Embed Size (px)

Citation preview

2015 BAW Conference

SHP Eligibility andACA Reporting for

2015LaShanti Geathers

Denise Hunter

Today’s topics

• Part I. Expanded Eligibility• Types of employees and Terms to Know• October Eligibility Reminders• What to Expect in 2016• Frequently Asked Questions

• Part II. ACA Reporting Requirements• Form Details to Consider• Helpful Information• How PEBA Will Assist Employers• Checklist for ACA Reporting

2

Expanded eligibility and the ACA

3

Expanded eligibility and the ACA

• All employers participating in PEBA insurance benefits must offer coverage to all employees eligible to participate in the insurance benefits.• The Plan of Benefits (POB) document has been

amended to allow coverage for permanent full-time employees, as well as non-permanent full-time employees and variable-hour, part-time and seasonal employees.

4

Types of employees

• All employees fall into one of three categories:• New full-time employee• New variable-hour, part-time or seasonal employee• Ongoing employee

• As an employer, it is your responsibility (not PEBA’s) to determine how to classify your employees

5

How to define an employee• New full-time employee as defined by the POB:• Employer reasonably determines based on facts and

circumstances at the date of hire, the employee will average 30 hours per week.

• New part-time employee as defined by the POB:• Has not completed a full standard measurement period as

of date of hire• Not expected to average 30 hours or more per week

during an initial measurement period

6

How to define an employee

• New seasonal employee as defined by the POB:• Has not completed a full standard measurement period• Hired into a position for which the customary annual

employment is six months or less.• Customary means by nature of the position, the employee

works six months or less, and that period begins each calendar year in approximately the same part of the year, such as summer or winter.

7

How to define an employee

• New variable-hour employee as defined by the POB:• Has not completed a full standard measurement period.• As of date of hire, employer cannot determine whether the

employee is reasonably expected to be employed an average of at least 30 hours per week.

• Ongoing Employee as defined by POB:• Has been employed by an employer for an entire standard

measurement period October 4 – October 3 of next plan year.

8

Summary of types of employees

• Full-time employee (permanent and non-permanent)• Employee expected to average 30 hours per week

• Variable hour, part-time, seasonal employee• Variable-hour: employer does not know• Part-time: employer does not expect• Seasonal: position is customarily less than six months that

begins around the same time each year

9

Initial stability period

• Variable-hour, part-time and seasonal employees that have been deemed eligible for benefits are eligible for the entire initial stability period, even if their hours are later reduced.

10

Terms to Know(Refer to Affordable Care Act Glossary)

11

Quick reviewNew variable-hour, part-time or seasonal employee

12

Example: Bruno

Bruno was hired part-time on June 6, 2015, by the Department of Public Safety. Bruno’s benefits administrator (BA) does not know or expect him to average 30 or more hours per week.•Initial measurement period• July 1, 2015 – June 30, 2016

•Initial administrative period• July 1, 2016 – July 31, 2016

•Initial stability period• August 1, 2016 – July 31, 2017

13

Sample timeline for Bruno

14

Sample timeline for Bruno new part-time employee

Initial measurement period begins Jul 1

Initial measurement period ends Jun 30 Initial stability period begins Aug 1

When does Bruno become and an ongoing employee?When does Bruno become and an ongoing employee?

Standard measurement period October 4 - October 3

Continue to measure

Bruno becomes ongoing October 3, 2016

Bruno becomes ongoing October 3, 2016

October eligibility reminders

16

October eligibility reminders

2015 October enrollment period• Offers coverage to newly eligible ongoing employees for

2016 plan year • Ongoing employees have been employed October 4, 2014,

through October 3, 2015• Any employees whose stability period, Standard or Initial

began on January 1 will not lose eligibility for insurance until December 31, 2015

17

October eligibility reminders

• 2015 open enrollment • Nonpermanent full-time, variable-hour, part-time, and

seasonal employees are eligible to participate with all insurance programs offered. • Be sure to provide the most recent Notice of Election form. • Part-time teachers are not eligible for life insurance and

long term disability.• Be sure to provide the Marketplace Exchange Notice to

newly eligible employees, and the initial COBRA notice to newly enrolled employees and/or their newly enrolled dependents.

