Embed Size (px)

Citation preview

ミャンマー国全国運輸交通プログラム形成準備調査

2014年7月24日

Presented by Junji Shibata, P.E. Japan, Oriental Consultants Co., Ltd.

Mya

nmar

Nat

iona

l Tra

nspo

rt D

evel

opm

ent M

aste

r Pl

an

Contents

1. MYT‐Plan Objectives2. Transport Vision, Policy, Strategy and Actions3. Corridor‐based Transport Infrastructure Development4. Financing5. Feasibility Studies6. Appendix

2

Mya

nmar

Nat

iona

l Tra

nspo

rt D

evel

opm

ent M

aste

r Pl

an

1. MYT-Plan Objectives

3

Mya

nmar

Nat

iona

l Tra

nspo

rt D

evel

opm

ent M

aste

r Pl

an

1. MYT-Plan Objectives

MYT-Plan is designed to provide guidance for a long-term investmentframework that will help the Government achieve its economic growth targetsby 2030.

MYT-Plan to provide guidelines that are adaptable to other industrial sectorsand to private investment, to assist with investment planning and decisionmaking for a variety of transport sector projects.

MYT-Plan to inform the transport sector’s development vision, by presenting aset of comprehensive policies and development strategies relevant to all modesof transport, and corresponding actions (projects) for specific modes bydevelopment corridor.

MYT-Plan is designed to be read in conjunction with Myanmar’s National Comprehensive Development Plan (NCDP).

MYT-Plan will be updated in conjunction with the achievement of national development objectives, guided by the NCDP.

4

Mya

nmar

Nat

iona

l Tra

nspo

rt D

evel

opm

ent M

aste

r Pl

an

2. Transport Vision, Policy, Strategy and Actions

5

Mya

nmar

Nat

iona

l Tra

nspo

rt D

evel

opm

ent M

aste

r Pl

an

2. Transport Vision, Policy, Strategy and Actions

‘To develop an efficient, modern, safe, and environmentally-

friendly transportation system in a coordinated and

sustainable manner that embraces all transport modes for

the benefit of the country and people of Myanmar’.

The National Transport Vision

6

Mya

nmar

Nat

iona

l Tra

nspo

rt D

evel

opm

ent M

aste

r Pl

an

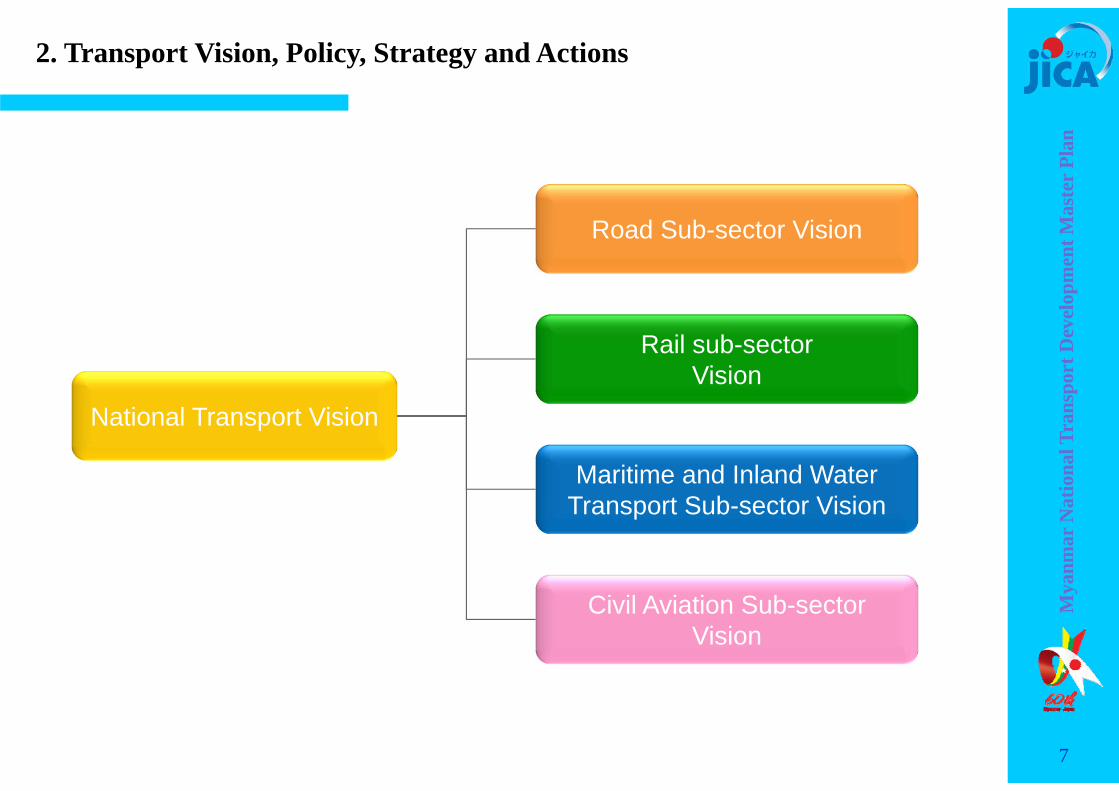

National Transport Vision

Road Sub-sector Vision

Rail sub-sectorVision

Maritime and Inland Water Transport Sub-sector Vision

Civil Aviation Sub-sectorVision

7

2. Transport Vision, Policy, Strategy and Actions

Mya

nmar

Nat

iona

l Tra

nspo

rt D

evel

opm

ent M

aste

r Pl

an

Implementation of the Policies – Strategic objective, Strategies, and Actions

Policy Statement

Strategic Objective

Strategy

Action (short-term)

Vision Statement

8

2. Transport Vision, Policy, Strategy and Actions

Mya

nmar

Nat

iona

l Tra

nspo

rt D

evel

opm

ent M

aste

r Pl

an

3. Corridor-based Transport Infrastructure Development

9

Mya

nmar

Nat

iona

l Tra

nspo

rt D

evel

opm

ent M

aste

r Pl

an

3. Corridor-based Transport Infrastructure Development

10

i. Existing Context

Mya

nmar

Nat

iona

l Tra

nspo

rt D

evel

opm

ent M

aste

r Pl

an

1a

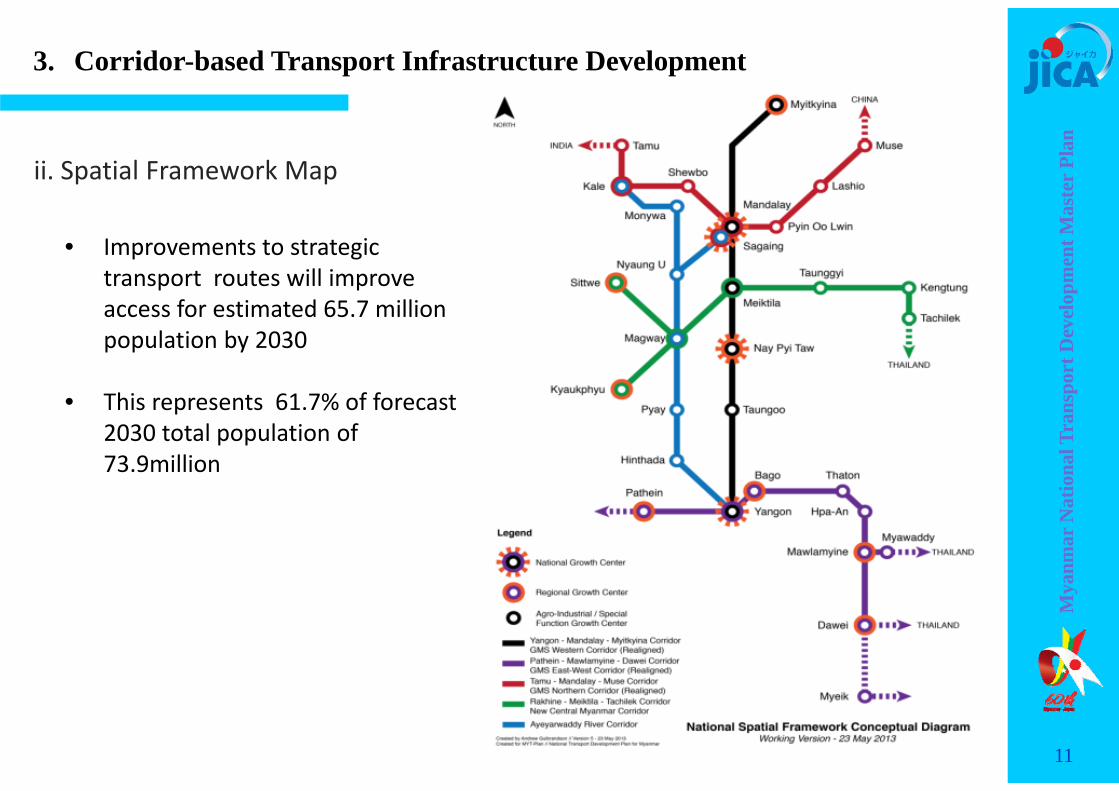

ii. Spatial Framework Map

• Improvements to strategic transport routes will improve access for estimated 65.7 million population by 2030

• This represents 61.7% of forecast 2030 total population of 73.9million

11

3. Corridor-based Transport Infrastructure Development

Mya

nmar

Nat

iona

l Tra

nspo

rt D

evel

opm

ent M

aste

r Pl

an

1a

iii. Consistency with DHSHD Concept

Multi‐Centric Balanced Development Strategy

National Growth Centers: Nay Pyi Taw, Yangon, Mandalay/Sagaing

Regional Growth Centers: Myitkyina, Sittwe/Kyaukphyu, Pathein, Bago(Hanthawaddy), Mawlamyine, Dawei

Agro‐industrial Centers: Lashio, Shwebo, Kale, Monywa, Meiktila, Taunggyi, Taungoo , Magway, Pyay, Hinthada, Thaton, Hpa‐an

Special Function Growth Centers: Muse, Tamu, Nyaung‐U, Kengtung, Tachileik, Myawaddy, Myeik

3. Corridor-based Transport Infrastructure Development

12

Mya

nmar

Nat

iona

l Tra

nspo

rt D

evel

opm

ent M

aste

r Pl

anThis National Spatial Framework should be:

Complementary with the National Transport Master Plan for Myanmar

Consistent with the MOC Department of Human Settlements and Housing Development Concept of Concentrated and Decentralized Development Strategy

