Embed Size (px)

Citation preview

2010 Tokyo AnalystM ti P t tiMeeting Presentation

Slides

September 13, 2010September 13, 2010

For more information contact:Ken Janke Jr. or

Robin Wilkeyy800.235.2667, Option 3

Fax: 706.324.6330aflac.com

Aflac Worldwide Headquarters1932 Wynnton RoadyColumbus, GA 31999

ABOUT AFLAC

When a policyholder gets sick or hurt, Aflac pays cash benefits fast. For 55 years, Aflac insurance policies have given policyholders the opportunity to focus on recovery, not financial stress. In the United States, Aflac is the number one provider of guaranteed-renewable insurance. In Japan, Aflac is the number one insurance company in terms of individual insurance policies in force. Aflac insurance products provide protection to more than 50 million people worldwide. For four consecutive years, Aflac has been recognized by Ethisphere magazine as one of the World's Most Ethical Companies, and Forbes magazine named Aflac as America's Best-Managed Company in the Insurance category. In 2010, Fortune magazine recognized Aflac as one of the 100 Best Companies to Work For in America for the twelfth consecutive year and also included Aflac on its list of Most Admired Companies for the ninth time. Aflac Incorporated is a Fortune 500 company listed on the New York Stock Exchange under the symbol AFL. To find out more about Aflac, visit aflac.com.

FORWARD-LOOKING INFORMATION

The Private Securities Litigation Reform Act of 1995 provides a “safe harbor” to encourage companies to provide prospective information, so long as those informational statements are identified as forward-looking and are accompanied by meaningful cautionary statements identifying important factors that could cause actual results to differ materially from those included in the forward-looking statements. We desire to take advantage of these provisions. This document contains cautionary statements identifying important factors that could cause actual results to differ materially from those projected herein, and in any other statements made by Company officials in communications with the financial community and contained in documents filed with the Securities and Exchange Commission (SEC).

Forward-looking statements are not based on historical information and relate to future operations, strategies, financial results or other developments. Furthermore, forward-looking information is subject to numerous assumptions, risks and uncertainties. In particular, statements containing words such as “expect,” “anticipate,” “believe,” “goal,” “objective,” “may,” “should,” “estimate,” “intends,” “projects,” “will,” “assumes,” “potential,” “target” or similar words as well as specific projections of future results, generally qualify as forward-looking. Aflac undertakes no obligation to update such forward-looking statements. We caution readers that the following factors, in addition to other factors mentioned from time to time, could cause actual results to differ materially from those contemplated by the forward-looking statements: difficult conditions in global capital markets and the economy; governmental actions for the purpose of stabilizing the financial markets; defaults and downgrades in certain securities in our investment portfolio; impairment of financial institutions; credit and other risks associated with Aflac’s investment in perpetual securities; differing judgments applied to investment valuations; subjective determinations of amount of impairments taken on our investments; limited availability of acceptable yen-denominated investments; concentration of our investments in any particular sector; concentration of business in Japan; ongoing changes in our industry; exposure to significant financial and capital markets risk; fluctuations in foreign currency exchange rates; significant changes in investment yield rates; deviations in actual experience from pricing and reserving assumptions; subsidiaries’ ability to pay dividends to Aflac Incorporated (the Parent Company); changes in law or regulation by governmental authorities; ability to attract and retain qualified sales associates and employees; decreases in our financial strength or debt ratings; ability to continue to develop and implement improvements in information technology systems; changes in U.S. and/or Japanese accounting standards; failure to comply with restrictions on patient privacy and information security; level and outcome of litigation; ability to effectively manage key executive succession; catastrophic events; and failure of internal controls or corporate governance policies and procedures.

1

Introduction to Aflac JapanTohru TonoikePresident Chief Operating OfficerPresident, Chief Operating Officer Aflac Japan

Life Insurance Policies in Force (FSA Basis, In Millions)

100

120

140

First sector Third sector

109.3 109.6 109.8110.0 110.0 113.0 117.1

Source: Life Insurance Association of Japan

0

20

40

60

80

3/04 3/05 3/06 3/07 3/08 3/09 3/10

20.3

The Number One Life Insurer in Japan(Policies in Force, FSA Basis, In Millions)

12

14

16

18

20 Aflac = No. 1

0

2

4

6

8

10

3/75 3/80 3/85 3/90 3/95 3/00 3/103/05

2

Third Sector Contribution to Life Insurance Industry New Policy Sales(FSA Basis, In Thousands)

8,000

10,000

12,000

14,000

Life industryThird sector

Source: Life Insurance Association of Japan, Insurance Research Institute

0

2,000

4,000

6,000

2002 2003 2004 2005 2006 2007 2008 200944.2% 47.7% 44.9%47.4%41.4% 40.3% 41.7%34.3%

% Third Sector

Japan’s Aging Population andDeclining Fertility Rate(In Thousands)

80,000

100,000

120,000

140,000 Actual Estimate

0

20,000

40,000

60,000

1950 1960 1970 1980 1990 2000 2010 2020 2030 2040 2050

Juvenile (0-14) Productive (15-64) Retirement (65+)

Source: National Institute of Population and Social Security Research, Future Estimated Population of Japan, 12/06

National Medical Expenses(Yen in Trillions)

10

12

14

60

70

80

90

100

Medical expenses For elderly National medical expenses to national income

%¥

¥698.9%

9.9%

13.2%

0

2

4

6

8

0

10

20

30

40

50

60

2007 2010 2025

Source: Ministry of Health, Labor and Welfare, 7/08

¥33¥41

3

Competitors in the Third Sector(Number of Life and Non-life Insurance Companies)

30

40

50

37

33

40

30

43

31

44

30

46

31

4747

3129

27

46

25

45

25

48

0

10

20

12/01 12/02 12/03 12/04 12/05 12/06 12/07 12/08 4/09 6/10

Stand-alone cancer Stand-alone medical

Reflects results of company mergers and companies that have discontinued sales Source: Web sites of each company

2525

21.3 21.5 21.7 22.8 23.5

60

80

100

Market Growth Market Share

Aflac’s Share of In-Force Business: Cancer(FSA Basis, Stand-alone, Life Industry Only)

%

(Policies in Thousands)

18,500

19,000

0

20

40

60

3/06 3/07 3/08 3/09 3/10

Aflac Others

17,000

17,500

18,000

3/06 3/07 3/08 3/09 3/10

Source: Insurance Research Institute,

Life Insurance Association of Japan

Aflac’s Share of New Business: Cancer(FSA Basis, Stand-alone, Life Industry Only)