18

October eligibility reminders

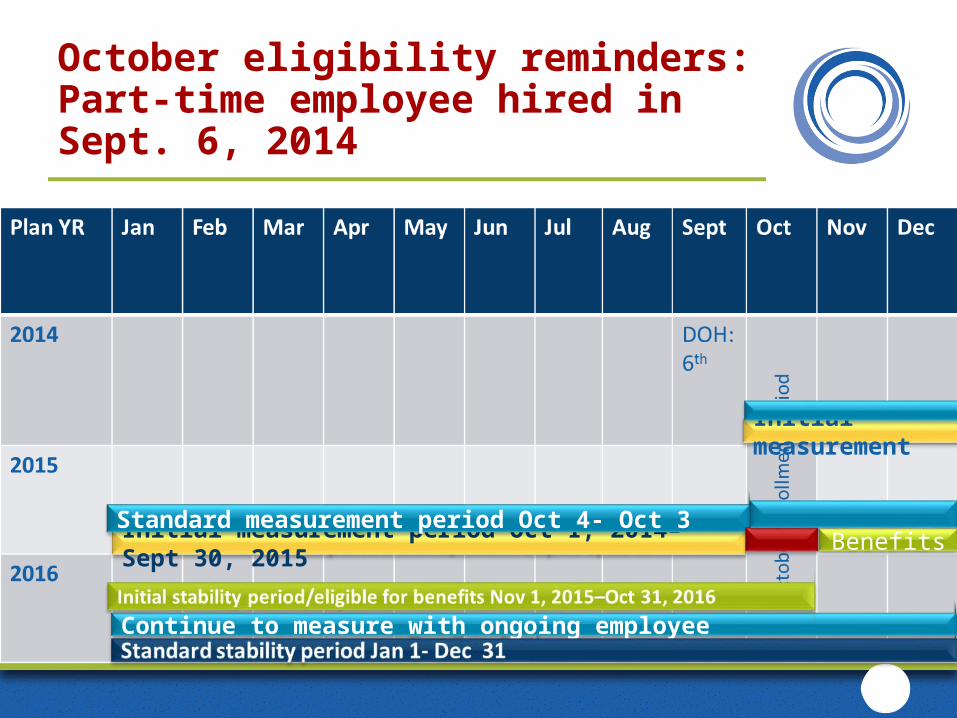

New variable-hour, part-time, and seasonal employees hired in September 2014•Initial measurement period

• October 1, 2014-September 30, 2015

• Don’t let these employees fall through the cracks

•Initial administrative period • October 1-31, 2015

•Initial stability period• November 1, 2015-October 31,

2016

19

When to begin tracking as an ongoing employee• Standard measurement period

• October 4, 2014-October 3, 2015

• Standard administrative period • October 4- Dec 31, 2015

• Standard stability period• January 1, 2016-December 31,

2016

October eligibility reminders: Part-time employee hired in Sept. 6, 2014

Initial measurement

Initial measurement period Oct 1, 2014–Sept 30, 2015Standard measurement period Oct 4- Oct 3

Continue to measure with ongoing employee

Benefits

What to expect in 2016

21

What to expect in 2016

• 2016 Standard Stability Period• January 1 – December 31 for ongoing employees• Employees who average 30 hours or more per week during

the standard measurement period are eligible for insurance the entire plan year if they remain employed with the same employer without a 13 week break in employment (26 weeks for academic employers)

22

2016 plan year

• Throughout the year “new” variable-hour, part-time and seasonal employees will reach the end of their initial stability period.• BA should look back to October 2015 • Employee should have been employed a full standard

measurement period October 4, 2014 – October 3, 2015• If the employee averaged 30 hours, his benefits continue.• If the employee did not average 30 hours, terminate his

benefits at the end of the initial stability period, and offer COBRA continuation and conversion information if applicable.