Balanced in terms of enabling growth in urban and rural regions and states

Focused on key growth centers to optimize investment funds and community benefits

Multi‐centric to improve access to a range of employment opportunities and social and community facilities

3. Corridor-based Transport Infrastructure Development

13

Mya

nmar

Nat

iona

l Tra

nspo

rt D

evel

opm

ent M

aste

r Pl

an

A

B

C

D

E

G

H

J

K

L

10 Major Corridors

A Central North‐South Corridor

B East ‐West Corridor

C Northern Corridor

D Mandalay ‐ Tamu Corridor

E Second East ‐West Corridor

G East ‐West Bridging Corridor

H Delta Area Network

J Southern Area Development Corridor

K Western North‐South Corridor

L Eastern North ‐ South Corridor

Priority corridors for urgentinvestment

14

3. Corridor-based Transport Infrastructure Development

Mya

nmar

Nat

iona

l Tra

nspo

rt D

evel

opm

ent M

aste

r Pl

an

Development Corridor Section Code2012

Population (,000)

% against National

Population by corridor

2012 GDP(Kyat

billion)

% against National GDP by corridor

Central North-South CorridorYangon-Nay Pyi Taw A1 11,714

41%13,170

50%Nay Pyi Taw- Mandalay A2 6,323 4,457Mandalay - Myitkyna A3 7,035 5,648

GMS East - West Corridor Yangon - Hpa-An - Myawaddy B1 14,052 28% 14,543 35%Mawlamyine - Dawei B2 2,753 2,039GMS Northern Corridor Mandalay - Muse C1 6,042 10% 4,503 10%

Mandalay - Tamu Corridor Mandalay - Tamu D1 8,722 14% 6,992 15%New East - West Corridor Tachilek - Meiktila - Kyaukpyu E1 10,636 17% 6,938 15%

East - West Bridging Corridor Hpasawing - Pyay G1 2,664 12% 1,727 11%Loikaw - Magway G2 4,767 3,214

Delta Area Network Yangon - Pathein H1 8,992 21% 10,076 27%Pathein - Hinthada H2 3,766 2,651

Southern Area Development Corridor

Thanbyuzayat - Hpayarthonesu J1 2,5378%

1,4828%Dawai - Thai Border J2 811 781

Dawei - Kawthaung J3 1,756 1,679

Western North-South Corridor Yangon - Pyay - Magway K1 12,810 33% 14,388 42%Magway - Mandalay K2 7,096 5,468

Eastern North - South Corridor Bilin - Loikaw L1 3,896 12% 2,550 9%Loikaw - Nawnghko L2 3,247 1,900

15

3.1 Corridor Analysis – population and GDP

Mya

nmar

Nat

iona

l Tra

nspo

rt D

evel

opm

ent M

aste

r Pl

an

Development Corridor Section Code

2013 Traffic

demand (ton-km)

Composition Modal Share

Total 2013 Road Rail River

Central North-South CorridorYangon-Nay Pyi Taw A1 23.3 27% 93% 7% 0%Nay Pyi Taw- Mandalay A2 15.4 18% 92% 8% 0%Mandalay - Myitkyna A3 2.6 3% 67% 13% 20%

GMS East - West Corridor Yangon - Hpa-An - Myawaddy B1 10.0 12% 95% 5% 0%Mawlamyine - Dawei B2 0.4 0% 92% 8% 0%

GMS Northern Corridor Mandalay - Muse C1 11.1 13% 98% 2% 0%Mandalay - Tamu Corridor Mandalay - Tamu D1 1.4 2% 75% 7% 18%New East - West Corridor Tachilek - Meiktila - Kyaukpyu E1 2.4 3% 97% 3% 0%

East - West Bridging Corridor Hpasawing - Pyay G1 0.1 0% 100% 0% 0%Loikaw - Magway G2 1.0 1% 100% 0% 0%

Delta Area Network Yangon - Pathein H1 1.4 2% 52% 0% 48%Pathein - Hinthada H2 0.2 0% 97% 3% 0%

Southern Area Development Corridor

Thanbyuzayat - Hpayarthonesu J1 0.0 0% - - -Dawai - Thai Border J2 0.0 0% 100% 0% 0%Dawei - Kawthaung J3 0.1 0% 100% 0% 0%

Western North-South Corridor Yangon - Pyay - Magway K1 8.8 10% 61% 6% 33%Magway - Mandalay K2 2.1 2% 12% 8% 80%

Eastern North - South Corridor Bilin - Loikaw L1 0.2 0% 100% 0% 0%Loikaw - Nawnghko L2 0.1 0% 97% 3% 0%

3.1 Corridor Analysis – Freight transport demand in 2013

16

Mya

nmar

Nat

iona

l Tra

nspo

rt D

evel

opm

ent M

aste

r Pl

an

Corridor Name Section Code2013 Traffic demand (person-km) Composition

Total Air Car IWT Rail Bus 2013

Central North-South Corridor

Yangon-Nay Pyi Taw A1 23.4 0% 13% 0% 3% 83% 30%Nay Pyi Taw- Mandalay A2 16.0 0% 14% 0% 6% 79% 20%

Mandalay - Myitkyna A3 4.1 13% 15% 12% 51% 9% 5%

GMS East - West Corridor Yangon - Hpa-An - Myawaddy B1 9.1 0% 19% 0% 7% 74% 12%Mawlamyine - Dawei B2 0.5 0% 19% 0% 5% 76% 1%

GMS Northern Corridor Mandalay - Muse C1 3.7 0% 49% 0% 8% 43% 5%Mandalay - Tamu Corridor Mandalay - Tamu D1 3.0 1% 15% 0% 5% 79% 4%New East - West Corridor Tachilek - Meiktila - Kyaukpyu E1 4.3 5% 25% 0% 10% 59% 6%

East - West Bridging Corridor

Hpasawing - Pyay G1 0.0 0% 0% 0% 0% 100% 0%Loikaw - Magway G2 2.3 0% 15% 0% 30% 55% 3%

Delta Area Network Yangon - Pathein H1 3.6 1% 24% 18% 0% 57% 5%Pathein - Hinthada H2 0.6 0% 23% 0% 18% 59% 1%

Southern Area Development Corridor

Thanbyuzayat - Hpayarthonesu J1 0.0 0% 100% 0% 0% 0% 0%Dawai - Thai Border J2 0.0 0% 40% 0% 0% 60% 0%Dawei - Kawthaung J3 0.9 87% 8% 0% 0% 5% 1%

Western North-South Corridor

Yangon - Pyay - Magway K1 4.3 0% 29% 0% 21% 50% 5%Magway - Mandalay K2 1.5 1% 12% 0% 39% 49% 2%

Eastern North - South Corridor

Bilin - Loikaw L1 0.1 0% 0% 0% 0% 100% 0%Loikaw - Nawnghko L2 0.2 0% 13% 0% 82% 4% 0%

3.1 Corridor Analysis – Passenger transport demand in 2013

17

Mya

nmar

Nat

iona

l Tra

nspo

rt D

evel

opm

ent M

aste

r Pl

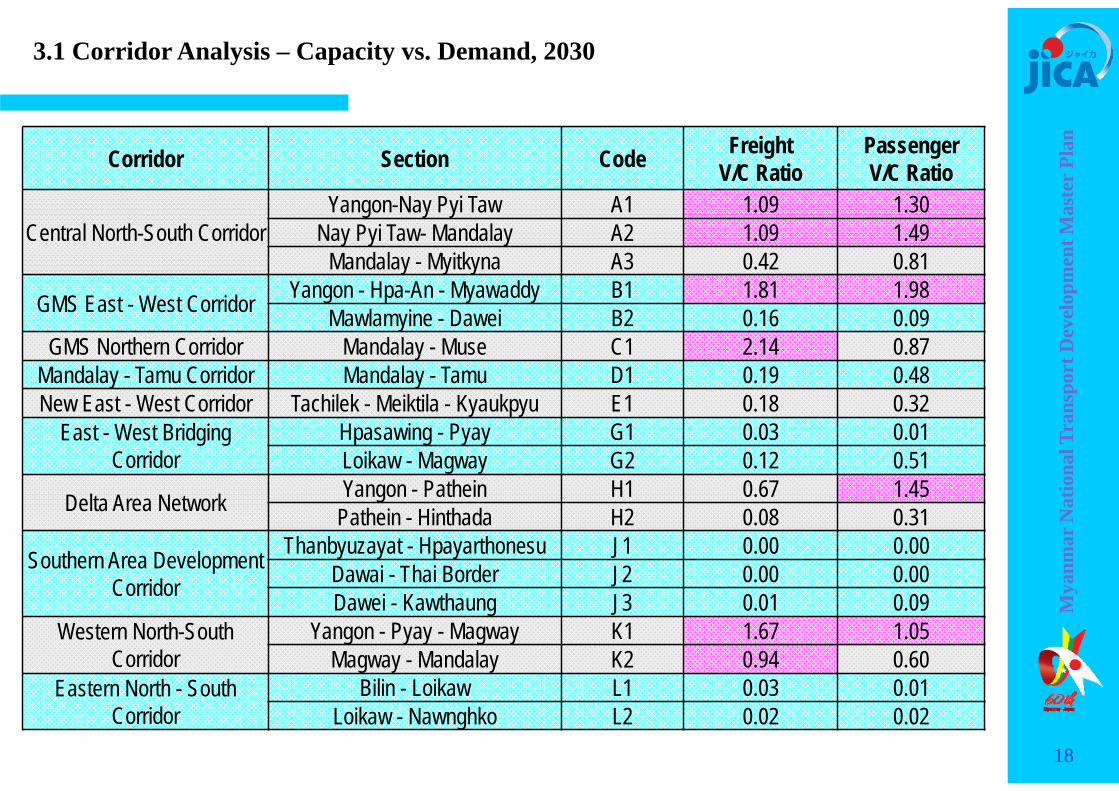

anCorridor Section Code FreightV/C Ratio

PassengerV/C Ratio

Central North-South CorridorYangon-Nay Pyi Taw A1 1.09 1.30

Nay Pyi Taw- Mandalay A2 1.09 1.49Mandalay - Myitkyna A3 0.42 0.81

GMS East - West Corridor Yangon - Hpa-An - Myawaddy B1 1.81 1.98Mawlamyine - Dawei B2 0.16 0.09

GMS Northern Corridor Mandalay - Muse C1 2.14 0.87Mandalay - Tamu Corridor Mandalay - Tamu D1 0.19 0.48New East - West Corridor Tachilek - Meiktila - Kyaukpyu E1 0.18 0.32