60

80

100

1 000

1,200

1,400

1,600

Market Growth Market Share

%

(Policies in Thousands)

Source: Insurance Research Institute,Life Insurance Association of Japan

0

20

40

60

3/06 3/07 3/08 3/09 3/10

Aflac Others

0

200

400

600

800

1,000

3/06 3/07 3/08 3/09 3/10

4

80

100

Market Growth Market Share

Aflac’s Share of In-Force Business: Medical(FSA Basis, Stand-alone, Life Industry Only)

%

(Policies in Thousands)

20,000

22,000

24,000

0

20

40

60

3/06 3/07 3/08 3/09 3/10

Aflac Others

10,000

12,000

14,000

16,000

18,000

3/06 3/07 3/08 3/09 3/10

Source: Insurance Research Institute,Life Insurance Association of Japan

Aflac’s Share of New Business: Medical(FSA Basis, Stand-alone, Life Industry Only)

60

80

100

Market Growth Market Share

%

(Policies in Thousands)

2,500

3,000

3,500

0

20

40

60

3/06 3/07 3/08 3/09 3/10

Aflac Others

0

500

1,000

1,500

2,000

3/06 3/07 3/08 3/09 3/10

Source: Insurance Research Institute,

Life Insurance Association of Japan

Insurance Product Penetration (Individual Basis)

60

80

100 %

77.7 77.979.9

73.069.3

71.3

0

20

40

2001 2004 2007

Life insurance Medical insurance Cancer insurance

Source: Japan Institute of Life Insurance

21.225.3

31.2

5

Economic IndicatorsComposite Indexes (2005=100)

85

90

95

100

105

Source: Cabinet OfficeThe periods indicated in light blue show economic expansion period

70

75

80

1/02 1/03 1/04 1/05 1/06 1/07 1/08 1/09 1/10

Leading Indicator Coincident Indicator

Aflac Japan’s Competitive Strengths

Products

Distribution

Internal Controls

Administrative Efficiency

Financial Strength

Midterm Management Policy

Midterm

Midterm Management Policy(2011-2013)

Company that gains confidence of all the stakeholders as an insurer that exists to “Support Your Way of Life”

Management Policy

(2008-2010)

Build a “Strong management base”

Establish a system that enables timely provision of products and services that contribute to customers’ high satisfaction and stable growth of new businesses and profits.

6

Aflac Japan Marketing and SalesKoji AriyoshiFirst Senior Vice President;First Senior Vice President;Director of Marketing and SalesAflac Japan

Aflac Japan’s Product Line

1st Sector 3rd Sector

Children Child Endowment

Young

Middle

Senior

Ordinary Life

Cancer Medical

7

Aflac Japan’s Product Mix

60

80

100 Others

Child Endowment

Life Insurance

%

0

20

40

1992 2000 6/2010

Medical

Rider Max

Cancer

New Business in Policies(FSA Basis, Policies in Thousands )

Nippon

Sumitomo

Aflac

1,400

1,600

1,800

Dai-ichiSumitomo

Alico

*Excludes Kampo

600

800

1,000

1,200

3/05 3/06 3/07 3/08 3/09 3/10

Meiji-Yasuda

Individual Policies in Force(FSA Basis, Policies in Thousands)

15,000

20,000

25,000

D i i hi

Nippon

Aflac

*Excludes Kampo

0

5,000

10,000

3/05 3/06 3/07 3/08 3/09 3/10

Dai-ichi

Alico

SumitomoMeiji-Yasuda

8

Consumers’ Brand Association with Cancer Insurance(Unaided Recognition Ratio)

40

50

60 Aflac Alico Nippon%

0

10

20

30

12/05 07/06 12/06 8/07 12/07 8/08 1/09 6/09 12/09 6/10

Source: Dentsu and Nippon Research Center

Consumers’ Brand Association with Medical Insurance(Unaided Recognition Ratio)

40

50

60 Aflac Alico Nippon%

Source: Dentsu and Nippon Research Center

0

10

20

30

12/05 7/06 12/06 8/07 12/07 8/08 1/09 6/09 12/09 6/10

MedicalCancer

The Most Preferred Insurer forCancer and Medical Insurance

Aflac30

3431

29

8/10 4/10 12/09 8/09

Aflac13

201617

8/10 4/10 12/09 8/09

% %0 10 20 30 40

Nippon

Alico

5

3

8

7

6

6

5

8

0 5 10 15 20

Nippon

Alico

8

5

9

5

7

6

7

7

Source: Macromill, Inc., 8/09, 12/09, 4/10, 8/10

9

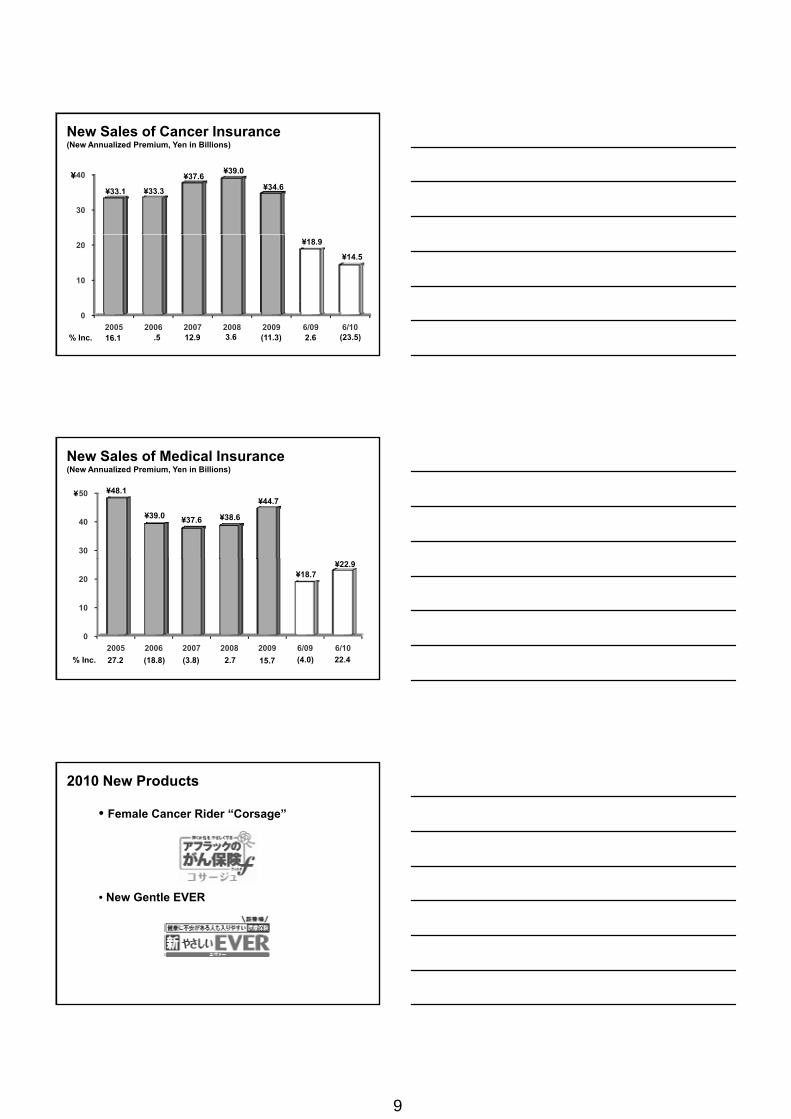

New Sales of Cancer Insurance(New Annualized Premium, Yen in Billions)