23

Arnold was hired May 7, 2014, as a variable-hour employee• October 4, 2015

• Did not average 30 hours over the standard measurement period

• January 1, 2016• Benefits continue; still in initial

stability period• June 30, 2016

• Benefits end; offer COBRA continuation and conversion if applicable

• October 4, 2016• Review hours again to determine

eligibility for 2017 plan year

24

Example: Employee not eligible at the end of initial stability period

• Initial measurement period • June 1, 2014-May 31,

2015

• Initial administrative period • June 1-30, 2015• Deemed eligible for

insurance

• Initial stability period• July 1, 2015–June 30,

2016

25

Example Arnold is not eligible at the end of stability period:

Bobby was hired May 7, 2014 as a variable-hour employee

• October 4, 2015• Averaged 30 over the standard

measurement period

• June 30, 2016• Benefits will continue through

December 31, 2016

• October 4, 2016• Review again to determine eligibility

for the 2017 plan year

26

Example: Employee eligible at the end of initial stability period

• Initial measurement period• June 1, 2014–May 31,

2015

• Initial administrative period• June 1-30, 2015• Deemed eligible for

insurance

• Initial stability period • July 1, 2015 – June 30,

2016

27

Example Bobby is eligible at the end of stability period:

Christina was hired as a full-time employee on August 3, 2015 • September 1, 2015, benefits became effective• November 1, 2015, unpaid leave begins. Insurance

coverage terminated due to reduction of hours and COBRA continuation coverage was offered• March 8, 2016, Christina returns to a full-time position

• Offer benefits the first of the month after she returns to work

28

Example: New full-time employee returns from unpaid leave

Frequently asked question

An ongoing full-time employee is actively at work. The employee did not average 30 hours during the standard measurement period due to unpaid leave. Can I terminate his benefits?•No. An employee who is actively at work in full-time position is eligible for coverage. However, if the employee experiences another reduction of hours or goes on unpaid leave during the plan year, coverage should terminate the first of the month following the reduction of hours and COBRA coverage should be offered (because the employee did not average 30 hours during the standard measurement period). Note: this is why we measure full-time employees.

29

Frequently asked question

An employee averaged 30 hours and is in a stability period. The employee had a reduction of hours and is going on unpaid leave. Can I charge the employer share of premiums?•No. After reviewing the Affordable Care Act employer mandates, PEBA amended the rules regarding unpaid leave.

30

Frequently asked question

A full-time teacher is a Medicare-eligible working retiree, who is also eligible for benefits during a stability period. The teacher is transitioning to a part-time position in the fall. Can she elect retiree health coverage over the summer?No. Because the teacher is eligible for Medicare and employer sponsored health coverage, she may not elect health coverage as a retiree. Federal law requires Medicare-eligible employees to elect active employer sponsored insurance whenever its available.

Medicare eligible employees may:• Enroll or remain enrolled in active coverage as an employee or • Cancel the health insurance offered through PEBA and continue dental and

vision as a retiree.

31

ACA reportingHow PEBA will assist employers

32

ACA reporting

• One of the biggest challenges for employers has been combining benefits information with payroll information for the purpose of creating the required forms

33

ACA reporting for active employees

After reviewing the final regulations released by the IRS in February for the 1094 and 1095 forms, PEBA has determined:•Each employer will be responsible for filing forms for any individual deemed eligible for benefits anytime during the preceding calendar year.•Members of the State ALE (state agencies, boards and departments that use the CG payroll) will be considered a single employer. Only one return for active employees will be submitted to the IRS. The entity to issue statements to the active employees has not been identified.