East - West Bridging Corridor

Hpasawing - Pyay G1 0.03 0.01Loikaw - Magway G2 0.12 0.51

Delta Area Network Yangon - Pathein H1 0.67 1.45Pathein - Hinthada H2 0.08 0.31

Southern Area Development Corridor

Thanbyuzayat - Hpayarthonesu J1 0.00 0.00Dawai - Thai Border J2 0.00 0.00Dawei - Kawthaung J3 0.01 0.09

Western North-South Corridor

Yangon - Pyay - Magway K1 1.67 1.05Magway - Mandalay K2 0.94 0.60

Eastern North - South Corridor

Bilin - Loikaw L1 0.03 0.01Loikaw - Nawnghko L2 0.02 0.02

3.1 Corridor Analysis – Capacity vs. Demand, 2030

18

Mya

nmar

Nat

iona

l Tra

nspo

rt D

evel

opm

ent M

aste

r Pl

anTraffic Volume between YNG ‐MDL

Road NH1 NH2 Expressway MC 56 39 -

Small Vehicles 794 126 2,037 Small Bus 265 134 60

Bus 135 74 367 Small Truck 146 45 -Large Truck 1,464 274 -

Total 2,860 692 2,464

・ UH1 + Expressway5,000 ~ 5,500 vehicles /day (=10,000 pcu)

・ UH1Large Truck: 1,500 Vehicles/day (51% of total)

・ ExpresswayCar: 2,000 Vehicles / day Bus: 370 Buses / day

*Daily Average Traffic Volume at Toll Gates*NH1: YNG‐NPT‐MDL Rd. NH2: YNG – PYAY‐MDL *Source: MOC

3.2 Corridor Analysis – A: Central North-South Corridor

19

Mya

nmar

Nat

iona

l Tra

nspo

rt D

evel

opm

ent M

aste

r Pl

an

0

10000

20000

30000

40000

50000

60000

70000

2010 2015 2020 2025 2030 2035

Year

PCU Traffic Volume

Truck

Road Traffic Demand Forecast along Yangon – Mandalay Corridor

Capacity of NH1

Truck demand exceeds the design capacity of NH1 open expressway for trucks

Capacity increase should be considered

Capacity of NH1 + Expressway

20

3.2 Corridor Analysis – Expressway

Mya

nmar

Nat

iona

l Tra

nspo

rt D

evel

opm

ent M

aste

r Pl

an

4. Financing

21

Mya

nmar

Nat

iona

l Tra

nspo

rt D

evel

opm

ent M

aste

r Pl

an

1,155

5,251

2,164 3,3

71

0

10,000

20,000

30,000

40,000

50,000

60,000

201420

1520

1620

1720

1820

1920

2020

2120

2220

2320

2420

2520

2620

2720

2820

2920

30Gov Expenditure

National Total FCF

Transport

Unit: billion Kyat at 2013 constant prices

Necessary Investment in the Transport Sector under Scenario 2,including national, urban, and rural transport systems,mostly by the public sector, but including investment by the private sector.

1389 billion KyatIn 2015

2164 billion Kyatin2020

5251 billion KyatIn 2030

4. Financing

22

Mya

nmar

Nat

iona

l Tra

nspo

rt D

evel

opm

ent M

aste

r Pl

an

4. Financing

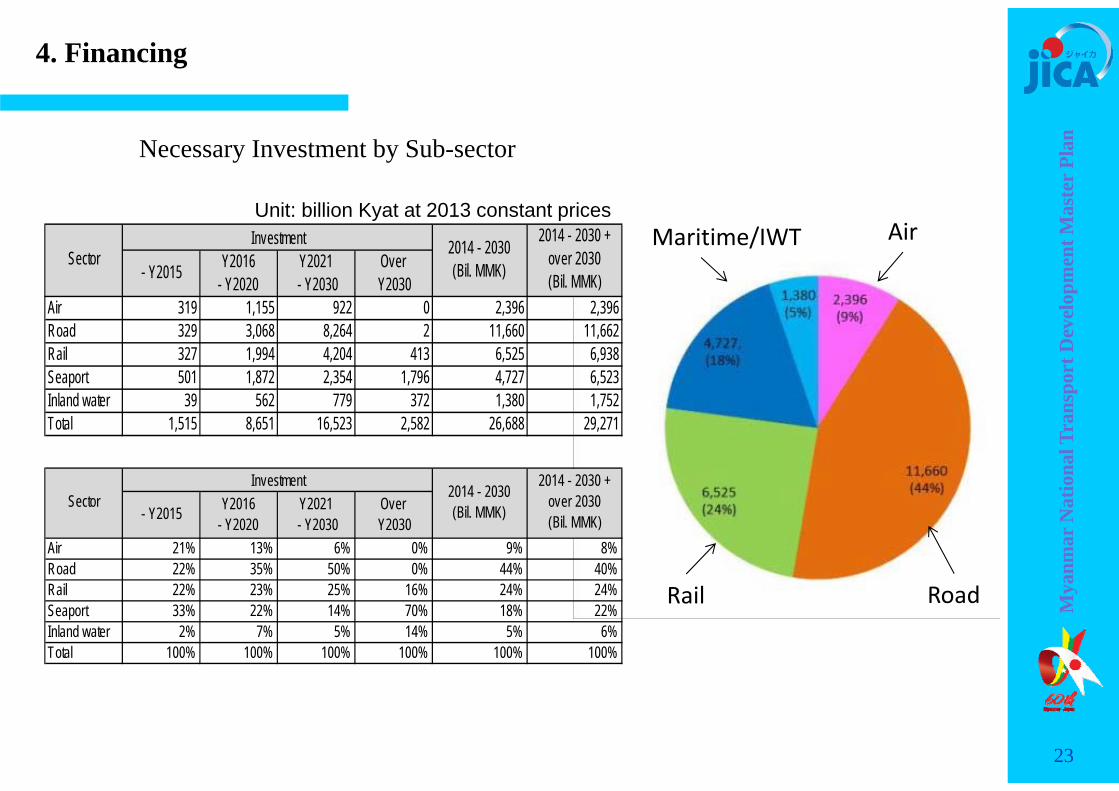

Unit: billion Kyat at 2013 constant prices

Necessary Investment by Sub-sector

Air

RoadRail

Maritime/IWT

23

- Y2015 Y2016- Y2020

Y2021 - Y2030

Over Y2030

Air 319 1,155 922 0 2,396 2,396Road 329 3,068 8,264 2 11,660 11,662Rail 327 1,994 4,204 413 6,525 6,938Seaport 501 1,872 2,354 1,796 4,727 6,523Inland water 39 562 779 372 1,380 1,752Total 1,515 8,651 16,523 2,582 26,688 29,271

2014 - 2030(Bil. MMK)

2014 - 2030 +over 2030(Bil. MMK)

SectorInvestment

- Y2015 Y2016- Y2020

Y2021 - Y2030

Over Y2030

Air 21% 13% 6% 0% 9% 8%Road 22% 35% 50% 0% 44% 40%Rail 22% 23% 25% 16% 24% 24%Seaport 33% 22% 14% 70% 18% 22%Inland water 2% 7% 5% 14% 5% 6%Total 100% 100% 100% 100% 100% 100%

2014 - 2030(Bil. MMK)Sector

Investment 2014 - 2030 +over 2030(Bil. MMK)

Mya

nmar

Nat

iona

l Tra

nspo

rt D

evel

opm

ent M

aste

r Pl

an

2014 – 2020 – Focused Investment to the Trunk Systems• 10,166 billion Kyat (at 2013 constant prices) for national transport systems.• This is about 87% of the total capital formation in the transport sector (11,700

billion Kyat).• The remaining 13% (1,534 billion Kyat) is allocated to urban and rural transport

systems.

2020 – 2030 – Well balanced funding• 16,523 billion Kyat (at 2013 constant prices) for trunk transport systems• This is about 45% of the total capital formation in the transport sector (36,390

billion Kyat)• The remaining 55% is allocated to urban and rural transport systems

24

4. Financing

Mya

nmar

Nat

iona

l Tra

nspo

rt D

evel

opm

ent M

aste

r Pl

an

5. Feasibility Studies

25

The Survey Program ForThe National Transport Development Plan in The Republic of The Union of Myanmar

Rehabilitation and Modernization of Yangon – Mandalay Railway

Presented by Junji Shibata, P.E. Japan, Oriental Consultants Co., Ltd.

