Embed Size (px)

Citation preview

i

ALLIANCE FINANCE COMPANY PLC | ANNUAL REPORT 2015/16

ANNUAL REPORT 2015/16

ii

ALLIANCE FINANCE COMPANY PLC | ANNUAL REPORT 2015/16

Alliance Finance Company PLC, the 3rd oldest finance company in Sri Lanka celebrated six decades of successful business operations on 18th July 2016.

Starting from humble beginnings in 1956, AFC has strived over a period of 60 years to strike a perfect balance and harmony between the interests of the multiple stakeholder groups that it represents. With a genuine concern for the well-being of our depositors, hirers, employees and shareholders, we have strived to meet the differing needs and aspirations of each and every one of them.

Achieving this balance over a sustained period of time has made the journey of 60 years a most fulfilling and gratifying one.

As we embody our core values of trust and innovation in an integrated People, Planet, Profit business philosophy, we look forward to maintaining this balance and continuing our journey steadfastly into the future, whilst embracing the exciting challenges and opportunities that await us.

1

ALLIANCE FINANCE COMPANY PLC | ANNUAL REPORT 2015/16

2

ALLIANCE FINANCE COMPANY PLC | ANNUAL REPORT 2015/16

3

ALLIANCE FINANCE COMPANY PLC | ANNUAL REPORT 2015/16

VisionTo be the most respected Licensed Finance Company in Sri Lanka, delivering superior stakeholder returns whilst supporting financial inclusion and social and environmental sustainability.

Mission To uphold the highest standards of social and environmental sustainability by delivering inclusive and innovative financial solutions to uplift the lives of people, whilst ensuring a superior experience for all our stakeholders

Core Values1. People CentricPeople includes all our stakeholders with a special emphasis on customers and staff. We consider customers as our first priority and provide what they need, ensuring their utmost satisfaction. Staff is our greatest asset and we value the voice of our staff and maintain an open door policy in the office premises to encourage dialogue.

2. IntegrityWe maintain the highest standards of integrity and accountability in all we say and do. We also strive to uphold customer trust earned throughout the period of our stand, by being committed to the highest levels of transparency. In addition to this, aligning to international standards of Social Performance Management with close monitoring of our impact created though Microfinance, we continue to

be a company accountable in providing responsible finance solutions to all our clients.

3. InnovationWe strive to keep our forward march steady in the current turbulent industry environment by positively undertaking various innovations to drive us ahead, whilst strengthening research and development to make innovation a continuous process.

4. Serve People & Conserve NatureWhilst adhering to the concept of triple bottom line, we as a company place high priority on social and environmental sustainability, with which the long term goals of the Company are strongly entwined.

5. DynamicThe business environment today is subject to rapid changes and is therefore very turbulent. Being dynamic is about keeping pace in the ever changing landscape and taking responsive action in order to meet challenges and surge ahead of the competition.

6. UnityWe take pride in the cohesion of the workforce in the Company working towards a common goal and it is a value that can only be created not infused. “All for one and one for all” philosophy has always been a key driving force of the Company’s success and we strive to maintain its consistency throughout.

4

ALLIANCE FINANCE COMPANY PLC | ANNUAL REPORT 2015/16

CONTENTS

overviewAbout AFC 6About This Report 6Financial Highlights 8Non-Financial Highlights 9Triple Bottom Line Achievements 10Economic Performance - Contribution to National Economy 11Milestones 12Awards, Certifications, Affiliations and Credit Rating 16Chairman’s Review 18Message from the Senior Advisor and past Chairman 21Deputy Chairman/ Managing Director’s Review 22

6-22Management Discussion and analysis

stewardship

AFC Sustainability Approach 32Stakeholder Engagement Approach 33Materiality assessment / Materiality Matrix 39Supply Chain Management 41Review on the Economic Environment 43SWOT Analysis 46Financial Review 48Operations Review 54Social and Environmental Review 65 Our Social Footprint 65 Customer and Product Responsibility 69 Human Capital 74 Our Environmental Footprint 82Support Services 85Geographic Footprint 96GRI G4 Index Table 101

Board of Directors 114Corporate Management 118Senior Management 120Corporate Governance 126Risk Management 134

32-101

114-134

5

ALLIANCE FINANCE COMPANY PLC | ANNUAL REPORT 2015/16

Financial InformationAnnual Report of the Directors 144Directors’ Statement on Internal Control Over Financial Reporting 148Directors’ Responsibility for Financial Reporting 149Report of the Audit Committee 150Independent Auditors’ Report 152Statement of Profit or Loss 153Statement of Comprehensive Income 154Statement of Financial Position 155Statement of Changes in Equity 156Statement of Cash Flows 157Significant Accounting Policies 158Notes to the Financial Statements 176Capital Adequacy Ratio 231

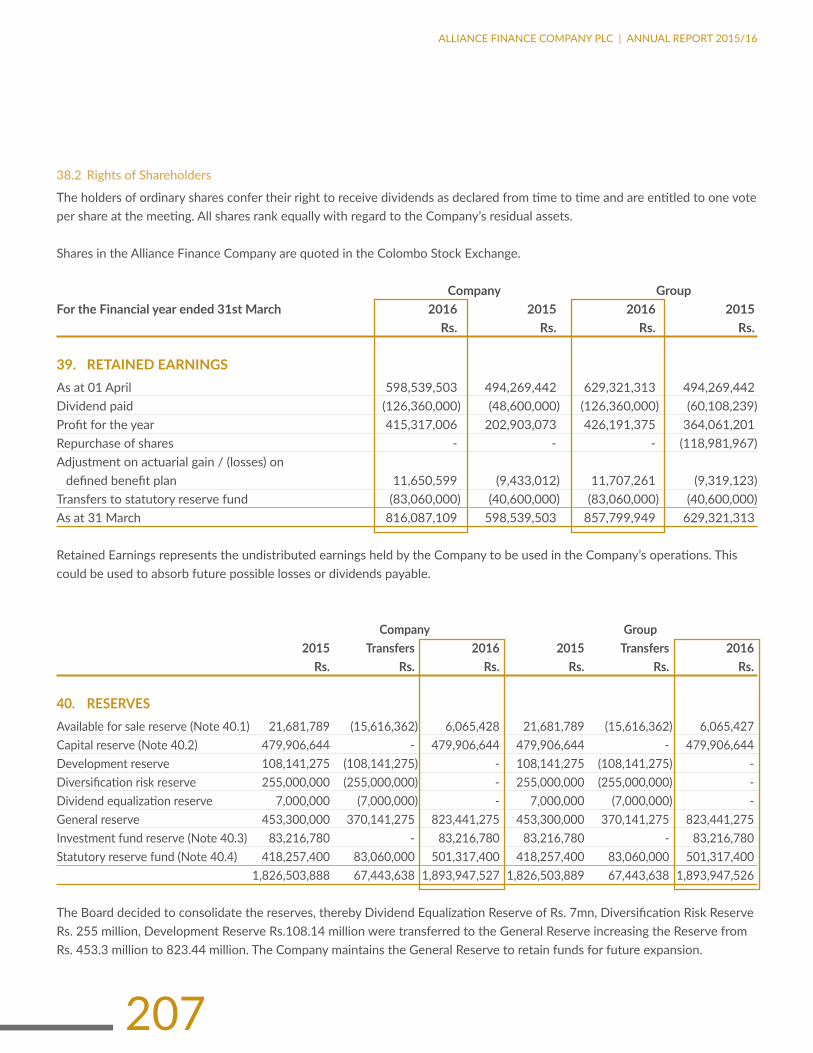

Other informationContribution to National Economy 232Depositors Information 233Debenture Investor Indicators 235Ten Year Summary - Company 236Shareholder Information 237Glossary 238

232-238

144-231Statutory InformationNotice of Meeting 241Notes 242Form of Proxy 243Corporate Information Inner Back Cover

241-iBC

6

ALLIANCE FINANCE COMPANY PLC | ANNUAL REPORT 2015/16

This report encompasses the entire operation of Alliance Finance Company PLC (AFC), strongly interwoven with the Triple Bottom Line; also covering the financial, social and environment sustainability strides of the Company. It also covers the overall strategy and future plans of the Company.

The information is presented in a more coherent, holistic and transparent manner with the intention that this report will give a clear and concise picture of our performance in terms of value creation over the short, medium and long term to all our stakeholders for their informed assessment and decisions.

Report ScopeIn the previous financial year, AFC produced the first integrated report, in compliance with Global Reporting Initiative G3 standards, which was received by the stakeholders with positive remarks. This time, AFC seeks to prepare a Sustainability Report where the sustainability performance is reported in line with the Global Reporting Initiative G4 standards. This report contains standard disclosures from the GRI sustainability guidelines. The GRI Content Index is given on pages 101-111 in this Annual Report.

Report Boundary The Annual Report contains information covering the Company’s operations of the Head Office and the branch network for the financial year ended 31st March 2016. The indicators and performance of the previous year is stated in places where comparative analysis is being used for interpretation and illustrations.

Moreover, the report also provides summary reviews on the performance of AFC’s two subsidiaries, Alfinco Insurance Brokers Private Limited and Macbertan Private Limited, for the financial year ended 31st March 2016.

MaterialityThe presentation of the information of this Annual Report has focused the most material aspects to AFC and its key stakeholders. AFC considers those aspects as the most vital pillars on which the business is built on and the future business will rely upon. The materiality

AbOuT AFC AbOuT ThiS REpORT

Alliance Finance Company PLC (AFC) is a Quoted Public Limited Liability Company incorporated under the Companies Ordinance No. 51 of 1938. The Company was approved and registered under the Finance Business Act No. 42 of 2011, Finance Leasing Act No. 56 of 2000 and is also an approved Credit Agency under the Mortgage Act No.6 of 1949 and Trust Receipt Ordinance No.12 of 1947. The Company operates from its head office in Colombo and with a network of 87 points of presence island wide. The Company’s corporate information is listed on the page inner back cover of this report.

7

ALLIANCE FINANCE COMPANY PLC | ANNUAL REPORT 2015/16

assessment and the basis of their materiality determination are given in the Materiality Assessment section on pages 39-40 of this report.

ComplianceThis Annual Report is prepared for the period starting from 1st April 2015 to 31st March 2016, complying with the general annual report cycle of the Company, for both financial and sustainability reporting. Consequently, the financial performance of the Company has been reported in compliance with the Sri Lanka Financial Reporting Standards (SLFRS) and Sri Lanka Accounting Standards (SLAS) promulgated by the Institute of Chartered Accountants of Sri Lanka. Where applicable, the Company has followed the rules and regulations of the following as well.

• Directions and rules of the Central Bank of Sri Lanka

• Companies Act No. 07 of 2007• Finance Business Act No. 42 of 2011• Finance Leasing Act No. 56 of 2000• The Listing Rules of the Colombo

Stock Exchange

The disclosures on Corporate Governance have been done in accordance with the Corporate Governance Direction No. 3 of 2008 issued by the Central Bank of Sri Lanka and the listing rules of the Colombo Stock Exchange.