34

ACA reportingfor non-employees

State Applicable Large Employer (ALE) consist of state agencies/boards/departments that use the CG payroll•PEBA will handle the return and statements required for former non-Medicare eligible employees, retirees, survivors, COBRA subscribers and their dependents who have not been employed any part of the reporting year

35

ACA reportingfor non-employees

Technical colleges, public universities, public school districts and certain public corporations•May designate PEBA as its Designated Governmental Entity (DGE) to make the return and statements required for former non-Medicare eligible employees, retirees, survivors, COBRA subscribers and their dependents who have not been employed any part of the reporting year

36

Designated governmental entity

• Only employers that participate in the State Health Plan pursuant to S.C. Code of Law Ann § 1-11-710 can designate PEBA as their DGE for reporting non-Medicare eligible retirees, COBRA and survivor subscribers. • Employers who can designate PEBA as their DGE• Technical colleges• Public universities • Public school districts• Certain public corporations

37

Designated governmental entity

• Local subdivisions as defined by S.C. Code of Law Ann § 1-11-720 cannot designate PEBA as its DGE• List of employers who cannot designate PEBA as it

DGE• PEBA will not report coverage for former

employees who were active one day or more during the reporting period• No employer may elect PEBA as its DGE for active

employees

38

How to designate PEBA as the DGEComplete the Designated Governmental Entity form

• Form may be completed and signed by agency head and sent to PEBA for consideration

• PEBA will verify if employer is eligible to designate PEBA as its DGE

• If PEBA accepts the designation, PEBA will return a signed copy of the form to the employer. If employer does not receive a signed copy of the form, PEBA is not the DGE, and the employer will be responsible for reporting all active and former employees.

• PEBA will only accept designation as an employer’s DGE for the purpose of reporting non-Medicare eligible retirees, survivors and COBRA subscribers.

• PEBA will not report active employees or former employees active even for one day during the reporting period.

Email form to [email protected] by October 31, 2015

39

40

PEBA as the DGE

• PEBA will complete and provide the 1095-B form to the employer’s former non-Medicare eligible employees and transmit it with the 1094-B. • PEBA will only report former employees who were not

active employees for any portion of the reporting period.• If an employee’s status changes from active to retiree or

COBRA subscriber in the same reporting year, the employer must report the former employee on the 1095-C form (1095-B for small employers), along with all other active employees. PEBA will send the employer coverage information for the employee.

41

ACA reportingfor non-employees

Local subdivisions•Employers are responsible for handling the return and statements required for their former non-Medicare eligible former employees, retirees, survivors, COBRA subscriber and their dependents. PEBA will provide employers with coverage information for these individuals.

42

Two types of ACA reporting

• Section 6056 Reporting (1095-C and 1094-C)• Applies to Applicable Large Employers (ALE) with 50 or more full-

time equivalent employees• Report includes the employer’s offers of coverage to employees

and the coverage for which the employee and his dependents were enrolled

• Section 6055 Reporting (1095-B and 1094-B)• Applies to all employers and includes the coverage for which

former employees and their dependents were enrolled• Employers with fewer than 50 full-time equivalent employees

will also use these forms to report coverage for their active employees

43

Section 6056 IRS reporting requirements for large employers

44

Section §6056 reporting requirements

• Applies to employers with 50 or more full-time equivalent employees (ALE groups)

Forms• 1095-C Employer-Provided Health Insurance Offer and

Coverage• Individuals employed in a full-time position at any time during

the preceding calendar year• Employers must use the 1095-C form to report former

employees who have retired, left employment and/or elected COBRA if the employee was enrolled in active coverage any part of the year/reporting period