Mya

nmar

Nat

iona

l Tra

nspo

rt D

evel

opm

ent M

aste

r Pl

an

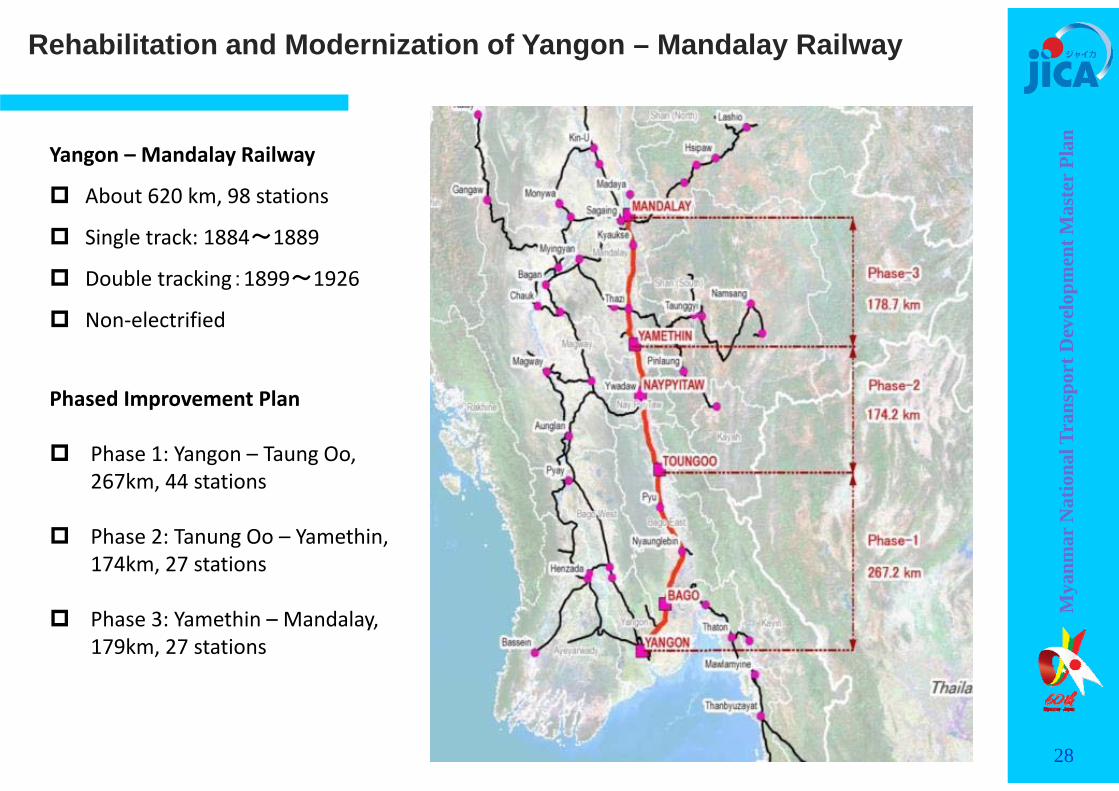

Phased Improvement Plan

Phase 1: Yangon – Taung Oo, 267km, 44 stations

Phase 2: Tanung Oo – Yamethin, 174km, 27 stations

Phase 3: Yamethin – Mandalay, 179km, 27 stations

Yangon – Mandalay Railway

About 620 km, 98 stations

Single track: 1884~1889

Double tracking:1899~1926

Non‐electrified

Rehabilitation and Modernization of Yangon – Mandalay Railway

28

The Survey Program ForThe National Transport Development Plan in The Republic of The Union of Myanmar

Inland Water Transport Facilities Improvement and Development in Mandalay

Mya

nmar

Nat

iona

l Tra

nspo

rt D

evel

opm

ent M

aste

r Pl

an

1a

Jetty 90m x 2 = 180mQuay Depth = - 2.0m

Access BridgeNorth 160mSouth 240m

Cargo Yard3 ha

Access Road304m

Mandalay Port Plan

30

The Survey Program ForThe National Transport Development Plan in The Republic of The Union of MyanmarPre‐Feasibility Study: The East‐West Economic Corridor Road Improvement Project

Mya

nmar

Nat

iona

l Tra

nspo

rt D

evel

opm

ent M

aste

r Pl

an

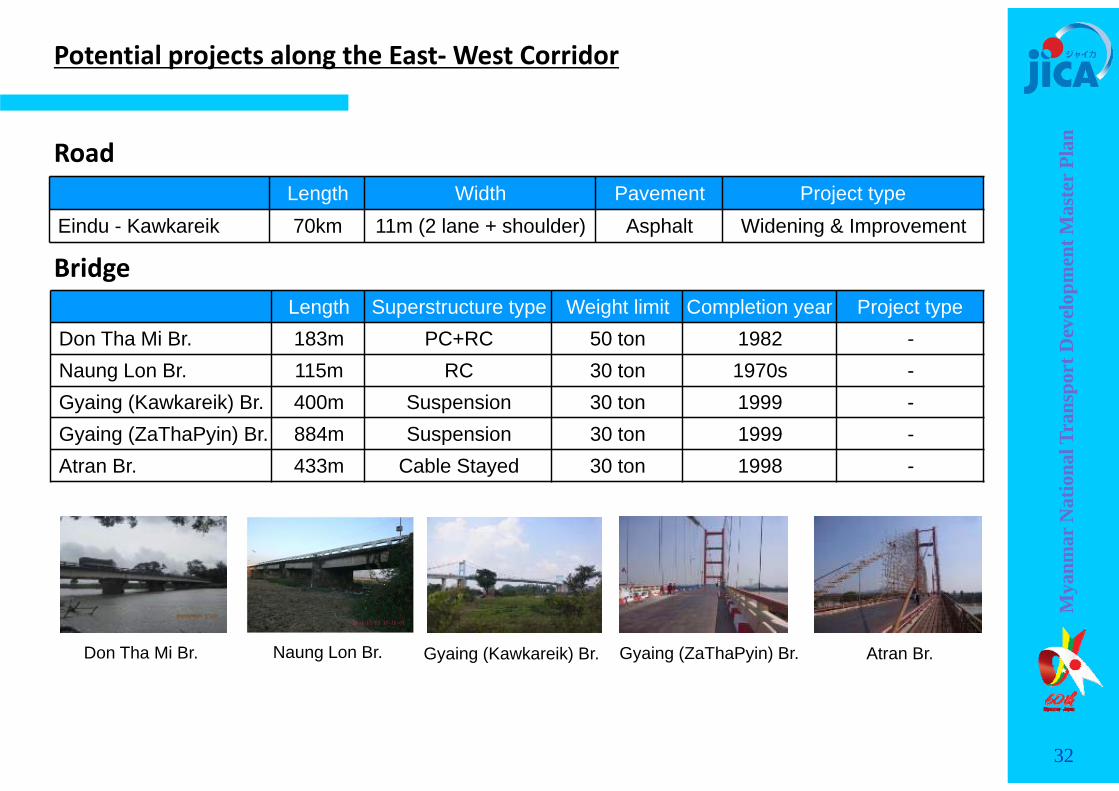

Gyaing (Kawkareik) Br.Don Tha Mi Br. Naung Lon Br. Gyaing (ZaThaPyin) Br. Atran Br.

Length Superstructure type Weight limit Completion year Project typeDon Tha Mi Br. 183m PC+RC 50 ton 1982 -Naung Lon Br. 115m RC 30 ton 1970s -Gyaing (Kawkareik) Br. 400m Suspension 30 ton 1999 -Gyaing (ZaThaPyin) Br. 884m Suspension 30 ton 1999 -Atran Br. 433m Cable Stayed 30 ton 1998 -

Potential projects along the East‐West Corridor

Length Width Pavement Project typeEindu - Kawkareik 70km 11m (2 lane + shoulder) Asphalt Widening & Improvement

Road

Bridge

32

Mya

nmar

Nat

iona

l Tra

nspo

rt D

evel

opm

ent M

aste

r Pl

an

Appendix: Frameworks for National Transport Planning

33

Mya

nmar

Nat

iona

l Tra

nspo

rt D

evel

opm

ent M

aste

r Pl

an

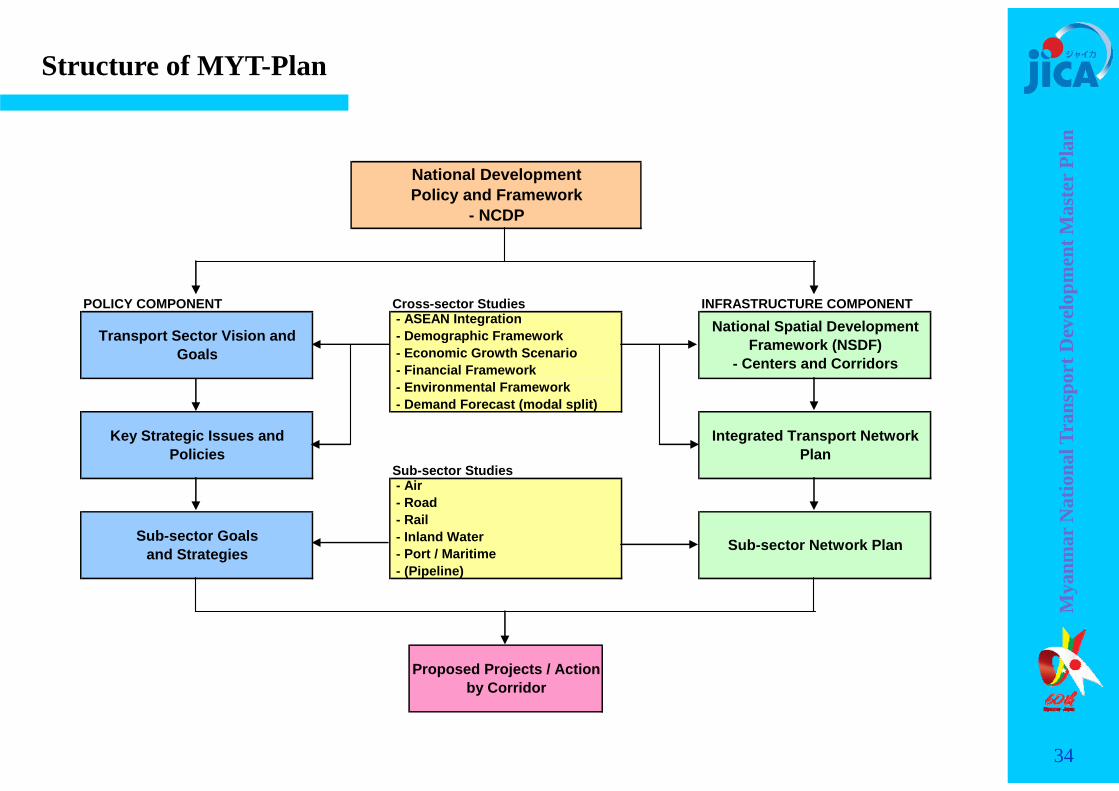

POLICY COMPONENT Cross-sector Studies INFRASTRUCTURE COMPONENT

Sub-sector Studies

Proposed Projects / Actionby Corridor

Key Strategic Issues andPolicies

Integrated Transport NetworkPlan

- Air - Road - Rail - Inland Water - Port / Maritime - (Pipeline)

Sub-sector Goalsand Strategies Sub-sector Network Plan

National DevelopmentPolicy and Framework

- NCDP

Transport Sector Vision andGoals

- ASEAN Integration - Demographic Framework - Economic Growth Scenario - Financial Framework - Environmental Framework - Demand Forecast (modal split)

National Spatial DevelopmentFramework (NSDF)

- Centers and Corridors

Structure of MYT-Plan

34

Mya

nmar

Nat

iona

l Tra

nspo

rt D

evel

opm

ent M

aste

r Pl

an

Considered frameworks Upstream National Development Policies and Plans ASEAN Corporation and Brunei Action Plan Demographic Framework Economic Growth Scenario Financial Framework Environmental Framework National Spatial Development Framework Demand Forecast

Missing issues that need further study toward complete transport planning Industrial development Rural transportation Urban transportation

Note: the existing version of MYT-Plan is limited to the national level trunk transport systems.

