Embed Size (px)

Citation preview

2015 Minnesota Economic OutlookJanuary 6, 2015

minneapolisfed.org

Agenda

Minnesota Economy Outlook

Surveys Models

Sector Analysis Agriculture Manufacturing Home building

9th District

Cleveland

Comparing 2014 with last year’s forecast

Employment growth stronger than forecast

Unemployment rate lower than forecast

Personal income growth slightly slower than forecast

Home building somewhat weaker than forecast

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

-5

-4

-3

-2

-1

0

1

2

3

4

2014 nonfarm employment stronger than forecast

Forecast

Actual

Percent change from a year earlier – 4th quarterMinnesota

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

0

1

2

3

4

5

6

7

8

9

2014 unemployment ratelower than forecast

Forecast

Actual

4th quarterMinnesota

Information and Financial Services

Trade, Transportation and Utilities

Government

Total Nonfarm Employment

Education and Health Services

Construction

Leisure and Hospitality

Manufacturing

Professional and Business Services

Natural Resources and Mining

-1 0 1 2 3 4 5 6 7 8 9

Minnesota United States

Source: Bureau of Labor Statistics

Employment increased in most sectorsNonfarm employment, percent change from a year earlier,

November 2014

2007

2008

2009

2010

2011

2012

2013

2014

2015

0123456789

1011

5.8%

3.7%USMN

Minnesota’s unemployment rate below prerecession levels

Percent

Source: Bureau of Labor Statistics

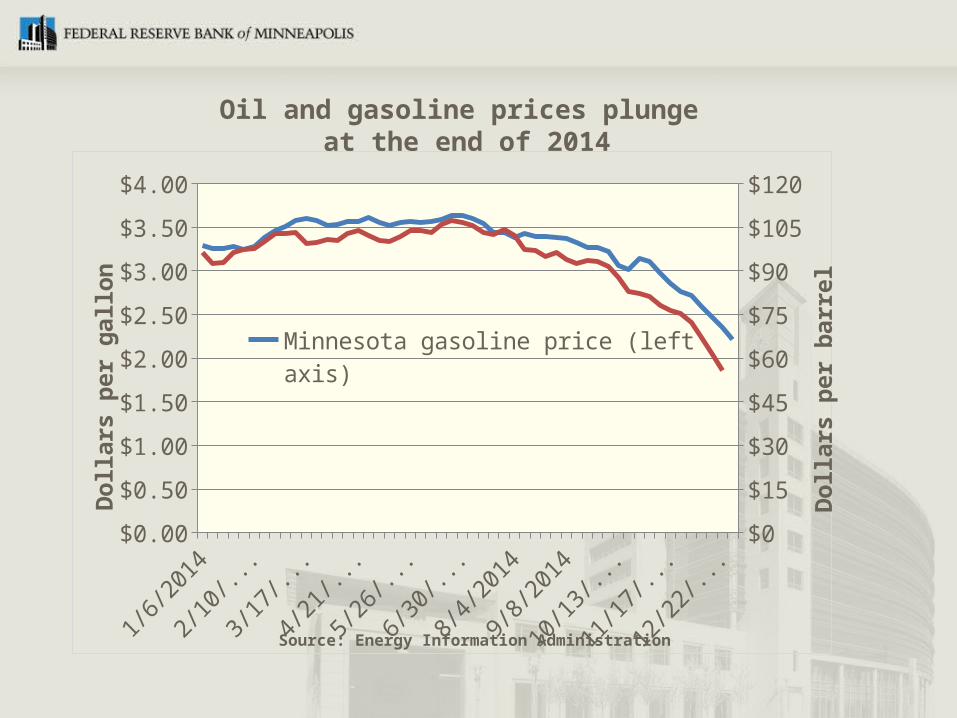

Oil and gasoline prices plunge at the end of 2014

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

$4.00

$0

$15

$30

$45

$60

$75

$90

$105

$120

Minnesota gasoline price (left axis)

