Embed Size (px)

Citation preview

Working Paper CompetitionintheMobileHandsetIndustry

CommissionedbyQualcomm

ByAntonioVaras,DavidC.Michael,DerekKennedy,andFrançois

Schaus

Working Paper 1

THE BOSTON CONSULTING GROUP JULY 2016

TheBostonConsultingGroup(BCG)isaglobalmanagementconsultingfirmandtheworld’sleadingadvisoronbusinessstrategy.Wepartnerwithclientsfromtheprivate,public,andnot‐for‐profitsectorsinallregionstoidentifytheirhighest‐valueopportunities,addresstheirmostcriticalchallenges,andtransformtheirenterprises.Ourcustomizedapproachcombinesdeepinsightintothedynamicsofcompaniesandmarketsandclosecollaborationatalllevelsoftheclientorganization.Thisensuresthatourclientsachievesustainablecompetitiveadvantage,buildmorecapableorganizations,andsecurelastingresults.Foundedin1963,BCGisaprivatecompanywith85officesin48countries.Formoreinformation,pleasevisitbcg.com.AboutthisPaperAsafollow‐uptoTheBostonConsultingGroup's“MobileRevolution”report,

publishedinDecember2015,QualcommcommissionedBCGtoconductan

independentstudytoassessthecompetitivedynamicsofthemobilehandsetvalue

chain.Theworkincludedassemblingandanalyzingobjectivedatafromindustry

sources.QualcommdidnotsupplyanydataorprovideanyinputintoBCG's

conclusions.BCGissolelyresponsibleforallanalysesandconclusionsincludedin

thispaper.

Working Paper 2

THE BOSTON CONSULTING GROUP JULY 2016

obiletechnologieshavebecomevitaltoeconomiesaroundtheworld.As

wediscussedinourpreviousreport,TheMobileRevolution:HowMobile

TechnologiesDriveaTrillion‐DollarImpact,themobileindustryhas

profoundlytransformedthewaywelive,work,andstayconnected.Mobilehas

rapidlyemergedasaprimaryengineofeconomicgrowth,generatingmorethan$1

trillionofGDPcontributionand$6trillionofconsumersurplusglobally.Noteven

theIndustrialRevolutioncreatedsuchaswiftandradicalexplosionintechnological

innovationandeconomicgrowthworldwide.

Givenmobile’sunprecedentedimpact,policymakersaroundtheworldare

interestedinhowtobestpromoteanddevelopthesector.Thenatureofcompetition

isacriticalaspecttoconsiderinformulatingpoliciesandregulatoryinitiatives

aimedatfosteringinnovationandincreasingadoptionofadvancedmobileservices.

Whiletherehasbeenextensiveresearchandpublicdebateaboutthemarket

structureattheservice‐providerlevel(mobilenetworkoperatorsandmobile

virtualnetworkoperators),thecompetitivedynamicsofthemobilehandsetmarket

anditsglobalvaluechainhavereceivedlessattention.Drawinguponananalysisof

industrydata,weprovideafactbaseonthestateofcompetitioninthemobile

handsetvaluechainandofferacomparativeperspective.

Usingmeasuressuchasmarketconcentrationandbarrierstoentryandmarket

characteristicssuchasconsumerchoice,prices,andperformanceimprovements,we

foundthatthemobileindustryisincreasinglycompetitive.(SeeExhibit1.)

M

Working Paper 3

THE BOSTON CONSULTING GROUP JULY 2016

Theintensifiedcompetitionhasbeenpromotedbyastructuraltransformationin

thehandsetvaluechainduringthepast15years:fromaverticallyintegratedmodel

whereeachcompanysellingabrandedmobilehandset(ahandsetmaker)hadto

developitsownversionofthephone’smostcomplextechnologyelements,toa

horizontalmodelinwhichthesecriticaltechnologyelementsarenowavailable

throughspecializedvendors.Thisshiftwasenabledbytheconfluenceoffourkey

drivers:

Theemergenceofdiverseandcompetitivecomponentmarkets,eachwithat

leastthreeorfourestablishedsuppliers.

Thetransitiontointegrated“system‐on‐chip”(SoC).

Theavailabilityofindependentsmartphoneoperatingsystemsand

ecosystems.

Theriseofunifiedglobalmobilecommunicationsstandards.

Exhibits - Inside the Smartphone - 2016 07 11 dk (AV edits).pptx 1

Sources: IDC; GSM Arena; Apple; BCG analysis OEM=original equipment manufacturer

Key facts about the mobile handset market

Low market

concentration

273 OEMs in the market today

Lowest degree of concentration (and sharpest decrease since 2007) among 10 high-tech industries evaluated

Low barriers to entry and dynamic landscape of competition

88% of current OEMs have entered the market after 2007

Only two of the top 10 OEMs by volume in 2015 were already in that echelon in 2007

25 new players in past five years with more than $100 million in revenues, generating combined revenues of approximately $35 billion in 2015

New entrants from all regions achieving significant market positions in all global markets, both emerging and developed

Wide consumer choice More than 700 different handsets available at prices ranging from $40 to $800

Similar premium hardware specifications found in handsets priced from $270 to $700

Lower prices over time

32% decline in the average selling price of smartphones in past five years

Explosion of low-cost smartphones (priced below $200), representing 54% of unit sales

High degree of innovation Approximately 3,000 times improvement in download and upload speeds since 2007

More than 50 times improvement in processors; 1.2 to 3 times improvement in non-silicon parts

Characteristics of competitive markets

Exhibit 1: The Mobile Handset Market is Highly Competitive

Working Paper 4

THE BOSTON CONSULTING GROUP JULY 2016

Underlyingeachofthesefactorsisalicensingmodelthatgivesallindustry

participantsaccesstoessentialtechnology,therebyloweringthebarrierstoentryin

criticalareasofthemobilehandsetvaluechain.

