Embed Size (px)

Citation preview

2018

Value Chain Analysis in District Charsadda Market and Employment Project (MEP)

Khalid Khan Khatki - Value Chain Consultant

i | P a g e

TABLE OF CONTENTS

LIST OF TABLES ........................................................................................................................... IV

LIST OF FIGURES ........................................................................................................................... V

ACRONYMS ................................................................................................................................. VI

ACKNOWLEDGEMENT ................................................................................................................ VII

EXECUTIVE SUMMARY .............................................................................................................. VIII

CONTEXT ..................................................................................................................................... 1

PURPOSE AND OBJECTIVE OF THE STUDY ...................................................................................... 1

STUDY OBJECTIVE ............................................................................................................................ 1

SCOPE OF STUDY .............................................................................................................................. 2

STUDY OUTPUT ............................................................................................................................... 2

METHODOLOGY AND APPROACH ................................................................................................. 3

STEP – 1: PRIORITIZATION OF VALUE CHAINS/SUB SECTORS ....................................................................... 3

STEP – 2: MAPPING AND DETAILED ANALYSIS OF SELECTED VALUE CHAINS .................................................... 3

STEP – 3: STRENGTH, WEAKNESSES, OPPORTUNITIES AND THREAT ANALYSIS (SWOT) ..................................... 4

STEP – 4: VALIDATION WORKSHOP ....................................................................................................... 4

LIMITATIONS OF THE STUDY ......................................................................................................... 4

VALUE CHAIN PRIORITIZATION ..................................................................................................... 6

APPROACH ..................................................................................................................................... 6

STRAWBERRY VALUE CHAIN ......................................................................................................... 9

OVERVIEW OF STRAWBERRY SUB-SECTOR .............................................................................................. 9

VALUE CHAIN FUNCTIONS ................................................................................................................ 10

INPUT SUPPLY ........................................................................................................................................... 10

PRODUCTION/POST-HARVEST MANAGEMENT ............................................................................................... 12

MARKETING.............................................................................................................................................. 14

PROCESSING ............................................................................................................................................. 15

CONSUMPTION ......................................................................................................................................... 16

ii | P a g e

VALUE CHAIN OPERATORS ............................................................................................................... 17

INPUT PROVIDERS ...................................................................................................................................... 17

PRODUCERS/FARMERS ............................................................................................................................... 17

MARKET FUNCTIONARIES ............................................................................................................................ 18

ENABLING ENVIRONMENT ................................................................................................................ 18

VC FACILITATORS ...................................................................................................................................... 18

VALUE CHAIN REGULATORS ......................................................................................................................... 20

Value Chain Governance/Integration 22 VALUE CHAIN MAP OF STRAWBERRY CROP (CHARSADDA) ....................................................................... 24

ECONOMIC ANALYSIS – STRAWBERRY VALUE CHAIN ............................................................................... 25

PROFITABILITY MARGINS ............................................................................................................................ 25

DISTRIBUTION OF VALUE ADDITION AND GROSS MARGINS ............................................................................... 28

EMPLOYMENT GENERATION ........................................................................................................................ 28

INEFFICIENCIES AND DISTORTIONS ................................................................................................................ 30

SWOT ANALYSIS – STRAWBERRY ...................................................................................................... 32

ROAD MAP – VALUE CHAIN DEVELOPMENT IN STRAWBERRY .................................................................... 34

RUNNER STAGE ......................................................................................................................................... 34

PRODUCTION STAGE .................................................................................................................................. 34

MARKETING.............................................................................................................................................. 34

VALUE CHAIN GOVERNANCE/TRANSPARENCY ................................................................................................ 35

TOMATO VALUE CHAIN .............................................................................................................. 36

OVERVIEW OF TOMATO SUB-SECTOR .................................................................................................. 36

VALUE CHAIN FUNCTIONS ................................................................................................................ 38

INPUT SUPPLY; .......................................................................................................................................... 38

PRODUCTION/POST-HARVEST HANDING: ...................................................................................................... 38

MARKETING.............................................................................................................................................. 41

VALUE CHAIN OPERATORS ............................................................................................................... 43

INPUT SUPPLIERS ....................................................................................................................................... 43

PRODUCTION/POST-HARVEST MANAGEMENT................................................................................................. 43

MARKETING.............................................................................................................................................. 44

ENABLING ENVIRONMENT ................................................................................................................ 44

VALUE CHAIN FACILITATORS ........................................................................................................................ 44

VALUE CHAIN REGULATORS ......................................................................................................................... 45

VALUE CHAIN INTEGRATION/GOVERNANCE ................................................................................................... 45

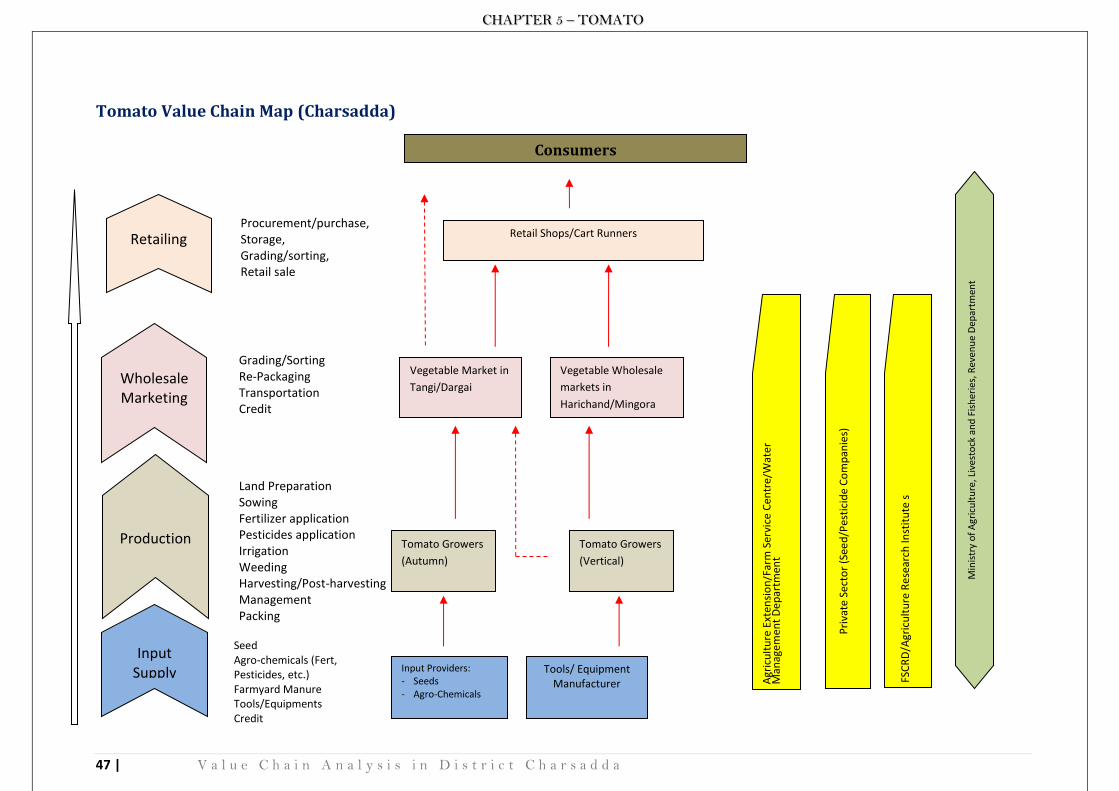

TOMATO VALUE CHAIN MAP (CHARSADDA) ......................................................................................... 47

ECONOMIC ANALYSIS – TOMATO VALUE CHAIN..................................................................................... 48

PROFITABILITY ANALYSIS ............................................................................................................................. 48

DISTRIBUTION OF VALUE ADDITION AND GROSS MARGINS: .............................................................................. 49

EMPLOYMENT GENERATION ........................................................................................................................ 50

DISTORTIONS AND INEFFICIENCIES ................................................................................................................ 52

SWOT ANALYSIS – TOMATO ............................................................................................................ 53

ROAD MAP – VALUE CHAIN DEVELOPMENT OF TOMATO ......................................................................... 54

ANNEX I: TERMS OF REFERENCE ......................................................................................................... 55

iii | P a g e

ANNEX II: CHECKLIST FOR FGDS/KEY INFORMANT INTERVIEWS ................................................................. 58

ANNEX III: OVERVIEW OF STRAWBERRY PRODUCTION IN PUNJAB .............................................................. 60

ANNEX IV: KEY CONTACT LIST ........................................................................................................... 62

iv | P a g e

List of Tables

Table 1: Finding of Prioritization Exercise in District Charsadda .......................................................... 7

Table 2: Seasonal Calendar of Strawberry Crop .................................................................................. 14

Table 3: Taxation Rates on Agriculture Land/Income (acre/annum) ................................................. 21

