Embed Size (px)

Citation preview

2015 University of South Florida Accounting Circle CPE Conference

May 28-29, 2015

4202 E. Fowler Ave. BSN3403 Tampa, FL 33620

2015 USF Accounting Circle Conference Speakers

Kristin Allen is an accomplished leader focused on helping making life easier for her finance peers. As a Senior Director in Jabil’s Finance Transformation team, Kristin facilitates change and process improvement through mentoring, applying proven process improvement and problem-solving methodologies, such as Lean Six Sigma, and leading a team of process improvement experts. She has been with Jabil’s Finance Transformation team for 4 years, working with both the corporate and plant finance teams. Prior to Jabil, Kristin worked as a finance process improvement and internal controls consultant with Protiviti and Arthur Andersen for 12 years. Kristin graduated from USF with both her Masters and Bachelors in Accounting and is a Florida CPA and CIA. She is excited to share how patience, a clear objective and a simple plan helped Jabil achieve a 4-day close.

Faith started her career at Publix Super Markets, Inc. 33 years ago working in corporate accounting, then initiating the continuous quality improvement effort throughout the company, and now has more than 15 years in Loss Prevention. She has field experience as a Regional Loss Prevention Specialist focusing on dishonest employee investigations/interviews and leading the effort to initiate shrink compliance auditing. As the Senior Manager of Analytics she was responsible for all loss prevention data systems and a staff who analyzed shrink, maintained company-wide case and audit file records, issued civil demand and managed recovery, conducted financial crimes investigations, and ensured compliance regarding Money Services reporting. As Lakeland Division Manager, she and her staff have responsibility for Loss Prevention and Safety in over 275 stores to include criminal investigations, physical security, shrink and safety awareness, audits, and investigations. Faith has a BA in Business from Warner Southern University and is a Certified Fraud Examiner.

Faith Clark, CFE Publix Super Markets, Inc. Divisional Loss Prevention & Safety Manager

Kristin Allen, CPA, CIA Jabil Circuit, Inc. Senior Director of Finance Transformation

Jason Guthrie, CPA Ernst & Young LLP. Americas Professional Practice- Audit

Judy Genshaft University of South Florida, System President

Judy Genshaft was appointed president of the University of South Florida System in July 2000. Under her tenure, USF has been named a Top 50 research university among both public and private institutions nationwide in total research expenditures, according to the National Science Foundation; is one of 63 public research universities recognized by the Carnegie Foundation for very high research activity; and has become a global leader in producing new U.S. patents. The USF System serves more than 48,000 students on three campuses and generates an annual economic impact of more than $4.4 billion. Additionally, President Genshaft has played a high-profile role in guiding the nation’s higher education agenda. She is a past Chair for the American Council on Education and is a member of the Association of Public and Land-Grant Universities Board of Directors. President Genshaft made history in 2010 when she became the first woman to chair the NCAA Division I board and is also the former chair of the American Athletic Conference Council of Presidents.

Jason is a Senior Manager within Americas Professional Practice – Auditing (APPAu) based in Cleveland, OH. He is originally from San Jose, California - home of EY’s Global Technology Center - where he spent over 6 years auditing many companies within the technology industry, including Hewlett-Packard Company (“HP”) and Juniper Networks, one of the world’s largest provider of networking hardware and software.

Jason leverages his broad experience addressing complex accounting and auditing matters in his current role in APPAu where he has led much of the research, design, learning and implementation of data analysis tools and techniques over the past 3 years across the Americas.

Jason is an active alumnus of BYU, from which he holds a Master and Bachelor degree in Accounting with a concentration in Audit and a Minor in Information Systems Management. He is a Certified Public Accountant in California and Ohio.

Brad is a Managing Director/Shareholder in the Assurance* Group of CBIZ MHM, Tampa Bay and Mayer Hoffman McCann P.C. Prior to joining the practice, he spent seven years in public accounting with Deloitte in Tampa. He most recently served as Director of Accounting and Risk Management for Bloomin’ Brands Inc.

Dividing his time between national and local responsibilities, he focuses significantly on building the SEC Consulting practice and additional areas of technical consulting for MHM in the Southeast. This includes consultations with companies considering going public as well as assistance with IPOs; assistance with SEC filings; review of complex contracts; and analysis of new accounting standards and application of them for public entities.

Brad also spends a portion of his time as a member of MHM’s Professional Standards Group where he performs internal consultations on complex private or public company engagements, as well as focus on the firm’s SEC audit methodology.

Jeff is a Director with Deloitte & Touche LLP in its National Office SEC Services Department in Washington, DC. The SEC Services Department performs pre-filing reviews of SEC filings, assists clients with the SEC comment process, and provides assistance and interpretative guidance to clients on SEC issues.

Jeff joined the firm’s National Office SEC Services Department in May 2012. He is also a speaker on current and emerging SEC accounting and financial reporting issues.

Prior to joining the firm’s National Office, Jeff spent over 7 years with the SEC in the Division of Corporation Finance, where he was an Accounting Branch Chief. Prior to joining the SEC, he worked for Deloitte & Touche LLP as a Manager where he served major clients that were SEC registrants.

Jeffrey Jaramillo, CPA Deloitte & Touche LLP Audit Director

Bradford L. Hale, CPA CBIZ MHM, LLC. Managing Director

Stephanie Lifshin Jabil Circuit, Inc. Manager of Finance Transformation

Dan Julevich, CPA, CIA, CISA, CRMA WellCare Health Plans, Inc. Senior Director, Internal Audit and ERM

Dan is responsible for the corporate Enterprise Risk Management (ERM) program at WellCare Health Plans. He has over 20 years of audit, consulting, and management experience across a broad range of subject matter and industries. Dan began his professional career with Ernst & Young and also worked for Protiviti and Bankers Financial Corporation prior to joining WellCare.

Dan is a CPA, CIA, CISA, and earned a bachelor’s degree in Accounting and Finance from Florida State University. He is a Little League baseball coach and a U.S. Air Force veteran.

Stephanie Lifshin has a broad base of experience gained from various roles within Jabil, ranging from internal control adherence to change and project management. She successfully led the multi-year global Finance initiative to reduce the close cycle from 6 days to 4. Stephanie joined Jabil in 2007, working in the Internal Audit department. After spending 4 years in Audit, she transferred to become a Manager on the Finance Transformation Team. In this current role, she focuses on process improvements and increasing efficiency within Corporate Finance. Prior to Jabil, Stephanie was a corporate accountant for a biopharmaceutical company. Stephanie received her Bachelor of Science in Business Management degree from Babson College.

Scott McKay is a Risk Advisory and Forensics Services Partner in the Raleigh office of Cherry, Bekaert LLP. Scott’s public accounting background and extensive industry experience enables him to provide keen insights when conducting investigations of potential irregularities and defalcations. He has extensive experience with fraud in the procurement cycle including corruption and misappropriation of assets. In addition, he has experience in the following areas:

• Corruption in the sales and distribution channels, involving customer incentive schemes

• Financial fraud – revenue recognition and improper estimates

• Stock-based compensation schemes Moreover, Scott has extensive experience in anti-fraud internal control design and establishing control self-assessment and ongoing monitoring techniques within the given organization. Prior to joining Cherry Bekaert, he served for several years in financial leadership roles as Corporate Controller and as Director of Corporate Audit for a large public multi-national semiconductor company. Prior to his industry experience, Scott served as Manager with a national accounting firm, where he performed assurance and risk advisory services for multinational organizations, construction, manufacturing, distribution and casinos.

Cary D. McMillan is Chief Executive Officer of True Partners Consulting LLC, a nationwide provider of tax and financial consulting services, headquartered in Chicago. Prior to joining True Partners, he served in many roles at Sara Lee Corporation including Executive Vice President, Chief Executive Officer of Sara Lee Branded Apparel and Chief Financial Officer. Before joining Sara Lee in 1999 he was managing partner of Arthur Andersen’s Chicago office. McMillan currently serves on the boards of McDonald’s Corporation, American Eagle Outfitters, Inc. and Hyatt Hotels Corporation. Previously he served on the boards of Hewitt Associates and Sara Lee Corporation He is also active in the Chicago non-profit community. He currently is the Chairman of the Board of The School of the Art Institute; Vice Chairman of The Art Institute of Chicago; and on the boards of the PBS affiliate, WTTW and Millennium Park. McMillan is a graduate of the College of Business at the University of Illinois. He is a member of the American Institute of Certified Public Accountants and Illinois CPA Society.

Cary McMillan True Partners Consulting, LLC CEO

Scott McKay, CPA, CFE, CIA Cherry Bekaert LLP Partner, Risk Advisory Services

Fred Nicely, Esq. Council On State Taxation Senior Tax Counsel

Kerry Myers, Esq., CFE University of South Florida Clinical Professor of Accounting and Law

Kerry Myers teaches graduate classes on forensic accounting, which includes the topics of white collar crime, fraud, money laundering, and financial investigation, at USF's Lynn Pippenger School of Accountancy in the Muma College of Business. He is also part of the Florida Center for Cybersecurity. Prior to joining USF, Myers worked 25 years as both an attorney and an accountant with the Federal Bureau of Investigation. He was one of the original members of the Tampa Bay Bank Fraud Task Force and also served on the Tampa Joint Terrorism Task Force. He was also certified as a bomb technician with the FBI and worked the Oklahoma City Bombing, Centennial Park Bombing in Atlanta, and the TWA Flight 800 crash off of Long Island Sound. He testified against both Timothy McVeigh and Terry Nichols during their respective trials. Myers received the Federal Law Enforcement Officers' Association Annual Award for Bravery in 2008 for his work in Afghanistan with improvised explosive devices, and a Director's Award from then-FBI Director Louis Freeh for leading a national terrorism undercover operation. Myers earned his Juris Doctorate, with distinction, from the University of Missouri and a Bachelor of Science in Business Administration-Accounting, summa cum laude, from Central Missouri State University. He is a Certified Fraud Examiner and is licensed to practice law in Missouri, where he was a trial attorney and prosecutor for almost a decade before joining the FBI.