Bytransformingwhatisinsidethesmartphone,thesechangeshavemadeitpossible

forhandsetmakerstobringadevicetomarketwithoutmakingsignificant

investmentsindevelopingcomponents,operatingsystems,andapplications.Indeed,

theR&Dcostasapercentageofrevenuesformobilehandsetmakershasdecreased

from7%to15%intheearly2000sto2%to6%in2014and2015.Theresulthas

beenadramaticincreaseinthechoiceandaffordabilityofhandsetsavailabletoall

consumersglobally,eveninemergingmarkets:morethan715newsmartphone

modelswerebroughttomarketworldwidein2015,accordingtoGSMArena,and54%

ofglobalunitsalescamefrommodelspricedbelow$200,accordingtoIDC.

Lookingahead,handsetmakerswillneedtopursuenewsourcesofdifferentiationin

theirincreasinglycompetitivemarket.Brandingandexcellenceinsaleschannelsare

becomingmoreimportant.Atthesametime,innovationwillcontinuetobecritical,

particularlyasnewtypesofdevicesemergethatmustbeconnectedand

orchestratedintotheInternetofThings.Newcapabilitieswillberequired,asthe

sourceofcompetitiveadvantageisrapidlyshiftingfromhardwaretosoftwareand

dataanalyticsthatdeliverthehighlypersonalized,richeruserexperiencesthat

consumersdemand.Asaresult,policymakersneedtoensurethattheregulatory

frameworkcontinuestopromotethehighlevelofinnovationandcompetitionthat

havebroughtthebenefitsoftheMobileRevolutiontoconsumersacrosstheglobe.

CompetitiveIntensityintheMobileHandsetMarket

Ourresearchfoundthatthemobilehandsetindustryisincreasinglycompetitive,

bothovertimeandrelativetootherrelevantindustries,whenassessedagainstfive

keyparameters.

Working Paper 5

THE BOSTON CONSULTING GROUP JULY 2016

1.LOWMARKETCONCENTRATION

UsingtheHerfindahl‐HirschmanIndex(HHI)1tomeasuremarketconcentration,we

foundthatthemarketformobilehandsetswasthemostcompetitiveamongtheten

consumerandenterprisetechnologyindustriesweexamined.Thetoptenhandset

makershaveanHHIof6.6%,comparedwith10.6%forthetopPCmanufacturers

and13.5%forthetopservermanufacturers,forexample.(SeeExhibit2.)Infact,the

mobilephonemarket’sconcentrationdecreasedby70%from2007through2015.

Thisisafargreaterdecreaseinconcentrationthananyotherelectronicsindustry

experiencedduringthatperiod.

Reflectingthehandsetmarket’sdecreasingconcentration,tenhandsetmakershad

marketshare(measuredinunitsshipped)ofatleast2%in2015,comparedwith

onlyfivein2007.Themarketshareoftoday’slargesthandsetmakerislessthan

22%.

1 TheHerfindahl‐Hirschman Index (HHI) is a commonly acceptedmeasure ofmarket concentration. It is calculatedby squaring themarketshareofeachfirmcompetinginamarket,andthensummingtheresultingnumbers.TheHHIcanrangebetween0%and100%.Thecloseramarketistobeingamonopoly,thehighertheHHI.AlowerHHImeansamorefragmentedandcompetitiveindustry.

Exhibits - Inside the Smartphone - 2016 07 11 dk (AV edits).pptx 2

Exhibit 2: The Mobile Handset Market Has the Lowest Concentration Among Comparable Tech Sectors

Herfindahl-Hirschman Index for top 10 vendors (%, based on 2014-2015 unit shipments)

41.7

27.225.6

18.318.214.813.5

10.68.56.6

Printers Digital cameras

Storage Servers PC TV Mobile handsets

Gaming consoles1

Enterprise network

equipment

Wireless network

infrastructure

15

25

Sources: IDC, Gartner, Euromonitor; BCG analysis Note: HHI=Herfindahl-Hirschman Index. HHI calculated for 2014 and 2015, depending on data availability. All market shares calculated in unit shipments, except revenues for wireless network infrastructure. 1. Top 3 players (Sony, Nintendo, and Microsoft) account for more than 99% of market share.

