Embed Size (px)

Citation preview

The modern Australian Metro Market Contemporary ingredients for success

METRO OFFICE

First Half 2016Australia

Research and Forecast Report

Accelerating success.

Luke Dixon Associate Director | Research+61 417 118 [email protected]

Want better insights, faster? Talk to a Colliers Edge expert today.

colliers.com.au/colliersedge

Want real time data that matters most to your business? Colliers Edge is a subscription service developed by our in-house property research specialists, drawing on the expertise of our national network of operators.

We provide clients with a quarterly series of real estate data, collected in a consistent and timely manner to ensure the highest standard of quality.

Colliers Edge has the longest data time series for office, industrial and retail markets across all major Australian cities. Updated quarterly, Colliers Edge is an all-encompassing data analytics tool that can help your business make informed decisions.

HOTELS

Second Half 2015Australia

Research and Forecast Report

Accelerating success.

Destination Australia Arrivals increase as accommodation sector takes off

Improve your perspective. We have. Property Research worth talking about. www.colliers.com.au/subscribe

Metro OfficeMETRO OFFICE

Investment tide continues 5

Our perspective - metro office 10

Sydney 12

Melbourne 18

Brisbane 24

Adelaide 27

Perth 29

Newcastle 33

Gold Coast 36

Our experience - metro office 38

Contents

How else can we help you?

Speak to one of our property experts today.

Partner with our Research and Consultancy team

Our highly experienced team of professionals can partner with you to ensure your next project has a positive outcome. We deliver strategic advice across a full range of property sectors, ensuring that your decisions are fully informed.

For more information about Colliers International

and working with us visit:

www.colliers.com.au

3Metro Office | Research & Forecast Report | First Half 2016

Louisa Lawson Building, 25 Colishaw Street, Canberra ACTSold on behalf of GDC (ACT) Pty Ltd

4 A Colliers International publication

Metro OfficeMETRO OFFICE

Creating Metro AppealPerhaps the best way to describe Australia’s metro office markets is “mixed”. There is no real “national metro market” due to the multitude of factors that have an impact in this sector and the variation of conditions across states. However there are some common themes that emerge when discussing the current state of metro markets together with factors that can potentially make certain markets more appealing over others in a commercial sense. By Daniel Lees Associate Director | Research [email protected] The merits of centralisationPost the Global Financial Crisis when vacancy and incentive levels increased across Australian CBDs, the competitive rents on offer provided tenants with the opportunity to centralise. The scenario brought with it some opportunities, with tenants in most cases having improved access to amenity, transport infrastructure, and potentially becoming more appealing to a wider pool of labour.

Today, a case remains for centralisation because much of the commercial supply pipeline being built is concentrated within core CBD precincts, particularly in Sydney and Melbourne. The incentives on offer in these CBDs are edging lower slowly but in some cases are still high enough to entice tenants away from metro alternatives.

Even so, many metro markets, especially within the inner and fringe areas of Melbourne and Sydney remain quite tight for a number of reasons. Firstly, there has been a significant amount of withdrawal for infrastructure, and many assets acquired in prior years for development are being sold as residential or other higher and best use purposes. Secondly, the supply pipeline is fairly limited in metro markets with new construction being concentrated in CBDs. Finally, it’s not only the metro markets experiencing a loss of secondary stock. Withdrawals have also been widespread in CBDs, placing pressure on secondary grade tenants to find new locations, and in some cases this may lead to an element of decentralisation over time.

Proximity to the CBDWhilst metropolitan locations can sometimes offer lifestyle upside to tenants, being close to the CBD remains an important tenant consideration due the close proximity of business and financial services, public and private clients, suppliers, financiers and key decision makers. From a talent retention and attraction perspective, CBD proximity allows tenants to access a wider pool of recruits due to the central location of the business. In terms of cost management, tenants can enjoy the amenity advantages of a CBD adjacent location at a lower rental cost. From an investment perspective, there tends to be higher levels of domestic institutional and offshore investment given the dynamics of fringe markets tend to be similar in nature to the CBD and enjoy easier access to transport services.

5Metro Office | Research & Forecast Report | First Half 2016

Transport infrastructureClose proximity to public transport networks, roads and taxis is consistently ranked as a top requirement by tenants and building owners in metropolitan locations. While road transport and car parking in metropolitan markets are often cited as a necessity to ensure tenants can readily access their office location, public transport access in the form of bus and rail are becoming increasingly important.

Transport accessibility works as a driver when:

• Well connected to arterial road, and freeway networks. Travel times to CBD locations under 30 minutes will be most positive for tenant accessibility;

• Close proximity to airports and other intermodal hubs. Where trucks, or other large vehicles can access locations will enable a wider use and expand the tenant mix;

• Public transport access to rail, tram, bus or taxis is within a 100-500 metre walk of the office site, at multiple times.

Examples of infrastructure development that will enhance the appeal of metro markets include;

• Sydney Metro: The Northwest component of the project is scheduled for completion in 2019. This will feature a metro rail system that will deliver eight new railway stations with trains running every four minutes in peak times. The infrastructure will improve the access and employee catchment for the North Western precincts of Sydney such as Macquarie Park.

• Perth City Link: A master plan designed to reconnect the Perth CBD with the Northbridge and beyond to West Perth. In 2013 the $360 million rail component of the project was delivered, and the second stage involving an underground bus station is scheduled for delivery this year. Once the bus station is completed and is delivered, accessibility between Northbridge and the CBD will improve and should start generating more interest from tenants to move to the Northbridge precinct.

AmenityAmenity covers services available in buildings where the cost of building such services is typically borne by landlords as an

25 Montpelier Road, Bowen Hills, QLD Leased on behalf of GWC Property

6 A Colliers International publication

Metro OfficeMETRO OFFICE

incentive or attraction for prospective tenants. It also covers local attractions that are available to the building’s workforce. Based on tenant surveys, amenity services in high demand include; end of trip facilities, bike parking, private lockers, meeting rooms on demand and client conference areas. However the location of a metro precinct will also heavily dictate the level of amenity on offer to tenants. Employees prefer to work in areas that have access to a variety of different food and beverage options, childcare centres, gyms, banking and medical services together with a compelling retail offering. It’s important to note that while relocating businesses to outer metro locations can reduce rental expenses, it can also adversely impact employee sentiment and result in increased staff churn and subsequent recruitment costs. In Sydney examples of metro markets with strong amenity include North Sydney and Parramatta, while Sydney Olympic Park has a less favourable offering. In Melbourne, the east City Fringe and Inner East markets are experiencing very strong demand due to the local amenity that suburbs within these precincts offer, while the Outer East still has issues when it comes to appropriate amenity for office workers, and demand is suffering as a result.

Stock withdrawal and preserving the commercial environmentA combination of record low interest rates and insufficient housing stock has led to prolific expansion of residential development as supply scrambles to catch up with demand. As such, the highest and best use of sites has in many cases rotated from commercial to residential and stock within both CBD and metro markets is being withdrawn for conversion. In Sydney, the withdrawals have been widespread although the effects are perhaps most noticeable in markets such as St Leonards, Chatswood and to a certain extent North Sydney. Likewise in Melbourne, St Kilda Rd has witnessed withdrawal for residential purposes. While the increase in housing supply is in most cases welcome, the impact can be detrimental as a precinct begins to lose its commercial look and feel. With little in the way of new supply coming on line in metro precincts, the growth of residential has the potential to steadily erode the commercial core. This dynamic is challenging for local councils who are under pressure from developers to make way for new projects

81-85 Flushcombe Road, Blacktown NSWValued on behalf of Denison Funds Management

7Metro Office | Research & Forecast Report | First Half 2016

Infrastructure InvestmentMetropolitan office markets across Australia will be transformed over the next decade as considerable infrastructure investment occurs along the eastern seaboard. Currently, New South Wales appears to be the hub of infrastructure activity with projects such as Sydney Metro, WestConnex, and the anticipated Parramatta Light Rail expected to open during this period. Our house view is that improved infrastructure will enable greater connectivity across metro markets, and enhance the appeal of metro accommodation to a broader tenant base.

Consequently, Sydney has been the focus of our attention this past year and has presented opportunities with compelling value.

PlanningUrban planning will continue to present prospects for superior performance with several large-scale urban renewal projects to take place over the long-term. In late 2015, Centuria, as co-tenderer with Mirvac, acquired assets within Australian Technology Park. This 14 hectare site, just three kilometres from the Sydney CBD, will be the site of a $1 billion development for CBA and will drastically impact the broader Central-to-Eveleigh corridor.

Stock WithdrawalGiven the significant amount of office stock being withdrawn across the Sydney CBD and various metro markets, we believe established markets will be supported by reduced vacancy and above average rental growth over the short to medium-term. In the case of the North Shore office markets, this trend will be further reinforced by a limited development pipeline for the foreseeable future.

