Embed Size (px)

Citation preview

China Connect Weekly

2018

Market StrategyMacro downturn reduces visibility

12 Nov 2018

Plea

se re

fer t

o th

e at

tach

men

t fo

r det

aile

d d

iscl

aim

er a

nd

reg

ula

tory

dis

clo

sure

s

Stock RecommendationsYunnan Tim Jinyu Bio-technology BYD China Railway Group

MacroeconomicsShort-term opportunities surfacing

csb.com.hk

CITIC Securities Brokerage (HK) LimitedInvestment Advisory ServicesTel:2237 9250E-mail:[email protected]

CompanyPrice

(Rmb)Target (Rmb)

Stop Loss (Rmb)

Upside (%)

Yunnan Tim (000960 CH)

10.63 18.00 10.1 69

Jinyu Bio-technology (600201 CH)

18.01 23.00 17.1 28

BYD (002594 CH)

50.00 62.00 47.5 24

China Railway Group (601390 CH)

7.29 8.60 6.9 18

MacroeconomicsShort-term opportunities

surfacingPolicy efforts are aiming at sustaining

infrastructure investment at a certain pace by

keeping projects in progress and fortifying

weak sectors. Among SOEs, leading developers,

power generators, railway and engineering

operators may present meaningful opportunities

for investors in the short term.

Macro downturn reduces visibility

Pick sectors least affected by the macro

downturn and volatility.

Market Strategy

2 12 Nov 2018

Please refer to the attachment for detailed disclaimer and regulatory disclosures.

Ch

ina

Con

nec

t W

eekl

y:M

acr

o dow

ntu

rn r

edu

ces

visi

bil

ity

Contents:

Source: Respective Company, CS

Weekly Top Pick

Yunnan Tim

3 12 Nov 2018

Please refer to the attachment for detailed disclaimer and regulatory disclosures.

Ch

ina

Con

nec

t W

eekl

y:M

acr

o dow

ntu

rn r

edu

ces

visi

bil

ity

Market strategy:

Sectors that were prev ious l y

believed to enjoy meaningfully

visible growth prospects are now –

to varying degrees – coming under

adverse macro pressure. These

include delivery, online booking,

property advertising and some giant

online retai l operators . As such,

look ing for high -growth shares

means looking for businesses that

have the least to do with macro

volatility. A retrospective study of

performances of sub-sectors and

their leaders in the two quarters prior

to the earnings bottom in three past

cycles shows that the following three

types of industries are better able

to withstand fluctuation when the

macro down-cycle nears the end: (i)

Sectors that are not highly cyclical in

nature; (ii) sectors whose own cycles

run independently from the macro

cycle; and (iii) sectors in the midst of

rapid penetration or scale expansion.

Based on 3Q18 result s and the

v iews of our indust r y analys t s ,

we recommend sectors boasting

relatively strong resilience over the

next 2-3 quarters: healthcare and

pharmaceuticals, defense, agriculture,

oilfield services, cloud computation,

enterprise IT services, 5G, duty-free

commerce, the new-energy industry

chain, health products within the

F&B sector and short-shelf-life bread/

pastry bakery.

Macro downturn reduces visibility

Sectors that are not highly cyclical in nature

Sectors whose own cycles run independently from the macro cycle

Sectors in the midst of rapid penetration or scale expansion

4 12 Nov 2018

Please refer to the attachment for detailed disclaimer and regulatory disclosures.

Ch

ina

Con

nec

t W

eekl

y:M

acr

o dow

ntu

rn r

edu

ces

visi

bil

ity

MaCroeConoMiCs:

Source: CS

Policymakers are endeavoring

t o s u s t a i n t h e g r o w t h o f

infrastructure investment at a certain

rate by supporting projects under

construct ion and strengthening

weak links. As personal mortgage

rates peak, investors may keep a

close watch on marginal pol icy

changes for the real estate industry,

as downstream segments along

this value chain diverge in terms of

business climate. Leading developers,

power generators, railway operators

and cons t r uc t ion f i r ms a t t he

central SOE level could present

remarkable oppor tuni t ies over

the short horizon, while property

management, water-proof material,

logistics and airport segments look

to promising long-term prospects. By

contrast, the fundamentals of other

infrastructure/property-related sub-

sectors (including environmental

protection, aviation and small/mid-

sized developers) are still murky.

Short-term opportunities surfacing

Source: Bloomberg, CS

CITIC S&P 50

(Index)

(Index)

5 12 Nov 2018

Please refer to the attachment for detailed disclaimer and regulatory disclosures.

Ch

ina

Con

nec

t W

eekl

y:M

acr

o dow

ntu

rn r

edu

ces

visi

bil

ity

Market review & teChiniCal:

2,6502,7002,7502,8002,8502,9002,9503,0003,0503,1003,1503,200

22/6

/18

27/6

/18

2/7/

185/

7/18

10/7

/18

13/7

/18

18/7

/18

23/7

/18

26/7

/18

31/7

/18

3/8/

188/

8/18

13/8

/18

16/8

/18

21/8

/18

24/8

/18

29/8

/18

3/9/

186/

9/18

11/9

/18

14/9

/18

19/9

/18

25/9

/18

28/9

/18

10/1

0/18

15/1

0/18

18/1

0/18

23/1

0/18

26/1

0/18

31/1

0/18

5/11

/18

8/11

/18

Market Review: On Monday, the

Shanghai and Shenzhen stock bourses

opened low. The broad market decline

steepened in the afternoon but eased

towards the end as brokerages and

insurers advanced. The Shanghai

Composite Index (SCI) closed off 0.41%.

On Tuesday, the two markets started

high to a weakening session. The

Shanghai gauge slipped 0.23%. On

Wednesday, the two exchanges jolted

upward in the morning and pulled

back after lunch. The SCI shed 0.68%.

On Thursday, both markets opened

high to hover at elevated levels before

heading south in the afternoon. The

SCI edged down 0.22%. On Friday,

the markets began from low and

remained uninspired, with the SCI

logging a 1.39% loss at the finish. In

the week, CITIC/S&P 50 and CITIC/S&P

300 fell 4.4% and 3.6%, respectively.

Technical analysis: The technical

trends of CITIC/S&P 50 and CITIC/

S&P 300 softened, leaving the two

stock gauges lingering near the bull-

bear border. The pair are expected to

fluctuate and consolidate in the near

term.

2,750

2,800

2,850

2,900

2,950

3,000

3,050

3,100

3,150

3,20022

/6/1

827

/6/1

82/

7/18

5/7/

1810

/7/1

813

/7/1

818

/7/1

823

/7/1

826

/7/1

831

/7/1

83/

8/18

8/8/

1813

/8/1

816

/8/1

821

/8/1

824

/8/1

829

/8/1

83/

9/18

6/9/

1811

/9/1

814

/9/1

819

/9/1

825

/9/1

828

/9/1

810

/10/

1815

/10/

1818

/10/

1823

/10/

1826

/10/

1831

/10/

185/

11/1

88/

11/1

8

Index 2,782.31

52-wk high/low 3,846.60/2,686.22

50/100/200D MA 3,294.8/3,397.8/3,465.1

RSI (14D) 49.6

MACD (12/26D)/Signal -10.08/-22.35

Index 2,869.26

52-wk high/low 3,852.92/2,804.88

50/100/200D MA 3,207.8/3,325.4/3,351.0

RSI (14D) 50.8

MACD (12/26D)/Signal 1.41/-4.98

CITIC S&P 300

6 12 Nov 2018

Please refer to the attachment for detailed disclaimer and regulatory disclosures.

Ch

ina

Con

nec

t W

eekl

y:M

acr

o dow

ntu

rn r

edu

ces

visi

bil

ity

stoCk reCoMMendations:

Source: Bloomberg, Respective Company, CS * Closing prices as of 9 Nov 2018

Risk Rating: 1 to 5 in ascending order

In 1H18, the new-energy segment ,

increas ing l y r ig id env i ronment a l

requirements and structural improvement

combined to drive up earnings of leading

plays in different sectors. But metal prices

have come under pressure enter ing

3Q18, which could curb earnings industry

leaders . T ightening env i ronment a l

regulat ions and the continuat ion of

supply -s ide reform are posi t i ves for

suppliers of basic metals such as copper

and aluminum. We recommend Yunnan

Tim (000960 CH).

Yunnan TinTarget Price: Rmb18 Upside: 69%

Potential rebound of industry leaders after excessive decline

Share Price Performance

8.58.89.19.49.7

10.010.310.610.9

18/9

/18

20/9

/18

25/9

/18

27/9

/18

8/10

/18

10/1

0/18

12/1

0/18

16/1

0/18

18/1

0/18

22/1

0/18

24/1

0/18

26/1

0/18

30/1

0/18

1/11

/18

5/11

/18

7/11

/18

9/11

/18

(Share price/Rmb)

Price/Target/Stop Loss 10.63/18.00/10.10

52 Weeks High/Low 16.67/8.79

50/100/200D MA 9.96/10.65/12.52

RSI (14D) 64.6

MACD (12/26D)/Signal 0.14/0.02

2017E PER (x) 13.5

Company: Yunnan Tin is engaged in the processes and export of non-ferrous metal products. The Company produces tin ingots, zinc, copper and lead products. It also conducts deep processing and trade businesses.

(A Shenzhen-HK Stock Connect Northbound Stock)

7 12 Nov 2018

Please refer to the attachment for detailed disclaimer and regulatory disclosures.

Ch

ina

Con

nec

t W

eekl

y:M

acr

o dow

ntu

rn r

edu

ces

visi

bil

ity

stoCk reCoMMendations:

Source: Bloomberg, Respective Company, CS * Closing prices as of 9 Nov 2018

Risk Rating: 1 to 5 in ascending order

BYD (002594 CH) has sped up the

launch of new models since the

start of 3Q18. In the short-to-medium

term, the new-energy vehicle industry

is a rare sector that its high season falls

in the second half of the year. Kicking

of f a new cycle, the Company could

see sales volume hitting new records,

bringing about considerable earnings

improvement. We expect it to report

markedly buoyant performances going

forward. In the long run, the strategy

to neutralize power battery production

could open up room for future growth.

The advance of BYD’s

D + + e c o s y s t e m i s

tipped to push capacity

boundaries and provide

fuel to the Company

as it dives into the new

blue ocean of smart EV.

Ji n y u B i o -Te c h n o l o g y (6 0 02 01

CH) boast s leadership in vaccine

product ion process and market ing

channels. The sector will bottom out in

the short term and its long-term prospects

appear upbeat. The launch of FMD OA

bivalent vaccine is helping the Company

to regain market share. Meanwhile, the

Company has built a tiered matrix of

non-compulsory swine vaccines as it

picks up the pace

to transform into a

leading player in the

international market

for animal health

so lut ions . We set

target at Rmb23 per

share and suggest

investors follow the

stock.