High

Low

-70 +62 +60 -36 +24 -24 -37 +163 -25 Change in 2007-2015 (%)

Level of concentration

Lowest HHI value and highest decrease

in the index since 2007

+5

Moderate

Working Paper 6

THE BOSTON CONSULTING GROUP JULY 2016

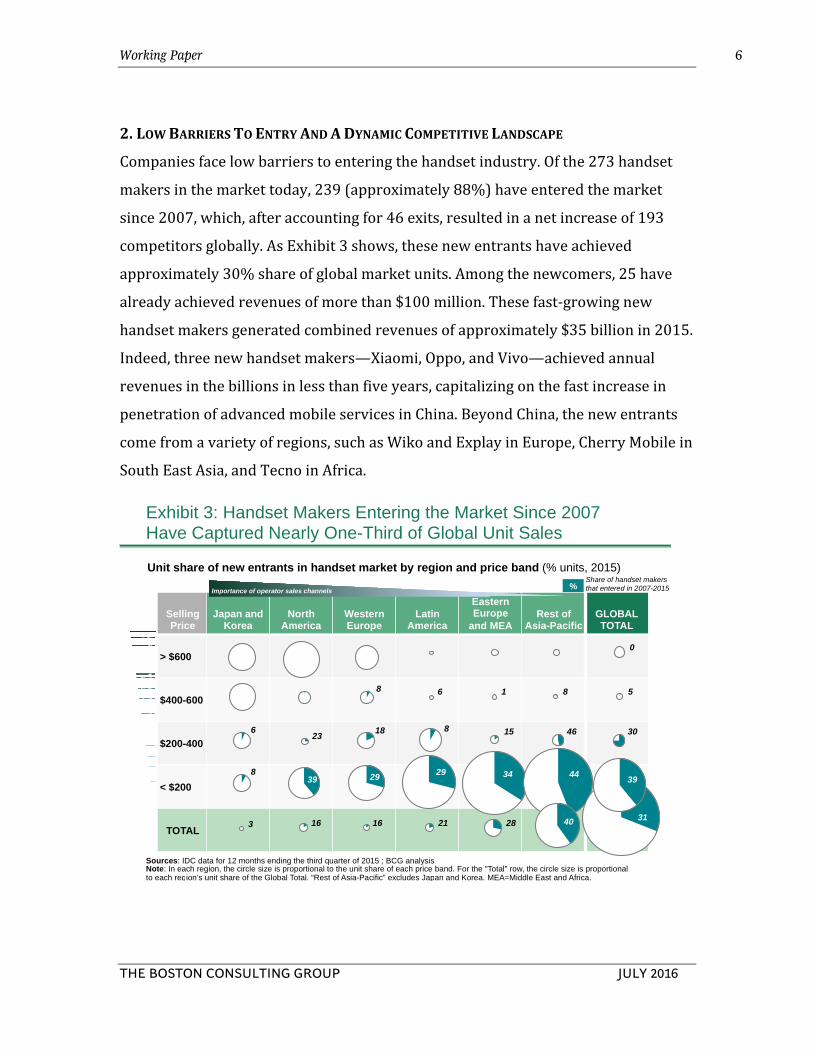

2.LOWBARRIERSTOENTRYANDADYNAMICCOMPETITIVELANDSCAPE

Companiesfacelowbarrierstoenteringthehandsetindustry.Ofthe273handset

makersinthemarkettoday,239(approximately88%)haveenteredthemarket

since2007,which,afteraccountingfor46exits,resultedinanetincreaseof193

competitorsglobally.AsExhibit3shows,thesenewentrantshaveachieved

approximately30%shareofglobalmarketunits.Amongthenewcomers,25have

alreadyachievedrevenuesofmorethan$100million.Thesefast‐growingnew

handsetmakersgeneratedcombinedrevenuesofapproximately$35billionin2015.

Indeed,threenewhandsetmakers—Xiaomi,Oppo,andVivo—achievedannual

revenuesinthebillionsinlessthanfiveyears,capitalizingonthefastincreasein

penetrationofadvancedmobileservicesinChina.BeyondChina,thenewentrants

comefromavarietyofregions,suchasWikoandExplayinEurope,CherryMobilein

SouthEastAsia,andTecnoinAfrica.

Exhibits - Inside the Smartphone - 2016 07 11 dk (AV edits).pptx 3

Exhibit 3: Handset Makers Entering the Market Since 2007 Have Captured Nearly One-Third of Global Unit Sales

Selling Price

Japan and Korea

North America

Western Europe

Latin America

Eastern Europe

and MEA Rest of

Asia-Pacific GLOBAL TOTAL

> $600

$400-600

$200-400

< $200

TOTAL

Unit share of new entrants in handset market by region and price band (% units, 2015)

6

8

3

23

39

16

8

18

29

16

6

8

29 34 44 39

31 40 21 28

15 46 30

1 8 5

0

Sources: IDC data for 12 months ending the third quarter of 2015 ; BCG analysis Note: In each region, the circle size is proportional to the unit share of each price band. For the "Total" row, the circle size is proportional to each region’s unit share of the Global Total. “Rest of Asia-Pacific” excludes Japan and Korea. MEA=Middle East and Africa.

% Share of handset makers that entered in 2007-2015Importance of operator sales channels

Imp

ort

an

ce o

f b

ran

d a

nd

o

pe

rato

r h

and

se

t su

bs

idy

Working Paper 7

THE BOSTON CONSULTING GROUP JULY 2016

Asanindicationoftheindustry’sintensecompetition,marketsharesfluctuated

significantlyfrom2007through2015.Theresulthasbeensignificantturnover

amongthemarketleaders.Forexample,onlytwoofthetoptenmobilehandset

makersbyunitssoldin2007(SamsungandLG)remainedinthetoptenin2015,

whiletwoothers(Nokia,Motorola)havebeenabsorbedbycompetitors.

