Embed Size (px)

Citation preview

SMM Press Conference - Shipbuilding

Martin Stopford 1

CLARKSON RESEARCH SERVICES LTD

SMM Advance Press Conference

23th May 2012

World ShipbuildingDr Martin Stopford

Managing Director, Clarkson Research

CLARKSON RESEARCH SERVICES LTD

1. The Shipping Market2. Shipyard Capacity & the Fleet3. Four Future Challenges4. Conclusions

How do you play this hand?

Is shipping more than just �the worlds biggest crap

game?�

SMM Press Conference - Shipbuilding

Martin Stopford 2

CLARKSON RESEARCH SERVICES LTD

2. Shipping Bankers

Shall we say 30 cents in the $, Sir?

1. Ship owners

What shall I

buy now?

4. Investment Funds

Time to drop your

pants, boys

3. Shipbuilders

We just build ships.. so ORDER

SOME!

What about our $1.2

billion loan?

CLARKSON RESEARCH SERVICES LTD

0

10

20

30

40

50

60

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Cla

rkse

a In

dex

$000

/day

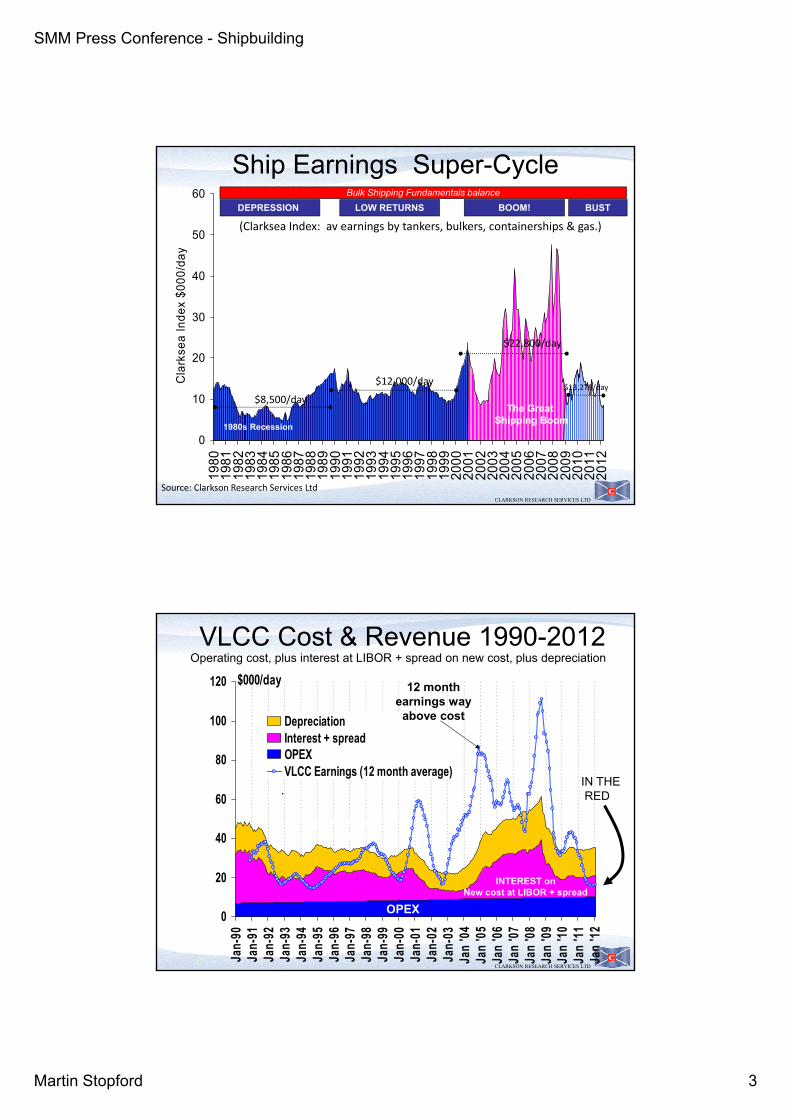

(Clarksea Index: av earnings by tankers, bulkers, containerships & gas.)

