Embed Size (px)

Citation preview

©2017 RSM US LLP. All Rights Reserved. ©2017 RSM US LLP. All Rights Reserved.

©2017 RSM US LLP. All Rights Reserved. ©2017 RSM US LLP. All Rights Reserved.

ACCOUNTING UPDATE

Presented by Paul J. Nockels

©2017 RSM US LLP. All Rights Reserved.

Broker-Dealer Accounting

ExchangesPrivate Company Council

Broker-Dealers

3

©2017 RSM US LLP. All Rights Reserved.

Definition of a Public Business Entity

A public business entity is a business entity meeting the following criteria:

• It is required by the U.S. Securities and Exchange Commission (SEC) to file or furnish financial statements, or does file or furnish financial statements (including voluntary filers), with the SEC (including other entities whose financial statements or financial information are required to be or are included in a filing).

• Broker-dealers are public business entities as they meet the above definition

• Other entities meet the definition under separate criteria

4

©2017 RSM US LLP. All Rights Reserved.

Is a Futures Commission Merchant a PBE?

Entities registered with the Commodity Futures

Trading Commission (CFTC) do not file with the

SEC, unless they are dually registered

• Not public business entities under “criteria a”

• Could be a PBE under other criteria

• If not a PBE, delayed required adoption of new

accounting standards

5

©2017 RSM US LLP. All Rights Reserved.

Agenda

• Accounting Topics

• Accounting Standards Updates

• Other Topics

6

©2017 RSM US LLP. All Rights Reserved. ©2017 RSM US LLP. All Rights Reserved.

ACCOUNTING TOPICS

©2017 RSM US LLP. All Rights Reserved.

Accounting Topics

• Revenue Recognition

• Leases

• Digital Currencies

• Restricted Cash

• Income Taxes (TCJA)

• Current Expected Credit Loss (CECL)

8

©2017 RSM US LLP. All Rights Reserved. ©2017 RSM US LLP. All Rights Reserved.

REVENUE RECOGNITION

©2017 RSM US LLP. All Rights Reserved.

Revenue Recognition Standard

• May 2014 – FASB and ISB issued substantially converged final standards

• Eliminates industry specific revenue recognition

• Comparability between industries

• Entity should recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services.

10

©2017 RSM US LLP. All Rights Reserved.

Revenue Recognition Standard

• Entity should apply the following steps:1. Identify the contract(s) with a customer

2. Identify the performance obligations in the contract

3. Determine the transaction price

4. Allocate the transaction price to the performance

obligation in the contract

5. Recognize revenue when (or as) the entity satisfies a

performance obligation

11

©2017 RSM US LLP. All Rights Reserved.

Effective Date of ASU 2014-09, Revenue from Contracts with Customers (Topic 606)

Effective Date

As issued As updated

Public entities Annual reporting periods

beginning after December

15, 2016, and the interim

periods within that year

Annual reporting periods

beginning after December

15, 2017, and the interim

periods within that year

Example: Calendar year end Quarter and year beginning

January 1, 2017

Quarter and year beginning

January 1, 2018

Nonpublic entities Annual reporting periods

beginning after December

15, 2017, and the interim

periods within annual periods

beginning after December

15, 2018

Annual reporting periods

beginning after December

15, 2018, and the interim

periods within annual periods

beginning after December

15, 2019

Example: Calendar year end Year ending December 31,

2018 and interim periods in

2019

Year ending December 31,

2019 and interim periods in

2020

12

©2017 RSM US LLP. All Rights Reserved.

Early Adoption of ASU 2014-09, Revenue from Contracts with Customers (Topic 606)

Early Adoption

As issued As updated

Public entities Prohibited Permitted in annual reporting

periods beginning after

December 15, 2016, and the

interim periods within that year

(which was the original effective

date for public entities)

Nonpublic entities Permitted in any of the following

periods: (a) an annual reporting

period beginning after December 15,

2016 or 2017, and the interim periods

within that year or (b) an annual

reporting period beginning after

December 15, 2016, and the interim

periods within annual periods

beginning after December 15, 2017

Permitted in any of the following

periods: (a) an annual reporting

period beginning after December

15, 2016, and the interim periods

within that year or (b) an annual

reporting period beginning after

December 15, 2016 and the

interim periods beginning one

year after that annual reporting

period

13

©2017 RSM US LLP. All Rights Reserved.