3.WIDECONSUMERCHOICE

Today,consumersinbothdevelopedandemergingmarketscanselectfromseveral

hundredmobilehandsetmodelsacrossawiderangeofpricepoints.Forexample,of

thenewsmartphonemodelstrackedbyGSMArenain2015,approximately40%

werepricedbelow$200,withmodelsavailableforaslowas$40.Similar

combinationsofleadingedgehardwarespecificationsandfeaturescanbefoundin

handsetsfrommultiplebrands,atpricesrangingfrom$270to$700.

4.LOWERPRICESOVERTIME

Inadditiontohavingmorechoices,consumersarebenefitingfromlowerpricesfor

handsets.Priceshavefallensignificantlyashandsetmakersfightforshareintheir

competitivemarket.From2008through2015,theoverallaveragesellingprice(ASP)

ofsmartphonesdeclinedby33%;excludingApple’siPhone,thedeclinewas46%.

ThedeclineinASPwasdrivenbythegreateravailabilityofsmartphonespriced

under$200.Theselow‐costhandsetsaccountedforanestimated54%ofmarket

sharein2015,upfrom5%in2008.Notably,nosmartphoneswerepricedunder

$100in2010,butby2015theseultra‐low‐costhandsetshadcapturedanestimated

24%ofthemarket.Theavailabilityofultra‐low‐costhandsetsisdrivingthefast

adoptionofsmartphonesinemergingmarkets.InChina,forexample,20%of

smartphonemodelssellforlessthan$100,whichhashelpedtopromotea45%

penetrationrateforsmartphones.InIndia,wherethepenetrationratefor

smartphoneshasrapidlygrownto26%oftotalpopulationinrecentyears,50%of

smartphonemodelssellforlessthan$100.

Working Paper 8

THE BOSTON CONSULTING GROUP JULY 2016

5.PERFORMANCEIMPROVEMENTS

Theindustry’sintensecompetitionpromotesinnovationthathasgenerated

dramaticperformanceimprovementsforhandsetssince2007.Amongthemain

driversoftheimprovedperformancehavebeenadvancesinthecoremobile

communicationstechnologies.Theseadvancesledtoa12,000‐foldimprovementin

capacityfromsecond‐generation(2G)tofourth‐generation(4G)standards.The

radiofrequencyspectrumisthefundamentalconstrainedresourceinthewireless

network.Astheefficiencyofusingtheradiofrequencyspectrumleapfrogged,sotoo

didtheperformanceofthewirelessnetworkequipment,mobiledevices,andkey

siliconcomponentsthatincorporatewirelesscommunicationstechnologies.As

showninExhibit4,therehasbeenaleapintheperformanceofkeysilicon

components(suchasthebasebandandprocessor)thatincorporatewireless

communicationstechnologies.Incontrast,theperformanceofkeynon‐silicon

components(display,camera,andbattery)hasimprovedbyalowerfactor.

Exhibits - Inside the Smartphone - 2016 07 11 dk (AV edits).pptx 4

Exhibit 4: Continuous Innovation Has Dramatically Improved Handset Performance

Sources: Factiva, Apple, GSM Arena 1. Refers to combination of handset modem and wireless network system. 2. Comparing LTE-advanced with a maximum throughput with reported speed of Cingular's GSM/EDGE network at the time of iPhone launch. 3. Based on Apple keynote presentations on the performance of central processing unit and graphics processing unit.

Apple A9 Dual-core 1.85 GHz

Samsung 32-bit ARM-11 412 Mhz 50-84x3

GSM/ EDGE

(75-135 Kb/s)

GSM/HSPA/CDMA/ EVDO/Advanced LTE

(300 Mb/s) ~3,000x2

750 x 1334 pixels (~326 ppi pixel density)

480 x 320 pixels (~165 ppi pixel density) ~2x

12 Mpx 2 Mpx

1,715 mAh 1,400 mAh ~1.2x

2007: iPhone 2015: iPhone 6s Improvement

in performance

16 Gb 128 Gb 8x Storage memory

Processor

Cellular data capability1

Display

Camera

Battery

Silicon

Non- silicon

~6x

Networkand

silicon

Working Paper 9

THE BOSTON CONSULTING GROUP JULY 2016

FourKeyChangesPromotingCompetition

Someonelookinginsidetoday’ssmartphonesandyesterday’smobilehandsets

wouldseeastrikingcomparison.Duringthepast15years,thehardwareand

softwarebeneaththebrandedexteriorhavechangeddramatically.Componentsthat

wereoncedesignedandmadein‐housebyhandsetmakers,oronabespokebasis,

arenowdesignedandmadebyspecializedvendorsthatsellcutting‐edgesilicon

componentsonamerchantbasistomanymobilehandsetmakers.Discretechips

havebeenreplacedwithanintegrated“system‐on‐chip,”orSoC.Andinmanycases,

theproprietaryoperatingsystem(OS)hasbeenreplacedwithanindependentOS

andapplicationdevelopmentecosystem.

Asaresult,theroleofhandsetmakershaschangedsignificantly:manyarenowable

tofocustheirresourcesandexpertiseonfeatureselectionandoptimization,

industrialdesign,marketing,andothereffortstodifferentiatetheirproductsina

crowdedmarket.Theycandosobecauseothervaluechainplayershavetakenon

thetechnicallydemandingrolesindesigningandsupplyingcriticalcomponents.