2. Frameworks for National Transport Planning

35

Mya

nmar

Nat

iona

l Tra

nspo

rt D

evel

opm

ent M

aste

r Pl

an

5 year plan (2011‐15): 7.7% annual growth (real term) target (Address by H.E. President U Thein Sein in June 2012)

Framework for Economic and Social Reforms (FESR): policy priorities for 2012‐2015 towards the long‐term goals of the national comprehensive development plan (NCDP) –“macroeconomic stability,” “inclusive development,” “quick win” and “sustainability”

National Comprehensive Development Plan (NCDP): Long term plan up to 2030; expected to be completed in July 2014

Myanmar Comprehensive Development Vision (MCDV): Long term development vision up to 2035; Collaboration with ERIA

Spatial Structure Development Concept by DHSHD

36

1. Upstream National Development Policies and Plans

Mya

nmar

Nat

iona

l Tra

nspo

rt D

evel

opm

ent M

aste

r Pl

an

Year 2010 2015 2020 2025 2030 2035 2040

High 59.8 63.8 67.8 71.6 75.0 78.0 80.7

Moderate 59.8 63.6 66.9 69.8 71.9 73.3 73.8

Low 59.8 63.4 66.5 68.9 70.3 70.9 70.4

Unit: million persons

55,000

60,000

65,000

70,000

75,000

80,000

85,000

2010 2015 2020 2025 2030 2035 2040

Population (000 persons)

Year

High Middle Low

Source: MYT‐Plan JICA Study Team

Likelygrowth scenario

3 Demographic Framework

37

Mya

nmar

Nat

iona

l Tra

nspo

rt D

evel

opm

ent M

aste

r Pl

an

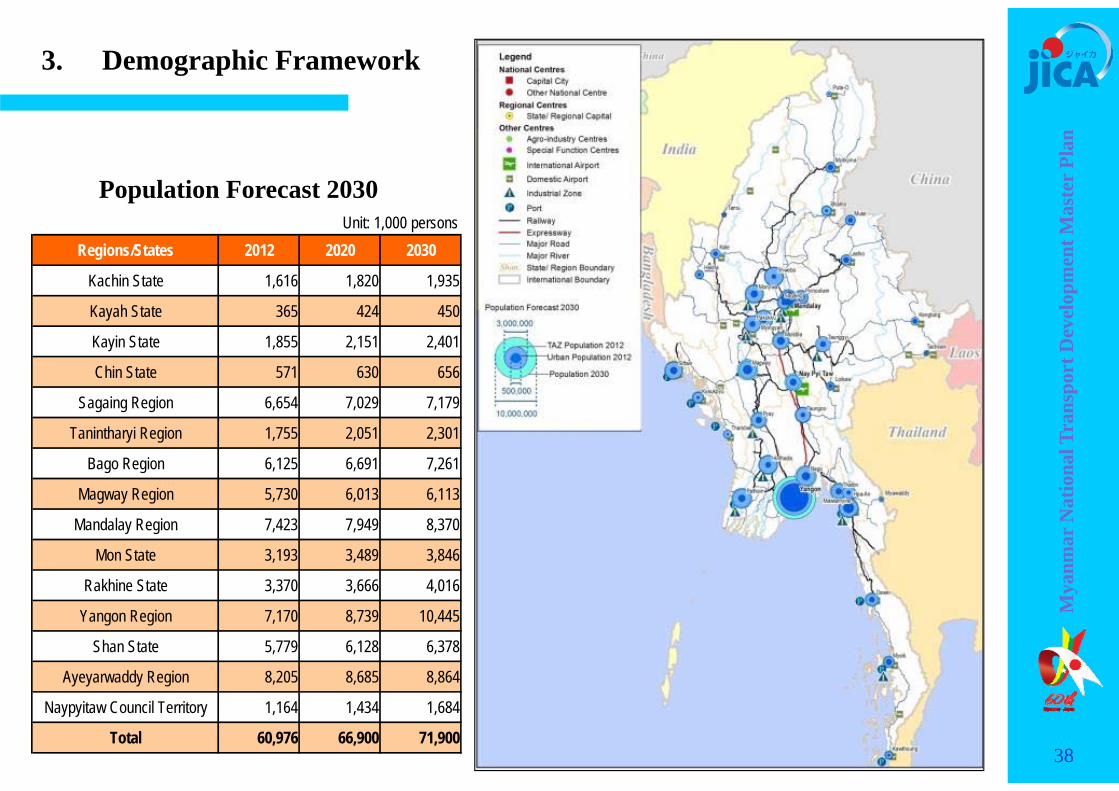

Population Forecast 2030Unit: 1,000 persons

Regions/States 2012 2020 2030

Kachin State 1,616 1,820 1,935

Kayah State 365 424 450

Kayin State 1,855 2,151 2,401

Chin State 571 630 656

Sagaing Region 6,654 7,029 7,179

Tanintharyi Region 1,755 2,051 2,301

Bago Region 6,125 6,691 7,261

Magway Region 5,730 6,013 6,113

Mandalay Region 7,423 7,949 8,370

Mon State 3,193 3,489 3,846

Rakhine State 3,370 3,666 4,016

Yangon Region 7,170 8,739 10,445

Shan State 5,779 6,128 6,378

Ayeyarwaddy Region 8,205 8,685 8,864

Naypyitaw Council Territory 1,164 1,434 1,684

Total 60,976 66,900 71,900

3. Demographic Framework

38

Mya

nmar

Nat

iona

l Tra

nspo

rt D

evel

opm

ent M

aste

r Pl

an

0

100

200

300

400

500

600

700

Index (2010=100

)Scenario 1 Scenario 2 Scenario 3

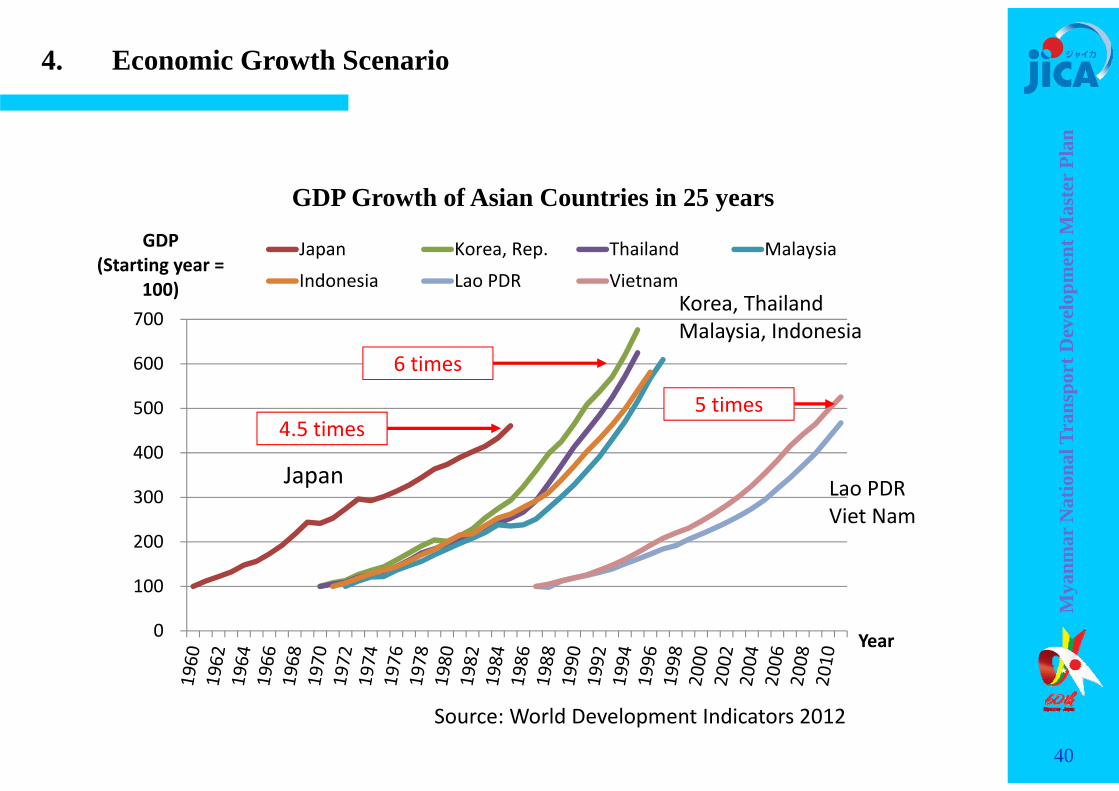

Economic Growth Scenarios: 7.7% GDP growth target from 2011 to 2015 (Myanmar Government)7 to 8 % GDP growth until 2030 (“Myanmar in Transition”, ADB)6.0 times

5.4 times

4.3 times

Source: MYT‐Plan JICA Study Team

Scenario 17.7% GDP growth during 2015‐35; Average growth rate of 7.5% from 2011 to 2035

Scenario 2 (recommended)7.2% GDP growth during 2013‐35; Average growth rate of 7.0% from 2011 to 2035

Scenario 36.0% GDP growth during 2014‐35; Debt sustainability analysis by IMF; trend growth

Growth of economy (real GDP)

39

4. Economic Growth Scenario

Mya

nmar

Nat

iona

l Tra

nspo

rt D

evel

opm

ent M

aste

r Pl

an

0

100

200

300

400

500

600

700

GDP(Starting year =

100)

