indenture ............................................. The notes will be issued under an indenture, to be dated as of January 15, 2010, between us and The Bank of New York Mellon, as trustee.

Guarantees ......................................... The notes will be jointly and severally guaranteed by certain of our existing and future wholly-owned direct and indirect subsidiaries. See “Business—Organizational Structure” and “Risk Factors—Risks Relating to the Notes.”

Ranking ............................................... The notes will be our senior unsecured obligations and will rank equally with all of our other unsecured senior indebtedness, except for our obligations that are preferred by statute, and senior to all of our subordinated indebtedness. The guarantees of the guarantors will be the senior unsecured obligations of the guarantors and will rank equally with all of the guarantors’ other senior indebtedness, except for their obligations that are preferred by statute, and senior to all of the guarantors’ subordinated indebtedness. The notes and the guarantees will be effectively subordinated in right of payment to all of our and the guarantors’ secured indebtedness, and the notes and the guarantees will also be effectively subordinated in right of payment to all liabilities, including trade payables, of our subsidiaries that are not guarantors.

As of September 30, 2009, after giving pro forma effect to the sale of the notes offered hereby and the application of the gross proceeds thereof, our total consolidated indebtedness would have been U.S.$412.8 million. Applying the same pro forma effect and assuming that we do not elect to prepay the Banco del Bajio facility referred to in clause 6 of the second paragraph of “Use of Proceeds”, we and the guarantors would have had approximately U.S.$5.6 million of secured debt outstanding, while the total indebtedness of our non-guarantor subsidiaries would have been U.S.$25.2 million. The guarantors represented 88% and 64%, and 85% and 62%, of our total revenues and assets in the nine months ended September 30, 2008 and 2009, respectively.

Optional Redemption......................... We may redeem the notes, in whole or in part, at a redemption price based on a “make-whole” premium. Prior to January 15, 2013, we may redeem up to 35% of the aggregate principal amount of the notes with the proceeds from certain qualified equity offerings.

Redemption for Tax Reasons ........... We may redeem the notes at a redemption price equal to 100% of their principal amount, plus accrued interest, and any

8

additional amounts thereon, in whole but not in part, upon giving not less than 30 or more than 60 days’ notice if, as a result of

• any change in, or amendment to, the laws, rules or regulations of any Relevant Jurisdiction (as defined in “Description of the Notes—Redemption for Tax Reasons”) or taxing authority thereof or therein; or

• any amendment to or change in any (or any subsequently enacted) official interpretation, application or pronouncement regarding such laws, treaties rules or regulations, which are of general applicability;

we or any guarantor would be obligated to pay additional amounts in respect of the notes, in excess of those payable at a rate of 10.0%. See “Description of the Notes—Redemption for Tax Reasons.”

Restrictive Covenants ....................... The indenture governing the notes contains certain covenants which, among other things, restrict our and our restricted subsidiaries’ ability to:

• incur additional indebtedness; • grant liens; • make restricted payments; • make certain investments; • sell assets; • permit restrictions on the ability of restricted subsidiaries to

declare dividends; • enter into certain types of transactions with affiliates; and • merge or consolidate with other companies or transfer all or

substantially all of our assets.

These covenants are subject to a number of limitations and exceptions. See “Description of the Notes—Certain Covenants.”

Change of Control Offer .................... If we experience a change of control, holders of the notes may require us to repurchase all or part of the notes at 101% of their principal amount, plus accrued and unpaid interest and any additional amounts to the redemption date. See “Description of the Notes—Repurchase at the Option of Holders—Change of Control.”

Transfer Restrictions ......................... We have not registered the notes under the Securities Act or any state securities laws, and we will not be required to do so. Consequently, the notes may not be offered or sold within the United States or to, or for the account or benefit of, U.S. persons, except pursuant to an exemption from, or in a transaction not subject to, the registration requirements of the Securities Act.

Pursuant to the Ley del Mercado de Valores (Mexican Securities Market Law), the notes may not be offered or sold publicly in Mexico but may be privately offered under the private placement exemption set forth in Article 8 of the Mexican Securities Market Law.

Form of Notes and Clearance ........... The notes will be issued in the form of one or more global notes in fully registered form, without interest coupons, in denominations of U.S.$100,000 and integral multiples of U.S.$1,000 in excess thereof. Each global note will be deposited with, or on behalf of, a custodian for The Depository Trust

9

Company, or DTC, and registered in the name of DTC or its nominee.

Beneficial interests in each global note will be shown on, and transfers will be effected only through, records maintained by DTC and its direct and indirect participants, and any such interest may not be exchanged for certificated notes, except in limited circumstances.