Fred Nicely is a Senior Tax Counsel at the Council On State Taxation (COST). His role as Senior Tax Counsel extends to all aspects of the COST mission statement: “to preserve and promote equitable and nondiscriminatory state and local taxation of multijurisdictional business entities.” Before joining COST, Fred served in the Ohio Department of Taxation for four years as Deputy Tax Commissioner over Legal and for the prior seven years as the Department’s Chief Counsel. Fred’s responsibilities at the Department included testifying before legislative committees, participating as an alternative delegate for Ohio at Streamlined Sales Tax Project meetings, and reviewing legal documents issued by the Department, including deciding the merits of filing an appeal. He is a frequent speaker and author on Ohio’s tax system and on multistate tax issues generally. Fred also has extensive experience in public utility tax law, having served as an administrator of the Department’s public utility tax division. Fred’s undergraduate degree in psychology (with a concentration in accounting) is from the Ohio State University. He obtained his MBA and JD from Capital University in Columbus, Ohio. He can be reached at 202/484-5213; ([email protected]).

Bruce Nunnally has over 30 years of public accounting experience, including 9 years with the international public accounting firm, Ernst & Young, LLP. Bruce is a national instructor of accounting and auditing issues. He has presented accounting and auditing continuing education classes for a quarter of the top 30 CPA firms in the U.S. Some of the courses he has led include:

• Annual Update for Accountants and Auditors

• Governmental and Not-for-Profit Update

• Audits of 401K Plans

• Fair Value Accounting

• FASB Update for Industry

In 2000, Bruce was recognized as an “Outstanding Discussion Leader” by the Florida Institute of Certified Public Accountants.

Bruce has been a Certified Public Accountant since 1981 and a partner with CRI since its inception.

Prior to graduating from the University of South Florida with a B.S. in Accounting, Steve spent 6 years on active duty in the US Navy’s Submarine Service.

Steve is the Managing Director of Oscher Consulting where he serves as a consulting and testifying expert in accounting, financial and economic matters. He has been appointed by the Courts as a Trustee, Receiver, Examiner and Special Master.

His professional activities have included:

• Chairman, Florida State Board of Accountancy

• Chairman, Audit Committee, USF Physicians Group

• Chairman, USF School of Accountancy Advisory Board

He has been recognized as:

• USF – 1987 Distinguished Alumnus Award

Steve Oscher, CPA, ABV, CFF, CFE Oscher Consulting, PA Managing Director

Bruce A. Nunnally, CPA, CGMA Carr, Riggs & Ingram, LLC Partner

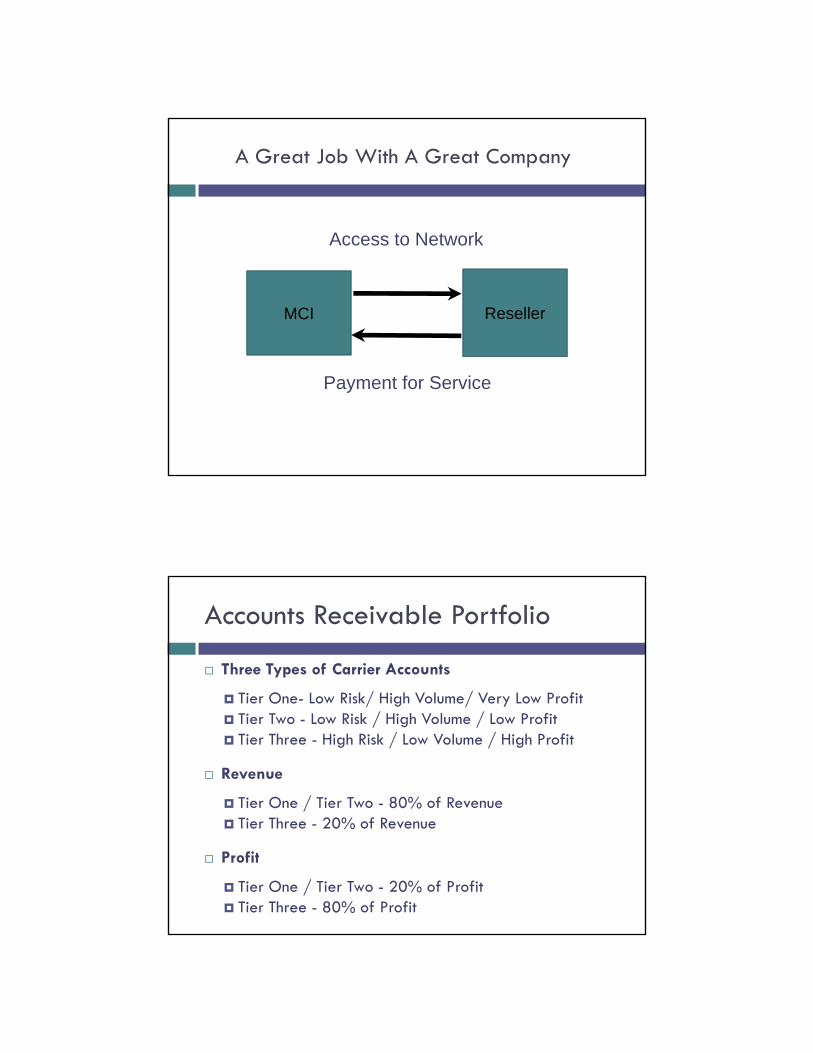

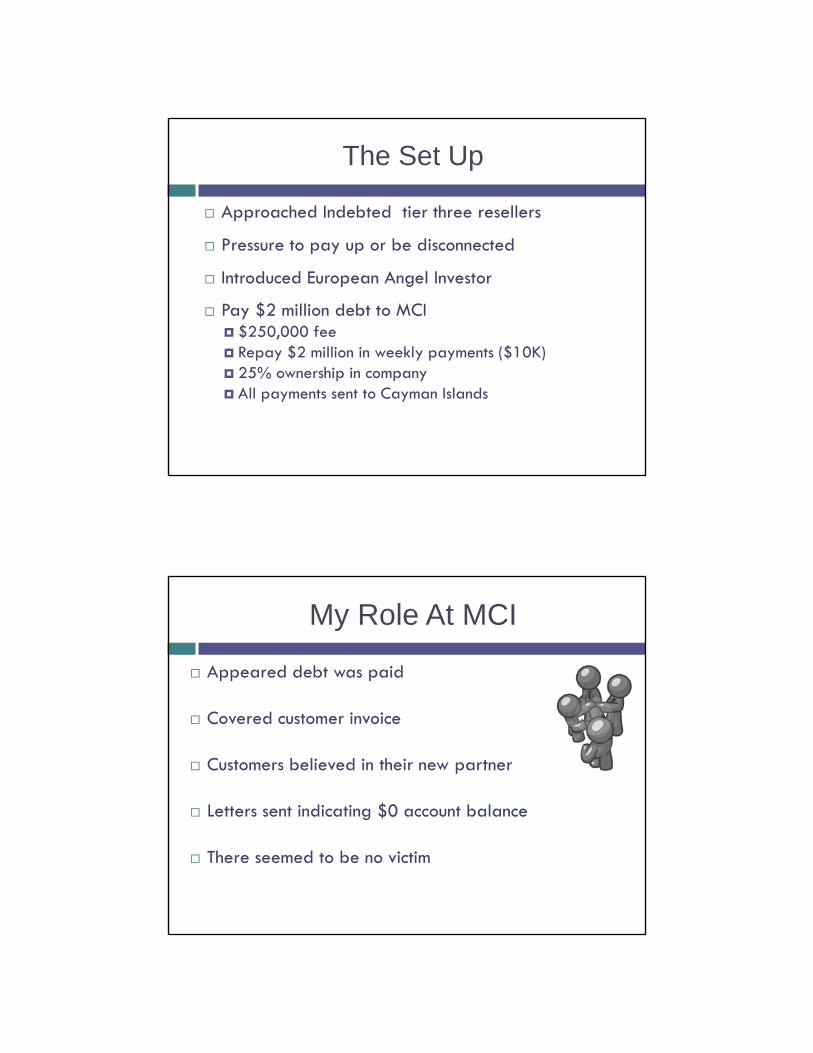

Walt Pavlo Jr. Forbes contributor Prisionlogy

Aakash Patel Elevate, Inc. President

Aakash Patel is here to help business owners learn, connect and grow in the community. Patel has a diverse work background in journalism, business development and public relations. In 2012 Patel started his firm, Elevate, Inc., a Florida-based strategic business consulting firm providing a public relations, community relations, target networking and social media. Prior to that, he worked as an Editorial Assistant at the Tampa Bay Times Tallahassee Bureau, served as Public Relations Coordinator for the Westin Tampa Bay Hotel and Aqua, and was the founding Director of Business Development for Chamber.com. He is an active member of the Greater Tampa Chamber of Commerce, Vistage, Tampa Downtown Partnership, Seminole Torchbearers, and Washington Leadership Program. And, in order to give back while staying connected, Patel volunteers and serves as Chair of The Early Learning Coalition of Hillsborough County and The University of Tampa Board of Counselors. In addition he also volunteers his time with the Indo-US Chamber of Commerce, the Gasparilla Film Festival Advisory Board, the Centre Club Board of Governors, and the Leadership Tampa Bay Board of Directors. Aakash holds both a degree in English Literature and a degree in Political Science from Florida State University.

Walt Pavlo is a contributor to Forbes.com where he writes about white-collar crime. He is the co-author of Stolen Without A Gun, which he co-wrote with Neil Weinberg (Editor-in-Chief at American Banker). Mr. Pavlo’s story has been a part of training programs at the Federal Bureau of Investigation, major corporations and top ranked MBA programs across the country. Walt Pavlo is the founder of www.500PearlStreet.com, which is a website dedicated to providing information on current White-collar crime cases with the purpose of educating people on the major cases in our federal court system. He is also an adjunct professor at Endicott College’s Van Loan School teaching graduate level classes in Finance and Ethics. Mr. Pavlo is a nationally recognized speaker on white-collar crime, ethics and federal prison. He specializes in helping future leaders, corporate leaders and employees understand how fraud starts within an organization by providing insight into the motivations of perpetrators and the opportunities they see when they commit crimes within a company. Mr. Pavlo was recruited by the Federal Bureau of Investigation to lead training and discussions on financial fraud in the corporate environment in order to create awareness that fraud can exist in any workplace. His case has been cited in numerous textbooks and periodicals as a classic story of how a lack of proper mentoring and support within an organization can lead to poor decisions. His story has been featured on ABC Nightline, The Katie Couric Show and the NBC Today Show. Mr. Pavlo earned his B.S. in Industrial Engineering from West Virginia University and his MBA in Finance from Mercer University.