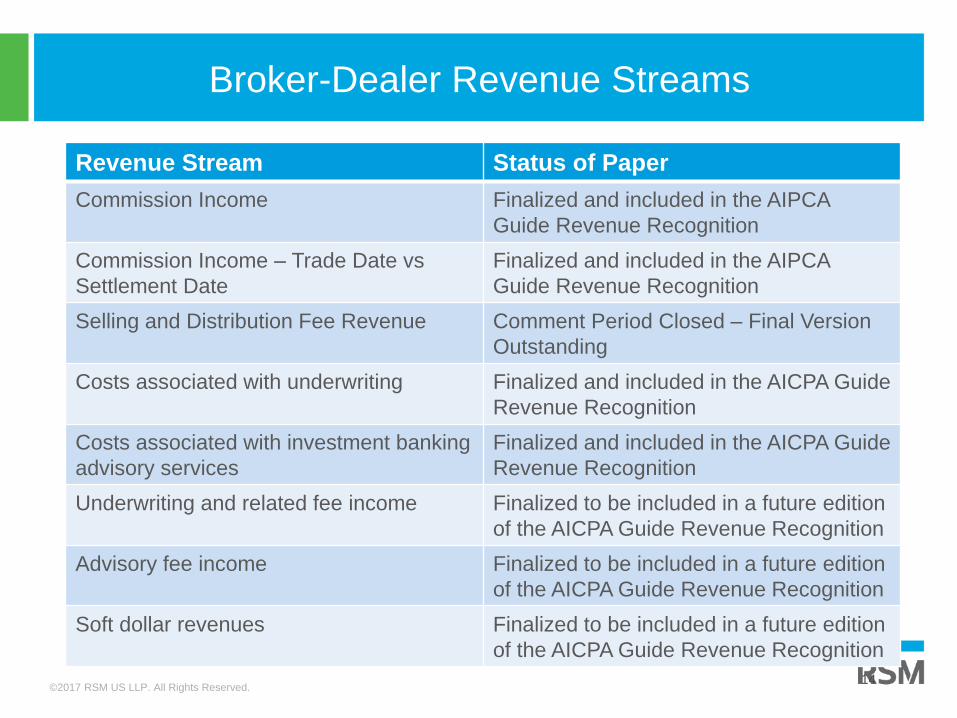

Broker-Dealer Revenue Streams

Revenue Stream Status of Paper

Commission Income Finalized and included in the AIPCA

Guide Revenue Recognition

Commission Income – Trade Date vs

Settlement Date

Finalized and included in the AIPCA

Guide Revenue Recognition

Selling and Distribution Fee Revenue Comment Period Closed – Final Version

Outstanding

Costs associated with underwriting Finalized and included in the AICPA Guide

Revenue Recognition

Costs associated with investment banking

advisory services

Finalized and included in the AICPA Guide

Revenue Recognition

Underwriting and related fee income Finalized to be included in a future edition

of the AICPA Guide Revenue Recognition

Advisory fee income Finalized to be included in a future edition

of the AICPA Guide Revenue Recognition

Soft dollar revenues Finalized to be included in a future edition

of the AICPA Guide Revenue Recognition

14

©2017 RSM US LLP. All Rights Reserved.

Transition Alternatives Upon Adoption

• Retrospective application to all periods presented

with the option to elect one or more practical

expedients

• Modified retrospective

− No restatement of prior periods

− Apply ASU 2014-09 to in-progress contracts as of the

adoption date going forward and subsequent contracts

− Recognize a cumulative effect adjustment at adoption

date for effects of applying ASU 2014-09 to in-progress

contracts

− Disclose in the year of adoption the effect on each line

item in the financial statements as a result of adoption

15

©2017 RSM US LLP. All Rights Reserved.

Required Disclosures

• Objective is to help financial statement users understand the nature, amount, timing and uncertainty of the related revenue and cash flows

• Annual and interim disclosures required of public entities − Less on an interim basis, but mostly quantitative in nature

• More disclosures required of public business entities and certain nonprofit entities and employee benefit plans − However, disclosures for all others are still significant

16

©2017 RSM US LLP. All Rights Reserved.

Required Disclosures

• Detailed quantitative and qualitative information

about the following must be disclosed:

− Disaggregated revenue

− Contract assets, contract liabilities and receivable

− Performance obligations in general and the transaction

price allocated to the remaining performance obligations

at the end of the reporting period

− Significant judgments related to when performance

obligations are satisfied and used to estimate and

allocate the transaction price − Capitalized customer

contract costs

− Capitalized customer contract costs

17

©2017 RSM US LLP. All Rights Reserved.

ASC Topic 606 disclosure requirements

• Entities that adopted ASC Topic 606 on a modified retrospective

basis must disclose what accounting treatment would have

been under legacy revenue guidance

©2017 RSM US LLP. All Rights Reserved.

General tax revenue recognition rules (accrual method)

• Under an accrual method of accounting,

income is includable when all the events to

fix the right to receive the income and the

amount can be determined with

reasonable accuracy

− Revenue is fixed for tax when (1) the payment

is earned through performance, (2) payment is

due to the taxpayer, (3) payment is received by

the taxpayer, or (4) the item of gross income, or

any portion thereof, is taken into account as

revenue in the AFS, whichever happens earliest

©2017 RSM US LLP. All Rights Reserved.

Tax considerations of ASC 606

• Direct impacts

− Federal current tax

− State current tax

• Indirect impacts

− Sales tax

− Excise taxes

− Transfer pricing

©2017 RSM US LLP. All Rights Reserved.

ASC 606 – assessment of tax impact

Define scope

Financial reporting assessment

Determine tax process

Review data and calculate

adjustments

Prepare deliverables

Implement

• Reflects company’s industry,

complexity and internal resources

• Work collaboratively with financial reporting team

to identify potential tax issues and opportunities

• Addresses level of analysis, specific

action steps, and implementation needs

• Involves determining proper tax

methods and calculating adjustments

• Provides summary of analysis and

implementation recommendations

• Includes assistance with

forms and ASC 740 tax-

related items

©2017 RSM US LLP. All Rights Reserved.

What about SIPC Revenue?

• Definition of SIPC Revenue unchanged by ASC

606

• It is not clear how to address the cumulative

effect adjustment at adoption date in the SIPC-6

− Broker-dealers that are impacted could contact SIPC

to clarify

©2017 RSM US LLP. All Rights Reserved. ©2017 RSM US LLP. All Rights Reserved.

LEASES

©2017 RSM US LLP. All Rights Reserved.

Leases

• Upon its effective date, FASB Update 2016-02,

Leases, will require a lessee to recognize on its

balance sheet assets and liabilities for all leases

other than those that meet the definition of short-

term leases.

©2017 RSM US LLP. All Rights Reserved.