Listing.................................................. We have applied to list the notes on the official list of the Luxembourg Stock Exchange and to trade on the Euro MTF market. However, we cannot assure you that the listing application will be approved.

Governing Law ................................... The notes, the guarantees and the indenture will be governed by the laws of the State of New York.

Use of Proceeds ................................. We intend to use the net proceeds from this offering to repay outstanding debt. Any remaining proceeds will be used for general corporate purposes. See “Use of Proceeds.”

Risk Factors........................................ Investing in the notes involves substantial risks. See “Risk Factors” for a description of certain of the risks that you should consider before investing in the notes.

10

SUMMARY CONSOLIDATED FINANCIAL AND OPERATING INFORMATION

The following tables set forth our summary historical and other financial data as of and for the periods indicated. The summary historical financial data for the years ended December 31, 2006, 2007 and 2008 were derived from the audited consolidated balance sheets as of December 31, 2008 and 2007 and the consolidated statements of operations for the years ended December 31, 2008, 2007 and 2006, of cash flows for the year ended December 31, 2008 and of changes in financial position for the years ended December 31, 2007 and 2006, as audited by Galaz, Yamakazi, Ruiz Urquiza, S.C., a member of Deloitte Touche Tohmatsu. The summary historical financial data as of and for the nine months ended September 30, 2008 and September 30, 2009, respectively, were derived from our unaudited condensed consolidated interim financial statements as of and for the periods then ended. Our unaudited condensed consolidated interim financial statements have been prepared on the same basis as our audited financial statements for the year ended December 31, 2008 and, in the opinion of management, include all adjustments, consistent only of normal, recurring adjustments, considered necessary for a fair presentation of our financial condition and results of operations for such periods. The following information is qualified by reference to, and should be read in conjunction with, “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and related notes beginning on page F-1 of this offering memorandum. The historical results are not necessarily indicative of results to be expected in any future period.

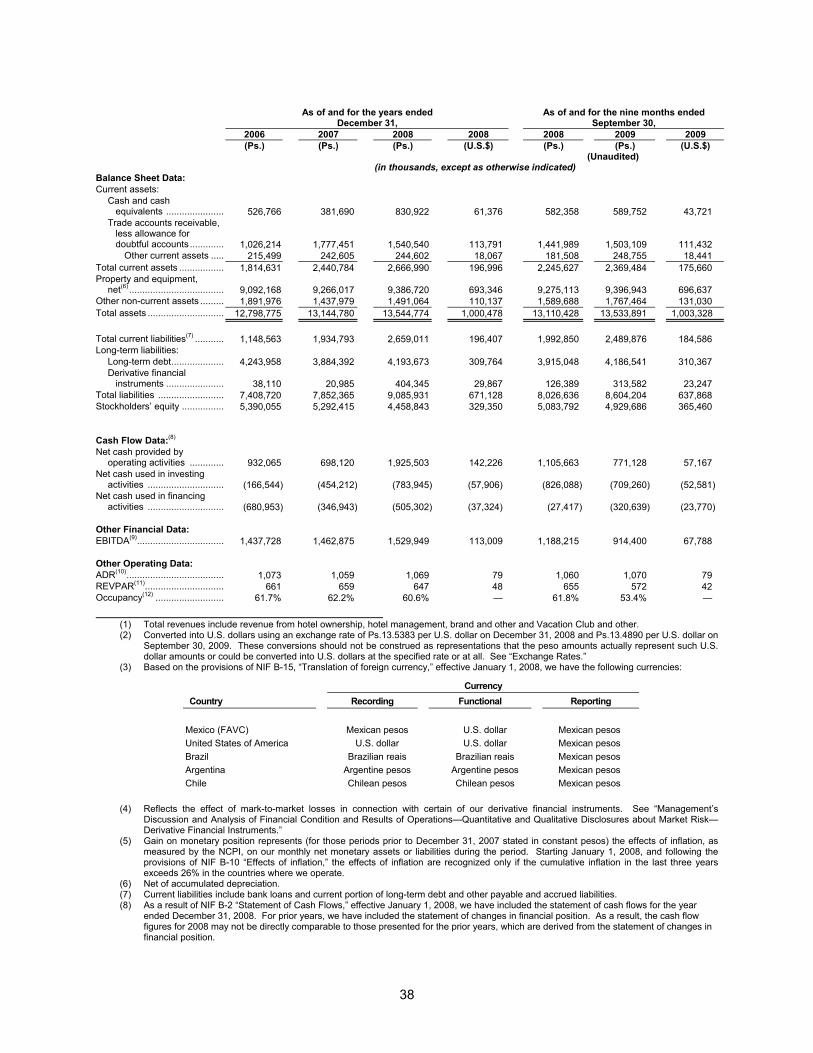

Years ended December 31, Nine months ended September 30, 2006 2007 2008 2008 2008 2009 2009 (Ps.) (Ps.) (Ps.) (U.S.$) (2) (Ps.) (Ps.) (U.S.$) (2) (Unaudited) (in thousands, except as otherwise indicated) Statement of Operations Data:

