Embed Size (px)

Citation preview

8/8/2019 (2010 - 2011) Pastel Tax Guide

http://slidepdf.com/reader/full/2010-2011-pastel-tax-guide 1/44

2010/2011

TAX G UI DE

8/8/2019 (2010 - 2011) Pastel Tax Guide

http://slidepdf.com/reader/full/2010-2011-pastel-tax-guide 2/44

PastEl accountants FoRum

The Pastel Accountants Forum is exclusively for accounting professionals who are

registered with a recognised accounting body. Members of the Pastel Accountants

Forum are entitled to a number of benets including:

• Reded priig Pe fwre

• ae previ veri f Pe aig

• Di Pe prd hd wih ree r refer

Pe r ie

• Free fwre pde d pgrde

• Priri eephi ppr

Join the Pastel Accountants Forum today and let us take you beyond accounting. Call

(011) 304 3550 or e-mail [email protected] to nd out more.

PastEl PayRoll

As an Accountant or business owner, we understand the multi-tasking that goes into

the day-to-day running of a business. Pastel Payroll saves you time and money by

doing everything for you.

Most Accountants trust Pastel. The logical step would be to entrust Pastel Payroll with

your tax, payroll and HR requirements.

• a he Bdge speeh hge wi be de fr

• Pwerf reprig fr e saRs x bii

• Free f-fered Repr Wrier

• see Gl Iegri

• Free eephi & e-i ppr we egiive

ad prd pdaes

• no pr e-p

• We kw he 6 jr a, h d’ hve

Pr

sfwre hde i fr

8/8/2019 (2010 - 2011) Pastel Tax Guide

http://slidepdf.com/reader/full/2010-2011-pastel-tax-guide 3/44

1

This booklet is published by FHPKF Publishers (Pty) Ltd for and on behalf of

• Allinformationcontainedhereinisbelievedtobecorrectatthetimeofpublication,17February2010. Thecontentsshouldnotbeusedasabasisforactionwithoutfurtherprofessionaladvice.• Whileeverycarehasbeentakeninthecompilationofthispublicationnoresponsibilityshallbe acceptedforanyinaccuracies,errorsoromissions.• Theinformationispreparedfromthebudgetspeechandthelegislationnallyenactedmaydiffer considerably.• ChangesinratesoftaxannouncedintheBudgetSpeechforthetaxyear2011becomeeffectiveonly oncethelegislationisenactedbyParliament.• Copyrightsubsistsinthiswork.Nopartofthisworkmaybereproducedinanyformorbyanymeans withoutthepublisher’swrittenpermission.

INDEX AdministrativePenalties 14

Bond/InstalmentRepayments 32

Broad-BasedEmployeeEquity 28

BudgetProposals 2

BursariesandScholarships 28CapitalGainsTax 22

CapitalIncentiveAllowances 19

ConnectedPersons 6

Deductions-Donations 18

Deductions-Employees 9

Deductions-Individuals 10

DeemedCapital-DisposalofShares 13

DeemedEmployees 7

Directors-PAYE 13

DividendsTax 3

DonationsTax 36

DoubleTaxationAgreements andWithholdingTaxes 30

EnvironmentalExpenditure 13

EstateDuty 36

ExchangeControlRegulations 38

ExecutorsRemuneration 36

Exemptions-Individuals 9

FarmingIncome 29FringeBenets 16

IndustrialPolicyProjects 35

InterestRates-Changes 33

LearnershipAllowance 31

LimitationofDeductions 25

MarriedinCommunity ofProperty 31

NationalCreditAct 34

Non-Residents 39OfcialInterestRates andPenalties 32

PassiveHoldingCompany 3

Patent/IntellectualProperty 25

Pre-ProductionInterest 28

Pre-TradingExpenditure 28

PrimeOverdraftRates 33

ProvisionalTax 12

PublicBenetOrganisations 18ReinvestmentRelief 25

RelocationofanEmployee 18

ResearchandDevelopment 25

ResidenceBasedTaxation 26

ResidentialBuildingAllowances 18

RestraintofTrade 28

RetentionofDocuments andRecords 40

RetirementLumpSumBenets 11

Ring-FencedAssessedLosses 11

RoyaltiestoNon-Residents 6

SecuritiesTransferTax 35

SkillsDevelopmentLevy 5

SmallBusinessCorporations 8

StampDuty 35

StrategicAllowances 22

TaxImpact-Companies 4

TaxRates-Companies 4

TaxRates-Individuals 5TaxRates-Trusts 6

TaxRebates 5

TaxThresholds 5

TransferDuty 34

TravelAllowances 14

Trusts-Losses 6

TurnoverTax 35

Value-AddedTax 37

ValueExtractionTax 3VentureCapitalInvestments 31

WearandTearAllowances 20

WithdrawalLumpSumBenets 11

chartered accountants

& business advisers

8/8/2019 (2010 - 2011) Pastel Tax Guide

http://slidepdf.com/reader/full/2010-2011-pastel-tax-guide 4/44

2

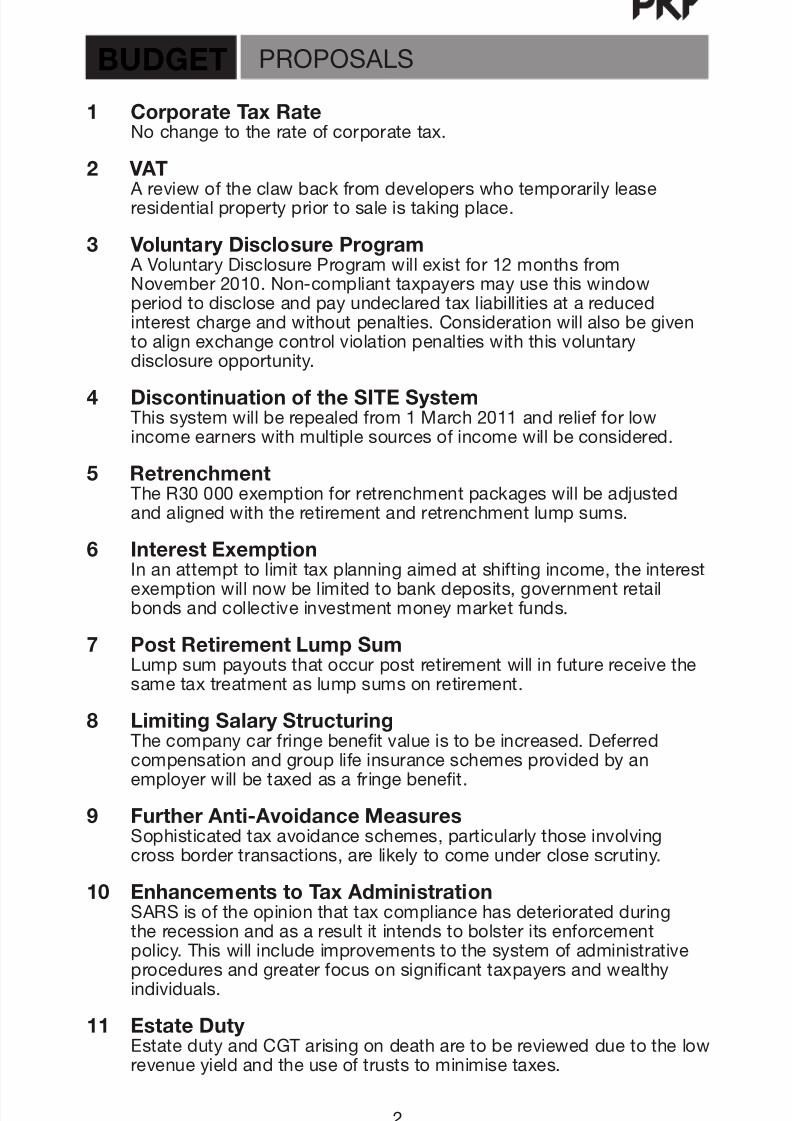

1 Corporate Tax Rate Nochangetotherateofcorporatetax.

2 VAT

Areviewoftheclawbackfromdeveloperswhotemporarilylease residentialpropertypriortosaleistakingplace.

3 Voluntary Disclosure Program AVoluntaryDisclosureProgramwillexistfor12monthsfrom November2010.Non-complianttaxpayersmayusethiswindow periodtodiscloseandpayundeclaredtaxliabillitiesatareduced interestchargeandwithoutpenalties.Considerationwillalsobegiven toalignexchangecontrolviolationpenaltieswiththisvoluntary disclosureopportunity.

4 Discontinuation o the SITE System Thissystemwillberepealedfrom1March2011andreliefforlow incomeearnerswithmultiplesourcesofincomewillbeconsidered.

5 Retrenchment TheR30000exemptionforretrenchmentpackageswillbeadjusted andalignedwiththeretirementandretrenchmentlumpsums.

6 Interest Exemption

Inanattempttolimittaxplanningaimedatshiftingincome,theinterest exemptionwillnowbelimitedtobankdeposits,governmentretail bondsandcollectiveinvestmentmoneymarketfunds.

7 Post Retirement Lump Sum Lumpsumpayoutsthatoccurpostretirementwillinfuturereceivethe sametaxtreatmentaslumpsumsonretirement.

8 Limiting Salary Structuring Thecompanycarfringebenetvalueistobeincreased.Deferred

compensationandgrouplifeinsuranceschemesprovidedbyan employerwillbetaxedasafringebenet.

9 Further Anti-Avoidance Measures Sophisticatedtaxavoidanceschemes,particularlythoseinvolving crossbordertransactions,arelikelytocomeunderclosescrutiny.

