Embed Size (px)

Citation preview

©2015, College for Financial Planning, all rights reserved.

Session 4Present Value Annuity DueSerial Payment Future SumAmortization

CERTIFIED FINANCIAL PLANNER CERTIFICATION PROFESSIONAL EDUCATION PROGRAMFinancial Planning Process & Insurance

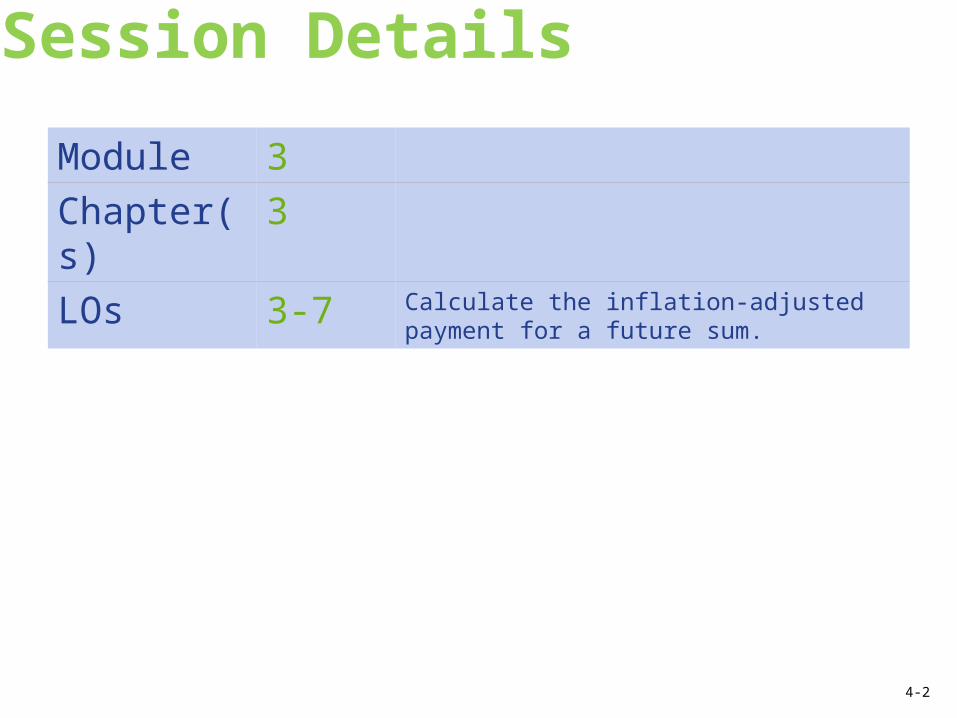

Session Details

Module 3

Chapter(s)

3

LOs 3-7 Calculate the inflation-adjusted payment for a future sum.

4-2

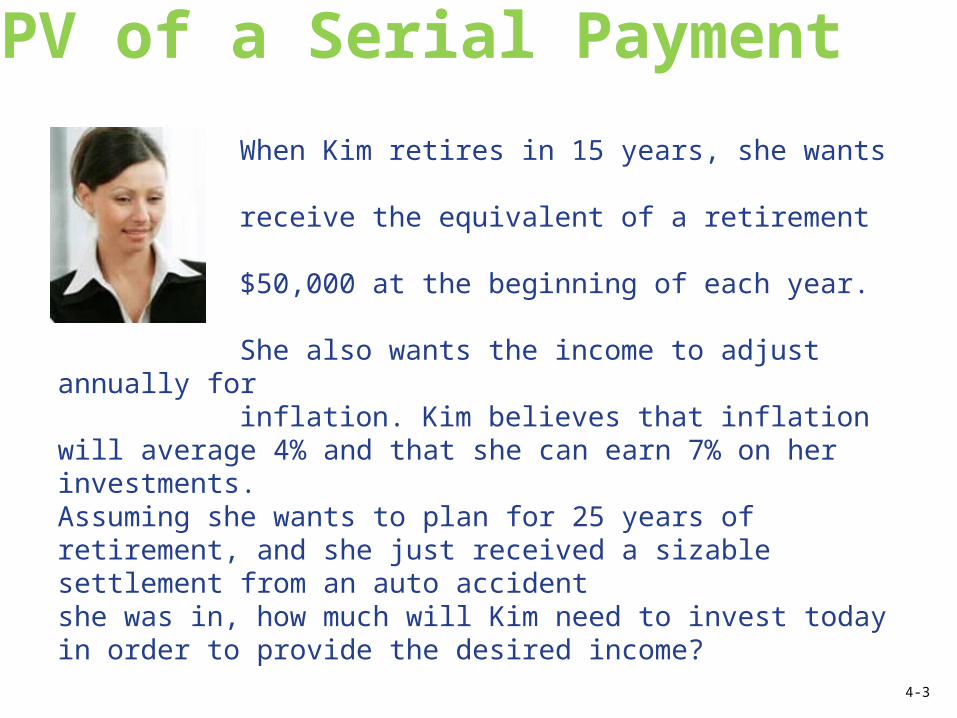

PV of a Serial Payment

When Kim retires in 15 years, she wants to receive the equivalent of a retirement

income of $50,000 at the beginning of each year.