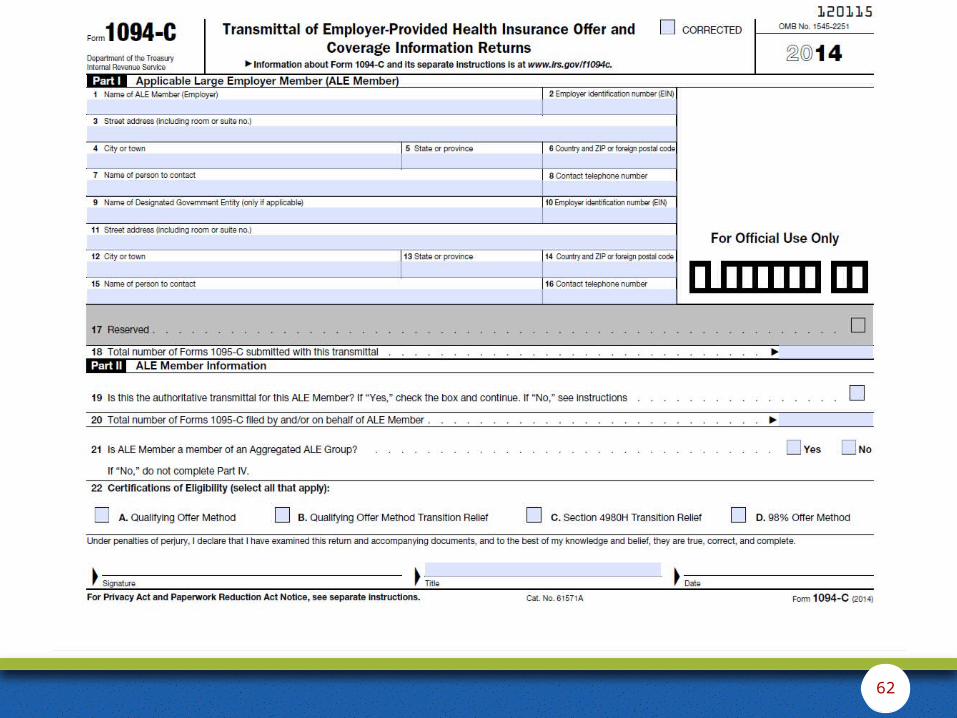

• 1094-C Transmittal of Employer (attached to the 1095-C and provided to IRS)

45

IRS form 1095-C

• Part I• Requests information about the employee and employer

• Part II• Requests information about whether the employee was

offered coverage• Part III• Requests information about when an employee and his

dependents were enrolled in coverage• PEBA will provide employers with an electronic file

containing information about which employees and dependents were covered

46

47

If you need assistance completing this form, consult with your legal counsel, a tax

professional or the IRS. PEBA cannot provide guidance for completing IRS forms.

PEBA will provide the information

needed to complete Part III.

Form details to consider

• Name, address and EIN of the employer• Name and phone number of employer’s contact

person• Calendar year for which the information is reported• Certification that the employer offered its full-time

employees (and their dependents) the opportunity to enroll in minimum essential coverage (by calendar month)

48

Form details to consider

• Employee’s name, address and Social Security number• Months during the plan year coverage was available

(offered) to the employee• Months during the plan year the employee and his

dependents enrolled in coverage• Employee’s share of the lowest cost monthly premium

(self-only) for coverage providing minimum value

49

Form details to consider

• Applicable safe harbor codes (depends on reporting method)• Whether the employee’s effective date of coverage

was affected by a permissible waiting period (limited non-assessment period)

50

Helpful information• The State Health Plan is a self-funded plan• Coverage offered by PEBA is minimum essential coverage

providing minimum value and is affordable • Based on SHP Savings Plan – Subscriber only coverage is

$9.70 per month• $9.70 per month x 12 months = $116.40 per year• $116.40 / .095 = $1,225.26 per year

• Coverage is not affordable if employee’s share of premium exceeds 9.5 percent of employee’s household income• Employee share of lowest cost monthly premium for self-only

minimum value coverage is $9.70(part-time teachers who do not average 30 hours pay higher

premiums)

51

Helpful information

• Limited non-assessment period is a period where the employer is not subject to a penalty under Code Section 4980H regardless of whether the employer offered coverage to a full-time employee