10 Enhancements to Tax Administration SARSisoftheopinionthattaxcompliancehasdeterioratedduring therecessionandasaresultitintendstobolsteritsenforcement

policy.Thiswillincludeimprovementstothesystemofadministrative proceduresandgreaterfocusonsignicanttaxpayersandwealthy individuals.

11 Estate Duty EstatedutyandCGTarisingondeatharetobereviewedduetothelow revenueyieldandtheuseoftruststominimisetaxes.

BUDGET PROPOSALS

8/8/2019 (2010 - 2011) Pastel Tax Guide

http://slidepdf.com/reader/full/2010-2011-pastel-tax-guide 5/44

3

DIVIDENDS TAX

Dividendstax,applicabletoSAresidentcompanies,willcomeinto operationatleastthreemonthsafteradateannouncedbytheMinister. DividendsTaxwillbebornebytheshareholderatarateof10%(subject toanyreductionintermsofdoubletaxationagreements).

Exemptions rom Dividends TaxThefollowingshareholdersareexemptfromdividendstax:SAresident companies,theGovernment,PBO’s,certainexemptbodies,rehabilitationtrusts,pension,providentandsimilarfunds,shareholdersinaregisteredmicrobusiness,providedthedividenddoesnotexceedR200000inayear ofassessment,anaturalpersonuponreceiptofaninterestinaprimary residenceandanon-residentreceivingadividendfromanon-resident companywhichislistedontheJSE,i.e.aduallistedcompany.

Withholding Tax Obligations in respect o Dividends TaxDividendstaxinitiallyrequiresthecompanydeclaringthedividendsto

withholddividendstaxonpayment.However,liabilityforwithholdingtaxshiftsifthedividendispaidtoaregulatedintermediarywhichincludescentralsecuritiesdepositoryparticipants,brokers,collectiveinvestmentschemesandlistedinvestmentserviceproviders.Dividendstaxcanbereducedoreliminateduponthetimelyreceiptofawrittendeclarationthat theshareholderisentitledtoanexemptionortotaxtreatyrelief.

Use o Unutilised STC CreditsUnutilisedSTCcreditsmustbeutilisedwithinveyearsofthechangeover tothedividendstaxsystem.STCcreditswillbeexhaustedrst.

Revised Dividend DefnitionThedenitionofadividendhasbeensimpliedandincludesalldistributionstoashareholderotherthan:areductionofcontributedtaxcapital(whichconsistsofuntaintedsharepremiumandsharecapitalofacompany), capitilisationissues,asharebuy-backofaJSElistedcompany,oraredemp-tionofaparticipatoryinterestinaforeigncollectiveinvestmentscheme.Inorderforadistributionofcontributedtaxcapitalnottoberegardedasadividendthedirectorsmust,immediatelypriortothedistribution,recordinwritingthatcontributedtaxcapitalisbeingdistributed.

Introduction o Value Extraction Tax (VET)

Thisisananti-avoidancemeasuresimilartothedeemeddividendprovisionswhichwillbeintroducedwhendividendstaxiseffective.Thisisaseparatetaxleviedonthecompanyandnottheshareholder.Thisarisesonlyin respectofSouthAfricanresidentcompaniesseekingtoextractvalue withoutdeclaringdividendsandiscalculatedat10%ofthevalueextracted.Thisisapplicablewhereacompany:provideslowinterestloansoradvancestoashareholder,releasesorrelievesloanspreviouslymadetoashareholder,settlesaloanowedbyashareholdertoathirdparty,orceasestobeaSouth Africanresident.Theseanti-avoidancerulesapplyalsotoallpersonswhoareconnectedpersonsinrelationtotheshareholder.

Passive Holding CompanyTopreventtheuseofprivateinvestmentcompaniesavoidingthepaymentofdividendstax,passiveholdingcompanies,whichearnmorethan80%oftheirgrossincomeintheformofinterestanddividendsandinwhichmorethan50%oftheparticipationrightsareheldbyveorlessresidentnaturalpersons,willbetaxedat10%ontheirdividendincomeandatarateof40%ontheirothertaxableincome,butwillnotberequiredtosubjectdividendstheydeclaretothedividendstax.

8/8/2019 (2010 - 2011) Pastel Tax Guide

http://slidepdf.com/reader/full/2010-2011-pastel-tax-guide 6/44

4

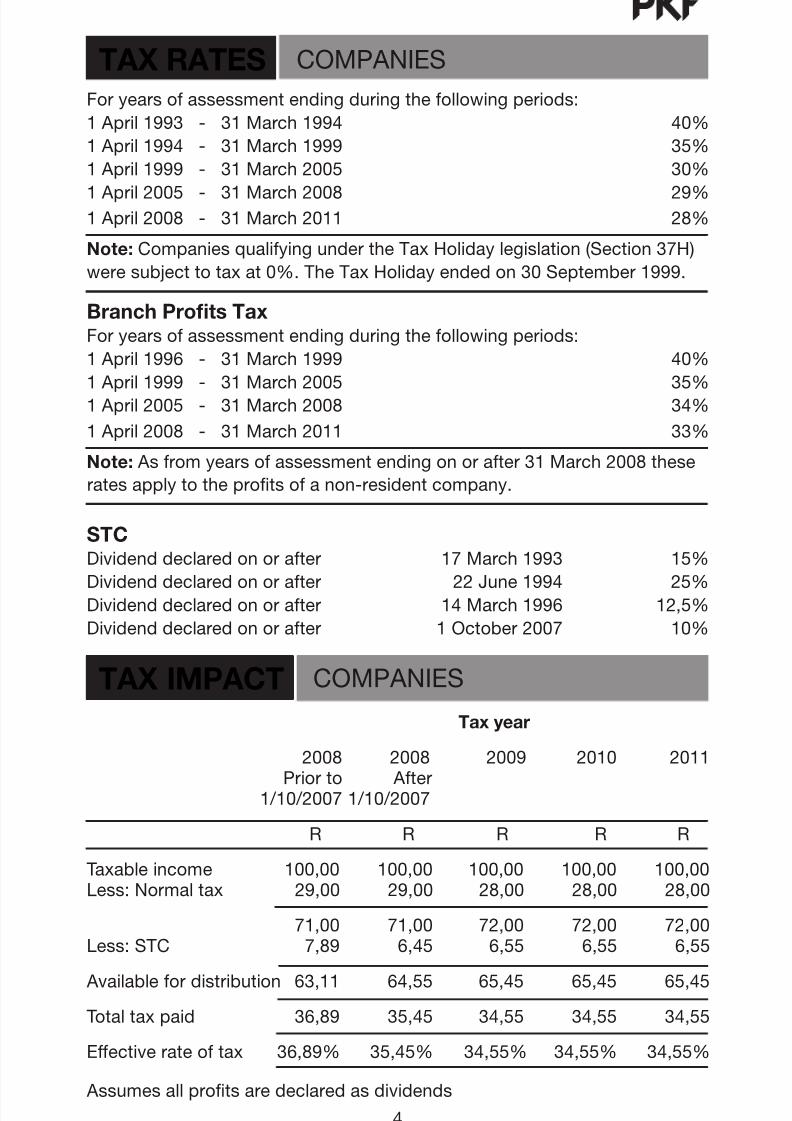

NORMALTAX

Foryearsofassessmentendingduringthefollowingperiods:

1April1993-31March1994 40%

1April1994-31March1999 35%

1April1999-31March2005 30%

1April2005-31March2008 29%1April2008-31March2011 28%

Note:CompaniesqualifyingundertheTaxHolidaylegislation(Section37H)

weresubjecttotaxat0%.TheTaxHolidayendedon30September1999.

Branch Profts TaxForyearsofassessmentendingduringthefollowingperiods:

1April1996-31March1999 40%

1April1999-31March2005 35%1April2005-31March2008 34%

1April2008-31March2011 33%

Note:Asfromyearsofassessmentendingonorafter31March2008these

STCDividenddeclaredonorafter 17March1993 15%

Dividenddeclaredonorafter 22June1994 25%Dividenddeclaredonorafter 14March1996 12,5%

Dividenddeclaredonorafter 1October2007 10%

2008 20082009 2010 2011 PriortoAfter 1/10/20071/10/2007

R RR R R

Taxableincome 100,00 100,00100,00 100,00 100,00Less:Normaltax 29,00 29,0028,00 28,00 28,00

71,00 71,0072,00 72,00 72,00Less:STC 7,89 6,456,55 6,55 6,55

Availablefordistribution 63,11 64,5565,45 65,45 65,45

Totaltaxpaid 36,89 35,4534,55 34,55 34,55

Effectiverateoftax 36,89% 35,45%34,55% 34,55% 34,55%

Assumesallprotsaredeclaredasdividends

TAX RATES COMPANIES

TAX IMPACT COMPANIES

Tax year

ratesapplytotheprotsofanon-residentcompany.