Thisdramaticshiftfromaverticallyintegratedindustrytoahorizontalindustrythat

includesspecializedtechnologyvendorshaspropelledtoday’sintensecompetition.

Tounderstandwhathashappened,weexaminefourkeychangesthathaveoccurred

inthevaluechain.

EMERGENCEOFADIVERSEANDCOMPETITIVECOMPONENTMARKET

Asrecentlyas2000,thetophandsetmakerswereverticallyintegratedformanyof

thephone’ssiliconhardwarecomponents,includingthecellularbasebandmodem,

radiofrequencytransceivers,otherchipcomponentsforcellularcommunications,

andapplicationprocessors(totheextenttheywereincluded).Today,mosthandset

makersdonotdesignormanufacturetheirowncomponents.Instead,theytypically

canchooseamongthreeorfourmerchantsuppliersforeachsiliconcomponent.

Theycanalsoselectfromfiveorsixsuppliersforeachnon‐siliconcomponent.(See

Exhibit5.)

Working Paper 10

THE BOSTON CONSULTING GROUP JULY 2016

Theabilitytosourcecomponentsfromawiderangeofmanufacturershasbeen

criticaltoenablingnewhandsetmakerstoenterthemarket.Forexample,the

fastest‐growinghandsetmakersthatenteredthemarketinthepastfewyearshave

usedsevendifferentvendorsformodemsandapplicationprocessors,accordingto

IDCindustrydata.

Itisworthtakingadeeperlookatsiliconcomponents,particularlymodemsand

applicationprocessors,which,asdescribedabove,haveseenthebiggest

performanceimprovements.Thefactthatthemarketforthesesiliconcomponents

hasconsistentlyhadamoreconcentratedstructurethanthemarketfornon‐silicon

componentsisaconsequenceoftheincreasinglychallengingeconomicsof

innovationinsilicontechnology.AsExhibit6shows,thecostofchipdesign

increasedapproximatelysix‐foldfrom2006through2014.Costshaveskyrocketed

becauseindustryplayershavepushedtheboundariesofphysicstocontinue

increasingthenumberoftransistorspersquareinchofintegratedcircuitinline

Exhibits - Inside the Smartphone - 2016 07 11 dk (AV edits).pptx 5

Exhibit 5: There are More than Three Established Merchant Suppliers for All Silicon and Non-silicon Components

Sources: IDC; IHS; Gartner; ROA; iSuppli; Morgan Stanley; BCG analysis Notes: QCOM = Qualcomm; MTK = MediaTek; SPRD = Spreadtrum. PA = Power Amplifier; RFFE = Radio Frequency Front End; XCVR = Transceiver 1. Battery includes battery cells and packs. 2. Camera includes lens, sensor, and auto-focus factor.

100

0

50

75

25

MTK 18

SPRD 8

Cameras2

Other 17

RFFE

Sony 18

Omnivision 10

Samsung 7

Largan 4

Other 61

Battery1

Samsung 17

Simplo 15

Panasonic 14

LG 11

Other 44

LCD/OLED

Samsung 23

Japan Disp. 17

Sharp 15

LG 14

Chimei 10

Other 21

Touch

Intel 4

Synaptics 26

Broadcom 21

Focaltech 12

Other 40

Image

Sony 43

Samsung

19

Omnivision 14

Other 24

Sensors

STMicro 22

Knowles 18

Bosch 17

Avago 42

Skyworks 24

Qorvo 16

Other 18

PA

Qorvo 33

Skyworks 31

Avago 18

InvenSense 17

Broad- band

analog

QCOM 50

Maxim 14

Cirrus 14

Dialog 11

Other 12

Discrete broad- band

QCOM 50

Samsung 9

MTK 9

SPRD 8

Other 24

Integrated System-on-Chip

QCOM 66

MTK 21

HiSilicon 4 SPRD 3 Other 5

Discrete application processor

AAC 6

NAND

Samsung 30

Other 21

SK Hynix 24

Toshiba 21

Sandisk 17

Micron 5 Other 4

DRAM

Samsung 45

SK Hynix 30

Micron 23

Connectivity

Broadcom 34

MTK 12

QCOM 11

Marvell 4

Other 39

XCVR

QCOM 53

Apple 69

Samsung 24

Intel 3 Other 4

Other 17

Memory RF and Connectivity

Baseband Modem

Application Processor

Sensors Non-silicon

Total market is ~$105 billion Bar width = market ($billion)

First competitor by market share Second competitor by market share Third competitor by market share Fourth competitor by market share

Market share of key components for mobile handsets (%, 2014–2015)

Working Paper 11

THE BOSTON CONSULTING GROUP JULY 2016

withtheratepredictedbyMoore’sLaw.Thishasallowedsiliconvendorstodeliver

regularstep‐changeperformanceimprovementsindigitalprocessingcapacity.

Despitetherisingdevelopmentcosts,thesiliconcomponentmarkethasbeen

dynamicandcompetitive.Severalmobilechipsetvendorsexitedthemarketasthe

mobileindustrytransitionedfrom2Gtothird‐generation(3G)andthento4G

technology,andthecomplexityofchipdesignincreased,butnewplayershavealso

emerged.Amongthesenewplayersarelarge‐scalehandsetvendorsthathave

developeddesigncapabilitiesin‐houseasasourceofdifferentiationorcost

advantage.ExamplesincludeAppleandSamsunginthepremiumsegment,HiSilicon

(Huawei’schipdivision),and,veryrecently,Xiaomiinthemid‐tolow‐tiersegment.