Total Revenues(1)..................... 5,528,221 5,974,224 6,904,520 509,999 5,211,854 5,224,969 387,350

Hotel ownership: Revenues .................................. 3,582,344 3,522,621 3,677,583 271,643 2,716,283 2,362,403 175,136 Direct costs and expenses ........ 2,569,770 2,625,464 2,791,774 206,213 2,063,135 1,875,420 139,033 Operating earnings from hotel ownership ......................

1,012,574

897,157

885,809

65,430 653,148

486,983

36,102

Hotel management, brand and other:

Revenues .................................. 1,040,469 1,289,110 1,655,402 122,275 1,240,637 1,219,952 90,441 Direct costs and expenses ........ 557,920 717,116 1,105,498 81,657 788,697 818,008 60,643 Operating earnings from hotel management, brand and other ................................

482,549

571,994

549,904

40,618 451,940

401,944

29,798

Vacation Club and other: Revenues .................................. 905,408 1,162,493 1,571,535 116,081 1,254,934 1,642,614 121,774 Direct costs and expenses ........ 660,308 844,594 1,046,496 77,299 856,647 1,268,469 94,037 Operating earnings from Vacation Club and other .........

245,100

317,899

525,039

38,782 398,287

374,145

27,737

Other operating expenses ......... 744,559 755,137 819,983 60,568 634,271 688,155 51,016 Operating income...................... 995,664 1,031,913 1,140,769 84,262 869,104 574,917 42,621 Comprehensive financing result:

Interest expense................. 415,179 388,397 420,311 31,046 296,311 289,760 21,481 Interest income .................. (35,979) (32,093) (6,989) (516) (14,736) (27,394) (2,031) Exchange loss (gain), net(3)...............................

65,738

(15,501)

(111,918)

(8,267) (54,084)

(29,296)

(2,172)

Loss from derivative financial instruments, net(4) ..............................

-

-

1,208,196

89,243 52,847

49,110

3,641 Gain on monetary position(5) .......................

(135,742)

(143,925)

——

——

——

——

——

Total comprehensive financing result .......................

309,196

196,878

1,509,600

111,506 280,338

282,180

20,919

Other expenses, net .................. 91,493 122,902 234,728 17,338 141,753 73,205 5,427 Equity in results of associated companies..............................

(1,114)

351,922

209,513

15,476 201,936

(1,350)

(100)

(Loss) income before income tax .............................

596,089

360,211

(813,072)

(60,057) 245,077

220,882

16,375

Income tax expense (benefit) .... 139,819 159,646 (111,226) (8,216) 220,016 86,330 6,400 Consolidated net (loss) income....................................

456,270

200,565

(701,846)

(51,842) 25,061

134,552

9,975

11

As of and for the years ended

December 31, As of and for the nine months ended

September 30, 2006 2007 2008 2008 2008 2009 2009 (Ps.) (Ps.) (Ps.) (U.S.$) (Ps.) (Ps.) (U.S.$) (Unaudited) (in thousands, except as otherwise indicated) Balance Sheet Data: Current assets: Cash and cash

equivalents ......................

526,766 381,690 830,922 61,376

582,358

589,752

43,721 Trade accounts receivable,

less allowance for doubtful accounts .............

1,026,214 1,777,451 1,540,540 113,791

1,441,989

1,503,109

111,432 Other current assets ..... 215,499 242,605 244,602 18,067 181,508 248,755 18,441 Total current assets ................. 1,814,631 2,440,784 2,666,990 196,996 2,245,627 2,369,484 175,660 Property and equipment, net(6) ....................................

9,092,168 9,266,017 9,386,720 693,346

9,275,113

9,396,943

696,637

Other non-current assets ......... 1,891,976 1,437,979 1,491,064 110,137 1,589,688 1,767,464 131,030 Total assets ............................. 12,798,775 13,144,780 13,544,774 1,000,478 13,110,428 13,533,891 1,003,328

Total current liabilities(7) ........... 1,148,563 1,934,793 2,659,011 196,407 1,992,850 2,489,876 184,586 Long-term liabilities: Long-term debt.................... 4,243,958 3,884,392 4,193,673 309,764 3,915,048 4,186,541 310,367 Derivative financial

instruments ......................

