Embed Size (px)

Citation preview

2018 Commerce and Payments Outlook

First Data Information and

Analytics Solutions

This document is a collection of opinions that are offered solely as a courtesy, and they do not represent

business or legal advice. The research is gathered from a wide range of industry publications, analyst reports,

white papers, websites, and interviews. The statements in this document related to future business or financial

performance may constitute forward-looking statements and actual results or performance may vary.

2

2018 Payment industry outlook

Top trends

Retailer and

Technology

Partnerships

Augmented Reality

and Virtual Reality

Delivery Changing

Physical Retail

Artificial Intelligence

Banking

Environment

On-Demand Services

in Physical Retail

Retailers Trying Smaller Stores

Mobile Only

Bank Accounts

Retail Digital Deals

Rental &

Subscription

Services

PSD2

Alipay & WeChat pay

Chinese Mobile Wallets

IoT Collaboration

P2P 2.0

FinTechs Eye

Bank Status

Blockchain

© 2018 First Data Corporation. All Rights Reserved.

All trademarks and trade names referenced in this material are the property of their respective owners.

3

Retailers – smaller is better?

Retailers testing smaller physical stores Why small-stores?

Response to shifting consumer demands, growing

populations in metro areas, and increased online shopping

Scaled-back spaces can be more profitable

per square foot

Forces retailers to be smarter about inventory and can

serve as a location for online pick up/returns

Allows retailers to tailor product offerings to the local

area, making the experience feel more personal

Overall, retailers are aiming to become a more desirable

place to shop

Sources: Company websites; “How Department Stores Will Re-Invent Themselves in 2018,” CNBC,

December 2017.

In the rise of online shopping, big-box retailers are experimenting with smaller brick-and-mortar stores

© 2018 First Data Corporation. All Rights Reserved.

All trademarks and trade names referenced in this material are the property of their respective owners.