Recententrantsalsoincludenewvendorsfocusedonservingthefast‐growing

handsetmakersinChinaandotheremergingmarkets,suchasMediaTek,

Spreadtrum,andLeadcore.

Exhibits - Inside the Smartphone - 2016 07 11 dk (AV edits).pptx 6

Evolution of advanced chip design cost1 by manufacturing node (illustration for complex chip)

Sources: IBS, Aug 2015; Synapsis; Apple keynote presentations 1. Represents the cost of developing a new primary design at high volume, such as a smartphone system-on-chip or application processor, at

a new process node, which requires qualifying a significant amount of intellectual property for that specific node. Subsequent designs at the same node typically cost less. 2. First year the node was achieved; typically becomes the iPhone production node one to two years later.

CPU=central processing unit

Node (year2) 2006 2008 2010 2012 2014

iPhone performance (CPU mark rating)

1 (base) iPhone 3G

5x iPhone 4

36x iPhone 5

65x iPhone 6

70x iPhone 6s

4867

105

188

300

310

240

180

130

90

0

100

200

300

0

100

200

300

400

R&D cost ($millions)

~6x increase in design cost

16/14nm 22/20nm 32/28nm 45/40nm 65nm

Number of transistors (millions)

# Transistors

Exhibit 6: R&D Cost to Achieve Leaps in Processor Performance Has Increased Sharply

Working Paper 12

THE BOSTON CONSULTING GROUP JULY 2016

Mostofthesenewentrantsinthemobileapplicationprocessorspaceusechip

designslicensedfromARM,anindependentsemiconductordesignhouse:infact,

ARMarchitectureaccountsformorethana90%shareinmobileapplication

processors.ARMregularlyreleasesnewdesignsforcoreprocessingunits(CPUs)at

differentperformancetiers.Similarly,ARMandotherspecialistvendors,suchas

ImaginationTechnologies,alsolicensedesignsforgraphicsprocessingunits(GPUs),

aswellassystemsintellectualproperty(IP).Whilesomeplayersmaychooseto

investsignificantresourcestooptimizeorextendARM’soriginaldesignsforhigher

performanceinspecificareas,othersmaybuildtheirprocessorswithonlyafew

changestothesedesigns,thusminimizingR&Dcostsandtime‐to‐market.

TheHHIshowsthatthemobileapplicationprocessormarketissignificantlyless

concentratedthanothersimilarprocessormarkets,suchasPCorserver.(See

Exhibit7.)

Thecompetitiveintensitytendstorapidlyincreaseinthebasebandmodemsmarket

aseachmobilegenerationmaturesandmorevendorsmasterthetechnologyand

Exhibits - Inside the Smartphone - 2016 07 11 dk (AV edits).pptx 7

Exhibit 7: Comparison of Competitive Intensity Indicators in Processor Markets

Sources: IDC, Gartner, IHS, Nomura, Bernstein, BCG analysis Notes: Herfindal-Hirschman Index calculated with revenue market shares. CPU=central processing unit. GPU=graphics processing unit. 1. Competitors with market share greater than 0.1%. 2. Reflects impact of change in mix due to integration of GPUs into CPUs, and also

supply constraints of leading vendor in 2014-2015. 3. Blended price increase for CPUs for desktop (46%) and notebook (4%) PCs 4. Includes only volume and mid-range servers, not high-end servers (made by PowerPC, Sparc, or Itanium) or mainframes.

39

28

75

91

99Server CPU

PC CPU

GPU

Application Processor

Baseband

Herfindahl-Hirschman Index (%, 2015; 100% = monopoly)

22

38

24

26

75

Change in Average Selling Prices

(% increase, 2008-2015)

Increase in 2008-2015 (%)

45

213

852

1

9

# players in 2015

Entries (exits) since 2008

Number of Competitors1

12

8

2

2

7 (7)

6 (6)

0 (2)

0 (0)

6 recent entries (0) 2

Working Paper 13

THE BOSTON CONSULTING GROUP JULY 2016

erodetheearlyleaders’time‐to‐marketadvantage.Asanillustration,theleading

vendorof3Gbasebandslost28pointsofmarketshare,from56%to28%between

2012and2015.Thetrendseemstobeacceleratingintherecentlyintroduced4G

technology,wheretheshareoftheleadingvendor(thefirstmarketentrant)has

alreadydecreasedfrom90%toapproximately60%inthesameperiod.This

suggeststhattheadvantagefromearlyinnovationisdiminishing.When4Gwas

introduced,thefirstintegrated4G‐3G‐2Gsolutionarrivedinthemarkettenmonths

beforethenextimmediatecompetingsystem.However,forthesecondmajor4G

innovation(CarrierAggregation,supportingamoreefficientuseofspectrumbands)

thistime‐to‐marketgapnarrowedtosixmonths.Andforthenextinnovation

steps—LTECategory6,doublingdownloadspeedsto300megabitspersecond

(Mbps),andCategory9/10,enabling450Mbps—itdecreasedagaintoonly

approximatelythreetofivemonths.