Source: Clarkson Research Services Ltd

The Great Shipping Boom

1980s Recession

$8,500/day

$12,000/day

$22,800/day

DEPRESSION LOW RETURNS BOOM!Bulk Shipping Fundamentals balance

BUST

$13,278/day

Ship Earnings Super-Cycle

SMM Press Conference - Shipbuilding

Martin Stopford 3

CLARKSON RESEARCH SERVICES LTD

0

10

20

30

40

50

6019

8019

8119

8219

8319

8419

8519

8619

8719

8819

8919

9019

9119

9219

9319

9419

9519

9619

9719

9819

9920

0020

0120

0220

0320

0420

0520

0620

0720

0820

0920

1020

1120

12

Cla

rkse

a In

dex

$000

/day

(Clarksea Index: av earnings by tankers, bulkers, containerships & gas.)

Source: Clarkson Research Services Ltd

The Great Shipping Boom

1980s Recession

$8,500/day

$12,000/day

$22,800/day

DEPRESSION LOW RETURNS BOOM!Bulk Shipping Fundamentals balance

BUST

$13,278/day

Ship Earnings Super-Cycle

CLARKSON RESEARCH SERVICES LTD

VLCC Cost & Revenue 1990-2012

0

20

40

60

80

100

120

Jan-

90Ja

n-91

Jan-

92Ja

n-93

Jan-

94Ja

n-95

Jan-

96Ja

n-97

Jan-

98Ja

n-99

Jan-

00Ja

n-01

Jan-

02Ja

n-03

Jan

'04Ja

n '05

Jan

'06Ja

n '07

Jan

'08Ja

n '09

Jan

'10Ja

n '11

Jan

'12

$000/day

DepreciationInterest + spreadOPEXVLCC Earnings (12 month average)

Operating cost, plus interest at LIBOR + spread on new cost, plus depreciation

INTEREST on New cost at LIBOR + spread

Depreciation �over 20 yrs

12 month earnings way

above cost

OPEX

IN THERED

SMM Press Conference - Shipbuilding

Martin Stopford 4

CLARKSON RESEARCH SERVICES LTD

-10%-8%-6%-4%-2%0%2%4%6%8%

10%12%14%

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

Wold GDP & Sea Trade GrowthWorld GDP (red line) and sea trade (blue line)