Rise of the Secondary MarketIn particular, we believe that stock withdrawals will be particularly favourable to owners of secondary office buildings. This is due to the fact that stock withdrawals have primarily been focused on this segment of the market, while nearly all of the future supply being developed is prime grade stock. This dynamic will have a powerful effect by markedly reducing the supply in the secondary market and increasing the number of displaced tenants seeking space. As a result, we anticipate B Grade buildings in select metro markets will face an exciting period with potentially robust rental growth.

Jason HuljichCEO, Unlisted Property FundsCenturia

Centuria commentary

however the impact of residential growth can be mitigated. For example in Sydney, markets of North Sydney and Macquarie Park have attempted to ring-fence the commercial core to preserve its identity, ensuring that amenity used to attract key tenants is retained.

Investment opportunities While domestic institutions are the overwhelming weight behind CBD office investment, metro markets are characterised by higher levels of private investor activity. Generally speaking, offshore investors are less active in the metro space due to the more complex set of drivers that can vary from market to market. It’s very hard to simply group all metro markets together and carry out analysis that would apply to all tenants in all precincts. For this reason investment activity is prevalent amongst smaller fund managers, high net worth private investors and a limited amount of offshore activity. We note however that as yields continue to compress in CBD markets, institutions and offshore investors may be forced to look outside of the CBD to boost yields by moving further up the risk curve. Still, the challenge of deploying large amounts of capital over a small number of transactions remains. For example, in the second half of 2015 average transaction amounts across Australian metro markets were ~$44 million in the second half of 2015 compared to CBD transactions which averaged ~$115 million over the same period.

146 Arthur Street, North Sydney NSWManaged by Colliers International

8 A Colliers International publication

Metro OfficeMETRO OFFICE

Foreign & domestic investor demand remains highAs a specialist, opportunistic property investor, we like Australia’s safe-haven status within the wider Asian market. Our investors who are typically large offshore pension funds and insurance companies are drawn to Australia’s strong economic fundamentals and transparent regulatory environment compared to some of our Asian counterparts.

Currently, metro office is a key sector focus for Forum Partners in Australia, obviously yielding higher than core CBD property, though moreover benefits from lower entry cost and greater turn around asset management expertise, such as intense leasing campaigns and capital expenditure strategies. Additionally, less vacancy risk exists as a result of lower stock introduction and higher withdrawals to residential than many CBD markets.

From a local capital markets perspective, the metro office sector has proven itself attractive both to private equity investors, like Forum and more recently to listed markets, evidenced by quality product and yield offerings, such as Centuria Metropolitan REIT. This is an important step for the evolution of the sector previously dominated by small syndicators and unlisted retail trusts that struggled with liquidity.

Evolving metro landscapeObvious metro markets with high demand, ongoing growth prospects and low vacancy are St Kilda Road, Melbourne and North Sydney just outside the Sydney CBD. Looking further afield, as a result of changing infrastructure, markets like Parramatta, 25 kilometres north-west of Sydney’s CBD will benefit from the further decentralisation of the CBD core office market, as we’ve seen in Macquarie Park, North Ryde. The same theory applies for Box Hill in Melbourne and Mount Gravatt in Brisbane.

The game changer could be major infrastructure developments like Sydney’s new airport at Badgerys Creek, having the potential to shift the demand for all types of property, especially metro office space, further west than ever before, thus dragging the geographic centre of Sydney further west.

The Sydney metropolitan office market is in an exciting phase. The current NSW Government infrastructure spending initiatives to increase density, development and employment areas primarily centered around transport hubs reflects the progressive nature of the state government to realign the workforce closer to home.

This shift is especially evident within the government where they continue to transition towards Parramatta and other western metropolitan markets, providing workspace that is closer to home for the western labor force.

Correspondingly, Propertylink expects that tenant demand for metropolitan office locations will continue to strengthen as the Sydney CBD vacancy tightens, tenants will be looking for cost effective solutions in the suburbs that also offer large floor plates and reasonable car parking ratios.

A further contributing factor to the demand equation in Sydney is the withdrawal of stock for alternative uses such as residential and also the compulsory acquisitions being conducted for the new metro rail line, however a negative net supply situation is anticipated for some time to come. This will accordingly lead to lower vacancy rates and competition amongst tenants for space.

The net loss of stock within the Sydney market compounded by the already low vacancy rates across all commercial grades, now provides strong parameters for effective rental growth and improved returns for owners. In an environment of historically low cap rates. Effective rental growth is the key to driving returns. Furthermore there will continue to be examples of additional upside as a result of conversions from commercial use to alternate uses.

The above factors all compound and point to a positive outlook for metro office market and as such Propertylink’s recent $94m acquisition of 4 buildings in North Ryde is a show of our confidence in the metro office markets. The recently created Propertylink Office Partnership III is seeking additional acquisitions in this market and will look to capitalise on the positive outlook.

Andrew FaulkManaging Director, Forum Partners Australia

Peter McDonaldExecutive Director and Head of Property, Propertylink

Forum commentary

Propertylink commentary

9Metro Office | Research & Forecast Report | First Half 2016

METRO OFFICE STOCK BEING ERODED BY RESIDENTIAL AND INFRASTRUCTURE WITHDRAWALS

PRIVATE INVESTORS ACCOUNT FOR 29% OF TRANSACTION VOLUME IN DOLLAR TERMS AND 47% OF OVERALL TRANSACTIONS

DOMESTIC INVESTORS DOMINATE METRO ACQUISITION

AVERAGE TRASACTION SIZES ARE FAR HIGHER IN CBD MARKETS

Number of Metro transactions Volume of transactions

OFFSHORE ACTIVITY REMAINS HIGH ON AN ABSOLUTE LEVEL

OffshoreDomestic

2013

55% 45%

2015

63% 31%

2014

60% 40%

2012

$670 MILLION

$1.67 BILLION

$2.72 BILLION

$1.83 BILLION

20142013 2015

Accelerating success.

How else can we help you?Speak to one of our property experts [email protected]

For more information about Colliers Internationaland working with us visit:www.colliers.com.au

Our perspective METRO OFFICE AUSTRALIAFIRST HALF 2016

CORPORATE DEVELOPMENT GOVERNMENT

PRIVATEINSTITUTION OTHER

CBD

$115.06 million

$43.65 million

METRO

$450 million

21

140

25

236

2

82

$7.1 billion

$1.28 billion

$4.34 billion

$60 million

$1.54 billion

7.34 million m²Jan-15

Jul-15

Jan-16

7.33 million m²

7.29 million m²

METRO OFFICE STOCK BEING ERODED BY RESIDENTIAL AND INFRASTRUCTURE WITHDRAWALS

PRIVATE INVESTORS ACCOUNT FOR 29% OF TRANSACTION VOLUME IN DOLLAR TERMS AND 47% OF OVERALL TRANSACTIONS

DOMESTIC INVESTORS DOMINATE METRO ACQUISITION

AVERAGE TRASACTION SIZES ARE FAR HIGHER IN CBD MARKETS

Number of Metro transactions Volume of transactions

OFFSHORE ACTIVITY REMAINS HIGH ON AN ABSOLUTE LEVEL

OffshoreDomestic

2013

55% 45%

2015

63% 31%

2014

60% 40%

2012

$670 MILLION

$1.67 BILLION

$2.72 BILLION

$1.83 BILLION

20142013 2015

Accelerating success.

How else can we help you?Speak to one of our property experts [email protected]

For more information about Colliers Internationaland working with us visit:www.colliers.com.au

Our perspective METRO OFFICE AUSTRALIAFIRST HALF 2016

CORPORATE DEVELOPMENT GOVERNMENT

PRIVATEINSTITUTION OTHER

CBD

$115.06 million

$43.65 million

METRO

$450 million

21

140

25

236

2

82

$7.1 billion

$1.28 billion

$4.34 billion

$60 million

$1.54 billion

7.34 million m²Jan-15

Jul-15

Jan-16

7.33 million m²

7.29 million m²

By Sas Liyanage Research Analyst | Research [email protected] The Sydney metro markets are embracing a long awaited evolution, underpinned by a historically high infrastructure spend and a state economy that remains the envy of the nation. Indeed, employment growth in Sydney has been staggering with the most recent state budget revealing a $2.1 billion surplus with over $68.6 billion of infrastructure spending over four years.

Vacancy rates in metro markets have continued their downward motion, driven by a lacklustre supply and a significant withdrawal of stock. In recent years, the omnipotent demand for residential developments has led to withdrawal of underperforming assets for conversion. The forthcoming Sydney Metro rail network project will amplify these effects as it triggers a new flurry of activity, with secondary assets set to face wrecking ball to make way for the proposed stations.