TRANSITIONTOSYSTEM‐ON‐CHIP

Inadditiontomakingitunnecessaryforhandsetmakerstodesigntheirowncustom

processors,merchantprocessorvendorshavealsogreatlysimplifiedtheprocessof

designinghandsetsbycombiningmanypreviouslydiscretecomponentsintoanSoC.

AnSoCisatinybuthighlycomplexchipthatintegratesmanysub‐components,such

astwotoeightCPUs,aGPUwithadvancedgraphicscapabilities,andmultipleother

smallerspecialpurposeco‐processorsthatperformspecificdiscretetasksthatmake

uptheoverallsystem.Forexample,theimageprocessorensuresthatphotosare

processedproperlyandsavedquickly,videoencodinganddecodinghardware

powersthevideorecordingfunctionality,andtheaudioprocessorfreestheCPUs

fromhavingtohandleaudiosignals.

ThekeyadvantageofanSoCisitssize.UsingSoCs,handsetmakerscanput

completecomputersinsmartphonesandtabletsandstillhaveplentyofspacefor

batteries.Additionally,owingtoitsveryhighlevelofintegrationandmuchshorter

wiring,anSoCusesconsiderablylesspower,whichisabigadvantageformobile

Working Paper 14

THE BOSTON CONSULTING GROUP JULY 2016

computing.CuttingdownonthenumberofphysicalchipsmeansthatSoCdesigns

usuallyhavelowercostsandhigherreliabilitythanthemulti‐chipsystemsthatthey

replace.And,withfewerpackagesinthesystem,assemblycostsarereducedaswell.

Furthermore,merchantprocessorvendorshavegoneastepfurtherandexpanded

theirofferingtoinclude“referencedesigns,”afulldeviceblueprintthatincludes

devicedriversandalistofcompatiblehardware.

SoCsandreferencedesignshavefacilitatedmarketentryfornewhandsetmakersby

enablingthemtoproduceahandseteveniftheylackcapabilitiesinelectronic

designandassembly.ThetransitiontoSoChasallowedhandsetmakerstobringa

newdevicetomarketinone‐thirdthetime,usingone‐tenththenumberof

engineers,andatabout3%ofthecost.

AVAILABILITYOFINDEPENDENTSMARTPHONEOPERATINGSYSTEMS

Adecadeago,fourfenced‐inoperatingsystemscompetedinmobile.Eachwasa

proprietarysystemcreatedbyanincumbenthandsetmaker(forexample,HPor

RIM)or,inthecaseofSymbian,aconsortiumofasmallnumberofhandsetmakers

ledbyNokia.Today,GoogleandMicrosoftoffersmartphoneoperatingsystemsthat

handsetmakerscanlicenseatminimalornocost.Consequently,smartphone

makerscanenterthemarketwithouthavingtoinvestindevelopingtheirownOS

andorchestratinganewecosystemofapplicationdevelopers.

Eighty‐fourpercentofsmartphonessoldworldwidein2015usedGoogle’sAndroid

OS.Androidprovideshandsetmakerswithaready‐made,low‐cost,and

customizableOSthathasalargeinstalledbaseofusersandanecosystemof1.8

millionapps.SmartphonemakerscanuseAndroidasis(includingallGoogle

services)ormodifyittovaryingdegrees.Somehandsetmakersonlymakeminimal

changestoAndroid’slookandfeel,whileothers,suchasXiaomiandAmazon,have

mademorefundamentalchangestocustomizetheiruserexperienceandcreate

theirownapplicationecosystem.Theoptionshaverecentlyexpanded,asnew

independentvendors,suchasCyanogen,haveemergedtoofferanalternativeopen‐

Working Paper 15

THE BOSTON CONSULTING GROUP JULY 2016

sourceOSbasedontheAndroidplatform.Itisestimatedthatapproximately30%of

totalAndroiddevicesin2015usedasignificantlymodifiedversionoftheAndroid

OS(knownasa“forked”version)notdirectlycontrolledbyGoogle.

UNIFIEDGLOBALMOBILECOMMUNICATIONSSTANDARDS

Intheearly2000s,thereweremultiplewirelessstandardsthatvariedbyregion.

Sevenstandardsexistedforfirst‐generation(1G)technologyandfivefor2G.While

GSMdominatedinEuropeandAfrica,theanalogstandardAMPSco‐existedinNorth

AmericaandLatinAmericawithmultipledigitalstandards(CDMA,TDMA/D‐AMPS,

andGSM).NostandardwasprevalentintheAsia‐Pacificregion.Asaresult,network

equipmentandhandsetmakerswereforcedtoproducemultipleversionsofthe

sameproducts,evenwithinoneregion.Theearlynetworksanddeviceswerenot

trulyglobalorinteroperable.

Asdescribedinourpreviousreport,TheMobileRevolution:HowMobileTechnologies

DriveaTrillion‐DollarImpact,eachgenerationofwirelesscellulartechnologies

takesbetweenfiveto15yearstodevelopininternationalstandards‐settingbodies,

withthecomplexityoffunctionalityandinteroperabilityrequirementsdramatically

increasingforeachnewgeneration.Duringthedevelopmentof3Gtechnologies,

industryparticipantsconvergeduponthecommontechnologysolutionsthatnow

formthewell‐knownandwidelyadopted3Gstandards:UMTSwasusedmost

extensively,whileCDMA2000wasusedbysomeoperatorsinNorthAmericaand

SouthKorea,andTD‐SCDMAwasusedonlyinChina.Apartfrominteroperability,3G

offeredsignificantperformanceimprovementscomparedwith2G/2.5G:between

threeand17timesfasterdownloadspeeds—upto384kilobitspersecond(kbps)

formobileusersand2Mbpsforstationaryusers)—anda95%reductionincostper

megabytetransmitted.