Crisis 11973

1st Oil Crisis

2001Dot.com

crisis

Crisis 21979

2nd OilCrisis

1991 Financial

Crisis

1997Asia Crisis

Crisis 62007

Credit Crisis

% change Oil Crisis Credit Crisis

CLARKSON RESEARCH SERVICES LTD

0102030405060708090

100110120130140150

1965

1970

1975

1980

1985

1990

1995

2000

2005

2010

2015

2020

2025

2030

2035

Oil price (2009 $)450 ScenarioNew PoliciesCurrent Policies!$100+ oil prices

change the economic framework for ship design

!Today�s fleet is partially obsolete

!But responding to this change is tricky

$2009/bbl

Figure 2: The IEA Oil price scenarios 2010

450$92/bl

New$118/bl

Current$140/bl

Oil Price 1965 to 2035

SMM Press Conference - Shipbuilding

Martin Stopford 5

CLARKSON RESEARCH SERVICES LTD

0

100

200

300

400

500

600

700

800

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

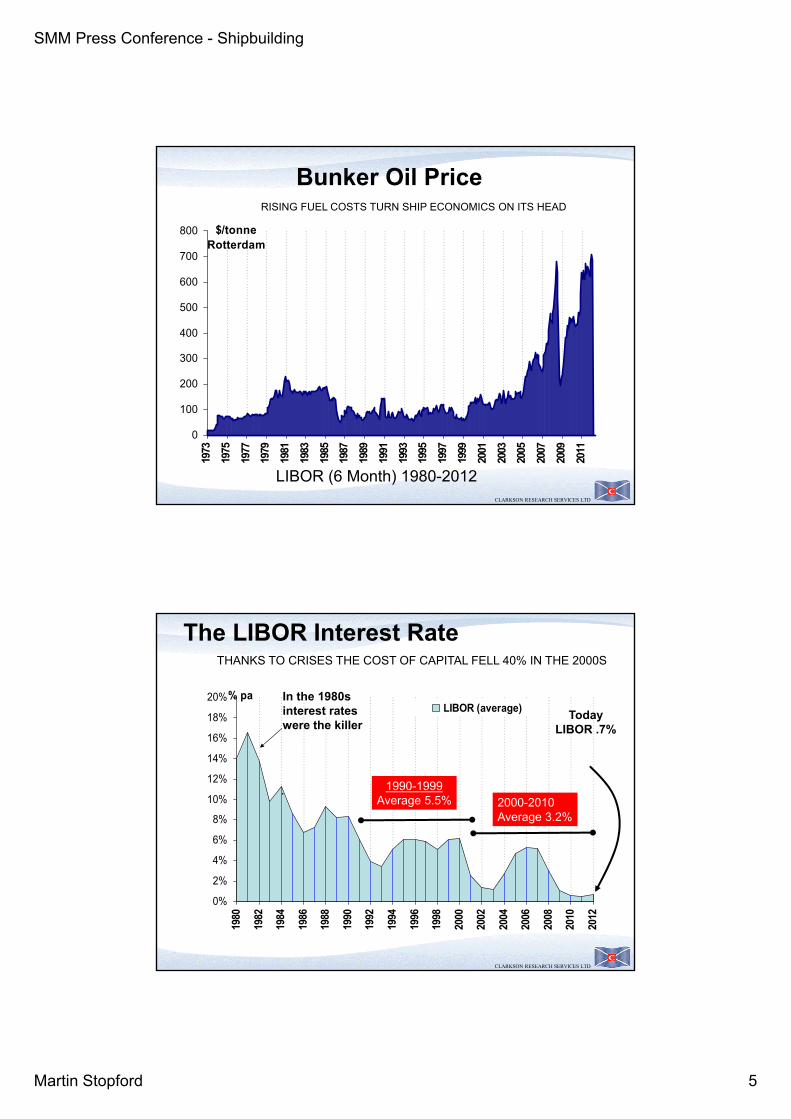

$/tonne Rotterdam

RISING FUEL COSTS TURN SHIP ECONOMICS ON ITS HEAD

LIBOR (6 Month) 1980-2012

Bunker Oil Price

CLARKSON RESEARCH SERVICES LTD

The LIBOR Interest Rate

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

% paLIBOR (average)

1990-1999Average 5.5% 2000-2010

Average 3.2%

THANKS TO CRISES THE COST OF CAPITAL FELL 40% IN THE 2000S

In the 1980s interest rates were the killer

Today LIBOR .7%

SMM Press Conference - Shipbuilding

Martin Stopford 6

CLARKSON RESEARCH SERVICES LTD

Bulk Trade Trends

-5%

0%

5%

10%

15%19

9019

9119

9219

9319

9419

9519

9619

9719

9819

9920

0020

0120

0220

0320

0420

0520

0620

0720

0820

0920

1020

11

Major Bulks Crude Oil Imports% growth

In the 2000s dry trade grew faster and oil trade slower

CLARKSON RESEARCH SERVICES LTD

Bulk Trade Trends

-5%

0%

5%

10%

15%

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

Major Bulks Crude Oil Imports% growth

In the 2000s dry trade grew faster and oil trade slower

SMM Press Conference - Shipbuilding

Martin Stopford 7

CLARKSON RESEARCH SERVICES LTD

Future Trade Scenarios

0123456789

1011121314151617

1950

1955

1960

1965

1970

1975

1980

1985

1990

1995

2000

2005

2010

2015

2020

seab

orne

impo

rts b

illio

n to

nne s

China ImportsWorld less China7% i

Figure 3 World & China�s seaborne imports with scenarios for future growth

Low Case1% scenario

Base Case3-4%

High case7%

4% pa trend1991-2001

Globalization has a way to go, which is good, but A) The next phase will be differentB) The Credit Crisis is not over yet