External Assurance External assurance for the Financial Statements and the related notes is given by M/s. Baker Tilly Edirisinghe and Company through their audit and their assurance is given on page 152 of this Annual Report. There has been no external assurance taken this time for the sustainability content of the report.

PresentationoftheReportThe Annual Report will be presented in both printed and electronic formats this year. All the shareholders will be given the report in the form of a CD-ROM and the same will be available on the official web page of AFC (www.alliancefinance.lk) in PDF format. As a measure of reducing the carbon footprint of the Company, the printed copies of this report will only be posted on request to those who need it in that format.

AbOuT ThiS REpORT

ContactforQueriesFor any inquiries on this Annual Report 2015/16 or any information included therein to be informed and obtained from the contact below.

The Chief Financial OfficerAlliance Finance Company PLC84, Ward PlaceColombo 07SRI LANKATel: +94 112 673 673Fax: +94 112 697 205Email: [email protected]

8

ALLIANCE FINANCE COMPANY PLC | ANNUAL REPORT 2015/16

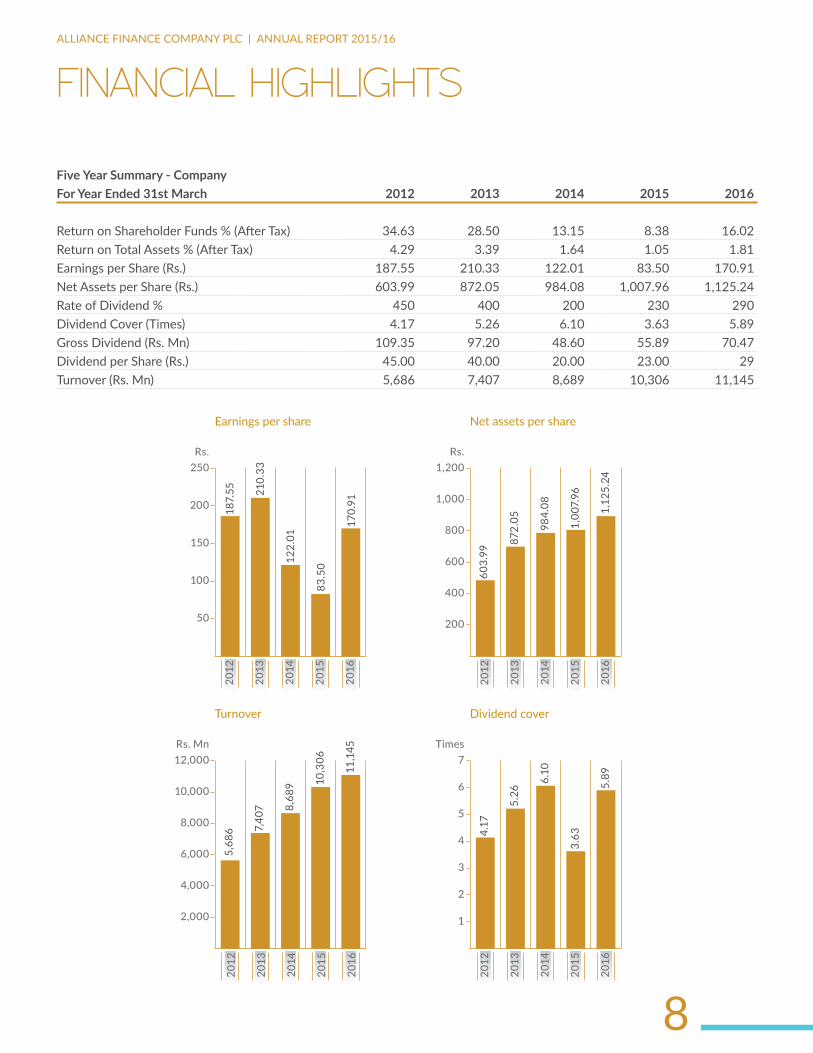

FiNANCiAl highlighTS

Five Year Summary - CompanyForYearEnded31stMarch 2012 2013 2014 2015 2016

Return on Shareholder Funds % (After Tax) 34.63 28.50 13.15 8.38 16.02Return on Total Assets % (After Tax) 4.29 3.39 1.64 1.05 1.81Earnings per Share (Rs.) 187.55 210.33 122.01 83.50 170.91Net Assets per Share (Rs.) 603.99 872.05 984.08 1,007.96 1,125.24Rate of Dividend % 450 400 200 230 290Dividend Cover (Times) 4.17 5.26 6.10 3.63 5.89Gross Dividend (Rs. Mn) 109.35 97.20 48.60 55.89 70.47Dividend per Share (Rs.) 45.00 40.00 20.00 23.00 29Turnover (Rs. Mn) 5,686 7,407 8,689 10,306 11,145

rs.

50

100

250

200

150

2012

2013

2014

2015

2016

Earnings per share

187.

55 210.

33

122.

01

83.

50

170.

91

rs. Mn

2,000

4,000

12,000

10,000

8,000

6,000

2012

2013

2014

2015

2016

Turnover

5,6

86 7,40

7 8,68

9 10,3

06

11,1

45

rs.

400

200

600

1,200

1,000

800

2012

2013

2014

2015

2016

Net assets per share

603.

99

872.

05

984.

08

1,00

7.96

1,12

5.24

Times

2

1

3

7

6

5

4

2012

2013

2014

2015

2016

Dividend cover

4.17

5.26

6.10

3.63

5.89

9

ALLIANCE FINANCE COMPANY PLC | ANNUAL REPORT 2015/16

NON-FiNANCiAl highlighTS

10 New PointsofPresence

3,570 Total no. oftraininghours

87 PointsofPresence 91

Trees Savedby Paper Recycling

6 Mn CSR investment

(Rs.)

14,000Trees planted forleasesgiven

2.3 Mn Employee training investment

(Rs.)

1,203 No.ofemployees

6 No.ofnewproducts introduced

10

ALLIANCE FINANCE COMPANY PLC | ANNUAL REPORT 2015/16

TRiplE bOTTOm liNE AChiEvEmENTS

Goals aspect achievements – 2015/16

People Return on Investment Shareholders Pre-tax ROE : 20.5%

People Development Employees Training investment : Rs. 2.7 MnNew Recruitments : 340

Improved quality of lifeCapacity Building

Customers Total number benefited : 133,984

Financial Inclusion Society CSR Investment : 6 MnNumber of EDS trainings conducted : 111Total number of EDS beneficiaries : 4,477

Profit Economic Value creation Economic Value created Total value : Rs. 1,560 Mn

Economic Value retention Economic Value retained Employee remuneration : Rs. 750.9 Mn

Government taxes : Rs. 353.2 Mn

Shareholder dividend : Rs. 70.4 Mn

Economic Value distribution

Economic Value distributed Allocation for Company expansion and growth : Rs. 384 Mn

Planet Reducing emissionAssist arresting global warming

Emission reduction/Cleaner and greener environment

Tree for a lease : Rs. 1.3 MnEco three wheeler : Rs. 0.3 Mn

Green financing solutionsEnergy conservation

Energy conservation Replacement of lighting system with LED bulbsEarth Hour celebration and 500 LED bulbs donation to Viharamahadevi park

Greener and Cleaner environment

Green Financing Hybrid and electric car leases at concessionary ratesLoans for Agriculture

11

ALLIANCE FINANCE COMPANY PLC | ANNUAL REPORT 2015/16

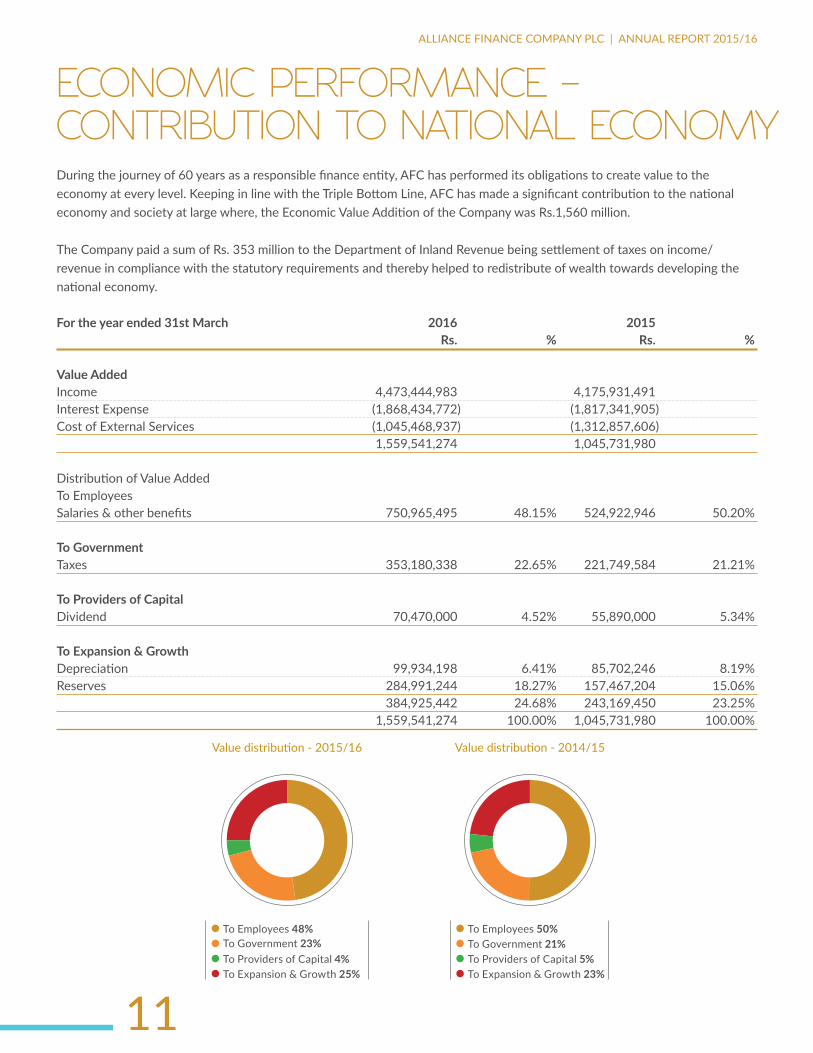

During the journey of 60 years as a responsible finance entity, AFC has performed its obligations to create value to the economy at every level. Keeping in line with the Triple Bottom Line, AFC has made a significant contribution to the national economy and society at large where, the Economic Value Addition of the Company was Rs.1,560 million.

The Company paid a sum of Rs. 353 million to the Department of Inland Revenue being settlement of taxes on income/ revenue in compliance with the statutory requirements and thereby helped to redistribute of wealth towards developing the national economy.