Jinyu Bio-TechnologyTarget Price: Rmb23 Upside: 28 %

Accelerating shift towards a global leader in animal health solutions

BYDTarget Price: Rmb62 Upside: %A promising last quarter

BYDTarget Price: Rmb62 Upside: 24%A promising last quarter

(A Shanghai-HK Stock Connect Northbound Stock)

(A Shenzhen-HK Stock Connect Northbound Stock)

Share Price Performance

42434445464748495051

18/9

/18

20/9

/18

25/9

/18

27/9

/18

8/10

/18

10/1

0/18

12/1

0/18

16/1

0/18

18/1

0/18

22/1

0/18

24/1

0/18

26/1

0/18

30/1

0/18

1/11

/18

5/11

/18

7/11

/18

9/11

/18

(Share price/Rmb)

Price/Target/Stop Loss 50.0/62.0/47.5

52 Weeks High/Low 72.79/37.29

50/100/200D MA 46.01/45.04/51.54

RSI (14D) 59.4

MACD (12/26D)/Signal 0.66/0.59

2017E PER (x) 45.5

C o m p a n y : B Y D , t h r o u g h i t s s u b s i d i a r i e s , manufactures and sells automobiles. The Company also researches, develops, manufactures and sells batteries, which are applied on mobile phones, cordless phones, power tools and other kinds of portable electronic devices.

Share Price Performance

14.014.515.015.516.016.517.017.518.018.519.0

18/9

/18

20/9

/18

25/9

/18

27/9

/18

8/10

/18

10/1

0/18

12/1

0/18

16/1

0/18

18/1

0/18

22/1

0/18

24/1

0/18

26/1

0/18

30/1

0/18

1/11

/18

5/11

/18

7/11

/18

9/11

/18

(Share price/Rmb)

Price/Target/Stop Loss 18.01/23.00/17.10

52 Weeks High/Low 24.454/14.350

50/100/200D MA 16.22/16.13/18.52

RSI (14D) 60.2

MACD (12/26D)/Signal 0.53/0.49

2017E PER (x) 20.9

Company: Jinyu Bio - technology manufactures and markets biopharmaceuticals for animals and cashmere products. The Company also produces linseed oil and invests in real estate development business.

8 12 Nov 2018

Please refer to the attachment for detailed disclaimer and regulatory disclosures.

Ch

ina

Con

nec

t W

eekl

y:M

acr

o dow

ntu

rn r

edu

ces

visi

bil

ity

stoCk reCoMMendations:

The infrastructure sector as a whole

has come under pressure due to

multiple factors, including deleveraging,

slowing investment and PPP regulations.

Su b - s e c to r s f a re d i f f e re n t l y, w i t h

private firms seeing their fundamentals

deteriorate more quickly than their SOE

peers. Given such positives as (i) concrete

measures to fortify weak links and sustain

progress at in-construction projects, (ii)

stabilizing financing and (iii) expectations

of an infrastructure investment rebound,

we believe the sector will bottom up

soon. As it takes time for loan recovery to

materialize at the company-level, central

SOEs in the construction industry are

likely to be ahead of others in getting

the benefits of increased financing. We

recommend those SOEs

w i th v i s ib le earn ings

outlook and the potential

to be the f irst to gain

f rom improvement in

f inancing. Our top pick

is China Railway Group

(601390 CH).

China Railway Group Target Price: Rmb8.6 Upside: 18%

The first to benefit from better financing

(A Shanghai-HK Stock Connect Northbound Stock)

Share Price Performance

7.0

7.2

7.4

7.6

7.8

8.0

8.2

18/9

/18

20/9

/18

25/9

/18

27/9

/18

8/10

/18

10/1

0/18

12/1

0/18

16/1

0/18

18/1

0/18

22/1

0/18

24/1

0/18

26/1

0/18

30/1

0/18

1/11

/18

5/11

/18

7/11

/18

9/11

/18

(Share price/Rmb)

Price/Target/Stop Loss 7.29/8.60/6.90

52 Weeks High/Low 9.05/6.96

50/100/200D MA 7.39/7.43/8.03

RSI (14D) 44.9

MACD (12/26D)/Signal -0.01/-0.01

2017E PER (x) 10.1

Company: China Railway Group offers transportation facility construction services. The Company builds railways, roads, tunnels and bridges. China Railway Group also conducts engineering survey, equipment manufactur ing, real es tate development and investment.

Source: Bloomberg, Respective Company, CS * Closing prices as of 9 Nov 2018

Risk Rating: 1 to 5 in ascending order

9 12 Nov 2018

Please refer to the attachment for detailed disclaimer and regulatory disclosures.

Ch

ina

Con

nec

t W

eekl

y:M

acr

o dow

ntu

rn r

edu

ces

visi

bil

ity

China/HK Stocks(50%)

US Stocks(10%)

Euro Stocks(5%)

Japan Stocks(8%)

Emerging Markets(2%)

Global ETF(10%)

Cash15%

Recommended global asset allocation (GAA)

Global Asset Allocation

Source: Bloomberg, Respective Company, CS

Hong Kong: Relatively undemanding stock valuation; potential benefit of “Shenzhen-Hong Kong Stock Connect” to small caps

Mainland China: Government preference for a “slow bull market”; relaxed fiscal policy in favor of equities

Japan: Real estates, exports and tourism enjoying monetary easing and weak yen

US: Macro stability and recovery; short-term pressure stemming from rate rise and strong USD

Europe: Stock valuation falling due to weak euro and further quantitative ease

The Philippines: Positive current account balance for over a decade; projected GDP growth of 6.8% in 2016E

India: Relatively strong growth versus other emerging markets; projected GDP growth of 8% in 2016E

Selected equity markets at a glance

10 12 Nov 2018

Please refer to the attachment for detailed disclaimer and regulatory disclosures.

Ch

ina

Con

nec

t W

eekl

y:M

acr

o dow

ntu

rn r

edu

ces

visi

bil

ity

China/Hong Kong StocksCompany Remarks

Realcan Pharm (002589 CH) Medical equipment distribution across the nation

Wellhope Agri-Tech (603609 CH) Wider margins in animal feed and upbeat growth in slaughter and trade

Dabeinong (002385 CH) Warming industry climate and growth-driving strategy

Huace Film & TV (300133 CH) Continued progress in SIP operations and promising VR content investment

Alpha Animation (002292 CH) Entering the baby/toddler market upon acquisition of BT and Jinwang

Kweichow Moutai (600519 CH) Steady and superb

CR Land (1109 HK) Benefiting from rate/RRR cuts + projects in top-tier cities

BOCHK (2388 HK) Revenue growth momentum: Top pick among local lenders

Zoomlion (1157 HK) A late-cycle equipment maker stands to win

Haitong Sec. (6837 HK) Gaining from IPO re-launch and rebounding A-share market turnover

Eastern Airlines (670 HK) To ride on Shanghai Disney and Beijing Winter Olympics

Tencent (700 HK) WeChat user experience significantly enhanced on subscription improvement

Mengniu Dairy (2319 HK) New products to drive up income and margins

CCB (939 HK) Outstanding spread and relatively mild impact from IFRS 9

Japan StocksCompany Remarks

Mizhuho (8411 JP) Expanding overseas portfolio remains the key driver

Nissan Motor (7201 JP) Robust sales, favorable currency, further cost cutting

Sony (6758 JP) Growth story continues...

US StocksCompany Remarks

Facebook (FB US) Strong products

Citigroup (C US) Economic growth and interest rate rise to support earnings

Alphabet (GOOG US) Positive data on page view

Euro StocksCompany Remarks

Adidas (ADS GY) Upbeat industry climate

Zurich Insurance (ZURN VX) High dividend yield

LVMH (MC FP) Gain from weak €

Global ETF / ETNName Remarks

Tracker Fund of HK (2800 HK) To track the performance of the Hang Seng Index

CSOP Hang Seng Index Daily (2x) Leveraged Product (7200 HK) To track the daily performance of Hang Seng Index (2x leverage)

CSOP Hang Seng H-Shares Index Daily (2x) Leveraged Product (7288 HK) To track the daily performance of Hang Seng H-Shares Index (2x leverage)

CSOP Hang Seng Index Daily (-1x) Inverse Product (7300 HK) To track the daily performance of Hang Seng Index (inverse 1x leverage)

CSOP Hang Seng H-Shares Index Daily (-1x) Inverse Product (7388 HK) To track the daily performance of Hang Seng H-Shares Index (inverse 1x leverage)

ChinaAMC Hang Seng SmallCap Index (3157 HK) To track the performance of the Hang Seng SmallCap Index

ChinaAMC CSI 300 Index (3188 HK) To track the performance of the CSI 300 Index

Powershares QQQ Trust Series 1 (QQQ US) To track the performance of the Nasdap 100 Index (Excluded Financial Sector)

PowerShares DB Commodity Index Tracking ETF (DBC US) To track the performance of the DBIQ Optimum Yield Diversified Commodity Index

XIE Shares FTSE Chimerica (3161 HK) To track the performance of the FTSE China N Shares All Cap Capped Net Tax Index

Deutsche X-Trackers MSCI Eur (DBEU US) To track the performance of the MSCI Europe USD Hedged Index

Deutsche X-Trackers MSCI Jap (DBJP US) To track the performance of the MSCI Japan US Dollar Hedged Net Index

iShares MSCI Philippines (EPHE US) To track the performance of the MSCI Philippines Investable Market Index

iShares MSCI India (INDA US) To track the performance of the MSCI India Index

SPDR Gold ETF (2840 HK) To track the performance of the price of gold bullion in COMEX

Value Gold ETF (3081 HK) To track the performance of the London Gold Morning Fixing Price

CSOP WTI OIL ETF (3135 HK) To track the performance of the Merrill Lynch Commodity index eXtra CLA Index ER

Source: Bloomberg, Respective Company, CS

Top GAA picks

11 12 Nov 2018

Please refer to the attachment for detailed disclaimer and regulatory disclosures.

Ch

ina

Con

nec

t W

eekl

y:M

acr

o dow

ntu

rn r

edu

ces

visi

bil

ity

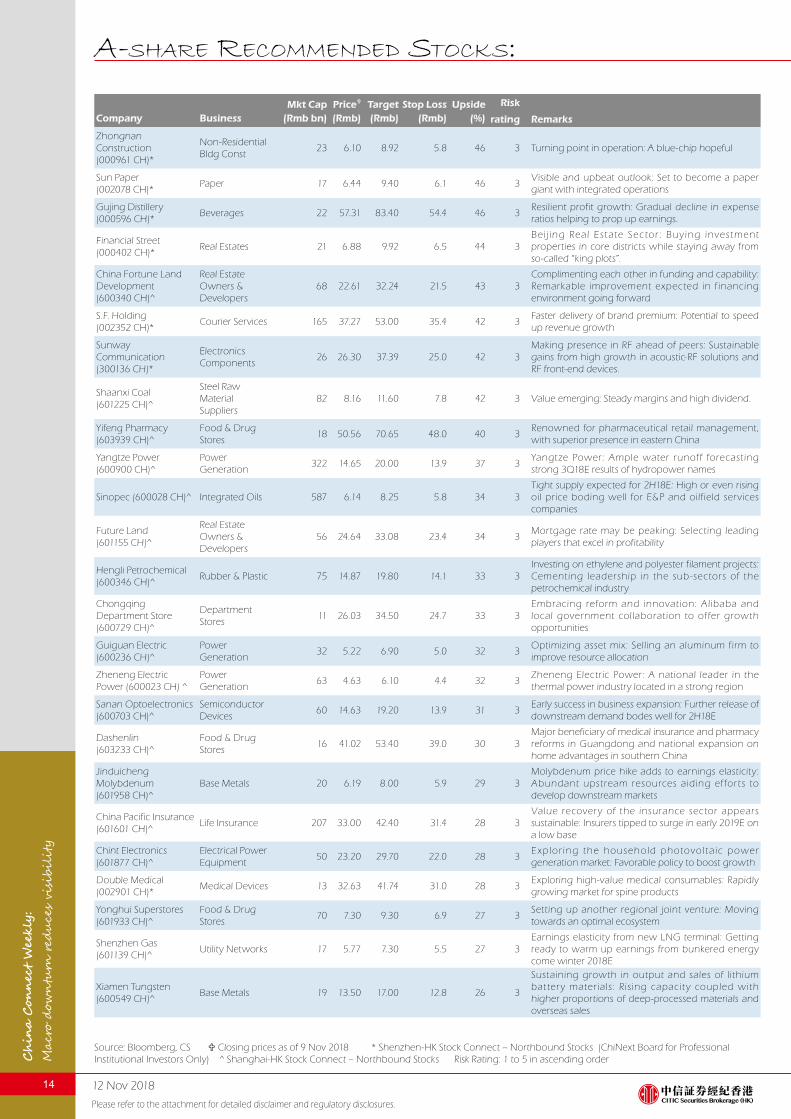

a-share reCoMMended stoCks:

Defensive StockSMkt Cap PriceU Target Stop Loss Upside Risk

Company Business (Rmb bn) (Rmb) (Rmb) (Rmb) (%) rating Remarks

Great Wall Motors (601633 CH)^ Automobiles 37 6.21 15.00 5.9 142 3

Beating market expectations: launching of new models and new powertrain will optimize its product mix and help improve profitability outlook.