8/8/2019 (2010 - 2011) Pastel Tax Guide

http://slidepdf.com/reader/full/2010-2011-pastel-tax-guide 7/44

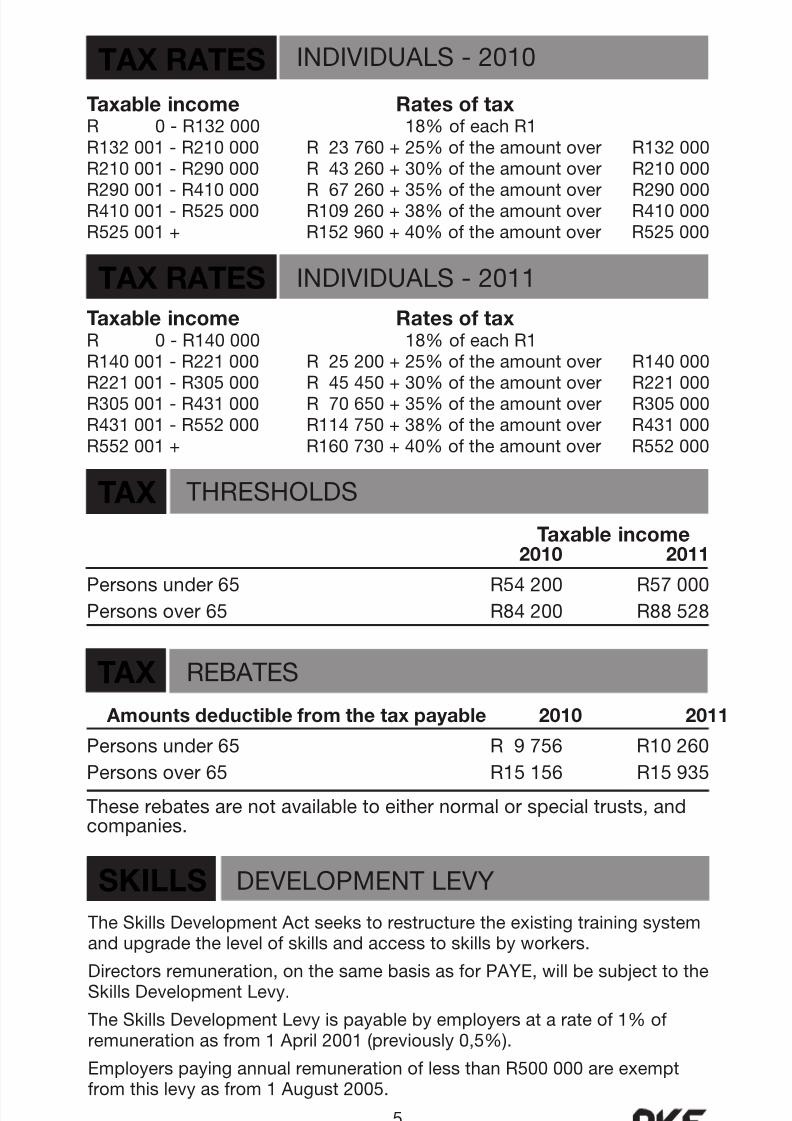

TAX RATES INDIVIDUALS-2010

Taxable income Rates o taxR0-R132000 18%ofeachR1R132001-R210000 R23760+25%oftheamountover R132000R210001-R290000 R43260+30%oftheamountover R210000

R290001-R410000 R67260+35%oftheamountover R290000R410001-R525000 R109260+38%oftheamountover R410000R525001+ R152960+40%oftheamountover R525000

Taxable income Rates o taxR0-R140000 18%ofeachR1R140001-R221000 R25200+25%oftheamountover R140000

R221001-R305000 R45450+30%oftheamountover R221000R305001-R431000 R70650+35%oftheamountover R305000R431001-R552000 R114750+38%oftheamountover R431000R552001+ R160730+40%oftheamountover R552000

TAX RATES INDIVIDUALS-2011

TAX THRESHOLDS

Taxable income2010 2011

Personsunder65 R54200 R57000

Personsover65 R84200 R88528

Amounts deductible rom the tax payable 2010 2011

Personsunder65 R9756 R10260

Personsover65 R15156 R15935

Theserebatesarenotavailabletoeithernormalorspecialtrusts,andcompanies.

TAX REBATES

TheSkillsDevelopmentActseekstorestructuretheexistingtrainingsystemandupgradethelevelofskillsandaccesstoskillsbyworkers.

Directorsremuneration,onthesamebasisasforPAYE,willbesubjecttotheSkillsDevelopmentLevy.

TheSkillsDevelopmentLevyispayablebyemployersatarateof1%ofremunerationasfrom1April2001(previously0,5%).

EmployerspayingannualremunerationoflessthanR500000areexemptfromthislevyasfrom1August2005.

SKILLS DEVELOPMENTLEVY

5

8/8/2019 (2010 - 2011) Pastel Tax Guide

http://slidepdf.com/reader/full/2010-2011-pastel-tax-guide 8/44

6

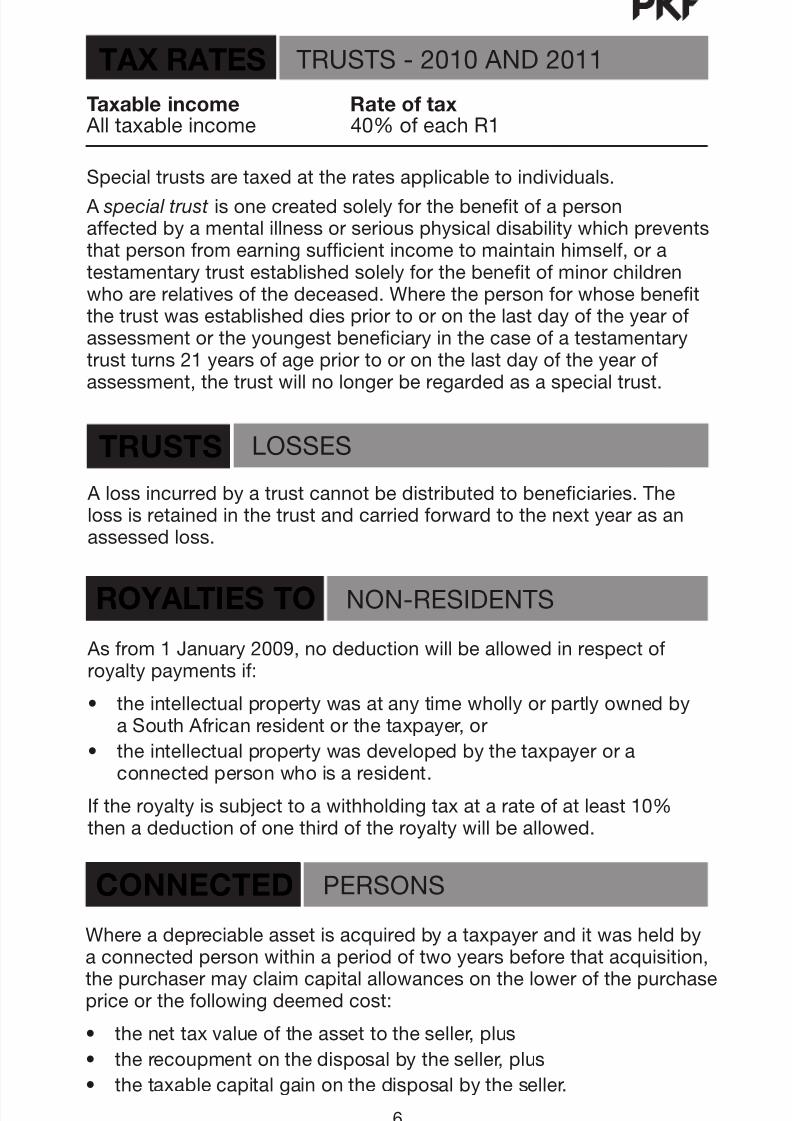

ROYALTIES TO NON-RESIDENTS

Asfrom1January2009,nodeductionwillbeallowedinrespectofroyaltypaymentsif:

• theintellectualpropertywasatanytimewhollyorpartlyownedby aSouthAfricanresidentorthetaxpayer,or

• theintellectualpropertywasdevelopedbythetaxpayerora

connectedpersonwhoisaresident.

Iftheroyaltyissubjecttoawithholdingtaxatarateofatleast10%thenadeductionofonethirdoftheroyaltywillbeallowed.

CONNECTED PERSONS

Whereadepreciableassetisacquiredbyataxpayeranditwasheldby

aconnectedpersonwithinaperiodoftwoyearsbeforethatacquisition,thepurchasermayclaimcapitalallowancesonthelowerofthepurchasepriceorthefollowingdeemedcost:

• thenettaxvalueoftheassettotheseller,plus

• therecoupmentonthedisposalbytheseller,plus

• thetaxablecapitalgainonthedisposalbytheseller.

TAX RATES TRUSTS-2010AND2011

Alossincurredbyatrustcannotbedistributedtobeneciaries.Thelossisretainedinthetrustandcarriedforwardtothenextyearasanassessedloss.

Taxable income Rate o tax Alltaxableincome 40%ofeachR1

Specialtrustsaretaxedattheratesapplicabletoindividuals.

A special trustisonecreatedsolelyforthebenetofaperson affectedbyamentalillnessorseriousphysicaldisabilitywhichpreventsthatpersonfromearningsufcientincometomaintainhimself,oratestamentarytrustestablishedsolelyforthebenetofminorchildrenwhoarerelativesofthedeceased.Wherethepersonforwhosebenetthetrustwasestablisheddiespriortooronthelastdayoftheyearofassessmentortheyoungestbeneciaryinthecaseofatestamentarytrustturns21yearsofagepriortooronthelastdayoftheyearof

assessment,thetrustwillnolongerberegardedasaspecialtrust.