She also wants the income to adjust annually for

inflation. Kim believes that inflation will average 4% and that she can earn 7% on her investments. Assuming she wants to plan for 25 years of retirement, and she just received a sizable settlement from an auto accident she was in, how much will Kim need to invest today in order to provide the desired income?

4-3

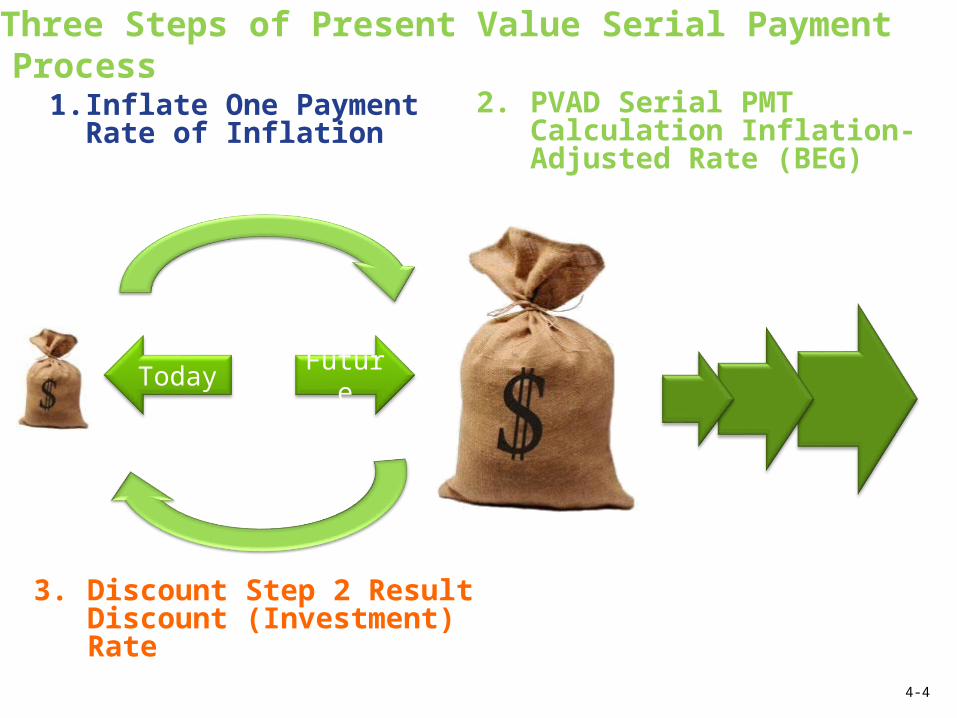

Three Steps of Present Value Serial Payment Process

Today

1. Inflate One Payment Rate of Inflation

3. Discount Step 2 ResultDiscount (Investment) Rate

Future

2. PVAD Serial PMT Calculation Inflation-Adjusted Rate (BEG)

4-4

Step 1: PV of a Serial Payment

HP10BII/10BII+

=

50,000 PV

4 I/YR

15 N

FV

+/–

Answer 1: $90,047(Becomes the PMT in Step 2)