52

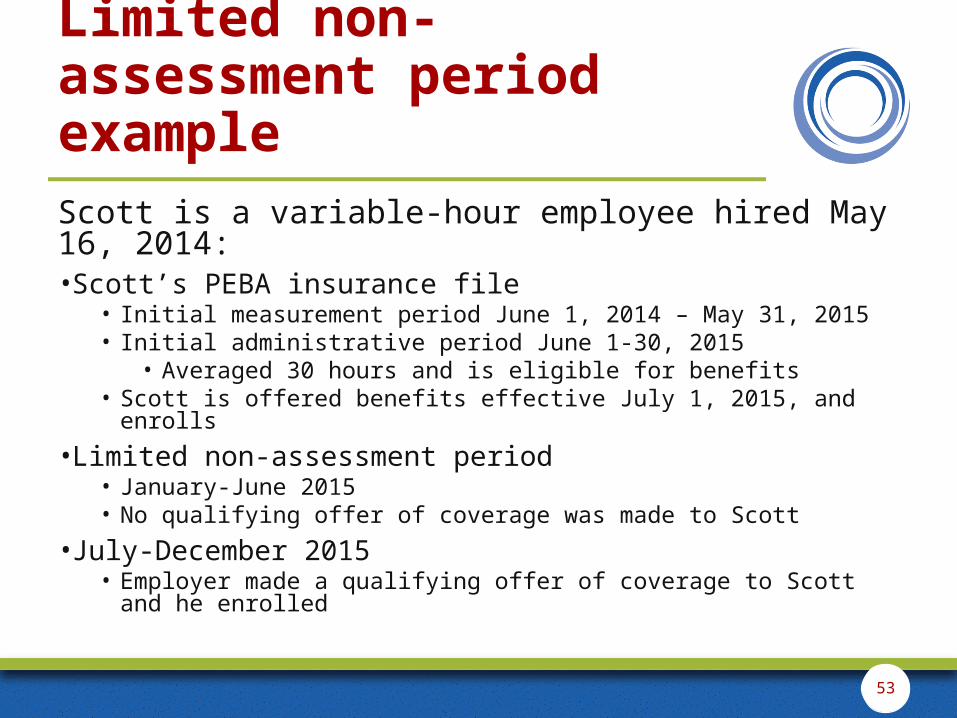

Scott is a variable-hour employee hired May 16, 2014:•Scott’s PEBA insurance file

• Initial measurement period June 1, 2014 – May 31, 2015• Initial administrative period June 1-30, 2015

• Averaged 30 hours and is eligible for benefits • Scott is offered benefits effective July 1, 2015, and enrolls

•Limited non-assessment period• January-June 2015• No qualifying offer of coverage was made to Scott

•July-December 2015• Employer made a qualifying offer of coverage to Scott and he enrolled

53

Limited non-assessment period example

Tina is a variable-hour employee hired July 17, 2014:•Tina’s PEBA insurance file

• Initial measurement period August 1, 2014 – July 31, 2015• Initial administrative period August 1-31, 2015• March 15, 2015, Tina is offered a full-time position and accepts• Tina is offered benefits effective April 1, 2015, and enrolls

•Limited non-assessment period• January– March 2015• No qualifying offer of coverage was made to Tina

•April-December 2015• Employer made a qualifying offer of coverage to Tina and she enrolled

54

Limited non-assessment period example

Joan was hired by Company ABC July 16, 2015, as a full-time employee:•Joan is offered benefits effective August 1, 2015, and enrolls•January-June 2015

• Joan is not employed by Company ABC•Limited non-assessment period

• July 2015• No qualifying offer of coverage was made to Joan

•August-December 2015• Employer made a qualifying offer of coverage to Joan and she

enrolled

55

Limited non-assessment period example

Sample coverage file for 1095-C

56

57

PEBA coverage information example

• Sharon was hired as a full-time employee at Midlands Technical College on January 15, 2014. • Sharon was offered health coverage and enrolled effective

February 1, 2014, and has had continuous health coverage.• Around the last week of December, PEBA will send

Midlands Tech information indicating that Sharon was enrolled in health coverage January through December 2015.• In other words, an “X” will be indicated for each month, January

through December 2015, (or one “X” indicating coverage for the entire year) for Sharon.