Treatment of Operating Leases under SEC Rule 15c3-1

• In a letter to SIFMA dated November 8, 2016, the

staff of the Division of Trading and Markets stated

it would not recommend enforcement action to the

SEC under Exchange Act Rule 15c3-1 if a broker-

dealer computing net capital adds back an

operating lease asset to the extent of the

associated operating lease liability.

©2017 RSM US LLP. All Rights Reserved.

Treatment of Operating Leases under SEC Rule 15c3-1

• Further, the Division will not recommend

enforcement action to the SEC if a broker-dealer

determining its minimum net capital requirement

using the AI standard does not include in its

aggregate indebtedness an operating lease

liability to the extent of the associated operating

lease asset.

©2017 RSM US LLP. All Rights Reserved.

Treatment of Operating Leases pursuant to Rule 1.17 under the Commodity Exchange Act

• SIFMA issued a no-action letter request to the

CFTC dated February 8, 2018

− Includes appendix of examples

©2017 RSM US LLP. All Rights Reserved.

Leases

• Overview

• Scope

• Disclosures

• Effective date and transition

©2017 RSM US LLP. All Rights Reserved.

Leases overview

©2017 RSM US LLP. All Rights Reserved.

Related Party Leases

• No distinction between leases with related parties vs. third parties

• Application of Step 1 – determine if contract contains a lease− Included in expense sharing agreements?

− Determination of contract terms, including length, renewal options, etc.?

− Form over substance… if there is no contract that is enforceable, is there no lease?

− NOW is a good time to revisit to clarify arrangements

©2017 RSM US LLP. All Rights Reserved.

Leases overview

• Changes for lessees− Will record lease liability and right-of-use (ROU) asset for

most leases

− Income statement expense presentation will depend on classification of lease

• Changes for lessors− Limited changes to lessor accounting model

− Classification criteria modified

− Leveraged lease accounting prospectively eliminated

• Changes for both− Sale-leaseback criteria

− New presentation and disclosure requirements

©2017 RSM US LLP. All Rights Reserved.

Scope

• Standard is applicable to all leases except:

− Leases of intangible assets

− Leases to explore for or use minerals, oil, natural gas,

and similar nonregenerative resources

− Leases of biological assets

− Leases of inventory

− Leases of assets under construction

• Short-term leases election

©2017 RSM US LLP. All Rights Reserved.

Lessee disclosures

Extensive qualitative and quantitative disclosures

Type Example disclosures

Qualitative • Nature of leases

• Leases that have not yet commenced

• Variable payment arrangements

• Termination/purchase/renewal options

Quantitative • Amortization and interest for finance leases

• Operating lease cost

• Variable lease cost

• Short-term lease cost

• Maturity analysis of lease liabilities

Significant

judgments

and

assumptions

• Determining if a lease exists

• Standalone prices

©2017 RSM US LLP. All Rights Reserved.

Lessor disclosures

Extensive qualitative and quantitative disclosures

Type Example disclosures

Qualitative • Nature of leases

• Variable payment arrangements

• Termination/purchase/renewal options

• Information about management of residual asset risk

Quantitative • Lease income (in tabular format)

• Maturity analysis of undiscounted cash flows

(segregated by finance/operating lease)

©2017 RSM US LLP. All Rights Reserved.

Effective date

Public business entities

• Annual and interim periods

in fiscal years beginning

after 12/15/2018

• Early adoption permitted

• Modified retrospective

transition

− Certain reliefs

Nonpublic business entities

• Fiscal years beginning after 12/15/2019

• Interim periods in fiscal years beginning after 12/15/2020

• Early adoption permitted

• Modified retrospective transition

− Certain reliefs

©2017 RSM US LLP. All Rights Reserved.

Transition

• Modified retrospective transition

− Full retrospective adoption is prohibited

− All comparative periods presented are restated

− “Packaged” transition reliefs

• Expired/existing contracts contain leases

• Lease classification for expired/existing leases

• Whether previously capitalized initial direct costs could still be

capitalized

− Other transition relief

• Hindsight can be used in determining lease term and

assessing impairment of ROU assets

©2017 RSM US LLP. All Rights Reserved.

Leases: Targeted improvements to ASC 842

Transition—Comparative Reporting at Adoption

• Entities will be given an additional option for transition, under which

they will be allowed to elect to recognize a cumulative-effect

adjustment to the opening balance of retained in the period of adoption,

rather than in the earliest period presented.

• Reporting for comparative periods would remain under ASC 840

Separating Components of a Contract

• Lessors would be allowed to apply a practical expedient to not separate

nonlease components from the related lease components

• Lessors applying this expedient would account for the combined

components as a single lease component, if both:

1. The timing and pattern of revenue recognition for the nonlease

component(s) and related lease component are the same

2. The combined single lease component would be classified as an

operating lease Pro

posed

Proposed ASU

©2017 RSM US LLP. All Rights Reserved.