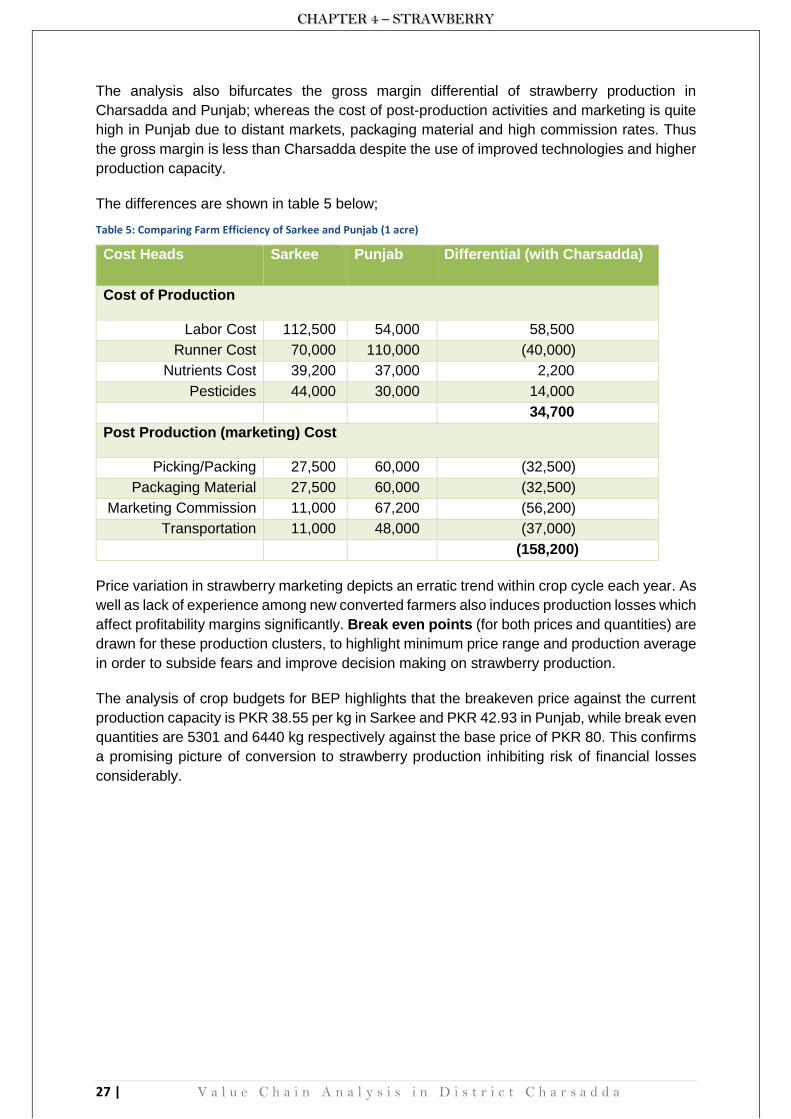

Table 4: Budget of Strawberry Crop in KPK (Sarkee) and Punjab (Sharaqpur) .................................. 26

Table 5: Comparing Farm Efficiency of Sarkee and Punjab (1 acre) ................................................... 27

Table 6: Breakeven Point Calculation for Strawberry in KPK and Punjab (1 acre) ............................ 28

Table 7: Gross Margins and Value Additions in Strawberry Crop (per kg of strawberry turnover) .. 28

Table 8: Calculation of Labor Intensity in Strawberry Cultivation ...................................................... 29

Table 9: Project New Job Opportunities with MEP Support ............................................................... 30

Table 10: Inefficiencies and Distortions in Strawberry Production Cycle (1 acre) ............................. 31

Table 11: SWOT Analysis of Strawberry Crop ..................................................................................... 32

Table 12: Supply Patterns of Tomato in Pakistan ............................................................................... 37

Table 13: Seasonal Calendar of Autumn Tomato Production............................................................. 39

Table 14: Seasonal Calendar of Vertical Tomato Production ............................................................. 40

Table 15: Seasonal Calendar of Surface Tomato ................................................................................. 41

Table 16: Tomato Budgets in Autumn, Vertical and Surface Tomato (Charsadda – 1 acre).............. 48

Table 17: Breakeven Point Calculation for Different Tomato Cultures in Charsadda (1 acre) .......... 49

Table 18: Gross Margins and Value Added by Value Chain Players (per kg tomato turnover) ......... 50

Table 19: Distribution of Labor in Tomato VC Functions (1 acre) ....................................................... 51

Table 20: Projected New Labor Opportunities of Conversion from Ground to Vertical Tomato

Production ............................................................................................................................................ 51

Table 21: Distortions and Inefficiencies in Tomato Value Chain (1 acre) ........................................... 53

Table 22: SWOT Analysis of Tomato Crop ........................................................................................... 53

v | P a g e

List of Figures

Figure 1: Prioritization Criteria for Value Chain Selection .................................................................... 6

Figure 2: Prioritization of Fruits and Vegetables, Agribusiness Support Fund, 2012 ........................... 8

Figure 3: Global Production of Strawberry (FAOSTAT) ......................................................................... 9

Figure 4: Strawberry Runner Production ............................................................................................. 10

Figure 5: Input Dealer in Sarkee .......................................................................................................... 12

Figure 6: Ready to harvest Strawberry, the surface contact of fruit with soil devalues quality

(Courtesy: ASF, PHRA 2012) ................................................................................................................. 12

Figure 7: Some Processed Products of Strawberry in Super Market .................................................. 16

Figure 8: Value Chain Integration in Strawberry ................................................................................. 22

Figure 9: Some Examples of Farmer Group Interaction on WhatsApp in Punjab .............................. 23

Figure 10: Well Managed Mulched Strawberry Field in Punjab ......................................................... 25

Figure 11: Improved Technologies in Punjab: Consumer Packaging; Tunnel + Drip Irrigation;

Strawberry Runners in Peat moss Trays .............................................................................................. 35

Figure 12: Provincial Tomato Shares and Their Respective Production Potential ........................... 36

Figure 14: Vegetable Production in KPK (2015-16) ............................................................................. 37

Figure 15: Area and Production of Major Vegetable in KPK ............................................................... 37

Figure 16: Field Based Ripening Heaps of Tomato .............................................................................. 39

Figure 17: Tomato in Tangi Market Offered for Auction .................................................................... 42

Figure 19: Private Company Banner of Pest Management ................................................................. 45

Figure 18: Value Chain Integration in Tomato Crop ............................................................................ 46

Figure 20: Farmer Using Hand Made Cultivator for Hoeing ............................................................... 50

Figure 21: Post-harvest Losses of Tomato ........................................................................................... 52

vi | P a g e

ACRONYMS

ADP Annual Development Plan

AED Agriculture Extension Department

ASF Agribusiness Support Fund

CRS Crop Reporting Service

CMP Crop Maximization Project

EDT Enterprise Development Training

FEG Farmer Enterprise Group

FSC Farm Service Centre

FSC&RD Federal Seed Certification and Registration Department

FFS Farmer Field School

FBS Farmer Business School

GM Gross Margin

KG Kilogram

KPK Khyber Pakhtunkhwa

PRA Participatory Rural Appraisal

PKR Pakistan Rupees

RMA Rapid Market Appraisal

ROI Return on investment

SRSP Sarhad Rural Support Programme

MEP Market and Employment Project

MIS Market Information System

MT Metric Tons

VC Value Chain

VCD Value Chain Development

vii | P a g e

ACKNOWLEDGEMENT

Value Chain Analysis in district Charsadda is commissioned by Market and Employment Project of Helvetas Swiss Intercooperation. The assessment was made possible through the active support, facilitation and continuous guidance of MEP Management and their focal Points, Mr. Fayaz Ahmed (Value Chain Specialist) and Mr. Kaleemullah Shinwari (Field Coordinator) during field work. I need to express my sincere gratitude to Mr. Liaquat Ali (District Director Agriculture) for his overall facilitation and support, Mr. Mohammad Idress (Subject Matter Specialist, Charsadda), Mr. Rafiq Jan (Field Assistant, Sarkee) for their dedication and continuous facilitation throughout field work. The cooperation of all stakeholders consulted during field work was commendable in providing every possible detail for assessment parameters in a candid manner.

viii | P a g e

EXECUTIVE SUMMARY

Market and Employment Project (MEP) is Dutch Funded (Ministry of Foreign Affairs) project implemented by Helvetas Swiss Intercooperation in District Charsadda with the specific goal to create sustainable income generating and livelihoods opportunities leading to jobs, income and more resilient communities. Market and Employment Project (MEP) has commissioned a value chain study to identify the most feasible value chains and devise a comprehensive strategy for the value chain development in the short, medium and long term in district Charsadda.

The methodology used for value chain analysis was interactive and drawn from the participatory tools of Participatory Rural Appraisal. Primary data collection through focus group discussion and key informant interviews, and triangulation with authentic secondary research was used as an approach for value chain analysis. Prioritization of agriculture sub-sectors, mapping and detailed analysis of selected value chains, SWOT analysis for value chain development and validation workshops were important steps in the exercise. Total of 8 focus groups discussions have been held with different stakeholders and more than 35 key informants have been contacted and interviewed for the subject value chain analysis in Charsadda, Peshawar, Swat, Lahore and Sheikhupura (Sharaqpur) areas.