CLARKSON RESEARCH SERVICES LTD

The shipyards are Winding down from the

biggest boom ever

8 Wheel Shipyard � armed and dangerous!

SMM Press Conference - Shipbuilding

Martin Stopford 8

CLARKSON RESEARCH SERVICES LTD

Investment falls to $90 billion in 2011

1. Investment in new ships was $90 billion in 2011

8 13 7 5 13 11 10 21 21 2355

39 357 15 65 6

3 75 3 7

11 13 14

25

105

68

13

34

1012

0 13 4 3

212 9

9

5

1

0

1

109 35 6

11 7 4

2221 28

28

47

17

1

8

1912 1417 14

167 9

1321

33

40

61

42

7

27 43

020406080

100120140160180200220240260280300

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

Bill $ Orders

20

25

30

35

40

45

50

55

60

65

3,600 TEU $MM

Others

ContainerLPG

LNG

Bulk

TankersNew 3600 TEU $MM

Investment in new ships & newbuilding prices

Investment In New Ships 1996-2011

Offshore

Container

BulkerTanker

CruiseGas

CLARKSON RESEARCH SERVICES LTD

World Shipbuilding 35 Year Cycle

0

20

40

60

80

100

1902 1912 1922 1932 1942 1952 1962 1972 1982 1992 2002 2012

Milli

on G

T De

liver

ies

The last shipbuilding peak was in 1975 when output

reached 36 million GT

Source Maritime Economics 3rd Ed Martin Stopford (2009)

Period 11886-1919

Period 21920-1940

Period 31945-1973

Period 41973-1987

Rapid growth of sea trade driven

forward by a series of cycles

Over capacity & trade slump

triggered by 1930s depression

Shortages of yard capacity at start & post

war trade boom

Yard overcapacity and trade slump

Period 51988-2010

Trade growth & yard expansion

Peak 47 m GRT

Peak 820 m GRT

Peak 1036 m GT

Peak1

Peak2

Peak3 Peak

5Peak

6

Peak7

Peak9

Peak11

3 Mini-cycles

Peak 12

2011New record

100.9 million GT

SMM Press Conference - Shipbuilding

Martin Stopford 9

CLARKSON RESEARCH SERVICES LTD

Shipbuilding Deliveries by Country 2011

18.415.8

8.90.40.30.60.50.30.20.30.6

0 5 10 15 20 25

China S. Korea

JapanGermany

ItalyPhilippines

NorwayTurkeySpain

NetherlandsOthers

Million CGT Output 2011

Source: Clarkson Research

212 yards

24 yards

51 yards

What is CGT?CGT is the Gross Tonnage (GT) of the ship weighted to reflect its

work content per GT. For example the weight for a

containership might be 1.0 and the weight for a big tanker 0.25)

CLARKSON RESEARCH SERVICES LTD

Orderbook in 2011 - Falling

20%24% 25%

33%

47%51%

41%

30%

21%

0%

10%

20%

30%

40%

50%

60%

2004

2005

2006

2007

2008

2009

2010

2011

2012

% fl

eet

Orderbook % Fleet By Ship Type (Dwt)

Orderbook % Fleet

SMM Press Conference - Shipbuilding

Martin Stopford 10

CLARKSON RESEARCH SERVICES LTD

World Shipbuilding Capacity 2011Shows the CGT output by ship type

World Shipbuilding Production by Country and Ship TypeGrand TotalOtherGasContainershipTankerBulkerCountry