Bill leads Protiviti’s Tampa Market practice. In this capacity, he oversees client engagements focused on a broad range of operational, technology and compliance risks. His primary areas of focus include corporate governance; business risk management and internal audit services. Bill’s professional experience includes more than 20 years of internal audit, information systems audit and fraud examination services. His experience includes over 12 years in private industry and 8 in public accounting and consulting. Bill is a frequent speaker and author of articles on matters related to corporate governance, risk management and internal auditing. Bill often examines Client continuity plans including tests of operational effectiveness of plans, thoroughness of continuity and disaster recovery preparations and tests of operational effectiveness of plans Bill is the lead executive for providing ERM services for a specialty financial services company in St. Petersburg, FL. Initial work performed included an enterprise-wide risk assessment via facilitated session with the company’s Executive Management team and implementation of the ISO31000 framework. Bill also supervised an engagement to provide advisory oversight of the development of the Firm’s business continuity plans and tests. Bill supervised the evaluation of Business Continuity Plans as part of Internal Audit engagements at numerous clients, covering review of documented plans, adequacy of tests, confirmation that remediation activities were implemented, and reporting of status to Executive Management and the Board.

Todd Webster is an Audit Managing Director with KPMG LLP and is from KPMG’s Tampa, FL office. He recently completed a four year rotation with KPMG’s Department of Professional Practice in New York City where his role was to function as a technical resource for engagement teams in the field who are providing audit services to state and local governments, health care entities, and not-for-profit entities. In July 2014, Todd returned to the Tampa. He has been with KPMG for 13 years, during which time he has primarily served clients in the health care, state and local government, and not-for-profit industries. Prior to joining KPMG, Todd spent 5 years with Arthur Andersen LLP in the audit practice serving clients in a variety of industries. As part of his rotation in NY, Todd served as a GASB Practice Fellow from July 2010 to July 2012. As a practice fellow, Todd was the project manager on GASB Statements No. 60, No. 62, and No. 65, and fielded all technical inquiries related to those Statements. Todd is a Certified Public Accountant in the states of Florida, New York, and North Carolina. He is also a member of the American Institute of Certified Public Accountants and the Florida Institute of Certified Public Accountants.

Todd Webster, CPA KPMG LLP Managing Director

William Thomas, CFE, CIA, CISA, CRMA Protiviti Managing Director

D. Keith Wilson, CPA Public Company Accounting Oversight Board (PCAOB) Deputy Chief Auditor

Brian Wiegmann, CPA PricewaterhouseCoopers LLP Director, Transaction Services- Capital Markets and Accounting Advisory Services

Brian Wiegmann is a Director in PricewaterhouseCoopers' Transaction Services Capital Markets & Accounting Advisory Services group ("TS-CMAAS") in Miami, Florida. He provides accounting advisory services to help clients understand the accounting and financial reporting consequences of complex and sophisticated financial structures employed in mergers, acquisitions, divestitures and financing transactions, while helping clients balance a transaction’s commercial and accounting objectives. Brian also advises clients regarding the impact of new accounting standards and the implementation process. Prior to re-joining TS-CMAAS last year, Brian spent two years as a Director in PwC’s U.S. National Office - Accounting Services Group based in Florham Park, NJ. During his tour with the National Office, Brian focused on a broad array of technical accounting areas but spent a majority of his time on current and future revenue recognition and compensation matters. During his time with TS-CMAAS and the National Office, Brian has also specialized in business combination transactions, fair value accounting, leasing transactions, securitizations, joint ventures and alliances, and consolidation analyses. Brian started his career with PwC in the audit practice, working on utility and other consumer and industrial product services’ companies. Brian has a Master's and Bachelor's in Accounting from the University of Florida, and he is a licensed CPA in Florida and New York.

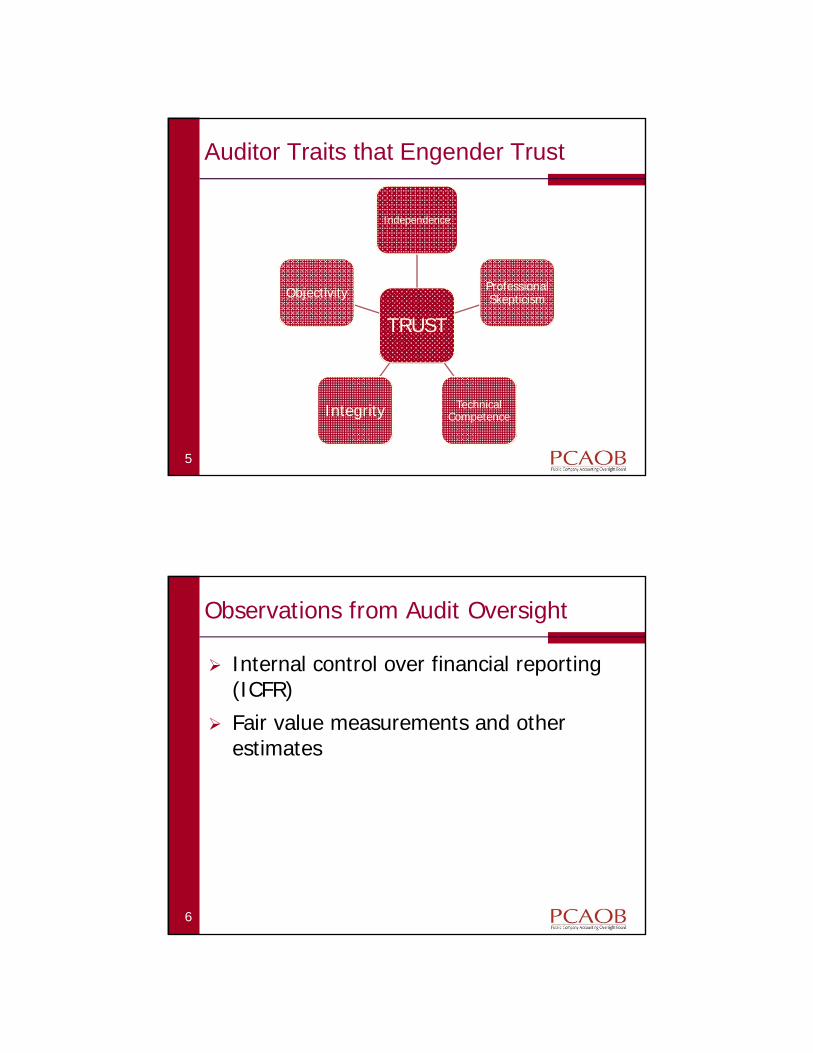

Keith Wilson, CPA, is Deputy Chief Auditor for the Public Company Accounting Oversight Board (PCAOB) in Washington, D.C. He works in the Office of the Chief Auditor, assisting in the development of auditing and related professional practice standards. While at the PCAOB, Mr. Wilson has led a number of standards-related projects, resulting in development of several of the Board's audit and attest standards. He has also been involved in the development of staff guidance addressing topics such as internal control over financial reporting, professional skepticism, and audit risks in certain emerging markets.

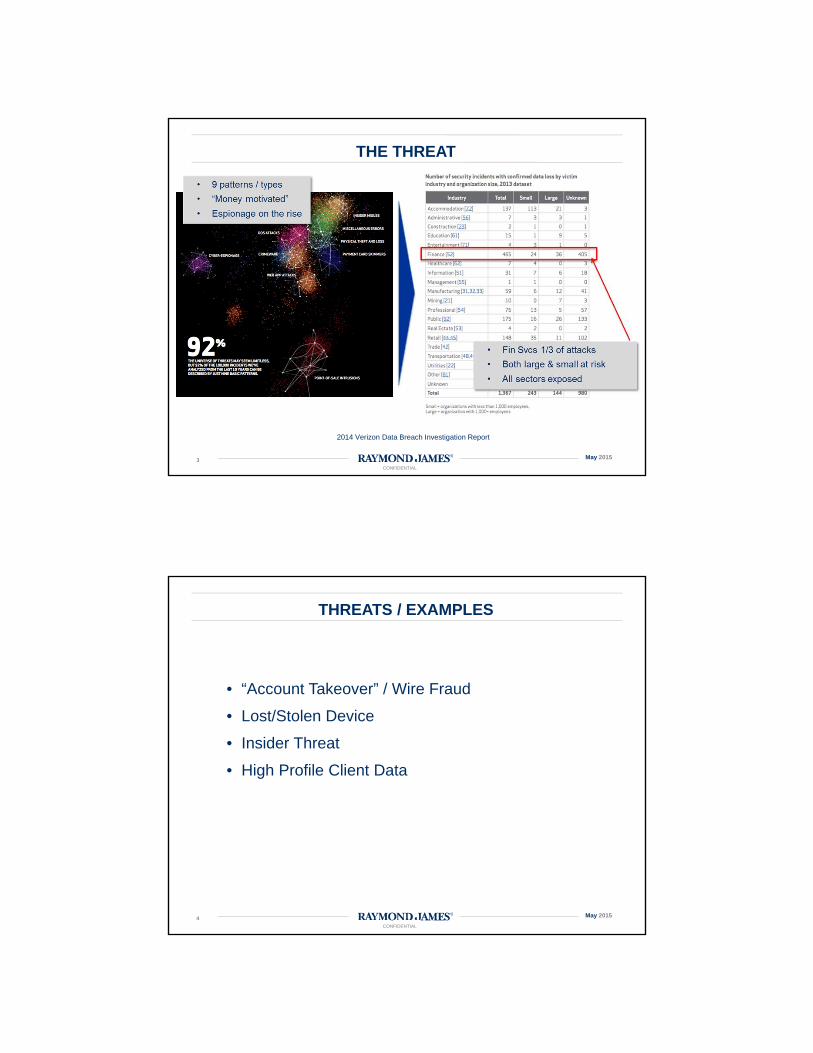

Andy Zolper is Chief Information Security Officer for Raymond James Financial, Inc, a diversified financial services provider with subsidiaries engaged in investment and financial planning, investment banking and asset management. Through its three broker/dealer subsidiaries, Raymond James Financial has more than 6,300 financial advisors serving more than 2.5 million accounts in more than 2,500 locations throughout the United States, Canada and overseas. As CISO, Andy provides strategic direction to identify appropriate security measures, sponsors implementation of security solutions, manages daily security operations, and provides governance to manage technology risk – all in order to help Raymond James achieve its business objectives. Andy was previously at UBS as CISO of its Wealth Management Americas division, and later as global head of IT Risk Management. Prior to joining UBS, he led teams in IT risk management, global program management, and business process reengineering at JPMorgan Chase. Before JPMC, Andy was responsible for application development at Sterling Resources Inc, and developed the company's process reengineering, e-learning and knowledge management software products. Before joining Sterling Resources, Andy served in various management roles at Verizon ranging from staff director of competitive intelligence analysis to field management of "fiber to the curb" deployment. Andy graduated from the Virginia Military Institute. He is a US Marine Corps veteran, having served as a communications and signals intelligence officer. He is a graduate of SIFMA's Securities Industry Institute at The Wharton School, a Registered Operations Professional (Series 99), a certified Six Sigma Black Belt and a Certified Information Security Manager (CISM). He represents Raymond James on the Advisory Council of BITS, the technology policy division of The Financial Services Roundtable, and is a member of SIFMA’s Cyber Security Working Group. Andy lives in St. Petersburg Florida with his wife and five children.