4

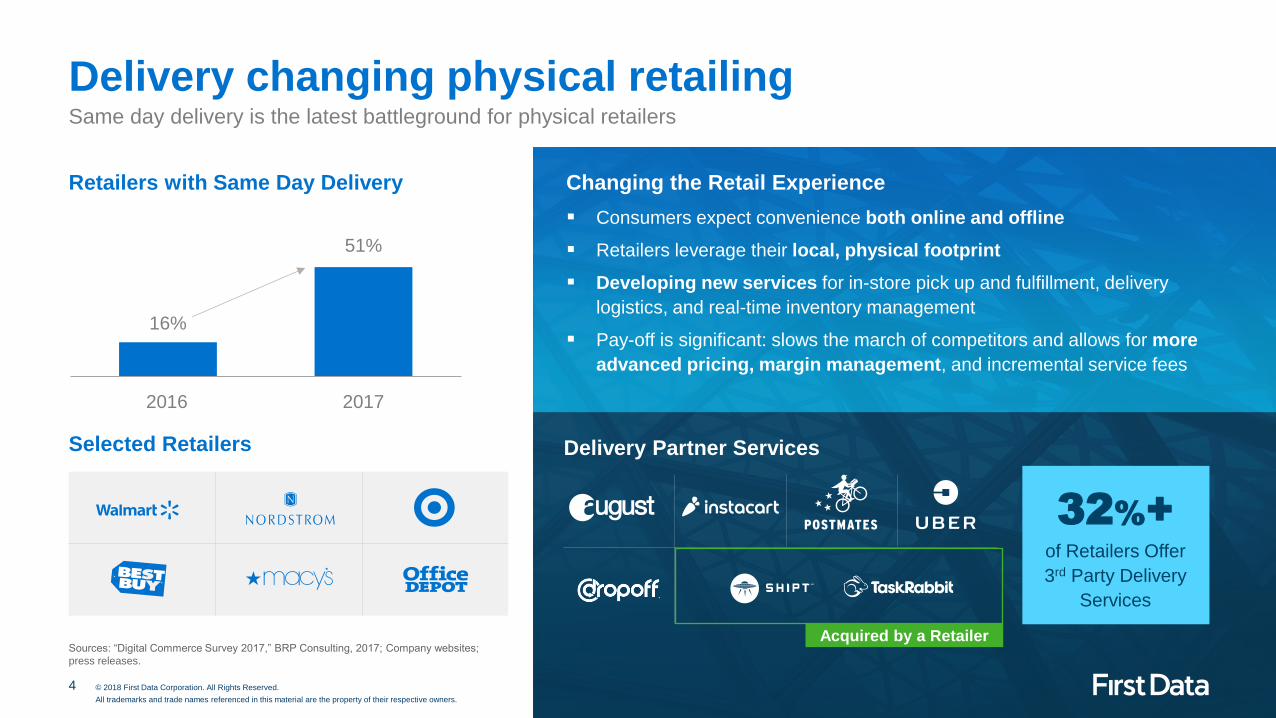

Delivery changing physical retailing

Retailers with Same Day Delivery

16%

51%

Selected Retailers

2016 2017

Changing the Retail Experience

Consumers expect convenience both online and offline

Retailers leverage their local, physical footprint

Developing new services for in-store pick up and fulfillment, delivery

logistics, and real-time inventory management

Pay-off is significant: slows the march of competitors and allows for more

advanced pricing, margin management, and incremental service fees

Delivery Partner Services

of Retailers Offer

3rd Party Delivery

Services

32%+

Acquired by a Retailer Sources: “Digital Commerce Survey 2017,” BRP Consulting, 2017; Company websites;

press releases.

Same day delivery is the latest battleground for physical retailers

© 2018 First Data Corporation. All Rights Reserved.

All trademarks and trade names referenced in this material are the property of their respective owners.

…to offer home improvement

professionals and advice to customers.

…a marketplace of service providers

where customers can shop for

professional service help.

…to create an omnichannel tech

services platform to provide IT support

services to business customers.

…to strengthen its digital customer

service capabilities and expand its

home goods and installation offerings.

acquires… acquires…

offers… partners with…

On-demand services meets physical retailing

The “gig” economy

(on-demand services)

coming to more stores

near you

5 © 2018 First Data Corporation. All Rights Reserved.

All trademarks and trade names referenced in this material are the property of their respective owners.

Sources: Company websites.

6

The rise of rental and subscription retail

The concept gained prominence with startups… …and is now spreading to larger retailers

+

© 2018 First Data Corporation. All Rights Reserved.

All trademarks and trade names referenced in this material are the property of their respective owners.

Consumers want value, flexibility, and personalized discovery

7

Retail deals for digital

Add digital capabilities Strengthen eCommerce reach Connecting with customers

Online shopping

Product selection

Logistics

Mobile

Chat / messaging

Personalization

AR / VR / 3D

Big data

Robotics / automation

© 2018 First Data Corporation. All Rights Reserved.

All trademarks and trade names referenced in this material are the property of their respective owners.

Sources: “The state of the deal: M&A trends 2018,” Deloitte, November 15, 2017.

Increasingly retail and digital/technology are converging

Traditional retailers are turning to startup M&A to catch up on the retail transformation

8

Retailer and technology partnerships

Why partner? – If you can’t beat them, join them.

Increase customer traffic and expand online presence

Ensure a position on the next generation of platforms (i.e. voice-ordering, smart home products)

Partnerships highlight retailers’ willingness to increase dependence on shopping and payments technology

Notable new partnerships made between retailers and tech giants:

© 2018 First Data Corporation. All Rights Reserved.

All trademarks and trade names referenced in this material are the property of their respective owners.

Sources: Company websites.

Unexpected partnerships are formed as competition increases, particularly in rise of voice-ordering

© 2018 First Data Corporation. All Rights Reserved.

All trademarks and trade names referenced in this material are the property of their respective owners.

9

All aboard for IoT collaboration

Industries working

together through

connected commerce to

reach more households.

Retailers Tech

Banks

Auto

Third Party

Developers

Devices &

Appliances

Travel &

Entertainment

Grocery &

Restaurant

Insurance

Content

CONNECTIVITY

10

Augmented reality and virtual reality in retail

Augmented Reality: It’s Real

But Virtual

Reality…?

Sources: Warby Parker app; Amazon app; The Verge 10/25/17; “Lowe’s Introduces In-Store Navigation Using Augmented Reality,” Lowe’s

press release, 3/23/17; Dailymail; “VR: The Brands that are imagining a new commerce reality,” Forbes, March 7, 2017.

Two powerful technologies could reshape commerce, but we believe

AR may be the winner

© 2018 First Data Corporation. All Rights Reserved.

All trademarks and trade names referenced in this material are the property of their respective owners.