Bank of Beijing (601169 CH)^

Banks 127 6.00 11.50 5.7 92 3Aggressive and resil ient at the same time: Solid financials poised for growth, backed by safe assets and quality clients

China United Network (600050 CH)^

Telecom 167 5.37 9.14 5.1 70 3The approaching 5G era: transformation and profit rebound on SOE reform

Baiyun International Airport (600004 CH)^

Transport Support Services

20 9.87 16.00 9.4 62 3

More duty free operation tipped to ease T2 impact: Contribution from arrival duty free business revenue plus more departure duty free sales to offset new capacity cost

Tielong Container Logistics (600125 CH)^

Rail Freight 10 7.63 11.60 7.2 52 3Enhanced ef fect of the highway-to-railway shif t: Unique core business of container shipping plus rising volume and price on the Shaba line

Daqin Railway (601006 CH)^

Rail Transportation

120 8.06 12.00 7.7 49 3Enhanced ef fect of the highway-to-railway shif t: A rare investment vehicle to the west-to-east coal shipping, featuring attractive valuation and dividend

Sany Heavy Industry (600031 CH)^

Construction & Mining Machinery

63 8.02 11.82 7.6 47 3Still better performance ahead: Sales volume tipped to rise, leading to wider margins

Bank of Nanjing (601009 CH)^

Banking Services 60 7.03 10.10 6.7 44 3Active expansion: A better-than-expected first half thanks to scale expansion; capital replenishment a positive response to business model.

SZ Expressway (600548 CH)^

Infrustructure Construction

11 8.02 10.80 7.6 35 3

Strengthening core while seeking transformation: Net cash of Rmb3bn upon repurchase of three toll roads will be used to consolidate main business and facilitate transformation

Zhejiang Dingli (603338 CH)^

Construction & Mining Machinery

13 54.32 61.82 51.6 14 3Building up f irs t-mover edge through mult iple dimensions: New articulating lifts to buoy up income next year

Aggressive StockSMkt Cap PriceU Target Stop Loss Upside Risk

Company Business (Rmb bn) (Rmb) (Rmb) (Rmb) (%) rating Remarks

Xinjiang Tianye (600075 CH)^

Basic & Diversified Chemicals

5 4.74 19.49 4.5 311 3Prices of chemicals tipped to remain elevated: Prices likely to hike further on re-stocking, providing drive to sector earnings growth

NBTM New Materials (600114 CH)

Auto Parts 4 6.83 24.80 6.5 263 3Riding on new powder metallurgical technology: High value-added products securing profitability

Yibai Pharmaceutical (600594 CH)^

Generic Pharma 5 6.18 22.40 5.9 262 3A new healthcare arm to integrate tumor treatment resources: Speeding up resource consolidation and looking to set up shops across the nation

Qingdao Kingking (002094 CH)*

Basic & Diversified Chemicals

4 5.26 16.60 5.0 216 3New retail a key growth driver in 2018E: Planning to erect 10,000 pilot stores practicing new retail

Hengtong Optic Electric (600487 CH)^

Optical fiber and cables

34 17.67 55.75 16.8 216 3Anticipating more pleasant surprises ahead: All lines of businesses set to ride on the upbeat industry climate.

Yunnan Germanium (002428 CH)*

Base Metals 4 5.40 16.50 5.1 206 3Explosive demand spells opportunity: Upgrading products and investing in high-end manufacturing

Xinhua Pharmaceutical (000756 CH)*

Specialty Pharma 3 6.36 18.13 6.0 185 3Multi-dimensional re-rating: Accelerating growth in preparation and hiking price for preparation

Jianghuai Automobile (600418 CH)^

Automobile 9 4.56 12.00 4.3 163 3Volkswagen JV approved: A win-win deal for both parties

Huayou Cobalt (603799 CH)^

Base Metals 31 37.13 90.00 35.3 142 3Continuous catalysts for the NEV sector: Optimistic long-term visibility

Focus Media (002027 CH)*

Advertising & Marketing

84 5.72 13.80 5.4 141 3Dominating the out-of-home advertising scene: Building advertising to expand steadily and cinema advertising to surge

Source: Bloomberg, CS U Closing prices as of 9 Nov 2018 * Shenzhen-HK Stock Connect – Northbound Stocks (ChiNext Board for Professional Institutional Investors Only) ^ Shanghai-HK Stock Connect – Northbound Stocks Risk Rating: 1 to 5 in ascending order

12 12 Nov 2018

Please refer to the attachment for detailed disclaimer and regulatory disclosures.

Ch

ina

Con

nec

t W

eekl

y:M

acr

o dow

ntu

rn r

edu

ces

visi

bil

ity

a-share reCoMMended stoCks:

Mkt Cap PriceU Target Stop Loss Upside Risk

Company Business (Rmb bn) (Rmb) (Rmb) (Rmb) (%) rating Remarks

Grand Auto (600297 CH)^

Agricultural Chemicals

36 4.36 10.50 4.1 141 3Driven by auto financing and second-hand car sales: China’s largest car dealer aiming at top-of-the-world rank

Tasly Pharma (600535 CH)^

Specialty Pharma 33 21.80 52.15 20.7 139 3Top-tier drug R&D: Core biological drug Pro-UK looking to be a new blockbuster

Grandland (002482 CH)*

Non-Residential Bldg Const

8 5.10 12.00 4.8 135 3Launching employee stock ownership plan: ESOP to fuel endogenous growth

COFCO Biochemical (000930 CH)*

Biofuels 8 8.10 18.90 7.7 133 3Cementing leadership in corn deep-processing: Rising oil prices to boost revenue of fuel ethanol business

CNHTC (000951 CH)*Commercial Vehicles

7 10.81 25.00 10.3 131 3

Expecting high growth for heavy truck sector in 1H18E: improving competit ion landscape of the industry helps leading players to register significantly improvement in earnings.

Chilong Zinc & Germanium (600497 CH) ^

Base Metals 22 4.32 9.50 4.1 120 3Benefiting from price hike potentials: Entering an up-cycle for explosive earnings growth

CYTS Tours (600138 CH)^

Tourism Services 10 13.80 29.80 13.1 116 3Earnings poised to pick up next year: Price hike for Wuzhen and strong income from Gubei

China Meheco (600056 CH)^

Healthcare Supply Chain

15 14.17 29.80 13.5 110 4

An emerging integrated platform: One of the few Chinese companies that have already established diversified operations including manufacturing, sales and international trade.

Guangshen Railway (601333 CH)^

Transit Services 17 3.05 6.40 2.9 110 3Picking up steam on reform: Faster railway reform expected to boost earnings

Luzhou Laojiao (000568 CH)*

Beverages 57 38.97 80.50 37.0 107 3Four-pronged reform: Long-term outlook improving on dynamic execution with product, channel, brand and management reforms

Weichai Power (000338 CH)*

Commercial Vehicles

45 7.41 15.00 7.0 102 3

Expecting high growth for heavy truck sector in 1H18E: improving competit ion landscape of the industry helps leading players to register significantly improvement in earnings.

Truchum Advanced Materials (002171 CH)*

Base Metals 5 5.02 10.10 4.8 101 3Skewing towards new materials: Developing new materials a part of national strategy

China Molybdenum (603993 CH) ^

Base Metals 73 4.12 8.20 3.9 99 3Molybdenum sector rebound expected: Further price hike against disrupted supply

Huangshan Tourism (600054 CH)^

Real Estate Owners & Developers

5 9.76 19.20 9.3 97 3Better-than-expected 1Q16 results: Strong tourist flow sustainable, cost reduction effective and profitability enhanced.

Broad-Ocean Motor (002249)*

Industrial Machinery

8 3.44 6.50 3.3 89 3New era of clean and efficient energy: A key player in the core section of the fuel cell chain

Wuliangye (000858 CH)*

Beverages 194 50.01 93.80 47.5 88 3

Mixed-ownership reform to boost OP efficiency: The private placement will likely align the interests of the management and distributors with the Company, and thus improve the operational efficiency.

Greenland (600606 CH)^

Real Estate Services

74 6.08 11.40 5.8 88 3Gross margin upturn as expected: Moderate increase in real estate income, coupled with significantly wider margins

Huadong Medicine (000963 CH)*

Medicines Retailing

55 37.55 70.16 35.7 87 3Innovative diabetes drug approved for clinical trial: New diabetes medicine approved and coming to the market circa 2021E

Sinoma International (600970 CH)^

Industrial Distribution & Rental

10 5.65 10.35 5.4 83 3Across-the-board synergy on M&A deal to widen margins and lead to a profit upturn

Yang Quan Coal (600348 CH)^

Coal Operations 13 5.55 10.05 5.3 81 3Hit t ing the sweet spot : Warmer- than-expected industry climate and increasingly clear earnings visibility

O-film Tech (002456 CH)*

Electronics Components

34 12.40 22.44 11.8 81 3Sensing the future: To be driven by market expansion on dual camera and OLED technology advancement and increasing number of major clients

Yunnan Copper (000878 CH)*

Base Metals 12 8.36 15.00 7.9 79 3Rationale for copper price hike: Picking stocks with resource edge, potential capacity expansion, earnings elasticity, M&A plans and sustainable operation

SDIC Power (600886 CH)^

Power Generation

51 7.45 13.20 7.1 77 3Approaching season of power shortage: Pick thermal power companies in high-demand regions

Linglong Tyre (601966 CH)^

Auto Parts 17 14.18 25.00 13.5 76 3Pumping up: Potential to become a tier-2 international brand and one of the global top 10 tire makers

Source: Bloomberg, CS U Closing prices as of 9 Nov 2018 * Shenzhen-HK Stock Connect – Northbound Stocks (ChiNext Board for Professional Institutional Investors Only) ^ Shanghai-HK Stock Connect – Northbound Stocks Risk Rating: 1 to 5 in ascending order

13 12 Nov 2018

Please refer to the attachment for detailed disclaimer and regulatory disclosures.