30

40 ¥

¥33.3

¥37.6¥39.0

¥34.6¥33.1

0

10

20

2005 2006 2007 2008 2009 6/09 6/10% Inc. 12.9.5 3.6 2.6

¥18.9

(11.3) (23.5)

¥14.5

16.1

New Sales of Medical Insurance(New Annualized Premium, Yen in Billions)

30

40

50 ¥

¥39.0 ¥37.6 ¥38.6

¥44.7¥48.1

0

10

20

2005 2006 2007 2008 2009 6/09 6/10

% Inc. (3.8)(18.8) 2.7 15.7 (4.0)

¥18.7

22.4

¥22.9

27.2

2010 New Products

• Female Cancer Rider “Corsage”

• New Gentle EVER

10

New Sales of Life Insurance(New Annualized Premium, Yen in Billions)

30

40 Child endowment Others

¥

¥27.5¥25.6 ¥26.2

¥35.0

¥23.3¥23.5

0

10

20

2005 2006 2007 2008 2009 6/09 6/10

% Inc. (6.9) 2.6 33.9 21.7

¥15.4

17.0 51.42.6

Number of Agencies by Type

19,782

15,000

20,000Bank

Independent/Individual

Affiliated

0

5,000

10,000

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 6/10

No. of companies listed on the Tokyo Stock Exchange: 2,334

Worksite Marketing

89%

11

30

40

3331

34

27

32

27

34

26

8/09 12/09 4/10 8/10

Communication Preferences for Insurance Purchases

%

0

10

2017

8

17

10

18

9

16

9

On the Internet Sales at home Sales at agencies/shops

Sales at worksite

Source: Macromill, Inc., 8/09, 12/09, 4/10, 8/10

100

120

140 %

(In Billions)

¥99.8

Historical Transition of Sales Channels(New Annualized Premium Sales)

¥¥122.3

60

80

100

Bank

0

20

40

60

80

1992 2000 2009

¥68.4

0

20

40

60

1992 2000 2009

Dai-ichi

Individual/ independent

Affiliated corporate

CorporateMarketing

Retail MarketingBank Channel

Marketing

Aflac Japan Sales Organization

Director of Marketing and Sales

11 corporatesales offices

Affiliated corporate

agencies in Tokyo, Osaka,

Nagoya district

61 retailsales offices

Independent,individual,

other affiliatedcorporate,Dai-ichi,

Japan Post

11 financial Institution

sales offices

Bank

12

3,000

4,000

5,000

Recruitment of New Agencies

3,4633,195

4,651

3,944

2,413 2,499

4,388

0

1,000

2,000

2005 2006 2007 2008 2009 6/09 6/10% Inc. (7.7) 23.4 17.9 14.4(21.0) 3.55.4

Aflac’s Support for New Agencies - Training

• New Associates Basic Training

• Light Consulting Training

Aflac’s Support for New Agencies -Incentives

• Advanced commissions

• Rookie Challenge Bonus

• e-App incentives

13

1,500

2,000

2,500

Growth of Newly Recruited Producing Agencies*

1,580

2,008

1,715

2,449

1,970

0

500

1,000

2005 2006 2007 2008 2009

*Three months after registered as an agency

% Inc. (19.7) 8.5 17.0 22.04.0

92.3% 80.3%

Public Recognition of Aflac Characters

Question: Do you recognize them as an Aflac character?

Aflac Duck Maneki Neko Duck

TV Commercials

• Female Cancer Rider “Corsage”

• New Gentle EVER

14

TV Commercials

Female Cancer Rider “Corsage”

TV Commercials

New Gentle EVER

80

100

120

140¥

Aflac Japan New Annualized Premium Sales(Yen in Billions)

¥117.4 ¥114.6 ¥114.6¥122.3

¥64 1

¥128.7

0

20

40

60

2005 2006 2007 2008 2009 6/09 6/10% Inc. (8.8) (2.4) - 6.7 2.3 11.4

¥57.6¥64.1

5.1

15

The Operations of an AffiliatedCorporate AgencyYoshinori YunokiPresidentPresident, Aeon Insurance Service Co., Ltd.

Company Overview

Founded in 2008

425 employees

Annual sales of ¥3.9 billion (2009)

Target markets:

Customers visiting our insurance shops

Cardholders of Aeon Card

Employees of the Aeon Group

Other Aeon Group companies

16

Share of Aflac Business in Our Life Insurance Business

61%Aflac61%

Others

400

500

600

700

¥549

¥668

¥478

New Annualized Premium Sales(Yen in Millions)

¥

0

100

200

300

400

2008 2009 2009 2010

¥263

(Jan.-Jun.)(Jan.-Jun.)

Premium Income(Yen in Billions)

5

6

7 ¥6.0 ¥6.2¥

0

1

2

3

4

2008 2009

17

Commissions from Aflac(Yen in Millions)

600

700

800

900

¥857 ¥837

¥

0

100

200

300

400

500

600

2008 2009

Aflac in Our View

Solid brand

Appealing products

Good service

Strong support for sales activities

Sales Approach

Insurance shops

18

Sales Approach

Insurance shops

Worksite sales within the Aeon Group

Sales Approach

Insurance shops

Worksite sales within the Aeon Group

Internet and direct mailing

Typical Insurance Shop

19

The Operations of an Independent Corporate AgencyMikio YoshizawaMikio YoshizawaPresident; Representative Director,Miki Business Corporation

Location of the Miki Business Corporation

Saitama City, Saitama Pref.