Prioritization exercise was held with key stakeholders of agriculture sectors in district Charsadda, drawing representative of agriculture line departments, private sector, and progressive farming communities from all 3 Tehsils of district Charsadda. The approach for prioritization exercise was adopted from the earlier experience of Helvetas in Sindh, Pakistan. The parameters were primarily based on market orientation, employment generation, and important cross cutting themes. Fruits, Vegetables, Wheat, Sugarcane and Maize were presented for ranking exercise, keeping in view the economic significance of these crops in district Charsadda. Strawberry and tomato were selected for detailed value chain analysis. Commercialization, profitability margins, shift toward intensive farming practices, and land fragmentation were some of the reason identified for shifting tendency towards high value crops in fruits and vegetable groups.

The enabling environment is facilitated through range of line departments, farm service centers and private sector institutions. The role of private sector is more vibrant in transfer of technologies, extensive outreach and technical advisory services. Dedicated extension material is not available for either vegetable and fruit crop from credible institution in district Charsadda, some barely available extension leaflets and brochures are available through private companies but merely promoting their own products. However, the facilitation is mostly products oriented, which induced pest resistance, impact crop efficiency and also pose environmental hazards. The regulatory framework is well defined through proper legislations but implementation mechanisms are rather weak to check sub-standards crop inputs. Strong advocacy with Agriculture Ministry, capacity building of department representatives and awareness among farming communities is required to improve accountability, check and balance, and sustainable public private networking in agriculture crop sector.

Strawberries (Fragaria x ananasa Duch.)

was introduced in Charsadda in 1994-95. The economic return of strawberry crop is 4 times higher than sugarcane and 9 times higher than wheat crop in district Charsadda which helped rapid conversion towards strawberry cultivation.

Strawberry is being cultivated exclusively from propagative material (runner) in its entire history in Pakistan. TOPS, CORONA and SCHINDLER are few successful varieties in Strawberry crop; however, SCHINDLER is the only strawberry cultivar these days. Runners are procured exclusively from Swat and Upper Dir areas, where more than 500 million runners have been channeled to Sindh, Punjab and KPK areas in 2017. Both strawberry plant and fruit are succulent and susceptible to number of insect pests during production stages. The crop

ix | P a g e

suffered significant losses during rainy season, and inappropriate post production handling. Mites become a major pest problem in strawberry crop due to favorable climatic conditions and increased pest resistance. Lack of knowledge provides opening for pesticide/fertilizer adulteration, subsequently provide basis for the use in-efficient and sub-standard chemicals.

Intensive management practices and high cost of investment limits farm size of strawberry. The usual practice is 1-acre average in Charsadda where research confirmed 0.68 acres of farm size is optimum for strawberry cultivation.

An un-conventional market place in Sarkee is the major marketing venue for strawberry. The same market is linking Inter-market trade with far flung district of KPK and Punjab. The farm gate marketing option is more preferred by farming community for price premium, save marketing charges, loading/unloading, and time efficient. The retail function of strawberry expands rapidly in recent years owing to increased consumption of strawberry; however, the potential consumption growth is constrained due to health concerns related with extensive usage of chemicals.

The budget demonstrates that strawberry crop in Charsadda returns a lucrative gross margin of PKR 455,900 (52%) per acre of land and the rate of return on investment is 107%. The profitability of strawberry in Charsadda is slightly higher than Punjab (46% gross margin), owing to differences in some major cost heads (for instance, higher seed rate, the marketing cost and distant markets). Comparative analysis did point out lapses in farm efficiency of district Charsadda, where farmers can enhance profitability margins with improved practices, especially mulching of crop to save labor cost. It is estimated that strawberry production in Charsadda alone generated 149,000 man-days in a single crop cycle. Shortage of labor is a growing concern at all levels of strawberry production. The feasibility of mechanization and innovation need to be tested from different experiences to subside pressure on growing labor needs.

Tomato (Solanum lycopersicum) is a major vegetable crop in Pakistan both in terms of areas sown and production capacity in the country. Sindh is the major producer of tomato in Pakistan, followed by KPK, Baluchistan and Punjab. The seasonal calendar is evenly distributed all across Pakistan, where the supply during September – December is relatively tight which provide opening for tomato import from India, Afghanistan and Iran. Tomato production is leading crop among all vegetable produced in KPK (23% area and production). Charsadda is ranked 3rd for tomato production in the province, and has grown under diverse cultural practices in the district. Rabi crop (Spring-Summer) is more prominent in Tehsil Charsadda and Shabqadar, while kharif crop (Autumn-Winter) in grown exclusively in the frost free zones of Tehsil Tangi.

The Autumn Crop is practiced mainly on the strips stretched along Mohmand Agency toward Malakand on a rainfed area, approximately on around 1000 acres. Vertical Gardening is more common in Tehsil Tangi and Charsadda (Harichand, Sarkee, Mandani, Gulabad are main Union Councils in Tehsil Tangi) on an area of 1000-1200 acres in Charsadda. Surface tomato is more common in Tehsil Shabqadar on an area of around 100 acres, using traditional production technologies. The seasonal calendar of tomato Rabi crop is started in January, the crop lasts in May-June under traditional practices, while extends till August under vertical cultivation. The autumn crop cycle is in between August and January.

Tangi and Dargai vegetable markets are specialized in tomato autumn crop while Harichand, Swat and Timergara markets are prime options for vertically produced tomato. Tomato production from Shabqadar is traded in Shabqadar and Peshawar vegetable markets. The packaging materials used in all production patterns is traditional and tends to have un-necessary crop losses during harvesting and marketing cycles. High rate of price fluctuations in tomato crop induced discouraging tendency among tomato growers during last 3-4 cropping cycles.

x | P a g e

Vegetable export is more emphasized on bitter gourd, peas, brinjal, cucumber, fresh beans and carrot from the same production clusters. Tomato is not a preferred crop, not only because of perishability but also not complying with the consumer preference of Middle East (prefer round tomatoes). Production capacity of improved hybrid seeds is not attained largely due to non-compliance of technical recommendations and structural limitations inherent in the farming system (technical capacities, quality of agro-chemicals, irrigation issues, and in-efficient post-harvest management).

Analysis revealed that winter crop performs the best among all cropping patterns of tomato in district Charsadda, it offers high gross margin (68%) and minimize the risk associated with least production capital required for tomato production. The Return on Investment (ROI) is much higher for autumn crop (212%) than vertical (32%) and ground tomatoes (17%) in 2016-17. The vertical gardening though high investment rate and extensive production, offered risky gross margin (24%) for tomato growers in 2017. Likewise, the performance of surface tomato is not outstanding during last 3-4 years, the least gross margin of 15% during last cropping season resulted in further reduction of tomato cropping area in 2018.

Though there are some valid limitations of current research due to data biasedness, paucity of time and resources, analysis framework and purposive sampling techniques, and the scope of improvement should not be overruled with further detailed and thematic research. However, the consultation process did highlight certain important recommendations for value chain development interventions in both studied value chains. The interventions related to enabling environment and service delivery will not only benefit the studied crops and its subsequent expansion, the spill over will also have positive impact on other high value crops in the region.