Andy Zolper Raymond James Financial, Inc. SVP and Chief IT Security Officer

This conference is made possible thanks to the

following: USF Lynn Pippenger School of Accountancy

Uday Murthy, Director

Katie Davis, Conference Coordinator

Denise Gelia, Office Staff

Sarah Moyer, Office Staff

Beta Alpha Psi, Delta Gamma Chapter

Accounting Circle Board of Directors

Luke Buzard, TECO Energy, Board Chair

Rachel Hardy, KPMG, CPE Conference Chair

CPE Conference Committee Members

Bryce Faraguna, PwC

Kathy Howe, TECO Energy

Jamil Jones, Deloitte

Cathy Leone, Resources Global Professionals

Lauren Martin, Cherry Bekaert

Jon Minch, Grant Thorton

Tanya Pavlik, 1 Source Partners

Ron Tambasco, True Partners Consulting, LLC

Sponsorship Chairs

Elizabeth Eriksen, Raymond James Financial

Michael Jerman, PwC

Thank you to all of our sponsors!!

Integrating Risk Management and Strategy

Bill ThomasManaging Director

Dan JulevichSenior Director, Internal Audit and

Enterprise Risk Management

2 © 2015 Protiviti Inc. An Equal Opportunity Employer M/F/Disability/Vet. CONFIDENTIAL: This document is for your company's internal use only and may not be copied nor distributed to another third party.

ERM establishes the oversight, control and discipline to drive continuous improvement of an entity’s risk management capabilities in a constantly changing operating environment.

ERM – A Simple Definition

3 © 2015 Protiviti Inc. An Equal Opportunity Employer M/F/Disability/Vet. CONFIDENTIAL: This document is for your company's internal use only and may not be copied nor distributed to another third party.

Enterprise Risk Management

Risk isn’t blameless, but if someone pushes the accelerator…the car doesn’t go on its own

• Review

• Inform

• Advise

• Monitor/Measure

• Control

• Review

• Inform

• Advise

• Monitor/Measure

• Control

ERM Can:

• Initiate

• Decide

• Initiate

• Decide

ERM Can’t :

4 © 2015 Protiviti Inc. An Equal Opportunity Employer M/F/Disability/Vet. CONFIDENTIAL: This document is for your company's internal use only and may not be copied nor distributed to another third party.

Latest News…..Current State of Risk Management…..

AICPA 2015 Report on the Current State of Enterprise Risk Oversight (2/15):

• Maturity of risk oversight has leveled off, with more mature models in public companies and FSI organizations

─ 25% of companies report “complete” ERM processes in place; 52% report status as “not at all” or “minimally” in place

• “Significant” opportunities remain to strengthen approaches to identifying risk and align oversight with strategy

─ 68% of companies report that Boards are “extensively” involved

o Significantly higher for public companies and large organizations

• Risk Oversight leadership is more formalized

─ 32% of companies have a CRO; 56% at FSI companies

─ 45% have a management risk committee

─ 58% have formal risk policies, statements; 48% have explicit guidelines for defining risk (e.g., scales)

AICPA 2015 Report on the Current State of Enterprise Risk Oversight (2/15):

• Maturity of risk oversight has leveled off, with more mature models in public companies and FSI organizations

─ 25% of companies report “complete” ERM processes in place; 52% report status as “not at all” or “minimally” in place

• “Significant” opportunities remain to strengthen approaches to identifying risk and align oversight with strategy

─ 68% of companies report that Boards are “extensively” involved

o Significantly higher for public companies and large organizations

• Risk Oversight leadership is more formalized

─ 32% of companies have a CRO; 56% at FSI companies

─ 45% have a management risk committee

─ 58% have formal risk policies, statements; 48% have explicit guidelines for defining risk (e.g., scales)

5 © 2015 Protiviti Inc. An Equal Opportunity Employer M/F/Disability/Vet. CONFIDENTIAL: This document is for your company's internal use only and may not be copied nor distributed to another third party.

Latest News…..

2015 Protiviti NC State’s ERM Initiative noted…..

• Sudden changes remind us that risk assessment and scenario planning and are crucial…what’s emerged……

─ Cyber risk and related Reputation Risk Management

─ Commodity price fluctuations(e.g., oil)

─ Currency instability

• Maybe we missed a few things we thought we understood…..

─ Geopolitical “hot spots” in areas previously thought to be stable

─ Renewed focus on business relationships and vendor risk management

─ Regulation and increasing enforcement activities

2015 Protiviti NC State’s ERM Initiative noted…..

• Sudden changes remind us that risk assessment and scenario planning and are crucial…what’s emerged……

─ Cyber risk and related Reputation Risk Management

─ Commodity price fluctuations(e.g., oil)

─ Currency instability

• Maybe we missed a few things we thought we understood…..

─ Geopolitical “hot spots” in areas previously thought to be stable

─ Renewed focus on business relationships and vendor risk management

─ Regulation and increasing enforcement activities

6 © 2015 Protiviti Inc. An Equal Opportunity Employer M/F/Disability/Vet. CONFIDENTIAL: This document is for your company's internal use only and may not be copied nor distributed to another third party.

Latest News…..What Does the Board Think?

• 48.2% of boards assign risk oversight to the audit committee; 33.9% assign risk oversight to the full board

• 51.5% of directors indicated that the full board should have primary responsibility for risk oversight

Source: 2014-15 NACD Public Company Governance Survey

• 72% of directors are “very confident” they can monitor operational risk and internal fraud.

• 15% of directors are “very confident” they can monitor cyber risk (gulp).

Source: Corporate Board Member Magazine, First Quarter 2015 “What Directors Think”

• 48.2% of boards assign risk oversight to the audit committee; 33.9% assign risk oversight to the full board

• 51.5% of directors indicated that the full board should have primary responsibility for risk oversight

Source: 2014-15 NACD Public Company Governance Survey

• 72% of directors are “very confident” they can monitor operational risk and internal fraud.

• 15% of directors are “very confident” they can monitor cyber risk (gulp).

Source: Corporate Board Member Magazine, First Quarter 2015 “What Directors Think”

7 © 2015 Protiviti Inc. An Equal Opportunity Employer M/F/Disability/Vet. CONFIDENTIAL: This document is for your company's internal use only and may not be copied nor distributed to another third party.

A Multiple Lines of Defense Model Can Clarify Everyone’s Role…

The board and CEO must have mutual understanding of the value contributed by the independent function with the intent of preserving its independent role within the organization

Positioning of risk management/compliance functions entails several important principles:

• Viewed as a peer with business line leaders

• Direct reporting line to the CEO

• Reporting line to the board or a committee of the board with no access constraints

• Mandatory and regularly scheduled executive sessions with the board or a board committee

• Formalized escalation process should exist

In summary, clearly defined positioning of these functions and how they interface with business management

Positioning of risk management/compliance functions entails several important principles:

• Viewed as a peer with business line leaders

• Direct reporting line to the CEO

• Reporting line to the board or a committee of the board with no access constraints

• Mandatory and regularly scheduled executive sessions with the board or a board committee

• Formalized escalation process should exist

In summary, clearly defined positioning of these functions and how they interface with business management

8 © 2015 Protiviti Inc. An Equal Opportunity Employer M/F/Disability/Vet. CONFIDENTIAL: This document is for your company's internal use only and may not be copied nor distributed to another third party.

Getting to the Core of Risk Management

What we don’t know may be more important than what we do know

9 © 2015 Protiviti Inc. An Equal Opportunity Employer M/F/Disability/Vet. CONFIDENTIAL: This document is for your company's internal use only and may not be copied nor distributed to another third party.

Are We Flying Blind, But We Just Don’t Know It Yet?

Adapting is a game every organization must play to be successful in a rapidly changing business environment

Think about it! What will be the effect of:

“Everyone has a plan until they get punched in the mouth.”Mike Tyson, Former Heavyweight Champion

• Disruptive technological developments?

─ Consolidation to create friendlier, more intelligent devices─ Increased mobile connectivity. bigger/thinner TVs, 3D displays and

speech recognition ─ Hybrids in automotive industry─ Solar energy in the power industry─ Bandwidth availability

• Disruptive market forces?

─ Significant demographic changes─ Political and social instability─ Increased regulation

• Emerging new and/or unexpected threats?

─ Cybersecurity issues─ Catastrophic natural disasters─ Terrorist events like 9/11

10 © 2015 Protiviti Inc. An Equal Opportunity Employer M/F/Disability/Vet. CONFIDENTIAL: This document is for your company's internal use only and may not be copied nor distributed to another third party.

11 © 2015 Protiviti Inc. An Equal Opportunity Employer M/F/Disability/Vet. CONFIDENTIAL: This document is for your company's internal use only and may not be copied nor distributed to another third party.

Enabling activities to operationalize ERM

ERM Framework

12 © 2015 Protiviti Inc. An Equal Opportunity Employer M/F/Disability/Vet. CONFIDENTIAL: This document is for your company's internal use only and may not be copied nor distributed to another third party.

Limitations in the Time-Honored Risk Map…

Risk maps, heat maps and risk rankings based on subjective assessments of severity and likelihood of occurrence often leave an organization with a list of risks and little insight as to what to do next

PROS

• Provide an overall picture

• Seems simple and understandable enough

• Some view it as a rough risk profile

CONS

• A common complaint: Rarely surfaces an “aha”

• Qualitative descriptions of severity/likelihood are understood differently by different people

• Intersections on map are mean averages of widely dispersed views

• Subjects risks with different characteristics, including time horizon, to a common grid

• Doesn’t consider speed to impact and response readiness

• Doesn’t consider the complexities of the extended enterprise

13 © 2015 Protiviti Inc. An Equal Opportunity Employer M/F/Disability/Vet. CONFIDENTIAL: This document is for your company's internal use only and may not be copied nor distributed to another third party.