38,110 20,985 404,345 29,867

126,389

313,582

23,247 Total liabilities ......................... 7,408,720 7,852,365 9,085,931 671,128 8,026,636 8,604,204 637,868 Stockholders’ equity ................ 5,390,055 5,292,415 4,458,843 329,350 5,083,792 4,929,686 365,460 Cash Flow Data:(8) Net cash provided by

operating activities .............

932,065 698,120 1,925,503 142,226

1,105,663

771,128

57,167 Net cash used in investing activities .............................

(166,544) (454,212) (783,945) (57,906)

(826,088)

(709,260)

(52,581)

Net cash used in financing activities .............................

(680,953) (346,943) (505,302) (37,324)

(27,417)

(320,639)

(23,770)

Other Financial Data: EBITDA(9)................................. 1,437,728 1,462,875 1,529,949 113,009 1,188,215 914,400 67,788 Other Operating Data: ADR(10)..................................... 1,073 1,059 1,069 79 1,060 1,070 79 REVPAR(11).............................. 661 659 647 48 655 572 42 Occupancy(12) .......................... 61.7% 62.2% 60.6% — 61.8% 53.4% —

(1) Total revenues include revenue from hotel ownership, hotel management, brand and other and Vacation Club and other. (2) Converted into U.S. dollars using an exchange rate of Ps.13.5383 per U.S. dollar on December 31, 2008 and Ps.13.4890 per U.S. dollar on

September 30, 2009. These conversions should not be construed as representations that the peso amounts actually represent such U.S. dollar amounts or could be converted into U.S. dollars at the specified rate or at all. See “Exchange Rates.”

(3) Based on the provisions of NIF B-15, “Translation of foreign currency,” effective January 1, 2008, we have the following currencies:

Currency

Country Recording Functional Reporting

Mexico (FAVC) Mexican pesos U.S. dollar Mexican pesos

United States of America U.S. dollar U.S. dollar Mexican pesos

Brazil Brazilian reais Brazilian reais Mexican pesos

Argentina Argentine pesos Argentine pesos Mexican pesos

Chile Chilean pesos Chilean pesos Mexican pesos

(4) Reflects the effect of mark-to-market losses in connection with certain of our derivative financial instruments. See “Management’s

Discussion and Analysis of Financial Condition and Results of Operations—Quantitative and Qualitative Disclosures about Market Risk—Derivative Financial Instruments.”

(5) Gain on monetary position represents (for those periods prior to December 31, 2007 stated in constant pesos) the effects of inflation, as measured by the NCPI, on our monthly net monetary assets or liabilities during the period. Starting January 1, 2008, and following the provisions of NIF B-10 “Effects of inflation,” the effects of inflation are recognized only if the cumulative inflation in the last three years exceeds 26% in the countries where we operate.

(6) Net of accumulated depreciation. (7) Current liabilities include bank loans and current portion of long-term debt and other payable and accrued liabilities. (8) As a result of NIF B-2 “Statement of Cash Flows,” effective January 1, 2008, we have included the statement of cash flows for the year

ended December 31, 2008. For prior years, we have included the statement of changes in financial position. As a result, the cash flow figures for 2008 may not be directly comparable to those presented for the prior years, which are derived from the statement of changes in financial position.

12

(9) We calculate EBITDA by adding depreciation and amortization to our consolidated operating income as determined in accordance with Mexican FRS. EBITDA is not a measure of financial performance under Mexican FRS and should not be considered as an alternative to net income as a measure of operating performance or to cash flow from operations as a measure of liquidity. The following table sets forth the reconciliation between EBITDA to operating income (loss) under Mexican FRS for each of the periods presented.

Years ended December 31, Nine months ended September 30,

2006 2007 2008 2008 2008 2009 2009 (Ps.) (Ps.) (Ps.) (US$) (Ps.) (Ps.) (US$) (Unaudited) Operating income....... 995,664 1,031,913 1,140,769 84,262 869,104 574,917 42,621 Depreciation and amortization............. 442,064 430,962 389,180 28,747 319,111 339,483 25,167 EBITDA...................... 1,437,728 1,462,875 1,529,949 113,009 1,188,215 914,400 67,788

(10) ADR or average daily rate per room, is determined by dividing total room revenues for the period indicated by total room nights sold during

such period. (11) REVPAR is calculated as ADR multiplied by the occupancy rate (equivalent to dividing total room revenues by total room nights available

for sale). (12) Occupancy is determined for a period by dividing total room nights sold during the period by total rooms available for each day during the

period.