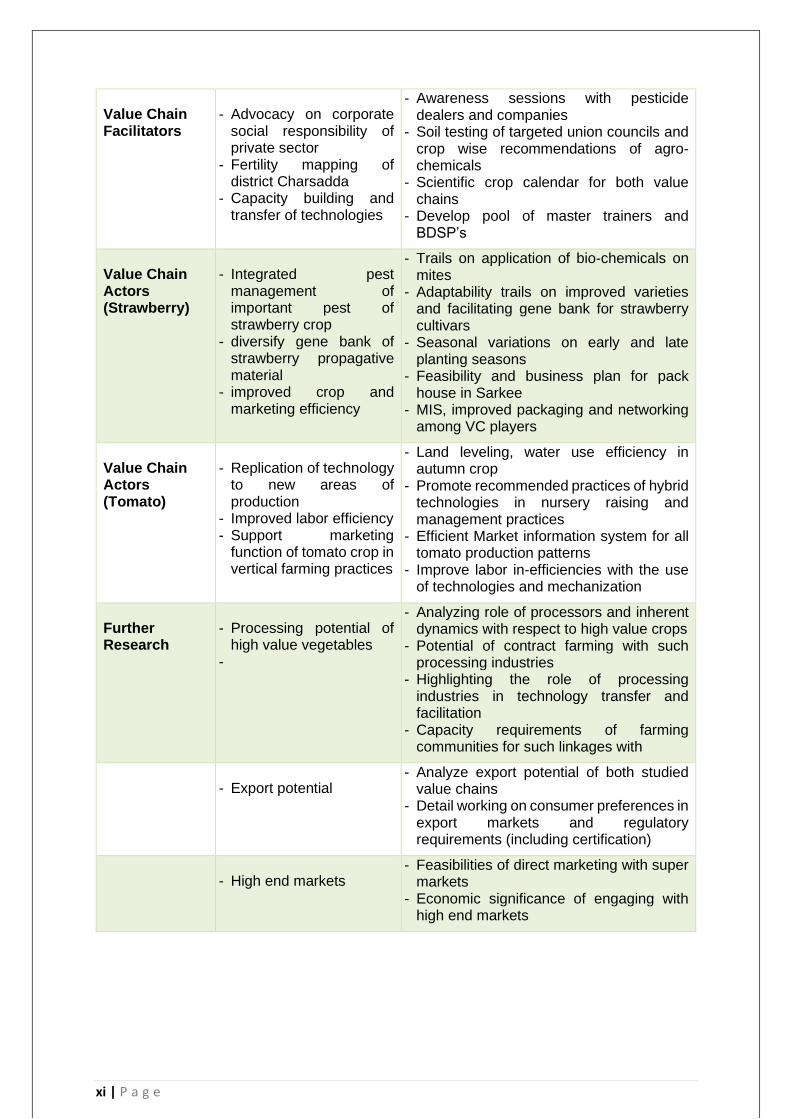

The value chain development recommendations are summarized herewith for improved decision making and drawing road maps for value chain development strategies. Interventions on part of regulatory framework and service delivery of public/private institutions will foster the overall enabling environment for agriculture development in the area. Crop specific recommendations are also listed separately for targeted interventions. Similarly, areas of further detailed research are also mentioned separately for future consideration. It is forecasted that MEP value chain development strategies in these 2 crops will generate additional 115,490 (both strawberry and tomato) direct/in-direct employment opportunities in district Charsadda.

Value Chain Domains

Projected Outcomes Output Level Interventions

Value Chain Regulators

- Improving check and balance

- Awareness and advocacy campaigns

- Improve decision making on high value crops

- Facilitating practical SOPs for Agriculture Policy, Pesticide/fertilizer/seed acts,

- Orientation sessions on regulatory framework,

- Capacity building of AED, FSC, Agriculture Research

- Action plans for high value crops - Mapping un-conventional crops, and

advocating targeted strategies for the expansion of such niche crops (value chain studies, technical feasibilities, Crop Reporting Service etc)

xi | P a g e

Value Chain Facilitators

- Advocacy on corporate social responsibility of private sector

- Fertility mapping of district Charsadda

- Capacity building and transfer of technologies

- Awareness sessions with pesticide dealers and companies

- Soil testing of targeted union councils and crop wise recommendations of agro-chemicals

- Scientific crop calendar for both value chains

- Develop pool of master trainers and BDSP’s

Value Chain Actors (Strawberry)

- Integrated pest management of important pest of strawberry crop

- diversify gene bank of strawberry propagative material

- improved crop and marketing efficiency

- Trails on application of bio-chemicals on mites

- Adaptability trails on improved varieties and facilitating gene bank for strawberry cultivars

- Seasonal variations on early and late planting seasons

- Feasibility and business plan for pack house in Sarkee

- MIS, improved packaging and networking among VC players

Value Chain Actors (Tomato)

- Replication of technology to new areas of production

- Improved labor efficiency - Support marketing

function of tomato crop in vertical farming practices

- Land leveling, water use efficiency in autumn crop

- Promote recommended practices of hybrid technologies in nursery raising and management practices

- Efficient Market information system for all tomato production patterns

- Improve labor in-efficiencies with the use of technologies and mechanization

Further Research

- Processing potential of high value vegetables

-

- Analyzing role of processors and inherent dynamics with respect to high value crops

- Potential of contract farming with such processing industries

- Highlighting the role of processing industries in technology transfer and facilitation

- Capacity requirements of farming communities for such linkages with

- Export potential - Analyze export potential of both studied

value chains - Detail working on consumer preferences in

export markets and regulatory requirements (including certification)

- High end markets - Feasibilities of direct marketing with super

markets - Economic significance of engaging with

high end markets

CHAPTER 1 - BACKGROUND

1 | V a l u e C h a i n A n a l y s i s i n D i s t r i c t C h a r s a d d a

CONTEXT

Market and Employment Project (MEP) is Dutch Government (Ministry of Foreign Affairs) project implemented by Helvetas Swiss Intercooperation in District Charsadda with the specific goal of creating sustainable income generation and livelihoods opportunities leading to jobs, income and more resilient communities. The project intends to develop strategies that could help in creating more job opportunities for the people in services sector as well as in the commodity sector like agriculture, livestock etc.

PURPOSE AND OBJECTIVE OF THE STUDY

Market and Employment Project (MEP) has commissioned a value chain study to identify the most feasible value chains and devise a comprehensive strategy for the value chain development in the short, medium and long term in district Charsadda.

The study intends to identify the agriculture based value chains and prioritize these value chains based on the set criteria provided by the project for further exploration. The research is supposed to gain a comprehensive and deeper understanding of the existing status of the value chains and identify areas of improvement for high economic returns for the value chain players. The scope of work involved prioritization of the value chains, detail value chain analysis and market research and based on the field findings develop workable implementation strategy for identified value chains keeping in view the context of the area.

Study Objective

The overall objective of the study is to conduct a detailed value chain analysis of selected sub-sectors in order to:

- Identify most suitable agriculture value chains/sub-sectors in district Charsadda, taking into consideration potential replacement of imported supply by local production;

- Conduct detail assessment for the top 2 prioritized sub sectors/value chains keeping in view its market potential, employment generation, extended outreach and align with the scope of commissioned project in the target location;

- Identify handy skills, capacities and inputs that each sub-sector requires for up-gradation;

- Identify and analyze potential business areas, commercial status, value addition possibilities, gaps and intervention points for the identified sub-sectors;

- Identify strengths, weaknesses, opportunities and threats (SWOT) of the identified commodities/products/services, and draw a road map of strengthening identified value chains;

- Identify main constraints faced by the existing producers in each of the value chain and suggest possible solutions;

- Identify the main trends and drivers for enabling environment in each sub-sector.

CHAPTER 1 - BACKGROUND

2 | V a l u e C h a i n A n a l y s i s i n D i s t r i c t C h a r s a d d a

Scope of Study

The scope of the study included key market for agriculture products (current and potential) produced in various parts of the district Charsadda; tracing and tracking national markets, regional consolidation centers and local aggregation points for agriculture produced in the selected district. Study in the domestic markets was undertaken by conducting key informants’ interviews, and focus group discussions with market players in commodity chains. Whilst the study TORs also deliberated on the potential role of women in the target district, emphasis will be given to those potential sector and value chains which engage women as key entrepreneurs and provide potential to improve their skills for income optimization and creating an enabling environment to improve women empowerment in the studied value chains.

Study Output

The proposed assignment was required to conduct a comprehensive value chain analysis of potential sub-sectors in district Charsadda; by employing appropriate approach and methodology, inter-alia review of credible secondary data (published) and relevant past studies of the same nature. The findings are supposed to support the targeted groups of the MEP to explore the inherent potential among the farming and non-farming communities of district Charsadda to improve their well-being and economic return. The report will help the project to introduce skills that will help small farmers and entrepreneurs to engage in profitable small businesses, improve and diversify their livelihoods and contribute to improved household resilience through better response to the local market demand. The analysis will facilitate the development of appropriate design of interventions with community involvement and utilization of a market oriented approach. It will enable the project to work with individual farmers and groups to improve their existing market access strategies. The study findings will bridge the gap between the target group and the market by exploring market opportunities and ways to address market constraints and obstacles for the mutual benefits of all players in the respective sub-sectors. It is expected that a market assessment and value chain study report will enable the Project to develop a comprehensive value chain development program for the project target group in district Charsadda to transform agribusinesses paying dividends to disadvantaged communities and ultimately leading to economic growth and stability in the area.

CHAPTER 2 – METHODOLOGY

3 | V a l u e C h a i n A n a l y s i s i n D i s t r i c t C h a r s a d d a

METHODOLOGY AND APPROACH

“Making Value Chain Work Better for the Poor” is considered an appropriate model for value chain analysis in the context of developing countries. Guiding principles from the same model was used during said assessment using standard indicators and parameters as found appropriate for the context and further discussion with project personnel. Both primary and secondary sources, vis-a-vis appropriate quantitative and qualitative tools are used in the methodological approach. The primary research was emphasized on interactive and consultative PRA tools of focus group discussions and key informant interviews while secondary research took guidance from published research of credible sources in district Charsadda. Qualitative and quantitative parameters were built upon perception and institutional knowledge of representative stakeholders during field research. Information collected during FGD and KIIs will lead to subsequent analysis like agro-ecological zoning, supply trends, activity calendar, price fluctuation, profitability analysis, employment generation, market positioning and mapping of value chain players and functions.