Ch

ina

Con

nec

t W

eekl

y:M

acr

o dow

ntu

rn r

edu

ces

visi

bil

ity

a-share reCoMMended stoCks:

Mkt Cap PriceU Target Stop Loss Upside Risk

Company Business (Rmb bn) (Rmb) (Rmb) (Rmb) (%) rating Remarks

Satellite Petrochemical (002648 CH)*

Chemicals 11 10.30 18.00 9.8 75 3Rebounding climate: Recovering demand for acrylic acid and ester, sanguine prospects in SAP.

Shanghai Mech & Elect (600835 CH)^

Elevator 12 15.10 26.16 14.3 73 3Smart equipment platform established: The Company may serve as platform for parent to float more quality assets going forward.

Wangfujing (600859 CH)^

Department Stores

11 14.18 24.50 13.5 73 3Riding on high-end consumption recovery: Exploring supermarket and premium store formats via joint ventures

Jiangxi Copper (600362 CH)^

Base Metals 28 13.29 22.80 12.6 72 3Rationale for copper price hike: Picking stocks with resource edge, potential capacity expansion, earnings elasticity, M&A plans and sustainable operation

Chuangxin New Material (002812 CH)*

Containers & Packaging

20 41.90 71.60 39.8 71 3First-mover advantage: Cutting into battery supply chain abroad to embrace explosive growth in 2018-19E orders

Yunnan Tim (000960 CH)*

Base Metals 18 10.63 18.00 10.1 69 3Potential rebound of industry leaders after excessive decline: Stricter environmental rules and further reform boding well for basic metals

Yinlun Machinery (002126 CH) *

Auto Parts 6 7.39 12.50 7.0 69 3Continuous catalysts for the NEV sector: Optimistic long-term visibility

Gree Electric (000651 CH)*

Air-con 232 38.64 64.50 36.7 67 3Getting smart: Transition into an intelligent appliances era with volume and price rising in tandem

CCB (601939 CH) ^ Banks 64 6.72 11.20 6.4 67 3Optimizing asset structure: Steady operation and good asset quality

Sunlord Electronics (002138 CH)*

Electrical Components

12 14.50 24.00 13.8 66 3L ikely breakthrough in appl icat ion of ceramic components: Use of ceramic parts to dif ferentiate mobile phones.

Vanke (000002 CH)*Real Estate Owners & Developers

229 23.55 38.51 22.4 64 3Investment cues for anticipated rebound: Potential rebound of property counters on easing concern over funding cost

Yili (600887 CH)^ Dairy products 139 22.87 36.70 21.7 60 3Beginning of a beautiful story: Faster growth ahead on recovering demand in lower-tier cities, regulatory approval and channel restocking

BTG Hotels (600258 CH)^

Leisure & Travel Services

17 17.14 27.50 16.3 60 3New incent i ve scheme to un leash potent ia l : Expecting strong earnings rebound in the short run

Three-Circle (300408 CH)*

Advanced Ceramics

32 18.48 29.12 17.6 58 3Expert electro ceramics maker upgrading business structure and looking to promising future with new products

Ninestar (002180 CH)*Power Generation

28 26.30 41.42 25.0 57 3

A dawning golden decade for semiconductor plays: China-US trade dispute to reinforce Chinese determination to replace imports with home-made products

Shanghai Jahwa (600315 CH)^

Household Products

17 25.54 40.00 24.3 57 3Rapid revenue growth on brands appealing to young consumers: Accelerating new product launches and robust digital operations

ABC (601288 CH)^ Banking Services 1,165 3.65 5.70 3.5 56 3Healthy growth drivers: Expecting upbeat results for the next quarter

CMSK (001979 CH)*Investment Companies

140 17.73 26.72 16.8 51 3Mortgage rate may be peaking: Selecting leading players that excel in profitability

China South Publishing & Media (601098 CH)^

Media 21 11.76 17.72 11.2 51 3Deserving richer valuation: A much undervalued stock seeing catalysts emerging on the upside

SAIC Motor (600104 CH)^

Automobiles 318 27.22 41.00 25.9 51 3Speculating on measures to boost car sales: Potential policy to stimulate auto consumption after continuous decline in sales

CMB (600036 CH)^ Banking Services 590 28.60 43.00 27.2 50 3Steady growth: Consolidating retail base and leaning towards asset management

Xingrong Environment (000598 CH)*

Utility Networks 13 4.23 6.30 4.0 49 3Anticipating faster growth on mixed-ownership reform: Progress in reform to exert impact far and wide

CRCC (601186 CH)^Infrastructure Construction

122 10.64 15.70 10.1 48 3Wait for infrastructure stocks to bottom out on policy: Less demanding share prices and wider margin of safety

Industrial Bank (601166 CH)^

Banking Services 326 15.68 23.00 14.9 47 3Freeing up excess reserve to smooth volat i l i t y : Moderate improvement in f inancia l data and accommodating new rules for reserves .

Fosun Pharma (600196 CH)^

Pharmaceutical 55 27.51 40.32 26.1 47 3Pocketing a rare gem: Adding a Shenzhen hospital to form a strong healthcare network in the Pearl River Delta

Source: Bloomberg, CS U Closing prices as of 9 Nov 2018 * Shenzhen-HK Stock Connect – Northbound Stocks (ChiNext Board for Professional Institutional Investors Only) ^ Shanghai-HK Stock Connect – Northbound Stocks # Sell Only Risk Rating: 1 to 5 in ascending order

14 12 Nov 2018

Please refer to the attachment for detailed disclaimer and regulatory disclosures.

Ch

ina

Con

nec

t W

eekl

y:M

acr

o dow

ntu

rn r

edu

ces

visi

bil

ity

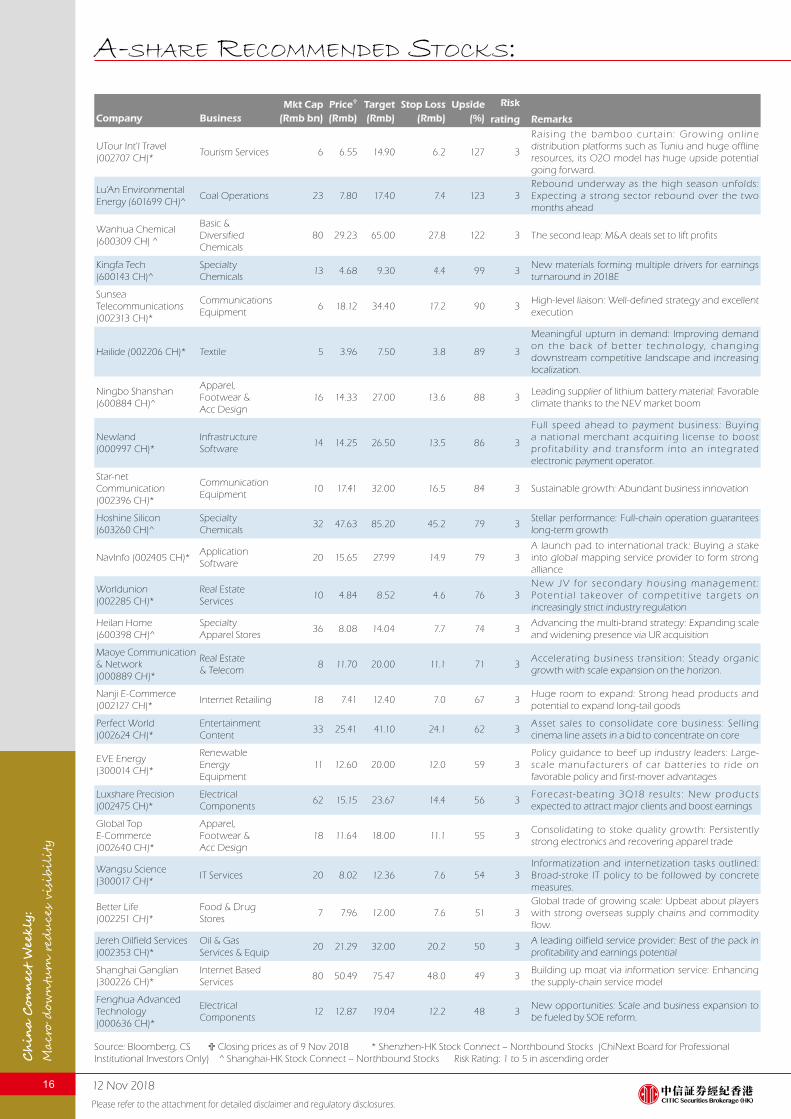

a-share reCoMMended stoCks:

Mkt Cap PriceU Target Stop Loss Upside Risk

Company Business (Rmb bn) (Rmb) (Rmb) (Rmb) (%) rating Remarks

Zhongnan Construction (000961 CH)*

Non-Residential Bldg Const

23 6.10 8.92 5.8 46 3 Turning point in operation: A blue-chip hopeful

Sun Paper (002078 CH)*

Paper 17 6.44 9.40 6.1 46 3Visible and upbeat outlook: Set to become a paper giant with integrated operations

Gujing Distillery (000596 CH)*

Beverages 22 57.31 83.40 54.4 46 3Resilient profit growth: Gradual decline in expense ratios helping to prop up earnings.

Financial Street (000402 CH)*

Real Estates 21 6.88 9.92 6.5 44 3Bei j ing Real Es tate Sector : Buy ing inves tment properties in core districts while staying away from so-called “king plots”.

China Fortune Land Development (600340 CH)^

Real Estate Owners & Developers

68 22.61 32.24 21.5 43 3Complimenting each other in funding and capability: Remarkable improvement expected in f inancing environment going forward

S.F. Holding (002352 CH)*

Courier Services 165 37.27 53.00 35.4 42 3Faster delivery of brand premium: Potential to speed up revenue growth

Sunway Communication (300136 CH)*

Electronics Components

26 26.30 37.39 25.0 42 3Making presence in RF ahead of peers: Sustainable gains from high growth in acoustic-RF solutions and RF front-end devices.

Shaanxi Coal (601225 CH)^

Steel Raw Material Suppliers

82 8.16 11.60 7.8 42 3 Value emerging: Steady margins and high dividend.

