Embed Size (px)

Citation preview

26th Annual Health Sciences Tax ConferenceThe role of technology in today’s tax department

December 7, 2016

Page 2 The role of technology in today’s tax department

Disclaimer

► EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young LLP is a client-serving member firm of Ernst & Young Global Limited operating in the US.

► This presentation is © 2016 Ernst & Young LLP. All rights reserved. No part of this document may be reproduced, transmitted or otherwise distributed in any form or by any means, electronic or mechanical, including by photocopying, facsimile transmission, recording, rekeying, or using any information storage and retrieval system, without written permission from Ernst & Young LLP. Any reproduction, transmission or distribution of this form or any of the material herein is prohibited and is in violation of US and international law. Ernst & Young LLP expressly disclaims any liability in connection with use of this presentation or its contents by any third party.

► Views expressed in this presentation are those of the speakers and do not necessarily represent the views of Ernst & Young LLP.

► This presentation is provided solely for the purpose of enhancing knowledge on tax matters. It does not provide tax advice to any taxpayer because it does not take into account any specific taxpayer’s facts and circumstances.

► These slides are for educational purposes only and are not intended, and should not be relied upon, as accounting advice.

Page 3 The role of technology in today’s tax department

Presenters

► Simon KnightbridgePfizerLondon, UK

► Lisa BedardWaters CorporationMilford, MA

► Hadley LeachErnst & Young LLPNew York, [email protected]+1 617 585 3438

► Kyle HarkraderErnst & Young LLPRichmond, [email protected]+1 202 257 9105

Page 4 The role of technology in today’s tax department

Agenda

► What’s driving technology investments in the tax department?► Disruptive megatrends and impact on the life sciences sector ► Rapidly changing tax legislation and regulatory environment

► What are some of the emerging technologies and approaches to enable today’s tax department?► Assessing automation opportunities► Intelligent automation with emphasis on robotic process

automation (RPA)► Content management + data + analytics

► Q&A

Page 5 The role of technology in today’s tax department

► What is driving technology investments in the tax department?

► Are there specific goals or expectations that you’ve set?

► How have you gained sponsorship within your company?

Page 6 The role of technology in today’s tax department

Disruptive megatrends and impact on the life sciences sector

Page 7 The role of technology in today’s tax department

Guiding principle

Skate to where the puck is going to be, not where it has been.

— Wayne Gretzky

Page 8 The role of technology in today’s tax department

The forces driving our future: megatrends

Age of discovery Colonialism Bretton Woods trade liberalization East Asian newly industrialized countries China/India/Brazil Latin America/Africa

Industrial Revolution Information technology Mainframes PCs Online (web) Social Mobile Smart Internet of Things

(IoT) Virtual reality Intelligent automation

Demographics is destiny Post-WWII “baby boom” China “One Child” Policy Millennial Workforce Urbanization Aging West Global migration Young India/Africa

3Three primary forces …► Independent variables► Long-term, multiple waves► Interact and catalyze each other

Demographics

Technology

Globalization

… are driving multiple megatrends► Cohesive narratives with significant interplay ► Driven by interaction between the next waves of

technology, globalization and demographics

1. Industry redefinedIs every industry now your industry?

2. The future of smartWhat intelligence will we need to create a smart future?

3. The future of workWhen machines become workers, what is the human role?

4. Behavioral revolutionHow will individual behavior impact our collective future?

5. Empowered customerHow will you change buyersinto stakeholders?

6. Urban worldIn a fast-changing world, can cities be built with long-term perspective?

7. Health reimaginedWith growing health needs, is digital the best medicine?

8. Resourceful planetCan innovation make the planet resource-rich instead of resource-scarce?

Page 9 The role of technology in today’s tax department

M&A continues to drive growth Life sciences M&A value reaches US$226b in 2016, likely to surpass record-setting M&A total in 2014

Source: Thomson One

0

50

100

150

200

250

300

350

2007 2008 2009 2010 2011 2012 2013 2014 2015 Sep-16

US

$b

Big pharma Big biotech Specialty pharma Generics Medtech

Page 10 The role of technology in today’s tax department

Legislative and regulatory changes heighten scrutiny

► Country-by-country (CbC) reporting ► Requires information about jurisdictional

allocation of profits, revenues, intercompany pricing, employees and assets. Data often needs to be gathered from multiple systems to comply.

► Final Section 385 Regulations ► Focus on substantiation of

intercompany debt and evidence of creditor/debtor relationship with significant documentation requirements.