8.7

1.9

0.0

0.0

0.1

0.0

0.3

0.4

0.0

1.1

1.8

3.0

M CGT

0.30.00.20.00.1Romania

19.20.20.93.112.0China

16.01.04.84.04.4South Korea

9.00.30.42.05.2Japan

0.70.00.00.00.7Philippines

0.40.00.00.00.0Italy

M CGT

Total

Other

Turkey

Vietnam

Taiwan

Germany

22.9

0.1

0.0

0.2

0.1

0.0

M CGT

9.6

0.2

0.2

0.0

0.0

0.0

M CGT

6.7

0.1

0.1

0.0

0.2

0.0

M CGT

1.5

0.0

0.0

0.0

0.0

0.0

M CGT

49.5

2.3

0.3

0.4

0.4

0.4

Grand TotalOtherGasContainershipTankerBulkerCountry

8.7

1.9

0.0

0.0

0.1

0.0

0.3

0.4

0.0

1.1

1.8

3.0

M CGT

0.30.00.20.00.1Romania

19.20.20.93.112.0China

16.01.04.84.04.4South Korea

9.00.30.42.05.2Japan

0.70.00.00.00.7Philippines

0.40.00.00.00.0Italy

M CGT

Total

Other

Turkey

Vietnam

Taiwan

Germany

22.9

0.1

0.0

0.2

0.1

0.0

M CGT

9.6

0.2

0.2

0.0

0.0

0.0

M CGT

6.7

0.1

0.1

0.0

0.2

0.0

M CGT

1.5

0.0

0.0

0.0

0.0

0.0

M CGT

49.5

2.3

0.3

0.4

0.4

0.4

Indicates market leader for each ship type

CLARKSON RESEARCH SERVICES LTD

32%25%

24%

19%

18%

17%

9%

9%

8%

8%

7%

5%

5%

2%

0%

0%

0% 10% 20% 30% 40%

BulkersOffshore

ContainerLNG

Tankers >10KMPP

ChemicalLPG

Ro-RoPCC

Other TankersTankers<10K

Other cargoGen cargo

CombosReefers

Orderbook % Fleet

Merchant Fleet Orderbook Ranked by % FleetTotal orderbook 344 m dwt and average is 23% of fleet

SMM Press Conference - Shipbuilding

Martin Stopford 11

CLARKSON RESEARCH SERVICES LTD

0

20

40

60

80

100

120

140

1967 1972 1977 1982 1987 1992 1997 2002 2007 2012

$ millionVLCC Suezmax Aframax TankerProducts Capesize Panamax Bulk30,000 dwt bulker 6700 TEU

Source: Compiled from several sources including Fearnleys, CRSL

Shipbuilding Prices Falling

Figure 7: World prices for new ships 1967 to 2011

Under pressure

CLARKSON RESEARCH SERVICES LTD

World Merchant Fleet Growing at 9% pa

0100200300400500600700800900

100011001200130014001500

1978

1981

1984

1987

1990

1993

1996

1999

2002

2005

2008

2011

wor

ld fl

eet m

dw

t

-4%

-2%

0%

2%

4%

6%

8%

10%

12%OtherCombosTankers% pa

1980s recession fleet falls

fleet up 8.6% pa in

2011

Flee

t gro

wth

% p

a

Figure 9: Merchant fleet (bars) and growth per annum (line)

The zero growth line

SMM Press Conference - Shipbuilding

Martin Stopford 12

CLARKSON RESEARCH SERVICES LTD

� So what about the future?

� We need to take the cycle �one step at a time�.

� It�s not just about the market, there are four CHALLENGES we need to think about!!