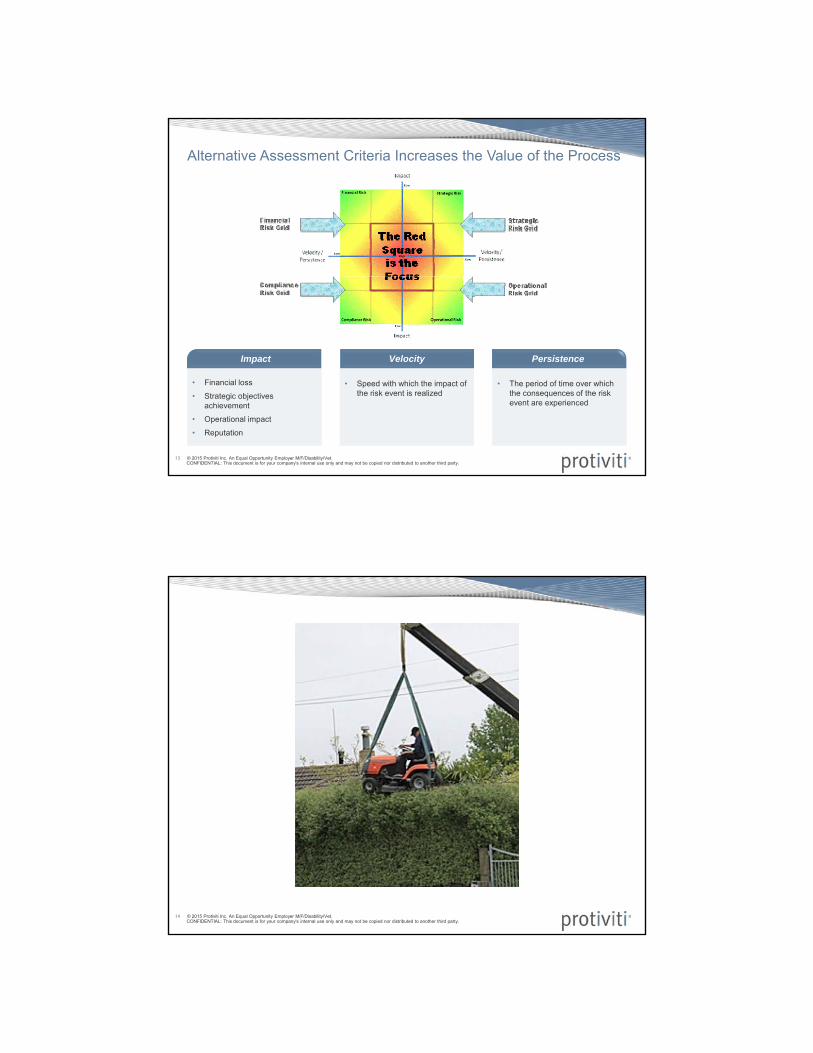

Alternative Assessment Criteria Increases the Value of the Process

• Financial loss

• Strategic objectives achievement

• Operational impact

• Reputation

• Financial loss

• Strategic objectives achievement

• Operational impact

• Reputation

Impact

• Speed with which the impact of the risk event is realized

• Speed with which the impact of the risk event is realized

Velocity

• The period of time over which the consequences of the risk event are experienced

• The period of time over which the consequences of the risk event are experienced

Persistence

14 © 2015 Protiviti Inc. An Equal Opportunity Employer M/F/Disability/Vet. CONFIDENTIAL: This document is for your company's internal use only and may not be copied nor distributed to another third party.

15 © 2015 Protiviti Inc. An Equal Opportunity Employer M/F/Disability/Vet. CONFIDENTIAL: This document is for your company's internal use only and may not be copied nor distributed to another third party.

Risk Management Concepts

Risk Culture:

“set of encouraged and acceptable behaviors, discussions, decisions and

attitudes toward taking and managing risk within an institution.”

Source: Risk Management Association

16 © 2015 Protiviti Inc. An Equal Opportunity Employer M/F/Disability/Vet. CONFIDENTIAL: This document is for your company's internal use only and may not be copied nor distributed to another third party.

17 © 2015 Protiviti Inc. An Equal Opportunity Employer M/F/Disability/Vet. CONFIDENTIAL: This document is for your company's internal use only and may not be copied nor distributed to another third party.

Themes of Successful Risk Cultures

High-level executive involvement and support vital

ERM lead is independent, supported by small, focused group

ERM lead drives the process, business units own risk and IA validates

Proactive emphasis

Consistency of risk language/frameworks important

Integration with core management activities a key success factor

Board risk oversight driven by broader Board participation

18 © 2015 Protiviti Inc. An Equal Opportunity Employer M/F/Disability/Vet. CONFIDENTIAL: This document is for your company's internal use only and may not be copied nor distributed to another third party.

Components of an Effective Risk Culture

Does your culture support your words regarding risk management?Does your culture support your words regarding risk management?

• High Impact “Top to Bottom” Message

• Consistent Messages

• Open Discussion on Risk, Compliance, Behavior

• High Impact “Top to Bottom” Message

• Consistent Messages

• Open Discussion on Risk, Compliance, Behavior

Tone

• Alignment of “subcultures”

• Reinforcement

• Prioritization of Risk Culture

• Alignment of “subcultures”

• Reinforcement

• Prioritization of Risk Culture

Drivers

• Stated Values, Codes

• Ethics Program

• Clear Oversight and Communications

• Stated Values, Codes

• Ethics Program

• Clear Oversight and Communications

Tangibles

• Experienced Values

• Belief Systems

• Risk Taking Behaviors and Warning Signs

• Experienced Values

• Belief Systems

• Risk Taking Behaviors and Warning Signs

Intangibles

19 © 2015 Protiviti Inc. An Equal Opportunity Employer M/F/Disability/Vet. CONFIDENTIAL: This document is for your company's internal use only and may not be copied nor distributed to another third party.

Man Versus Geological Time…Commentary on Risk Culture?

Strategy for a Utility: Operate a nuclear power station in Japan near a quake zone by the ocean located up a bluff between 14 and 23 feet above sea level

Key Assumptions

Presume a worst case scenario of an earthquake causing a tsunami of more than 20 feet as extremely low risk

Contrarian Statement

A 40+ foot tsunami hits the plant location site, a 1,000 year event based on geological studies

Implication Statement

Evaluate the plant’s safety planning in light of a catastrophic tsunami scenario, including its back-up power facilities for avoiding a fatal loss of power

20 © 2015 Protiviti Inc. An Equal Opportunity Employer M/F/Disability/Vet. CONFIDENTIAL: This document is for your company's internal use only and may not be copied nor distributed to another third party.

Decision-makers use their best and informed judgment to take risks. When the potential effect is outside their authority level, they escalate the decision to more senior management – in the same way they make purchasing decisions.

The consideration of risk is an integral and essential element of decision-making and management in general. It is not a separate discipline.

Management considers the potential risks introduced to other departments/business units when considering changes to its processes.

Management shares the kind of information that signals risk events which allows the company to resolve emerging issues before they become crises.

Management recognizes that when they make decisions they have to consider what might happen (i.e., the risk), assess it (upside and downside), and if it is at an unacceptable level, act to modify it.

Management accountability for risks and risk mitigation is clearly established.

Risk management is embedded in processes and strategies.

Management has an adequate respect for risk. Risk management requirements are neither too lax nor too stringent.

The Senior Executive Team establishes a culture that values employees who proactively identify risks and/or potential issues.

Measuring Risk Culture…9 Statements to Consider

21 © 2015 Protiviti Inc. An Equal Opportunity Employer M/F/Disability/Vet. CONFIDENTIAL: This document is for your company's internal use only and may not be copied nor distributed to another third party.

22 © 2015 Protiviti Inc. An Equal Opportunity Employer M/F/Disability/Vet. CONFIDENTIAL: This document is for your company's internal use only and may not be copied nor distributed to another third party.

…is the most difficult task of risk management and internal control

Managing Tension Between Value Creation and Protection

For risk management and internal control to function when a crucial decision-making moment arises, directors and executive management must be committed to making it work

1

Aligning the governance process, risk management and internal control toward striking the appropriate balance is crucial in this regard

2

The objective is to balance the entrepreneurial activities and control activities of the organization so that neither one is too disproportionately strong relative to the other

3

This task is fundamental to managing risk culture

4

23 © 2015 Protiviti Inc. An Equal Opportunity Employer M/F/Disability/Vet. CONFIDENTIAL: This document is for your company's internal use only and may not be copied nor distributed to another third party.

Risk Management Concepts

A risk appetite statement is a guidepost to management and the board of directors of the core risk strategy arising from the strategy-setting process”

“Would you tell me, please, which way I ought to go from here?""That depends a good deal on where you want to get to.""I don't much care where –""Then it doesn't matter which way you go.”

- Alice in Wonderland

24 © 2015 Protiviti Inc. An Equal Opportunity Employer M/F/Disability/Vet. CONFIDENTIAL: This document is for your company's internal use only and may not be copied nor distributed to another third party.

Risk Appetite Statement Objectives

COMMUNICATE, REVISIT AND REVISE!

Risk appetite is a deceivingly complex topic and challenge for organizations to establish. Taking an objectives based approach may help you get there.

Risk appetite is a deceivingly complex topic and challenge for organizations to establish. Taking an objectives based approach may help you get there.

Risk Appetite

Risk Tolerances

Define what risk appetite means to the organization.Communicate the level of risk the organization is willing to take in the pursuit of strategic objectives.Link to strategic planning and priorities.Establish why the organization is developing a risk appetite statementAlign with enterprise risk managementMeet regulatory requirements

Define what risk appetite means to the organization.Communicate the level of risk the organization is willing to take in the pursuit of strategic objectives.Link to strategic planning and priorities.Establish why the organization is developing a risk appetite statementAlign with enterprise risk managementMeet regulatory requirements

Strategy

Risk Appetite

25 © 2015 Protiviti Inc. An Equal Opportunity Employer M/F/Disability/Vet. CONFIDENTIAL: This document is for your company's internal use only and may not be copied nor distributed to another third party.