The following table sets forth the number of our hotels by type of hotel, the number of available rooms by type of hotel, the number of our hotels by brand and the number of available rooms by brand, in each case, as of and for the years ended December 31, 2006, 2007 and 2008 and as of and for the nine months ended September 30, 2008 and 2009:

As of and for the years ended December 31,

As of and for the nine months ended

Sep 30,

2006 2007 2008 2008 2009

Number of hotels............................................................................... 94 100 108 105 110

Owned Hotels .................................................................................. 31 32 33 33 33

Managed Hotels ............................................................................. 42 47 54 51 58

Leased Hotels.................................................................................. 21 21 21 21 19

Number of available rooms .............................................................. 17,227 18,049 19,270 18,867 19,454

Owned Hotels .................................................................................. 6,675 6,807 6,933 6,933 6,933

Managed Hotels ............................................................................. 7,310 8,000 8,892 8,489 9,378

Leased Hotels.................................................................................. 3,242 3,242 3,445 3,445 3,143

Number of hotels............................................................................... 94 100 108 105 110

Live Aqua ....................................................................................... — — 1 1 1

Fiesta Americana(1) ........................................................................ 20 20 19 19 18

Fiesta Americana Vacation Club...................................................... 3 3 4 4 4

Fiesta Inn......................................................................................... 53 57 59 57 60

One Hotels ...................................................................................... 1 4 8 7 10

Caesar Park..................................................................................... 5 4 5 5 5

Caesar Business ............................................................................ 8 8 8 8 8

Other brands.................................................................................... 4 4 4 4 4

Number of available rooms .............................................................. 17,227 18,049 19,270 18,867 19,454

Live Aqua ........................................................................................ — — 371 371 371

Fiesta Americana(1) ........................................................................ 5,198 5,406 5,366 5,366 5,213

Fiesta Americana Vacation Club...................................................... 637 637 677 677 677

Fiesta Inn......................................................................................... 7,860 8,390 8,662 8,385 8,747

One Hotels ...................................................................................... 126 510 1,014 888 1,266

Caesar Park..................................................................................... 979 679 753 753 753

Caesar Business ............................................................................. 1,535 1,535 1,535 1,535 1,535

Other brands.................................................................................... 892 892 892 892 892 (1) Includes hotels operated under the Fiesta Americana Grand brand.

13

RISK FACTORS

You should review and consider carefully the following risk factors, as well as all the other information presented in this offering memorandum, before purchasing the Notes. The risks and uncertainties described below are not the only ones that we face. Additional risks and uncertainties that we are not aware of or that we currently think are immaterial, or that in our judgment do not reach the level of materiality that merits disclosure may also impair our business operations. Any of the following risks, if they were to occur, could materially and adversely affect our business, results of operations, prospects and financial condition. In that event, the market price and liquidity of the Notes could decline and you could lose all or part of your investment. This offering memorandum also contains forward-looking statements that involve risks and uncertainties. Our actual results could differ materially from those anticipated in these forward-looking statements as a result of certain factors, including the following risks faced by us and the risks described elsewhere in this offering memorandum.

Risks Relating to Our Hotel and Vacation Club Business

The current disruption in the global credit markets and its effects on the global and Mexican economies could adversely affect our business.

Substantial volatility in the global capital markets, unavailability of financing in the global capital markets at reasonable rates and widely documented commercial credit market disruptions since the fall of 2008 have had a significant negative impact on financial markets, as well as the global and domestic economies. The effects of these disruptions are widespread and difficult to quantify, and it is impossible to predict when the global financial markets will improve. There is now general consensus among economists that the economies in which we operate and much of the rest of the world were and may continue to be in a recession, and we are experiencing reduced demand for our hotel rooms and vacation club units. Substantial increases in air and ground travel costs, and decreases in airline capacity arising primarily from reduced flights, have also reduced demand for our hotel rooms and vacation club units. Accordingly, our financial results have been impacted by the economic slowdown and both our future financial results and growth could be further harmed if current global economic conditions persist or worsen, resulting in wide-ranging, adverse and prolonged effects on general business conditions, and material and adverse effects on our results of operations and liquidity. The effects of the current economic situation are extremely difficult to forecast and mitigate.

A high percentage of the hotel rooms we manage are in luxury hotels or in hotels in locations which have been particularly impacted by the current economic downturn, which has had and may continue to have a significant adverse effect on our results of operations and financial condition.