SYDNEY METRO OFFICE SPACE INDICATORS

0%

2%

4%

6%

8%

10%

12%

14%

-50000

-30000

-10000

10000

30000

50000

70000

90000

110000

130000

Jan-07 Jul-07 Jan-08 Jul-08 Jan-09 Jul-09 Jan-10 Jul-10 Jan-11 Jul-11 Jan-12 Jul-12 Jan-13 Jul-13 Jan-14 Jul-14 Jan-15 Jul-15 Jan-16

Met

ro M

arke

t Ave

rage

Vac

ancy

(%)

Floo

rspa

ce (

sqm

)

Net Supply Net Aborption Vacancy (RHS)

Source: PCA OMR Jan-16/Colliers Edge

SYDNEY METRO OFFICEThe new frontier for Sydney metro

First Half 2016

Research and Forecast Report

22 Lambs Road, Artarmon Project managed on behalf of Bard Medical

SYDNEY METROPOLITAN A GRADE OFFICE MARKET

MARKET AVERAGE NET FACE RENTS ($/m² pa)

AVERAGE INCENTIVES

AVERAGE MARKET YIELD

REGION H1 2016 H2 2016 H1 2016 H2 2016 H1 2016 H2 2016

North Sydney $600 28% 6.75%St Leonards/ Crows Nest $455 28% 7.38%

Chatswood $480 25% 7.75%North Ryde/Macquarie Park $323 30% 7.13%

Parramatta $445 18% 7.38%Sydney Olympic Park/Homebush Bay

$363 28% 7.63%

Rhodes $380 26% 7.75%

Norwest $355 23% 8.50%

South Sydney $375 18% 7.25%

Sydney CBD Fringe $545 24% 6.25%

Note: Figures represent market averages at 1 March 2016Figures relate to existing A Grade floorspace, not newly built floorspaceSource: Colliers Edge

COLLIERS INTERNATIONAL RESEARCH FORECASTS

12 A Colliers International publication

Metro OfficeMETRO OFFICE

SYDNEY METRO OFFICE VACANCY

0% 5% 10% 15% 20%

North Sydney

St Leonards

Chatswood

Macquarie Park

Parramatta

Jan-16 Jul-10

Source: PCA OMR Jan-16/Colliers Edge

These withdrawals have undoubtedly increased leasing activity, as tenants are forced back into the market to vie over an ever diminishing vacant space. However, in certain markets, the sheer scale of withdrawals are now at risk of undermining their commercial culture. Councils presiding over these markets continue the acrimonious debate over the quantum and location of residential developments amongst the commercial precincts. Markets like St Leonards, grappled by 3 councils, will be challenged to reverse course as it snowballs towards a residential precinct. The market’s viability as a commercial hub is contingent on the councils’ ability to work in concert on an effective, well-planned, activation precinct. By contrast, markets like North Sydney, North Ryde and Parramatta with the luxury of scale, have protected their commercial core from encroaching residential uses.

Above all, the market will benefit from infrastructure. Long-term funding for these multi-year programs to rebuild the metro landscape has never been more powerful. Over 33 buildings in the metro markets will be compulsory acquired for the aforementioned Metro Rail project. With major construction scheduled to commence in 2017, a large number of commercial properties have received vacant possession notices. These withdrawals, all involving secondary grade assets, will have implications for this tightly held market as displaced tenants look to secure space. Now, for the first time since the GFC, these markets have a platform to emerge from a period of mediocre rental growth. As the competition for scarce secondary space intensifies, secondary grade assets are likely to experience a decline in vacancy and, in turn, incentives offered.

Although investment volumes were below those in 2014, they were above the high levels witnessed in 2007. Symptomatic of the scarcity of stock on market, and sustained competition, transactional yields continued to decline. As such, average yields on Metro assets transacted in the Sydney markets reached their lowest level since 2007, falling to 7.49 per cent. Unlike the significant participation by offshore investors witnessed in 2014, investment from offshore buyers was largely restricted to North Sydney market, which accounted for 59 per cent of the overseas based transaction volumes in 2015.

Looking forward, the significant infrastructure development will ease trepidations for the longer term investor. Public transportation fears that stalked the metro market are finally being addressed. Most significantly, there will be access to a larger working population. This will be achieved directly through an increased population from the induced residential development, and indirectly through the shorter travel times to other regions. Given comparatively higher yield offer, a at lower price point, metro assets will continue to lure investment while providing a shelter for capital.

North SydneyNorth Sydney is on the forefront of this transition, with significant investment activity underscored by the implicit uplift in infrastructure and leasing conditions. In the last year, over 48,000sqm was withdrawn from the market. Indeed much of this was for the residential conversation, with over 1,700 units and 57,000sqm of residential floorspace in the current pipeline. These withdrawals, though, were restricted to market fringe, with the commercial core ring-fenced by defensive zoning.

An additional five buildings amounting to 19,223sqm will be withdrawn for the proposed Victoria Cross Metro line station. This will impose further pressure on a historically tight secondary market, with the secondary grade vacancy currently at its lowest level since the peak of the GFC. The B Grade market in particular is expected to experience the greatest tightening as displaced

33 Berry Street, North Sydney Sold by Colliers International

13Metro Office | Research & Forecast Report | First Half 2016

tenants scramble to secure deals. This demand is exemplified by the fall in incentives given to smaller sized leases, with incentives dropping from 30 per cent to 25-27 per cent. The North Sydney secondary market now has the tailwinds for effective rental growth, which has hitherto been benign. The market remains a recipient of tenants looking to centralise. Major leases of this nature recently signed include Jacobs, Beam Suntory and Vodafone, totalling to over 17,151sqm of floorspace. Moreover, the quantum of space leased in the second half of 2015 was 74 per cent higher than the first half of the year and 28 per cent higher the corresponding period in 2014.

Similarly, development activity is now gathering pace. 177 Pacific Highway will be the first new development to the market in six years and scheduled for completion in the third quarter this year. It is now all but fully let. Building on this momentum, Dexus Property Group (DEXUS) and DEXUS Wholesale Property Fund (DWPF) has activated the 41,163sqm premium development at 100 Mount Street after acquiring it in February. With construction programmed to commence in the middle of the year, vacant notices have been handed to occupiers, placing more tenants back into market. Finally, it is understood Charter Hall has entered into discussions for North Sydney’s last remaining major mooted development, 1 Denision. If successful, the development will likely include the shopping centre on Berry Street, and expand beyond the proposed 40,000sqm tower.

Investment activity continued at high levels, with over $301 million of sales occurring the second half of the year. Although 26 per cent below the corresponding period in the previous year, the average transaction value was at a 23 per cent premium. North Sydney remains a beneficiary of foreign interest, with 70 per cent of sales volume in the second half of 2015 originating from China. Sales growth is expected to continue with transaction volumes and average values in the current half-year already exceeding those in the previous 4 periods. In addition to the aforementioned Dexus acquisition of 100 Mount Street for $41 million, Ascendas purchased the Innovation Centre on Arthur Street for $315 million at a yield of 6.2 per cent.

St Leonards/ Crows Nest The St Leonards market vacancy has fallen to its lowest level since July 2008, ending at 8.5 per cent. This fall was predicated by an anaemic supply and withdrawals for conversation. This lack of supply lies subordinate to ongoing demand for residential developments. Notwithstanding this, the second half of 2015 was the first positive half-year net absorption since 2012. The market has recently undergone significant rezoning, with over 6,279 units or 108,716sqm of residential floorspace in the pipeline. Meanwhile, the commercial leases signed in the second half the year was 58 per cent below the first half of the year and 63.5 per cent under the same period the previous year. But despite this, positives lie

ahead. The leasing market will benefit from the withdrawal of 9,791sqm of space for the Crows Nest Metro line station. And once the large supply of residential developments are completed, the commercial developments will likely benefit from immediate proximity to a larger working population. The market, moreover, will receive an uplift from the major developments; Gore Hill and 88 Christie Street. The developments will provide 46,000sqm and 28,000sqm of floorspace respectively. Furthermore, the market will also benefit from the extensive expansion of NSW health infrastructure, with an additional 40,000sqm to be provided. In the interim, however, the leasing market will encounter challenges with several small tenants pushed out to the North Sydney and North Ryde markets.

Sales volumes in 2015, somewhat disconnected from leasing movements, were the highest ever recorded. There were over $424 million worth of sales in 2015, 62 per cent above the previous record high levels seen in 2014. This was driven by acquisition of 203 Pacific Highway by Centuria Capital Ltd and Centuria Metropolitan for $86 million, at a yield of eight per cent. Although investment interest will continue moving forward, volumes will likely be curtailed by the availability of stock.

ChatswoodChatswood much like St Leonards will be challenged by the competing forces posed by residential developments. The overall vacancy rate climbed in the 6 months to January 2016, increasing from 6.8 per cent to 7.7 per cent. Some larger deals signed recently will reverse this upward leg in vacancy, though. In a strong start to this period, in excess of 4,493sqm of leases are

181 Miller Street, North SydneyLeased on behalf of Local Government Superannuation Scheme

14 A Colliers International publication

Metro OfficeMETRO OFFICE

to commence in the first half of the year. Indeed, demand will remain relatively stable given its quality in the retail amenity and strong transportation links. Chatswood’s main attraction will be its relatively lower price offer compared to North Sydney. In the near term, the market will continue to tighten with no commercial developments in the pipeline and lease lengths tied up existing stock. Chatswood is likely to have reached its peak commercial office development capacity. Meanwhile, investment activity in the market has been subdued. The Zenith still remains on the market, after being brought to the market in the first half of 2015.