TRUSTS LOSSES

8/8/2019 (2010 - 2011) Pastel Tax Guide

http://slidepdf.com/reader/full/2010-2011-pastel-tax-guide 9/44

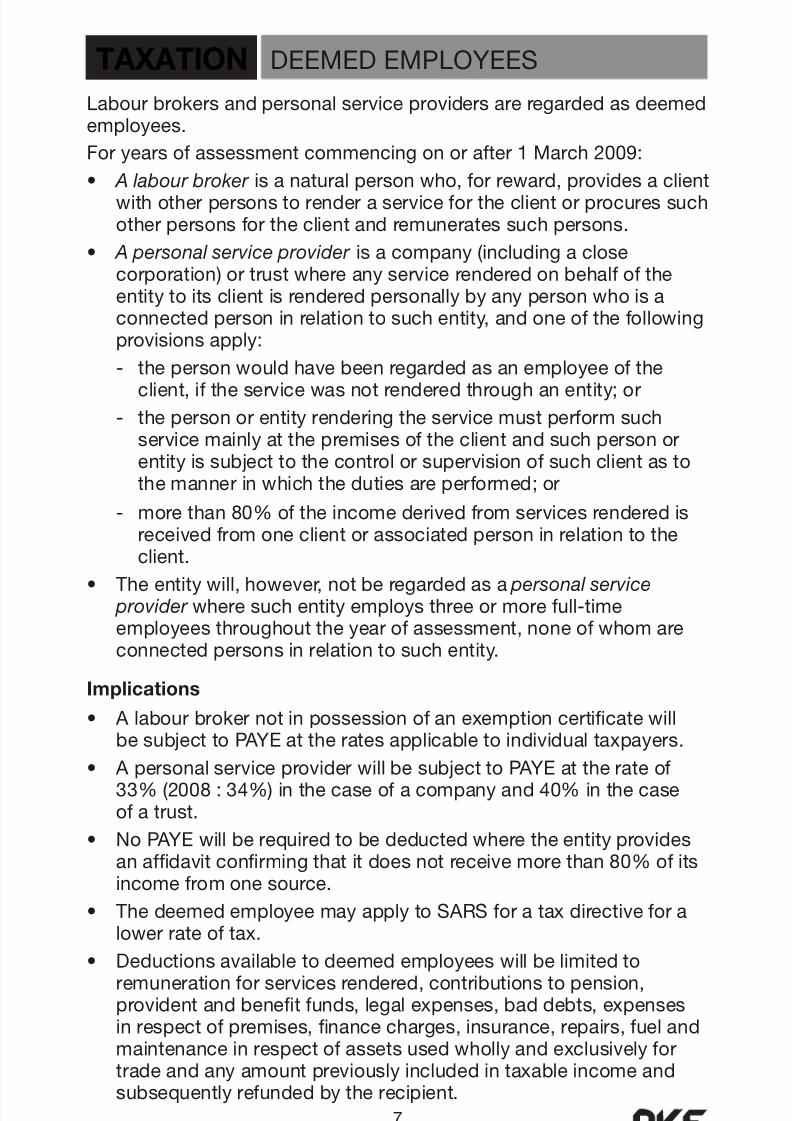

Foryearsofassessmentcommencingonorafter1March2009:

• A labour broker isanaturalpersonwho,forreward,providesaclient withotherpersonstorenderaservicefortheclientorprocuressuch otherpersonsfortheclientandremuneratessuchpersons.

• A personal service provider isacompany(includingaclose corporation)ortrustwhereanyservicerenderedonbehalfofthe entitytoitsclientisrenderedpersonallybyanypersonwhoisa connectedpersoninrelationtosuchentity,andoneofthefollowing provisionsapply:

- thepersonwouldhavebeenregardedasanemployeeofthe

client,iftheservicewasnotrenderedthroughanentity;or

- thepersonorentityrenderingtheservicemustperformsuch servicemainlyatthepremisesoftheclientandsuchpersonor entityissubjecttothecontrolorsupervisionofsuchclientasto themannerinwhichthedutiesareperformed;or

- morethan80%oftheincomederivedfromservicesrenderedis receivedfromoneclientorassociatedpersoninrelationtothe client.

• Theentitywill,however,notberegardedasa personal service provider wheresuchentityemploysthreeormorefull-time

employeesthroughouttheyearofassessment,noneofwhomare connectedpersonsinrelationtosuchentity.

Implications

• Alabourbrokernotinpossessionofanexemptioncerticatewill besubjecttoPAYEattheratesapplicabletoindividualtaxpayers.

• ApersonalserviceproviderwillbesubjecttoPAYEattherateof 33%(2008:34%)inthecaseofacompanyand40%inthecase ofatrust.

• NoPAYEwillberequiredtobedeductedwheretheentityprovides anafdavitconrmingthatitdoesnotreceivemorethan80%ofits incomefromonesource.

• ThedeemedemployeemayapplytoSARSforataxdirectivefora lowerrateoftax.

• Deductionsavailabletodeemedemployeeswillbelimitedto remunerationforservicesrendered,contributionstopension, providentandbenetfunds,legalexpenses,baddebts,expenses inrespectofpremises,nancecharges,insurance,repairs,fueland maintenanceinrespectofassetsusedwhollyandexclusivelyfor tradeandanyamountpreviouslyincludedintaxableincomeand subsequentlyrefundedbytherecipient.

Labourbrokersandpersonalserviceprovidersareregardedasdeemedemployees.

TAXATION DEEMEDEMPLOYEES

7

8/8/2019 (2010 - 2011) Pastel Tax Guide

http://slidepdf.com/reader/full/2010-2011-pastel-tax-guide 10/44

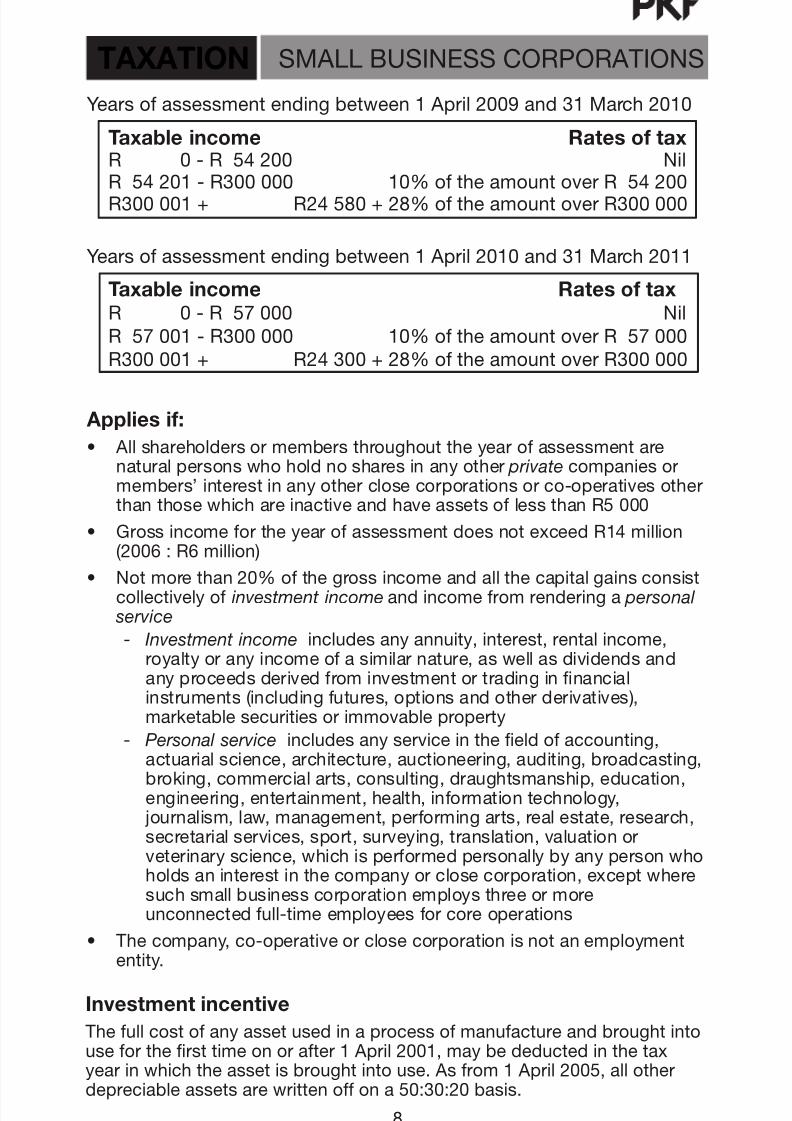

8

Yearsofassessmentendingbetween1April2010and31March2011

Yearsofassessmentendingbetween1April2009and31March2010

Applies i:

• Allshareholdersormembersthroughouttheyearofassessmentare naturalpersonswhoholdnosharesinanyother privatecompaniesor members’interestinanyotherclosecorporationsorco-operativesother thanthosewhichareinactiveandhaveassetsoflessthanR5000

• GrossincomefortheyearofassessmentdoesnotexceedR14million (2006:R6million)

• Notmorethan20%ofthegrossincomeandallthecapitalgainsconsist collectivelyof investment incomeandincomefromrenderinga personal

service

- Investment income includesanyannuity,interest,rentalincome, royaltyoranyincomeofasimilarnature,aswellasdividendsand anyproceedsderivedfrominvestmentortradinginnancial instruments(includingfutures,optionsandotherderivatives), marketablesecuritiesorimmovableproperty

- Personal serviceincludesanyserviceintheeldofaccounting,

actuarialscience,architecture,auctioneering,auditing,broadcasting, broking,commercialarts,consulting,draughtsmanship,education, engineering,entertainment,health,informationtechnology, journalism,law,management,performingarts,realestate,research, secretarialservices,sport,surveying,translation,valuationor veterinaryscience,whichisperformedpersonallybyanypersonwho holdsaninterestinthecompanyorclosecorporation,exceptwhere suchsmallbusinesscorporationemploysthreeormore unconnectedfull-timeemployeesforcoreoperations

• Thecompany,co-operativeorclosecorporationisnotanemployment

entity.