Yifeng Pharmacy (603939 CH)^

Food & Drug Stores

18 50.56 70.65 48.0 40 3Renowned for pharmaceutical retail management, with superior presence in eastern China

Yangtze Power (600900 CH)^

Power Generation

322 14.65 20.00 13.9 37 3Yangtze Power: Ample water runof f forecasting strong 3Q18E results of hydropower names

Sinopec (600028 CH)^ Integrated Oils 587 6.14 8.25 5.8 34 3Tight supply expected for 2H18E: High or even rising oil price boding well for E&P and oilf ield services companies

Future Land (601155 CH)^

Real Estate Owners & Developers

56 24.64 33.08 23.4 34 3Mortgage rate may be peaking: Selecting leading players that excel in profitability

Hengli Petrochemical (600346 CH)^

Rubber & Plastic 75 14.87 19.80 14.1 33 3Investing on ethylene and polyester filament projects: Cementing leadership in the sub-sectors of the petrochemical industry

Chongqing Department Store (600729 CH)^

Department Stores

11 26.03 34.50 24.7 33 3Embracing reform and innovation: Alibaba and local government collaboration to of fer growth opportunities

Guiguan Electric (600236 CH)^

Power Generation

32 5.22 6.90 5.0 32 3Optimizing asset mix: Selling an aluminum firm to improve resource allocation

Zheneng Electric Power (600023 CH) ^

Power Generation

63 4.63 6.10 4.4 32 3Zheneng Electric Power: A national leader in the thermal power industry located in a strong region

Sanan Optoelectronics (600703 CH)^

Semiconductor Devices

60 14.63 19.20 13.9 31 3Early success in business expansion: Further release of downstream demand bodes well for 2H18E

Dashenlin (603233 CH)^

Food & Drug Stores

16 41.02 53.40 39.0 30 3Major beneficiary of medical insurance and pharmacy reforms in Guangdong and national expansion on home advantages in southern China

Jinduicheng Molybdenum (601958 CH)^

Base Metals 20 6.19 8.00 5.9 29 3Molybdenum price hike adds to earnings elasticity: Abundant upstream resources aiding ef for ts to develop downstream markets

China Pacific Insurance (601601 CH)^

Life Insurance 207 33.00 42.40 31.4 28 3Value recovery of the insurance sector appears sustainable: Insurers tipped to surge in early 2019E on a low base

Chint Electronics (601877 CH)^

Electrical Power Equipment

50 23.20 29.70 22.0 28 3Explor ing the household photovol ta ic power generation market: Favorable policy to boost growth

Double Medical (002901 CH)*

Medical Devices 13 32.63 41.74 31.0 28 3Exploring high-value medical consumables: Rapidly growing market for spine products

Yonghui Superstores (601933 CH)^

Food & Drug Stores

70 7.30 9.30 6.9 27 3Setting up another regional joint venture: Moving towards an optimal ecosystem

Shenzhen Gas (601139 CH)^

Utility Networks 17 5.77 7.30 5.5 27 3Earnings elasticity from new LNG terminal: Getting ready to warm up earnings from bunkered energy come winter 2018E

Xiamen Tungsten (600549 CH)^

Base Metals 19 13.50 17.00 12.8 26 3

Sustaining growth in output and sales of lithium bat tery materials: Rising capacit y coupled with higher proportions of deep-processed materials and overseas sales

Source: Bloomberg, CS U Closing prices as of 9 Nov 2018 * Shenzhen-HK Stock Connect – Northbound Stocks (ChiNext Board for Professional Institutional Investors Only) ^ Shanghai-HK Stock Connect – Northbound Stocks Risk Rating: 1 to 5 in ascending order

15 12 Nov 2018

Please refer to the attachment for detailed disclaimer and regulatory disclosures.

Ch

ina

Con

nec

t W

eekl

y:M

acr

o dow

ntu

rn r

edu

ces

visi

bil

ity

a-share reCoMMended stoCks:

Mkt Cap PriceU Target Stop Loss Upside Risk

Company Business (Rmb bn) (Rmb) (Rmb) (Rmb) (%) rating Remarks

Zijin Mining (601899 CH)^

Precious Metal Mining

59 3.42 4.30 3.2 26 3Gold price directed by short- term risk aversion: Increase in institutional positions in gold plays to hedge against risk of overall market decline

Gemdale (600383 CH)^Real Estate Owners & Developers

41 9.18 11.48 8.7 25 3Embracing peak season for project launch: Rolling out more projects than previously planned

Spring Airlines (601021 CH)^

Airlines 32 34.40 43.00 32.7 25 3Returning to positive growth: Greater earnings upside in high-end markets

Shandong Gold Mining (600547 CH)^

Precious Metal Mining

47 25.35 30.40 24.1 20 3Gold price directed by short- term risk aversion: Increase in institutional positions in gold plays to hedge against risk of overall market decline

China Railway Group (601390 CH)^

Infrastructure Construction

136 7.29 8.60 6.9 18 3

T h e f i r s t t o b e n e f i t f ro m b e t t e r f i n a n c i n g : R e c o m m e n d i n g c o n s t r u c t i o n S O E s w i t h undemanding share valuation and potential to lead in getting results on improved financing

Asymchem Laboratories (002821 CH)*

Specialty Pharma 16 70.55 82.32 67.0 17 3Joining hands with domestic and international leading names: Rapid growth ahead on domestic and offshore drivers

ZTE (000063 CH)*Communications Equipment

68 19.87 23.02 18.9 16 3Steadily delivering promised growth: Upbeat 1H17 results and visible 5G prospects

very Agressive StockSMkt Cap PriceU Target Stop Loss Upside Risk

Company Business (Rmb bn) (Rmb) (Rmb) (Rmb) (%) rating Remarks

Taihai Manoir Nuclear (002366 CH)*

Flow Control Equipment

9 9.87 47.70 9.4 383 3New business deals in of fshore nuclear power equipment: Improving fundamentals to support further growth

Kangni Mechanical (603111 CH)^

Electronic Components

4 4.18 17.60 4.0 321 3Acquisi t ion target may surprise on the upside: Proposing merger to tap into the growing mobile casing market

Kehua Hengsheng (002335 CH)*

Electrical Power Equipment

4 13.95 47.40 13.3 240 3Emerging in top-t ier markets: Cloud computing project in Shanghai received go-ahead

Shouhang Resources Saving (002665 CH)*

Comml & Res Bldg Equip & Sys

9 3.45 11.70 3.3 239 3Killing two birds with one mixed-ownership stone: Faster advance on reform and business upturn

Vtron Tech (002308 CH)*

Consumer Electronics

5 5.36 18.00 5.1 236 3Acquiring a controlling share in Keer Education: Leveraging on top-quality education resources and offline development in core cities.

Huayi Brothers (300027 CH)*

Movie/TV drama 13 4.65 14.97 4.4 222 3

Set sail for an exciting long journey with powerful partners onboard: Cooperate with Alibaba and Tencent in e -commerce, new media and movie production development.

Changjiang Electronics (600584 CH)^

Semi Conductor 17 10.32 31.95 9.8 210 3Leading the race: Intensifying M&As as the Moore’s Law coming towards a bottleneck

Zhiyun Automation (300097 CH)*

Automation Equipment

3 11.34 34.68 10.8 206 3O n w a y t o l e a d h o m e - g r o w n e q u i p m e n t makers: Acquisition to pave way into a new market segment.

Eastone Century Technology (300310 CH)*

IT Services 4 4.72 14.40 4.5 205 3Beefing up prospective research in IoT: Joining hands with strong player in the field to reinforce R&D muscle

Guoxuan High-Tech (002074 CH)*

Electrical Power Equipment

15 12.81 36.00 12.2 181 3Policy guidance to beef up industry leaders: Large-scale manufacturers of car bat teries to r ide on favorable policy and first-mover advantages

CIMC (000039 CH)*Fabricated Metal & Hardware

14 11.01 29.00 10.5 163 3Framework pact signed for Qianhai plot : Land conversion to commercial use t ipped to boost valuation and balance sheet

Originwater (300070 CH)*

Waste Water Treatment

29 9.08 22.50 8.6 148 3“River chiefs” assuming duty: Shanghai rolling out new system to clean polluted waters .

Hytera Communications (002583 CH)*

Communications Equipment

15 8.20 19.70 7.8 140 3Seeking global dominance in private communication net works: Core technology and r ich product s pointing way to industry leader worldwide

CHJ Industry (002345 CH)*

Jewelries and Accessories

5 5.04 11.60 4.8 130 3All that glitters is gold: The Company appears ready to attract industry capital from China and abroad to facilitate future M&As and incubate new brands.

Source: Bloomberg, CS U Closing prices as of 9 Nov 2018 * Shenzhen-HK Stock Connect – Northbound Stocks (ChiNext Board for Professional Institutional Investors Only) ^ Shanghai-HK Stock Connect – Northbound Stocks Risk Rating: 1 to 5 in ascending order

16 12 Nov 2018

Please refer to the attachment for detailed disclaimer and regulatory disclosures.

Ch

ina

Con

nec

t W

eekl

y:M

acr

o dow

ntu

rn r

edu

ces

visi

bil

ity

a-share reCoMMended stoCks:

Mkt Cap PriceU Target Stop Loss Upside Risk

Company Business (Rmb bn) (Rmb) (Rmb) (Rmb) (%) rating Remarks

UTour Int'l Travel (002707 CH)*

Tourism Services 6 6.55 14.90 6.2 127 3

Rais ing the bamboo cur ta in: Growing onl ine distribution platforms such as Tuniu and huge offline resources, its O2O model has huge upside potential going forward.

Lu'An Environmental Energy (601699 CH)^

Coal Operations 23 7.80 17.40 7.4 123 3Rebound underway as the high season unfolds: Expecting a strong sector rebound over the two months ahead

Wanhua Chemical (600309 CH) ^

Basic & Diversified Chemicals

80 29.23 65.00 27.8 122 3 The second leap: M&A deals set to lift profits

Kingfa Tech (600143 CH)^

Specialty Chemicals

13 4.68 9.30 4.4 99 3New materials forming multiple drivers for earnings turnaround in 2018E

Sunsea Telecommunications (002313 CH)*

Communications Equipment

6 18.12 34.40 17.2 90 3High-level liaison: Well-defined strategy and excellent execution

Hailide (002206 CH)* Textile 5 3.96 7.50 3.8 89 3

Meaningful upturn in demand: Improving demand on the back o f bet ter technology, changing downstream competitive landscape and increasing localization.

Ningbo Shanshan (600884 CH)^

Apparel, Footwear & Acc Design

16 14.33 27.00 13.6 88 3Leading supplier of lithium battery material: Favorable climate thanks to the NEV market boom

Newland (000997 CH)*

Infrastructure Software

14 14.25 26.50 13.5 86 3

Full speed ahead to payment business: Buying a national merchant acquir ing l icense to boost prof i tabi l i t y and t rans form into an integrated electronic payment operator.

Star-net Communication (002396 CH)*

Communication Equipment

10 17.41 32.00 16.5 84 3 Sustainable growth: Abundant business innovation

Hoshine Silicon (603260 CH)^

Specialty Chemicals

32 47.63 85.20 45.2 79 3Stellar performance: Full-chain operation guarantees long-term growth

NavInfo (002405 CH)*Application Software

20 15.65 27.99 14.9 79 3A launch pad to international track: Buying a stake into global mapping service provider to form strong alliance

Worldunion (002285 CH)*

Real Estate Services

10 4.84 8.52 4.6 76 3New JV for secondar y housing management : Potent ia l t akeover o f compet i t i ve t a rget s on increasingly strict industry regulation

Heilan Home (600398 CH)^

Specialty Apparel Stores

36 8.08 14.04 7.7 74 3Advancing the multi-brand strategy: Expanding scale and widening presence via UR acquisition

Maoye Communication & Network (000889 CH)*

Real Estate & Telecom

8 11.70 20.00 11.1 71 3Accelerating business transit ion: Steady organic growth with scale expansion on the horizon.

Nanji E-Commerce (002127 CH)*

Internet Retailing 18 7.41 12.40 7.0 67 3Huge room to expand: Strong head products and potential to expand long-tail goods

Perfect World (002624 CH)*

Entertainment Content

33 25.41 41.10 24.1 62 3Asset sales to consolidate core business: Sell ing cinema line assets in a bid to concentrate on core

EVE Energy (300014 CH)*

Renewable Energy Equipment

11 12.60 20.00 12.0 59 3Policy guidance to beef up industry leaders: Large-scale manufacturers of car bat teries to r ide on favorable policy and first-mover advantages

Luxshare Precision (002475 CH)*

Electrical Components

62 15.15 23.67 14.4 56 3Forecas t-beat ing 3Q18 resul t s : New product s expected to attract major clients and boost earnings

Global Top E-Commerce (002640 CH)*

Apparel, Footwear & Acc Design

18 11.64 18.00 11.1 55 3Consolidating to stoke quality growth: Persistently strong electronics and recovering apparel trade

Wangsu Science (300017 CH)*

IT Services 20 8.02 12.36 7.6 54 3Informatization and internetization tasks outlined: Broad-stroke IT policy to be followed by concrete measures.