58

PEBA coverage information example

• Jason was hired as a full-time employee at Charleston County School on July 15, 2015. • Jason was offered health coverage, and enrolled himself

and his family effective August 1, 2015.• Around the last week of December, PEBA will send

Charleston County School information indicating that Jason and each of his dependents were enrolled in health coverage August through December 2015.• In other words, an “X” will be indicated for each month, August

through December, for Jason and each of his covered dependents.

59

PEBA coverage information example• Linda was hired as a full-time employee at the City of Sumter on

March 17, 2015. • Linda was offered health coverage and enrolled effective April 1,

2015.• Effective July 1, 2015, Linda left employment.• On October 15, Linda was rehired at the City of Sumter.• Linda was offered health coverage and enrolled, effective

November 1, 2015.• Around the last week of December, PEBA will send the City of

Sumter information indicating that Linda was enrolled in health coverage April through June and November through December.• In other words, an “X” would be indicated for each month, April through

June and November through December, for Linda.

60

PEBA coverage information example

• Jim retired from USC several years ago and enrolled in retiree coverage. • Jim decides to return to work and is hired in a full-time

position at USC effective August 17, 2015.• Jim was offered health coverage and enrolled effective

September 1, 2015.• Around the last week of December, PEBA will send USC

information indicating that Jim was enrolled in health coverage January through December.• In other words, an “X” would be indicated for each month,

January through December for Jim even though part of his coverage was retiree coverage and part was active coverage.

61

62

63

64

Form details to consider

• Name, address and EIN of the employer• Name and phone number of employer’s contact

person• Calendar year for which the information is reported• Total number of forms (1095-C) submitted• Months for which MEC is offered by employer

65

Form details to consider

• Number of full-time employees for each month of the calendar year (does not include those in limited non-assessment period)• Total number of employees (head count) for each

month of the calendar year• If part of an Aggregated Group, other members• Election of Section 4980H Transition Relief Indicator, if

applicable

66

IRS form 1094-C

• The 1094-C should be attached to the 1095-C and submitted to the IRS. • If you need assistance completing this form, consult

your legal counsel, a tax professional or the IRS. PEBA cannot provide guidance for completing IRS forms.

67

Section 6055IRS reporting requirements for both small and large employers

68

Section 6055 reporting requirements

• Applies to employers with fewer than 50 full-time equivalent employees (non-ALE groups)• Applies to all employers who offer coverage to former

non-Medicare eligible employees (retirees, COBRA and survivor subscribers)

Forms• 1095-B Health Coverage form

• Individuals employed in a full-time position (small employers) at any time during the preceding calendar year