Fortheyearended31stMarch 2016 2015 Rs. % Rs. %

Value AddedIncome 4,473,444,983 4,175,931,491Interest Expense (1,868,434,772) (1,817,341,905)Cost of External Services (1,045,468,937) (1,312,857,606) 1,559,541,274 1,045,731,980

Distribution of Value AddedTo EmployeesSalaries & other benefits 750,965,495 48.15% 524,922,946 50.20%

To GovernmentTaxes 353,180,338 22.65% 221,749,584 21.21%

ToProvidersofCapitalDividend 70,470,000 4.52% 55,890,000 5.34%

ToExpansion&GrowthDepreciation 99,934,198 6.41% 85,702,246 8.19%Reserves 284,991,244 18.27% 157,467,204 15.06% 384,925,442 24.68% 243,169,450 23.25% 1,559,541,274 100.00% 1,045,731,980 100.00%

Value distribution - 2014/15

To Employees 50%To Government 21%To Providers of Capital 5%To Expansion & Growth 23%

Value distribution - 2015/16

To Employees 48%To Government 23%To Providers of Capital 4%To Expansion & Growth 25%

ECONOmiC pERFORmANCE – CONTRibuTiON TO NATiONAl ECONOmy

12

ALLIANCE FINANCE COMPANY PLC | ANNUAL REPORT 2015/16

The Deposit base surpasses a milestone of Rs.

100 Million

AFC moves into “Alliance House” – a

new, three-storied complex which is

today a well-known landmark in the city

milESTONES

AFC was incorporated on 18th

July 1956 at No. 43, Campbell Place

Colombo 8 with the motto “Earn before

you spend & Others before self”

The Company’s shares quoted in the

Colombo Brokers’ Association

Deposit base surpasses Rs.

One million

Acquired “Arpico Finance”

AFC purchases the land and buildings at

No. 84 Ward Place Colombo 7

Commemorated the Company’s

Silver Jubilee

1993

19941956 1965

1967

1969

19811959

13

ALLIANCE FINANCE COMPANY PLC | ANNUAL REPORT 2015/16

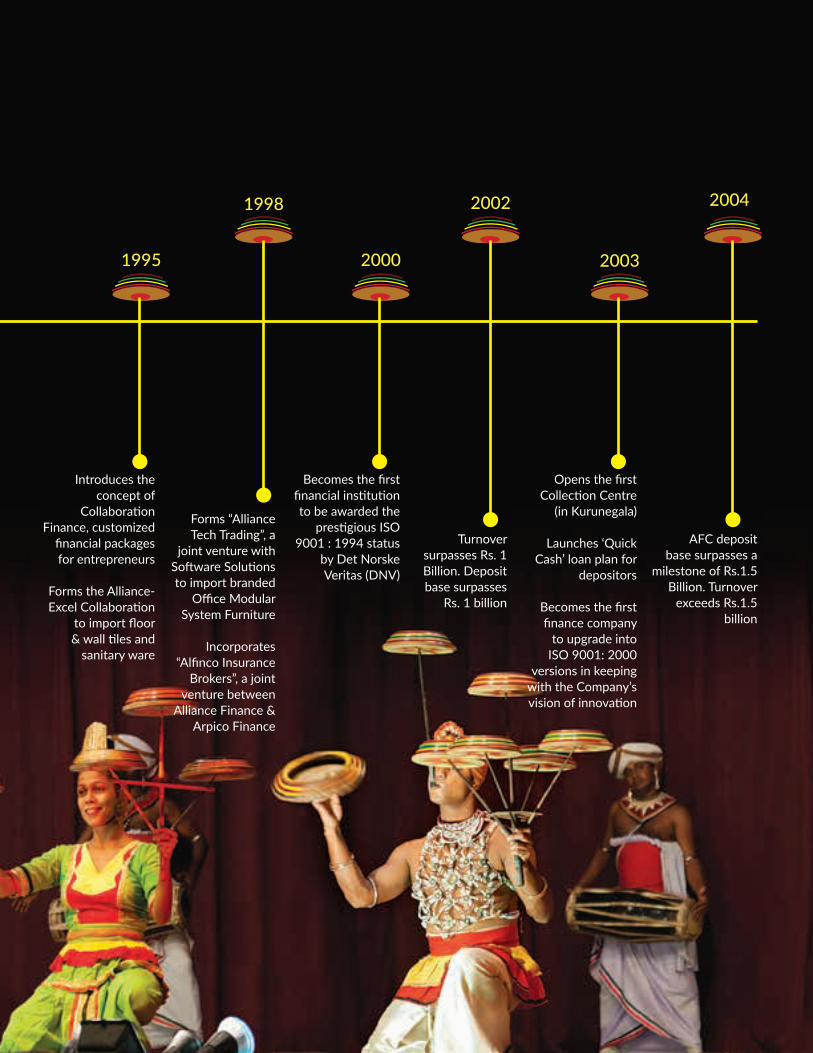

Introduces the concept of

Collaboration Finance, customized

financial packages for entrepreneurs

Forms the Alliance-Excel Collaboration

to import floor & wall tiles and

sanitary ware

Forms “Alliance Tech Trading”, a

joint venture with Software Solutions to import branded

Office Modular System Furniture

Incorporates “Alfinco Insurance

Brokers”, a joint venture between

Alliance Finance & Arpico Finance

Becomes the first financial institution to be awarded the

prestigious ISO 9001 : 1994 status

by Det Norske Veritas (DNV)

Turnover surpasses Rs. 1 Billion. Deposit base surpasses

Rs. 1 billion

Opens the first Collection Centre

(in Kurunegala)

Launches ‘Quick Cash’ loan plan for

depositors

Becomes the first finance company

to upgrade into ISO 9001: 2000

versions in keeping with the Company’s vision of innovation

AFC deposit base surpasses a

milestone of Rs.1.5 Billion. Turnover

exceeds Rs.1.5 billion

1995 2000

2002

2003

1998 2004

14

ALLIANCE FINANCE COMPANY PLC | ANNUAL REPORT 2015/16

Ms. Sonali de Silva, a

Non-Executive Director is

appointed as Chairperson on 31st May

2011

Alliance Finance becomes the Joint Winner (with

Peoples’ Leasing Company) of the Gold Award at

the National Business Excellence Award 2012

Also wins the overall Silver Award for “The Best

Management Practices” at the National Business Excellence Awards 2012

Becomes the first Sri Lankan company in the Banking

and Non-Banking Finance Sector to receive the

British Standard for BCMS Certification (Business

Continuity Management System)

The Company initiates a greater effort to

communicate its commitment to a Triple

Bottom Line philosophy, and thus a symbolic wave in colours of Blue, Green

and Orange is introduced to all its brand communiqué

signifying and reminding all stakeholders of its

commitment to PEOPLE, PLANET and PROFIT

The Company launches its first TV Commercial

milestones Contd.

Becomes the first finance company

to introduce Savings Accounts

Obtains ISO 9001 : 2000

certification for the Company’s

Motor Division, becoming the

second garage to be certified in Sri

Lanka

Celebrates the Company’s

Golden Anniversary.

Launches “Pride of Priority”,

a deposit scheme for

Senior Citizens with the offer

of an extra 1% interest

for their fixed deposits

The Company makes a new

addition to its product

portfolio with “Gold Loans”

The ISO certification

for Quality Management

System is upgraded to

the ISO 9001 : 2008 version

The Chairman and Joint

Managing Director Mr. Pratapkumar

de Silva retires from the

post of Joint Managing

Director and continues as

Chairman. Mr. Romani de

Silva continues as Deputy Chairman and takes

on the role of Managing

Director

2011

20122005

2009

201020082006

15

ALLIANCE FINANCE COMPANY PLC | ANNUAL REPORT 2015/16

In January, AFC becomes the first organization in Sri Lanka’s Finance and Non-

Banking Financial Sector to receive Certification for

BCMS (Business Continuity Management Systems) ISO

222301 : 012

Receives an international accolade for its Sustainable

Business products with a Merit Award at the Global Sustainable

Finance Conference held in Karlsruhe, Germany for the AFC

Ezy drive Green taxi service

Mr. Sunil Karunanayake is appointed as the Chairman of

AFC

AFC achieves its highest ever profit to date, with a Profit After

Tax of Rs. 511 Million and also records a net asset growth of

44%

The branch network is increased to 32 branches with a representation in every province

in Sri Lanka

Launches the Microfinance Division

In March, AFC was awarded the Asia Responsible Entrepreneurship Award for the Ezy

Drive gas taxi meter project at the award

ceremony held in New Delhi, India

AFC recorded the highest

investment of Rs. 10.6 Billion

AFC Chairman Mr. Sunil Karunanayake was awarded the Professional Excellence Award 2015 by the Institute of Certified Management Accountants of Sri Lanka (CMA) in recognition of his outstanding leadership capabilities

Successfully obtained the AFC’s inaugural foreign funding line from the prestigious Triodos Bank of

Netherlands. Along with that AFC also received its first FCY loan facility from Bangladesh as well

Microfinance SBU emerges as a dominant SBU in the Company structure, expanding its outreach by

completing 40 business locations

Introduced m-Cash pilot project in 15 branches for Microfinance clients, enabling a speedy recovery

process, facilitating efficiency

AFC took part in Rotary Sri Lanka’s One Million Trees Project, commenced in Kurunegala District as a step

forward in the “Tree for a Lease” initiative of the Company. Under the project, as of end-February 2016,

AFC had contributed 14,000 trees for 13,550 leases given during that period of the financial year

For the first time, AFC joins hands with Associated Motorways (Private) Limited (YAMAHA) to promote two

wheelers to prospective AFC customers

Completes the clearance of the drawbacks due to the Gold Loan industry crisis

2016

2013

2014

2015

16

ALLIANCE FINANCE COMPANY PLC | ANNUAL REPORT 2015/16

AwARdS, CERTiFiCATiONS, AFFiliATiONS ANd CREdiT RATiNg

17

ALLIANCE FINANCE COMPANY PLC | ANNUAL REPORT 2015/16

awarding Body awarded For award/accolade received Category Year

1 ICASL Annual Report Certificate of Recognition Non-Banking and Finance Sector 2015

2 EA Asia Responsible Entrepreneurship

Winner Green Leadership 2014

3 EOSD EZY Taxi Merit Certificate Best Innovation in Sustainable Financial Products and Services

2013

4 ICASL Annual Report Certificate of Recognition Non-Banking and Finance Sector 2013

5 DNV BCMS ISO 22301 Not Applicable 2013

6 NCCSL NBEA Gold - Joint winner Non-Banking and Finance Sector 2012

7 NCCSL NBEA Silver Performance Management Practices - Overall 2012

8 ICASL Annual Report Certificate of Recognition Non-Banking and Finance Sector 2012

9 BSI BCMS BS25999 Not Applicable 2012

10 NCCSL NBEA Silver Specialised Banking and Finance Sector 2011

11 ICASL Annual Report Certificate of Recognition Non-Banking and Finance Sector 2011

12 ICASL Annual Report Certificate of Recognition Non-Banking and Finance Sector 2010

13 ICASL Annual Report Certificate of Recognition Non-Banking and Finance Sector 2009

BSI - British Standards Institution EA - Enterprise Asia DNV - Det Norske VeritasEOSD - European Organisation for Sustainable DevelopmentICASL - Institute of Chartered Accountants of Sri LankaNCC - National Chamber of Commerce of Sri Lanka

Certifications• AFC is the first finance company in Sri Lanka to be awarded an ISO certification

• The Company became the first and the only finance company in Sri Lanka to be awarded ISO 22301 – the only accepted global standard for Business Continuity Management

Affiliations• Member of the Finance Houses Association of Sri Lanka

• Member of the Leasing Association of Sri Lanka

• Member of the Ceylon Chamber of Commerce

CreditRating• Rated BB+ (lka) by Fitch Ratings Lanka Limited

18

ALLIANCE FINANCE COMPANY PLC | ANNUAL REPORT 2015/16

For six decades Alliance Finance Company plC has established an indelible position in the NbFi sector that is built on trust, stability, enduring relationships and friendship.