Macquarie ParkThe Macquarie Park market has continued on its progression towards a dominant office precinct. Buoyed by scale and a healthy supply, the market has experienced over 43,896sqm of net absorption in the 18 months to January 2016. Macquarie Park has run a course contrary to the other markets, with stock expanding steadily, while others contracted. In the past 36 months Macquarie Park’s stock grew by six per cent. By contrast, in the same period, the average metro market contracted by 13 per cent. Despite this significant supply of over 84,529sqm since July 2013, the vacancy rate declined from 9.5 per cent to 8.2 per cent. Additionally, the market will be the beneficiary on infrastructure investment. Macquarie Park will accommodate both the Sydney Metro line project as well as the Northwest Rapid Transit project. Once complete, Macquarie Park will receive trains every four minutes at peak times, substantially quicker than a train every 15 minutes seen presently.

Leasing activity has continued to grow since the first half of 2015. The volume of spaces leased was in the six months January 2016 was 55 per cent percent higher than the corresponding period in 2014. The $48 million in sales volume witnessed in the second half of 2015 was 31 per cent above that in the preceding

6 months, but 65 per cent below that in same period in 2014. Volumes in this half have already exceeded those in corresponding half last year. This was largely a result of the Propertylink and Grosveners acquisition of 4 buildings from Blackstone. The assets, valued at $94 million, will be placed into a new fund; Propertylink Office Partnership 3.

ParramattaAs the political spectre surrounding Parramatta and its prospects as Sydney’s second CBD settles, the material advantages of a substantial infrastructure spend is now emerging in the investment and leasing indicators. Despite CBA’s announcement to vacate 40,000sqm of floorspace, tenant demand has remained robust. Leasing demand was largely driven by the education sector and businesses priced out of the CBD and fringe markets. Meanwhile, average yields have progressed in downward fashion. In the 6 months to January, B grade yields compressed by 25 basis points, declining from 8.00 to 7.75 per cent. Investment demand remained in the hand local buyers; syndicates and wealthy privates. Indeed, sales in the last 2 years have only been B grade assets. However now, for the first time since 2012, 18 Smith Street will be the first sub $100 million building brought to market.

Parramatta has experienced a mediocre level of commercial supply, with the current stock levels akin to those at the beginning of 2010. In recent years, the demand for residential developments has led to a withdrawal fringe assets for conversion. Presently over 3700 apartments are mooted or under construction. Given the complexity in satisfying the pre-commitment requirements, the pressure for residential developments will continue in the near term. As such, the commercial supply remains restricted. Nevertheless, the increased tenant demand is now beginning to trigger mooted developments. 89 George Street, 169 Macquarie Street, and 105 Phillip Street will now commence having secured pre-commitments. At 105 Phillip Street, it is understood that HoA were reached with GPNSW for the 25,000sqm development, programmed for completion in March 2018.

There however remains a shortage of large contiguous space. This was exemplified in the 6,300sqm lease at 126 Church Street to Parramatta Council, which attracted a low incentive of 8.33 per cent. Similarly, this lack of larger floor plates has pushed Office of State Revenue (OSR) to look in building a new development at 12 George Street Parramatta, on the Justice Precinct site of 32,000sqm.

Vacancy rates in the market have fallen well below the 10-year-average of 8.2 per cent, currently at 5.4 per cent. In the 6 months to January 2015, meanwhile, there was a net absorption 5,715sqm of floorspace. This was the highest half-year net absorption in three years. However, unlike 2013, where this positive absorption was caused by the addition in 25,050sqm of floorspace, the recently experienced absorption was the result of an increase in tenant demand. Mirroring this, average rents in the market have climbed by $30-$40/sqm since mid-2015.

Lachlan Tower Base, ParramattaProject managed by Colliers International

15Metro Office | Research & Forecast Report | First Half 2016

Sydney Olympic ParkSydney Olympic Park was shaken by CBA’s announcement to leave the precinct. The market has suffered from an intermittent train and bus lines available to tenants. However, now, given the recent announcement for the delivery of a light rail station, these transportation trepidations will be more acute rather than a chronic condition. Furthermore, the Westconnex project will provide improved road transportation to the precinct. Both these projects will provide the long required access to the large western Sydney working population. In the interim however the precinct will likely incur a spike in vacancy. Temporary relief will come from tenants unable to find space in the tighter markets like Parramatta, Norwest and Rhodes. Additionally, the buildings, similar to those in the wider metro markets, will be pursued for residential conversion.

Norwest The Norwest market remains robust with significant interest growing in anticipation of the Norwest Metro line. The sale and 15-year-leaseback of the iconic Woolworths headquarters was a source of reassurance for the precinct. The building was sold for $336 million on a yield of 6.07 to the Korean based firm Inmark Asset Management. The vacancy rate continued its downward progression ending on 8.01 per cent, down from 10.4 per cent. The quantum of floorspace leased increased for the third consecutive quarter, with leases signed in the second half of year 41 per cent higher than the preceding half of year and 400 per cent greater than those in the corresponding period in 2014.

City fringe Vacancy in the city fringe market has continued to tighten following a third consecutive year in leasing growth. This activity, however, will be restricted by the availability of stock moving forward. The city fringe will now be insulated by the ongoing development in Darling Park and proposed ones in the South Sydney. Furthermore, the market has received an increase in demand from tenants displaced by the withdrawals for the infrastructure and residential projects alike.

The Southern CBD and fringe areas are undergoing a significant rejuvenation, underpinned by a renewal in the surrounding markets and infrastructure spend. Commercial markets in the area will benefit from improved connections as a result of the Sydney Light rail project and Sydney Metro project. Moreover, tenants will look to the precinct to capitalise from its proximity to South Sydney, one the nation’s fastest growing residential corridors. In the near term the precinct will be sought after by tenants displaced by the metro line. These tenants, all from secondary buildings, will be seeking affordable alternatives which may exclusively be available in the South or the fringe. These withdrawals, all involving secondary grade assets, will have implications for this tightly held market as displaced tenants look to secure space, as approximately 78 per cent of the floor space to be withdrawn will be from B grade properties. The most important effect of these withdrawals will be firstly, a reduction in smaller tenancies available for lease and secondly a large uptick in demand for smaller sized tenancies as the displaced tenants seek alternate premises. With particular reference to the CBD Metro project, the average size of the incumbent tenants in the buildings to be acquired, and therefore withdrawn from stock, is 417sqm, with only five tenancies above 900sqm. In contrast, the weighted average size of the floor plates of the developments scheduled for delivery in the coming 24 months is 2,000sqm. Ahead of these changes, the number of leases for tenancies under 800sqm increased by 49 per cent since 2013, with limited new supply to meet this smaller occupier market. Incentives in the market are likely to tighten further from its inundation of interest from the secondary tenants in the surrounding markets.

Tenants within the precinct have experienced organic growth, too. These firms need to be domiciled in the market to succeed. Moreover, there has been increased activity in the creative advertising and media groups as consolidation of offices occur, or conglomerate organisations decide to keep businesses separate. In the six months to January, there was over 10,000sqm of advertising agency or creative related demand in the fringe. There are presently minimum options for spaces in the 2,000-4,000sqm range, making it challenging for tenants to find space. Pyrmont’s A Grade vacancy in the Pirrama Rd area adjoining the Star Casino is now all but exhausted following a lease to Fairfax Media Limited (FXJ). FXJ took up 1,610sqm of space at “Wharf 10” Pirrama Road

8 Australia Avenue, Sydney Olympic Park Valued on behalf of The Trust Company (Australia)

16 A Colliers International publication

Metro OfficeMETRO OFFICE

How else can we help you? Speak to one of our property experts [email protected]

For further information please contact: Sas Liyanage Research Analyst | Research | Tel +61 2 9249 2039 [email protected]

to facilitate its growth in the digital business. Outside Pyrmont, Trip Advisor leased 2,700sqm at Cleveland Street to service growth in its business. Overall, in the second half of 2015, A grade vacancy in the City fringe fell from 5.3 per cent to 4.4 per cent. Similarly the vacancy in the B grade market, predominantly due to the withdrawal of 100 Harris St for refurbishment, fell from 7.4 per cent to 2.3 per cent. Surry Hills will likely experience effective rental growth as its overall vacancy rate tightened from 4.2 per cent in July 2015 to an estimated 0.9 per cent by January 2016. Investment volumes in the precinct remained relatively modest, restrained by an availability of stock. The largest sale in the market was 1-3 Small Street in Ultimo. This building was acquired by Mirvac for $53 million at an initial passing yield 6.57 per cent. Elsewhere, was a 6 storey, under-leased commercial office at 64-76 Kippax Street was sold. This building transacted at an initial yield of 4.3 per cent for $31.5 million dollars.