Better Life (002251 CH)*

Food & Drug Stores

7 7.96 12.00 7.6 51 3Global trade of growing scale: Upbeat about players with strong overseas supply chains and commodity flow.

Jereh Oilfield Services (002353 CH)*

Oil & Gas Services & Equip

20 21.29 32.00 20.2 50 3A leading oilfield service provider: Best of the pack in profitability and earnings potential

Shanghai Ganglian (300226 CH)*

Internet Based Services

80 50.49 75.47 48.0 49 3Building up moat via information service: Enhancing the supply-chain service model

Fenghua Advanced Technology (000636 CH)*

Electrical Components

12 12.87 19.04 12.2 48 3New opportunities: Scale and business expansion to be fueled by SOE reform.

Source: Bloomberg, CS U Closing prices as of 9 Nov 2018 * Shenzhen-HK Stock Connect – Northbound Stocks (ChiNext Board for Professional Institutional Investors Only) ^ Shanghai-HK Stock Connect – Northbound Stocks Risk Rating: 1 to 5 in ascending order

17 12 Nov 2018

Please refer to the attachment for detailed disclaimer and regulatory disclosures.

Ch

ina

Con

nec

t W

eekl

y:M

acr

o dow

ntu

rn r

edu

ces

visi

bil

ity

a-share reCoMMended stoCks:

Mkt Cap PriceU Target Stop Loss Upside Risk

Company Business (Rmb bn) (Rmb) (Rmb) (Rmb) (%) rating Remarks

Sinnet Technology (300383 CH)*

Network Integration Services

20 13.29 19.60 12.6 47 3Sustainable high growth in cloud comput ing: Subsidiary formed to lift AWS cloud sales and own cloud computing business tipped to grow rapidly

Lianchuang Electronic (002036 CH)*

Consumer Electronics

5 9.20 12.80 8.7 39 3Investment prospects in science and technology: 2017E to see equipment market expansion and explosive content growth.

AVIC Helicopter (600038 CH)^

Aircraft & Parts 21 35.99 50.00 34.2 39 3Promising target: The sole listed helicopter asset in parent group

Cha Cha Food (002557 CH)*

Packaged Food 9 18.31 25.00 17.4 37 3

Nuts are core in online food sales: Nuts outrunning all other snacks in online food sales during the Chinese New Year holidays; online venders with nuts as core products ready for a bumper harvest ahead

AECC Aviation Power (600893 CH)^

Aircraft & Parts 54 23.87 32.50 22.7 36 3Promising target: A whole-engine plat form with sustainable strong growth

Sunner Develop (002299 CH)*

Meat Type Chicken Products

20 16.00 21.40 15.2 34 3Consumption upturn: Hiking chicken prices and its potential passage onto upstream companies

Haid Group (002311 CH)*

Agricultural Producers

34 21.20 27.40 20.1 29 3Galloping growth: Deserving premium for sustainable growth and visibility

Jinyu Bio-technology (600201 CH)^

Animal Biophar-maceuticals

21 18.01 23.00 17.1 28 3

Accelerating shift towards a global leader in animal health solutions: Regaining market share via new products and faster transformation to a leading global player

Aier Eye (300015 CH)* Health Care 66 27.84 35.40 26.4 27 3Private placement to solidify basis for robust growth: Strong outlook for the next few years on the back of hospital acquisitions.

AVIC Electromechanical (002013 CH)*

Aircraft Parts 28 7.75 9.70 7.4 25 3Asset injection on the door steps: Private placement of shares approved by regulator.

BYD (002594 CH)* Automobiles 91 50.00 62.00 47.5 24 3A promising last quar ter : Driv ing up sales and profitability via faster release of new models

Tongwei (600438 CH)^Agricultural Producers

30 7.68 9.36 7.3 22 3A big deal: New order to account for 30% of capacity in the next three years, sustaining robust growth of the Company’s PV power division

Source: Bloomberg, CS U Closing prices as of 9 Nov 2018 * Shenzhen-HK Stock Connect – Northbound Stocks (ChiNext Board for Professional Institutional Investors Only) ^ Shanghai-HK Stock Connect – Northbound Stocks Risk Rating: 1 to 5 in ascending order

18 12 Nov 2018

Please refer to the attachment for detailed disclaimer and regulatory disclosures.

Ch

ina

Con

nec

t W

eekl

y:M

acr

o dow

ntu

rn r

edu

ces

visi

bil

ity

top twenties:

Top 20 GainersCompany

Price (Rmb)

WoW Chg (%)

Shenzhen Geoway (600462 CH) 4.49 62

Shibei Hi-Tech (600604 CH) 5.68 61

Jiangsu Holly (600128 CH) 9.79 61

Shanghai Sanmao (600689 CH) 12.65 61

Dymatic Chemicals (002054 CH) 7.49 61

Minfeng Special Paper (600235 CH) 6.82 61

Qunxing Toys (002575 CH) 6.93 61

Hengli Industrial (000622 CH) 7.90 57

Luxin Venture Capital (600783 CH) 15.14 54

Fudan Forward (600624 CH) 6.69 52

Huayi Electric (600290 CH)s 5.47 45

Huajin Capital (000532 CH) 11.87 40

Zhangjiang High-Tech (600895 CH) 13.68 39

Vanfund Investment (000638 CH) 6.38 39

Youngy (002192 CH) 19.25 39

East Lake High Technolog (600133 CH) 6.48 35

Golden Eagle (600232 CH) 6.22 34

Hi-Tech Development (600082 CH) 4.94 32

Jiuding Investment (600053 CH) 19.05 32

Qianjiang Water Resources (600283 CH) 12.76 31

Top 20 LosersCompany

Price (Rmb)

WoW Chg (%)

Neoglory Prosperity (002147 CH) 7.06 (41)

Eastern Gold Jade (600086 CH) 5.35 (41)

Shouhang Resources (002665 CH) 3.45 (41)

Wanda Film (002739 CH) 22.17 (36)

Hongtu High Technology (600122 CH) 4.53 (32)

Tianyin Electromechan (300342 CH) 8.12 (30)

Homa Appliances (002668 CH) 6.26 (19)

Kangde Xin (002450 CH) 13.78 (19)

Topstrong Living (300749 CH) 26.19 (18)

JL Mag Rare-Earth (300748 CH) 27.28 (17)

Hodgen Technology (300279 CH) 5.38 (17)

Great Wall Securities (002939 CH) 12.22 (17)

Sunrise Elc Technology (002937 CH) 24.88 (16)

Focus Media (002027 CH) 5.72 (16)

Unigroup Xue (000526 CH) 21.83 (15)

Wuxi Lihu (300694 CH) 22.21 (14)

ADD Industry (603089 CH) 18.65 (14)

Emerging Eastern (002933 CH) 43.26 (13)

Huge Leaf (600226 CH) 2.90 (13)

Yijiahe Technology (603666 CH) 47.29 (12)

Source: Bloomberg, CS * Closing prices as of 9 Nov 2018

19 12 Nov 2018

Please refer to the attachment for detailed disclaimer and regulatory disclosures.

Ch

ina

Con

nec

t W

eekl

y:M

acr

o dow

ntu

rn r

edu

ces

visi

bil

ity

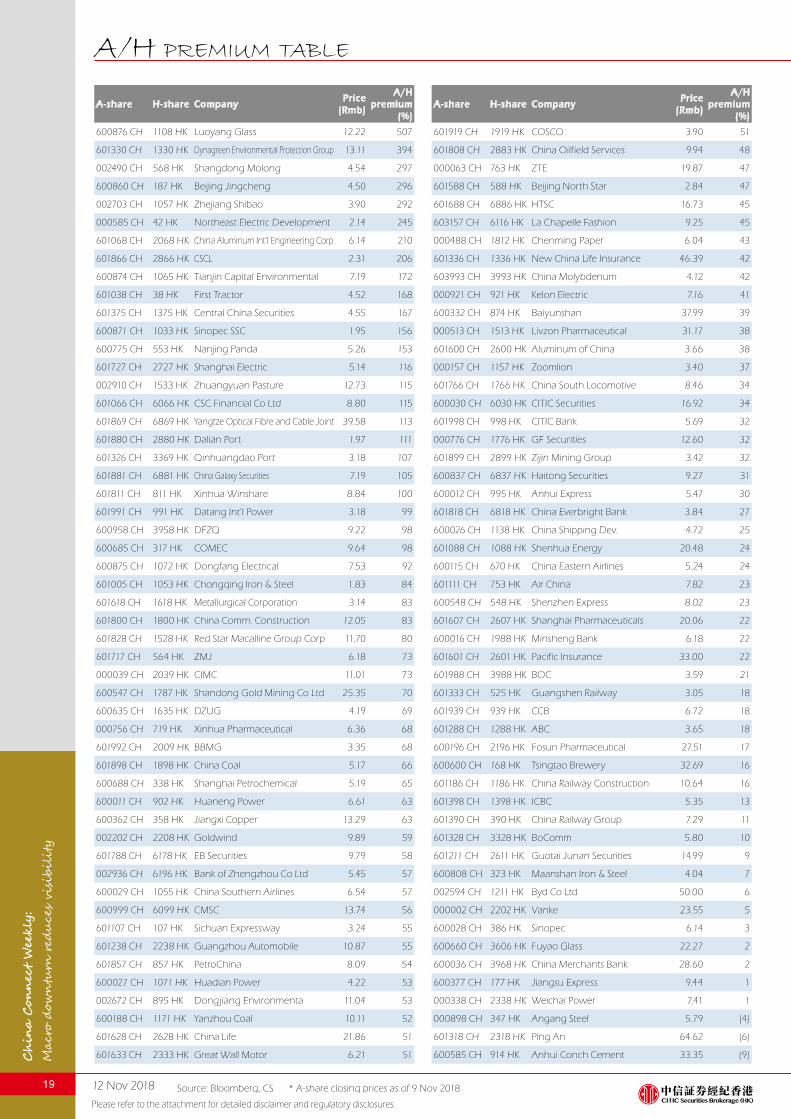

a/h preMiuM table

A-share H-share CompanyPrice

(Rmb)

A/H premium

(%)