Taxable income Rates o tax R0-R54200 Nil

R54201-R300000 10%oftheamountoverR54200R300001+ R24580+28%oftheamountoverR300000

Taxable income Rates o taxR0-R57000 NilR57001-R300000 10%oftheamountoverR57000R300001+ R24300+28%oftheamountoverR300000

TAXATION SMALLBUSINESSCORPORATIONS

Investment incentive

Thefullcostofanyassetusedinaprocessofmanufactureandbroughtintouseforthersttimeonorafter1April2001,maybedeductedinthetaxyearinwhichtheassetisbroughtintouse.Asfrom1April2005,allotherdepreciableassetsarewrittenoffona50:30:20basis.

8/8/2019 (2010 - 2011) Pastel Tax Guide

http://slidepdf.com/reader/full/2010-2011-pastel-tax-guide 11/44

9

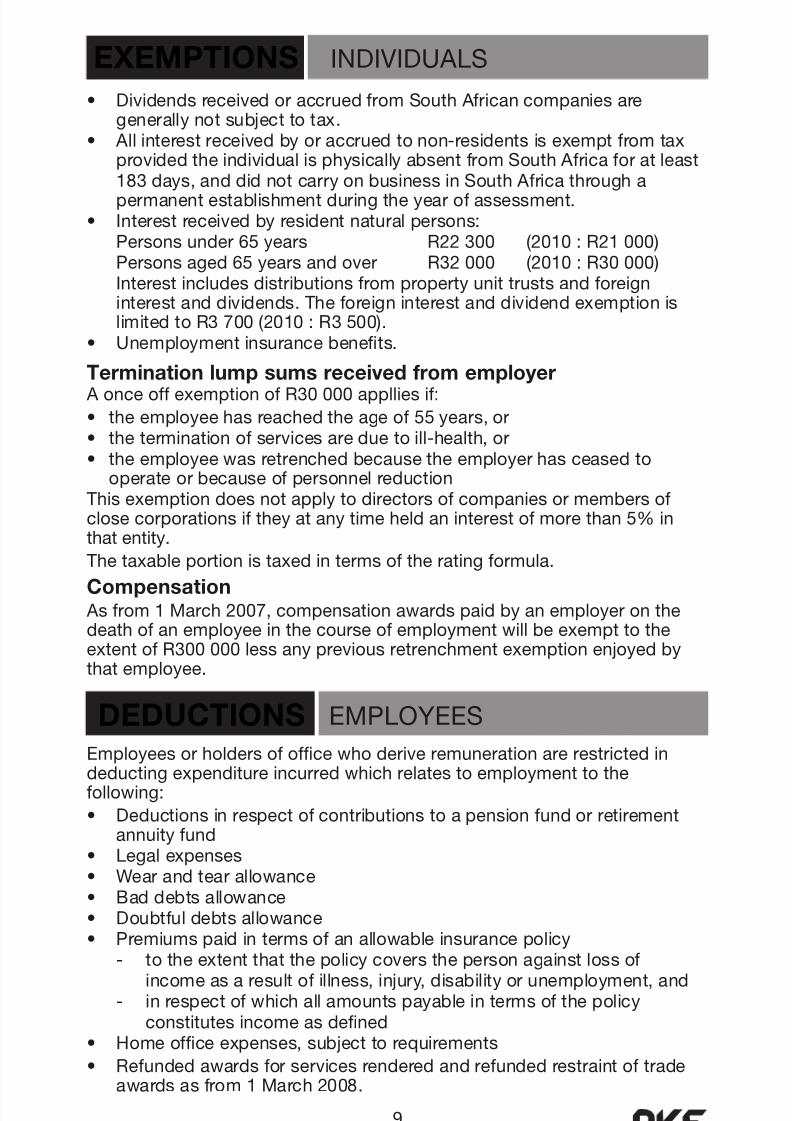

Employeesorholdersofofcewhoderiveremunerationarerestrictedin

deductingexpenditureincurredwhichrelatestoemploymenttothe following:

• Deductionsinrespectofcontributionstoapensionfundorretirementannuity fund

• Legalexpenses• Wearandtearallowance• Baddebtsallowance• Doubtfuldebtsallowance• Premiumspaidintermsofanallowableinsurancepolicy

- totheextentthatthepolicycoversthepersonagainstlossof incomeasaresultofillness,injury,disabilityorunemployment,and - inrespectofwhichallamountspayableintermsofthepolicy constitutesincomeasdened• Homeofceexpenses,subjecttorequirements

• Refundedawardsforservicesrenderedandrefundedrestraintoftrade awardsasfrom1March2008.

• DividendsreceivedoraccruedfromSouthAfricancompaniesare generallynotsubjecttotax.• Allinterestreceivedbyoraccruedtonon-residentsisexemptfromtax providedtheindividualisphysicallyabsentfromSouthAfricaforatleast 183days,anddidnotcarryonbusinessinSouthAfricathrougha permanentestablishmentduringtheyearofassessment.• Interestreceivedbyresidentnaturalpersons: Personsunder65years R22300 (2010:R21000) Personsaged65yearsandover R32000 (2010:R30000) Interestincludesdistributionsfrompropertyunittrustsandforeign interestanddividends.Theforeigninterestanddividendexemptionis limitedtoR3700(2010:R3500).• Unemploymentinsurancebenets.

Termination lump sums received rom employer AonceoffexemptionofR30000applliesif:

• theemployeehasreachedtheageof55years,or• theterminationofservicesareduetoill-health,or• theemployeewasretrenchedbecausetheemployerhasceasedto operateorbecauseofpersonnelreductionThisexemptiondoesnotapplytodirectorsofcompaniesormembersofclosecorporationsiftheyatanytimeheldaninterestofmorethan5%inthatentity.

Thetaxableportionistaxedintermsoftheratingformula.

Compensation Asfrom1March2007,compensationawardspaidbyanemployeronthedeathofanemployeeinthecourseofemploymentwillbeexempttotheextentofR300000lessanypreviousretrenchmentexemptionenjoyedbythatemployee.

DEDUCTIONS EMPLOYEES

EXEMPTIONS INDIVIDUALS

8/8/2019 (2010 - 2011) Pastel Tax Guide

http://slidepdf.com/reader/full/2010-2011-pastel-tax-guide 12/44

10

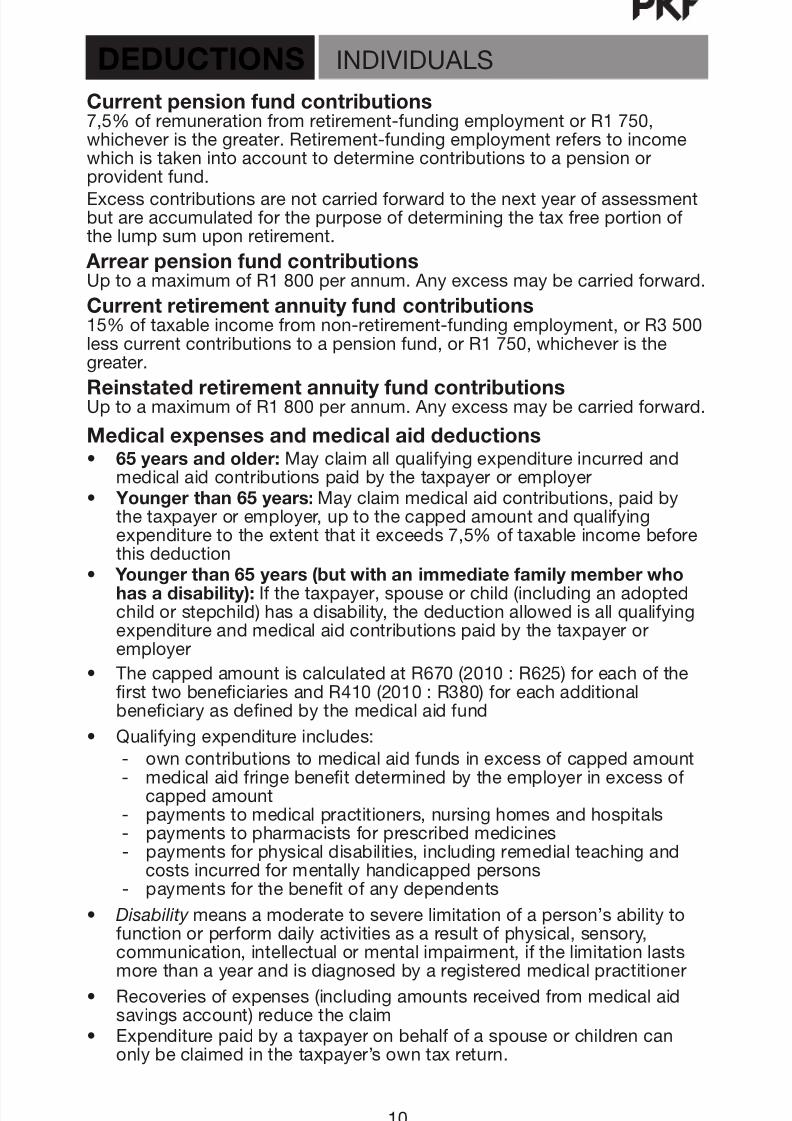

Current pension und contributions7,5%ofremunerationfromretirement-fundingemploymentorR1750,whicheveristhegreater.Retirement-fundingemploymentreferstoincomewhichistakenintoaccounttodeterminecontributionstoapensionor providentfund.