It’s a Wrap….

Sooner or later, something fundamental in your business world will change

• ERM can be central to knowing when to change Strategy

The ERM structure really matters

Boards look to ERM to enable Risk Oversight

Consider innovative ways to evaluate risk

• Your risk profile is unique

Support an effective risk culture, and,

Whatever you do, don’t do this.....

26 © 2015 Protiviti Inc. An Equal Opportunity Employer M/F/Disability/Vet. CONFIDENTIAL: This document is for your company's internal use only and may not be copied nor distributed to another third party.

27 © 2015 Protiviti Inc. An Equal Opportunity Employer M/F/Disability/Vet. CONFIDENTIAL: This document is for your company's internal use only and may not be copied nor distributed to another third party.

Q&A

28 © 2015 Protiviti Inc. An Equal Opportunity Employer M/F/Disability/Vet. CONFIDENTIAL: This document is for your company's internal use only and may not be copied nor distributed to another third party.

Confidentiality Statement and Restriction for Use

This document contains confidential material proprietary to Protiviti Inc. ("Protiviti"), a wholly-owned subsidiary of Robert Half ("RHI"). RHI is a publicly-traded company and as such, the materials, information, ideas, and concepts contained herein are non-public, should be used solely and exclusively to evaluate the capabilities of Protiviti to provide assistance to your Company, and should not be used in any inappropriate manner or in violation of applicable securities laws. The contents are intended for the use of your Company and may not

be distributed to third parties.

Revenue Recognition:Where to Start

Presented by:

Brad Hale, Managing Director & Shareholder,

CBIZ MHM

Today’s AgendaBackground

The Business Side

Topic 606 - High level overview

Example: Software Company

Transition Resource Group

1

2

3

4

5

Background

Reasons for the New GuidanceThe FASB and the IASB initiated a joint project to clarify the principles for recognizing revenue and to develop a common revenue standard for U.S. GAAP and IFRS that would:

1.Remove inconsistencies and weaknesses in existing revenue recognition standards and practices. U.S. GAAP has a multitude of Industry and transaction specific standards. IFRS has two standards on Revenue Recognition IAS 11 and IAS 18.

2.Provide a more robust framework for addressing revenue recognition issues. Weaknesses exist in both set of standards.

3.Improve comparability of revenue recognition practices across entities, industries, jurisdictions and capital markets.

4.Simplify the preparation of financial statements by reducing the number of requirements to which entities must refer.

The Business Side

Example• Company X contracts with a customer to build a new

building for $1 million on 12/1/2014. Company X has completed two similar buildings in this area.

• If construction is completed in 6 months, Company X receives a $300,000 bonus.

• If construction goes beyond 6 months, Company X gets no bonus.

Guidance: To include variable consideration in the estimated transaction price, the entity has to conclude that it is probable that a significant revenue reversal will not occur in future periods.

Industries Subject to Largest ImpactThose entities that are currently subject to significant industry

guidance are likely to experience the most significant impact.• Telecommunication

• Software

• Construction/Aerospace and Defense

• Real Estate

• Entertainment and Media

• Multiple Deliverable Contracts

Impact will be Far-reaching within the 4 WallsThe impact from the adoption of the new revenue recognition standard will likely be complex and far-reaching and involve many different functions within an organization.

• Information systems may require adjustment

• Standard “sales” contracts and other sales agreements should be evaluated in light of the changes

• Sales incentives/commissions should be considered

• Internal control processes may need updating

• Executive compensation arrangements

• Debt covenants

• Tax implications

• Supply chain

Impact will be Far-reaching outside the 4 WallsThe impact from the adoption of the new revenue recognition standard will likely be complex and far-reaching and involve many different players outside an organization.

• Attorneys• Drafting of contracts, purchase agreements, compensation agreements

• Bankers• Covenant reporting

• Underwriting

• Transaction Advisors• Diligence on assumptions

• Investors• Understanding areas of judgment

• Assessing comparability

Topic 606- High level overview

Core principle: The core principle of the guidance is that an entity should recognize revenue to depict the transfer of promised goods, or services, to customers in an amount that reflects the consideration to which the entity expects to be entitled, in exchange for those goods or services.

Five steps to apply the core principle:1. Identify the contract(s) with a customer2. Identify the performance obligations in the contract3. Determine the transaction price4. Allocate the transaction price to the performance obligations in the

contract5. Recognize revenue when (or as) the entity satisfied a performance

obligation

Core Principle and the Five Step Process:Basic Observations

• On the surface the five step process does not seem overly complex and arguably, it appears to include much of what is currently done to determine revenue recognition.

• However, each of the five steps will require significant judgments by management and auditor in applying the underlying principles included in the new guidance.

• The transfer of “control” to the customer becomes the driving issue in evaluating the appropriateness of revenue recognition under the new guidance.• Currently, the evaluation of “risk and reward” often drives the

determination of revenue recognition. While it remains an important consideration, it is no longer determinant under the new guidance.

1. Identify the Contract with the CustomerA contract is an agreement between two or more parties that creates enforceable rights and obligations.

• The entity can identify the payment terms for the goods or services to be transferred.

• The contract has commercial substance (that is, the risk, timing, or amount of the entity’s future cash flows is expected to change as result of the contract).

• It is probable that the entity will collect the consideration to which it will be entitled in exchange for the goods or services that will transferred to the customer.

The Five Step Process

2. Identifying Performance ObligationsA performance obligation is a promise in a contract with a customer to transfer to the customer:

• A good or service (or bundle of goods or services) that is distinct.

• A series of distinct goods or services that are substantially the same and that have the same pattern of transfer to the customer.

Generally explicit but may also include promises that are implied by an entity’s customary business practices, published policies or specific statements, if at the time of entering into the contract those promises create a valid expectation of the customer that the entity will transfer a good or service to the customer.

The Five Step Process

2. Identifying Performance ObligationsA promised good or service is considered distinct if both of the following conditions are met:

• The customer can benefit from the good or service either on its own or together with other resources that are readily available to the customer (that is, the good or service is capable of being distinct).

• The entity’s promise to transfer the good or service to the customer is separately identifiable from other promises in the contract (that is, the good or service is distinct within the context of the contract).

The Five Step Process

3.Determining the Transaction PriceThe transaction price is the amount of consideration that an entity expects to be entitled to in exchange for transferring promised goods or services to a customer. Issues that impact the determination of the transaction price include the following:

• Fixed consideration

• Variable consideration

• Constraining estimates of variable consideration

• The existence of a significant financing component in the contract

• Non cash consideration

• Consideration payable to a customer

The Five Step Process

4. Allocating the Transaction Price The objective when allocating the transaction price is for an entity to allocate the transaction price to each performance obligation (or distinct good or service) in an amount that depicts the amount of consideration which the entity expects to be entitled in exchange for transferring the promised goods or services to the customer.

To meet the allocation objective, an entity shall allocate the transaction price to each performance obligation in the contract on a relative stand-alone selling price basis.

• Relative selling price is best evidenced by the observable price of a good or service when sold separately in similar circumstances and to similar customers.

• If a stand-alone selling price is not directly observable, an entity shall estimate the standalone selling price.

The Five Step Process

4. Allocating the Transaction Price When estimating the relative stand-alone selling price, management should maximize the use of observable inputs. The following are some possible estimation methods (not all inclusive):

• Adjusted market assessment approach

• Expected cost plus a margin approach

• Residual approach (in certain circumstances)

The Five Step Process

5. Recognize Revenue When a Performance Obligation is SatisfiedAn entity shall recognize revenue when (or as) the entity satisfies a performance obligation by transferring a promised good or service (that is, an asset) to a customer. An asset is transferred when (or as) the customer obtains control of that asset.

• Control of an asset refers to the customer’s ability to direct the use of and obtain substantially all of the remaining benefits from the asset. Indicators that a customer has obtained control are as follows:

• The entity has a right to payment for the asset

• The entity transferred legal title to the asset

• The entity transferred physical possession of the asset

• The customer has the significant risk and reward of ownership

• The customer has accepted the asset

The Five Step Process

5. Recognize Revenue When a Performance Obligation is SatisfiedPerformance Obligations Satisfied Over Time

• An entity transfers control of a good or service over time and, therefore, satisfies a performance obligation and recognizes revenue over time if one of the following criteria are met:• The customer simultaneously receives and consumes the benefits

provided by the entity’s performance as the entity performs.

• The entity’s performance creates or enhances an asset (WIP) that the customer controls as the asset is created or enhanced.

• The entity’s performance does not create an asset with an alternative use to the entity and the entity has a right to payment for performance completed to date.

The Five Step Process

5. Recognize Revenue When a Performance Obligation is SatisfiedPerformance Obligations Satisfied at a Point in Time

• If a performance obligation is not satisfied over time, an entity satisfies the performance obligation at a point in time. The specific point in time is dependent on when the customer obtains control of the promised asset and the entity satisfies the performance obligation.

The Five Step Process

The objective of the disclosure requirements (Topic 606) is for an entity to disclose sufficient information to enable users of financial statements to understand the nature, amount, timing, and uncertainty of revenue and cash flows arising from contracts with customers.

• The disclosure requirements found in the new revenue recognition guidance are significantly in excess of what is currently required under U.S. GAAP.

Disclosures

An entity shall disclose qualitative and quantitative information about all of the following:

• Its contracts with customers

• The significant judgments, and changes in the judgments made in applying the guidance in Topic 606 to those contracts

• Any assets recognized from the costs to obtain or fulfill a contract with a customer

Disclosures

Example: Software Company

• Derives its revenues primarily from the sale of perpetual software licenses and related services.

• Most contracts are sold in combination with a service license agreement to provide customer support and maintenance services (post-contract customer support or “PCS”), which usually includes software updates.

• PCS provides customers with rights to unspecified software updates that the Company chooses to provide on a when and if available basis.

• VSOE has not been established as products/services are not sold separately.

Example: Software Company

• Current GAAP• ASC 985-605-25-70: If sufficient vendor-specific objective

evidence does not exist to allocate the fee to the separate elements and the only undelivered element is postcontractcustomer support, the entire arrangement fee shall be recognized ratably over either of the following:

a. The contractual postcontract customer support period for those arrangements with explicit rights to postcontract customer support

• Revenue for the perpetual licenses is recognized on a straight-line basis over the service contract term

Example: Software Company

2. Identifying Performance Obligations(1) Software license

(2) Technical support

(3) Software updates on an if-and-when available basis

Note: In practice software updates may or may not be a separate performance obligation. In some circumstance they may be considered a single performance obligation with technical support, or as a product warranty, which is not a separate performance obligation.