► Digital tax administration► Tax authorities are increasingly relying

on digital tax data gathering and analytics to facilitate real-time or near-real-time collection and assessment of taxpayer data.

Country-by-country (CbC)

reporting

Digital Tax Administration

Final Section 385

Regulations

Rise in enforcement

and audit activity

Influences

Impact

Page 11 The role of technology in today’s tax department

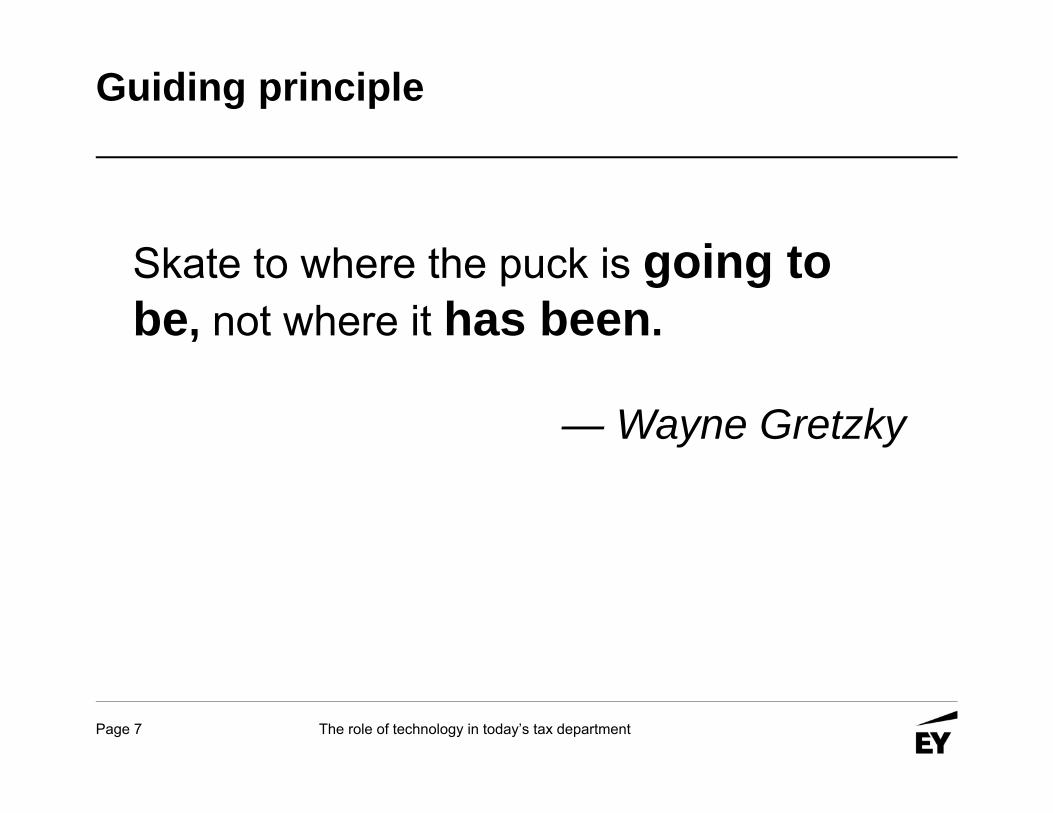

Digital tax administration life cycle

Level 1 Level 2

Para

digm

shi

ft

Level 3 Level 4

Dis

rupt

ive

Level 5“E-file” “E-accounting” “E-match” “E-audit” “E-assess”Use of standardized electronic form for filing tax returns required or optional. Other income data (e.g., payroll, financial) filed electronically and matched annually.

Submit accounting or other source data to support filings (e.g., invoices, trial balances) in a defined electronic format at a defined frequency; additions and changes at this level occur frequently.

Submit additional accounting and source data; government accesses additional data (bank statements), begins to match data across tax types and potentially across taxpayers and jurisdictions in real time.

L2 data is analyzed by government entities and cross-checked to filings in realtime to map the geographic economic ecosystem. Taxpayers receiveelectronic audit assessments with limited time to respond.

Government entities use submitted data to assess tax without the need for tax forms. Taxpayers have a limited time to audit government-calculated tax.

Note: Not all governments collect the same information or treat it the same under this model. Further, the move to digitization is not necessarily linear.