600876 CH 1108 HK Luoyang Glass 12.22 507

601330 CH 1330 HK Dynagreen Environmental Protection Group 13.11 394

002490 CH 568 HK Shangdong Molong 4.54 297

600860 CH 187 HK Beijing Jingcheng 4.50 296

002703 CH 1057 HK Zhejiang Shibao 3.90 292

000585 CH 42 HK Northeast Electric Development 2.14 245

601068 CH 2068 HK China Aluminum Int'l Engineering Corp 6.14 210

601866 CH 2866 HK CSCL 2.31 206

600874 CH 1065 HK Tianjin Capital Environmental 7.19 172

601038 CH 38 HK First Tractor 4.52 168

601375 CH 1375 HK Central China Securities 4.55 167

600871 CH 1033 HK Sinopec SSC 1.95 156

600775 CH 553 HK Nanjing Panda 5.26 153

601727 CH 2727 HK Shanghai Electric 5.14 116

002910 CH 1533 HK Zhuangyuan Pasture 12.73 115

601066 CH 6066 HK CSC Financial Co Ltd 8.80 115

601869 CH 6869 HK Yangtze Optical Fibre and Cable Joint 39.58 113

601880 CH 2880 HK Dalian Port 1.97 111

601326 CH 3369 HK Qinhuangdao Port 3.18 107

601881 CH 6881 HK China Galaxy Securities 7.19 105

601811 CH 811 HK Xinhua Winshare 8.84 100

601991 CH 991 HK Datang Int'l Power 3.18 99

600958 CH 3958 HK DFZQ 9.22 98

600685 CH 317 HK COMEC 9.64 98

600875 CH 1072 HK Dongfang Electrical 7.53 92

601005 CH 1053 HK Chongqing Iron & Steel 1.83 84

601618 CH 1618 HK Metallurgical Corporation 3.14 83

601800 CH 1800 HK China Comm. Construction 12.05 83

601828 CH 1528 HK Red Star Macalline Group Corp 11.70 80

601717 CH 564 HK ZMJ 6.18 73

000039 CH 2039 HK CIMC 11.01 73

600547 CH 1787 HK Shandong Gold Mining Co Ltd 25.35 70

600635 CH 1635 HK DZUG 4.19 69

000756 CH 719 HK Xinhua Pharmaceutical 6.36 68

601992 CH 2009 HK BBMG 3.35 68

601898 CH 1898 HK China Coal 5.17 66

600688 CH 338 HK Shanghai Petrochemical 5.19 65

600011 CH 902 HK Huaneng Power 6.61 63

600362 CH 358 HK Jiangxi Copper 13.29 63

002202 CH 2208 HK Goldwind 9.89 59

601788 CH 6178 HK EB Securities 9.79 58

002936 CH 6196 HK Bank of Zhengzhou Co Ltd 5.45 57

600029 CH 1055 HK China Southern Airlines 6.54 57

600999 CH 6099 HK CMSC 13.74 56

601107 CH 107 HK Sichuan Expressway 3.24 55

601238 CH 2238 HK Guangzhou Automobile 10.87 55

601857 CH 857 HK PetroChina 8.09 54

600027 CH 1071 HK Huadian Power 4.22 53

002672 CH 895 HK Dongjiang Environmenta 11.04 53

600188 CH 1171 HK Yanzhou Coal 10.11 52

601628 CH 2628 HK China Life 21.86 51

601633 CH 2333 HK Great Wall Motor 6.21 51

A-share H-share CompanyPrice

(Rmb)

A/H premium

(%)

601919 CH 1919 HK COSCO 3.90 51

601808 CH 2883 HK China Oilfield Services 9.94 48

000063 CH 763 HK ZTE 19.87 47

601588 CH 588 HK Beijing North Star 2.84 47

601688 CH 6886 HK HTSC 16.73 45

603157 CH 6116 HK La Chapelle Fashion 9.25 45

000488 CH 1812 HK Chenming Paper 6.04 43

601336 CH 1336 HK New China Life Insurance 46.39 42

603993 CH 3993 HK China Molybdenum 4.12 42

000921 CH 921 HK Kelon Electric 7.16 41

600332 CH 874 HK Baiyunshan 37.99 39

000513 CH 1513 HK Livzon Pharmaceutical 31.17 38

601600 CH 2600 HK Aluminum of China 3.66 38

000157 CH 1157 HK Zoomlion 3.40 37

601766 CH 1766 HK China South Locomotive 8.46 34

600030 CH 6030 HK CITIC Securities 16.92 34

601998 CH 998 HK CITIC Bank 5.69 32

000776 CH 1776 HK GF Securities 12.60 32

601899 CH 2899 HK Zijin Mining Group 3.42 32

600837 CH 6837 HK Haitong Securities 9.27 31

600012 CH 995 HK Anhui Express 5.47 30

601818 CH 6818 HK China Everbright Bank 3.84 27

600026 CH 1138 HK China Shipping Dev. 4.72 25

601088 CH 1088 HK Shenhua Energy 20.48 24

600115 CH 670 HK China Eastern Airlines 5.24 24

601111 CH 753 HK Air China 7.82 23

600548 CH 548 HK Shenzhen Express 8.02 23

601607 CH 2607 HK Shanghai Pharmaceuticals 20.06 22

600016 CH 1988 HK Minsheng Bank 6.18 22

601601 CH 2601 HK Pacific Insurance 33.00 22

601988 CH 3988 HK BOC 3.59 21

601333 CH 525 HK Guangshen Railway 3.05 18

601939 CH 939 HK CCB 6.72 18

601288 CH 1288 HK ABC 3.65 18

600196 CH 2196 HK Fosun Pharmaceutical 27.51 17

600600 CH 168 HK Tsingtao Brewery 32.69 16

601186 CH 1186 HK China Railway Construction 10.64 16

601398 CH 1398 HK ICBC 5.35 13

601390 CH 390 HK China Railway Group 7.29 11

601328 CH 3328 HK BoComm 5.80 10

601211 CH 2611 HK Guotai Junan Securities 14.99 9

600808 CH 323 HK Maanshan Iron & Steel 4.04 7

002594 CH 1211 HK Byd Co Ltd 50.00 6

000002 CH 2202 HK Vanke 23.55 5

600028 CH 386 HK Sinopec 6.14 3

600660 CH 3606 HK Fuyao Glass 22.27 2

600036 CH 3968 HK China Merchants Bank 28.60 2

600377 CH 177 HK Jiangsu Express 9.44 1

000338 CH 2338 HK Weichai Power 7.41 1

000898 CH 347 HK Angang Steel 5.79 (4)

601318 CH 2318 HK Ping An 64.62 (6)

600585 CH 914 HK Anhui Conch Cement 33.35 (9)

Source: Bloomberg, CS * A-share closing prices as of 9 Nov 2018

20 12 Nov 2018

Please refer to the attachment for detailed disclaimer and regulatory disclosures.

Ch

ina

Con

nec

t W

eekl

y:M

acr

o dow

ntu

rn r

edu

ces

visi

bil

ity

CITIC S&P 50 IndexPER (x) 17-19E Chg (%) 6M Avg Daily T/O Mkt Cap

Sector 17 18E 19E PEG (x) 1-wk 1-mth YTD 1-yr (Rmb mn) (Rmb bn)

Market cap weighted average 15 13 11 0.9 (4.4) (3.2) (13.7) (11.9) 43,203 12,462

Energy 12 9 9 0.7 (1.3) (5.0) (4.1) (3.5) 1,148 924

Materials 13 9 8 0.6 (5.3) (3.6) (9.3) (0.9) 2,092 408

Capital Goods 22 18 14 0.9 (3.5) (1.3) (19.8) (23.2) 1,714 781

Transportation 9 8 8 2.0 (1.7) 1.6 (11.1) (9.6) 301 120

Automobiles & Components 9 8 8 1.2 (3.1) (9.4) (15.0) (13.4) 505 318

Consumer Durables & Apparel 13 11 10 0.8 (3.4) (3.1) (21.8) (20.1) 4,300 576

Retailing 115 16 43 1.8 (4.3) (10.7) (7.0) (20.1) 671 106

Food, Beverage & Tobacco 24 19 16 1.1 (6.0) (18.4) (23.3) (17.6) 7,239 1,182

Pharmaceuticals, Biotechnology & Life Sciences 62 50 39 2.4 (4.8) (1.3) 7.9 5.0 2,010 297

Banks 7 6 6 0.9 (5.0) (1.5) (9.3) (5.9) 6,790 4,631

Diversified Financials 15 17 15 8.8 (5.1) 3.3 (15.8) (19.9) 2,134 316

Insurance 16 15 12 0.9 (4.4) (0.5) (16.3) (15.7) 4,824 1,363

Software & Services 108 69 47 2.1 (4.1) (12.6) (39.8) (40.0) 1,018 50

Technology Hardware & Equipment 21 17 17 1.7 (3.0) 4.6 (39.1) (42.3) 4,848 406

Telecommunication Services NA 42 27 NA (2.7) 0.6 (15.2) (34.4) 684 167

Media & Entertainment 14 14 13 2.4 0.1 (3.1) (26.7) (36.0) 95 32

Utilities 16 15 14 3.2 (5.6) (7.1) (8.1) (13.7) 370 370

Real Estate 9 7 6 0.4 (3.9) 7.8 (20.9) (5.1) 2,461 415

CITIC S&P 300 IndexPER (x) 17-19E Chg (%) 6M Avg Daily T/O Mkt Cap

Sector 17 18E 19E PEG (x) 1-wk 1-mth YTD 1-yr (Rmb mn) (Rmb bn)

Market cap weighted average 22 16 13 0.8 (3.6) (4.1) (15.3) (14.9) 98,478 22,631

Energy 44 18 15 0.6 (2.1) (9.4) (2.0) (4.3) 2,477 2,332

Materials 22 16 14 0.8 (4.5) (7.3) (24.0) (19.8) 11,594 1,225

Capital Goods 21 17 14 1.0 (3.2) (3.5) (22.5) (26.0) 10,064 2,092

Commercial & Professional Services 16 15 11 0.8 (2.2) (10.2) (44.4) (51.4) 284 42

Transportation 14 15 13 2.4 (4.4) (0.7) (22.1) (18.9) 2,703 667

Automobiles & Components 17 15 12 0.9 (1.5) (5.3) (24.8) (25.5) 2,250 827

Consumer Durables & Apparel 15 13 11 0.8 (3.3) (4.9) (25.6) (25.4) 5,861 749

Consumer Services 31 22 18 1.0 (2.7) (8.5) 9.2 10.8 1,035 168

Retailing 63 13 27 1.2 (2.7) (11.5) (23.1) (32.4) 1,148 224

Food & Staples Retailing 32 40 29 5.7 (0.4) (9.0) (30.5) (32.7) 427 91

Food, Beverage & Tobacco 27 22 19 1.3 (3.9) (14.5) (18.3) (13.6) 9,717 1,738

Household & Personal Products 44 33 26 1.5 (5.4) (7.6) (30.8) (31.6) 147 17

Health Care Equipment & Services 39 31 31 3.4 (1.4) (3.5) (11.1) (6.7) 1,268 176

Pharmaceuticals, Biotechnology & Life Sciences 48 39 31 2.1 (2.0) (3.7) (7.6) (8.4) 8,765 1,067

Banks 7 6 6 0.9 (4.7) (1.1) (9.4) (6.5) 7,792 5,861

Diversified Financials 17 19 16 11.5 (4.4) 3.2 (18.4) (23.6) 2,690 510

Insurance 16 15 12 0.9 (4.4) (0.5) (16.3) (15.7) 4,824 1,363

Software & Services 67 47 35 1.7 (1.6) (5.9) (0.3) (6.7) 3,816 240

Technology Hardware & Equipment 26 21 18 1.3 (3.7) (3.6) (34.3) (37.3) 12,792 940

Semiconductors & Semiconductor Equipment 19 19 15 1.3 (0.7) 1.8 (41.5) (45.2) 1,381 122

Telecommunication Services 1 40 26 NA (2.5) (1.1) (17.6) (36.2) 818 177

Media & Entertainment 21 16 14 0.9 (9.6) (8.4) (36.8) (42.1) 585 166

Utilities 25 16 14 0.7 (2.9) (5.1) (10.8) (16.4) 1,359 901

Real Estate 13 8 6 0.3 (2.2) 5.2 (18.2) (8.7) 4,682 935

Source: Bloomberg, CS * Closing prices as of 9 Nov 2018 GICS (Global Industry Classification Standard)

Major index perforManCe:

21 12 Nov 2018

Please refer to the attachment for detailed disclaimer and regulatory disclosures.