Excesscontributionsarenotcarriedforwardtothenextyearofassessmentbutareaccumulatedforthepurposeofdeterminingthetaxfreeportionofthelumpsumuponretirement.

Arrear pension und contributionsUptoamaximumofR1800perannum.Anyexcessmaybecarriedforward.

Current retirement annuity und contributions15%oftaxableincomefromnon-retirement-fundingemployment,orR3500lesscurrentcontributionstoapensionfund,orR1750,whicheveristhegreater.

Reinstated retirement annuity und contributionsUptoamaximumofR1800perannum.Anyexcessmaybecarriedforward.

Medical expenses and medical aid deductions• 65 years and older:Mayclaimallqualifyingexpenditureincurredand medicalaidcontributionspaidbythetaxpayeroremployer• Younger than 65 years:Mayclaimmedicalaidcontributions,paidby thetaxpayeroremployer,uptothecappedamountandqualifying expendituretotheextentthatitexceeds7,5%oftaxableincomebefore thisdeduction

• Younger than 65 years (but with an immediate amily member whohas a disability):Ifthetaxpayer,spouseorchild(includinganadopted

childorstepchild)hasadisability,thedeductionallowedisallqualifying expenditureandmedicalaidcontributionspaidbythetaxpayeror employer

• ThecappedamountiscalculatedatR670(2010:R625)foreachofthe rsttwobeneciariesandR410(2010:R380)foreachadditional beneciaryasdenedbythemedicalaidfund

• Qualifyingexpenditureincludes:

- owncontributionstomedicalaidfundsinexcessofcappedamount - medicalaidfringebenetdeterminedbytheemployerinexcessof cappedamount - paymentstomedicalpractitioners,nursinghomesandhospitals - paymentstopharmacistsforprescribedmedicines - paymentsforphysicaldisabilities,includingremedialteachingand costsincurredformentallyhandicappedpersons - paymentsforthebenetofanydependents

• Disability meansamoderatetoseverelimitationofaperson’sabilityto functionorperformdailyactivitiesasaresultofphysical,sensory,

communication,intellectualormentalimpairment,ifthelimitationlasts morethanayearandisdiagnosedbyaregisteredmedicalpractitioner

• Recoveriesofexpenses(includingamountsreceivedfrommedicalaid savingsaccount)reducetheclaim• Expenditurepaidbyataxpayeronbehalfofaspouseorchildrencan onlybeclaimedinthetaxpayer’sowntaxreturn.

DEDUCTIONS INDIVIDUALS

8/8/2019 (2010 - 2011) Pastel Tax Guide

http://slidepdf.com/reader/full/2010-2011-pastel-tax-guide 13/44

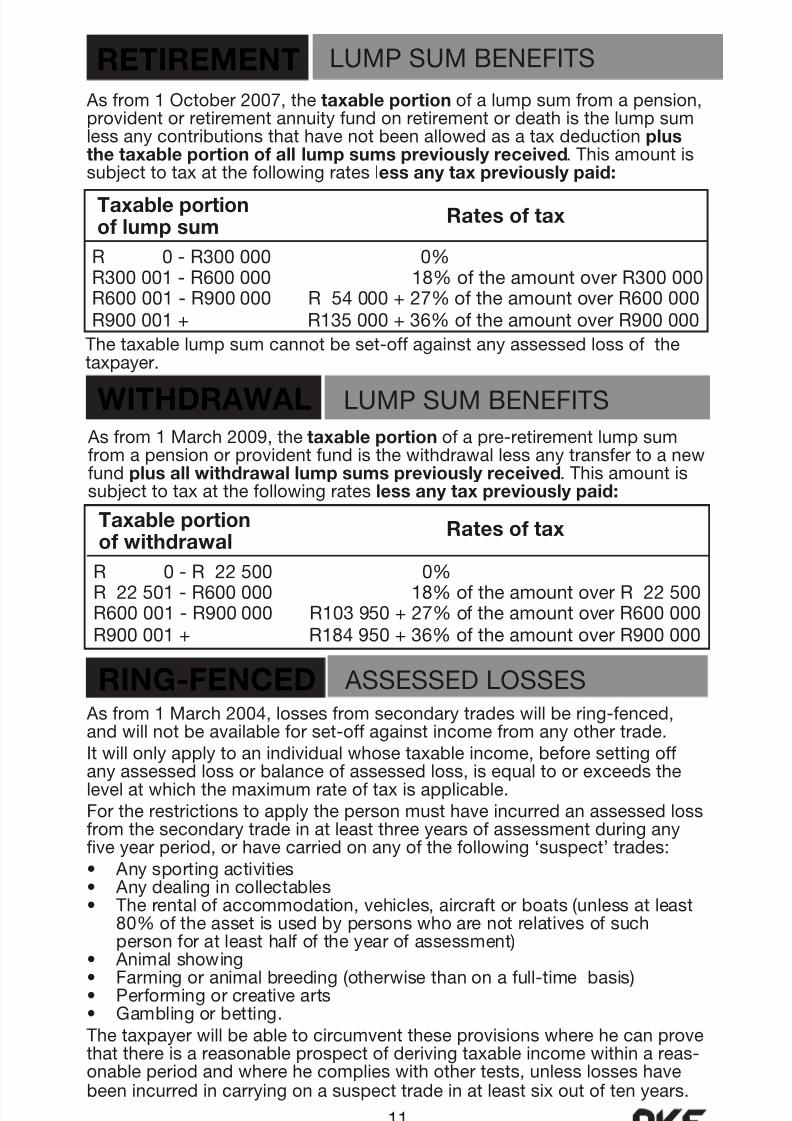

Asfrom1March2004,lossesfromsecondarytradeswillbering-fenced,andwillnotbeavailableforset-offagainstincomefromanyothertrade.Itwillonlyapplytoanindividualwhosetaxableincome,beforesettingoffanyassessedlossorbalanceofassessedloss,isequaltoorexceedsthelevelatwhichthemaximumrateoftaxisapplicable.Fortherestrictionstoapplythepersonmusthaveincurredanassessedlossfromthesecondarytradeinatleastthreeyearsofassessmentduringanyveyearperiod,orhavecarriedonanyofthefollowing‘suspect’trades:• Anysportingactivities• Anydealingincollectables• Therentalofaccommodation,vehicles,aircraftorboats(unlessatleast 80%oftheassetisusedbypersonswhoarenotrelativesofsuch personforatleasthalfoftheyearofassessment)

• Animalshowing• Farmingoranimalbreeding(otherwisethanonafull-timebasis)• Performingorcreativearts• Gamblingorbetting.Thetaxpayerwillbeabletocircumventtheseprovisionswherehecanprovethatthereisareasonableprospectofderivingtaxableincomewithinareas- onableperiodandwherehecomplieswithothertests,unlesslosseshavebeenincurredincarryingonasuspecttradeinatleastsixoutoftenyears.

ASSESSEDLOSSESRING-FENCED

RETIREMENT LUMPSUMBENEFITS

Asfrom1October2007,thetaxable portionofalumpsumfromapension,providentorretirementannuityfundonretirementordeathisthelumpsumlessanycontributionsthathavenotbeenallowedasataxdeductionplusthe taxable portion o all lump sums previously received.Thisamountissubjecttotaxatthefollowingratesless any tax previously paid:

Taxable portion o lump sum

R0-R300000 0%R300001-R600000 18%oftheamountoverR300000R600001-R900000R54000+27%oftheamountoverR600000R900001+ R135000+36%oftheamountoverR900000

11

Thetaxablelumpsumcannotbeset-offagainstanyassessedlossofthetaxpayer.

WITHDRAWAL LUMPSUMBENEFITS

Asfrom1March2009,thetaxable portionofapre-retirementlumpsumfromapensionorprovidentfundisthewithdrawallessanytransfertoanewfund plus all withdrawal lump sums previously received.Thisamountissubjecttotaxatthefollowingratesless any tax previously paid:

Taxable portion o withdrawal

R0-R22500 0%R22501-R600000 18%oftheamountoverR22500R600001-R900000R103950+27%oftheamountoverR600000R900001+ R184950+36%oftheamountoverR900000

Rates o tax

Rates o tax

8/8/2019 (2010 - 2011) Pastel Tax Guide

http://slidepdf.com/reader/full/2010-2011-pastel-tax-guide 14/44

12

PROVISIONAL TAX

Allprovisionaltaxpayersarerequiredtoremittwoprovisionaltaxpaymentsayear.Athirdvoluntarypaymentmayberequiredtoavoidinterestbeingcharged.

First Year o AssessmentWhereataxpayerhasnotbeenassessedpreviously,areasonableestimateofthetaxableincomemustbemade.Thebasicamountcannotbeestimatedatnilaswaspreviouspractice,unlessfullymotivated.

First PaymentOnehalfofthetotaltaxinrespectoftheestimatedtaxableincomeforthe yearispayablesixmonthsbeforethenancialyearend.Theestimateof taxableincomemaynotbelessthanthebasicamountwithouttheconsent ofSARS.

Second Payment Atwo-tiermodelappliesdependingonthetaxpayer’staxableincome: • Actual taxable income equal to or less than R1 million Toavoidanyadditionaltaxontheunderestimationoftaxableincome thiscanbebasedonthebasicamountasdenedorifalowerestimate isusedtheestimatemustbewithin90%ofthetaxableincomenally assessed.• Actual taxable income exceeds R1 million Toavoidanyadditionaltaxontheunderestimationtheestimatemustbe within80%ofthetaxableincomenallyassessed.Iftheaboverequirementsarenotmet,apenaltyof20%oftheprovisionaltaxunderpaidmaybeimposed.