ChAiRmAN’S REviEw

Dear Shareholders,It gives me immense pleasure to place before you the progress and achievements of Alliance Finance Company PLC (AFC) for the financial year 2015/16.

As we are all aware, Alliance Finance Company PLC is one of our country’s foremost and pioneering Non-Bank Financial Institution (NBFI) which proudly celebrated its 60th year of successful operation. For almost six decades Alliance Finance Company PLC has established an indelible position in the NBFI sector that is built on trust, stability, enduring relationships and friendship.

Emerging successfully from extremely volatile economic conditions that existed in the previous year, particularly affecting the financial sector due to vagaries in commodity prices and interest rates, the Company entered 2015/16 with increasing confidence and optimism. Launching many

19

ALLIANCE FINANCE COMPANY PLC | ANNUAL REPORT 2015/16

The Company has achieved commendable results considering the challenges faced during the year. whilst focusing on major goals which include industry positioning, credit rating and brand value the Company was able to achieve its strategic objectives of profitability, growth and sustainability.

strategic, operational and structural improvements, the Company was able to almost double its profitability during the year under review and will now look for further consolidation in order to sustain progress into the future.

Global EconomyThe global economic environment reflected a mediocre outlook in 2015. Whilst growth in advanced economies has somewhat increased, albeit marginally, the slowdown in emerging markets was noticeable as a result of falling global trade volumes and the uncertainty surrounding the scope and depth of the economic downturn in China.

Overall, global growth recorded around 3.1% during the year 2015 and is projected to remain below 4% in 2016. Emerging markets registered a 4.0% growth, mainly driven by China and India whilst Russia’s negative growth due to the fall in oil prices brought down the overall numbers for these economies.

Sri Lankan Economy2015 was a year of significant change in the Sri Lankan political landscape with the arrival of a new President in January and subsequently a new Government in the second half of the year. As a result of such eventful happenings, the country grappled with the usual challenges faced by a new Government. Although the global economic crisis did affect the local economy to some extent, Sri Lanka managed to escape relatively unscathed, recording single digit inflation and a GDP growth of 4.8% for the year based on the new methodology for measuring GDP introduced during the year.

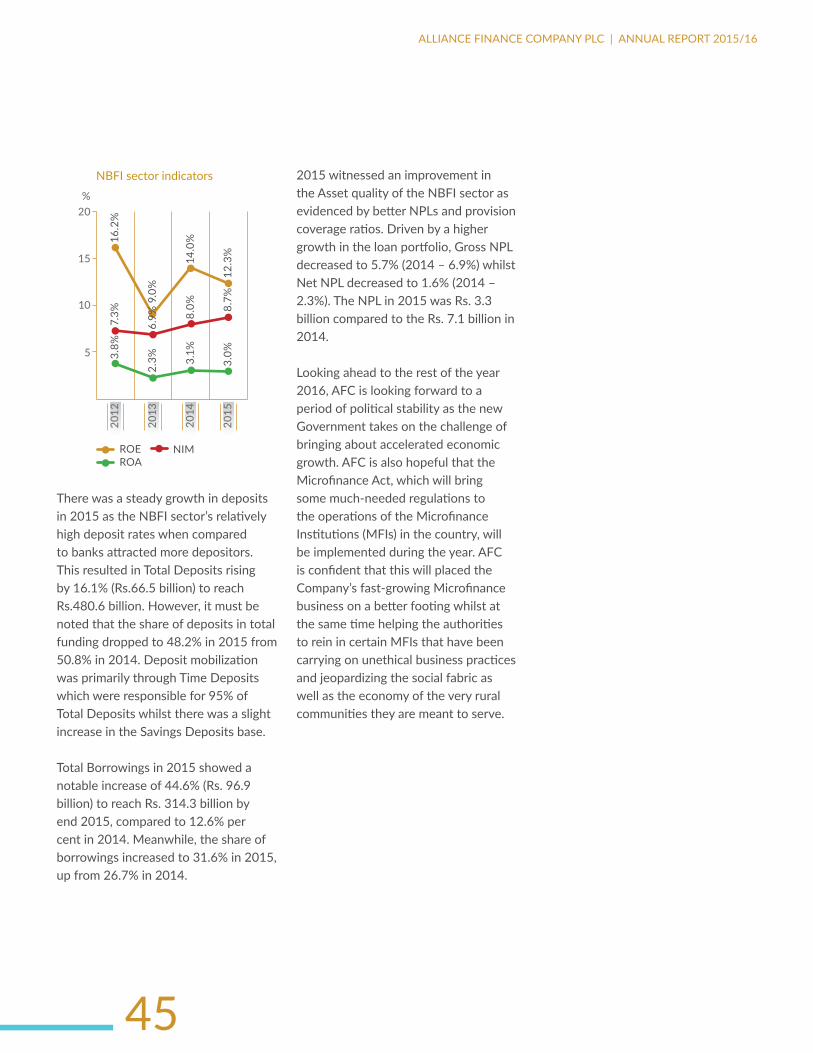

FinancialInstitutionSectorThe NBFI sector registered increased growth in assets and profitability, together with an expansion of branch and ATM networks. This was fuelled by the acceleration in loans and advances, in consumption activities driven by low interest rates and availability of relatively short-term funding from domestic and foreign sources. NBFIs were able to maintain adequate liquidity despite an increased reliance on short-term funding. Whilst profitability increased during 2015, the capital position remained well above the minimum regulatory requirement. The CBSL continued to introduce new prudent policy measures with a view to enhancing safety and soundness in the NBFI sector.

The introduction of regulations such as vehicle duties and a Loan To Value (LTV) ratio brought forward a new set of challenges to the NBFI sector during the year and companies were compelled to explore other avenues to increase their revenue. The low interest rate regime that was witnessed in the market enabled the sector to record a notable profit and maintain Non-Performing Loans at a manageable level. Further it is reported that credit has grown by 31.8% during the year 2015 compared to the previous year.

The drop in the global market price of gold that was prevalent in 2014/15 continued into 2015/16 resulting in a contraction of the Gold Loans portfolio across the NBFI sector. However, an increase in loans and advances took place in the sectors of construction, infrastructure, trading as well as financial and business services. Meanwhile, with Microfinance emerging

20

ALLIANCE FINANCE COMPANY PLC | ANNUAL REPORT 2015/16

as a key element in driving economic growth amongst rural communities, the NBFI sector is expected to continue to play a key role serving customers at the grass root level of the economy.

Year in ReviewThe Company has achieved commendable results considering the challenges faced during the year. Whilst focusing on major goals which include industry positioning, credit rating and brand value the Company was able to achieve its strategic objectives in profitability, growth and sustainability.

The importance of the Microfinance SBU was further highlighted during the year. Although the SBU remained one of the key drivers and expanded its outreach to 40 branches, in keeping with our balanced approach, the Company focused on maintaining a sustainable growth rather than proceeding with an overly-aggressive approach.

The Company continued its focus on reducing its Gold Loan Portfolio by disposing matured stock during the year and was successful in reducing its Gold Loan exposure to a mere 2%. The setback caused by the dependency on the exposure to Gold loans has duly been mitigated thereby bringing in a more conducive environment for future profitable growth.

AFC’s organizational structure was further strengthened with the appointment of highly-experienced individuals to spearhead development. During the year, we welcomed Mr. Mahinda Gunasekera to the Board as Director Sustainability. Mr. Gunasekera’s vast experience in the fields of SME finance, livelihood

development, Microfinance and agri business will allow us to introduce ground-breaking initiatives and respond positively to external dynamics. He will play a key role in the area of our Microfinance business with his proven experience and expertise in this vital sector. Meanwhile, Mr. Emmanuel Muttupulle, who retired from the Board on reaching the age of 70, continued to function in the capacity of Chief Operating Officer (COO) a vital strength at this juncture in AFC’s growth and development.

Our subsidiary company Alfinco Insurance Brokers registered a year of consistent performance whilst our associate Company Macbertan formed a Joint Venture with PidiLite of India, known to be the largest manufacturer of adhesives in Asia.