Ch

ina

Con

nec

t W

eekl

y:M

acr

o dow

ntu

rn r

edu

ces

visi

bil

ity

what to watCh out for:

Results Announcement Code Company Estimated Date Financial Year / Quarter^

- - - - -

*Companies included in CITIC S&P 300 Index only ^ MM/YY QQSource: Bloomberg, CS

Publication of Economic DataDate/Time* Event Period Figures Actual Previous Revision

11/08 - 11/18/2018 Foreign Direct Investment YoY CNY Oct -- -- 8.0% --

11/10 - 11/15/2018 Money Supply M1 YoY Oct 4.3% -- 4.0% --

11/10 - 11/15/2018 Money Supply M2 YoY Oct 8.4% -- 8.3% --

11/10 - 11/15/2018 Money Supply M0 YoY Oct 2.6% -- 2.2% --

11/10 - 11/15/2018 Aggregate Financing CNY Oct 1,297.0b -- 2,205.4b --

11/10 - 11/15/2018 New Yuan Loans CNY Oct 900b -- 1,380b --

11/14/2018 10:00 Retail Sales YoY Oct 9.2% -- 9.2% --

11/14/2018 10:00 Retail Sales YTD YoY Oct 9.3% -- 9.3% --

11/14/2018 10:00 Industrial Production YoY Oct 5.8% -- 5.8% --

11/14/2018 10:00 Industrial Production YTD YoY Oct 6.3% -- 6.4% --

11/14/2018 10:00 Fixed Assets Ex Rural YTD YoY Oct 5.5% -- 5.4% --

11/14/2018 10:00 Property Investment YoY Oct -- -- 9.9% --

11/14/2018 10:00 Surveyed Jobless Rate Oct -- -- 4.9% --

11/15/2018 09:30 New Home Prices MoM Oct -- -- 1.0% --

Source: Bloomberg, CS * MM/DD/YYYY

Major corporate results and economic data

Source: Bloomberg, CS

22 12 Nov 2018

Please refer to the attachment for detailed disclaimer and regulatory disclosures.

Ch

ina

Con

nec

t W

eekl

y:M

acr

o dow

ntu

rn r

edu

ces

visi

bil

ity

what to watCh out for:

(10)

0

10

20

30

40

50

31/1

0/20

17

30/1

1/20

17

31/1

2/20

17

31/1

/201

8

28/2

/201

8

31/3

/201

8

30/4

/201

8

31/5

/201

8

30/6

/201

8

31/7

/201

8

31/8

/201

8

30/9

/201

8

31/1

0/20

18

2018

E

China Export Trade USD YoY

China Import Trade USD YoY

(%)

6.4

6.5

6.6

6.7

6.8

6.9

7.0

31/1

2/20

15

31/3

/201

6

30/6

/201

6

30/9

/201

6

31/1

2/20

16

31/3

/201

7

30/6

/201

7

30/9

/201

7

31/1

2/20

17

31/3

/201

8

30/6

/201

8

30/9

/201

8

2018

E

China GDP Constant Price YoY

China GDP Constant Price CumulativeYoY

(%)

012345678

31/1

0/20

17

30/1

1/20

17

31/1

2/20

17

31/1

/201

8

28/2

/201

8

31/3

/201

8

30/4

/201

8

31/5

/201

8

30/6

/201

8

31/7

/201

8

31/8

/201

8

30/9

/201

8

31/1

0/20

18

2018

E

China CPI YoY

China PPI YoY

(%)

50.0

50.3

50.6

50.9

51.2

51.5

51.8

52.1

31/1

0/20

17

30/1

1/20

17

31/1

2/20

17

31/1

/201

8

28/2

/201

8

31/3

/201

8

30/4

/201

8

31/5

/201

8

30/6

/201

8

31/7

/201

8

31/8

/201

8

30/9

/201

8

31/1

0/20

18

(Index)

GDP ►China posted 3Q18 GDP growth of

6.5% YoY, below the 6.7% f igure in

2Q18 and the lowest since the global

f inancial crisis in 2008. The National

Bureau of Statistics pointed to a sharp

increase in the number of challenging

externali t ies and continuing pains

f rom China’s restructuring ef for t s .

The economy is decelerating steadily

as downward pressure mounts. The

market forecasts full-year 2018E GDP

growth to be 6.6% YoY.

Import and Export ►In Oct 2018, China saw its exports and imports increase respectively 15.6% and 21.4% YoY in value terms, far exceeding market consensus. We believe the export spike was mainly due to a low base and the race to sell ahead of the imposition of the trade war-triggered higher tarif fs . However, the surge did not stem directly from trading between China and the US. It was possibly the result of a short-term and overall expansion on the back of exports to or through surrounding regions (such as Hong Kong). The market forecasts full-year 2018E exports and imports will advance 10.0% and 17.7% YoY, respectively.

◄ Manufacturing PMI

China’s manufacturing PMI came to 50.2

in Oct 2018, down 0.6 MoM. Growth

slackened and pressure on the economy

is emerging. We foresee the economy

remain depressed over the next few

months. Expansionary policies need to be

stepped up further.

◄ CPI and PPI

China’s CPI ticked up 2.5% YoY in Oct 2018,

flat MoM; PPI climbed 3.3% YoY, the weakest

growth in seven months, with the Sep

reading being 3.6%. The market expects

2018E CPI and PPI to rise 2.2% and 3.5% YoY,

respectively.

Major economic indicators

Source: Bloomberg, CS

23 12 Nov 2018

Please refer to the attachment for detailed disclaimer and regulatory disclosures.

Ch

ina

Con

nec

t W

eekl

y:M

acr

o dow

ntu

rn r

edu

ces

visi

bil

ity

what to watCh out for:

3

57

911

1315

17

31/1

0/20

17

30/1

1/20

17

31/1

2/20

17

31/1

/201

8

28/2

/201

8

31/3

/201

8

30/4

/201

8

31/5

/201

8

30/6

/201

8

31/7

/201

8

31/8

/201

8

30/9

/201

8

2018

E

China Monthly Money Supply M1 YoY

China Monthly Money Supply M2 YoY

(%)

5.75.96.16.36.56.76.97.17.37.57.7

30/9

/201

7

31/1

0/20

17

30/1

1/20

17

31/1

2/20

17

Jan-

Feb

2017

31/3

/201

8

30/4

/201

8

31/5

/201

8

30/6

/201

8

31/7

/201

8

31/8

/201

8

30/9

/201

8

2018

E

China Value Added of Industry YoY Cumulative

China Value Added of Industry YoY

(%)

0

500

1,000

1,500

2,000

2,500

3,000

30/9

/201

7

31/1

0/20

17

30/1

1/20

17

31/1

2/20

17

31/1

/201

8

28/2

/201

8

31/3

/201

8

30/4

/201

8

31/5

/201

8

30/6

/201

8

31/7

/201

8

31/8

/201

8

30/9

/201

8

(Rmb bn)

8.4

8.8

9.2

9.6

10.0

10.4

31/1

0/20

17

30/1

1/20

17

31/1

2/20

17

Jan-

Feb

2018

31/3

/201

8

30/4

/201

8

31/5

/201

8

30/6

/201

8

31/7

/201

8

31/8

/201

8

30/9

/201

8

2018

E

(YoY %)

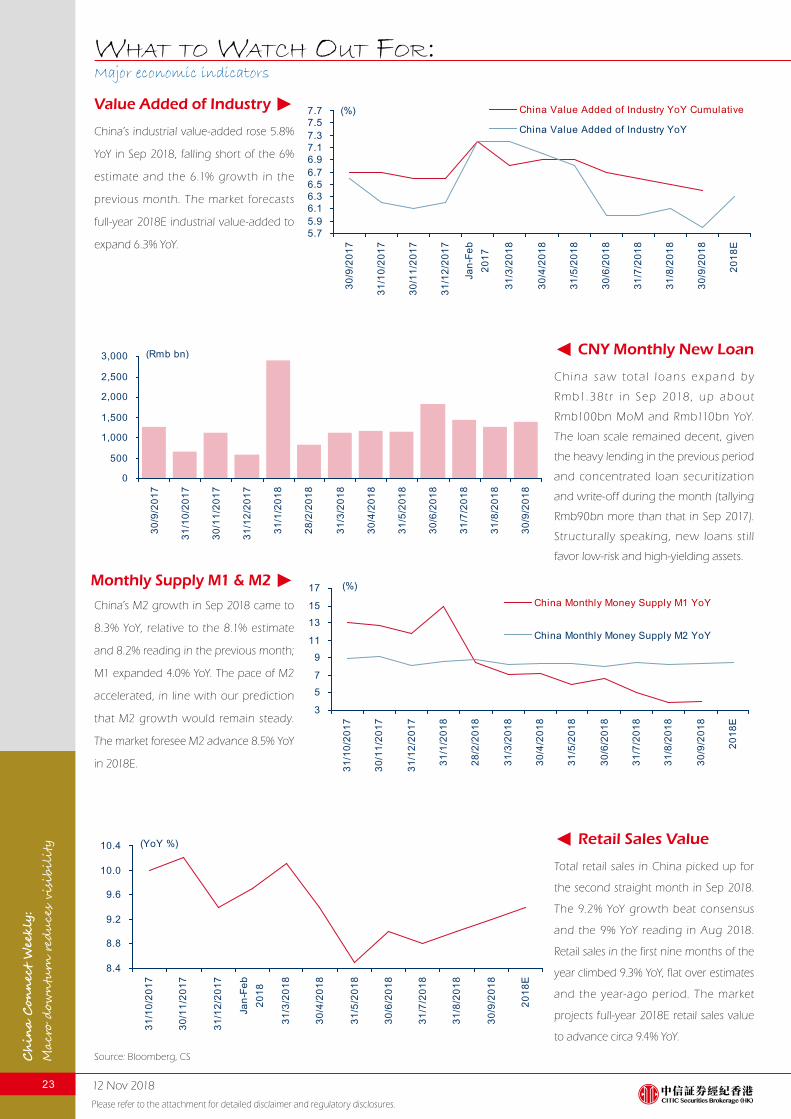

Value Added of Industry ►China’s industrial value-added rose 5.8%

YoY in Sep 2018, falling short of the 6%

estimate and the 6.1% growth in the

previous month. The market forecasts

full-year 2018E industrial value-added to

expand 6.3% YoY.

Monthly Supply M1 & M2 ►China’s M2 growth in Sep 2018 came to

8.3% YoY, relative to the 8.1% estimate

and 8.2% reading in the previous month;

M1 expanded 4.0% YoY. The pace of M2

accelerated, in line with our prediction

that M2 growth would remain steady.

The market foresee M2 advance 8.5% YoY

in 2018E.

◄ Retail Sales Value

Total retail sales in China picked up for

the second straight month in Sep 2018.

The 9.2% YoY growth beat consensus

and the 9% YoY reading in Aug 2018.

Retail sales in the first nine months of the

year climbed 9.3% YoY, flat over estimates

and the year-ago period. The market

projects full-year 2018E retail sales value

to advance circa 9.4% YoY.

◄ CNY Monthly New Loan

China saw tot a l loans expand by