4-5

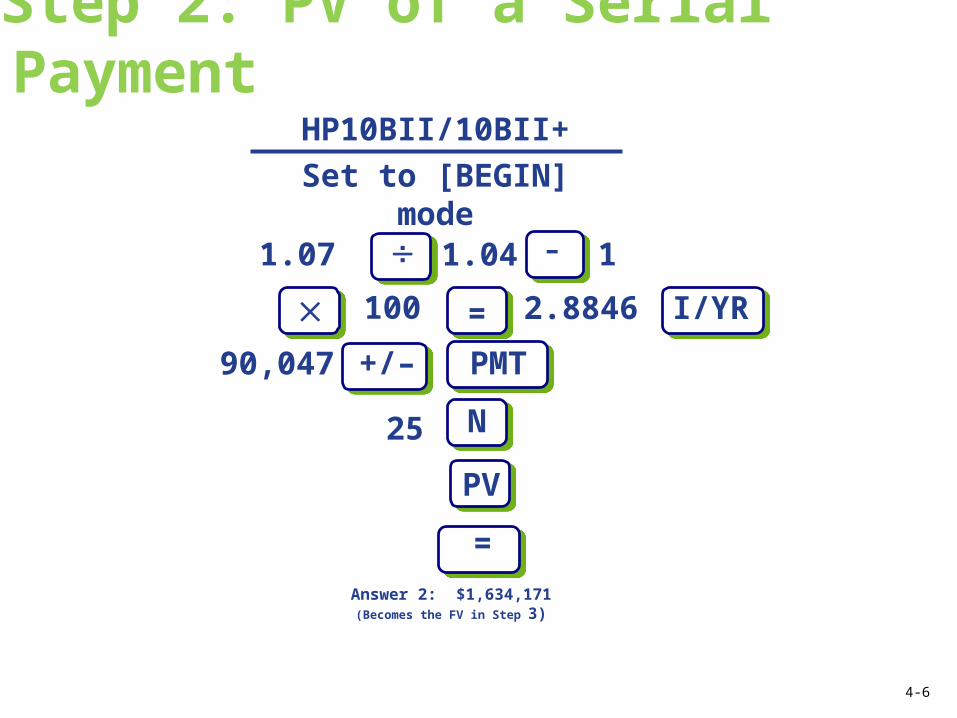

Step 2: PV of a Serial Payment

Answer 2: $1,634,171(Becomes the FV in Step 3)

1.07 –

HP10BII/10BII+

Set to [BEGIN] mode

100

90,047 PMT

N

= I/YR

1

25

PV

=

1.04

+/–

2.8846

4-6

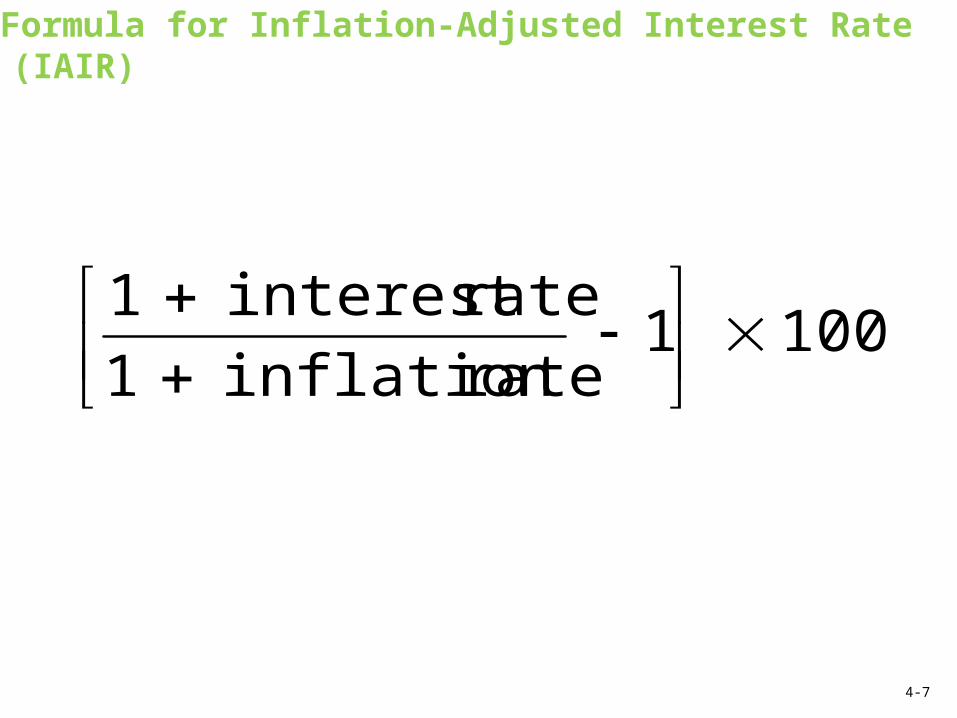

Formula for Inflation-Adjusted Interest Rate (IAIR)