Page 12 The role of technology in today’s tax department

Digital tax administration evolutionContinuous change

Note: Darker-shaded countries are further along with the implementation of the respective digital tax regimes.

Investing in advanced analytics capabilities,IT and talent

Targeted digital submissions with audit capabilities in tax invoices, auditing, etc.

Strong focus on value-added tax (VAT) digitization; growing use of SAF-T or similar standards; data submission upon audit commencement

Strong focus on near real-time submission of financial/accounting data

Widespread: Common reporting standards, BEPS and country-by-country reporting, exchange of information

Page 13 The role of technology in today’s tax department

Emerging technologies utilized to address challenges for today’s tax function

Page 14 The role of technology in today’s tax department

Drivers for investments in technology to support Tax

The future(trends)

Emerging technologies► Intelligent automation► Content + data + analytics

The present(challenges)

Page 15 The role of technology in today’s tax department

Assessing opportunities for automation

► Identify level of effort and degree of manual/iterative effort required for each tax process. Where is the pain?

► Evaluate if resources are spending time on high-value-added tasks such as review and analysis vs data collection, reconciliation and “wrangling”

► Perform analysis to identify whether existing technology can be expanded to support automation or if supplementary technology is required

Low

Hig

hM

oder

ate

Low Moderate High

[Process]

[Process]

[Process]

[Process]

[Process]

Number of Hours

Manual/ repetitive

L1 processes prioritized

[Process]Highest priority

Page 16 The role of technology in today’s tax department

The big picture of intelligent automation

Process automation enables organizations to automate existing high volume and/or complex, multi-step data handling actions and workflows to run autonomously without manpower. It captures and interprets existing applications, manipulates data, triggers responses and communicates with other digital systems.

Definition: robotic process automation is the application of a cost-effective software that mimics human action and connects multiple fragmented systems together through automation without changing the current enterprise IT landscape.

Pattern-based machine learning

Statistical modeling

Optimized processthrough automation

Improved workflow

Cognitive intelligence

(CI)Semi-

cognitiveRobotic process

automation(RPA)

Structured data

interaction

Incr

emen

tal

valu

e

Mimics human actions

Augments human intelligence

Mimics human intelligence

Past1990s–2000s

Present Future2015–20 2020+

Page 17 The role of technology in today’s tax department

A quick glance at how robotics actually works

RPA software emulating human interaction with systems:► A quick video of a proof of concept using an RPA

software, Blue Prism, where the bot assists in the tax provision process

► The professional used to take 15 to 20 minutes to do what the bot does in 3 to 5 minutes!

► Link to Video

Page 18 The role of technology in today’s tax department

RPA driving enterprise value in transformation

Sits alongside existing infrastructure, governed and controlled by IT

Emulates human execution of repetitive processes via existing user interfaces

Robots are a virtual workforcecontrolled by the business operations teams

4 to 6 X

faster

24/7

<1 Yr.

<1 Yr.

Cos

ts

Significant increase in accuracy with on-time delivery

Increased capacity to handle significantly higher transaction volume

Software robots work with existing IT architecture (multiple robotics providers to select from)

Automated solution works 24/7, driving responsiveness

~$7k–$10kannual license costs per bot vs professional salary cost

Potential payback within a year

Fully maintained audit trail for compliance

Enhanced processing speed compared to human beings

Robotic process

automation

Page 19 The role of technology in today’s tax department

Content management — a tax platformDefining the technology

SharePoint as a tax platform is an approach to improve the efficiency and effectiveness of the tax function centered around connectivity, innovation and day-to-day operations.

Function Description

Portal ► Access to secure areas with links to needed resources

Document management

► Centralized documents► Version control, access control► Rapid search capability

Processmanagement

► Task tracking► Transparency brings efficiency and lowers risk► Email notification prompting action

Collaboration► Collection and distribution of information with internal and external stakeholders — investors,

accounting firms, investment managers, controllers, deal teams, portfolio companies, administrators

Data management► Tax master and transactional data, centralized tax facts and business rules leveraged by

applications through data governance, security, standardization, mapping and policies► Data robotics integration

Reporting► Centralized, standardized and simplified access to critical data► Predictive analytics ► Visualizations

Page 20 The role of technology in today’s tax department

SharePoint — a tax platformA smartphone analogy to describe a vision

Core functionality► Document management► Workflow► Reporting/dashboard► SearchHighly leverageable platform► Built on a technology framework (SharePoint, OneSource)► Integrates with other vendor technologies► Additional apps take advantage of core functionality► Apps use the same data sources (e.g., entity listing, accounts,

financial data)► Apps talk to each other (e.g., planning memos into compliance

process)Highly modular ► Document management► Compliance status tracker (i.e., workflow)► State apportionment management► Legal entity tracker► Data/reporting/analytics/visualization