I feel very nervous

CLARKSON RESEARCH SERVICES LTD

Regional imports 1950-2010

0.00.51.01.52.02.53.03.54.04.55.0

1952

1957

1962

1967

1972

1977

1982

1987

1992

1997

2002

2007

Billi

on to

ns o

f im

ports

� Asia started to grow in about 1975

� Chinese trade picked up in the 1990s

� Non OECD overtook OECD in 2008

� New world order developing

7. Challenge 1: The Future of Globalization

Oecd, 589

Non Oecd, 458

Fleet Ownership Non OECD

OECD

SMM Press Conference - Shipbuilding

Martin Stopford 13

CLARKSON RESEARCH SERVICES LTD

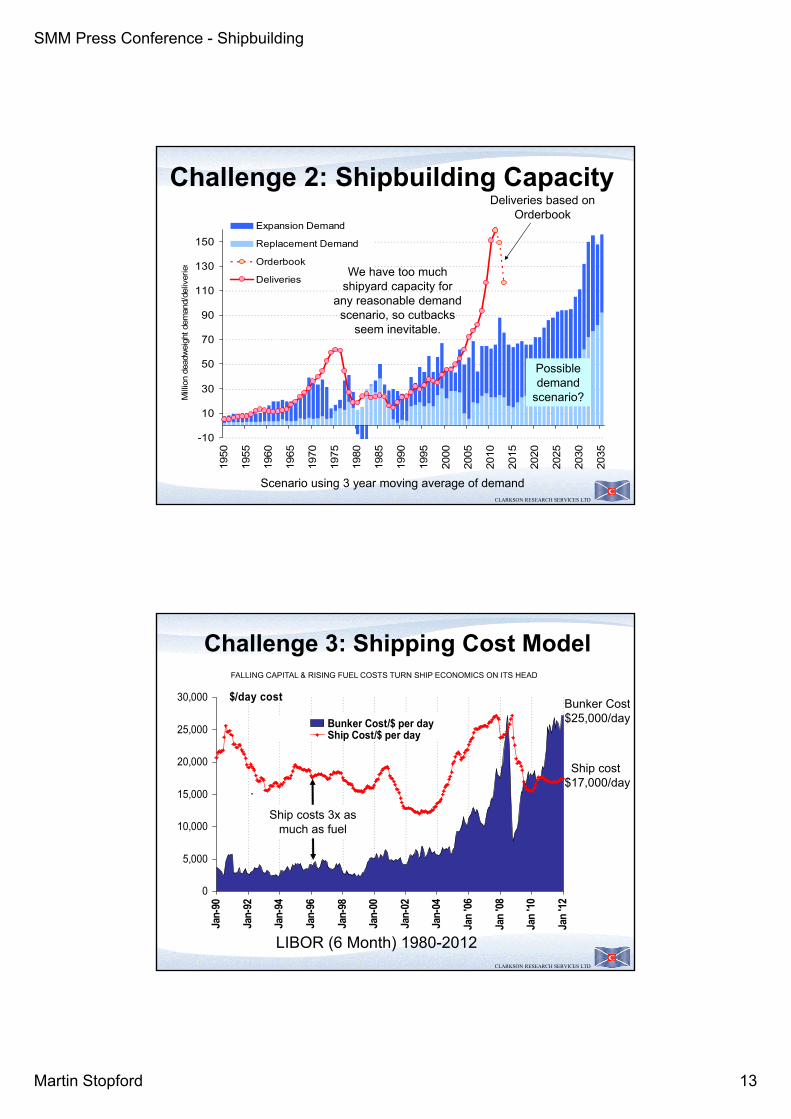

Challenge 2: Shipbuilding Capacity

Scenario using 3 year moving average of demand

-10

10

30

50

70

90

110

130

150

1950

1955

1960

1965

1970

1975

1980

1985

1990

1995

2000

2005

2010

2015

2020

2025

2030

2035

Mill

ion

dead

wei

ght d

eman

d/de

liver

ies

Expansion Demand

Replacement Demand

Orderbook

Deliveries

Deliveries based on Orderbook

Possible demand

scenario?