20

Company Overview

Founded in July 1982

More than 70,000 policies in force

46 employees (including 37 salespeople)

Premium Income(Yen in Millions)

2,000

2,500

3,000

¥1,890 ¥2,060

¥2,288¥2,446

¥2,586¥

% Inc. 6.9 5.710.1 9.0 11.1

0

500

1,000

1,500

2005 2006 2007 2008 2009

Commissions from Aflac(Yen in Millions)

300

350

400

450

¥320 ¥328¥355

¥382¥407

¥

% Inc. 7.6 6.78.6 2.6 8.3

0

50

100

150

200

250

2005 2006 2007 2008 2009

21

Changes in Consumers’ Needs

Coverage: From first to third sector products

Increasing needs for reviewing

existing coverage

Sales approach: More customers prefer

face-to-face consultation

Only face-to-face sales

Aflac’s Strengths

Strong brand

Excellent products:

» Competitive medical, cancer and other

insurance policies

High-quality customer service:

» Good response to claims payments

New Sales of Cancer Insurance(Yen in Millions)

120

140

160

180

¥88.6

¥126.6

¥168.4¥

% Inc. 51.5 34.6(21.3) 10.3 95.6

0

20

40

60

80

100

2005 2006 2007 2008 2009

¥36.9 ¥40.7

¥88.6

22

New Annualized Premium Sales(Yen in Millions)

300

350

400

450

500

¥321 ¥313¥342

¥371

¥439¥

% Inc. 8.5 18.1(1.1) (3.5) 9.4

0

50

100

150

200

250

2005 2006 2007 2008 2009

Main Markets and Sales Approach

Markets: Prefectural government,

Public offices (city hall, etc.),

Hojinkai (small businesses such as

restaurants and repair garages)

Sales approach: Face-to-face sales

Efforts on Development of Human Resources

Focus on training employees

Fair and transparent personnel policy

Implementing benefits program

Results in high productivity of sales persons

23

Productivity of Producing Salespeople(Yen in Millions)

10

12

14

¥9.39 ¥9.06¥9.85

¥

0

2

4

6

8

2007 2008 2009

Future Strategies

Continue to focus on third sector products

Respond to needs for policy reviewing

Enhance development of human resources

Pursue new sales approaches

24

Aflac Japan Bank Channel SalesHisayuki ShinkaiHisayuki ShinkaiFirst Senior Vice President,Financial InstitutionsAflac Japan

History of Bank Channel Deregulation

December 1998 Investment trusts first offered

April 2001 Long-term fire insurance related to housing loans, etc.

October 2002 Individual annuity, accident insurance with annuity, etc.insurance with annuity, etc.

December 2005 Single premium whole-life, single-premium endowment insurance, etc.

December 2007 All remaining insurance products

Financial Institutions in Japan(June 30, 2010)

Mega banks 4 2,192 548 86,431 21,608

Major banks 7 451 64 26,868 3,838

No. of Institutions Total

Avg. per Institution Total

Avg. per Institution

No. of Branches No. of Employees

Regional banks 105 10,638 101 181,068 1,724

Shinkin banks 272 7,618 28 115,569 425

Other banks* 14 325 23 5,555 397

Total 402 21,224 53 415,491 1,034

*Includes Citibank Japan, Seven Bank, e-Bank, Jibun Bank, Aeon Bankand nine credit associations.

25

Reasons for Banks' Compatibility with Insurance Sales

• Consumers have strong comfort level with banks

• Consumers have strong level of familiarity and

confidence with banksconfidence with banks

• Many regional and Shinkin banks sell door-to-door

Considerations for Insurer Selection

• Company with products that will drive sales

• Brand recognition of insurer

• Easy-to-explain products

• Commission levelCommission level

• Sales support and training

Aflac's Extensive Reach Within the Bank Channel(June 30, 2010)

Mega banks 4 4 100 100 100

Major banks 7 3 43 53 45

Regional banks 105 95 90 93 93

TotalAflac

Agencies

CoverageNo. of Banks

No. ofBanks

No. ofEmployees

No. ofBranches

% % %

Regional banks 105 95 90 93 93

Shinkin banks 272 239 88 89 90

Other banks* 14 13 93 98 94

Total 402 354 88 91 90

*Includes Citibank Japan, Seven Bank, e-Bank, Jibun Bank, Aeon Bankand nine credit associations

% % %

26

The Shinkin Industry

Insurance companies

National Association of Shinkin Banks

Selection

• Sales policy• Recommendation of products

Application for selection

companies

272 Shinkin banksnationwide

7,700 branches

Recommendation of products• Administration system

Contracts

Regulatory Restrictions Related to Bank Sales

• Bank cannot make insurance sales a lending condition and certain limits for coverage amount are imposed.

• Restrictions may be loosened after three-year FSA it i i dFSA monitoring period

Aflac Bank Channel Sales(Annualized Premium Basis, In Millions of Yen)

2,500

3,000

3,500

4,000

¥2,178

¥2,904¥3,094

¥¥3,897

0

500

1,000

1,500

2,000

1Q/08 2Q/08 3Q/08 4Q/08 1Q/09 2Q/09 3Q/09 4Q/09 1Q/10 2Q/10

¥276

¥680

¥1,311

¥959 ¥1,009

¥1,403

27

Aflac Sales Contribution by Type of Bank(Annualized Premium Basis)

60%

70%

80%

90%

100%

Mega banks Regional banks Shinkin banks Other

0%

10%

20%

30%

40%

50%

1Q/08 2Q08 3Q/08 4Q/08 1Q/09 2Q/09 3Q/09 4Q/09 1Q/10 2Q/10

25,000

30,000

35,000

40,000 Cancer EVER Sanjuso WAYS Child Annuity

No. of Policies Sold

Policy Sales by Product

24,35527,229

36,70734,533

36,418

0

5,000

10,000

15,000

20,000

,

1Q/08 2Q/08 3Q/08 4Q/08 1Q/09 2Q/09 3Q/09 4Q/09 1Q/10 2Q/10

5,075

12,635

17,49016,205

21,649

Sales Activity at the Branch Level

Mega banks 30.6% 14.3%

Regional banks 17.4 9.7

Percentage of Branches Selling

Six or MorePolicies

Percentage of Branches Selling Twelve or More

Policies

g

Shinkin banks 28.6 17.0

Avg. for bank branches 23.0% 12.9%

28

Number of Banks Offering Aflac Products

Cancer 227 271 274

EVER 180 215 223

Gentle EVER 24 43 50

WAYS 9 22 29

12/31/08 6/30/103/31/10Products

No. of Banks

WAYS 9 22 29

Sanjuso 6 32 32

Child endowment 133 207

Annuity 89 89 92

Total 535 805 907

Average per bank 1.6 2.3 2.6

Strategy for Bank Sales in Fourth Quarter and 2011

• Focus on increasing sales at existing banks

• Promote adoption of multiple products

• Leverage government initiatives

» Child subsidies» Child subsidies

» Cancer screening and education

• Strategic promotion of WAYS

29

Insurance Sales at Resona BankMasahito KumakuraChief ManagerChief Manager,Consumer Banking Division,Resona Bank, Ltd.