100 1 rate inflation 1

rate interest 1

4-7

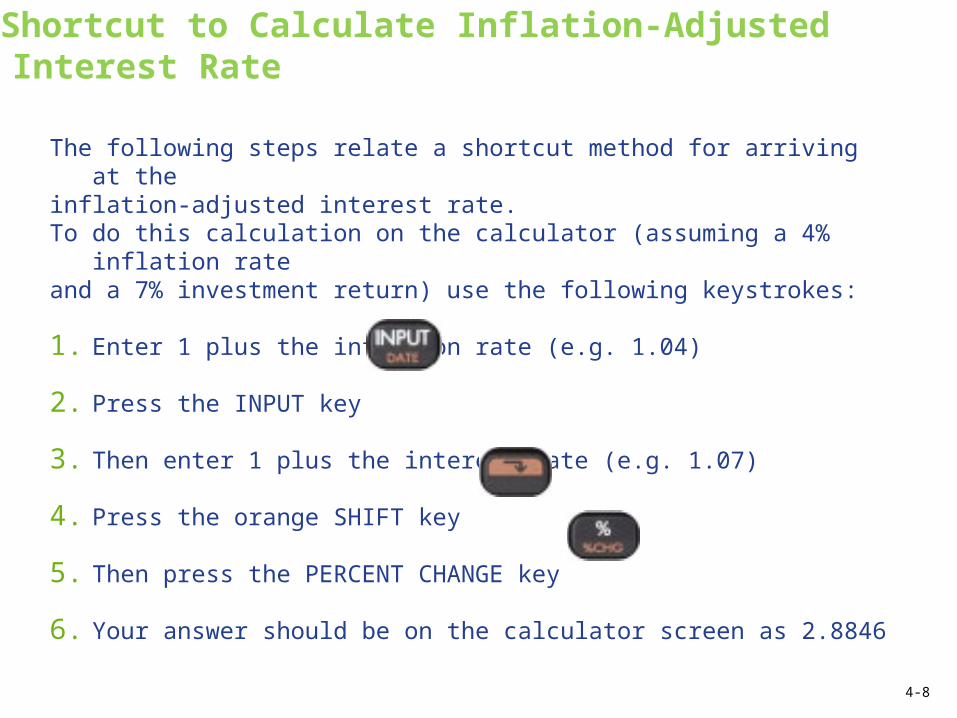

Shortcut to Calculate Inflation-Adjusted Interest Rate

The following steps relate a shortcut method for arriving at theinflation-adjusted interest rate.To do this calculation on the calculator (assuming a 4%

inflation rateand a 7% investment return) use the following keystrokes:

1. Enter 1 plus the inflation rate (e.g. 1.04)

2. Press the INPUT key

3. Then enter 1 plus the interest rate (e.g. 1.07)

4. Press the orange SHIFT key

5. Then press the PERCENT CHANGE key

6. Your answer should be on the calculator screen as 2.88464-8

Step 3: PV of a Serial Payment

Final Answer: $592,300

HP10BII/10BII+

1,634,171 FV

7 I/YR

15

PV

+/–

N

=

4-9

Three Steps of Present Value Serial Payment Process

Today

3. Discount Step 2 ResultDiscount (Investment) RateFV = $1,634,171N = 15I/YR = 7PV = $592,300

2. PVAD Serial PMT Calculation Inflation-Adjusted Rate (BEG)

Future

PMT

= $9

0,04

7PM

T =

$90,

047

PMT=

$90,

047

N = 25

I/YR = ([1.07/1.04] 1)×100IAIR = 2.8846 PMT= 90,047I/YR = 2.8846N = 25PV = $1,634,171(Begin Mode)

1. Inflate One Payment Rate of InflationPV=$50,000I/YR= 4N = 15FV = $90,047 (becomes PMT)

4-10

Session Details

Module 3

Chapter(s)

3

LOs 3-8 Calculate the present value for an inflation-adjusted payment.