Example: Software Company

3.Determining the Transaction Price• Fixed consideration – Contract price

• Variable consideration – N/A

• Constraining estimates of variable consideration – N/A

• The existence of a significant financing component in the contract – N/A

• Non cash consideration – N/A

• Consideration payable to a customer – N/A

Example: Software Company

4. Allocating the Transaction Price Determine standalone selling price to calculate allocation of transaction price:

(1) Software license – 70%

(2) Technical support – 20%

(3) Software updates on an if-and-when available basis – 10%

• In practice many companies will account for technical support and software updates as “combined” performance obligations because they will be recognized ratably over the length of the support period.

• However, in some cases the software updates may be recognized over time by a different measure, for instance if an entity almost always releases a software update in November, then the transaction price allocated to the “if-and-when” available update may be recognized ratably each November.

Example: Software Company

5. Recognize Revenue When a Performance Obligation is Satisfied(1) Software license

• Recognition would be upfront for 70% of the transaction price when the customer obtains the software and has the right to use it.

(2) Technical support and (3) if-and-when available software updates

• 30% of the transaction price is recognized ratably over the period that support is provided per the terms of the contract.

Example: Software Company

Transition Resource Group

Effective Date of Adoption (Based upon FASB Exposure Draft)• Public Entities

• Annual reporting periods beginning after December 15, 2017, including interim periods within that reporting period.

• Nonpublic Entities• Annual reporting periods beginning after December 15, 2018

and interim periods within annual periods beginning after December 15, 2019

Early adoption by both public and nonpublic entities as early as original public adoption date (annual reporting periods beginning after December 15, 2016 and interim periods therein).

THE ACCOUNTING CIRCLE - USF

Will Congress Grant the States Remote Seller Collection Authority?

Fred Nicely, Council On State Taxation

May 28, 2015

Agenda

• Why The Fuss?

• History – Timeline

• Post Quill - States’ Self-Help Measures

• Dormant Commerce Clause and Due Process Clause

• Colorado’s Notification and Reporting LAw

• States and Businesses work on Streamlined Sales & Use Tax Agreement

• Federal Legislation Initiatives

2

Why All The Fuss

3

Why All The Fuss?

• 45 states plus District of Columbia impose sales and use taxes• Over 9,000 local jurisdictions – administered by the state except in AL, AZ, CO and LA• Retailers required to collect and remit sales tax to states where retailer has physical presence (Quill v. North Dakota)• Use tax is owed by consumer when retailer does not collect the sales tax

Why All The Fuss?

It’s All About the Money:

• Brick-N-Click collecting tax in all states where present – losing sales to Internet sellers• Small sellers losing sales to Internet retailers• State and local governments:

• Do not want to audit consumers (i.e., voters) • Need revenue

• Dr. Fox study in 2009 estimated by 2012 states would lose a combined $11.2 billion in uncollected sales/use tax revenue from electronic commerce

Historical Timeline

6

1921 – WV imposes first sales tax

1933 – Depression era – 11 states enact sales/use taxes

1944 – Early US SCt cases (McLeod, General Trading & Int’l Harvester)

1954 – Miller Bros.

1960 – Scripto

1967 – Nat’l Bellas Hess

1977 – Complete Auto

1992 – Quill

1994 – DMA talks

Timeline of Sales Tax Nexus Developments

1998 – ITFA enacted, creating ACEC

1999 – NTA Electronic Commerce Tax Project Final Report

2000 – ACEC recommendations; SSTP forms; Federal SST proposals

2002 – SSUTA adopted

2005 – SST Governing Board formed

2011 – Federal legislation proposed bypassing SSUTA

2013 – Marketplace Fairness passes U.S. Senate

2015 – DMA decision – Justice Kennedy questions Quill

Timeline of Sales Tax Nexus Developments

Dormant Commerce Clause and Due Process Clause

9

Distinguishing The Commerce Clause

• The Congress shall have power “to regulate Commerce…among the several States”• Focus is discrimination against and burden on commerce, versus

Due Process focus on protection of individual rights

• Complete Auto, 430 U.S. 274 (1977)• Substantial Nexus

• Non-Discriminatory (against interstate commerce)

• Fairly Apportioned• Internal Consistency

• External Consistency (not arbitrary)

• Fairly Related to Services Provided (not one-to-one relationship)

Due Process and Commerce Clause Tests Distinguished

• Quill Corp. v. North Dakota, 504 U.S. 298 (1992)

- Due Process Clause nexus ("minimum contacts") is different from Commerce Clause nexus ("substantial nexus")

- Due Process Clause – Fundamental fairness as interpreted by the U.S. Supreme Court (not Congress)

- Commerce Clause nexus, at least with sales/use taxes, requires physical presence

- Commerce Clause – Subject to Congressional oversight

Page 11

Daimler AG v. Bauman, 134 S. Ct. 746 (2014).

• Conduct of U.S. sub on behalf of foreign parent corporation does not create

general jurisdiction over foreign corporation

Goodyear Dunlop Tires v. Brown, 131 S. Ct. 2846 (2011).

• No general jurisdiction over foreign subs of U.S. parent corporation because

subs lacked “continuous and systematic general business contacts” with

forum state.

J. McIntyre Machinery, Ltd. v. Nicastro, 131 S. Ct. 2780 (2011).

• Lead opinion says defendant must “purposefully avail itself of the privilege of

conducting activities within the forum state, thus invoking the benefits and

protections of its laws.”

Walden v. Fiore, 134 S. Ct. 1115 (2014).

• Two professional gamblers could not force defendant to litigate in NV for

alleged conduct that took place in GA even though the conduct impacted

defendants in forum state.

Nexus: Don’t Forget the Due Process Clause

Post Quill -States’ Self-Help Measures

13

States’ “Self-Help” Legislative Efforts

States’ efforts to force remote vendors to collect sales tax:

• Use Tax 1099-like Information Reporting (CO & NC)

• Amazon Laws NY’s 2008 law: Click-through nexus statutes(agreement with resident to refer customers via an internet link orotherwise) and rebuttable presumption of nexus

• Affiliate Nexus Laws [MTC Model Statute based on CA]

• In-State Delivery Arrangements: Arrangements, with other than acommon carrier, to facilitate delivery of property to in-state customerat an in-state location

• Indiana 2014 proposed legislation (did not pass)

States’ “Self-Help” Legislative Efforts

States’ efforts to force remote vendors to collect sales tax:

• Use Tax Notification: Requirement to notify customers ofrequirement to report use tax (e.g., CO, KY & OK)

• Warranty Nexus: In-state contractors performing warranty &repair work

• Marketplace Facilitator – New York (recently rejected) andWashington (HB 2224) have proposals to attribute nexus if salesmade through a facilitator (e.g. E-Bay)

• Credit Card Processor - Washington has proposed legislationthat would assert nexus from the use of a credit card processor orother payment facilitator (HB 2224)

• Factor Nexus – Washington also has proposed legislation torequire remote sellers with more than $267k in sales to collect

Agency Litigation

• Scripto

• Tyler Pipe

• Teachers as Agents – Scholastic & Troll Cases• CA, CT, KS and TN have found nexus; AR, MI and Ohio have not

• Most Recent – Internet Links• Click-through laws talk about “affiliates” but really asserting an

agency relationship

• Passive solicitation (advertising) v. active solicitation (door-to-door)

• Law held by New York’s highest court not to be facially unconstitutional (versus “as applied”)

• Amazon.com

• Overstock.com

16

Click-Through Nexus Laws – Part 1

State Effective Date Affiliate Threshold Statute

AR (rebuttable presumption) Oct. 24, 2011 More than $10,000 Ark. Code Ann. § 26-52-117

CA (rebuttable presumption) Sept. 15, 2012 More than $10,000 (and more than $1 million in annual in-state sales)

Cal. Rev. & Tax. § 6203(c)

CT (irrebuttable presumption) July 1, 2011 More than $2,000 Conn. Gen. Stat. § 12-407(a)(12)(L)

GA (rebuttable presumption) Oct. 1, 2012 More than $50,000 Ga. Stat. Ann. § 48-8-2(8)(K)

IL (now rebuttable) July 1, 2011; Jan. 1, 2015 More than $10,000 35 ILCS 105/2 and 110/2; amended by 2014 IL SB 352

KS (rebuttable presumption) July 1, 2013 More than $10,000 K.S.A. 79-3702(C)

LA (rebuttable presumption) Not Passed - pending More than $50,000 HB 355 (Only passed House W&M)

ME (rebuttable presumption) Oct. 9, 2013 More than $10,000 Me. Rev. Stat. Ann. § 1754-B(1-A)(C)

MI (rebuttable presumption) Oct. 1, 2015 More than $10,000 (and more than $50,000 in annual in-state sales)

Mich. Comp. Laws § 205.52b

MN (rebuttable presumption) July 1, 2013 More than $10,000 Minn. Stat. § 297A.66(4a)

Click-Through Nexus Laws – Part 2State Effective Date Affiliate Threshold Statute

MO (rebuttable presumption) Aug. 28, 2013 More than $10,000 Mo. Rev. Stat. § 144.605(2)(e)

NV (rebuttable presumption) Not Passed - pending More than $10,000 SB 382 – only introduced

NJ (rebuttable presumption) July 1, 2014 More than $10,000 N.J. Rev. Stat. § 54:32B-2

NY (rebuttable presumption) June 1, 2008 More than $10,000 N.Y. Tax Law § 1101(b)(8)(vi)

NC (rebuttable presumption) Aug. 7, 2009 More than $10,000 N.C. Gen. Stat. § 105-164.8

PA Reg. Sept. 1, 2012 None specified Tax Bulletin 2011-01; proposed legislation in 2013 (HB 1043) did not pass

RI (rebuttable presumption) July 1, 2009 More than $5,000 R.I. Gen. Laws § 44-18-15

TN (rebuttable presumption) July 1, 2015 More than $10,000 HB 644 – pending Gov. signature

VT (rebuttable presumption) When adopted in 15 other states. More than $10,000 Vt. Stat. Ann. tit. 32, § 9701(9)(I) (H.B. 436)

WA (?) Not Passed - pending More than $10,000 (or factor nexus w/$267,000 WA sales)