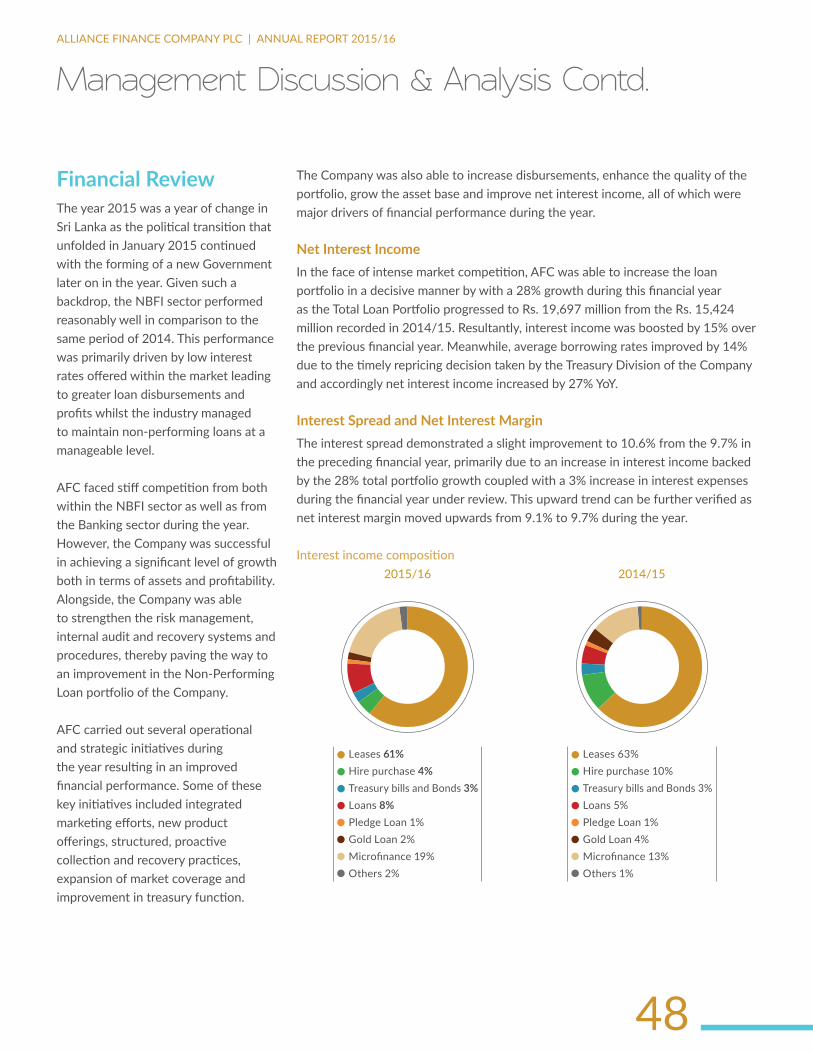

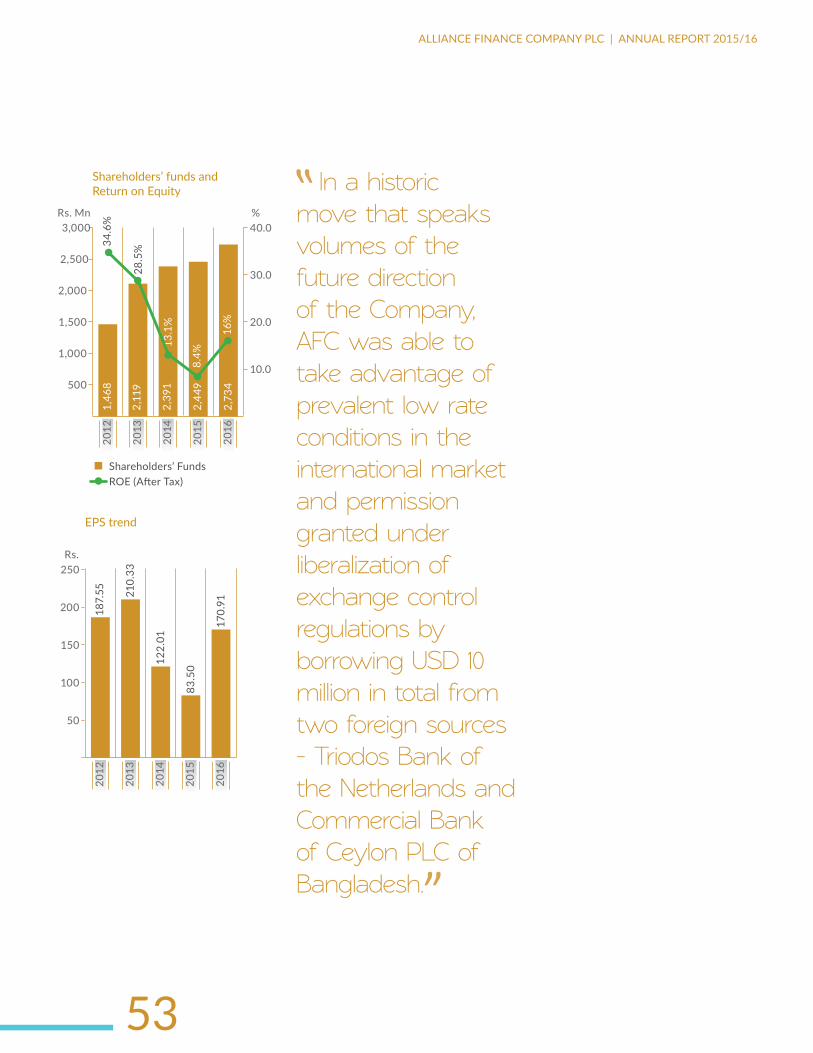

FinancialPerformanceThe Profit before Tax of AFC grew 91% YoY, from Rs.277 million to Rs.531 million, during the year under review whilst the Profit After Tax increased from Rs.203 million achieved in 2014/15 to Rs.415 million in the year under review. Total assets increased to Rs. 25,857 million from Rs. 19,910 million in the preceding year.

During the year, total disbursements aggregated to Rs.16,300 million a 56% increase compared to the previous year, due to improved credit demand in a lower interest regime. Both Gross and Net NPL ratios are below industry averages with the gross NPL ratio dropping to 2.46% (Industry –5.7%) and net NPL ratio dropping to 0.71% (Industry –1.6%).

Chairman’s Review Contd.

Future OutlookLooking ahead, your Company will continually strive to bring in results based on its triple bottom line approach. Stable government policies conducive to the development and stability of the industry will be expected from the government which in return will help us in our strategic direction resulting in profitability, growth and sustainability.

AcknowledgementsI would like to take this opportunity to convey my gratitude to the Board of Directors for their guidance and support extended throughout the year. The Deputy Chairman/ Managing Director Mr. Romani de Silva, with his visionary leadership, played a key role in helping the Company perform well during the year and I thank him for his unswerving efforts. I also wish to thank our loyal customers for continuing to trust in AFC and to our shareholders for being an integrated stakeholder group in the Company, even during the toughest of times. Last but not least, I would like to state my appreciation to the committed employees of the AFC family. Without their hard work, determination and pursuit of excellence, we would not have been able to achieve as much as we have and I look forward to working closely with them as we continue on this journey into the future.

Sunil KarunanayakeChairman

31st May, 2016Colombo

21

ALLIANCE FINANCE COMPANY PLC | ANNUAL REPORT 2015/16

mESSAgE FROm ThE SENiOR AdviSOR ANd pAST ChAiRmAN OF AlliANCE FiNANCE COmpANy plCIt is a poignant moment in time when a Company celebrates its Diamond Jubilee. Being an integral part of the Company since its humble beginnings in 1956 and witnessing its rise to the position it enjoys today as a trusted financial services provider, I am honored to share my thoughts on this occasion.

Foremost, is that the Company has achieved this milestone upholding intrinsic time tested values adopted by its founder Directors, Mr. Eardley de Silva, Mr. Fred Perera, Mr. Hayes Jayasundera, Mr. N.M. Appuhami and Mr. Heyward Fernando. Guided by an unwritten business philosophy and a Code of Ethics for which the Company is renowned the Company has steadfastly traveled on a long journey of six decades in an industry that has witnessed turbulent times. This journey bears testimony to the Company’s sustainability and the foresight of its leadership through three generations.

This would have not been possible without the unstinted support and loyalty of our employees who have come on board at varied times and faithfully served the Company. We are extremely grateful to four generations of loyal depositors and hirers who have trusted the Company and become a part of the Alliance Family which was built on the values of trust, friendship and innovation.

Whilst looking at the past and recalling the special moments witnessed along this journey, it is also a time to reflect on the future that lies ahead. I wish the Company and all its stakeholders continued success as it continues to move forward in this new era of challenges and opportunities in post war Sri Lanka.

Pratapkumar de SilvaFormer Chairman

guided by an unwritten business philosophy and a Code of Ethics for which the Company is renowned the Company has steadfastly traveled on a long journey of six decades in an industry that has witnessed turbulent times.

22

ALLIANCE FINANCE COMPANY PLC | ANNUAL REPORT 2015/16

dEpuTy ChAiRmAN/ mANAgiNg diRECTOR’S REviEw

Starting its journey from humble beginnings six decades ago, your Company has steadfastly contributed to the development of our country by faithfully serving four generations of loyal customers from all walks of life.

Dear Shareholders,I consider it a privilege to present to you the Annual Report of a unique Company that has concluded 60 years of successful business operations in Sri Lanka. Starting its journey from humble beginnings six decades ago, your Company has steadfastly contributed to the development of our country by faithfully serving four generations of loyal customers from all walks of life.

Built on a strong foundation of trust and powered by innovation, we have in recent times, formalized our core values which have been handed down through generations into a triple bottom line business philosophy that guides us towards inclusive and sustainable value creation across multiple stakeholder groups.

23

ALLIANCE FINANCE COMPANY PLC | ANNUAL REPORT 2015/16

On reaching our 60th year in business, i am pleased to announce that the profit before Tax of the Company increased from Rs.277 million to Rs.531 million during the year under review, which is a commendable growth of 91%

YearofSignificantChangeThe year 2015 brought forth monumental changes in Sri Lanka with the advent of a new Executive President in January 2015 followed by the installation of a new government in the same year. Despite such dramatic changes in the political landscape, the country progressed reasonably well to record a satisfactory GDP growth of 4.8%. Thus with the ill effects of the 30 year old national conflict well behind us, Sri Lanka is on its way to regaining its position of eminence as the ‘Pearl of the Indian Ocean’.

The Budget for 2016 has focused on promoting construction, facilitating competitive exports and developing tourism, health and education. Many initiatives have also been introduced to drive FDI’s into the country. As the new Government settles into its role of accelerating sustainable development whilst improving good governance, we are hopeful that the initiatives taken will be able to create the necessary infrastructure and bring in the much needed reforms along with consistent and stable policies. We are confident that the current strategies will serve as a catalyst to further increase much needed confidence levels amongst both local and foreign investors.

NBFI SectorDespite many policy changes affecting the industry during the year under review, the NBFI sector was able to perform creditably. Due to increases in duties on vehicles and the introduction of a 70% ceiling in the Loan to Value

(LTV) ratio, most companies in the NBFI sector have gradually commenced migrating towards products such as mortgage loans, business loans and other types of financial products and services. We believe that this is a step in the right direction as it would result in a greater contribution towards the development of the economy and a more diversified and balanced business portfolio for the sector. At Alliance, we are firmly of the view that the LTV ratio is necessary to prevent customers from becoming over-indebted and leading themselves and the country into a debt trap. We are also confident that such healthy measures will help prevent the formation of an asset bubble and will ensure the long-term sustainability of the industry and all its stakeholders in the longer term.

FinancialPerformanceHighlightsIt is against this backdrop that I take pleasure in reviewing the performance of your Company during the financial year 2015/16 and present to you our corporate goals and strategies which will guide us in facing the challenges in the times ahead.

FinancialPerformanceOn reaching our 60th year in business, I am pleased to announce that the Profit Before Tax of the Company increased from Rs.277 million to Rs.531 million during the year under review, which is a commendable growth of 91%, whilst the Profit After Tax more than doubled from Rs.203 million achieved in 2014/15 to Rs.415 million in the reported year. In 2015/16, total disbursements increased by 56%,

24

ALLIANCE FINANCE COMPANY PLC | ANNUAL REPORT 2015/16

deputy Chairman/ managing director’s Review Contd.

from Rs.10,471 million in 2014/15 to Rs.16,300 million, as a result of significant improvements made to our marketing operations.

The Microfinance SBU achieved a growth rate of 29%, from Rs.2,506 million in 2014/15 to Rs.3,244 million this year, which helped maintain this segment at 10% of the overall portfolio, thereby limiting our exposure and risk. With the 56% growth in total disbursements the Company’s total portfolio of advances recorded a growth of 28% as it moved up from Rs.15,424 million in 2014/15 to Rs.19,697 million in 2015/16.

Having successfully disposed most of its non-performing articles during the year, the Company also managed to further reduce the exposure of its aged gold loan portfolio to 2% from 5% recorded in 2014/15. Significant improvements were witnessed in both gross and net NPL ratios during the year mainly due to the disposal of most of the Company’s non-performing assets viz a viz the gold loan assets and the repossessed vehicle stocks. This resulted in a 62% reduction in the absolute NPL value reducing from Rs.1,280 million to Rs. 484 million during the financial year. Both NPL ratios are well below the industry ratio with our gross NPL ratio dropping to 2.46% (Industry – 5.7%) and net NPL ratio moving downwards to 0.71% (Industry – 1.6%).