The step wise approach and pattern of the analysis followed as mentioned below;

Step – 1: Prioritization of Value Chains/Sub sectors

The scoping and prioritization of value chains was done in two steps i.e. stock taking of the existing data collected through market analysis and participatory prioritization exercise with representatives of on farm communities, consultation with respective field staff, key public and private sector institutions. The criterion was adopted from the previous similar work of Helvetas Swiss Intercooperation, and coherent with the scope of Market and Employment Project. Major factors important for inclusion in the prioritization will emerge from the three pillars of sustainable development i.e. social, economic and environmental. The important consideration in prioritization was mutual agreement on relative weightage to each indicator and subsequent scoring on the same for different sub-sectors. The outcome was presented in the form of grid analysis of the potential areas.

Paucity of time and resources was limiting the detailed value chain analysis to 2 sub-sectors at this point in time; however, the long listing of potential areas from prioritization exercise will be kept for later consideration and detailed analysis by MEP.

Step – 2: Mapping and Detailed Analysis of Selected Value Chains

The start and end points of the value chain are usually determined to be input supply and consumption respectively. The allocated time and resources was efficiently utilized between these two ends for analysis and draw valid recommendations for MEP to introduce programmatic interventions in the project targeted locations of district Charsadda. Mapping of the prioritized and selected value chains was undertaken in detail wherein key stakeholders were visited, including value chain players, facilitators and influencers for selected sub-sectors from start to end. This was done in a detailed consultative process using interactive techniques of focus group discussions and individual key informants’ interviews as found appropriate. All issues and gaps were discussed and documented in a structured manner. For effectively conducting the FGDs, a framework/checklist was developed and used for gathering information from the participants at all levels. Within the chain analysis, efforts will be made to identify the next stakeholder through referral methods for both backward and forward actors in the chain. Mapping exercise captured all relevant information that pertain to value chain functions, activities, actors and relationships, service providers as well as enablers. Mapping will also be used to identify key opportunities and critical constraints.

CHAPTER 2 – METHODOLOGY

4 | V a l u e C h a i n A n a l y s i s i n D i s t r i c t C h a r s a d d a

Both quantitative and qualitative analysis of the value chains were carried out that include analysis of the volumes of supplies of each chain, number of actors involved from start to the end, creation of employment at each node, an estimated job creation and enterprises in the support function level, market margins and profitability, and inefficiencies and distortions identified in respective value chain. The analysis captured inefficiencies in the chain and estimated pre/post-harvest losses that could be avoided. In addition, an overall assessment of the competitiveness was also undertaken, benchmarking and tapping unexplored niches in the local and regional markets.

The study was based on purposive sampling of actors involved and relevant to the various areas of the value chains. The approach was mainly explorative and key informants drawn for different levels of analysis were based on their relevance, collaboration, institutional knowledge, referral, and credibility. The study approach in the field was probing and case building for each operator and looking at the chains from the perspective of the private sector. Though the sampling frame was purpose, 2-3 players were approached at each value chain function to make sure cross checks, validate and triangulate information for valid analysis and better precision.

The initial scope of work was designed for district Charsadda only, however the identification of Strawberry for detailed analysis compelled to include runner production cycle in Swat as well as strawberry production in Lahore and Sheikhupura for comparative analysis for technology innovations and benchmarking.

Total of 8 focus groups discussions have been held with different stakeholders and more than 35 key informants have been contacted and interviewed for the subject value chain analysis in Charsadda, Peshawar, Swat, Lahore and Sharaqpur areas.

Step – 3: Strength, Weaknesses, Opportunities and Threat Analysis (SWOT)

The key findings and analysis patterns were structured in a SWOT analysis and ascertain implications of each weakness and threat with respect to the opportunities. Prioritization of constraints were undertaken in order to identify the most relevant and to address critical constraints in order to achieve competitiveness in the selected businesses. The SWOT analysis was further translated in stipulating road-maps for selected value chains. The recommendations were in line with the organization strategy as per regular consultation with project focal points and detailed debriefing session after field work.

Step – 4: Validation workshop

A one-day validation workshop was organized with key stakeholders of selected and analyzed value chains in district Charsadda at the end of field survey. Preliminary analysis was shared with the group of 40 participant stakeholders, not only to validate the findings of field work for discrepancies, the proposed framework of value chain development was also being authenticated with much pragmatic inputs from stake-holding groups. Representatives of Agriculture Extension Department, Agriculture Research, Water Management, input provides, companies representatives, and progressive farmers participated in the consultation workshop. The analysis was updated and more inputs were integrated in devising road maps of value chain development of strawberry and tomato sub-sectors in district Charsadda.

LIMITATIONS OF THE STUDY

The study design was crafted in accordance with standard methodology for value chain assessment exercise, duly customized with the TOR requirement of the study. The methodology calls for covering representative operators in each function of the value chains

CHAPTER 2 – METHODOLOGY

5 | V a l u e C h a i n A n a l y s i s i n D i s t r i c t C h a r s a d d a

as well as key informants having relevance to the service delivery and enabling environment aspects. The study approach in the field was probing and case building for each operator and looking at the chains from the perspective of the private sector, contextual with poverty reduction and efficient management of resources.

The research findings are in line with the aspirations of MEP project, however certain valid limitations are attached with the nature of analysis and data collection tools. The use of purposive sampling methodology over systematic sampling technique may have induced research biasedness of respondents and analyst. Probing and cross validation through reaching value chain players at different layers helped in overcoming individual biasedness, however the confidence level on analyzed thematic areas could be improved with repeated consultation and supporting research exercise. Moreover, price analysis is a stand-alone domain of marketing research; price inconsistencies, and dramatic fluctuations in the marketing patterns of fruits/vegetables coupled with lack of documented data in the country make it challenging for pragmatic farm budgets and efficiency analysis. Best possible estimates are used in quantitative analysis for this study, however, a robust market information system is required for informed and improved decision making about the studied value chains.

Certain aspects of the value chains were asking for further detailed and thematic research, especially the areas of processing and export potential having an extended scope and was not possible to be analyzed in the stipulated timeframe. Moreover, in-situ analysis of strawberry marketing chain as well as vertical and ground tomato markets would provide a chance to consulting more diverse market players and direct observation would augment the collected information. The benchmarking and comparative analysis with

CHAPTER 3 - PRIORITIZATION

6 | V a l u e C h a i n A n a l y s i s i n D i s t r i c t C h a r s a d d a

VALUE CHAIN PRIORITIZATION

With support and due facilitation of district Agriculture Extension Department, a prioritization

exercise was organized with key stakeholders in district Charsadda. The exercise was the first

step towards detailed value chain assessment and intended to identify the most potential sub-

sectors for detailed analysis. The exercise was held with the key informant group, identified

together with Agriculture Extension department from the important stakeholders of agriculture

sector in district Charsadda.

Approach

Participation: The exercise was held with representative stakeholders from agriculture line

departments (Agriculture Extension, Water Management, Soil Conservation and Testing

laboratories, Crop Reporting Service), farm service centers, progressive farmers, and inputs

suppliers. Stakeholders from all 3 Tehsils of district Charsadda were invited to have a

balanced geographic representation and to raise inputs for important cultivated crops in

different pockets.

Criteria: The prioritization criteria was adopted from the earlier experience of MEP1, whereas

respective importance was given to market oriented factors while also considering specific

vulnerabilities of poor involvement, gender consideration and impact on environment. Eight

factors along with their respective weightage are listed here;

Figure 1: Prioritization Criteria for Value Chain Selection

Mechanism: The prioritization exercise was initiated with the brainstorming session on the

status of agriculture sector in district Charsadda, pinpointing the strategic strengths of farming

practices and the broader socio-economic realities faced by the rural communities of district

Charsadda. Five crops or/and crop groups have been selected for detailed prioritization on

1 Rapid Value Chain Assessment in Sindh, Helvetas Swiss Intercooperation, March 2016

CHAPTER 3 - PRIORITIZATION

7 | V a l u e C h a i n A n a l y s i s i n D i s t r i c t C h a r s a d d a

the basis of their economic significance, commercial aspects and relevance for overall

livelihood patterns in district Charsadda. The selected crops were;

- Vegetables (Tomato, Bitter Gourd, Tinda Gourd);

- Fruits (Strawberry, Honey Dew Melon, Plum);

- Wheat;

- Maize;

- Sugar Cane;

Participants were encouraged to assign values to each crop on these factors during discussion

and consensus building. Fruit and vegetable groups have been scored the highest ranking

followed by wheat, sugar cane and maize. Commercialization, profitability margins, shift

toward intensive farming practices, and land fragmentation were some of the reason identified

for shifting tendency towards high value crops in fruits and vegetable groups.

Table 1: Finding of Prioritization Exercise in District Charsadda

Though fruits and vegetables identified were having equal significance, however after further

elaboration and due validation with Agriculture Extension Department and some key

informants, tomato and strawberry was selected for detailed value chain analysis and

stipulating road map for the project engagement in district Charsadda. The remaining identified

fruits and vegetables will be given due consideration in the later phases of the Market and

Employment Project.