Overview of Resona Holdings

Consists of three banks» Resona Bank» Saitama Resona» Kinki Osaka Bank

Total assets (March 2010)Total assets (March 2010)» ¥41 trillion → 4th largest banking group in Japan

No. of branches (March 2010)» 576 – on a par with other three major banking

groups in Japan » Concentrated in Tokyo and Osaka areas

Strengthening Trust Banking Function

Resona Holdings

SaitamaResona

ResonaResona

TrustKinki

Osaka+

Resona Bank

» Offer trust banking services» Support customers’ life plan

30

Next Generation Sales Outlets• Branch renewal initiatives

Eliminating inefficiencies in the branch

Goal

・ administrative costReduce ・ administrative space by half

・ administrative personnel

Double the space for sales activities

Next Generation Sales Outlets

Quick Navi Consulting Booths

General Reception Counter

Call Center

• 220 operator booths• 2 million inbound and 600,000 outbound calls a year

31

Collaboration Between Channels

Customers

Branch Call Center InternetATM

Customer Relations Management System

Branch Call CenterBanking ATM

Next generationsales outlet

Call centerIzumo City

Convenience for customers

No withdrawal fee during

closed times

Products – Reflecting Customers’ Feedback

Credit Agricole Asset ManagementAsia Fund Series

Dai-ichi Frontier LifeAnshin Series (Individual annuity)

Products – Preparing for Life Events

Risks Aflac Products

• Illness

• Nursing

• New EVER• Cancer Forte

Aflac Products

WAYSNursing

• Post retirement

• Death

(Ippo, Ippo)

32

1,200

1,400

1,600

1,800

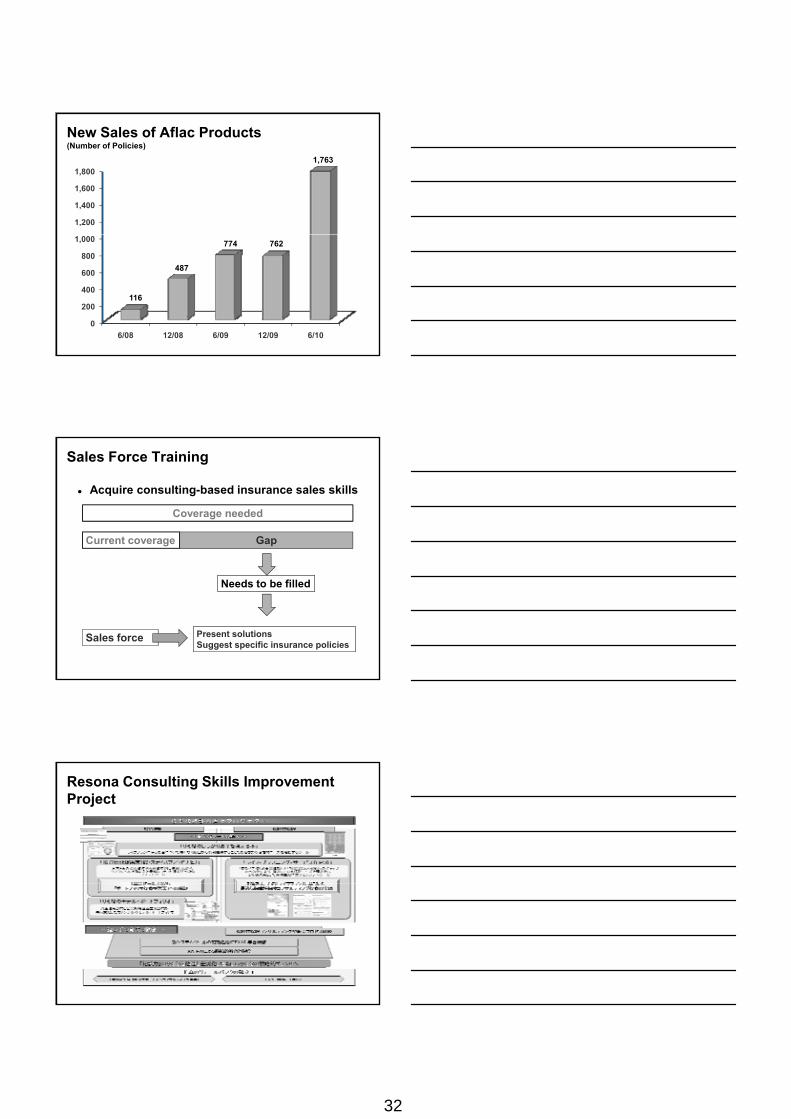

New Sales of Aflac Products(Number of Policies)

1,763

0

200

400

600

800

1,000

6/08 12/08 6/09 12/09 6/10

116

487

774 762

Sales Force Training

Acquire consulting-based insurance sales skills

Coverage needed

Current coverage Gap

Sales force Present solutionsSuggest specific insurance policies

Needs to be filled

Resona Consulting Skills Improvement Project

33

Support Customers’ Life Planning

Large

Potential of Financial Business

• Inheritance• Single premium

whole-life insurance• Saving type of product

Protection type of insurance products

Employment Marriage/Childbirth Home/Education Retirement Inheritance

Life Stage

Mortgage loans

The No.1 Bank for Women

150 frontline female employees voluntarily take part

Discuss products they really want to purchase

Come up with tools or leaflets to convey that message

to customers

The Power of Mine Project

Activities to improve cancer screening rate

Remain committed to CSR activities at Resona Bank

through various initiatives

Establishing our brand

34

35

Japan’s Public Policy and Regulatory EnvironmentCharles D. Lake IIChairman Aflac Japan

The Japanese Government

• Constitutional monarchy with parliamentary government

• Bicameral parliament

» House of Representatives (“Lower House”)

» House of Councillors (“Upper House”)

• Executive power vested in a cabinet composed of a prime minister and ministers of state (all civilians)

• Prime minister must be member of parliament and is chosen by peers

LDP116

members DPJ307

members

House of Representatives (Lower House)

• 480 members elected for four-year terms

• The prime minister can dissolve the Lower House and call for an

People's New Party (4)Japan Communist Party (9)New Komeito (21)

Your Party (5)

LDP (116)

DPJ (307) Social Democratic Party (6)Other (12)

election at any time

• Can override Upper House decisions with a 2/3 majority vote

36

LDP83

members DPJ106

members

House of Councillors (Upper House)

• 242 members elected for six-year terms

• Elections held every three

People's New Party (3)Japan Communist Party (6)New Komeito (19)

Your Party (11)

LDP (83)

DPJ (106) Social Democratic Party (4)Other (10)

yyears, for 1/2 of seats

Control of the Government

• The Lower House is the key to gaining control of Japan’s government.