The total assets increased from Rs.19,910 million in the preceding year to Rs. 25,857 million in the year under review recording a commendable growth of 30%.

The Company secured a BB + rating from Fitch Ratings Lanka Limited and the analysis provided in the Rating Report has been studied in detail by our Senior Management team. Many initiatives are being introduced to improve key drivers which in turn will enhance business performance and result in further improvements to our rating.

FundingAFC recognizes the importance of long term funding and the necessity to constantly address the inherent funding mismatch of the NBFI sector. Many years ago, as a result of this proactive thinking, an Assets and Liability committee was also set up in the Company and many initiatives were commenced to develop and diversify our sources of long term funding.

I am pleased to report that the Company was able to reach an important milestone during the year by obtaining two lines of foreign funding from Commercial Bank PLC- Bangladesh and from the Triodos Bank – Netherlands. The facility from Commercial Bank, Bangladesh was USD 6 million with a tenure of 1 year and the facility from the Triodos Bank was USD 5 million with a tenor of 3 years. The Triodos Bank has been voted as the world’s most sustainable Bank and granting of the facility was a result of

a strategic dialogue that was initiated several years ago. Both facilities were obtained under the relaxed exchange control programme offered through the External Borrowing Scheme introduced by the CBSL.

The Triodos Bank is an organization that invests globally in companies that achieve a best-in-class combination of social, environmental and economic performance. Therefore they follow a comprehensive research and selection process in order to clearly identify whether a company meets all their criteria prior to investing. The fact that Alliance Finance was able to meet such exacting standards speaks volumes of the international standards that we have achieved in terms of our approach to social, environmental and governance aspects.

Though market risk cannot be eliminated, the Treasury Division took calculated steps to manage such risks by changing the profile of the risks that were encountered. The division strives to manage the adverse effects of exchange rate risk arising out of foreign currency transactions in the most cost-efficient manner.

MicrofinanceIn keeping with our sustainability commitments and long term business strategy, we established the Microfinance SBU in 2013. The creation of this SBU has enabled the Company to extend its services to a wider segment of our society. As a socially responsible corporate entity, we consider Microfinance as a means

25

ALLIANCE FINANCE COMPANY PLC | ANNUAL REPORT 2015/16

of making a positive contribution to the lives of thousands of individuals with limited opportunities by affording them an opportunity to uplift their lives by providing access to credit and entrepreneurial skills.

We now have a Microfinance base of 66,455 customers. A majority of them are female entrepreneurs who are catered to by our fast-growing team of 316 Field Officers. The total Microfinance portfolio grew by 28% to register Rs.2.0 billion during the year under review. In keeping with the growth, through a comprehensive Entrepreneur Development Services (EDS) programme, we have also been able to impart financial and technical knowledge, thereby assisting these rural entrepreneurs to grow their businesses to greater heights.

Standing at approximately 10% of our total portfolio the Microfinance SBU has emerged as a significant SBU in the Company structure with a presence in 40 locations. The Company has however decided to focus on consolidating the existing branch network and expand with caution in this segment until a proper regulatory framework is introduced by the Authorities via the Central Bank or through a dedicated Microfinance regulatory body. The Government urgently needs to take steps to regulate NBFIs engaged in Microfinance thereby improving the quality and sustainability of the industry. The industry is suffering due to a multitude of reasons including poaching of employees, excessive competition to grant loans to the same

customer resulting in unsustainable multiple borrowings and the creation of over indebtedness which in turn would lead the customers, the sector and the country into a debt trap. As mentioned earlier we have capped our growth in this sector until we see improvements in the macro fundamentals of the industry. Recommendations and inputs for the setting up of an enabling regulatory framework has been given to the policy makers by the industry association – The FHA. We are hopeful that a practical regulatory framework and directions will be implemented soon in consultation with the industry.

Governance and Risk ManagementAn Enterprise Risk Management Framework was implemented in the previous financial year in order to facilitate robust governance and the effective management of risks. Spearheaded by the Chief Risk Officer, this framework continued to meet the Company’s needs and contributed to maintaining the quality of the portfolio during the year under review. A strong emphasis was also placed on the audit function given the fact that fraudulent activities are on the rise within the industry. We are confident that these proactive measures will help the Company significantly in its efforts to enhance the sustainability of its portfolio.

Standing at approximately 10% of our total portfolio the microfinance Sbu has emerged as a significant Sbu in the Company structure with a presence in 40 locations.

26

ALLIANCE FINANCE COMPANY PLC | ANNUAL REPORT 2015/16

A Greener CompanyAs one of the pioneering financial institutions to embrace the Triple Bottom Line philosophy in Sri Lanka, the Company strives to make a positive impact on the environment at every level. Some of the noteworthy initiatives carried out during the year are given below.

AFC embarked on a research to develop a kit to reduce threewheeler emissions by entering into a joint partnership agreement with Vialle of Netherlands, a leading LPG gas technology specialist in Europe. With the assistance of the Dutch government we will continue to progress in this project in the future.

AFC took part in a ’One Million Trees Project’ by the Rotary Club of Sri Lanka which commenced in the Kurunegala District. Through this project we hope to fulfil our pledge for the “Tree for a Lease” initiative of the Company. As of end February 2016, the Company had contributed to plant 14,000 trees for 13,550 leases given out during that period of the financial year. Validation of the process of this initiative is currently being carried out.

Earth Hour celebrations were carried out with the co-operation of the Colombo Municipal Council. This included an awareness walk and donation of 500 LED bulbs to illuminate the Viharamahadevi Park.

In March 2016, AFC took significant steps to increase its focus on energy conservation by making a pledge under the “AFC Green Pledge” to reduce the energy consumption of the Company by 5% by the end of the 2016/17 financial year.

TechnologicalDevelopmentsWe believe that Information Technology (IT) is a strategic asset in ensuring that each and every employee is enabled to perform at the highest level and deliver service excellence to the customer. As a result, the Company is constantly considering ways to improve the IT infrastructure within the organization. Some of the key initiatives carried out this year include upgrading the Company’s entire IT system with state-of-the-art hardware, commencement of online data replication to the Disaster Recovery (DR) site, establishment of an automated file approval process, utilization of SMS technology for customer communication and initiation of a Mobile Cash pilot project in 15 branches in collaboration with Mobitel.

HumanCapitalGrowthThe Company considers human capital to be one of its most important resources as it plays a key role in navigating AFC towards its vision. By creating a diverse, strong pool of talent, the Company strives to foster its human capital and considers it to be one of its key competitive advantages. Having surpassed the 1,000 employee mark in recent years, we now have 1,203 employees, a figure which was boosted by 340 new recruitments during the year mainly for the Microfinance SBU. The HR Department has placed great significance in ensuring that the Company attracts the right people with the right skills and attitude and providing them with an environment where they can perform, learn, grow and reach their full potential.

As one of the pioneering financial institutions to embrace the Triple bottom line philosophy in Sri lanka, the Company strives to make a positive impact on the environment at every level.

deputy Chairman/ managing director’s Review Contd.

27

ALLIANCE FINANCE COMPANY PLC | ANNUAL REPORT 2015/16

Way ForwardThe Company has mapped out a 3 year strategy outlining the Way Forward and lays emphasis on industry positioning, credit rating and brand value. Accordingly, the objectives and strategies are primarily based on achieving sustainable growth in a volatile environment.

The most vital development for the Company would be the formulation of stable, long-term policies for the industry. This would enable the Company to take calculated risks and make long-term plans. We see opportunities opening up for the SME sector and are in the process of acquiring the requisite skills to upgrade the Company’s expertise in this area even further. Overall, the approach will be one of steady growth as we consolidate our systems and processes on the back of strong growth and lay the necessary foundation to launch a more aggressive approach once definitive macro level policies are implemented hopefully in the not too distant future.

Against the backdrop of a highly competitive market, it is imperative that we constantly focus on ways of improving our existing product offerings whilst also creating new, innovative products to cater to the changing needs of today’s evolving customer. Therefore, we intend to come up with associated derivatives stemming from our core areas of transport and motor-related products.

PerformanceofSubsidiariesandAssociate CompaniesAlfinco Insurance Brokers (Pvt) Ltd

Alfinco Insurance Brokers recorded another year of steady performance. The Company, which acts as the agent and broker for the insurance business generated from the customers of Alliance Finance, played a more active role in order to bring in more business from our customers in addition to the motor business. Looking ahead, we believe that this approach would help to increase revenue from their portfolio. Considering the structural change within the Company during the last financial year the operations were consolidated and the internal processes strengthened positioning the Company to aggressively engage in marketing. The Company made a profit before tax of Rs. 23.3 million.

Macbertan (Pvt) Ltd

Our associate company Macbertan (Pvt) Ltd performed very well during the year. Macbertan formed a Joint Venture with Pidilite International PLC of India, known to be the largest manufacturer of adhesives in Asia. Macbertan has been the Distributor for Pidilite products in Sri Lanka over a long period and this JV was a natural progression of our partnership and underscored the trust placed on us by this giant in the adhesive industry. Under this newly-formed company, a new manufacturing plant will be setup in Sri Lanka. During the year under review, the product offering of Macbertan expanded providing customers with a wider choice of selection in the face of intense competition in the

core business of the Company. The extensive dealer network is being utilised to provide the hardware sector with complementary products. We have also setup a new production plant for a roofing product.

It is a considerable feat that the Company was able to increase its profitability from Rs. 30 million to Rs. 36 million in the face of intense competition. The success and the performance of the Company was made possible due to the excellent product mix and we are confident that given the current market potential and the diversified portfolio the profits of the Company should continue to rise sustainably.

AcknowledgementsOn this momentous occasion of the 60th anniversary of the Company, I would like to extent our deep appreciation to our Senior Advisor and former Chairman, Mr. Pratapkumar de Silva for completing six decades of association with our Company and the Finance Industry of Sri Lanka.

Over a period of six decades he has been instrumental in inculcating many of the time tested values in the Company which we continue to uphold. Inspired by the concept of “small is beautiful”, approximately 30 years ago, during his period of leadership as the Chairman and the Managing Director, he pioneered the concept of financial inclusion in the industry by providing credit to the marginalized segments of our society to purchase three-wheelers thus creating significant numbers of

28

ALLIANCE FINANCE COMPANY PLC | ANNUAL REPORT 2015/16

On our 60th anniversary it is my privilege to also place on record our sincere appreciation to the founding Chairman – late mr. Eardley de Silva and founding board members, late messrs, Fred perera, hayes Jayasundera, N.m. Appuhami and heyward Fernando. Their foresight, pioneering spirit and hard work paved the way for Alliance to reach the position of strength it enjoys in the industry today.

self-employment opportunities. This unique product has become a major source of revenue for the Company and continues to contribute significantly to our bottom line up to now. This successful strategy which was a result of his foresight also opened up many more lucrative financing opportunities which have since added much value to the Company and its smaller customers, whilst creating financial inclusion in Sri Lanka.