South Sydney Over the course of the last 10 years, South Sydney has undergone one the nation’s fastest transformations. And now, it’s set to embark on the next step of this evolutionary tale. The precinct has now all but transitioned away from its industrial heritage, with the shortcomings of amenity eroding with every new development. The newly completed B4 developments will work with the grain of public infrastructure spending to entice new commercial developments. Meanwhile, the Mirvac and Centuria Property’s successful campaign to build a new home for CBA in Redfern’s Australia Technology Park will inspire confidence in the South. Much like its commercial counterparts, South Sydney’s pipeline is constrained by the competing forces posed by residential developments. The precinct is thus limited with the availability of quality stock, with very little programmed to come online. Goodman’s Connect Corporate Centre is the sole major development under construction having secured a 2,500sqm pre-commitment by Qantas Credit Union. Major leasing deals elsewhere included; Genisis Care (3,386sqm) in 41-43 Bourke Road, Blackmores (1,408sqm) at 185 O’Riordan Street, Hansen Yuncken (1,412sqm) at 75 O’Riordan Street, and Seafolly (2,433sqm) at 41-43 Bourke Road.

There is also an ongoing demand from tenants displaced within the market, looking to remain in South Sydney. These tenant demands are sticky due to their requirements of office space offering co-located warehouses. Furthermore, moving their premises to alternate markets would present consequences on

staff retention. Similarly, there has been an increased appetite from fashion orientated tenants, attracted by co-located warehousing facilities. The market, moreover, has received an influx of fleet-footed tenants priced out of the City South and fringe markets. The number of briefs for spaces above 600sqm higher than ever before, too. This increase in overall demand has driven rental growth in both smaller and larger tenancies. So now, this rental growth is pushing the pendulum towards strata commercial developments as a remedy to absorb absorb this excess demand, particularly in the 300-600sqm range.

South Sydney is set to benefit from the Westconnex, Sydney Metro and Light rail projects. However, in the interim there remains dependency on road transportation. Parking is in high demand with rates currently at $1,500–$2,500 per car space. Consequently, Goodman are building with parking in mind, and now charging where they used to give it away. Notwithstanding this, estates like Sydney Corporate Park have found success in offering free shuttle buses to their tenants.

1-3 Smail Street, UltimoSold on behalf of Anton Capital

17Metro Office | Research & Forecast Report | First Half 2016

MELBOURNE METRO OFFICE

By Anneke Thompson Associate Director | Research [email protected]

The 2015 calendar year was the second year in a row that the Melbourne metro office market recorded a total sales volume above $1 billion. In 2015, the total sales volume came in just under $1.1 billion, compared to $1.07 billion in 2014. Buyers were most active in the outer east precinct, despite more challenging leasing conditions in that market, with 19 of the 49 office sales occurring here, followed by the city fringe, where 17 sales occurred.

Foreign buyers were particularly active in the outer east, accounting for 11 out of the 19 sales. The majority of these properties were purchased for future redevelopment purposes. Interestingly, 30 of the 49 transactions recorded in 2015 occurred off-market, with only 19 being sold through on-market campaigns.

This highlights the strength of demand in the market, with vendors who may have had limited motivation to sell being convinced to part with their property with generous unsolicited offers.

MELBOURNE METRO OFFICE SALES VOLUMES (>$5 MILLION)

$466

$117

$463

$348

$142

$404

$607

$1,067 $1,091

$-

$200

$400

$600

$800

$1,000

$1,200

2007 2008 2009 2010 2011 2012 2013 2014 2015

Mill

ions

$AU

D

Source: Colliers Edge

In this environment, average yields compressed over the year to March 2016 from 7.93 per cent to 7.58 per cent. In the city fringe and the inner east, average lower-end yields are 6.75 per cent.

Continuing low interest rates and volatile equities markets were the main drivers behind the strong sales volumes in both 2014 and 2015. While it is difficult to estimate what volumes will look like come the end of 2016, those factors still remain the same, so we expect continuing strong demand. The challenge for the market, however, will be supply. What assets will be available for motivated vendors to buy? Both local and international buyers are competing aggressively for prime assets in Melbourne’s metro office market. We expect that A Grade or newer assets will be keenly sought after in the $40 million plus price range, as institutions with specific Melbourne metropolitan office market mandates seek to increase their quota of acquisitions. We also expect the trend of foreign buyers actively seeking office buildings situated on land-rich sites or properties that have flexible zonings to continue.

Owner occupiers, especially those in the education, health and medical industries, will continue to purchase office buildings

Another record sales year for Melbourne’s Metro Office Market

First Half 2016

Research and Forecast Report

5 Burwood Road, HawthornLeased on behalf of Lazzcorp

18 A Colliers International publication

Metro OfficeMETRO OFFICE

for their own occupation, especially in the inner suburbs, whilst developers will also seek properties with zonings that allow for future multi-level residential or mixed use developments.

8.18 per cent in March 2016, although this increase is not being felt in the eastern fringe markets, rather the majority of vacancy is around the West Melbourne, South Melbourne and Inner North areas. In the inner east, vacancy decreased from 6.20 per cent in September 2015 to 5.29 per cent in March 2016, and net effective rents increased by 6.07 per cent over the same time period.

The reason for strong demand in these markets is metro tenants increasingly seeking to be close to amenity, employment bases and, most importantly, public transport. The Richmond, Cremorne, Abbotsford, Collingwood, South Yarra, Hawthorn and Camberwell office markets certainly meet these requirements. Rents have been increasing in part due to this strong demand, but also due to constrained supply as well. Any development sites that come to market in these areas are heavily sought after by residential developers, and to a growing extent, childcare, education and healthcare operators. This means that there has been no new supply in these markets over the past year. Overall, the city fringe saw 20,144 sqm of new supply in the year to March 2016, but this was new stock built in South Melbourne, so does not impact the eastern fringe market.

A good example of the tightly held nature of the east city fringe and the appeal of the area is Red Energy’s deal at 570 Church Street. Red Energy – already tenants in the area – were considering two deals as part of their move strategy. One of those was a new building in the CBD, the other 570 Church Street. After incentives were taken into account, the CBD deal was actually the cheaper option. However, Red Energy still chose to stay in Richmond, as the more interesting character-style space offered at 570 Church St, as well as continuity of location and staff retention, were key factors in the deal. The net face rent achieved was believed to be between $450 and $460/sqm, significantly above the city fringe average.

235 Springvale Road, Glen WaverleyProject Managed On behalf of MYOB Winner of PCA Innovation and Excellence Awards 2015

MELBOURNE METRO OFFICE A GRADE MARKET INDICATORS

REGION AVERAGE NET FACE ($/M² PA) INCENTIVE RANGE YIELD RANGE

H1 2016 H2 2016 H1 2016 H2 2016 H1 2016 H2 2016

City Fringe $355 15%-27% 6.75%-7.25%

Inner East $360 15%-20% 6.75%-7.25%

Outer East $308 20%-37% 7%-7.5%

South East $293 20%-25% 7%-9%

North & West $253 18%-25% 8%-9%

St Kilda Rd $335 25%-28% 7%-7.5%

Southbank $440 20%-30% 6.25%-7.5%

COLLIERS INTERNATIONAL RESEARCH FORECASTS

City fringe/inner eastGood effective rental growth demonstrates strength of demandAccording to Deloittes Access Economics, white collar employment growth in Greater Melbourne was 2.98 per cent – the fastest that employment has grown in five years. Demand for office space by both tenants and owner occupiers in the eastern portion of the city fringe and inner east in 2015 certainly reflected this, with landlords seeing very good net effective rental growth on the back of this demand. In the city fringe, A Grade net effective rents have grown from an average of $258/sqm in March 2015, to $280/sqm in March 2016 – a very healthy annual increase of 8.53 per cent. The vacancy rate did actually increase slightly, from 7.83 per cent in September 2015, to

19Metro Office | Research & Forecast Report | First Half 2016

Looking forward, the lack of new supply in the early half of the year should see effective rental growth continue to climb. As rents do continue to climb, we may see some renewed interest in the area from commercial developers, who may start to see these developments become more feasible as face rents move towards economic rent levels. Later in 2016, we will see the completion of the new 13,000 sqm building at Chadstone Shopping Centre, currently pre-committed by Vicinity Centres, who are already based at Chadstone.

MELBOURNE METRO AVERAGE A GRADE NET EFFECTIVE RENTAL GROWTH YEAR TO MARCH 2016

-9.4%

0.0%

1.9%

2.9%

8.5%

-12% -10% -8% -6% -4% -2% 0% 2% 4% 6% 8% 10%

Outer East

North & West

South East

Inner East

City Fringe

Source: Colliers Edge

Outer eastVacancy at record levelsIn contrast to the Melbourne city fringe and inner east markets, the outer east has seen a slowdown in demand at the secondary end of the market, as well as an increase in Prime Grade supply. This has resulted in an increase of vacancy from 10.83 per cent to 11.82 per cent – the highest vacancy rate that Colliers has ever recorded for the outer east office market. In terms of square metres, the outer east now has almost 104,000 sqm of space vacant – also the first time that over 100,000 sqm of space has been available.