HB 2224 (Pending in House Finance)

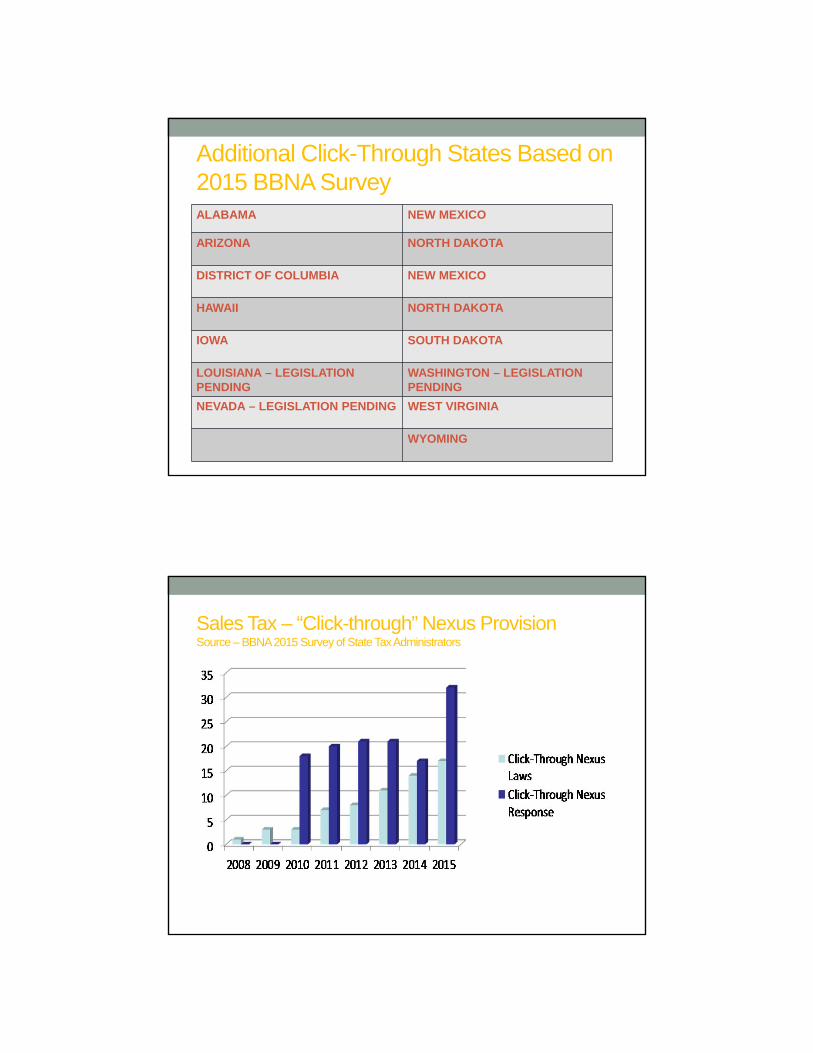

Additional Click-Through States Based on 2015 BBNA SurveyALABAMA NEW MEXICO

ARIZONA NORTH DAKOTA

DISTRICT OF COLUMBIA NEW MEXICO

HAWAII NORTH DAKOTA

IOWA SOUTH DAKOTA

LOUISIANA – LEGISLATION PENDING

WASHINGTON – LEGISLATION PENDING

NEVADA – LEGISLATION PENDING WEST VIRGINIA

WYOMING

Sales Tax – “Click-through” Nexus Provision Source – BBNA2015 Survey of State Tax Administrators

Click-Through/Remote Nexus Litigation

• Performance Marketing Ass’n, Inc. v. Hamer (Ill. Cir. Ct., Cook County 2012)

• The Cook County Circuit Court held Illinois' "Amazon" law violated the Commerce Clause and the Internet Tax Freedom Act ("ITFA")• Held that the law violated the Commerce Clause

because it required retailers with no substantial nexus to register and collect sales and use taxes

• Also held that the law violated the ITFA as a "discriminatory tax" on e-commerce

• The Illinois Supreme Court affirmed the decision without addressing the Commerce Clause – dissent argued the Court should have addressed the Commerce Clause

• Illinois changed its law and it now: 1) applies to more than just Internet links and 2) has a rebuttable presumption

21

Fairly Recent Legislation – Nexus Presumed created by Commonly Owned “Affiliate”

5% direct or indirect ownership• NY (2009)

Parent/Sub – 80% vote or value, Brother/Sister – 50% vote or value• AR (2010) • CO (2010)• GA (2012)• VA (2012)

A “substantial ownership interest” is defined with reference to 15 U.S.C. §78p, which is more than 10% ownership.

• OK (2010)• SD (2010) • UT (2012)

50% ownership in affiliate• CA (2010)(50% vote)• TX (2011)

Noteworthy – Regulation• Pennsylvania

Affiliate Nexus

• Some states, such as Ohio and Pennsylvania, have had an affiliate nexus laws for several decades• OH: SFA Folio (652 N.E.2d 693 (Ohio 1995)) – retailer

accepting isolated returns from catalog sales does not create nexus

• PA: Bloomingdale’ s By Mail (567 A.2d 773 (Pa. 1989)) –Local stores were not agents of the catalog company

• In general, these laws provide that nexus is established based on the presence of a related entity in the state• Definition of “related” differs for each state

• Some states require the related entity to perform certain actions in the state, such as: sell a similar line of products; advertise, promote, or facilitate sales for the retailer; maintain an office, distribution facility, warehouse, or storage place to facilitate delivery of the retailer’s sales; use the same/similar trademarks; or deliver, install, assemble, or perform maintenance services for the retailer’s purchasers within the state

23

Affiliate Nexus Litigation

• New Mexico Tax & Rev. Dept. v. Barnesandnoble.com LLC, No. 31,231 (N.M. Ct. App., April 18, 2012)• Barnesandnoble.com LLC (“B&N”) is Internet retailer with no physical

presence in NM• Barnes & Noble Booksellers, Inc. (“Booksellers”), an affiliate, owned

and operated 3 physical bookstores in NM• NM issued an assessment for gross receipts tax and interest against

B&N based on Booksellers’ in-state activities• Department’s hearing officer ruled in favor of B&N• Department appealed to the NM Court of Appeals• The Court of Appeals reversed the trial court and held that there

was substantial nexus with NM due to in-state activities by the affiliate’s stores that created goodwill for a shared trademark

• This case has been appealed to the New Mexico Supreme Court, Dkt. No. 33,627

24

Colorado’s Notification and Reporting Law

25

Alternative Approaches

Colorado's Law – Different Approach - 2010• Two Provisions To “Encourage” Remote Seller Collection

• Non collecting seller notification requirement – must tell purchaser transaction subject to sales/use tax and provide link to CO DOR website.

• Non collecting seller reporting requirement – must send annual report to its Colorado purchasers (1099-like) by first class mail and to the CO DOR.

• No other state has incorporated Colorado’s “1099-like”annual reporting

Disclosure/Reporting – Enacted Laws

27

Effective Date Type of Disclosure De minimis

Exception?

Colorado

§ 39-21-112

3/10/2010 To purchaser (at time of sale and at end of year) and to

revenue department

Yes, by Colo. Code Regs. 39-21-112.3.5

(less than $100,000 in sales)

Oklahoma

Tit. 68, § 1406.1

7/1/2010 To purchaser (at time of sale) Yes, by OAC Rule 710:65-21-8 (less than

$100,000 in sales)

South Dakota

§ 10-63-1 et seq.

7/1/2011 To purchaser (at time of sale) Yes (less than $100,000 in sales)

Tennessee

§ 67-6-515

3/23/2012 To purchaser (at time of sale in an email and at end of year)

No, however, law is limited to seller using fulfillment affiliate in

TN

Vermont

§ 9783

5/24/2011 –repealed when

Amazon law eff.

To purchaser (at time of sale) Yes (less than $100,000 in sales)

DMA v. CO DOR – Docket 13-1032, cert. granted 7/1/2014 (from 10th Cir. Ct. of Appeals, 735 F.3d 904); Decided 3/3/2015

Held: Justice Thomas explains that DMA’s suit does not “restrain” Colorado from assessing, levying or collecting a tax within the context of how “restrain” is used for purposes of the TIA. Case remanded back to 10th Circuit to see if non-jurisdictional comity doctrine is still a viable argument.

Justice Kennedy gives “unqualified” concurrence to majority opinion; however, he goes out of his way to say Quill needs reconsidered – it “now harms States to a degree far greater than could have been anticipated earlier.”

Justice Ginsburg joined by Justice Breyer and partially by Justice Sotomayor also concur on the understanding that this case does not address whether refund claims are barred by the TIA. She also indicated the Court’s decision is consistent with Hibbs.

DMA’s Majority, Concurrence and Dissenting Opinions

State & Businesses Work on Streamlined Sales & Use Tax

Agreement

29

Streamlined Sales & Use Tax Agreement (SSUTA)

• SSUTA approved November 2002 by the Implementing States, and amended since

• Agreement came into effect on October 1, 2005 (at least 10 states with 20% of the U.S. population)

• Provisions are based on simplification, uniformity and technology principles:

o Simplification (e.g., state-level administration of tax)o Uniformity (e.g., uniform definition of “lease,” lease sourcing rule) o Technology (e.g., certification of tax calculation software)

• Balancing interests of state sovereignty

Best Practice: Reduce Complexity

• Reducing complexity provides a win-win The existing state and local sales and use tax system creates

burdensome and unnecessary complexity

This complexity imposes substantial costs on vendors, states, and consumers

A simple sales tax system offers the potential to promote equitable and nondiscriminatory taxation, lower rates, reduce administrative burdens, and improve compliance

Goals of the Streamlined Sales Tax Effort –Sec. 102 of SSUTA

A. State level administration of sales and use tax collections

B. Uniformity in the state and local tax basesC. Uniformity of major tax base definitionsD. Central electronic registration system for all member

statesE. Simplification of state and local tax ratesF. Uniform sourcing rules for all taxable transactionsG. Simplified administration of exemptionsH. Simplified tax returnsI. Simplification of tax remittancesJ. Protection of consumer privacy

22 Full Member States2 Assoc. Member States

Federal Legislation Initiatives

34

Federal Legislation: Overview of the Proposals

Since 2005, the following types of legislative bills have been introduced:

• Main Street Fairness Acts (MSFA)

• Marketplace Equity Act (MEA)