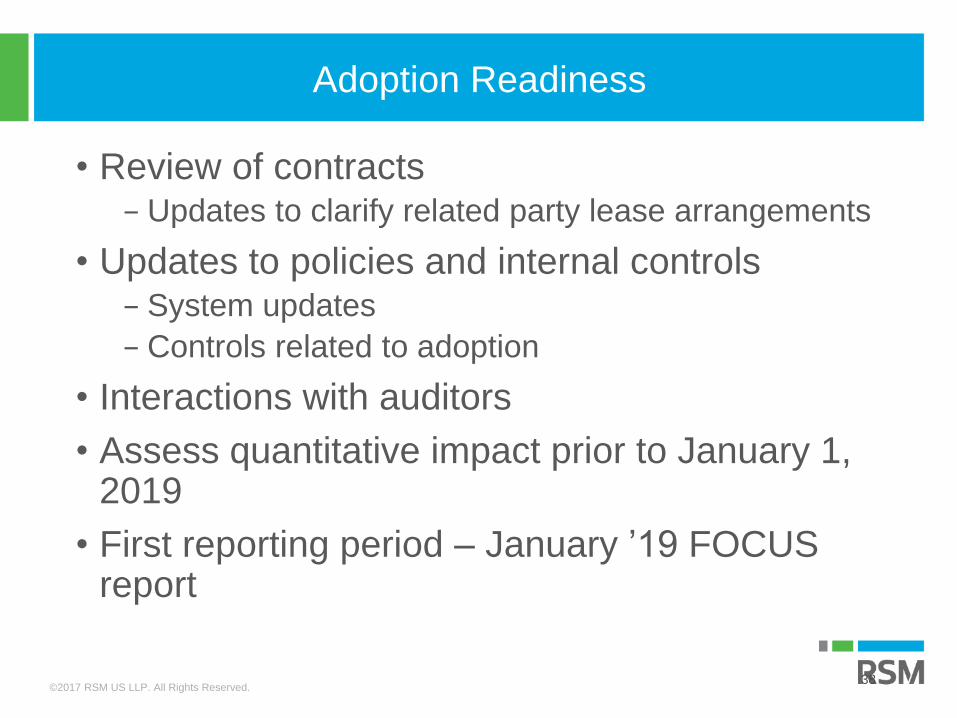

Adoption Readiness

• Review of contracts − Updates to clarify related party lease arrangements

• Updates to policies and internal controls − System updates

− Controls related to adoption

• Interactions with auditors

• Assess quantitative impact prior to January 1, 2019

• First reporting period – January ’19 FOCUS report

38

©2017 RSM US LLP. All Rights Reserved.

New Lease Accounting Resource Center

• Information about adoption and

implementation of ASU 2016-02,

Leases (Topic 842), including:− Leases: Bring on the balance sheet

− Leases: New accounting requirements for

lessees

− Leases: Overview of the new guidance

− SAB 74 disclosures for new standard on

lease accounting

• A contact form for those who need

help implementing the new standard

• Additional resources on lease

accounting

visit - rsmus.com/asc842

©2017 RSM US LLP. All Rights Reserved. ©2017 RSM US LLP. All Rights Reserved.

DIGITAL CURRENCIES

©2017 RSM US LLP. All Rights Reserved.

Accounting and Financial Reporting of Digital Currencies

• Currently no authoritative literature under US GAAP that specifically addresses resulting in diversity in practice

• What is it?− Cash? Financial Instrument? Intangible?

Inventory?

− Security? Commodity? Something New?

• Why is it?− ICOs? Trading? Liquid Asset? Economics

consideration?

©2017 RSM US LLP. All Rights Reserved.

Accounting and Financial Reporting of Digital Currencies

• Recognition and measurement− Trade/execution date?

− Time of day? Close of business?

− Offsetting considerations

− Carrying value (fair value vs. cost, subject to impairment?)

• Disclosure considerations− If fair value, fair value hierarchy?

− Operating risks (keys stolen, lost, destroyed or otherwise compromised)

− Market risks

− Liquidity risks

− Counterparty and credit risks – cryptocurrency platforms/exchanges

©2017 RSM US LLP. All Rights Reserved.

What about SIPC Revenue?

• It is not clear whether revenues earned by a

broker-dealer related to digital asset activities is

included in SIPC revenue

− Is the digital asset a security? Does it matter?

©2017 RSM US LLP. All Rights Reserved. ©2017 RSM US LLP. All Rights Reserved.

RESTRICTED CASH

©2017 RSM US LLP. All Rights Reserved.

Restricted Cash

• ASU 2016-18, Statement of Cash Flows (Topic 230): Restricted Cash

• Effective for public business entities for fiscal years ending after December 15, 2017

• Designed to reduce diversity in practice in cash flow presentations

• Entities must include restricted cash and cash equivalents in the reconciliation from beginning to end-of-period total cash amounts

• Entities must disclose the nature of restrictions on restricted cash

45

©2017 RSM US LLP. All Rights Reserved.

Broker-Dealer Considerations

• ASU does not include a definition – covers “…

amounts generally described as restricted cash

or restricted cash equivalents”

• Broker-dealers would consider proper

presentation of disclosure of cash segregated

under SEC 15c3-3/PAB requirements and

CFTC regulations

• Several broker-dealers adopted for Q1 2018

10-Q

46

©2017 RSM US LLP. All Rights Reserved. ©2017 RSM US LLP. All Rights Reserved.

INCOME TAXES (TCJA)

©2017 RSM US LLP. All Rights Reserved.

Financial statement impacts of Tax Cuts and Jobs Act

• On December 22, the Tax Cuts and Jobs Act (the “Act”) was

signed into legislation

• Most significant change in U.S. tax law since 1986

• Significant financial statement impacts on a number of

areas as a result of the Act including:

─ Deferred tax assets and liabilities

─ Accumulated Other Comprehensive Income (AOCI)

─ Net operating losses (NOLs)

─ Alternative minimum tax

─ Foreign operations

©2017 RSM US LLP. All Rights Reserved.

The Act

• New law changes the discussion on tax impacts of revenue recognition

• New tax revenue recognition rules for entities with applicable financial statements (AFS)

• Significant changes− Revenue is fixed for tax when (1) the payment is earned through

performance, (2) payment is due to the taxpayer, (3) payment is received by the taxpayer, or (4) the item of gross income, or any portion thereof, is taken into account as revenue in the AFS, whichever happens earliest

• Tax will also follow the allocation of the transaction price

• Does not apply to special methods of accounting (e.g., percentage-of-completion, installment sales)

©2017 RSM US LLP. All Rights Reserved.