Year

Japan Korea, Rep. Thailand Malaysia

Indonesia Lao PDR Vietnam

GDP Growth of Asian Countries in 25 years

6 times

5 times

Lao PDRViet Nam

Japan

4.5 times

Korea, ThailandMalaysia, Indonesia

Source: World Development Indicators 2012

40

4. Economic Growth Scenario

Mya

nmar

Nat

iona

l Tra

nspo

rt D

evel

opm

ent M

aste

r Pl

an

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

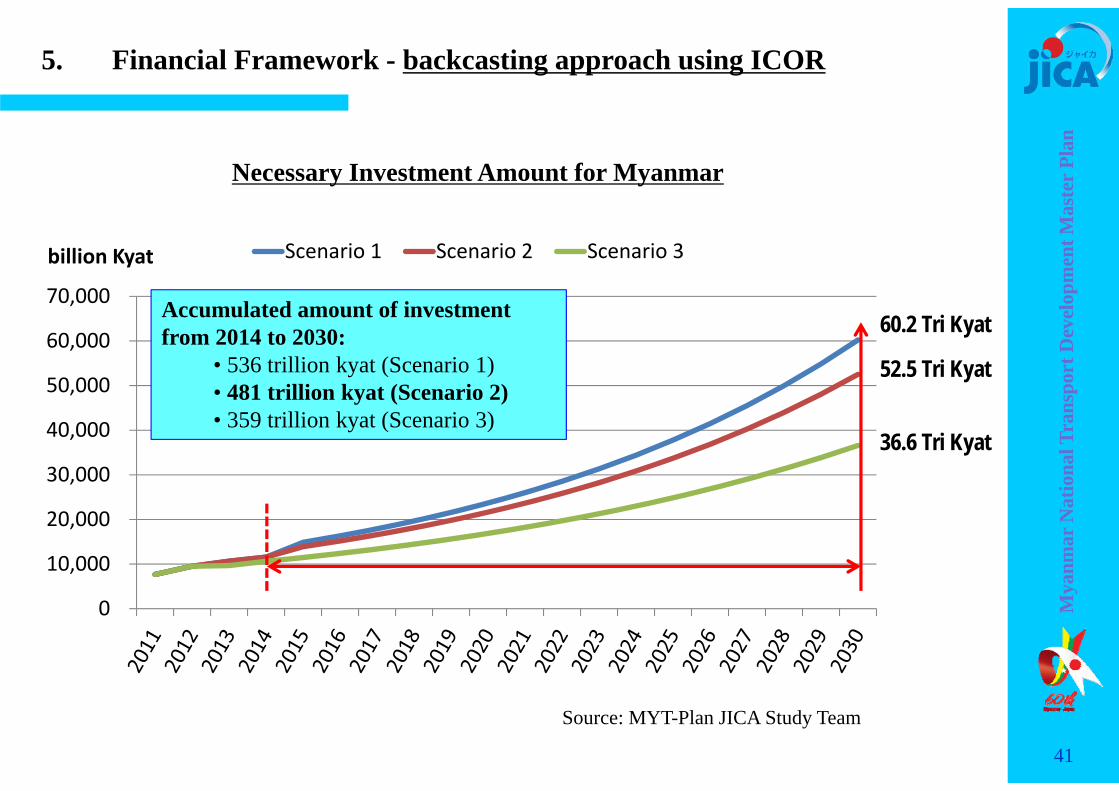

billion Kyat Scenario 1 Scenario 2 Scenario 3

Necessary Investment Amount for Myanmar

Source: MYT-Plan JICA Study Team

60.2 Tri Kyat

36.6 Tri Kyat

52.5 Tri Kyat

Accumulated amount of investmentfrom 2014 to 2030:

• 536 trillion kyat (Scenario 1)• 481 trillion kyat (Scenario 2)• 359 trillion kyat (Scenario 3)

5. Financial Framework - backcasting approach using ICOR

41

Mya

nmar

Nat

iona

l Tra

nspo

rt D

evel

opm

ent M

aste

r Pl

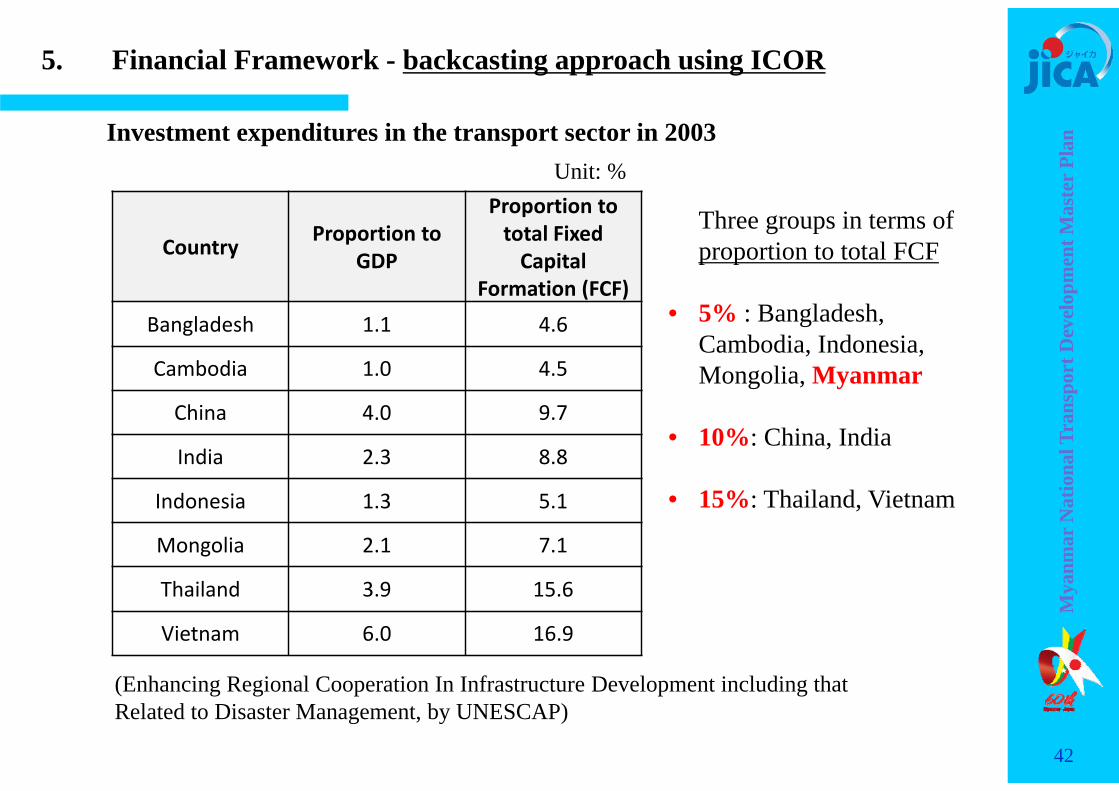

anInvestment expenditures in the transport sector in 2003

Country Proportion to GDP

Proportion to total Fixed Capital

Formation (FCF)Bangladesh 1.1 4.6

Cambodia 1.0 4.5

China 4.0 9.7

India 2.3 8.8

Indonesia 1.3 5.1

Mongolia 2.1 7.1

Thailand 3.9 15.6

Vietnam 6.0 16.9

Unit: %

(Enhancing Regional Cooperation In Infrastructure Development including that Related to Disaster Management, by UNESCAP)

Three groups in terms of proportion to total FCF

• 5% : Bangladesh, Cambodia, Indonesia, Mongolia, Myanmar

• 10%: China, India

• 15%: Thailand, Vietnam

42

5. Financial Framework - backcasting approach using ICOR

Mya

nmar

Nat

iona

l Tra

nspo

rt D

evel

opm

ent M

aste

r Pl

an

Unit: %Investment expenditures in the transport sector in Myanmar

Note 1: Higher level investment in 2004/05 and 2005/06 is due to Yangon – Mandalay Expressway and Nay Pyi Taw development.

Note 2: Transport capital expenditure: Union government budget + State administrative organization budget + state economic enterprises, calculated by MYT-Plan JICA Study Team from Myanmar Data CD-ROM 2010 and 2011

Fiscal YearProportion to Total

Fixed Capital Formation

Proportion to Total Government Capital

Expenditure

2004‐05 12.8 21.0

2005‐06 14.4 29.7

2006‐07 7.5 14.0

2007‐08 6.9 13.5

2008‐09 4.8 12.0

2009‐10 5.3 13.4

2010‐11 3.5 9.9

43

5. Financial Framework - backcasting approach using ICOR

Mya

nmar

Nat

iona

l Tra

nspo

rt D

evel

opm

ent M

aste

r Pl

an

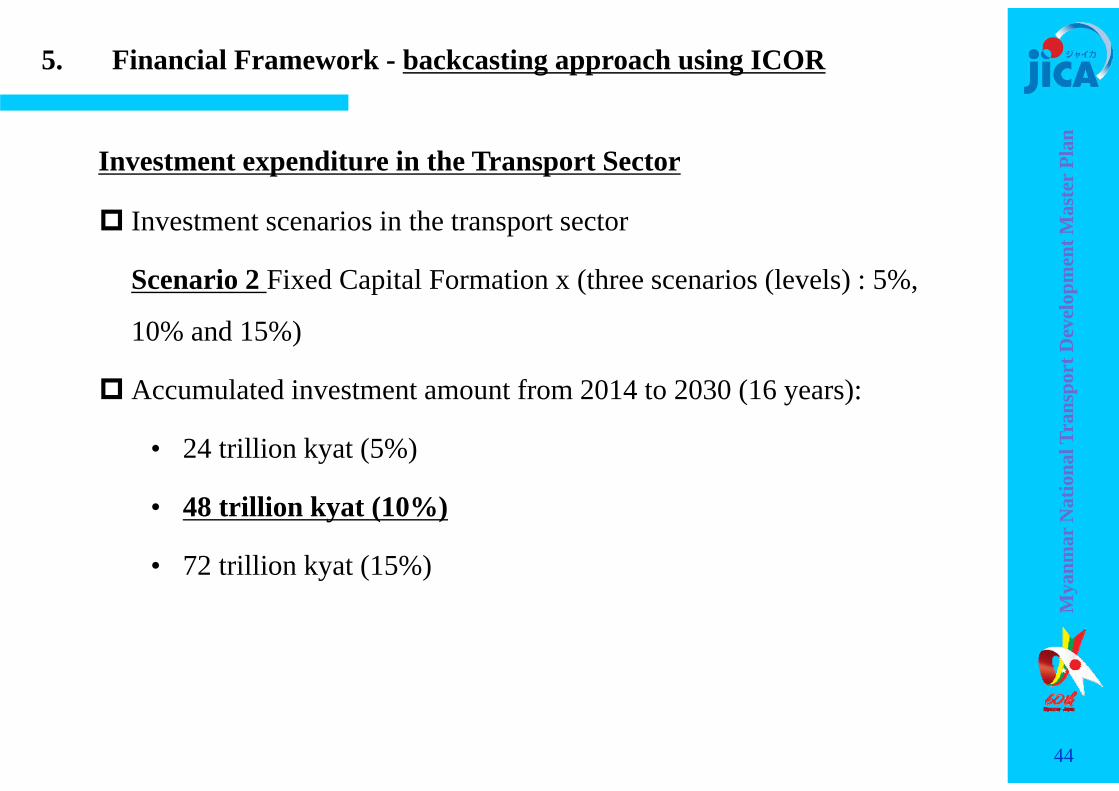

Investment expenditure in the Transport Sector

Investment scenarios in the transport sector

Scenario 2 Fixed Capital Formation x (three scenarios (levels) : 5%,

10% and 15%)