WTI oil price (right axis)

Dollars

per

gallon

Dollars

per

barr

el

Source: Energy Information Administration

Forecast models: Solid employment growth and continued decrease in the unemployment rate

Business optimism near record high

Manufacturers expect growth

Home building flat

Minnesota economy: Signs of optimism for 2015

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

20150%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Business leader optimism jumps

Greater MN

Twin Cities

Percent of respondents selecting somewhat optimistic or very optimistic

Minnesota employment expected to grow by 1.9 percent

MN MT ND SD WI UP0.0

1.0

2.0

3.0

4.0

5.0

6.0

2014

2015

Nonfarm employment forecastPercent change from a year earlier – 4th quarter

Montana

U.P. of MI

Greater MN

South Dakota

District

North Dakota

Twin Cities

NW Wisconsin

0 20 40 60 80 100

2014 Out-look

2015 Out-look

Diffusion index*

Twin Cities business leaders expect increased employment at their

companies

*Index number above 50 indicates expansion. Index number below 50 indicates contraction.

Services

Total MN

Retail

Manufacturing

Construction

F.I.R.E.

0 20 40 60 80 100

2014 Out-look

2015 Out-look

Diffusion index*

Minnesota employment outlook positive

*Index number above 50 indicates expansion. Index number below 50 indicates contraction.

MN MT ND SD WI UP0

1

2

3

4

5

6

7

8

2014

2015

Unemployment rate – 4th quarter

Minnesota unemployment rate forecast at 3.3 percent by end of 2015

0% to 1%

2% to 3%

4% to 5%

Above 5%

0 10 20 30 40 50 60 70 80 90

2014 Out-look

2015 Out-look

Percent of respondents

Overall Minnesota business leaders anticipate moderate increases in wages and

salaries

Agriculture

Retail

Manufacturing

District

Construction

0 10 20 30 40 50 60 70 80 90 100

2014 Outlook

2015 Outlook

Diffusion index*

Minnesota business leaders foresee overall moderate price increases

*Index number above 50 indicates expansion. Index number below 50 indicates contraction.

Minnesota personal income growth expected to increase by 4.6 percent

MN MT ND SD WI0

1

2

3

4

5

6

2014

2015

Percent change from a year earlier – 4th quarterNot adjusted for inflation

Crop prices dropped

Average farm prices

2011/2012 2012/2013 Estimated 2013/2014

Projected 2014/2015

(Current $ per bushel)Corn 6.22 6.89 4.46 3.20-3.80Soybean 12.5 14.4 13.00 9.00-11.00Wheat 7.24 7.77 6.87 5.80-6.20

U.S. Department of Agriculture, estimates as of December 2014

Cattle prices solid

Average farm prices

2012 2013Estimated 2014 Projected 2015

(Current $ per cwt)All Milk 18.52 20.05 24.05-24.15 18.45-19.25Steers 122.82 125.89 155.29 160-172Hogs 60.88 64.05 76.22 63-68

U.S. Department of Agriculture, estimates as of December 2014

Minnesota manufacturing survey indicates

faster growth expected in 2015

Investment

Profits

Employment

Production level

0 20 40 60 80 100

2014 Ac-tual

2015 Outlook

Diffusion index*

*Index number above 50 indicates expansion. Index number below 50 indicates contraction.

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014*0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

Home building recovery moderates in Minnesota

Housing Units Authorized*Estimate based on November year-to-date change from 2013 to 2014

UP of MI

SD

Western WI

MT

Greater MN

MPLS MSA

ND

0 10 20 30 40 50 60 70 80 90 100

2014 Outlook

2015 Outlook

Diffusion index*

Minnesota business leaders expect slower growth in home building

*Index number above 50 indicates expansion. Index number below 50 indicates contraction.

Minnesota economy: Signs of optimism for 2015

Forecast models: Solid employment growth and continued decrease in the unemployment rate

Business optimism at record high

Manufacturers expect growth

Home building flat

Questions?