4-11

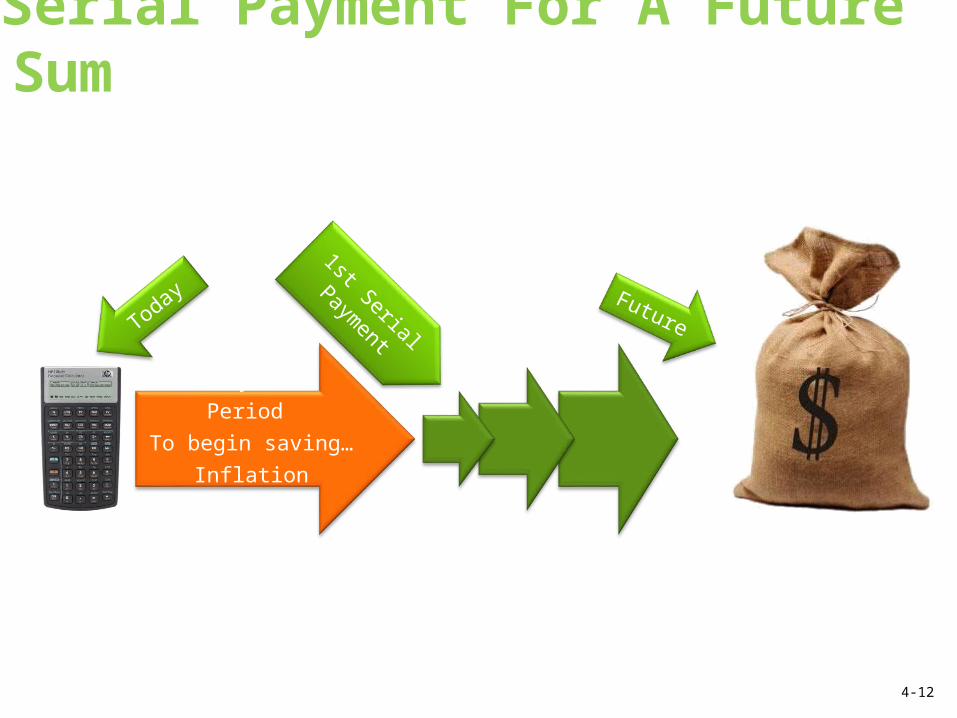

Serial Payment For A Future Sum

Today

Delay of 1 Period

To begin saving…

Inflation

Adjustment

Future

1st Serial

Payment

4-12

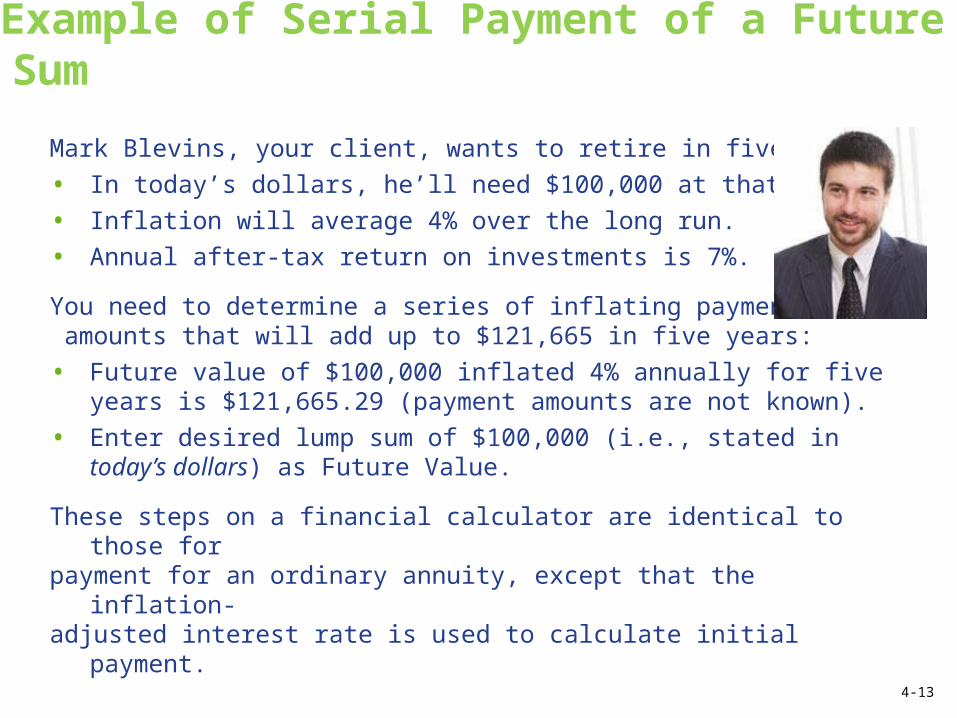

Example of Serial Payment of a Future Sum

Mark Blevins, your client, wants to retire in five years:

• In today’s dollars, he’ll need $100,000 at that time.

• Inflation will average 4% over the long run.

• Annual after-tax return on investments is 7%.

You need to determine a series of inflating payment amounts that will add up to $121,665 in five years:

• Future value of $100,000 inflated 4% annually for five years is $121,665.29 (payment amounts are not known).

• Enter desired lump sum of $100,000 (i.e., stated in today’s dollars) as Future Value.

These steps on a financial calculator are identical to those for

payment for an ordinary annuity, except that the inflation-adjusted interest rate is used to calculate initial payment.