Deferred tax assets and liabilities under the Act

• ASC 740 requires that the effects of a change in tax law and rates be accounted for in the period of enactment

− Deferred tax assets and liabilities are required to be adjusted to reflect the effect of a change in tax rates in the period of enactment

• The Act reduces corporate tax rates from 35% to 21% for tax years beginning after 12/31/17

− In financial statements for interim or annual periods after 12/22/17, deferred tax assets and liabilities should be determined based on the new corporate tax rate in effect when they will reverse

− Changes to deferred taxes would be recorded in continuing operations and would not be subject to the intraperiod allocations

©2017 RSM US LLP. All Rights Reserved.

Non-calendar year-end public business entities

• Non-calendar year-end public entities must reflect the

changes under the Act in the quarter that includes

12/22/17

• Estimated annual effective tax rate for the current year

should be adjusted in the quarter of enactment

• Estimated change in the deferred tax items as of the

beginning of the year should be treated as a discrete

item in the quarter of enactment

• Scheduling of deferred tax items may be needed to

determine the appropriate tax rate for reversal

©2017 RSM US LLP. All Rights Reserved.

ASU 2018-02, Reclassification of Certain Tax Effects from Accumulated Other Comprehensive Income

• Changes in rates for items included in AOCI go through

income taxes from continuing operations

• This results in a disproportionate tax effect being

recorded in AOCI (referred to as stranded tax effects)

• Historically this disproportionate impact would have

been reversed based upon an accounting policy election

• The ASU allows for reclassification from AOCI to

retained earnings for stranded tax effects resulting from

the Tax Cuts and Jobs Act

©2017 RSM US LLP. All Rights Reserved.

ASU 2018-02, Reclassification of Certain Tax Effects from Accumulated Other Comprehensive Income

Permitted

2019

If elected, the effective date for calendar year-ends

Required

©2017 RSM US LLP. All Rights Reserved.

NOLs under the Act

• NOLs arising in taxable years beginning after 12/31/17

may only offset 80% of current year taxable income

• NOLs arising in taxable years ending after 12/31/17

may not be carried back but can be carried forward

indefinitely

• The Act does not change the pre-2018 NOL usage,

carryover or carryback periods

• These changes will affect a company’s assessment of

the ability to utilize NOLs against deferred tax liabilities

©2017 RSM US LLP. All Rights Reserved.

Corporate alternative minimum tax under the Act

• Corporate alternative minimum tax is repealed for

taxable years beginning after 12/31/17

• Existing AMT credits will continue to be allowed to

offset regular tax liability after other credits

• Any AMT credits not used to reduce regular tax will

begin to be refunded starting in years beginning after

2017

• These changes will result in a release of a valuation

allowance against any AMT credits

©2017 RSM US LLP. All Rights Reserved.

Foreign operations under the Act

• U.S. companies will be required to include in U.S. taxable income the total amount of unremitted foreign earnings of its controlled foreign subsidiaries

− Effective for a foreign corporation’s final year beginning prior to 2018, which would include years ending 12/31/17

− As a result, the concept of permanent reinvestment in a foreign subsidiary would no longer be relevant as it relates to potential U.S. tax on foreign earnings

• Tax due on deemed repatriation may be paid over an eight-year period

− An entity that elects to pay the tax related to repatriation over eight years will need to record a portion of the payable as a current liability and a portion as a non-current liability

− Amount should not be recorded as a deferred tax item as it represents an actual tax liability

©2017 RSM US LLP. All Rights Reserved.

SEC guidance

• In late December, the SEC issued SAB 118 (codified in SAB Topic

5.EE) which addresses the application of ASC 740 in the reporting

period that includes the date on which the Act was signed into law

• While ASC 740 provides accounting and disclosure guidance on

accounting for income taxes, it does not address the treatment

when the accounting for certain income tax effects of the Act is

incomplete at the time financial statements are issued

• SAB 118 provides that in cases in which the accounting for certain

income tax effects of the Act is incomplete but companies can

make a reasonable estimate of the effects of the tax law change,

that estimate should be recorded with appropriate disclosures

─ The estimate would be reported as a provisional amount in the company’s

financial statements during the one-year measurement period

─ Any adjustments during the measurement period should be included in

income from continuing operations as a tax expense/benefit in the

reporting period the adjustments are determined

©2017 RSM US LLP. All Rights Reserved.

SEC guidance (cont.)

─ If a company does not have the necessary information

available, prepared, or analyzed regarding certain

income tax effects of the Act to determine a reasonable

estimate to be included as provisional amounts:

• No related amounts should be included in an entity’s

financial statements for those specific income tax effects for

which a reasonable estimate cannot be determined

• A company should continue to apply ASC Topic 740 (e.g.,

when recognizing and measuring current and deferred

taxes) based on the provisions of the tax laws in effect

immediately prior to the Act being enacted

©2017 RSM US LLP. All Rights Reserved.

January 10th FASB meeting

• FASB issued a Q&A indicating that

− Private companies could follow the SAB 118 guidance

− Deemed repatriation payments and refundable AMT

credits should not be discounted

©2017 RSM US LLP. All Rights Reserved.

Challenges?

• Since enacted date of Act is tax years

beginning after 12/31/17, tax

acceleration for ASC 605/various other

GAAP guidance in 2017 (private

companies)

• Then additional potential change in

2018/2019 as ASC 606 is fully

implemented across all required entities

• IRS has not yet commented on how to

effect any of these changes

©2017 RSM US LLP. All Rights Reserved.