Part of the reason for the increase in vacancy in the outer east is an increase in supply – again in stark contrast to other metro markets in Melbourne, which are either seeing no supply additions, or withdrawals of office stock. Just over 36,000 sqm of new supply was added to the outer east market in the year to March 2016. Most of these new buildings are predominately pre-committed, and attracting tenants to the remaining new space is proving successful, given the flight to quality currently being experienced by the market as tenants take advantage of good incentives.

The real challenge that this excess supply creates is for the secondary grade market. The secondary buildings find it difficult to compete with the A Grade backfill space as well as newer prime grade offices, given that rents in the Outer east for both grades are relatively affordable, compared to the rest of the Melbourne market. Average A Grade net effective rents for the outer east are $220/sqm, compared to $280/sqm in the city fringe, $297/sqm in the inner east and $316/sqm in the CBD, meaning rents in the outer east are considered very affordable. Unlike the city fringe and inner east markets, secondary grade buildings in the outer east that have reached the end of their office lifecycle and have limited exit strategy, due to the restrictive nature of zoning in the City of Monash. While most metro office precincts around the country are moving towards a mixed use make up, the outer east commercial precincts are subject to limited opportunity to re-purpose their buildings for uses such as showroom, retail and hotel/other accommodation.

Another issue causing an increase in the vacancy rate in the outer east is the relocation of some tenants to different markets – the largest by far being Jemena vacating 6,900 sqm at 351 Burwood Highway and 7,000 sqm at Ferntree Gully Road.

Deals are still being done in Prime Grade buildings, indicating there is still demand in precinct, and high calibre tenants that still like to be located in the outer east. BSN Medical and Alphera (BMW Finance) have committed to Frasers Property’s Mulgrave Office Park. Renault have also expanded into larger premises at Salta’s Nexus Business Park, also in Mulgrave. In Box Hill, Serco also committed to just over 5,000 sqm of refurbished space at 990 Whitehorse Road.

MELBOURNE METRO AVERAGE A GREADE OFFICE YIELDS

6%

6.5%

7%

7.5%

8%

8.5%

9%

9.5%

10%

Mar

-04

Sep-

04

Mar

-05

Sep-

05

Mar

-06

Sep-

06

Mar

-07

Sep-

07

Mar

-08

Sep-

08

Mar

-09

Sep-

09

Mar

-10

Sep-

10

Mar

-11

Sep-

11

Mar

-12

Sep-

12

Mar

-13

Sep-

13

Mar

-14

Sep-

14

Mar

-15

Sep-

15

Mar

-16

City Fringe Inner East Outer East

Source: Colliers Edge31 Vision Drive, Burwood East

Managed on behalf of Private Co Investments No 4 Pty Ltd

20 A Colliers International publication

Metro OfficeMETRO OFFICE

North & westVacancy in the Melbourne north and west market decreased from 5.35 per cent in September 2015 to 4.55 percent currently. The long term average vacancy rate in the North and West is 4.87 percent, so this market can now be viewed to be one that is slightly in favour of landlords.

Despite this decrease in vacancy, A Grade Net Face rents have remained steady, at an average of $253/sqm. While vacancy is low, the office market in the north and west is relatively immature, and landlords need rents to be competitive to encourage tenants to stay in the area.

South eastVacancy follows trend in outer eastThe vacancy rate in the South East market increased from 7.65 per cent in September 2015, to 11.76 per cent in March 2016. Just one year ago, the vacancy rate was a mere 2.90 per cent.

The major reason for the increase is an influx of smaller space to the market, again as tenants move to more quality spaces in the city fringe and the inner east. On the larger side of vacancy, Visionstream have vacated all of 236 East Boundary Road in Bentleigh East, following the loss of a contract. This has a major impact on vacancy in such a small market as the South East.

In Frankston, vacancy increased from 765 sqm in September 2015, to 1,629 sqm in March 2016, possibly due to the competition provided from the strata suites and serviced offices now available at APBC’s Peninsula on the Bay.

Rents and incentives for both Prime and Secondary Grade buildings in the South East have remained steady through the past six months, but expect that over 2016, effective rents will decline as landlords try to entice tenants back to the precinct.

MELBOURNE METRO VACANCY RATES

0%

2%

4%

6%

8%

10%

12%

14%

Mar

-04

Sep-

04

Mar

-05

Sep-

05

Mar

-06

Sep-

06

Mar

-07

Sep-

07

Mar

-08

Sep-

08

Mar

-09

Sep-

09

Mar

-10

Sep-

10

Mar

-11

Sep-

11

Mar

-12

Sep-

12

Mar

-13

Sep-

13

Mar

-14

Sep-

14

Mar

-15

Sep-

15

Mar

-16

City Fringe Inner East Outer East South East

Source: Colliers Edge

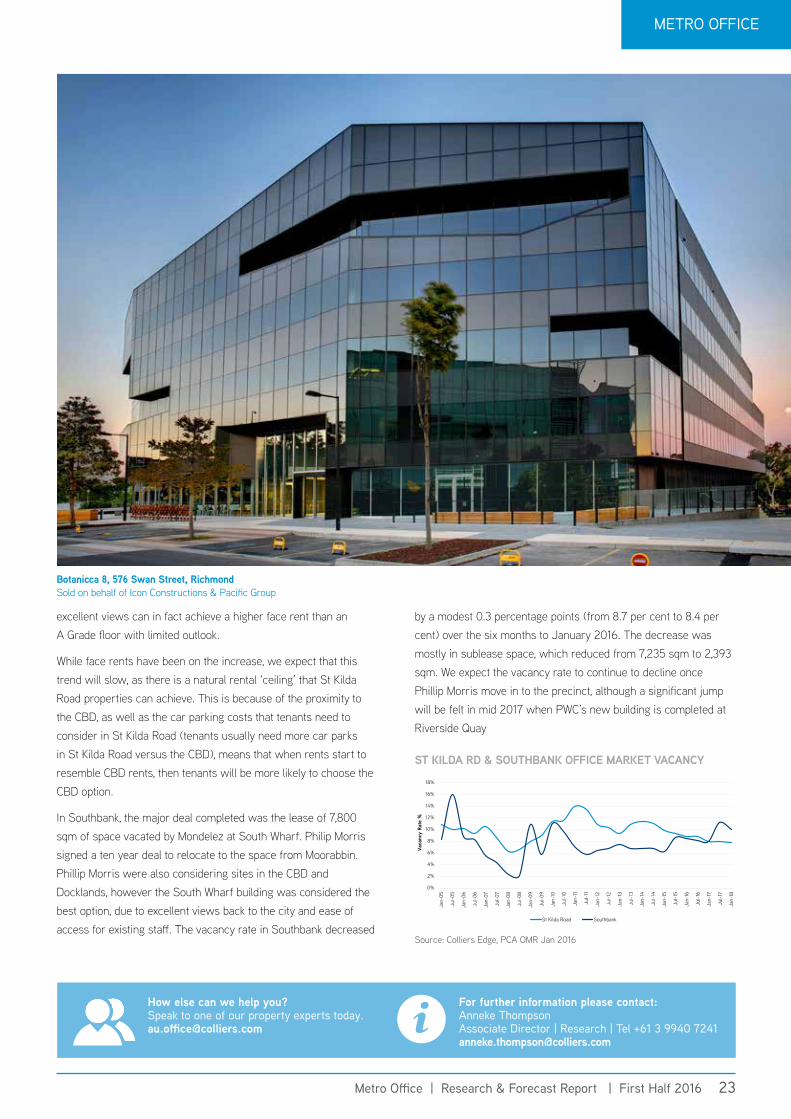

St Kilda Road & SouthbankFollowing a record year of office investment activity in 2014, where just over $500 million worth of office stock transacted in the St Kilda Road precinct, there was only one investment sale in St Kilda Road in 2015. This was the sale of 636 St Kilda Road to AMP Capital’s Wholesale Australian Property Fund (WAPF) for $87.5 million in December 2015. The property transacted at a 6.72 per cent fully let initial yield, and Colliers International brokered the sale.