4-13

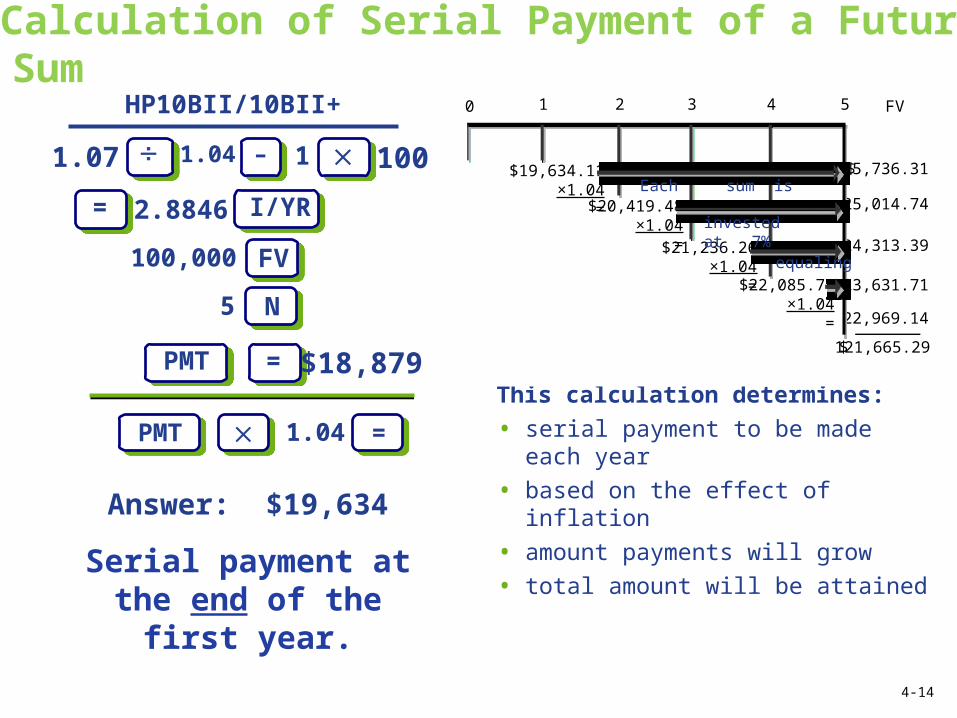

Calculation of Serial Payment of a Future Sum

This calculation determines:

• serial payment to be made each year

• based on the effect of inflation

• amount payments will grow

• total amount will be attained

2.8846

Answer: $19,634

Serial payment at the end of the first year.

1.07 –

HP10BII/10BII+

100

100,000 FV

N

1.04

= I/YR

1

5

PMT =

1.04

PMT = $18,879

FV21 3 4

$25,736.31

25,014.74

24,313.39

$121,665.29

$20,419.48×1.04

=

$19,634.11×1.04

=

23,631.71

22,969.14

0 5

$22,085.71×1.04

=

$21,236.26×1.04

=

Each sum is

invested at 7%

equaling

4-14

Amortization

• Amortization is the process of liquidating a debt by making installment payments.

• Amortization calculations are done to divide a series of payments into amounts that apply to interest and principal.

• The amortization process involves two sets of calculations: o the first step calculates the

periodic payment; o the second step identifies

the interest and principal amounts.

4-15

Amortization Question

In the process of assisting Barney and Betty to calculate what they still owe on their home, you are provided with the following information: They purchased their home eight years ago for $239,500. They made a 20% down payment, and financed the balance using a 30-year mortgage with a 5.15% interest rate. Taxes and insurance increase the payment by $300 per month. In the process of calculation you tell them that they have an outstanding principal balance of what amount?

a. $129,524b. $164,365c. $165,071d. $206,338

4-16

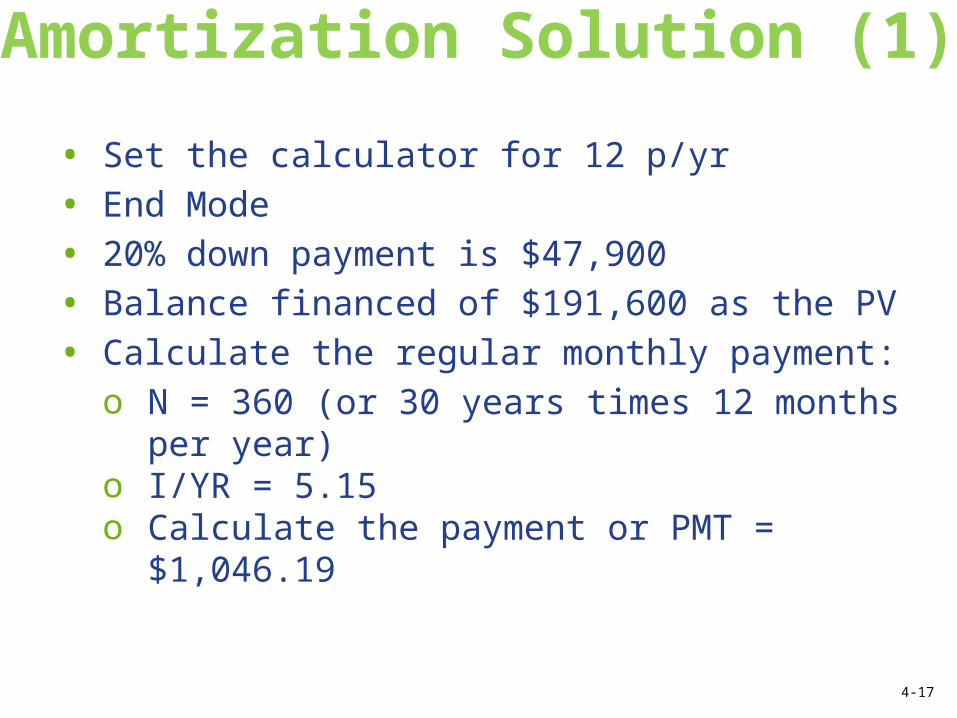

Amortization Solution (1)