Accumulated investment amount from 2014 to 2030 (16 years):

• 24 trillion kyat (5%)

• 48 trillion kyat (10%)

• 72 trillion kyat (15%)

44

5. Financial Framework - backcasting approach using ICOR

Mya

nmar

Nat

iona

l Tra

nspo

rt D

evel

opm

ent M

aste

r Pl

anInvestment expenditure scenarios in the transport sector

01,0002,0003,0004,0005,0006,0007,0008,000

Investment in the transport sector (Kyat

billion)

5% of total fixed capital formation 10% of total ifixed capital formation15% of total fixed capital formation

695 billion Kyat

2084 billion Kyat

1389 billion Kyat

Note: 1 billion Kyat = 1.14 million USD (1 USD=880Kyat) = 1.08 Oku Yen (1USD=95Yen)

1082 billion Kyat

3246 billion Kyat

2164 billion Kyat2084 billion Kyat

7877 billion Kyat

5251 billion Kyat

45

5. Financial Framework - backcasting approach using ICOR

Mya

nmar

Nat

iona

l Tra

nspo

rt D

evel

opm

ent M

aste

r Pl

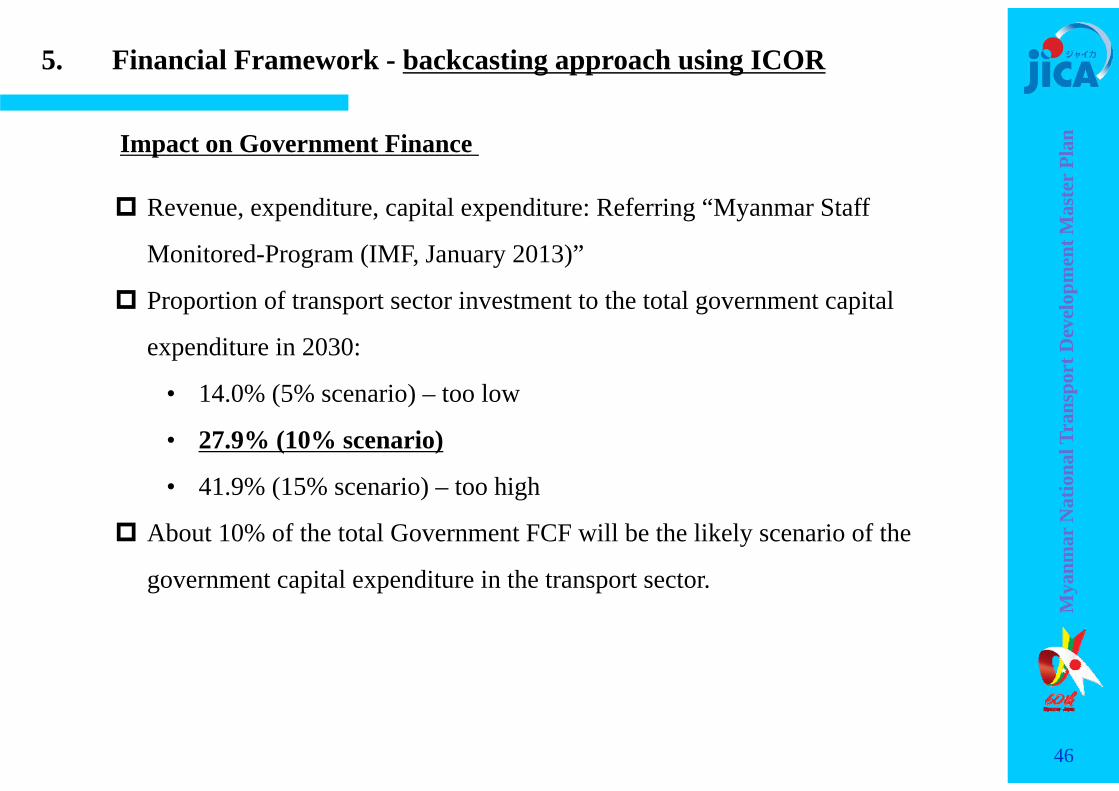

anImpact on Government Finance

Revenue, expenditure, capital expenditure: Referring “Myanmar Staff

Monitored-Program (IMF, January 2013)”

Proportion of transport sector investment to the total government capital

expenditure in 2030:

• 14.0% (5% scenario) – too low

• 27.9% (10% scenario)

• 41.9% (15% scenario) – too high

About 10% of the total Government FCF will be the likely scenario of the

government capital expenditure in the transport sector.

46

5. Financial Framework - backcasting approach using ICOR

Mya

nmar

Nat

iona

l Tra

nspo

rt D

evel

opm

ent M

aste

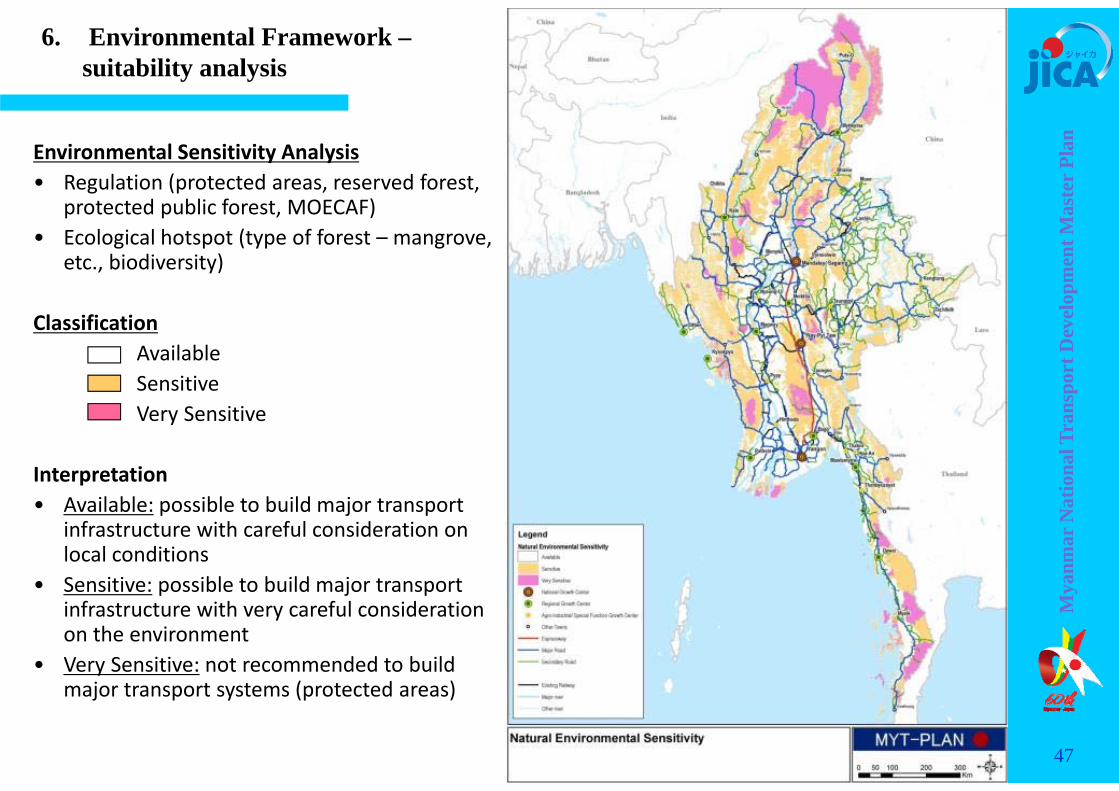

r Pl

anEnvironmental Sensitivity Analysis• Regulation (protected areas, reserved forest,

protected public forest, MOECAF)• Ecological hotspot (type of forest – mangrove,

etc., biodiversity)

ClassificationAvailableSensitiveVery Sensitive

Interpretation• Available: possible to build major transport

infrastructure with careful consideration on local conditions

• Sensitive: possible to build major transport infrastructure with very careful consideration on the environment

• Very Sensitive: not recommended to build major transport systems (protected areas)

6. Environmental Framework –suitability analysis

47

Mya

nmar

Nat

iona

l Tra

nspo

rt D

evel

opm

ent M

aste

r Pl

anRisk Analysis on Natural Disaster• Flood‐prone areas (days in flood) • Landslide‐prone areas (slope, rainfall,

geology, distance from active faults)• Earthquake (seismic areas in the past)• Cyclone (route, frequency)

ClassificationLowMediumHigh

Interpretation• Low: major (trunk) transport system can be

developed safely• Medium: Disaster preventive measures are

needed.• High: not recommended to build major

systems other than local systems

6. Environmental Framework –suitability analysis

48

Mya

nmar

Nat

iona

l Tra

nspo

rt D

evel

opm

ent M

aste

r Pl

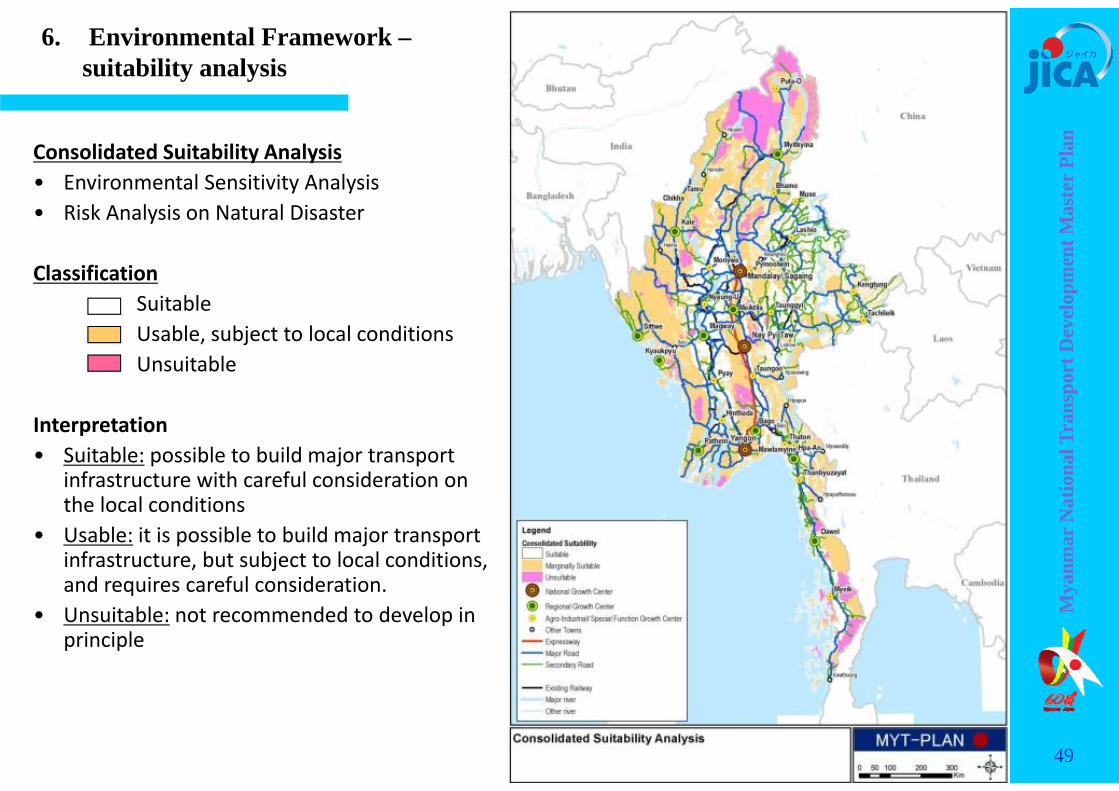

anConsolidated Suitability Analysis• Environmental Sensitivity Analysis• Risk Analysis on Natural Disaster