The output of the prioritization exercise is not unique, and evidence base is available that

these crops have been emphasized in the recent past of such development interventions.

Participatory Rapid Horticulture Appraisal (PRHA2), conducted by Agribusiness Support Fund

(ASF) in 2012 in an effort to draw a baseline for their agribusiness project identified the same

priority sub-sectors for development interventions in Peshawar Valley. Their criteria of

prioritization were drawn from the same approach of market orientation, and considering

important aspect of engaging small holders and women. They have identified peach, citrus,

strawberry, apple, melon, apricot, potato, tomato and onion as most potential sub-sector for

Peshawar Region. The overall ranking of fruits and vegetables under PRHA is given under.

2 http://pdf.usaid.gov/pdf_docs/PA00JQRJ.pdf

Score Weighted

scoreScore

Weighted

scoreScore

Weighted

scoreScore

Weighted

scoreScore

Weighted

score

Market Access 2 5 10 4 8 3 6 4 8 5 10

Volume 2 3 6 4 8 5 10 3 6 4 8

Income Generation 3 4 12 2 6 3 9 5 15 3 9

Employment Created 3 5 15 3 9 2 6 4 12 2 6

Market Demand 3 5 15 2 6 2 6 5 15 3 9

Poor Involvement 2 5 10 3 6 4 8 3 6 2 4

Women Involvement 2 1 2 2 4 1 2 2 4 3 6

Envrionment 2 0 0 2 4 4 8 1 2 4 8

Aggregate Weighted Score 70 22 51 24 55 27 68 26 60

Factors Weightage

Vegetables

(Tomato, Bitter

Gourd)

Maize Sugar CaneFruits (Strawberry,

Honey Dew melon)Wheat

CHAPTER 3 - PRIORITIZATION

8 | V a l u e C h a i n A n a l y s i s i n D i s t r i c t C h a r s a d d a

Figure 2: Prioritization of Fruits and Vegetables, Agribusiness Support Fund, 2012

CHAPTER 4 – STRAWBERRY

9 | V a l u e C h a i n A n a l y s i s i n D i s t r i c t C h a r s a d d a

STRAWBERRY VALUE CHAIN

Overview of Strawberry Sub-Sector

Strawberries (Fragaria x ananasa Duch.), originally grown in northern parts of Europe and

were also found in different parts of Russia, Chile and United States. Strawberries are also

thought to have been cultivated in ancient Rome in large scale for medicinal purposes. During

the 13th century, France also cultivated strawberries for its medicinal purpose. The roots, fruits

and leaves of Alpine strawberry were widely used in these countries to make medicine that

were used to cure digestive problems and skin diseases. Strawberries are known for its unique

taste and flavor, nutritionally low in calories, rich in vitamin C, potassium, folic acid, fiber, and

vitamin B63 (Allah Dad Khan, CMPII 2014). Strawberry is cultivated widely across the globe

and FAOSTAT reported strawberry cultivation from 77 countries as of 2016, however this

milestone might be higher due to non-reporting of strawberry crop from remaining countries

(Pakistan is an example!).

Over the last two decades, strawberries

have experienced one of the highest rates

of consumption growth of all fruit and

vegetables across the globe4. The growth

in strawberry production is recorded 23%

during last 5 years and is being

continuously growing with every passing

year5. Strawberry grown on an area of

402,338 ha globally and the production

exceed 9 million tonnes in 2016. China,

USA, Mexico, Egypt, and Turkey are five

leading producers of Strawberry crop,

these leading countries contributes 72% of

global production.

Strawberry has been introduced by Rafhan Foods as a crop in Swat during the period of 1979-

80 for flavoring their different products. When the quantities exceeded the company

requirement, they helped in linking the surplus crop to different 5 star hotels in Pakistan. The

Pioneer Progressive farmer is still alive and yet dedicated in introducing new varieties of

strawberries from his own networks and knowhow.

Strawberry Crop started in Charsadda in 1994-95, introduced by a progressive farmer from

Swat. It was fetching good price those days (PKR 18 per kg), encouraged other farmers to

replicate strawberry as a crop in the area. Strawberry cultivation is reported extensively in 4

adjacent union councils of Charsadda (Sarkee Titara, Utmanzai, Tarangzai, Behlola). It

3 Khan AD (2016) Straw Berry Cultivation in Charsadda A District Of Cmp-II In NWFP By Allah Dad Khan Agriculture Extension

And Ghulam Nabi Agriculture Research Tarnab Peshawar. Adv Plants Agric Res 4(3): 00142. DOI: 10.15406/apar.2016.04.00142

4 http://www.freshplaza.com/article/159848/OVERVIEW-GLOBAL-STRAWBERRY-MARKET (visited on 27 January 2018)

5 http://www.fao.org/faostat/en/#data/QC ((visited on 27 January 2018)

7,3

90

,08

8

7,8

86

,51

9

8,1

58

,70

3

8,7

52

,16

7

9,1

26

,33

7

0

2000000

4000000

6000000

8000000

10000000

2012 2013 2014 2015 2016

Pro

du

ctio

n (

Ton

ne

s)

Figure 3: Global Production of Strawberry (FAOSTAT)

CHAPTER 4 – STRAWBERRY

10 | V a l u e C h a i n A n a l y s i s i n D i s t r i c t C h a r s a d d a

replaced sugar beet, sugar cane, wheat and maize in this particular belt. Afridi et al (2009)6

informed that the economic return of strawberry crop is four times higher than sugarcane and

9 times higher than wheat crop in district Charsadda. Strawberry is yet considered an un-

conventional crop in Pakistan, despite its significant expansion throughout the country and

overwhelming economic significance. Economic valuation of strawberry crop in different value

chain functions estimated to be surpassing 12 billion rupees in a single cropping year

(estimates based on value generated in 2016-17), generating hundred and thousands of

employment opportunities for farming families.

Strawberry provide impetus for high value vegetable culture in district Charsadda during 2001-

02; agriculture laborers trained on off-season vegetable production (tunnel farming, vertical

gardening, hybrid technology) promoted the tendency of leasing land for commercial

vegetable production in Charsadda; strawberry was the preference crop of those farmers,

followed by other seasonal vegetables like tomato, bitter gourd, tinda gourd, long gourd and

honey dew melon.

Value Chain Functions

Input Supply

Strawberry is being cultivated exclusively from propagative material (runner) in its entire

history in Pakistan. TOPS, CORONA and SCHINDLER are few successful varieties in

Strawberry crop, however the performance of Schindler is regarded best in comparison to

other varieties due to its higher production capacity, fruit weight, adaptability to diverse agro-

climatic zones and shelf life. CORONA was shallow inside (reduced weight) while TOPS was

not considered good for shelf life, hence become obsolete with the passage of time. Schindler

was introduced in 1998-1999 and is being the sole source of strawberry cultivation these days.

Varietal introduction is not scientific and through proper adaptability trials, the pioneer

progressive farmer (Kazim Bacha) in Swat asks mutual friends visiting different countries to

bring few seedlings of new varieties for

adaptability. The farmer introduced 2 varieties

(“Communeral” and “Sacoa”) two years ago for

adaptability trials and replication; he is planning to

introduce it this year onwards for marketing.

Agriculture Research Station Mingora maintained

a gene bank of Strawberry cultivars but

unfortunately the progeny has been lost due to

closure of research station in 2008-10. Research

officials from the same station have visited

Australia in 2015, and brought back few seedlings

of a variety (they have given the name “Australian

Mark” themselves) for adaptability trials. The runners are distributed among few progressive

farmers last year, however farmers were not satisfied with its performance and high

susceptibility to intense heat.

6 “Cost and Revenue Analysis of Strawberry Production in the Sub-Tropical Areas of NWFP, Pakistan”, Ghulam Sadiq Afridi, M.

Ishaq and Sarfaraz Ahmed 2009; Pakistan Journal of life and social sciences (2009), 7(1):59-65

Figure 4: Strawberry Runner Production

CHAPTER 4 – STRAWBERRY

11 | V a l u e C h a i n A n a l y s i s i n D i s t r i c t C h a r s a d d a

Runner prices are increased gradually and rather un-predictable supply and demand pattern

was witnessed in previous years (last year runners were short due higher demand in Punjab

i.e. prices jumped to Rs. 5). Sometime farmers have losses due to unavailability of runners

and sometimes runner farmers have losses due to lack of demand.

Runners are produced in the month of March – April, onion is practiced as a major inter-crop

in strawberry (Peas, fresh beans are other intercropping option), onion is harvested in the

month of May, and runners are being re-directed to the main bed (3 feet) for onward growth

and runners’ production.

Mites - considered one of the major pest problems in strawberry crop - do attack runner crop

during the month of May – June in swat but controlled with good miticides and management

practices (power sprayers), climatic factors also favor management practices in Swat and the

control is rather manageable over there.

A healthy plant produces 5-50 runners in its life cycle, however initial 15-20 runners are

considered good in vigor (runners produced till the month of June-July) and has good

production capacity while runners produced during August – September are rather weak and

impotent, tend to have high chances of failure in transplantation and production stage.