• Set the calculator for 12 p/yr • End Mode • 20% down payment is $47,900• Balance financed of $191,600 as the PV • Calculate the regular monthly payment:

o N = 360 (or 30 years times 12 months per year)

o I/YR = 5.15 o Calculate the payment or PMT =

$1,046.19

4-17

Amortization Solution (2)

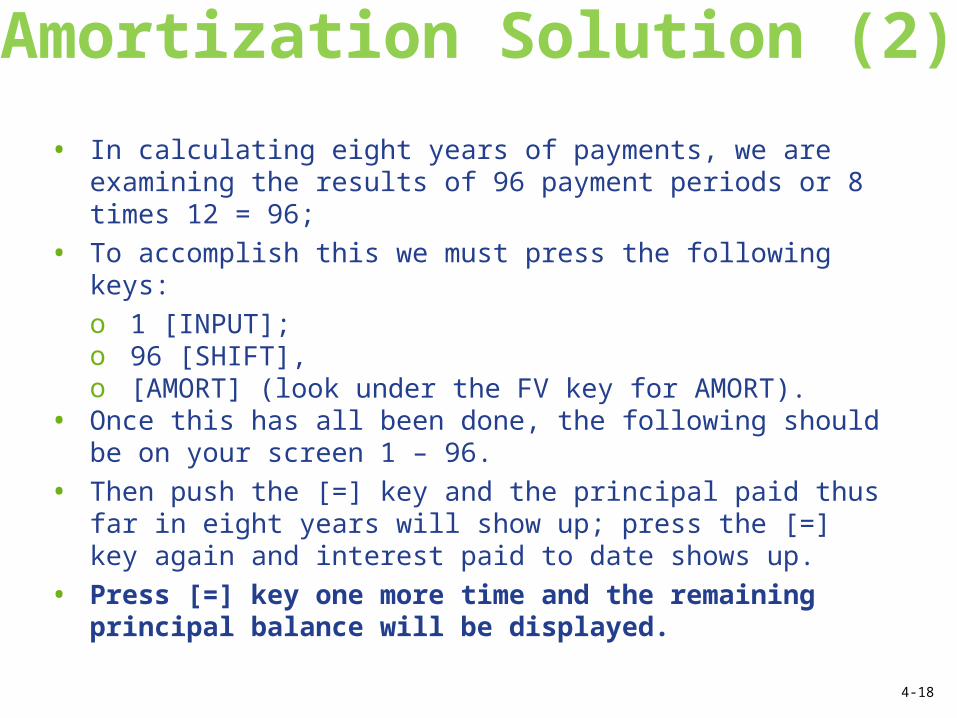

• In calculating eight years of payments, we are examining the results of 96 payment periods or 8 times 12 = 96;

• To accomplish this we must press the following keys: o 1 [INPUT]; o 96 [SHIFT], o [AMORT] (look under the FV key for AMORT).

• Once this has all been done, the following should be on your screen 1 – 96.

• Then push the [=] key and the principal paid thus far in eight years will show up; press the [=] key again and interest paid to date shows up.

• Press [=] key one more time and the remaining principal balance will be displayed.