There have been two further transactions of office properties in 2015; however both of these buildings are being converted

Bayside Junction, 973 Nepean Highway, BentleighSold on behalf of Icon Constructions & Pacific Group

21Metro Office | Research & Forecast Report | First Half 2016

to residential use. Private investment and development group Qualitas purchased 499 St Kilda Road in April 2015 for $80 million, and are currently partnering with LAS Group in marketing a residential development known as The Fawkner. The other major transaction was the sale of St Kilda Road Police complex at 412 St Kilda Road to Malaysian developer UEM Sunrise for $58 million. The Victorian Police Force are in the process of vacating the building to move into their new purpose built premises in Spencer Street in the CBD. UEM Sunrise will convert the building and/or site to a residential use. More recently, 596 St Kilda Road, a 1940s apartment complex sold for approximately $25 million, after the 19 owners banded together to sell the building and land as a whole. The site is also expected to be retained for residential use, with the sale representing a land value rate of approx. $14,000/sqm.

No investment sales were transacted in the Southbank precinct in 2015, although there were seven sales totalling almost $150 million of development sites over the year. The sites purchased were a mixture of industrial/showroom sites and small, C or D Grade offices. Most developments planned are residential, although one site (35-47 City Road) sold to hotel developer/operator Pro-Invest. ST KILDA RD NEW EFFECTIVE RENTS

$150

$170

$190

$210

$230

$250

$270

Mar

-09

Sep-

09

Mar

-10

Sep-

10

Mar

-11

Sep-

11

Mar

-12

Sep-

12

Mar

-13

Sep-

13

Mar

-14

Sep-

14

Mar

-15

Sep-

15

Mar

-16

$/sq

m

A Grade B Grade

Source: Colliers Edge

St Kilda Road effective rents on the riseThe St Kilda Road vacancy rate has declined from 9.3 per cent to 8.9 per cent, with total vacancy in the precinct reduced by 4,062 sqm. A decline in sublease vacancy of 4,870 sqm was the biggest factor in the decline in vacancy, as well as 15,685 sqm in withdrawals. The withdrawal of 499 St Kilda Road was the main contributor to this.

St Kilda Road now has very few large chunks of vacancy available, the biggest being 8,000 sqm at 553 St Kilda Road. The market has now very much become a small occupier market, with demand primarily coming from those local tenants displaced by the withdrawal of buildings for residential conversions, or other smaller tenants that don’t want to pay CBD rents, yet need to be close to the CBD. The vacancy rate will continue to trend down, as more buildings are withdrawn from the market. The largest of the upcoming withdrawals is 412 St Kilda Road, which is currently occupied by Victoria Police. The building was sold last year to Malaysian developer UEM Sunrise, who have recently submitted plans to convert the building to accommodate 182 high-end apartments. Net effective rents in both A and B Grade buildings in St Kilda Road have increased by 7.8 and 13 per cent respectively over the year to March 2016. These increases are due both an increase in face rents and a slight decrease in incentives, as space availability across both grades continues to dry up. Interestingly, there is a not a great deal of difference between A and B Grade effective rents ($246 versus $213 respectively), as there is a far smaller differential between quality of buildings in this market than there is in the CBD. Views on offer also play a major factor in the rental level that can be achieved in St Kilda Road - a B Grade floor with

990 Whitehorse Road, Box HillLeased on behalf of Glorious Sun

22 A Colliers International publication

Metro OfficeMETRO OFFICE

How else can we help you? Speak to one of our property experts [email protected]

For further information please contact: Anneke Thompson Associate Director | Research | Tel +61 3 9940 7241 [email protected]

excellent views can in fact achieve a higher face rent than an A Grade floor with limited outlook.

While face rents have been on the increase, we expect that this trend will slow, as there is a natural rental ‘ceiling’ that St Kilda Road properties can achieve. This is because of the proximity to the CBD, as well as the car parking costs that tenants need to consider in St Kilda Road (tenants usually need more car parks in St Kilda Road versus the CBD), means that when rents start to resemble CBD rents, then tenants will be more likely to choose the CBD option.

In Southbank, the major deal completed was the lease of 7,800 sqm of space vacated by Mondelez at South Wharf. Philip Morris signed a ten year deal to relocate to the space from Moorabbin. Phillip Morris were also considering sites in the CBD and Docklands, however the South Wharf building was considered the best option, due to excellent views back to the city and ease of access for existing staff. The vacancy rate in Southbank decreased

Botanicca 8, 576 Swan Street, RichmondSold on behalf of Icon Constructions & Pacific Group

by a modest 0.3 percentage points (from 8.7 per cent to 8.4 per cent) over the six months to January 2016. The decrease was mostly in sublease space, which reduced from 7,235 sqm to 2,393 sqm. We expect the vacancy rate to continue to decline once Phillip Morris move in to the precinct, although a significant jump will be felt in mid 2017 when PWC’s new building is completed at Riverside Quay ST KILDA RD & SOUTHBANK OFFICE MARKET VACANCY

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

Jan-

05

Jul-0

5

Jan-

06

Jul-0

6

Jan-

07

Jul-0

7

Jan-

08

Jul-0

8

Jan-

09

Jul-0

9

Jan-

10

Jul-1

0

Jan-

11

Jul-1

1

Jan-

12

Jul-1

2

Jan-

13

Jul-1

3

Jan-

14

Jul-1

4

Jan-

15

Jul-1

5

Jan-

16

Jul-1

6

Jan-

17

Jul-1

7

Jan-

18

Vaca

ncy

Rate

%

St Kilda Road Southbank

Source: Colliers Edge, PCA OMR Jan 2016

23Metro Office | Research & Forecast Report | First Half 2016

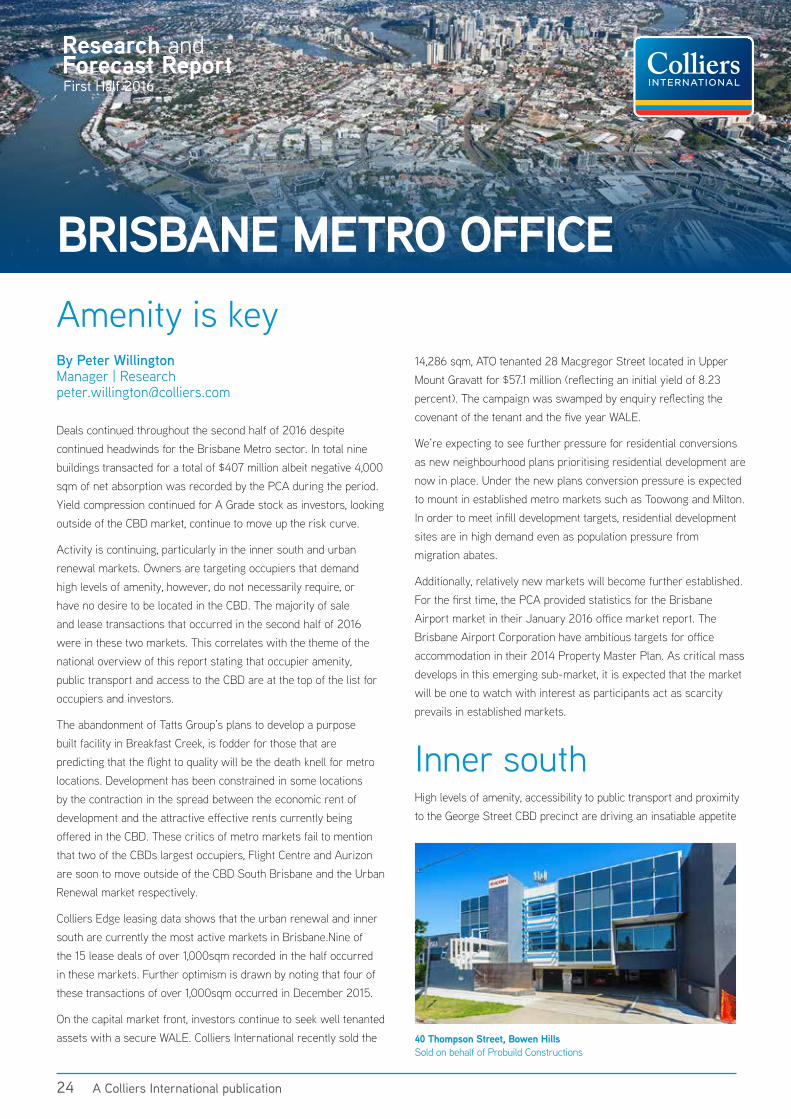

BRISBANE METRO OFFICE

By Peter Willington Manager | Research [email protected]

Deals continued throughout the second half of 2016 despite continued headwinds for the Brisbane Metro sector. In total nine buildings transacted for a total of $407 million albeit negative 4,000 sqm of net absorption was recorded by the PCA during the period. Yield compression continued for A Grade stock as investors, looking outside of the CBD market, continue to move up the risk curve.

Activity is continuing, particularly in the inner south and urban renewal markets. Owners are targeting occupiers that demand high levels of amenity, however, do not necessarily require, or have no desire to be located in the CBD. The majority of sale and lease transactions that occurred in the second half of 2016 were in these two markets. This correlates with the theme of the national overview of this report stating that occupier amenity, public transport and access to the CBD are at the top of the list for occupiers and investors.