ClassificationSuitableUsable, subject to local conditionsUnsuitable

Interpretation• Suitable: possible to build major transport

infrastructure with careful consideration on the local conditions

• Usable: it is possible to build major transport infrastructure, but subject to local conditions, and requires careful consideration.

• Unsuitable: not recommended to develop in principle

49

6. Environmental Framework –suitability analysis

Mya

nmar

Nat

iona

l Tra

nspo

rt D

evel

opm

ent M

aste

r Pl

an

National Growth Centers: Nay Pyi Taw, Yangon, Mandalay / Sagaing

Regional Growth Centers: Myitkyina, Sittwe/Kyaukphyu, Pathein, Bago(Hanthawaddy), Mawlamyine, Dawei

Agro‐industrial Centers: Lashio, Shwebo, Kale, Monywa, Meiktila, Taunggyi, Taungoo , Magway, Pyay, Hinthada, Thaton, Hpa‐an

Special Function Growth Centers: Muse, Tamu, Nyaung‐U, Kengtung, Tachileik, Myawaddy, Myeik

MYT‐Plan NSDF Concept ofMulti‐Centric Balanced Development Strategy

7. National Spatial Development Framework (NSDF)

50

Mya

nmar

Nat

iona

l Tra

nspo

rt D

evel

opm

ent M

aste

r Pl

an

1a

Consistency with DHSHD Concept

Capital City(Administrative, Transport & Logistic Hub)

National Economic Growth Center(SEZ, Port, Int’l Airport, Trading, Financial)

Other Growth Center(Town with more than 50,000 inhabitants)

Secondary Regional Growth Center(Administrative, Transport & Logistic Hub)

7. National Spatial Development Framework (NSDF)

51

Mya

nmar

Nat

iona

l Tra

nspo

rt D

evel

opm

ent M

aste

r Pl

an

8. Transport Demand – passenger movement

2013 2030 52

Mya

nmar

Nat

iona

l Tra

nspo

rt D

evel

opm

ent M

aste

r Pl

an

8. Transport Demand – freight movement

2013 2030 53

Mya

nmar

Nat

iona

l Tra

nspo

rt D

evel

opm

ent M

aste

r Pl

an

9. Summary of Transport Sub‐sector in Myanmar

AIR TRANSPORT INLAND WATER ROAD RAILWAY MARITIME

OWNERSHIP - Ministry Min. of Transport (MOT) Min. of Transport (MOT) Min. of Construction (MOC) Min. of Rail Transport

(MORT)Min. of Transport (MOT)

- Infrastructure Dept of Civil Aviation Directorate of WaterResources & Improvementof River Systems (DWIR)

Department of PublicWorks (DPW)

Myanma Railways Co. Myanma Port Authority(MPA)

- Services Myanma Airways (domestic& international)

Inland Water Transport(IWT)

Road Transport Enterprise Myanma Railways Co. Myanma Five Star Line

6 other domestic carriers,e.g. Air Bagan, YangonAirways

Several private operators Other shipping lines, e.g.,Myanmar-Taiwan Co.Anawar Shipping

REGULATORY - Crew Flight Standard Division DMA DMA - Vehicle/Vessel Airworthiness Division DMA Vehicle & Driver licensing

by Road TransportAdministration, under

Directorate of MarineAdministration (DMA)

- Terminal/Port Aerodrome Standards &Safety Division

DWIR MPA

54

Mya

nmar

Nat

iona

l Tra

nspo

rt D

evel

opm

ent M

aste

r Pl

an

AIR TRANSPORT INLAND WATER ROAD RAILWAY MARITIME

DEMAND - Pax 3.5m domestic (2012);

2.0m international22m pax in 2011 2,028 million pax-km

(2011)67.6m pax in 2011; using248 pax-trains/day

No data. Likely to beinsignificant

- Freight negligible 4.7m tons of cargo in 2011 25.2m tons carried ontrucks (2011)

3.3m tons in 2011; using21 freight trains/day

22m MT in 2012

SUPPLY 27 Domestic Airports(paved)

6,650 km of navigable rivers;5 river network

142,395km of roads; ofwhich 18,740 are national

About 5,865km routelength

9 ports under MPA

28 unpaved airports More than 400 rivercraftsowned by IWT

39,241 km under the MOC 386 locomotives

3 International Airports, butonly 2 have int'l flights

Two jetties: Yangon &Pathein. No fixed structure inother riverports

432,504 vehicles + 1.9mMCs in 2011

1,252 pax coaches

Buses of various sizes,mostly private operated

3,311 freight wagons

REGULATORY - Crew Flight Standard Division DMA DMA - Vehicle/Vessel Airworthiness Division DMA Vehicle & Driver licensing

by Road TransportAdministration, under

Directorate of MarineAdministration (DMA)

- Terminal/Port Aerodrome Standards &Safety Division

DWIR MPA

9. Summary of Transport Sub‐sector in Myanmar (continued)

55

Mya

nmar

Nat

iona

l Tra

nspo

rt D

evel

opm

ent M

aste

r Pl

an

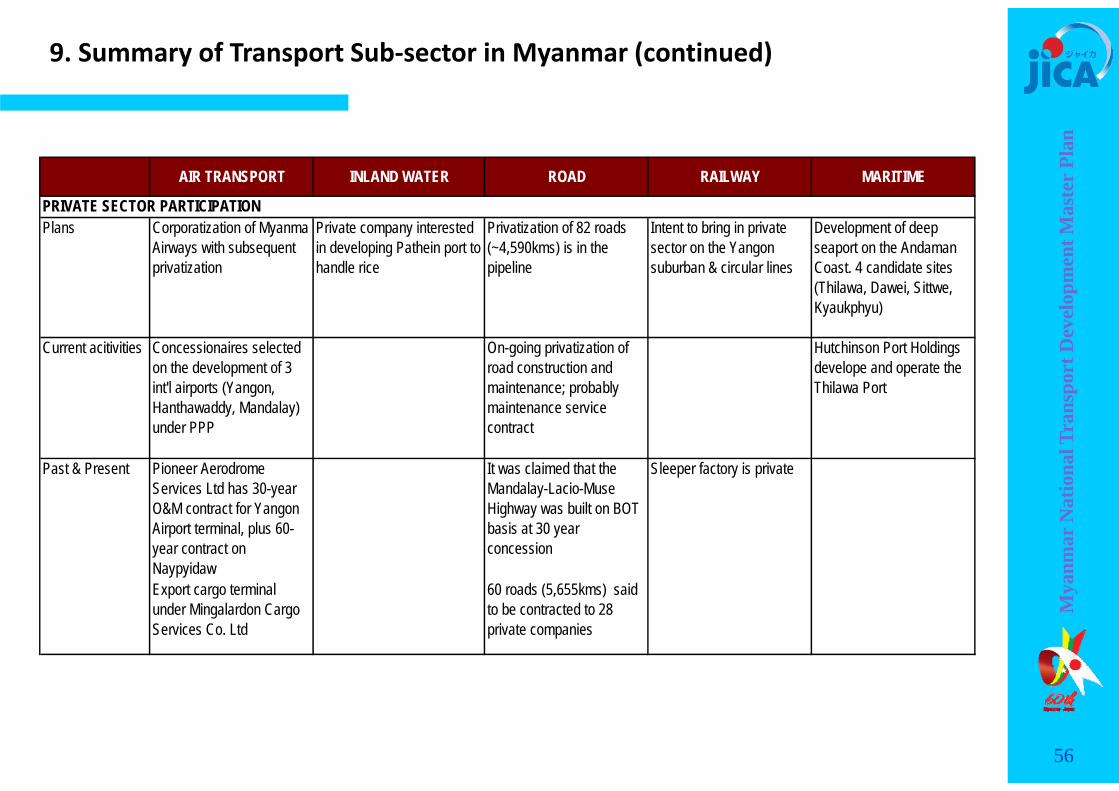

AIR TRANSPORT INLAND WATER ROAD RAILWAY MARITIME

Plans Corporatization of MyanmaAirways with subsequentprivatization

Private company interestedin developing Pathein port tohandle rice

Privatization of 82 roads(~4,590kms) is in thepipeline

Intent to bring in privatesector on the Yangonsuburban & circular lines

Development of deepseaport on the AndamanCoast. 4 candidate sites(Thilawa, Dawei, Sittwe,Kyaukphyu)

Current acitivities Concessionaires selectedon the development of 3int'l airports (Yangon,Hanthawaddy, Mandalay)under PPP

On-going privatization ofroad construction andmaintenance; probablymaintenance servicecontract

Hutchinson Port Holdingsdevelope and operate theThilawa Port

Past & Present Pioneer AerodromeServices Ltd has 30-yearO&M contract for YangonAirport terminal, plus 60-year contract onNaypyidaw

It was claimed that theMandalay-Lacio-MuseHighway was built on BOTbasis at 30 yearconcession

Sleeper factory is private

Export cargo terminalunder Mingalardon CargoServices Co. Ltd

60 roads (5,655kms) saidto be contracted to 28private companies

PRIVATE SECTOR PARTICIPATION

9. Summary of Transport Sub‐sector in Myanmar (continued)

56