His association with the industry which also spans a period of 60 years saw him also serve on the Board of the Credit Information Bureau of Sri Lanka for a record period of 25 years as the nominee Director of the FHA and also as the Chairman of the FHA initially from 1970 to 1972 and again from 1988 to 1991. His continued advice and contributions are deeply appreciated and valued by me and the members of the Board. We wish him many more years of successful association with the Company as its Senior Advisor.

On our 60th anniversary it is my privilege to also place on record our sincere appreciation to the founding Chairman – late Mr. Eardley de Silva and founding Board members, late messrs, Fred Perera, Hayes Jayasundera, N.M. Appuhami and Mr. Heyward Fernando. Their foresight, pioneering spirit and hard work paved the way for Alliance to reach the position of strength it enjoys in the industry today. I would also like to place on record my appreciation to the successive Boards of Directors who played an important role in the progress of the Company.

As yet another financial year has drawn to a close, I would like to convey my sincere appreciation to the present Chairman Mr. Sunil Karunanayake and the Board of Directors of the Company for their continued support and astute guidance. I would also like to congratulate Mr. Karunanayake on being awarded the “Professional Excellence Award 2015” by the Institute of Certified Management Accountants of Sri Lanka (CMA) in recognition of his outstanding leadership capabilities.

I also wish to thank Mr. Emmanuel Muttupulle for his indelible contribution to the Company during his brief tenure on our Board. He joined the Board during the last financial year to serve in the capacity of Executive Director – Operations and retired on reaching the age of 70 years. However, the Company is fortunate to retain his services in the capacity of Chief Operating Officer (COO) where his vast knowledge and unparalleled experience in the field of finance will undoubtedly be an asset to me and my colleagues on the Board.

I would like to take this opportunity to also welcome Mr. Mahinda Gunasekera who joined the Board as Director Sustainability. Mr. Gunasekera holds a MBA, BSc in Agriculture and has undergone Microfinance Training from the University of Colorado, USA. He has spent the past three decades working in the fields of SME finance, livelihood development, Microfinance and agribusiness within Asia in countries such as Sri Lanka, Afghanistan, Bangladesh and Nepal. Further details on his extensive profile can be found in

deputy Chairman/ managing director’s Review Contd.

29

ALLIANCE FINANCE COMPANY PLC | ANNUAL REPORT 2015/16

the “Board of Directors” section of this Annual Report. His core strengths in SME Microfinance and Agriculture will be of great value to our Board as we prepare to take the Company forward in an era of SME and Agro based financial inclusion.

In recognition of his contribution to the marketing activities of the core business lines, Dr. Ajith Medis was invited to join the Board in August 2016. We recognize with gratitude his efforts in growing the portfolio with better credit quality whilst improving the processes for efficient delivery of our product offerings. Dr. Medis holds a doctorate in Strategy, MBA, BCom (Special), a Diploma in Marketing (CIM UK) and he is also a certified Management Accountant. He is also attached to the academia of the University of Kelaniya. Further details on his profile can be found in the “Board of Directors” section of this Annual Report. We are confident that he will drive marketing to achieve impressive bottom line results for the Company.

I would also like to convey my gratitude to the Governor, Directors and officials of the Central Bank of Sri Lanka for their valuable guidance and continual interactions. As in previous years, the CBSL annual audits carried out by teams of experienced professionals have contributed significantly to strengthen many aspects of the Company’s operations, improve efficiencies as well as compliance capabilities. A big “thank you” goes

out to them for their commitment in the greater interest of all stakeholder groups.

At this juncture, I wish to express my deep appreciation to the Alliance Family of employees for all their hard work and dedication throughout the year without which this commendable performance would not have been possible. My sincere thanks to our loyal depositors who have remained with us for four generations. I thank our ever-expanding base of customers for their continued patronage as well as all our shareholders for the trust placed in the Company.

It is clear that we are heading into another challenging year where the Company will be tested on many fronts. I am confident that our performance during this financial year will provide the perfect platform for us to aim for even greater heights during the years ahead as we strive to become one of Sri Lanka’s most respected and sustainable NBFIs.

Romani de SilvaDeputy Chairman/ Managing Director

31st May, 2016Colombo

30

ALLIANCE FINANCE COMPANY PLC | ANNUAL REPORT 2015/16

it’s not just our stakeholders, we believe in the perfect balance between people, the planet and the profit that we generate and we continue to follow through on sustainable methods which will take us to the future and beyond

31

ALLIANCE FINANCE COMPANY PLC | ANNUAL REPORT 2015/16

32

ALLIANCE FINANCE COMPANY PLC | ANNUAL REPORT 2015/16

mANAgEmENT diSCuSSiON & ANAlySiS

AFCSustainabilityApproachAs a Triple Bottom Line company, AFC operates with continuous and significant emphasis on economic, social and environmental sustainability on which the sustainability of the Company depends on. The core values of AFC is about managing and contributing towards the sustainability of these components mainly via creating and distributing economic value, serving our people and conserving nature. The entire business structure and the strategy is developed in line with the Triple Bottom Line philosophy, so that the core values are preserved and the role of the Company on ensuring economic, environmental and social sustainability continues.

ThestrategictriplebottomlineapproachofAFC

Profitability

Sustainability

Growth

People

Social sustainability related practices to ensure deriving a

material outcome.

Planet

Profit

Sustainability initiatives integrated with all business

operations.

AFC Strategy

33

ALLIANCE FINANCE COMPANY PLC | ANNUAL REPORT 2015/16

StakeholderEngagementApproachOurMajorStakeholders

Customers

Shareholders

Management

Employees

Regulators/ Government/

Rating agenciesAgents/ Dealers/ Value

chain connectors

Business Partners and

Suppliers

Subsidiaries/Associations

Depositors and Investors

General Public/

Communities/Well-wishers/

Media/Professional

bodies

Alliance Finance Company PLC

StakeholderMapping:Interest-PowerMatrix

Government/Regulatory Bodies/RatingAgencies

ShareholdersManagement

Depositors and investorsEmployees

Customers(Credit)

Dealers/Agents/ Valuechainconnectors

Interest

Influence/Power

GeneralPublic/Communities/Well

Wishers/Media/ProfessionalBodies

Subsidiaries/AssociationsBusiness Partners and Suppliers

Low

High

High

Low

34

ALLIANCE FINANCE COMPANY PLC | ANNUAL REPORT 2015/16

StakeholderEngagementProcess

y Meetings y Direct dialogue y Questionnaire

surveys y CRM system y Annual Report y Quarterly

financial statements y Field audits y Newsletters y Company

website y CSE website y Press releases y Social media y Company hotline y E-mail and other

correspondence

y Meetings y Direct dialogue y Questionnaire

surveys y CRM system y Field audits y Social media y Company hotline y E-mail and other

correspondence

InformtheBoardandtheManagementonthepriorities

Takeactionstorectify/address/adopttheissues/concerns/suggestions

Analysisofthefeedbackreceived

Identifysuggestions,issues/concerns

Prioritizeissues/concerns,needs,responses

StakeholderCommunication StakeholderFeedback

management discussion & Analysis Contd.

1. strategic gap analysis

Performed via direct interviews with the key Senior Managers. The content was refined with the feedback from the CXOs and the Directors.

2. Stakeholder feedback

A questionnaire survey was performed for major stakeholders namely, the employees, customers (loan, deposit and Microfinance) and suppliers.

Additional information was obtained from the recent customer satisfaction surveys, feedback received during meetings and direct dialogue with customers and employees.

Based on the results of the Strategic Gap Analysis, the aspects which require immediate responses have been identified and the necessary course of action has been planned and implemented where possible to address the prioritized issues. In addition to that, minor issues and issues that can be addressed over a period of time have also been identified. The action to be taken for such issues have been discussed and reviewed. The strategic gap analysis will be performed every quarter to identify the major opportunities and risks pertaining to the Company.

Stakeholder assessment is an ongoing process in the Company, where the findings are being incorporated into the regular decision making and to plan the long-term approaches that will be aligned to the Company’s Strategic Plan. In addition to the regular assessments, regular stakeholder feedback surveys also will be conducted to re-affirm the policy changes and course of action taken to address the issues in a systematic manner. The engagement actions also will be carried out with continuous refinement to obtain precise feedback, maintaining highest level of transparency and quality of information to ensure the process of engagement to be fortified further.

35

ALLIANCE FINANCE COMPANY PLC | ANNUAL REPORT 2015/16

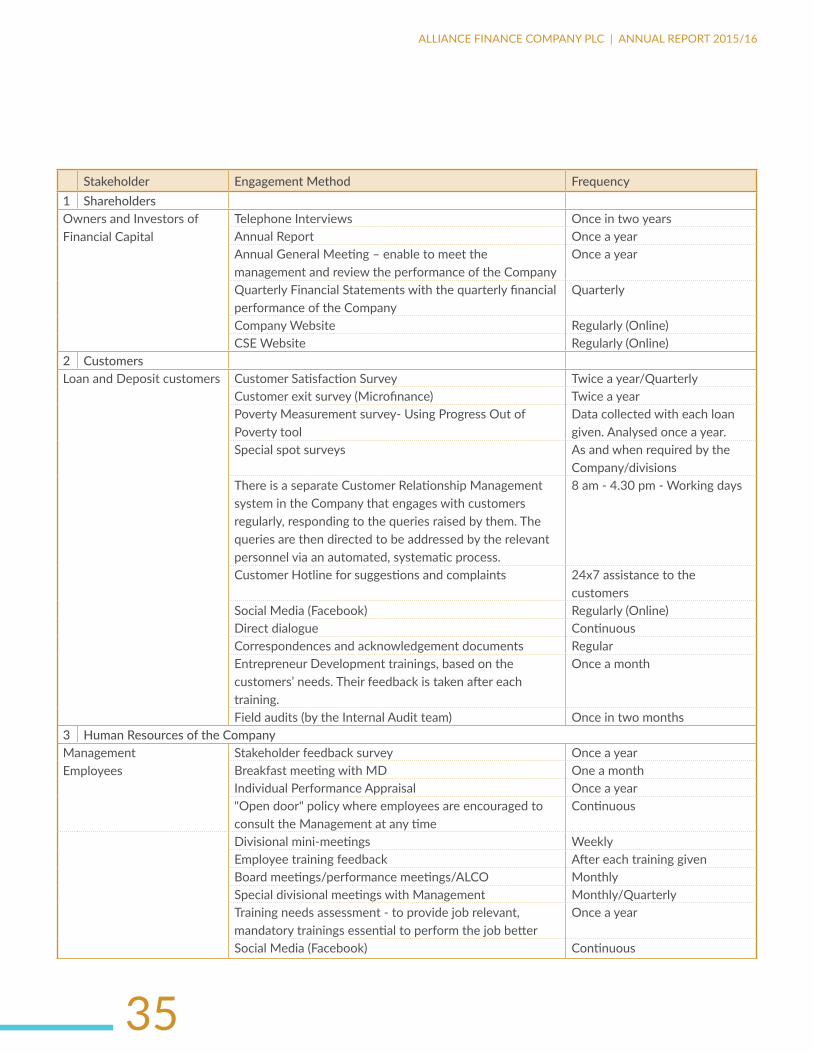

Stakeholder engagement Method Frequency1 shareholdersOwners and Investors of Financial Capital

Telephone Interviews Once in two yearsAnnual Report Once a yearAnnual General Meeting – enable to meet the management and review the performance of the Company

Once a year

Quarterly Financial Statements with the quarterly financial performance of the Company

Quarterly

Company Website Regularly (Online)CSE Website Regularly (Online)

2 CustomersLoan and Deposit customers Customer Satisfaction Survey Twice a year/Quarterly

Customer exit survey (Microfinance) Twice a yearPoverty Measurement survey- Using Progress Out of Poverty tool

Data collected with each loan given. Analysed once a year.