11

Artificial intelligence boosts retail and banking

Trading

Process

Automation

Chat

Bots

Contact

Centers

Fraud

Detection

Loan

Underwriting

Identity

Verification

Personal

Financial Mgmt.

uses AI to target ads to individuals based on what

they are talking about on social platforms.

uses AI-based machine learning to offer consumers

a personalized clothing subscription service.

uses AI-based voice technology in its call centers

to route customer complaints to the appropriate experts.

uses AI to enhance real-time fraud detection and to

increase the accuracy of transaction approvals.

Sample Uses Cases

© 2018 First Data Corporation. All Rights Reserved.

All trademarks and trade names referenced in this material are the property of their respective owners.

Sources: Company websites.

Utilizing machine learning and AI to strengthen products and services and streamline operations

Fashion &

Beauty

Recommendations

Chat

Bots

Local

Experiences

Voice-activated

Assistants

Sales

forecasting

Targeted/

Personalized

ads

Promotion

Management

Merchants Banks

12

Alipay and WeChat pay

MOBILE WALLET USERS

Undisputed Mobile Wallet Leaders WeChat Diving into MicroPayments Alipay Expanding Throughout Asia

© 2018 First Data Corporation. All Rights Reserved.

All trademarks and trade names referenced in this material are the property of their respective owners.

Sources: Press releases; web sites; China Academy of Information and Communications Technology.

Chinese mobile wallets are forging into new frontiers

600M

529M

210M

87M

60M

WeChat Pay

Alipay

PayPal

ApplePay

Klarna

Tips often range from as little as

$0.15 to

$1.50 +10%

Of WeChat users have

micro tipped

13

Blockchain’s great uphill climb

Enterprises Moving out of the

Research Lab

Technical

Advancement Blockchain’s Challenges

Blockchain’s Hope

Too often blockchain experiments

are tech solutions in search of a

business problem

Massive speculation in

cryptocurrencies creates noise and

negative connotations

Solving for the fiat currency

on/off ramp

Advancements in speed

(Layer 2)

Development of so-called

“interledgers” to connect disparate

ledgers (bitcoin, XRP)

Flood of capital into cryptocurrency

markets could drive accelerated

innovation

Sources: Forrester: Predictions 2018.

Corporates on the

Hype Machine

80% of Blockchain projects

fail to meet expectations

© 2018 First Data Corporation. All Rights Reserved.

All trademarks and trade names referenced in this material are the property of their respective owners.

Distributed ledger gains are being overshadowed by the cryptocurrency hype cycle

14

Banking outlook

0%

2%

4%

6%

2014A 2015A 2016A 2017E 2018E

Key themes in 2018

Bull Case

Fed Raises Interest Rates

Three-to-Four Times

Strong Economy Supports Benign

Credit Outlook

Favorable Regulatory Environment

Bear Case

Low Single-Digit Loan

Growth

Yield Curve Continues to

Flatten

Tech Spend Weighs on

Operating Leverage

Revenue growth

Sources: FDIC Quarterly Profile; Thomson Reuters Eikon; S&P.

Note: Growth rates from 2015-2017 come from the FDIC’s Quarterly Banking Profile. Forecasted growth

for 2018 looks at aggregate Wall Street estimates for the S&P Bank Index.

We expect the operating environment to remain

favorable for the banks

Wall Street Expects Mid-Single Digit Revenue

Growth to Continue

© 2018 First Data Corporation. All Rights Reserved.

All trademarks and trade names referenced in this material are the property of their respective owners.

15

Banking and technology

0

100

200

300

1999 2001 2003 2005 2007 2009 2011 2013 2015 2017

New U.S. Bank Charters

Despite all the innovation in

FinTech, new bank charters

are at an all time low.

OCC Head Joseph Otting Supports the

Creation of a FinTech Charter1

Square’s ILC Application Could Set a

Precedent for Other FinTech Companies

Regulatory Bodies Around the World

Are Adjusting Rules for FinTech2

Key Things to Watch

© 2018 First Data Corporation. All Rights Reserved.

All trademarks and trade names referenced in this material are the property of their respective owners.

Sources: 1) “FinTech Charter Is Still in Play”, The Wall Street Journal, December 201, 2017, 2) “Fine Tuning Licenses for Banks”, ECB, November 15, 2017.

2018 could open the door for more FinTech companies to become banks

16

US banks offer mobile only accounts

Common features

Mobile checking and savings account opening

Offers a debit card, but no physical checks

Remote deposit capture

Send money

No overdraft fees

Spend tracking and tagging

Savings tools

Bills management

© 2018 First Data Corporation. All Rights Reserved.