High profitability margin compel more farmers toward runner production and rapid shifting

tendency is noticed among farmers of upper swat and Dir areas. One acre of land produces

960,000 runners; each runner cost 0.6-0.7 Re for its entire life cycle and fetches more than 1

Re (average price this year was 1.4 per runner, however it varies between Re 1.2 and 3 per

runner; occasionally it was sold for Rs. 5 per runner last year due to shortage towards end

season. Consultations and triangulation confirms that more than 500 million runners were

channeled to Punjab, Sindh and Khyber Pakhtunkhwa this current season (it is believed that

around 1 billion runners will be available for marketing in the coming year).

The lease rate grows rapidly upward due to the same boom; the yearly rate was between

150,000 – 200,000 Rupees for an acre of land this season. Labor becomes expensive and not

available in strawberry extraction time (Rs. 12000/100,000 plants); usually farmers need to

extract more 300,000 plants on daily basis to subside demand. Contracted labor in Swat, while

women/children in Dir area are responsible for runners’ extraction from their fields in the

months of October-November. Runners quality from Swat has issues i.e. # of transplants in a

pack is not uniform, contain infertile runners, and mother plants. Runners from Upper Dir is

considered much better than Swat, runner growth is vigorous which result in better production

capacity, new land and high altitude to ensure chilling requirement of strawberry are few

important identified factors for this good quality.

Swat farmers fetch fruit and runners from the same plant, however farmer perceptions

revealed that plants not used for strawberry production has produced good quality runners.

Farmers of Charsadda are price conscious, and looking for cheaply available runners in

Swat/Dir, while Punjab/Sindh traders look for quality runners (vigorous growth), thus farmers

are willing to struck deals with Punjab and Sindh on priority basis and provided least quality

runners to farmers in Charsadda.

CHAPTER 4 – STRAWBERRY

12 | V a l u e C h a i n A n a l y s i s i n D i s t r i c t C h a r s a d d a

Apart from propagative material, local dealers are

providing range to remaining inputs like pesticides,

fertilizers and utensils in the production clusters.

Focused group discussion reveals that 70% farmers

are aware of pesticide usage from their previous

experience while 30% depend on the advice of input

providers. Lack of knowledge provides opening for

pesticide/fertilizer adulteration, subsequently

provide basis for the use in-efficient and sub-

standard chemicals. Majority of farmers (more than

90%) deals in credit for these agro-chemicals. The

risk associated with provided credit is another major

hurdle of not using good reputed pesticides; multinational products are available on cash only,

while generic products are available on credit to secure their market share. The institutional

capacity to maintain a robust check and balance is rather weak; hence quality of inputs

remains an issue of great concern.

Production/Post-Harvest Management

The production function encircles activities like land

preparation, transplantation, weeding, irrigation,

application of agro-chemicals, harvesting, and post-

harvest management. Crop rotation is practiced and

eventually desired in the strawberry management

cycle; extensive use of agro-chemicals has good

effects on succeeding crop.

Intensive management practices and high cost of

investment (PKR 50,000 seed money!) not allowing

to plan more than 2 acres of strawberry, the average

farm size of strawberry is reported between 2 kanal

and 2 acres of land each year while the usual practice

is 1-acre average in Charsadda. The practice is

realistic and is not much deviating from scientific

recommendation of 0.68 acres of strawberry as optimum farm size and realizing net revenue

from the crop (Afridi et al 2009).

Strawberry is a six-month crop, and crop cycle starts with procurement of runners in the month

of October, following land preparation. Sowing dates changed recently from November to the

month of October (farmer own testing on seasonal variation), though some farmers succeeded

in maintain a vigorous crop from early October plantation however mortality rate of seedling is

higher (heat factor) in early October plantation in district Charsadda. Majority of farmers are

reluctant to transplant early due to economic losses and managing runners for re-

transplantation. It offers prospects for further research trials on seasonal variation (early/late

cropping pattern) in district Charsadda. Strawberry is often inter-cropped with sugar cane in

Charsadda; extensive use of nutrients believed to have a better impact on sugar cane

production after the strawberry management cycle completed in late May. The same piece of

land is used for Kharif maize and fodder crops in the period between June-October. Wheat is

the preferred Rabi crop during November if land is not occupied by sugar cane. The crop

Figure 6: Ready to harvest Strawberry, the surface contact of fruit with soil devalues quality (Courtesy: ASF, PHRA 2012)

Figure 5: Input Dealer in Sarkee

CHAPTER 4 – STRAWBERRY

13 | V a l u e C h a i n A n a l y s i s i n D i s t r i c t C h a r s a d d a

rotation is believed to be a must-to-do practice in the case of strawberry. The choice of other

crops allows to maintain this healthy balance of crop rotation in 3 years’ cycle.

Farmers in Charsadda procured runners themselves from Swat and Dir rather in an inefficient

manner; 50-60% farmers visited Swat/Dir themselves while the remaining depend on

collective purchase and/or depending on traders for providing runners on farm gate for nominal

margins (recent development). Runner dealers bargain in cash only due to high demand and

payment issues with farmers; only few farmers deal on credit basis depending on mutual trust

and credibility.

Jute bags are used for transportation of Runners (contain 26,000-27,000 plants per 40 kg

bag); cleaning of runners and cutting of leaves is done at household level by children and

women. Transplantation period varies between October (early) and mid-November. Month of

December and January is dedicated exclusively to extensive hoeing cycles; it requires 7

hoeing cycles in these 2 months with intermittent irrigation and application of agro-chemicals.

Weedicides are not favored within strawberry crop therefore weeds are removed through

extensive hoeing cycles; this is rather in-efficient practice and incur extra cost of production.

Management practices in strawberry cultivation are rather static in Charsadda production belt;

farmers are learning management steps from each other however the mode of transformation

is not uniform and standard. Farmers even used pesticides and fertilizers without

understanding the fertility requirements of the crop in different soil. However, this learning and

doing did brought improvement in production capacity with the passage of time; production

capacity was 15-20 fruits per plant 20 years ago, improved to 30 fruits per plant 10 years ago,

while current production capacity is 50-60 fruits per plant with increased awareness and plant

growth regulators (humic acid, micronutrients application, increased fertilizer dosage and

range of pesticide application).

Strawberry is a water intensive crop; it need approximately 25 irrigation cycles in entire crop

production phase. Farmers tend to irrigate their strawberry field on every 3rd day during picking

season. However, research authenticates that 4-day interval might be good for fresh fruit

consumption, while irrigation interval of 10 days is appropriate for retaining quality during

storage and/or distant marketing. (Ijaz Akhtar and Abdur Rab, 20157).

Picking/harvesting starts from late January to early February (limited quantity), while peak

production harvested during mid-February to April continuously and diminished during the

month of May (production end till May 20 maximum). Harvesting was performed mainly

through school children, paying Rs 100 per day and also gave some strawberries for eating.

Though the practice is not efficient for post-harvest handling, the inexperience and

mishandling of such perishable crop by children resulted in 15-20% post-harvest losses.

MITES is the major crop problem in production stages, creates resistance towards extensive

use of pesticides (sprayed every 3rd day with miticide). Other common pest are nematodes,

cutworms, aphids and diseases like ‘damping-off’ is more common in Strawberry; attack of

wild boar was common in few areas but manageable with regular watch and ward.

7 “Effect of Irrigation Intervals on the Quality and Storage Performance of Strawberry Fruit”, Ijaz Akhter and Abdur Rab; The Journal of Animal & Plant Sciences, 25(3): 2015, Page: 669-678

CHAPTER 4 – STRAWBERRY

14 | V a l u e C h a i n A n a l y s i s i n D i s t r i c t C h a r s a d d a

MITES attack mostly in the month of March; an epidemic was witnessed in 2004-05 incurred

extensive losses to Strawberry crop in Charsadda. Mites has complicated life cycle and

nurturing overlapping generations (eggs, nymph, and adults at the same time), broad

spectrum pesticide might break the mites’ complex life cycle but it need further research trails.

Strawberry is prone to excessive rains during February – March; losses in rainy season are

40-50% of standing crop and also stressed production for the coming week to ten days’ period.

Complete failure of crop was recorded in 2006-07 due to hailstorm and extensive rainfall. No

protective measures are taken during rainy season, though the use of walk-in tunnels coupled

with weather forecast might save the crop from extensive damages during rainy season.