4-18

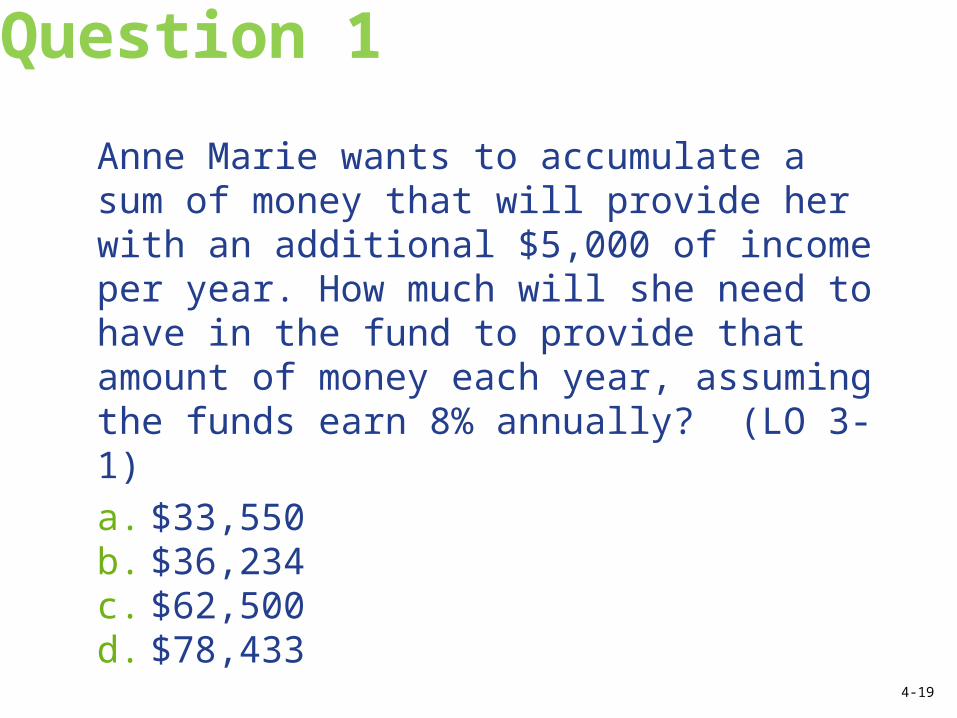

Question 1

Anne Marie wants to accumulate a sum of money that will provide her with an additional $5,000 of income per year. How much will she need to have in the fund to provide that amount of money each year, assuming the funds earn 8% annually? (LO 3-1)a. $33,550b. $36,234c. $62,500d. $78,433

4-19

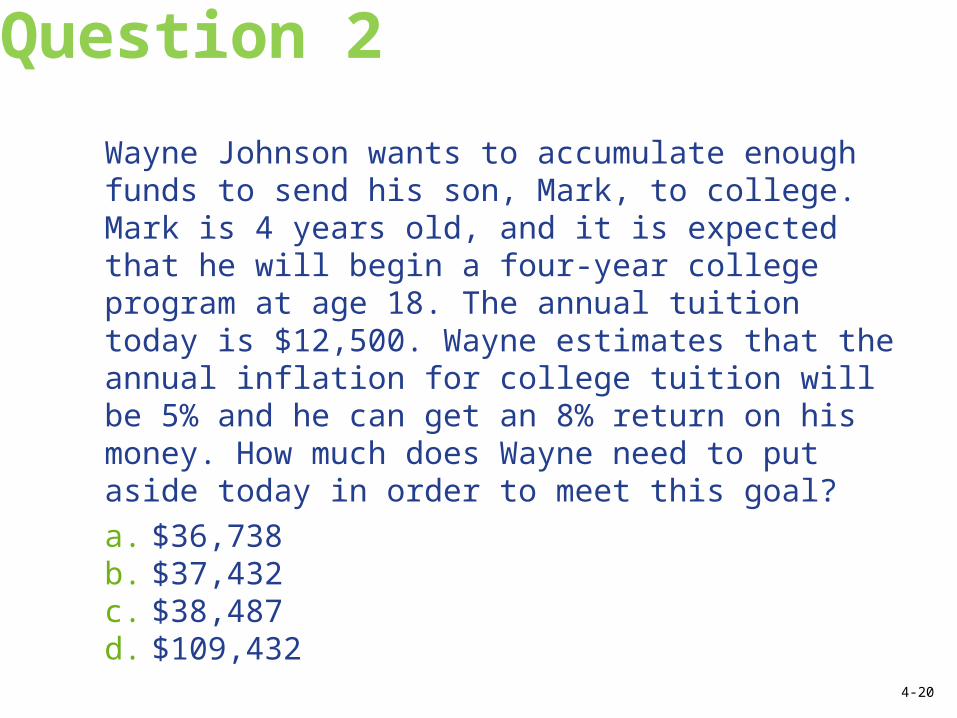

Question 2

Wayne Johnson wants to accumulate enough funds to send his son, Mark, to college. Mark is 4 years old, and it is expected that he will begin a four-year college program at age 18. The annual tuition today is $12,500. Wayne estimates that the annual inflation for college tuition will be 5% and he can get an 8% return on his money. How much does Wayne need to put aside today in order to meet this goal?a. $36,738b. $37,432c. $38,487d. $109,432

4-20

Question 3

An individual has $2,500 to invest and wants to accumulate $4,000 at the end of five years. What annual rate of return is required to meet this goal if earnings on the investment are compounded monthly?(LO 3-5)a. 9.4%b. 9.6%c. 9.7%d. 9.8%

4-21

©2015, College for Financial Planning, all rights reserved.

Session 4End of Slides

CERTIFIED FINANCIAL PLANNER CERTIFICATION PROFESSIONAL EDUCATION PROGRAMFinancial Planning Process & Insurance