BBA Audit Rules

IRS – amended partnership audit rules for tax years beginning in 2018

• TEFRA partnership audit rules replaced by the “BBA audit rules” (Bipartisan Budget Act of 2015)

• IRS will generally collect tax at partnership level on adjustments at the highest corporate or individual rate

• Accounting for uncertain tax positions will become more complex

61

©2017 RSM US LLP. All Rights Reserved.

Tax reform resource center

Additional information on how legislation can affect your business and

tax planning

visit - rsmus.com/taxreform

©2017 RSM US LLP. All Rights Reserved. ©2017 RSM US LLP. All Rights Reserved.

CURRENT EXPECTED CREDIT LOSS (CECL)

©2017 RSM US LLP. All Rights Reserved.

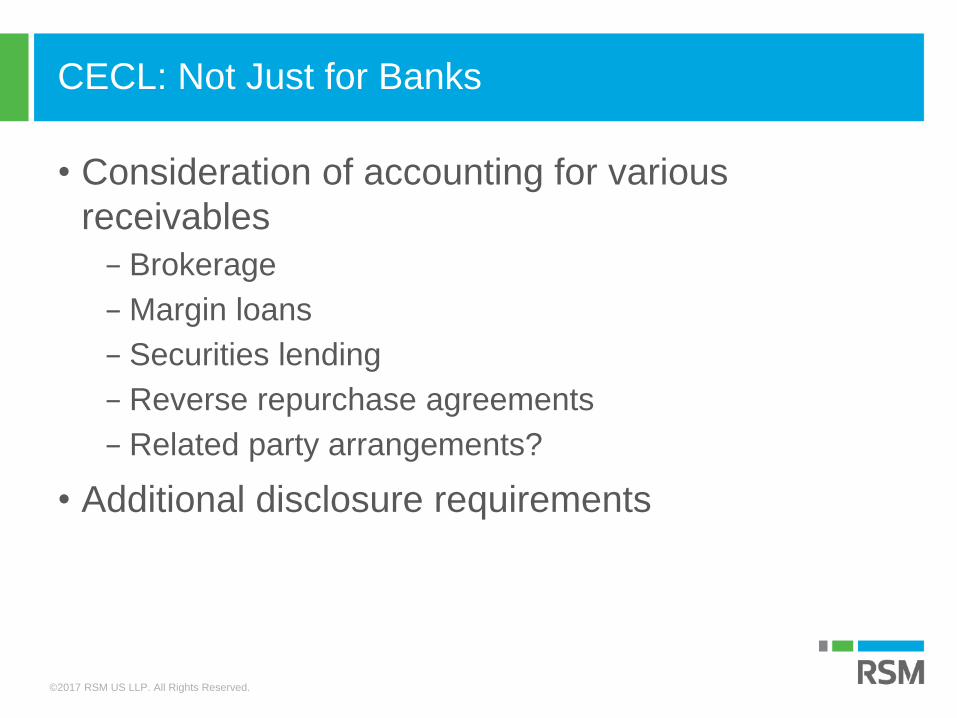

CECL: Not Just for Banks

• Consideration of accounting for various

receivables

− Brokerage

− Margin loans

− Securities lending

− Reverse repurchase agreements

− Related party arrangements?

• Additional disclosure requirements

©2017 RSM US LLP. All Rights Reserved.

Overview of the credit losses standard

• ASU 2016-13, Measurement of Credit Losses on

Financial Instruments

• Creates ASC Topic 326 • Subtopic 326-20 applies to financial assets measured at

amortized cost

− Supersedes impairment guidance in ASC 310 on

receivables/loans and ASC 320 on debt securities

(amongst other changes)

©2017 RSM US LLP. All Rights Reserved.

Effective dates of the credit losses standard

• SEC filers – fiscal years beginning after 12/15/19 (including interim periods) – 2020 for calendar year-end entities (“CYE”)

• Public Business Entities that are not SEC filers – fiscal years beginning after 12/15/20 (including interim periods) – 2021 for CYE

• All others – fiscal periods beginning after 12/15/20 (interim periods beginning after 12/15/21) – 2021 for CYE

• Early adoption is permitted for fiscal years beginning after 12/15/18 – 2019 for CYE

• Adopt through a cumulative effect adjustment to retained earnings− Special rules for other-than-temporary impairment (“OTTI”), purchased

financial assets with a more-than-insignificant amount of credit deterioration since origination (“PCD assets”) and beneficial interests

©2017 RSM US LLP. All Rights Reserved.

Applicability of ASC 326-20

• The following are in-scope:− Financial assets measured at amortized cost (AC)

including:• Financing receivables (loans)

• Held to maturity debt securities

• Receivables from revenue transactions with customers and other income

• Reinsurance receivables

• Receivables related to repo and securities lending agreements

− Net investment in leases

− Off-balance-sheet credit exposures• Loan commitments

• Standby letters of credit

• Financial guarantees/similar instruments

©2017 RSM US LLP. All Rights Reserved.

Applicability of ASC 326-20

• The following are out of scope:

− Financial assets measured at fair value (FV)

• Available-for-sale securities

• Other

− Loans made to participants by defined contribution

employee benefit plans

− Policy loans receivable of an insurance entity

− Promises to give (pledges receivable) of a not-for-

profit entity

− Loans and receivables between entities under

common control

©2017 RSM US LLP. All Rights Reserved.