Special spot surveys As and when required by the Company/divisions

There is a separate Customer Relationship Management system in the Company that engages with customers regularly, responding to the queries raised by them. The queries are then directed to be addressed by the relevant personnel via an automated, systematic process.

8 am - 4.30 pm - Working days

Customer Hotline for suggestions and complaints 24x7 assistance to the customers

Social Media (Facebook) Regularly (Online)Direct dialogue ContinuousCorrespondences and acknowledgement documents Regular Entrepreneur Development trainings, based on the customers’ needs. Their feedback is taken after each training.

Once a month

Field audits (by the Internal Audit team) Once in two months3 Human resources of the Company Management Employees

Stakeholder feedback survey Once a yearBreakfast meeting with MD One a monthIndividual Performance Appraisal Once a year"Open door" policy where employees are encouraged to consult the Management at any time

Continuous

Divisional mini-meetings WeeklyEmployee training feedback After each training givenBoard meetings/performance meetings/ALCO MonthlySpecial divisional meetings with Management Monthly/Quarterly Training needs assessment - to provide job relevant, mandatory trainings essential to perform the job better

Once a year

Social Media (Facebook) Continuous

36

ALLIANCE FINANCE COMPANY PLC | ANNUAL REPORT 2015/16

Stakeholder engagement Method Frequency

4 agents/dealers/value chain connectors

Stakeholder feedback survey Once a year

The Customer Relationship Management system of the Company has a separate portal for the agents/dealers as well. The process of the dealer management is done via an automated system. Apart from above the CRM unit is available for additional assistance when needed.

Continuous

Dealer/agent point visits by branch staff Monthly

Dealer/agent point spot visits by Head Office staff Twice a year

5 Business Partners and Suppliers

Direct dialogue Regularly

Service quality surveys Once a year

Stakeholder feedback survey Once a year

Negotiation and problem solving dialogue As and when required

6 Regulatory bodies/government (Central Bank)

Regulators/Government Annual Review Once a year, full one month extensive engagement

Annual Review follow up meetings Once a year

Special meetings for regulatory clarifications and business needs

On a need basis

Periodic compliance reports Monthly/Quarterly

CSE website Regularly (Online)

Rating agencies Meetings On a need basis

7 General Public/Communities/ Media/Professional bodies/Well-wishers

Written/direct dialogue Continuous

Company hotline 24x7 assistance

Company website Continuous

Social Media (Facebook) Continuous

CSR initiatives Continuous

Press releases On a need basis

Subsidiaries or Associates Meetings Periodically

Collective activities conducted Annually

Company Website Continuous

Newsletters Once a year

management discussion & Analysis Contd.

37

ALLIANCE FINANCE COMPANY PLC | ANNUAL REPORT 2015/16

OurResponsestotheIdentifiedStakeholderExpectations DuringtheYear2015/16Stakeholder group Stakeholder expectations our response

Shareholders

Further improve the Company performance balancing with the Triple bottom line concept

The new three year strategic plan of the Company was prepared during the reporting year with goals, strategies and targets encompassing the triple bottom line concept of the Company

Continuous monitoring and improvement of the triple bottom line initiatives are ongoing The Company was able to achieve notable improvements in all aspects during the reporting year that are reported in detail in financial review (Pages 48-53), Social and Environmental Review (Pages 65-84) section in this report.

Increase the brand awareness and brand value of the Company

A number of initiatives had been undertaken on this and the details are reported under Customer and Product responsibility section in pages 72-73 in this report.

Cust

omer

s

Expand the accessibility via increased points of presence

Points of presence of both Core business and Microfinance has been increased. The details are in Branch Network section in pages 96-100 in this report.

Improve customer communication and feedback

There is a system in place for this in the Company. The customer feedback and complaint handling process is ongoing successfully. More details on this are in pages 69-70 of this report.

Offer transaction/process flexibility with improved facilities

Sri Lanka Inter-Bank payment system has been introduced to the customers during the reporting year.

M-cash facility was introduced for instalment payments for the Microfinance customers. More details on this are in page 92 of this report.

Introduce new products Company introduced six new products during the reporting year. More details on this are in Customer and product responsibility section in the pages 69-73 in this report.

Empl

oyee

s

Provide essential and relevant trainings

43 training programs were conducted for the staff based on their training needs identified via personal questionnaire survey. More details on this are in Human Capital section in the pages 78-79 in his report.

Provide new opportunities to develop the skills and job knowledge

The staff members were engaged in more trainings on soft skills development, afforded internal transfer opportunities, assigned special projects on marketing, energy and paper saving initiatives during the year. These will be continued in the future.

Adopt bottom to top approach in relevant planning processes

This was adopted in the preparation of the Company Strategic Plan and Operational Planning for the business units. This practice will continue in the future as well.

38

ALLIANCE FINANCE COMPANY PLC | ANNUAL REPORT 2015/16

Stakeholder group Stakeholder expectations our response

Agen

ts/d

eale

rs/

Valuechain

conn

ecto

rs

Improved efficiency and speed of processes and approvals of the related processes

CRM system facilitates these needs and it was further systematized in the reporting period. Other process improvements will be undertaken and the actions are ongoing to address them.

Attractive and speedy payment process

The actions are ongoing to address this and the process improvements will be addressed.

Busin

ess p

artn

ers a

nd

supp

liers

Complementary relationship management

This has been a regular practice and will be continued with further improvements in accountability, negotiation and loyalty.

Improved process efficiency This is an ongoing process and will be continued.

Increased emphasis on environmental and social sustainability/welfare

Many initiatives have been undertaken to generate both short term and long term safeguards to the environment as well as to the society. Further details are in the Social and Environmental Review in pages 65-84 The strategic actions for these areas are detailed in the new strategic plan of the Company for implementation in the near future.

GeneralPublic/Communities/

Media/ProfessionalBodies/Well

wishers

Improved brand awareness This has been addressed in various ways. The actions taken and future aspirations are reported under Customer and Product responsibility section in pages 69-73 in this report.

New products designed for different potential customer segments

The details on this are in Customer and product responsibility section in the pages 69-73 in this report.

Increase awareness on products and services

Promotional campaigns, Newspapers advertisements, Website and Social Media are used extensively to educate and increase awareness of the general public.

Supporting community welfare activities/Sponsorships

Many CSR activities have been conducted during the reporting year. More details on this are in Our Social Footprint section (pages 65-68) in this report.

management discussion & Analysis Contd.

39

ALLIANCE FINANCE COMPANY PLC | ANNUAL REPORT 2015/16

Materiality assessment / Materiality MatrixMateriality Assessment is about identifying the most important aspects relevant to AFC and its stakeholders. This assessment is carried out based on the most material aspects for the business and the stakeholders in terms of the economic, social and environmental aspects, as well as the magnitude of impact each aspects has on the business.

During this assessment process, the Company identified certain relevant topics and their impact on the entire organisation’s products, services, activities and relationships, irrespective of whether they occur internally or externally. The assessment was carried out by analysing the internal and external spheres of the business

in the current industry context as well as the aspect boundaries of the Company in order to identify the most crucial issues. Senior management was actively involved in analysing the level of materiality of the identified issues to stakeholders and the business. Additionally, the stakeholder assessments conducted during the year provided further insights into understanding and establishing the impact on the stakeholders in a more comprehensive manner.

The assessment helped AFC identify, understand and prioritize the most important economic, social and environmental aspects of the business and the stakeholders in order to improve the focus of the business. It also helped to reveal the different strategies the Company should undertake and to outline possible

changes to current strategies, so that they will be adapted to improve the Company’s responses and strategies for sustainability.

The identified aspects and boundaries were prioritised based on the level of significance of their economic, environmental and social impacts on the Company. The subsequent ranking is strictly determined based on its significance both to the stakeholders and to AFC’s economic, environmental and social sustainability.

This is the first time that AFC has undertaken a materiality assessment, and the Company wishes to continue the assessment in order to monitor the changes and emerging priorities that will enable the Company to better plan and manage the sustainable strategies.

1. Economic performance2. Market Presence3. Indirect economic impacts4. Energy5. Emissions6. Products and services7. Compliance8. Employment9. Labour/Management relations

10. Occupational health and safety11. Training and education12. Diversity and equal opportunity13. Labour practices grievance mechanisms14. Non- discrimination15. Freedom of association and collective

bargaining16. Forced or compulsory labour17. Human rights grievance mechanisms

18. Local communities19. Anti-corruption20. Anti-competitive behaviour21. Grievance mechanisms for impacts on

society22. Product and service labelling23. Marketing Communication24. Customer privacy25. Compliance

8

43 7

19 10 14

51 9 11

18 21 22 23 24

12

62 13

2015 25

16 17

EconomicEnvironmentSocial

High

High

Medium

Medium

Low

Low

Influenceonstakeholderassessmentanddecisions

TheMaterialityMatrix

SignificanceofimpactonAFC

40

ALLIANCE FINANCE COMPANY PLC | ANNUAL REPORT 2015/16

management discussion & Analysis Contd.

TheMaterialityAssessmentTable

StakeholdersMateriality (High/Medium/Low)

aspe

ct b

ound

ary

repo

rted

Cate

gory

aspe

cts

aFC

shar

ehol

ders

empl

oyee

s

Cust

omer

s

regu

lator

s

supp

liers

Busin

ess p

artn

ers

socie

ty an

d en

viro

nmen

t

Sign

ifica

nce

of

impa

ct o

n aF

C

Influ

ence

on

stak

ehol

der

asse

ssm

ent a

nd

decis

ions

Economic

1 Economic performance • • • • • • • H H Internal/External Yes

2 Market Presence • • • M L Internal Yes

3 Indirect economic impact • • • • • M M External Yes

Environmental

4 Energy • • M M Internal/External Yes

5 Emissions • • • • • H H External Yes

6 Products and services • • M L External Yes

7 Compliance • • • • M M Internal/External Yes

Social- Labour practices and decent work

8 Employment • • • • • H M Internal Yes

9 Labour/Management relations • • • • H H Internal Yes

10 Occupational health and safety • • • M M Internal Yes

11 Training and education • • • H H Internal/External Yes