12:38

State Appnt Entities

Workflow Reports Search

Capital Calc Planning

Audit Manager Operations

Transfer Pricing FIN 48

TP

Tax Accounting Research

Training

Documents

Collaborate

Tax Policies

Support

Operations

K-1

Tax Accounting

Tax News Tax Alerts

Compliance

Issues

Page 21 The role of technology in today’s tax department

Changing project preferences Rapid solution delivery vs historic approach

His

toric

tran

sfor

mat

ion

appr

oach

Rap

id s

olut

ion

deliv

ery

Time

Time

Attributes► High investment threshold► End-to-end thinking► Significant IT expertise► Inertia to change

Attributes► Low investment threshold► Solutions focused, within a strategic vision► Lower IT expertise► Nimble, refine plan over time for emerging needs► Faster value realization

Page 22 The role of technology in today’s tax department

Analytics for TaxNot all analytics are created equal

Ad hoc queries/standard reports

4th quartile capability

Alerts/query/drill down

2nd/3rd quartile capability

Optimization/predictive modeling/

simulation

1st quartile capability

Audit analytics capabilities Industry-leading analytics capabilities

Hindsight Insight Foresight

Page 23 The role of technology in today’s tax department

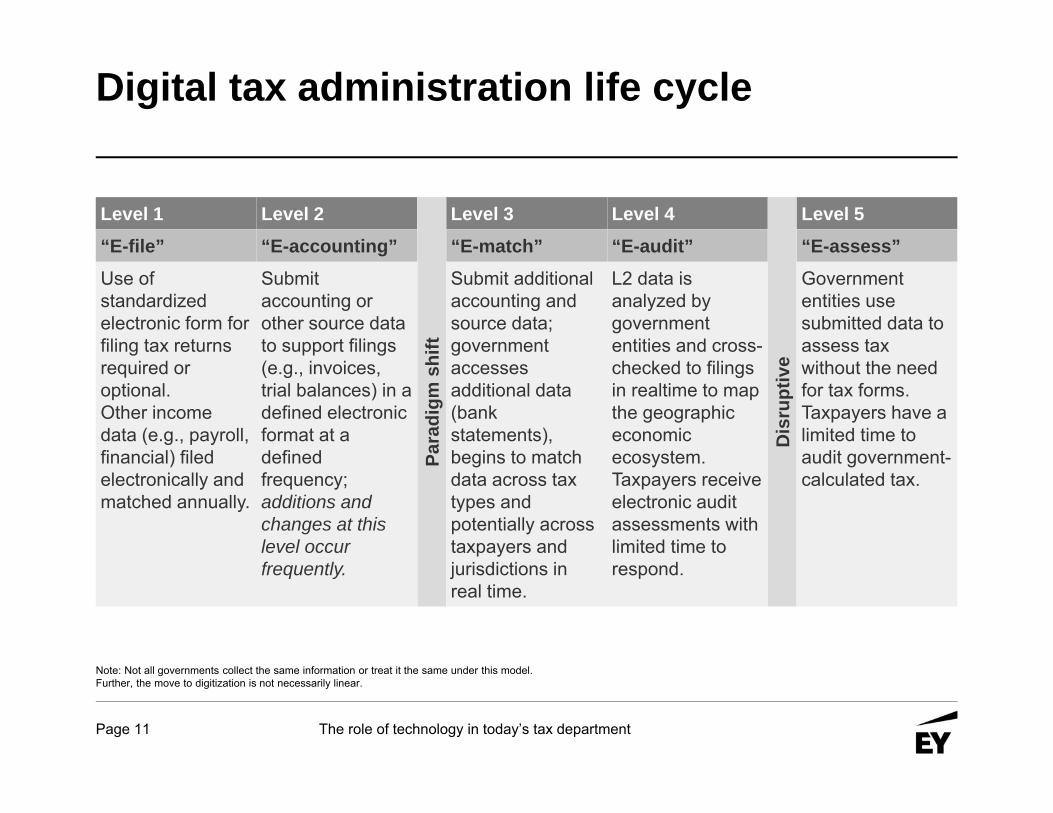

SAP

HFMHTP

JDE

ONESOURCE

Analytics engineData sources Dashboards & visualizations

Finance, IT, Controllers

Stakeholders

Tax Department

► Many analytics companies in the marketplace today are dominated by data warehousing and enterprise dashboard/reporting solutions.