Major provisions of ASC 326-20

• Recognize expected (rather than incurred) credit losses− Through allowance for recognized financial assets

(including held-to-maturity ("HTM”) debt securities)

− Through liability for off balance sheet exposures

− Results in day 1 life of asset expected loss recognition

• Exception: Initial allowance recorded as increase to purchase price for PCD assets (Assets that as of the date of acquisition have experienced a more-than-insignificant deterioration in credit quality since origination – “Purchased with credit deterioration”)

− Changes in the allowance (plus and minus) are recorded immediately through credit loss expense

©2017 RSM US LLP. All Rights Reserved.

Major provisions of ASC 326-20

• Measure expected losses on a pool basis

whenever similar risk characteristics exist

• No one method required. Some examples:

− Discounted cash flows

− Loss rate methods

− Roll-rate methods

− Probability of default methods

− Based on an aging analysis

©2017 RSM US LLP. All Rights Reserved.

Major provisions of ASC 326-20

• Consider relevant available information (internal and/or external) when estimating expected losses

• Don’t rely solely on past events – Adjust historical loss information for− Differences in current asset specific risk

characteristics

− Circumstances when historical info is not reflective of contractual term

− Current conditions

− Reasonable and supportable forecasts

©2017 RSM US LLP. All Rights Reserved.

Major provisions of ASC 326-20

• When estimating losses for periods beyond reasonable and supportable forecast, revert to historical loss information− Input level or based on the entire estimate

− Immediately, straight line basis or another rational and systematic basis

• Include measure of expected risk of loss even if remote− May reach conclusion expected credit loss is zero if

justified based on historical loss info adjusted for current conditions and reasonable and supportable forecasts

©2017 RSM US LLP. All Rights Reserved.

Major provisions of ASC 326-20

• Collateral dependent practical expedient (PE)

available when:

− Borrower is experiencing financial difficulty

− Repayment is expected substantially through the

operation or sale of the collateral

• Base estimate of credit loss on amortized cost

less fair value of collateral

− Adjust for selling costs if expect repayment through

sale of collateral

• Must be used if foreclosure is probable

©2017 RSM US LLP. All Rights Reserved.

Major provisions of ASC 326-20

• Collateral maintenance provisions PE

− Borrower required to continually adjust the amount of

collateral as a result of fair value changes in the collateral

− Limit allowance to excess of amortized cost of asset over

fair value of collateral

• Through PEs only, could conclude expected loss is

zero solely on the basis of the current collateral

value. Absent PE, would need to consider potential

future changes in collateral value and historical loss

info for assets with similar collateral

©2017 RSM US LLP. All Rights Reserved. ©2017 RSM US LLP. All Rights Reserved.

ACCOUNTING STANDARDS UPDATES

©2017 RSM US LLP. All Rights Reserved.

Final standards recently issued

ASU 2017-12, Derivatives and Hedging (Topic 815): Targeted

Improvements to Accounting for Hedging Activities

ASU 2017-11, Earnings Per Share (Topic 260); Distinguishing

Liabilities from Equity (Topic 480); Derivatives and Hedging (Topic

815): (Part I) Accounting for Certain Financial Instruments with

Down Round Features, (Part II) Replacement of the Indefinite

Deferral for Mandatorily Redeemable Financial Instruments of

Certain Nonpublic Entities and Certain Mandatorily Redeemable

Noncontrolling Interests with a Scope Exception

©2017 RSM US LLP. All Rights Reserved.

Final standards recently issued

ASU 2017-15, Codification Improvements to Topic 995, U.S.

Steamship Entities: Elimination of Topic 995

ASU 2017-14, Income Statement—Reporting Comprehensive

Income (Topic 220), Revenue Recognition (Topic 605), and

Revenue from Contracts with Customers (Topic 606) (SEC

Update)

ASU 2017-13, Revenue Recognition (Topic 605), Revenue from

Contracts with Customers (Topic 606), Leases (Topic 840), and

Leases (Topic 842): Amendments to SEC Paragraphs Pursuant to

the Staff Announcement at the July 20, 2017 EITF Meeting and

Rescission of Prior SEC Staff Announcements and Observer

Comments (SEC Update)

©2017 RSM US LLP. All Rights Reserved.

Final standards recently issued

ASU 2018-02, Income Statement—Reporting Comprehensive Income

(Topic 220): Reclassification of Certain Tax Effects from Accumulated

Other Comprehensive Income

ASU 2018-01, Leases (Topic 842): Land Easement Practical

Expedient for Transition to Topic 842

©2017 RSM US LLP. All Rights Reserved.

Final standards recently issued

ASU 2018-05, Income Taxes (Topic 740): Amendments to SEC

Paragraphs Pursuant to SEC Staff Accounting Bulletin No. 118 (SEC

Update)

ASU 2018-04, Investments—Debt Securities (Topic 320) and

Regulated Operations (Topic 980): Amendments to SEC Paragraphs

Pursuant to SEC Staff Accounting Bulletin No. 117 and SEC Release

No. 33-9273 (SEC Update)

ASU 2018-03, Technical Corrections and Improvements to Financial

Instruments—Overall (Subtopic 825-10): Recognition and

Measurement of Financial Assets and Financial Liabilities

©2017 RSM US LLP. All Rights Reserved.

ASU 2017-12, Targeted Improvements to Accounting for Hedging Activities

• ASU brings relief to the rigors of hedge accounting,

including:

− Reduced upfront documentation requirements for certain

private companies and ability to wait until financial

statements are available to be issued to assess

effectiveness

− Other entities can wait until the quarterly effectiveness

testing to perform the initial assessment of effectiveness

− Can apply long-haul method if short cut method was not or

no longer is appropriate

©2017 RSM US LLP. All Rights Reserved.