• A bill passed by the Lower House, but voted down by the Upper House, can be overridden by the Lower House with a two-thirds vote.

• In the case of disagreements over treaties, the budget, and the selection of the prime minister, the Lower House decision becomes the will of the Diet.

• The president of the majority party generally serves as prime minister.

Political Parties and Coalitions

• Japan’s political parties often form partnerships, or coalitions, with other parties.

• The DPJ currently has a coalition with the People’s New Party.

• New Party Nippon

• New Reform Party

• People’s New Party

• Social Democratic Party

• Sunrise Party

• Your Party

• Democratic Party of Japan

• Japan Communist Party

• Liberal Democratic Party

• New Komeito

Japan’s Political Parties Include:

37

Historic Change of Government

• The Democratic Party of Japan (DPJ) wins historic election in September 2009 and establishes first real non-Liberal Democratic Party (LDP) administration in post-war period.

• The DPJ is attempting to consolidate policymaking and governmental control within the Cabinet, which has

t ib t d t di i li kicontributed to disarray in policymaking process.

• Major DPJ defeat in July 2010 election leads to “twisted,”or divided, Diet, where the DPJ controls the Lower House, but not the Upper House.

• Governance, innovation, and reform continue to take place in Japan.

Goals of New Government Growth Strategy (June 2010)

• Increase nominal growth rate to higher than 3% and real growth rate to higher than 2% by fiscal year 2020

• Reduce the unemployment rate to between 3.0% and 4.0%

• Create ¥50 trillion in environment- and energy-related

Source: Office of the Prime Minister

Create ¥50 trillion in environment and energy related markets and 1.4 million new green jobs

• Foster health industry growth to meet demand for medical, nursing care and other health-related services

• Realize a Free Trade Area of Asia-Pacific by 2020

• Increase tourism to 25 million people by start of 2020

Progress in Financial Regulatory Reform

MOF“Convoy system”

Rules based approach1998 - June 2007

Pre-1998

FSA

Rules-based approach

“Better Regulation” policy

(The best mix of principles-based regulation and rules-based regulation)

July 2007-

38

Regulatory Developments Pertaining to Japan’s Financial and Capital Markets

New Growth Strategy commits to establishing Japan as a major financial player in Asia and supporting financial sector’s role in promoting overall economic growth

» Improvements in markets and exchanges

» Reforms to legal infrastructure for financing

» Development of bond market for professional investors

» Expansion of English financial disclosure scope

Postal Reform Developments

12/4/09 IPO freeze legislation

3/24/10 Postal reform outline

4/30/10 Postal legislation submitted to Dietsubmitted to Diet

6/16/10 Diet session ends without postal legislation passing

120

160Welfare Medical Pension

Rapidly Increasing Social Security Benefits(Yen in Trillions)

¥

¥116¥105

¥89 1

¥141

0

40

80

FY 2006 FY 2011 FY 2015 FY 2025

¥89.1

(Actual)Source: Ministry of Health, Labor and Welfare

39

Major Changes in Copayments for the Employed and Elderly

• Japan’s health care system is under great financial strain

» Copayments are now 30% for salaried workers under 70 and high-income seniors

• Advanced Elderly Health system was introduced in 2008 to try to separate fees for advanced elderly from that of the younger population, but the DPJ is currently designing a replacement system

• Details of the new system are unknown, but the reforms should lead to enhanced consumer interest in Aflac’s core products

21.7%

Daily Out-of-Pocket Hospitalization Expenses

¥15,000 to ¥20,000

More than ¥20,000

13.0%

32.0%

14.3%

2004 2007

15.9%

11.8%

25.9%

Less than ¥5,000

¥5,000 to ¥7,000

¥7,000 to ¥10,000

¥10,000 to ¥15,000

11.6%

Source: Japan Institute of Life Insurance, 12/07

10.8%

7.3%

28.0%

7.5%

The Public’s View on the NationalHealth Care System

58 8

63.8

65.5

2001

2004

2007

Adequate Don't know Inadequate

Source: Japan Institute of Life Insurance, 12/07

41.2

55.0

60.1

58.8

0% 20% 40% 60% 80% 100%

1993

1996

1998

2001

40

Aflac Japan AdministrationJun IsonakaSenior Vice President;Senior Vice President;Chief Administrative OfficerAflac Japan

Maintenance Expenses Per Policy in Force(FSA Basis, 03/10)

CostPer Policy

General OperatingExpenses

(In Millions)Rank byAssets

Policiesin Force**

(In Thousands)

1 Nippon ¥260,401 11,775 ¥22,1142 Dai-ichi 201,196 10,970 18,3403 Meiji Yasuda 177,294 8,535 20,772

*Excludes renewal commissions**Excludes individual annuitiesSource: Disclosure statement from each company

j , , ,4 Sumitomo 166,891 8,459 19,7296 Alico 78,431 5,773 13,585 7 Aflac* 104,379 20,100 5,1928 Taiyo 52,100 4,430 11,760

13 Sony 38,214 4,954 7,71316 Tokio Anshin 37,448 2,738 13,677

41

Number of Policies Per Administrative Employee(FSA Basis, 03/10)

Administrative Employees

Rank byAssets

Policies perEmployee

Policiesin Force*

(In Thousands)

1 Nippon 14,242 11,775 826 2 Dai-ichi 13,570 10,970 8083 Meiji Yasuda 9 071 8 535 940

*Excludes individual annuitiesSource: Disclosure statement from each company

3 Meiji Yasuda 9,071 8,535 9404 Sumitomo 9,612 8,459 8806 Alico 4,533 5,773 1,273 7 Aflac 3,791 20,100 5,3028 Taiyo 3,013 4,430 1,470

13 Sony 1,318 4,954 3,75816 Tokio Anshin 1,531 2,738 1,788

Efficiency Improvement Measures by Leveraging IT

• AANET

• Aflac Net Billing

Aflac’s Inbound Call Centers

Aflac Call Center(Inquiries from existing policyholders)(Inquiries from prospective customers)