► Most clients still struggle to embed analytics into operational decisions in a systematic and repeatable way, oftentimes resulting in clients not realizing the full value of analytics.

► Clients are improving performance, managing risk and driving the right decisions by utilizing analytics reports built with a view toward meeting key business needs and objectives.

CORPTAXLONGV

The key to success in utilizing analytics is to understand source data and business needs

Page 24 The role of technology in today’s tax department

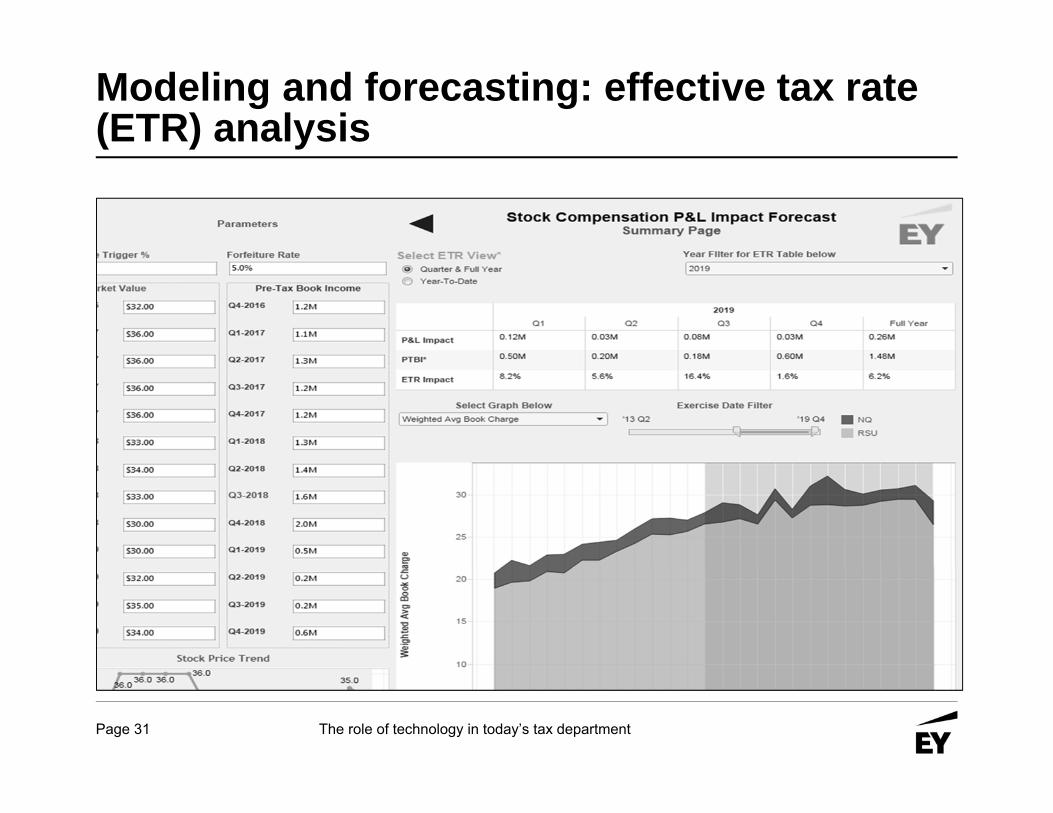

Modeling and forecasting► Effective tax rate (ETR) modeling► Stock option ETR impacts

Time savings► Year-over-year reviews► Identification of outliers within a computation► Identification of missing or inaccurate data

How analytics and visualizations empower the tax function

Risk mitigation► Status monitoring► Complete and accurate data ► Identification and analysis of substantive issues