Third Payment

ThirdprovisionalpaymentsareonlyapplicabletoindividualsandtrustswithtaxableincomeinexcessofR50000andcompaniesandclosecorporationswithtaxableincomeinexcessofR20000.Suchpaymentsshouldbemadebefore30SeptemberinthecaseofataxpayerwithaFebruaryyearendandwithinsixmonthsofotheryearendstoavoidinterestbeingcharged.

Basic AmountThebasicamountisthetaxableincomeofthelatestprecedingyearof assessmentincreasedby8%p.a.ifthatassessmentismorethanayearold.

Permissable Reductions in the Basic AmountCapitalgainsandtaxableportionsoflumpsumsarenotincludedin

thebasicamountfortherstperiodorthesecondperiod,wherethetaxableincomeisnotexpectedtoexceedR1million.Ifhoweveranestimatelowerthanthebasicamountisused,suchamountsmustbeincludedinthe estimate.TheseamountshavetobeincludedinthesecondprovisionaltaxpaymentswherethetaxableincomeisexpectedtoexceedR1million.

EstimatesSARShastherighttoincreaseanyprovisionaltaxestimate,evenifbasedonthebasicamount,toanamountconsideredreasonable.

Persons over 65Personsover65years,excludingdirectorsofcompaniesandmembersof

closecorporations,whosetaxableincomedoesnotexceedR120000(2009:R80000)areexemptfromprovisionaltax,providedthatsuchincomeconsistsexclusivelyofremuneration,rental,interestordividends.

Persons under 65Personsunder65yearswhodonotcarryonbusiness,andwhosetaxable incomedoesnotexceedthetaxthresholdorwhoseinterest,foreign dividendsandrentalincomedoesnotexceedR20000(2008:R10000)areexemptfromprovisionaltax.

8/8/2019 (2010 - 2011) Pastel Tax Guide

http://slidepdf.com/reader/full/2010-2011-pastel-tax-guide 15/44

13

DIRECTORS PAYE

Directorsofprivatecompaniesandmembersofclosecorporationsare deemedtohavereceivedamonthlyremuneration,subjecttoPAYE,calculatedinaccordancewiththefollowingformula:

Y=T

NWhere

Y=deemedmonthlyremuneration

T= thebalanceofremunerationpaidoraccruedinthelastyearof assessmentafterthedeductionofcontributionstopensionfunds, retirementannuityfunds,qualifyingmedicalaidcontributionsandincome protectionplansbytheemployee,qualifyingdonationsmadebythe employeronbehalfoftheemployee,lumpsumawardsfromtheemployer andwithdrawalsfromretirementfundsandshareincentivebenets.

N=numberofcompletedmonthswhichthedirector/memberwasemployed bythecompany/closecorporationduringthelastyearofassessment.

Actualremunerationpaidisstillsubjecttoemployeestax.Theemployeestaxpayablethereonmustbereducedbytheamountofemployeestaxpayableonthedeemedremuneration.

Theformulacalculatedremunerationdoesnotapplytodirectorsofprivatecompaniesandmembersofclosecorporationswheretheyearnatleast75% oftheirremunerationintheformofxedmonthlypayments.

ENVIRONMENTAL EXPENDITURE

Expenditureincurredbyataxpayertoconserveormaintainlandisdeduct- ibleifitiscarriedoutintermsofabiodiversitymanagementagreementwithadurationofatleastveyearsandthelandusedbythetaxpayerinhistradeconsistsof,includesorisincloseproximitytothelandwhichissubjecttothisagreement.Wheretheconservationormaintenanceoflandownedbythetaxpayeriscarriedoutintermsofadeclarationofatleast30years’duration,theexpenditureincurredisdeemedtobeadonationtotheGovernment

whichqualiesasadeductionundersection18A.Incertaincircumstanceswherethelandisdeclaredanationalparkornaturereserveanannualdonationbasedon10%ofthelesserofcostormarketvalueofthelandisdeemedtobemadetotheGovernmentandqualiesfor asection18Adeductionintheyearthedeclarationismadeandineachof thesubsequentnineyears.Recoupmentsarisewherethetaxpayerbreachestheagreementorviolatesthedeclaration.

DEEMED CAPITAL DISPOSALOFSHARES Asfrom1October2007,theproceedsonthesaleofanequityshareor collectiveinvestmentschemeunitwillautomaticallybeofacapitalnatureifheldcontinuouslyforatleastthreeyearsexcept:• ashareinashareblockcompany• ashareinanon-residentcompany• ahybridequityinstrument.Previouslythetaxpayercouldelectthattheproceedsonthesaleofalistedshareheldforatleastveyearsbetreatedascapital.

8/8/2019 (2010 - 2011) Pastel Tax Guide

http://slidepdf.com/reader/full/2010-2011-pastel-tax-guide 16/44

14

TRAVEL ALLOWANCES

Reimbursive Travel ExpensesWhereanemployeereceivesareimbursementbasedontheactualbusinesskilometrestravelled,noothercompensationispaidtothe employeeandthecostsarecalculatedinaccordancewiththeprescribedrateof292cents(2008:246cents)perkilometre,noemployeestaxneedbededucted,providedthebusinesstraveldoesnotexceed8000kilometresperannum.Thereimbursementmustbedisclosedundercode3703ontheIRP5certicate.NoPAYEiswith-

heldandtheamountisnotsubjecttotaxationonassessment.Ifthebusinesskilometrestravelledexceed8000kilometresper annum,orifthereimbursiverateperkilometreexceedstheprescribedrate,orifothercompensationispaidtotheemployeetheallowancemustbedisclosedseparatelyundercode3702ontheIRP5certicate.NoPAYEiswithheldandtheamountissubjecttotaxationon assessment.

Fixed Travel Allowances

Asfrom1March2010,80%(2007:60%)ofthexedtravel allowanceissubjecttoPAYEandthefullallowanceisdisclosedon theemployee’sIRP5certicate,irrespectiveofthequantumof businesstravel.

Failuretosubmitcertainreturnsorinformationwillgiverisetothe followingxedratepenalties:

ADMINISTRATIVE PENALTIES

Thepenaltywillautomaticallybeimposedmonthlyuntilthetaxpayerremediesthenon-compliance.

• Late payment o PAYE and provisional tax attracts a penalty o10% o the amount due.

• ThelatesubmissionofthePAYEreconciliationattractsapenalty

o 10% o the PAYE deducted or the tax year.

Assessed loss or taxable income Penalty

or preceding yearAssessedloss R 250

R0–R250000 R 250

R250001–R500000 R 500

R500001–R1000000 R 1000

R1000001–R5000000 R 2000

R5000001–R10000000 R 4000

R10000001–R50000000 R 8000

AboveR50000000 R16000

8/8/2019 (2010 - 2011) Pastel Tax Guide

http://slidepdf.com/reader/full/2010-2011-pastel-tax-guide 17/44

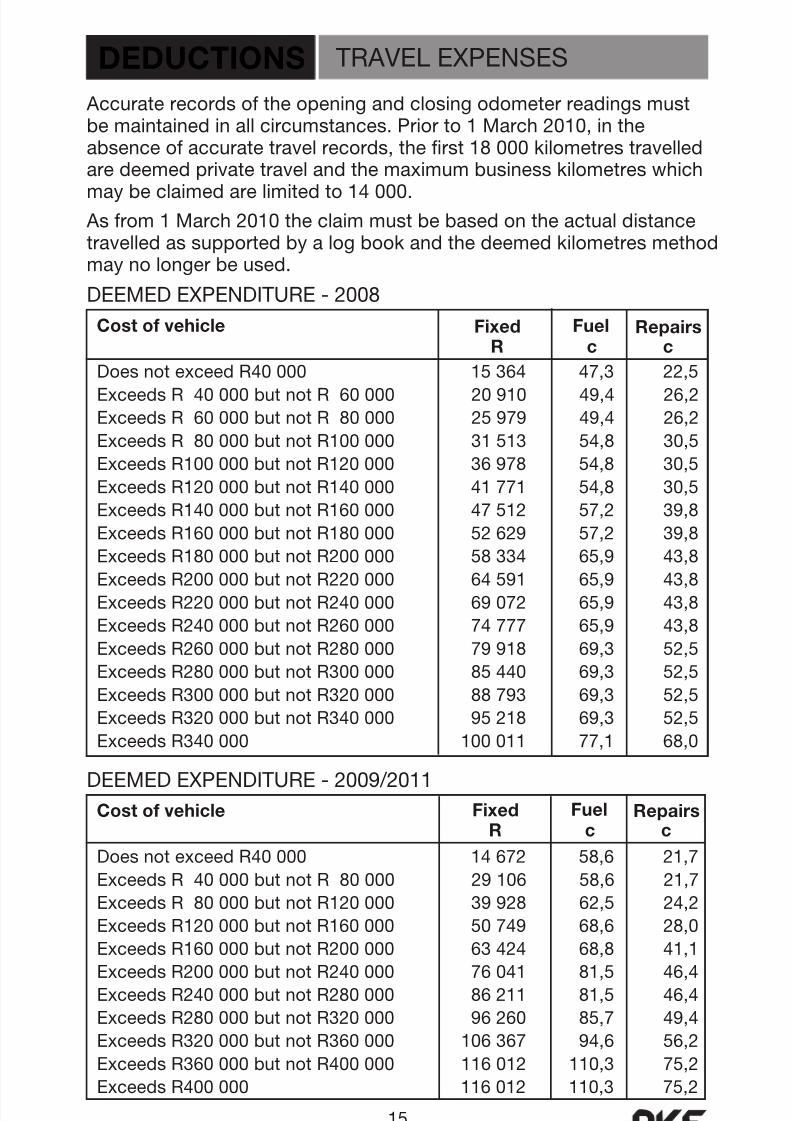

Accuraterecordsoftheopeningandclosingodometerreadingsmust bemaintainedinallcircumstances.Priorto1March2010,inthe absenceofaccuratetravelrecords,therst18000kilometrestravelled aredeemedprivatetravelandthemaximumbusinesskilometreswhich

maybeclaimedarelimitedto14000. Asfrom1March2010theclaimmustbebasedontheactualdistancetravelledassupportedbyalogbookandthedeemedkilometresmethodmaynolongerbeused.