Associates Support Center(Inquiries from sales agencies)

Alliance Support Center(Inquiries from banks, Japan Post and Dai-ichi Life)

42

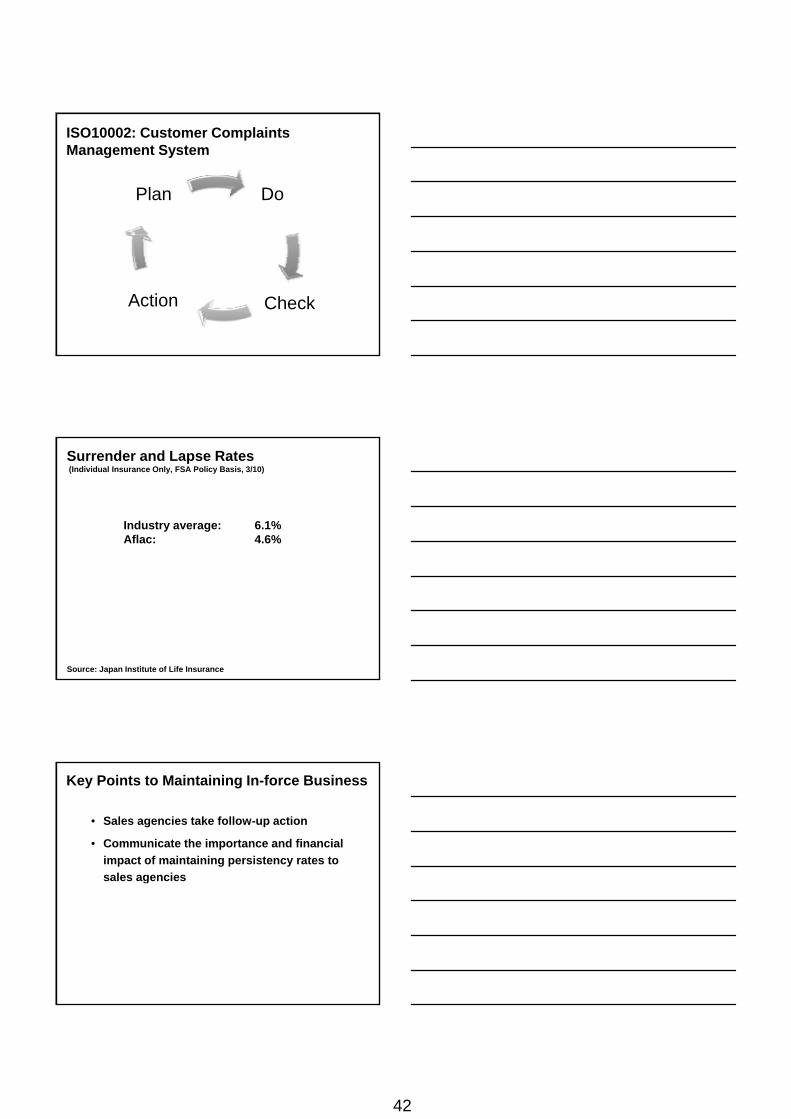

ISO10002: Customer Complaints Management System

DoPlan

CheckAction

Surrender and Lapse Rates (Individual Insurance Only, FSA Policy Basis, 3/10)

Industry average: 6.1%Aflac: 4.6%

Source: Japan Institute of Life Insurance

Key Points to Maintaining In-force Business

• Sales agencies take follow-up action

• Communicate the importance and financial

impact of maintaining persistency rates to

sales agencies

43

Claims Payments(Yen in Billions)

¥

300

400 Cancer Medical/Rider MAX

Source: Internal Aflac data

0

100

200

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Aflac Japan InvestmentsHitoshi OdaVice President,Investment Department,Aflac Japan

44

Aflac Japan Investment Considerations

• Product needs - Japan

» Long liability durations

» Yen-denominated policy liabilities

• Credit risk

• Aflac Incorporated objectives

Aflac Japan’s Investment Portfolio(June 30, 2010, In Millions of Dollars)

Book Value % of Total

Yen-denominated $65,331 94.6%

Dollar-denominated 3,758 5.4

Total Aflac Japan $69,089 100.0%

$Fixed-maturity securities $60,350 87.4%

Perpetual securities 7,225 10.4

Securitized securities 1,492 2.2

Equity securities 22

Total Aflac Japan $69,089 100.0%

Officers 2 3

General managers 1 3

Staff/Managers:

3/2007 8/2010

Organizational Chart for Aflac Japan Investment Division

Investments 9 9

Risk management 4 12

Credit analysis 5 10

Investment accounting 10 12

Total number of employees 31 49

45

Process of Privately Issued Yen Purchases

• Ideas sourced from investment banks

• Rules of engagement

• Credit analysis

• Documentation

• Negotiation

• Pricing

Investment Pricing Methods*

Level I (Active market feeds) 26% 28%

Level II (Model pricing, custodian feeds, broker quotes) 63 71

3/2010 6/2010

Level III (Best efforts) 11 1

Total 100% 100%

*Applies to available-for-sale securities only on a consolidated basis

2010 Investment Activities

46

Challenges

• Low interest rate

• Tight credit spread

• Swap and other costs

• Credit diversificationCredit diversification

• Overall market conditions

New Money Investments(In Billions of Yen)

JGBs ¥105.4 17.6%

Privately issued yen securities 381.6 63.6

Dollar bonds 31.9 5.3

Publicly traded bonds 26.7 4.5

Other 54.1 9.0

Total ¥599.7 100.0%

Amount % of Total2009

JGBs ¥120.7 42.8%

Privately issued yen securities 87.1 30.8

RDCs 40.0 14.2

Dollar bonds 16.6 5.9

Other 17.8 6.3

Total ¥282.2 100.0%

Amount % of Total6/30/10

U.S. Dollar Investments

• Interest rate differential

• Rated ‘A’ or better on average

• 7-10 years remaining to maturity

• Investment of $1 billion in third and fourth quarters of 2010

47

Tender/Exchange Offers and Other Disposals (6/30/10, In Billions of Yen)

Tenders ¥31.5 -30.5 +34.4

Exchanges 53.8 -25.6

AmountDecreasing

HybridsIncreasing

JGBs

Other disposals 42.7 +25.1

Total -56.1 +59.5

JGBs 14.7% 14.8% 15.2% 17.3%Financials 45.3 42.4 38.0 36.3Perpetuals 16.4 14.0 11.2 10.1

2008 2009 6/30/10

Changes in Aflac Japan Portfolio Composition(Percentage of Total Portfolio)