ASU 2017-12, Targeted Improvements to Accounting for Hedging Activities

• Expanded risks eligible for hedging:

− Contractually specified component in cash flow hedge of

commodities

− Contractually specified interest rate in cash flow hedge of

interest rate risk

− Changes in fair value attributable to changes in SIFMA for

fair value hedge of interest rate risk

• Additional flexibility for fair value hedges of interest

rate risk

©2017 RSM US LLP. All Rights Reserved.

ASU 2017-12, Targeted Improvements to Accounting for Hedging Activities

• Less quantitative analysis will be required

− If initial quantitative assessment indicates relationship is

highly effective, can elect to perform subsequent

assessments qualitatively absent a significant change in

facts and circumstances

− Can assume dates match if forecasted transaction

occurs, and derivative matures, within same 31 day

period

− Ineffectiveness is no longer separately measured and

recognized

©2017 RSM US LLP. All Rights Reserved.

ASU 2017-12, Targeted Improvements to Accounting for Hedging Activities

• Certain transition elections permitted including:

− Switch from quantitative assessment to qualitative

− Indicate quantitative method to be used in the event short

cut method fails

− Redesignate hedged risk as contractually specified

component

− Reclassify debt security from HTM to AFS if eligible to be

hedged under last-of-layer method

• PBEs and certain private companies must make

elections in quarter of adoption, others before next

financial statements are available to be issued

©2017 RSM US LLP. All Rights Reserved.

ASU 2018-03, Technical Corrections and Improvements to Financial Instruments—Overall (Subtopic 825-10)

The amendments clarify certain aspects of the guidance issued in

ASU 2016-01

Issue Summary of amendment

Equity Securities without a Readily

Determinable Fair Value –

Discontinuation: Once an entity elects

the measurement alternative in ASC

321-10-35-2, the entity must continue to

apply the alternative until the investment

has a readily determinable fair value or

becomes eligible for the net asset value

practical expedient.

Are there additional situations that may

allow for an entity to discontinue the

measurement alternative?

An entity measuring an equity

security using the measurement

alternative may change its

measurement approach to a fair

value method, through an

irrevocable election that would apply

to that security and all

identical or similar investments of

the same issuer.

©2017 RSM US LLP. All Rights Reserved. ©2017 RSM US LLP. All Rights Reserved.

OTHER TOPICS

©2017 RSM US LLP. All Rights Reserved.

On the Horizon

FASB is working on various projects including

targeted improvements and clarifications:

Related party guidance for VIEs

Leases

Disclosures of fair value measurements

Digital currencies?

86

©2017 RSM US LLP. All Rights Reserved.

Segment Reporting

Are broker-dealers subject to the segment reporting requirements under ASC 280?

− PBEs are encouraged but not required to provide disclosures in Topic 280, unless those entities also meet the definition of a “public entity” as defined in Section 280-10-20

− Public entity is a business entity… that is required to file financial statements with the SEC

− When issued, SFAS 131 superseded FASB Technical Bulletin No. 79-8, which scoped out broker-dealers

87

©2017 RSM US LLP. All Rights Reserved.

Going Concern

Statement on Auditing Standards No. 132

effective for audits of financial statements for

periods ending on or after December 15, 2017

• Includes consideration of management’s

evaluation (now required post ASU 2014-15)

• Assumption that the entity will continue its

operations for a reasonable period of time

− Generally one year from when financial statements

are issued or available to be issued, where

applicable

88

©2017 RSM US LLP. All Rights Reserved.

Resources

• AICPA Expert Panel - Stockbrokerage and

Investment Banking website (Minutes)

• FASB Website (fasb.org)

• FINRA - Annual Regulatory and Examination

Priorities Letter

• SEC Examination Priorities

• SEC No-Action Letter dated November 8, 2016

• RSM Financial Reporting Resource Center

89

©2017 RSM US LLP. All Rights Reserved.

RSM thought leadership

visit - rsmus.com/frrc

©2017 RSM US LLP. All Rights Reserved. ©2017 RSM US LLP. All Rights Reserved.

FOR MORE INFORMATION PLEASE CONTACT:

PAUL J. NOCKELSPARTNER, GREAT LAKES FINANCIAL SERVICES PRACTICE LEADER

RSM US LLPONE SOUTH WACKER DRIVE, SUITE 800CHICAGO, ILLINOIS 60606OFFICE: [email protected]

©2017 RSM US LLP. All Rights Reserved. ©2017 RSM US LLP. All Rights Reserved.

92

©2017 RSM US LLP. All Rights Reserved.

This document contains general information, may be based on authorities that are subject to change, and is not a substitute for professional

advice or services. This document does not constitute audit, tax, consulting, business, financial, investment, legal or other professional

advice, and you should consult a qualified professional advisor before taking any action based on the information herein. RSM US LLP, its

affiliates and related entities are not responsible for any loss resulting from or relating to reliance on this document by any person. Internal

Revenue Service rules require us to inform you that this communication may be deemed a solicitation to provide tax services. This

communication is being sent to individuals who have subscribed to receive it or who we believe would have an interest in the topics

discussed.

RSM US LLP is a limited liability partnership and the U.S. member firm of RSM International, a global network of independent audit, tax and

consulting firms. The member firms of RSM International collaborate to provide services to global clients, but are separate and distinct legal

entities that cannot obligate each other. Each member firm is responsible only for its own acts and omissions, and not those of any other

party. Visit rsmus.com/about us for more information regarding RSM US LLP and RSM International.

RSM® and the RSM logo are registered trademarks of RSM International Association. The power of being understood® is a registered

trademark of RSM US LLP.

© 2017 RSM US LLP. All Rights Reserved.