Today’swidelyadopted4Gstandard,LTEanditsevolution,LTEAdvanced,hasalso

enabledaleapinperformance:enhancedvoicequality(HDVoice)andfiveto150

timesfastertransmissionspeedsrelativeto3G/3.5G(upto450/50MbpswithLTE

Working Paper 16

THE BOSTON CONSULTING GROUP JULY 2016

Category9/10),whilethecostpermegabytehasdecreasedby67%.Infact,withthe

buildoutof4Gnetworks,Ciscoestimatesthattheaverageglobalnetwork

connectionspeedwillincreaseatacompoundannualgrowthrateofalmost50%,

takingtheaveragespeedfrom512kbpsin2012tomorethan3.9Mbpsby2017.

LTEprovidessupportforinter‐operationwithbothGSM/UMTSnetworksand

CDMA2000networks,whichmakesLTEasinglecommonglobal4Gstandard.

Althoughtherearetwovariantsofmobiledatatransmissiontechnologiesthatfall

undertheinternationalstandardofLTE—LTE‐TDDandLTE‐FDD—theyhave90%

oftheircoretechnologyincommon.

Byestablishingcommonglobaltechnologystandards,theindustryhasreduced

investmentriskandloweredbarrierstoentryforallplayersacrossthemobilevalue

chain.Companiesthatholdpatentsontheunderlyingglobalstandardsagreeto

openlylicensethistechnologyonfairandreasonabletermstomanufacturersof

standardscompliantproducts.Thisallowshandsetmakerstodevelopglobally

compatibledevicesthatcanworkwithmobilenetworksanywhere.Indeed,

accordingtodatafromIDC,in2015(approximatelyfiveyearsafterthestartofthe

roll‐outofthefirstLTEnetworksworldwide)therewere106makersof4G‐capable

handsets,almostdoublethenumberof3Ghandsetmakersin2007.

LookingAhead

With4Gpenetrationof14%globallyattheendof2015,andlessthan5%in

emergingmarkets,thereisstillampleroomfortheMobileRevolutiontomagnifyits

alreadytremendousimpact.However,inthecontextoflowbarrierstoentryand

expandedconsumerchoice,handsetmakerswillcontinuetofinditchallengingto

differentiatetheirproducts.Criticaltechnologycomponentsarenowavailablefrom

multiplemerchantvendors,anditisincreasinglyeasierforhandsetmakersto

integratethesecomponentsthankstotheSoCarchitectureandreferencedesigns.

Working Paper 17

THE BOSTON CONSULTING GROUP JULY 2016

Inordertoearnsustainableprofitmargins,handsetmakersmustconsidernew

sourcesofdifferentiationandcompetitiveadvantage.Thefast‐growingrecent

entrants,manyfromemergingmarkets,arealreadypioneeringnewcompetitive

approaches.Theseapproachesinclude:

reachingoptimalscalethroughglobalmarketpenetration

maximizingR&Dandsupplychainefficiencybysystematicallyapplyingdesign‐

to‐valueanddesign‐to‐costapproaches

pursuingcontinuous,rapidinnovationthatpreservesatime‐to‐market

advantagebyprovidingaconstantflowofnewvaluablefeatures

buildingstrongbrandsandadvocacythroughdirectengagementswith

consumers,leveragingdigitalmarketingandanalytics

developingnewrevenuestreamsinancillaryproducts,softwareadd‐ons,and

services

Atthesametime,mobilevaluechainplayerscanpursueopportunitiesinpromising

newmarkets.ThemostimportantopportunitiesrelatetotheInternetofThings.

Mobiletechnologyprovidesthefabricforthisnextbigwaveofinnovation,whichis

expectedtogeneratemorethan$250billioninannualrevenuesby2020.Awide

rangeofnewdevicesandapplicationssuchaswearables,drones,self‐drivingcars,

andsmartcitiesrequirethesamecomponentsusedinmobilehandsets.

Toensurethatthenextwaveofinnovationfulfillsitspromisetogenerateeconomic

growthandconsumervalue,policymakersaroundtheworldneedtoconsider

policiesandinitiativesthatnotonlystimulateend‐useradoptionofmobileservices

intheshortandmediumterms,butalsocontinuetopromotemarket‐driven

innovationandcompetitionacrossthemobilevaluechain.

AntonioVarasDavidC.MichaelDerekKennedyFrançoisSchaus

Working Paper 18

THE BOSTON CONSULTING GROUP JULY 2016

AntonioVarasisapartnerandmanagingdirectorintheSanFranciscoofficeofThe

BostonConsultingGroup.

DavidC.Michaelisasenioradvisorandformerseniorpartnerandmanaging

directorinthefirm’sSanFranciscooffice.

DerekKennedyisapartnerandmanagingdirectorinBCG’sSanFranciscooffice

andGlobalLeadoftheTechnologySectorpractice.

FrançoisSchausisaprojectleaderinthefirm’sSanFranciscooffice.

Youmaycontacttheauthorsbye‐mailat:[email protected]