2007

pSecuritized assets 1.9 2.6 2.1 2.2

Comparison of Fixed Income Ratio(FSA Basis)

%

75

80

85

90

95

100 Industry Aflac Japan

Source: Life Insurance Association of Japan

50

55

60

65

70

75

89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09

48

Comparison of Yields(FSA Basis)

%

4

5

6

7

8 Industry Aflac Japan

Source: Life Insurance Association of Japan

0

1

2

3

4

91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09

Comparison of Interest Margin Ratio(FSA Basis)

%

0.0

0.5

1.0 Aflac Japan Nine Domestic Insurers

Source: Press reports and company disclosure statements

-1.5

-1.0

-0.5

2000 2001 2002 2003 2004 2005 2006 2007 2008

Net Investment Income (In Billions of Yen)

¥

150

200

250

¥180.2¥196.4

¥212.1 ¥211.4¥212.0

(.0)9.07.0% Inc. 8.0 0.1 2.7(.3)

0

50

100

2005 2006 2007 2008 2009 6/09 6/10

¥105.3 ¥108.1

49

Aflac Japan Financial Results Yuji Arai Senior Vice President;Senior Vice President;Principal Financial Officer,Aflac Japan

Comparison of Premium Income Growth(FSA Basis, 3/05 = 100)

100

125

150%

50

75

100

3/05 3/06 3/07 3/08 3/09 3/10

Aflac Life Industry

Source: Japan Institute of Life Insurance

50

Premium Income(FSA Basis, 3/10)

1 Nippon ¥4,817 (4.3) %2 Meiji Yasuda 3,281 22.23 Sumitomo 3,059 21.04 Dai-ichi 2,836 (2.3)

RankAmount

(In Billions)Company % Increase

, ( )5 Aflac 1,231 5.96 Alico 863 (21.2)7 Daido 860 6.0 8 Dai-ichi Frontier 805 119.6 9 Taiyo 714 19.6

10 Sony 698 5.7

Source: Disclosure statement from each company

Total Assets(FSA Basis, 3/10)

RankAmount

(In Billions)Company % Increase

1 Nippon ¥48,685 6.2%2 Dai-ichi 30,822 2.73 Meiji Yasuda 25,012 4.64 Sumitomo 23,018 1.85 Mit i 7 499 1 6

Source: Disclosure statement from each company

5 Mitsui 7,499 1.66 Alico 6,716 5.97 Aflac 6,414 8.08 Taiyo 5,842 1.29 Asahi 5,668 .6

10 Fukoku 5,613 1.8

Individual Policies in Force(FSA Basis, 3/10, Policies in Thousands)

1 Aflac 20,302 3.3%2 Nippon 14,714 (1.1)3 Dai-ichi 12,203 (.4)4 Sumitomo 11,076 .85 Meiji Yasuda 10 516 ( 8)

Rank No. of PoliciesCompany % Increase

5 Meiji Yasuda 10,516 (.8)6 Asahi 8,255 (1.2)7 Alico 6,548 1.98 Taiyo 5,656 21.29 Sony 5,010 6.4

10 AXA 4,017 7.7

Source: Disclosure statement from each company

51

Nippon 2.81% 2.67% ¥(60)Dai-ichi 2.89 2.56 (83)Meiji Yasuda 2.48 2.19 (59)Sumitomo 3.11 2.56 (91)

AssumedInterest Rate

Actual Investment Yield

Amount Gain/Loss

Investment Margin(FSA Basis, Yen in Billions)

Company

Source: Disclosure statement from each company* N/D: No disclosure is available

Mitsui 3.14 2.12 (59)Alico 4.44 4.65 N/D*Aflac 3.79 3.84 3Taiyo 2.66 2.42 (13)Asahi 3.85 2.18 (84)Fukoku 2.38 2.07 (15)

Other

Medical

Ordinary

Premiums in Force by Product

100%

80

60Ordinary

Care

Riders

Cancer

1992 1998 6/10

40

20

0

2007

Traditional cancer life - full CSV 68% - 73%

Cancer life - reduced CSV 63% - 68%

21st Century Cancer life - full CSV 55% - 60%

21st Century Cancer life - reduced CSV 50% - 55%

Cancer Forte full CSV 55% 60%

Expected Benefit Ratios by Product

Cancer Forte - full CSV 55% - 60%

Cancer Forte - reduced CSV 48% - 53%

Riders to cancer and medical 40% - 53%

Ordinary life products 60% - 75%

EVER 50% - 55%

52

Persistency Rates*

96

98

100%

94 093 994 094.594.794.794.7

90

92

94

2005 2006 2007 2008 2009 6/09 6/10

*All product lines, excluding annuities

94.093.994.0

Comparison of Persistency Rates(FSA Policy Basis)

95

100Aflac Industry

%

85

90

3/03 3/04 3/05 3/06 3/07 3/08 3/09 3/10

Source: Japan Institute of Life Insurance, Life Insurance Association of Japan

Operating Expense Ratio*(GAAP Basis)

20

25%

15

2005 2006 2007 2008 2009 6/09 6/10

*As percentage of total revenue

53

Solvency Margin, Real Net Asset, Basic Earnings(FSA Basis, 3/10)

Solvency margin 939.3%

Real net assets ¥501 billion

* Real Net Assets/Total Assets** Basic Earnings/Total Assets

Real net asset ratio* 7.8%

Basic earnings ¥158 billion

Basic earnings ratio** 2.46%

Financial Strength Ratings

S&PRating*

Rank byPoliciesin Force

1 Aflac AA- Aa22 Nippon AA- Aa33 Dai-ichi A A14 Sumitomo BBB+ A2

Moody’sRating*Company

4 Sumitomo BBB A25 Meiji Yasuda A- A16 Asahi BB- -7 Alico A+ A18 Taiyo A- A29 Sony A+ Aa3

10 AXA AA- -

* As of 8/31/10

Impact of Solvency Margin Calculation Revision

• Limitations on recognition of policy reserves, hybrid capital, etc.

• Risk factors to reflect greater volatility g y

• Solvency margin ratios to decline significantly

• New rule to take effect 3/31/12

54

Pretax Operating Earnings Growth(Yen in Billions)

2005 ¥1,146.1 × 14.5% = ¥166.4

2006 1,218.8 × 15.8 = 192.1

2007 1 279 0 × 16 8 214 7

TotalRevenues

ProfitMargin

PretaxOperatingEarnings

2007 1,279.0 × 16.8 = 214.7

2008 1,314.7 × 17.7 = 232.8

2009 1,353.7 × 19.3 = 261.7