1

2

3

Page 25 The role of technology in today’s tax department

Risk mitigation: gaining visibility over VAT compliance

Page 26 The role of technology in today’s tax department

Risk mitigation: gaining visibility over global tax controversy

Page 27 The role of technology in today’s tax department

Risk mitigation: analyzing country-by-country reporting

Page 28 The role of technology in today’s tax department

Risk mitigation: tracking debt balances for Section 385 compliance

Page 29 The role of technology in today’s tax department

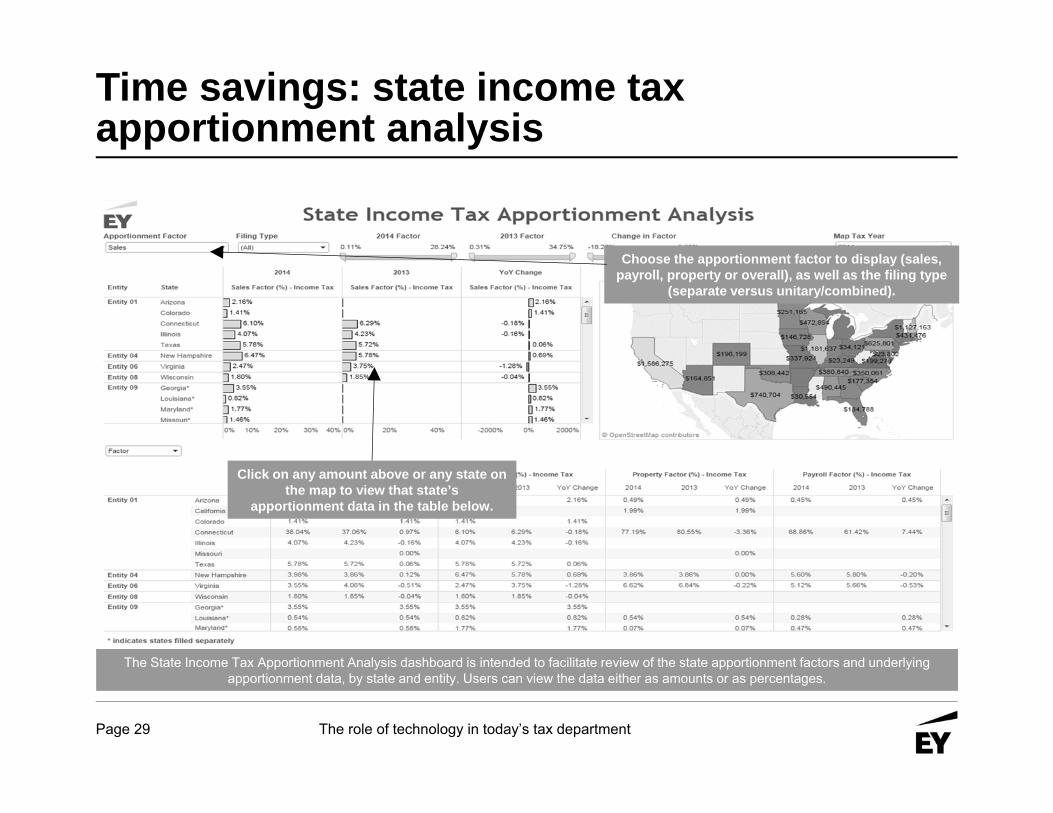

Time savings: state income tax apportionment analysis

Click on any amount above or any state on the map to view that state’s

apportionment data in the table below.

Choose the apportionment factor to display (sales, payroll, property or overall), as well as the filing type

(separate versus unitary/combined).

The State Income Tax Apportionment Analysis dashboard is intended to facilitate review of the state apportionment factors and underlying apportionment data, by state and entity. Users can view the data either as amounts or as percentages.

Page 30 The role of technology in today’s tax department

Time savings: tracking earnings and profits (E&P)

Select a country to display

country/entity detail below.

Page 31 The role of technology in today’s tax department

Modeling and forecasting: effective tax rate (ETR) analysis

Page 32 The role of technology in today’s tax department

Data analytics best practices

► Data visualizations are used to empower your audience by providing a high-level overview of information. The key is to understand your audience and know what story they are looking to tell from compiling and analyzing the data.

► Key items to consider:► Keep visualizations and dashboards simple and digestible► Choose the right visual for your purpose:

► Dashboards allow for filtering of different categories based on underlying data source.

► Line charts track changes or trends over time and show the relationship between two or more variables.

► Bar charts are used to compare quantities of different categories.► Pie charts are used to compare parts of a whole.

Page 33 The role of technology in today’s tax department

Questions?

EY | Assurance | Tax | Transactions | AdvisoryAbout EYEY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

Ernst & Young LLP is a client-serving member firm of Ernst & Young Global Limited operating in the US.

© 2016 Ernst & Young LLP.All Rights Reserved.

1608-2011220

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax or other professional advice. Please refer to your advisors for specific advice.