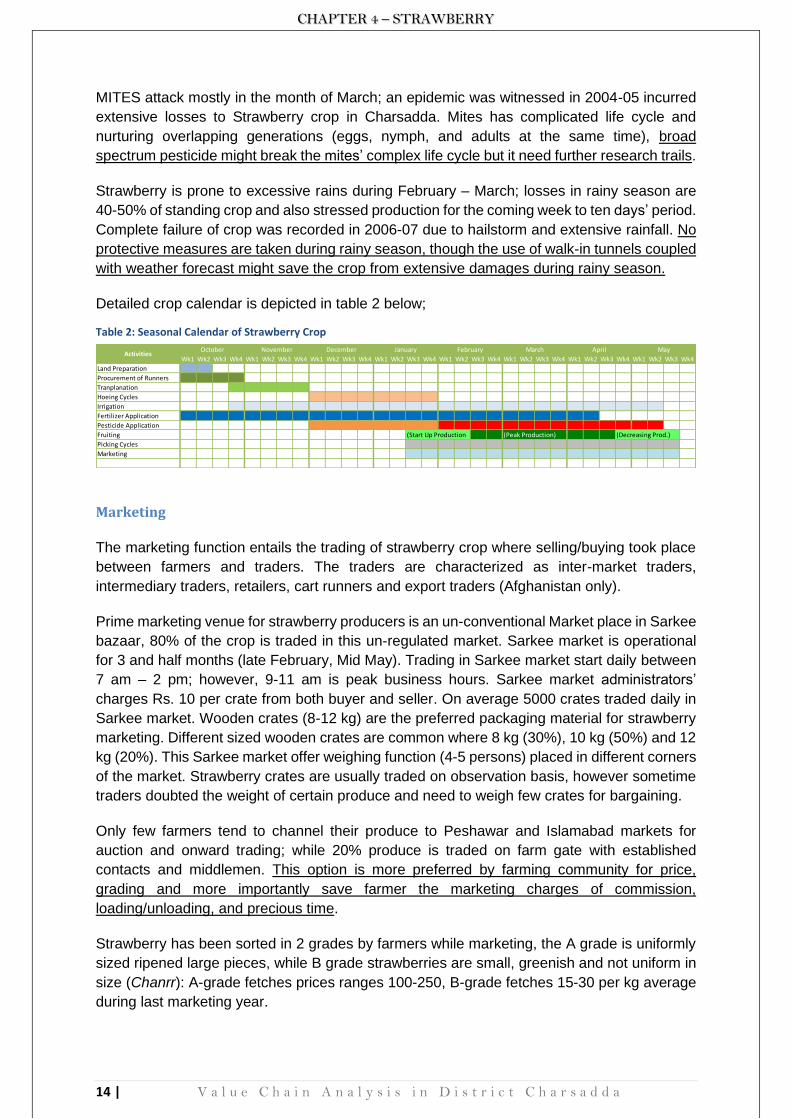

Detailed crop calendar is depicted in table 2 below;

Table 2: Seasonal Calendar of Strawberry Crop

Marketing

The marketing function entails the trading of strawberry crop where selling/buying took place

between farmers and traders. The traders are characterized as inter-market traders,

intermediary traders, retailers, cart runners and export traders (Afghanistan only).

Prime marketing venue for strawberry producers is an un-conventional Market place in Sarkee

bazaar, 80% of the crop is traded in this un-regulated market. Sarkee market is operational

for 3 and half months (late February, Mid May). Trading in Sarkee market start daily between

7 am – 2 pm; however, 9-11 am is peak business hours. Sarkee market administrators’

charges Rs. 10 per crate from both buyer and seller. On average 5000 crates traded daily in

Sarkee market. Wooden crates (8-12 kg) are the preferred packaging material for strawberry

marketing. Different sized wooden crates are common where 8 kg (30%), 10 kg (50%) and 12

kg (20%). This Sarkee market offer weighing function (4-5 persons) placed in different corners

of the market. Strawberry crates are usually traded on observation basis, however sometime

traders doubted the weight of certain produce and need to weigh few crates for bargaining.

Only few farmers tend to channel their produce to Peshawar and Islamabad markets for

auction and onward trading; while 20% produce is traded on farm gate with established

contacts and middlemen. This option is more preferred by farming community for price,

grading and more importantly save farmer the marketing charges of commission,

loading/unloading, and precious time.

Strawberry has been sorted in 2 grades by farmers while marketing, the A grade is uniformly

sized ripened large pieces, while B grade strawberries are small, greenish and not uniform in

size (Chanrr): A-grade fetches prices ranges 100-250, B-grade fetches 15-30 per kg average

during last marketing year.

Wk1 Wk2 Wk3 Wk4 Wk1 Wk2 Wk3 Wk4 Wk1 Wk2 Wk3 Wk4 Wk1 Wk2 Wk3 Wk4 Wk1 Wk2 Wk3 Wk4 Wk1 Wk2 Wk3 Wk4 Wk1 Wk2 Wk3 Wk4 Wk1 Wk2 Wk3 Wk4

Land Preparation

Procurement of Runners

Tranplanation

Hoeing Cycles

Irrigation

Fertilizer Application

Pesticide Application

Fruiting (Start Up Production (Peak Production) (Decreasing Prod.)

Picking Cycles

Marketing

November December January FebruaryActivities

March April MayOctober

CHAPTER 4 – STRAWBERRY

15 | V a l u e C h a i n A n a l y s i s i n D i s t r i c t C h a r s a d d a

Some farmers (5-6% approximately) are compelled to sold their produce at flowering stage,

the crop need to be taken care onwards by the traders with their own labor and management.

Some farmers tried to link their produce with high end markets and companies but the

experiment wasn’t successful because of un-clean strawberry produce (Key Informant).

Following the lucrative business of Sarkee strawberry market, at least 2 efforts have been

made by other business minded people to offer alternate market place for strawberry

marketing but couldn’t succeeded, as both farmers and traders don’t want to come out of their

comfort zone. A modern Pack house was built by ASF (USAID) in year 2014-15 with an idea

to offer improved packing/grading facilities, and linkages with high end markets; the facility is

yet to be operationalized to date as it is distantly located from the main market hub and also

have management issues.

Runners Marketing: There is no proper market for runners in Swat and Dir region; farmers,

middlemen and inter-provincial traders bargain with runner farmers directly in their farms and

rural hubs. The concept of farmer-cum-traders is expanding every year, where farmers not

only bargain for their own runner crop but also cut deals with other small and needy farmers

by offering some advance 2-3 months earlier than runners marketing. Exact estimates are not

available but it is believed that Swat produces more than 500 million runners this year; (350

million plus to Punjab, 100 million plus to Sindh, 50 million plus to Mardan and Charsadda);

Dir produces approximately 50-60 million runners this year; Runners marketing starts in

August-September each year; good prices and high demand compel farmers to convert more

land to strawberry runners, almost 1 billion plants are projected to be produced next year.

Inter-market traders channel strawberry to Peshawar, Islamabad, Lahore and other parts of

KP and Punjab; they used their own linkages for such trading, keeping some nominal

percentages of profit share (10-20 rupees’ margin after incurring expense).

Traders from Afghanistan has a positive effect on market prices, they not only purchase larger

quantities but also offer good prices. However, closure of Trade route to Afghanistan was a

major impediment in 2017, owing to stressed security relations between armed forces at both

end. This Closure has significant impact on market prices of fruits and vegetables in Pakistan

(especially on the products of KPK), more than half of vegetable export value is linked with

Afghanistan (52%), has a value of 91 million dollars8.

Processing

Range of products is available in the markets which are flavored/blended with strawberry

essence. Few renowned national companies are Mitchells, Rafhan Foods, TOPS, Salmans,

Shezan, Crispo, National Foods, Fauji Fresh-n- Freeze, while Lacnor and Kelloggs

(International) products are available on shelves. Jam, Jelly, Berry Crunch, Corn Flakes,

custard, frozen strawberry, topping, Juice (nectar), Syrup, and Squashes are strawberry

products range witnessed during supermarket visit (METRO). Pakistan is also importing frozen

strawberry from Mexico and USA i.e. in FY 2014-15 imported 8,540 kg with worth 1,766,000

PKR9. Frozen strawberry cost Rs 425/kg from a national company while imported quality of

the same product (Belgium) cost Rs 400/500 gm. Tarnab farm also purchase strawberry when

8 http://www.tdap.gov.pk/tdap-statistics.php 9 Ibid

CHAPTER 4 – STRAWBERRY

16 | V a l u e C h a i n A n a l y s i s i n D i s t r i c t C h a r s a d d a

price is lower than Rs 50 per kg (mostly B-grade quality) for processing in products like Jams

and Juices, they haven’t made products in 2017 due to higher prices of strawberry.

Though processing has been advocated as viable alternate option in fruits and vegetable,

especially keeping in view the risk associated with ups and down of market price. However,

processing industry prefers low grades and cheap prices traditionally, and often fulfills their

demand in peak production season. Artificial essence is more preferred option for these

industries, when it comes to strawberry products. The trend offer little prospect to farming

communities, however information lag demand for detailed research/feasibility on how

processing industry could be explored for the benefits of small holders. Moreover, further

analysis of respective market shares of processing industries in total supply of strawberry

produce, mapping of these units, and estimation of overall seasonal demand will further

elaborate their economic significance in networking and contract farming options with small

holders.

Figure 7: Some Processed Products of Strawberry in Super Market

Consumption