All trademarks and trade names referenced in this material are the property of their respective owners.

Sources: Company websites.

Big banks target millennials and the underserved with mobile only banking alternatives

All Mobile Banking Apps

17

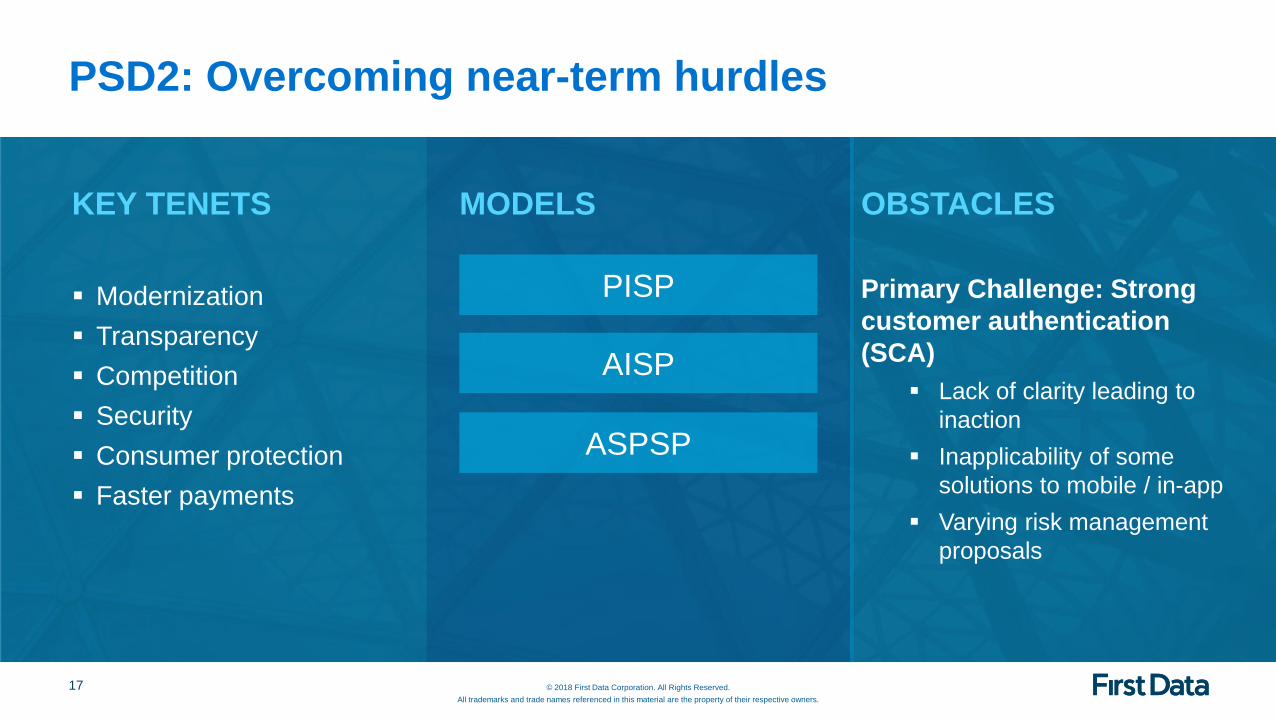

PSD2: Overcoming near-term hurdles

© 2018 First Data Corporation. All Rights Reserved.

All trademarks and trade names referenced in this material are the property of their respective owners.

KEY TENETS MODELS OBSTACLES

Modernization

Transparency

Competition

Security

Consumer protection

Faster payments

PISP

AISP

ASPSP

Primary Challenge: Strong

customer authentication

(SCA)

Lack of clarity leading to

inaction

Inapplicability of some

solutions to mobile / in-app

Varying risk management

proposals

P2P Payments to

Exceed $120B this Year Zelle Makes

it Debut

Big Banks Show

Major P2P Growth Venmo Now Accepted

at 2M Merchants US Bank Announces

Disbursements via Zelle

PYPL Buys Tio

Networks for $223M

18

P2P 2.0: In pursuit of financial relevance

P2P 1.0 – Consumer Only, Limited Revenues P2P 2.0 – New Ways to Pay

Businesses Consumer

P2P Apps

Merchants

Billers

© 2018 First Data Corporation. All Rights Reserved.

All trademarks and trade names referenced in this material are the property of their respective owners.

Sources: Press releases

Venmo, Zelle, et al pivot towards merchant and biller payments

19