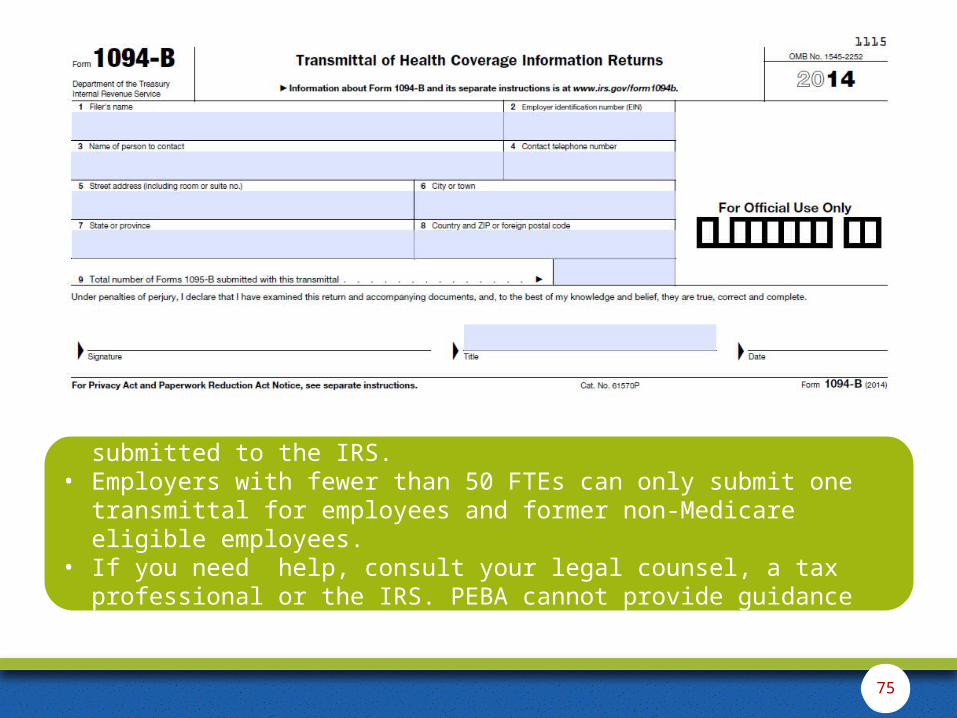

• Retirees, COBRA and survivor subscribers• 1094-B Transmittal of Employer (attached to the 1095-B

and provided to IRS)

69

IRS form 1095-B

• Part I • Contains information to identify the employee, retiree,

survivor or COBRA participant

• Part II & Part III• Contact legal counsel, tax professional or the IRS for

assistance

70

IRS form 1095-B

• Part IV• Lists when an employee and his dependents were enrolled

in coverage• Local Subdivision and Non-designated Governmental Entity

(DGE) Groups• PEBA will provide an electronic file with the information needed to

complete Part IV of the form

71

72

If you need assistance completing this form, consult with your legal counsel, a tax

professional or the IRS. PEBA cannot provide guidance for completing IRS forms.

PEBA will provide the information (not guidance) needed to complete Part IV for active employees and former employees, survivors and COBRA participants for local subdivisions and employers that do not designate PEBA as their designated governmental entity.

Sample coverage file for 1095-B

73

74

75

• The 1094-B should be attached to the 1095-B and submitted to the IRS.• Employers with fewer than 50 FTEs can only submit one transmittal for employees

and former non-Medicare eligible employees.• If you need help, consult your legal counsel, a tax professional or the IRS. PEBA

cannot provide guidance for completing IRS forms.

Deadlines and penalties

76

IRS reporting requirements

• All statements (1095-C and 1095-B) should be provided to all covered subscribers by January 31, 2016.• Forms should be submitted to the IRS by February 28,

2016, or March 31, 2016, if filing electronically.• Penalties can be imposed for: (1) failing to provide

statements or timely file a return; and/or (2) failing to provide a correct or complete statement. See IRS guidelines for penalty amounts.

77

Checklist forACA reporting

• Review the IRS forms and instructions to become familiar with the reporting requirements• Identify where the required data is collected and stored in

your systems (in-house or external)• Develop systems to collect any data that is not currently

captured in existing systems and aggregate this data to prepare the required forms• Verify employee addresses• Verify information in MyBenefits (employees)• Determine whether assistance is needed from an outside

vendor• Consult with legal counsel

78

Questions

79

Disclaimer

This presentation does not constitute a comprehensive or binding representation regarding the employee benefits offered by the South Carolina Public Employee Benefit Authority (PEBA). The terms and conditions of the retirement and insurance benefit plans offered by PEBA are set out in the applicable statutes and plan documents and are subject to change. Please contact PEBA for the most current information. The language used in this presentation does not create any contractual rights or entitlements for any person.

80