The abandonment of Tatts Group’s plans to develop a purpose built facility in Breakfast Creek, is fodder for those that are predicting that the flight to quality will be the death knell for metro locations. Development has been constrained in some locations by the contraction in the spread between the economic rent of development and the attractive effective rents currently being offered in the CBD. These critics of metro markets fail to mention that two of the CBDs largest occupiers, Flight Centre and Aurizon are soon to move outside of the CBD South Brisbane and the Urban Renewal market respectively.

Colliers Edge leasing data shows that the urban renewal and inner south are currently the most active markets in Brisbane.Nine of the 15 lease deals of over 1,000sqm recorded in the half occurred in these markets. Further optimism is drawn by noting that four of these transactions of over 1,000sqm occurred in December 2015.

On the capital market front, investors continue to seek well tenanted assets with a secure WALE. Colliers International recently sold the

14,286 sqm, ATO tenanted 28 Macgregor Street located in Upper Mount Gravatt for $57.1 million (reflecting an initial yield of 8.23 percent). The campaign was swamped by enquiry reflecting the covenant of the tenant and the five year WALE.

We’re expecting to see further pressure for residential conversions as new neighbourhood plans prioritising residential development are now in place. Under the new plans conversion pressure is expected to mount in established metro markets such as Toowong and Milton. In order to meet infill development targets, residential development sites are in high demand even as population pressure from migration abates.

Additionally, relatively new markets will become further established. For the first time, the PCA provided statistics for the Brisbane Airport market in their January 2016 office market report. The Brisbane Airport Corporation have ambitious targets for office accommodation in their 2014 Property Master Plan. As critical mass develops in this emerging sub-market, it is expected that the market will be one to watch with interest as participants act as scarcity prevails in established markets.

Inner southHigh levels of amenity, accessibility to public transport and proximity to the George Street CBD precinct are driving an insatiable appetite

Amenity is key

First Half 2016

Research and Forecast Report

40 Thompson Street, Bowen Hills Sold on behalf of Probuild Constructions

For further information please contact: Peter Willington Manager | Research | Tel +61 7 3026 3305 [email protected]

24 A Colliers International publication

Metro OfficeMETRO OFFICE

BRISBANE METRO OFFICE PRIME GRADE MARKET INDICATORS

REGIONAVERAGE

GROSS FACE ($/m² pa)

INCENTIVE RANGE YIELD RANGE

H2 2015

H1 2016 H2 2015 H1

2016 H2 2015 H1 2016

Urban Renewal $545 30% - 40% 6.75% - 7.5%

Inner South $560 25% - 35% 6.75% - 7.5%

Milton $485 35% - 45% 8% - 8.75%

Toowong $475 30% - 35% 8.5% - 9%

Spring Hill $490 30% - 40% 8.5% - 9%

COLLIERS INTERNATIONAL RESEARCH FORECASTS

for space in the inner south precinct. The continued demand for space in the inner south led to the PCA reporting the lowest vacancy rate in all Brisbane markets at 9.7 per cent. This is a substantial increase from the previous half of six per cent, however, the vacancy is primarily in secondary accommodation.

The inner south will be home to Flight Centre’s global headquarters, at SouthPoint, the last vacant site in the South Bank precinct. Currently being constructed by the Anthony John Group, the 20,000 sqm office building is on top of the South Brisbane train station and is in the heart of the revamped restaurant and parkland precinct of South Bank. The building was awarded a five star Green Star Rating in November and will set a new benchmark for prime office space in metro markets.

No further development is expected in the South Brisbane Precinct until the Parlamat site, on Montague Road, is released to market, however, the end use and configuration of this site is still being debated. Vacancy levels are expected to decline on the back of a subdued future development pipeline and as secondary office space is withdrawn for redevelopment or conversion for residential uses.

INNER SOUTH - SUPPLY ADDITIONS, WITHDRAWALS, VACANCY

0%

2%

4%

6%

8%

10%

12%

14%

-15000

-10000

-5000

0

5000

10000

15000

20000

25000

30000

35000

40000

6 Month Net Absorption Net Supply Additions Vacancy Rate

Source: Colliers Edge

Two sales were recorded in the half, 99 Melbourne Street and Stanley Street House. Lasalle Investment sold Stanley Street House to AMP Life Limited for $26.3 million at an initial yield of

25 Montpelier Road, Bowen HillsLeasing exclusively on behalf of GWC Property

6.24 percent reflecting the high demand for good quality assets in the market. 99 Melbourne Street transacted at an initial yield of 7.55 per cent, informed by a high tenancy risk with Stockland rumoured to be looking for alternate accommodation at the expiry of their current lease.

The inner south is expected to remain attractive to developers, investors and occupiers in the medium to long term. The increasing amenity of the area, strong public transport links and connectivity to the future Queens Wharf precinct are expected to be a competitive edge for occupiers when comparing metro markets.

Urban Renewal The urban renewal market continues to be one of the most sought after markets for occupiers. This is reflected by a further 7,000 sqm of net absorption recorded by the PCA in the second half of 2016. The urban renewal market follows the inner south market as the second tightest market in terms of vacancy at a reported 9.8 per cent.

Attracted to the area by the high levels of amenity offered and close links to the Fortitude Valley and CBD, the urban renewal market has seen continual positive net absorption for a number of years. The area has been subject to continual gentrification and now that the Gasworks development has reached maturity, we’re expecting to see continual contraction in the vacancy rate supported further by withdrawals of secondary stock.

The development pipeline that brought some 111,000 sqm of office space to the market over the past three years, has now slowed with no new development expected. The abandonment of plans for the Tatts Group to develop a purpose built facility at Breakfast Creek is a minor setback, however, has no material impact on the current market.

Two notable transactions occurred in the second half of 2016; 1 King Street in Bowen Hills (as reported last half) and 1-3 Breakfast Creek

25Metro Office | Research & Forecast Report | First Half 2016

How else can we help you? Speak to one of our property experts [email protected]

For further information please contact: Peter Willington Manager | Research | Tel +61 7 3026 3305 [email protected]

Road in Newstead for $131.9 million and $36.3 million respectively. Continuing the theme of compressing yields in metro markets for quality accommodation, the 16,500 sqm building in King Street transacted at an initial yield of 7.02 per cent; a yield expected for an A Grade building in the CBD.

As a swathe of residential development completes in the Newstead precinct, further amenity and close links and access to an increased resident population is expected to drive a positive perception of the urban renewal market.

Spring HillThe Spring Hill market has come under further pressure for residential conversion as the Spring Hill Neighbourhood Plan has progressed through the approval process. With new height limits of up to 15 storeys and a declining office market, we expect to see further withdrawals from the market as the highest and best use of some assets changes to residential uses.

While only approximately 30,000 sqm of office space has been withdrawn in recent years, as the planning scheme is approved, we expect to see a large uptick in withdrawals over the coming years. The withdrawals are expected to be accelerated by the migration of occupiers to emerging and higher amenity precincts such as the inner south and urban renewal or into competitive occupancy costs in the struggling Milton area.

While the outlook is less than positive for the Spring Hill office market, leasing deals have continued. However, transactions that have occurred have been relatively small, averaging just over 100 sqm.

No major sales were recorded in the half, as many investors are in a holding pattern waiting for the final neighbourhood plan.

Milton & ToowongSimilar to Spring Hill, the other traditional metro market of Milton (including Toowong) is coming under increasing pressure for residential conversion. Some 2,000 residential units are currently being marketed or in the development pipeline along the in the area which has been the traditional home of metro office accommodation. Unlike the Spring Hill market, the relative quality and age of stock is much better in Milton and the office precincts are somewhat insulated from residential development by a buffer of alternate uses and as such we’re yet to see any major withdrawals from the market.

The competitive advantage of the inner south and urban renewal markets is most aptly represented in the relative vacancy rates. Milton sits substantially higher than these other markets at 20.1 per cent reported vacancy. Anecdotally however the underlying sublease vacancy factor of 3.8 per cent is underreported as contracting tenants continue to use space that is marketed for sub-lease.

Of further concern is the looming expiry of the Origin Energy lease; who are expected to relocate approximately 20,000sqm to either the inner south or urban renewal markets, further impacting the vacancy rate.

The declining nature of the Milton market is reflected in the sales data where no major transactions were recorded in the half.

PROPORTION OF STOCK BY MARKET

-

100,000

200,000

300,000

400,000

500,000

600,000

Urban Renewal Inner South Milton Spring Hill Toowong

Source: Colliers Edge

We’re expecting to see the Milton office market compress further into the pocket surrounding Suncorp Stadium, where larger scale buildings and surrounding amenity will be able to compete with the high quality assets in the other metro markets. As such the proportion of office space in the Milton market as a percentage of the total metro market is expected to continue to decrease.

419 Upper Edward Street, Spring Hill Sold on behalf of Daniel Butlera

26 A Colliers International publication

Metro OfficeMETRO OFFICE

ADELAIDE METRO OFFICE

By Kate Gray Associate Director | Research [email protected]