We have too much shipyard capacity for

any reasonable demand scenario, so cutbacks

seem inevitable.

CLARKSON RESEARCH SERVICES LTD

0

5,000

10,000

15,000

20,000

25,000

30,000

Jan-

90

Jan-

92

Jan-

94

Jan-

96

Jan-

98

Jan-

00

Jan-

02

Jan-

04

Jan

'06

Jan

'08

Jan

'10

Jan

'12

$/day cost

Bunker Cost/$ per dayShip Cost/$ per day

FALLING CAPITAL & RISING FUEL COSTS TURN SHIP ECONOMICS ON ITS HEAD

LIBOR (6 Month) 1980-2012

Ship costs 3x as much as fuel

Challenge 3: Shipping Cost Model

Ship cost $17,000/day

Bunker Cost$25,000/day

SMM Press Conference - Shipbuilding

Martin Stopford 14

CLARKSON RESEARCH SERVICES LTD

Challenge 4: Environmental Footprint

14.421.4

36.263.3

76.7

77.4121.2

139

0 20 40 60 80 100 120 140Million Kilowatt capacity

German Power StationsContainers fleet

Non cargoBulker fleetTanker fleet

Other dry fleetOther specialized

Gas fleet

Container fleet has as much

power as Germany�s electricity industry

The installed power capacity of the shipping industry. Container fleet similar to W German power stations.

+ SOX, NOX, ballast etc.

CLARKSON RESEARCH SERVICES LTD

No Magic Solutions

0

50

100

150

200

250

300

350

400

24 23 22 21 20 19 18 17 16 15 14 13 12 11 10 9 8

Fuel

cos

t sav

ing

, cha

rter c

ost i

ncre

ase

$000

Shows the effect on the cost of fuel (green lines) & the cost of shipping capacity (yellow line) of changing ship operating speed in 1 knot increments (based on 5000 mile voyage)

best speed at $1500/tonne

bunkers

best speed at $200/tonne

bunkers

Speed of ship (knots)

80% saving

LNGwindNUCLEAR

Hull formEngineering

logistics

Note 1: Just difficult decisions

COATINGS

EEDIscrubbers

No ballast

Fuel Cells

Back haulShipping lanes

SMM Press Conference - Shipbuilding

Martin Stopford 15

CLARKSON RESEARCH SERVICES LTD

Energy Efficiency Design Index

margin Sea x speed Reference capacity x CargoCO iesEffiicienc -2COmotor Shaft 2CO engineAux 2CO engineMain 2++

� Main Engines: grams of carbon after deducting shaft generator calculated from fuel consumption times a conversion factor (about .85)

� Aux Engines: same as main engine� Shaft motor: less any waste heat recovery (e.g. exhaust

gas boiler with turbo generator)

CLARKSON RESEARCH SERVICES LTD

Conclusions1. Key drivers today are:-� Globalization: positive as we spread into

Non OECD.. we still need to sort out credit crisis

� Shipbuilding overcapacity: over-production inevitable!but so are cheaper ships, willingness to do innovative work; & lower earnings will make cost control key.

� New economic model: Fuel replaces capital as key input. Major challenge to identify the design and equipment package for the new conditions

� Environmental pressure shipping�s oversized carbon footprint means emission regulation is here to stay. Again a technical challenge facing the marine equipment industry as EEDI & SEEMP move forward

2. Shipbuilding technology has no magic solutions � �improvement engineering�.

3. It sound tough but the cycle make us deal with these problems, whether we like it or not!

Don�t worry, there�s still plenty of cargo to

move

![Martin Stopford Marine Money 24 Feb 2011[1]](https://img.dokumen.tips/doc/110x75/54e996e14a7959de428b4a49/martin-stopford-marine-money-24-feb-20111.jpg)