DEDUCTIONS TRAVELEXPENSES

Cost o vehicle

DoesnotexceedR40000 15364 47,3 22,5

ExceedsR40000butnotR60000 20910 49,4 26,2

ExceedsR60000butnotR80000 25979 49,4 26,2

ExceedsR80000butnotR100000 31513 54,8 30,5

ExceedsR100000butnotR120000 36978 54,8 30,5

ExceedsR120000butnotR140000 41771 54,8 30,5

ExceedsR140000butnotR160000 47512 57,2 39,8

ExceedsR160000butnotR180000 52629 57,2 39,8

ExceedsR180000butnotR200000 58334 65,9 43,8

ExceedsR200000butnotR220000 64591 65,9 43,8ExceedsR220000butnotR240000 69072 65,9 43,8

ExceedsR240000butnotR260000 74777 65,9 43,8

ExceedsR260000butnotR280000 79918 69,3 52,5

ExceedsR280000butnotR300000 85440 69,3 52,5

ExceedsR300000butnotR320000 88793 69,3 52,5

ExceedsR320000butnotR340000 95218 69,3 52,5

ExceedsR340000 100011 77,1 68,0

DEEMEDEXPENDITURE-2008

15

DEEMEDEXPENDITURE-2009/2011

Cost o vehicle

DoesnotexceedR40000 14672 58,6 21,7

ExceedsR40000butnotR80000 29106 58,6 21,7

ExceedsR80000butnotR120000 39928 62,5 24,2

ExceedsR120000butnotR160000 50749 68,6 28,0

ExceedsR160000butnotR200000 63424 68,8 41,1

ExceedsR200000butnotR240000 76041 81,5 46,4

ExceedsR240000butnotR280000 86211 81,5 46,4

ExceedsR280000butnotR320000 96260 85,7 49,4

ExceedsR320000butnotR360000 106367 94,6 56,2

ExceedsR360000butnotR400000 116012 110,3 75,2

ExceedsR400000 116012 110,3 75,2

Fixed Fuel RepairsR cc

Fixed Fuel RepairsR cc

8/8/2019 (2010 - 2011) Pastel Tax Guide

http://slidepdf.com/reader/full/2010-2011-pastel-tax-guide 18/44

16

Thecashequivalentoftaxablebenetsgrantedtoemployeesistaxable.

Use o Company Owned VehicleThedeterminedvalueforthefringebenetisthecashcostexcludingVAT, nancechargesandinterest.Theemployeewillbetaxedon2,5%(2006:1,8%)permonthofthedeterminedvalueofthemotorvehiclehavingthehighest

value,and4%permonthofthedeterminedvalueofanysecondorsubsequentvehicleusedprimarilyforprivatepurposes.Iftheemployeebearsthefullcostof:• allfuelusedforprivateuse(includingtravelbetweenplaceofresidence andemployment),themonthlyvalueisreducedby0,22%(2006:R120);• maintainingthevehicle(includingrepairs,servicing,lubricationandtyres), themonthlyvalueisreducedby0,18%(2006:R85).Iftheemployeehastheuseofacompanycarandreceivesatravelallowanceforanothervehicle,thecompanycaristaxedat4%ofthedeterminedvalue andnot2,5%.Ifthecostsfortheothervehiclearereimbursedbasedonactual

distancetravelledonbusinessandtheratedoesnotexceed292cents(2008:246cents)perkilometrethe2,5%(2006:1,8%)willstillapply.Theprivateusebyanemployeeofamotorvehicleshallhavenovalueif:• thevehicleisavailabletoandusedbyallemployeesandtheprivateuseis infrequentandincidentaltoitsbusinessuse,or• wherethenatureoftheemployee’sdutiesrequiresregularuseofthe vehicleforperformanceofdutiesoutsidenormalhoursofworkanditis notusedforprivatepurposesotherthantraveltoandfromwork.Whereitcanbeshownthatthedistancetravelledforprivatepurposes (includingtravellingbetweentheemployee’splaceofresidenceandhisplaceofemployment)islessthan10000km,thefringebenetmaybereduceduponassessmentbytheratioofthisdistanceto10000km.TheprovisionofacompanycarresultsinadeemedconsiderationandthusliableforoutputVATforthevendoremployer.Thedeemedconsideration,inclusiveofVAT,isasfollows:Motorvehicle/Doublecab 0,3%ofcostofvehicle(excl.VAT)permonthBakkies 0,6%ofcostofvehicle(excl.VAT)permonth

Medical Aid Contributions Asfrom1March2010,thefullcontributionbyanemployerisafringebenet.

Theamountbywhichanemployer’scontributiontoamedicalaidfundexceedsR670(2010:R625)foreachofthersttwobeneciariesasdenedbythemedicalaidfundandR410(2010:R380)foreachadditionalbeneciaryissubjecttoPAYE.Iftheemployermakesalumpsumpaymentforallemployees,theeffectivebenetisdeterminedinaccordancewithaformula,whichwillhavetheeffectofapportionmentamongstallemployeesconcerned.

Holiday AccommodationTheemployeeistaxedontheprevailingmarketrateifthepropertyisownedbytheemployerorrentedfromanassociatedentity;ortheactualrentaliftheemployerrentedtheaccommodation.

Long Service and Bravery AwardsTherstR5000ofthevalueofanyassetawarded,excludingcash,isnotsubjecttotax.

Use o Business Cellphones and Computers Asfrom1March2008notaxablevaluewillbeplacedontheprivateuseby employeesofemployerownedcellphonesandcomputerswhichareusedmainlyforbusinesspurposes.

FRINGE BENEFITS

8/8/2019 (2010 - 2011) Pastel Tax Guide

http://slidepdf.com/reader/full/2010-2011-pastel-tax-guide 19/44

17

Low Interest/Interest-Free Loans• Theamounttaxedisthedifferencebetweeninterestpayableontheloan bytheemployeeandtheofcialinterestrate• Short-termloans,notgrantedregularly,whicharenotinexcessofR3000, arenottaxablebenets• Aloantotheemployeetoenablehimtofurtherhisownstudiesisnota taxablebenet.

Subsistence AllowancesIfanemployeeisobligedtospendatleastonenightawayfromhisusual residenceinSouthAfricaonbusiness,theemployermaypayanallowanceforpersonalsubsistenceandincidentalcostswithoutsuchamountsbeing includedintheemployee’staxableincome,subjecttotheemployeetravellingforbusinesswithinthefollowingmonth.Ifsuchallowanceispaidtoanemployeeandthatemployeedoesnottravelforbusinesspurposesbytheendofthefollowingmonth,theallowancebecomessubjecttoPAYEinthatmonth.Iftheallowancesdonotexceedtheamountsorperiodsdetailedbelow,thetotalallowancemustbereectedundercode3705ontheIRP5certicate.

Wheretheallowancesexceedtheamountsorperiodsdetailedbelow,thetotalallowancemustbereectedundercode3704ontheIRP5certicate.Thefollowingamountsaredeemedtohavebeenexpendedbyanemployeeinrespectofasubsistenceallowance:Local travel• R85(2010:R80)perdayorpartofadayforincidentalcosts;or• R276(2010:R260)perdayorpartofadayformealsandincidentalcosts.Whereanallowanceispaidtoanemployeetocoverthecostofaccommo- dation,mealsorotherincidentalcosts,theemployeehastoprovehowmuchhespentwhileawayonbusiness.Thisclaimislimitedtotheallowance received.Overseas travel Actualaccommodationcostsplusanallowancepercountryassetouton www.sars.gov.za(2009:$215)perdayformealsandincidentalcostsincurredoutsideSouthAfrica.Thedeemedexpenditurewillnotapplywherethe absenceisforacontinuousperiodinexcessofsixweeks.

Residential Accommodation Supplied by Employer Asfrom1March1999,whereaccommodationisprovidedtoanemployeeandisnotownedbytheemployerorassociatedentity,thevalueofthefringe benettobetaxedshallbethegreateroftheformulavalueortherentalandotherexpensespaidbytheemployer.Theformulawillneverthelessapplyifitis:• customaryfortheindustrytoprovidefreeorsubsidisedaccommodation toemployees;• necessaryfortheparticularemployertoprovidefreeaccommodationfor properperformanceoftheemployee’sdutiesorasaresultoffrequent movementofemployeesorlackofexistingaccommodation;and• providedforbonadebusinesspurposes,otherthanobtainingatax benet. Asfrom1March2008,norentalvaluewillbeplacedonthe:• supplyofaccommodationtoanemployeeawayfromhisusualplaceof

residenceinSouthAfricafortheperformingofduties• supplyofaccommodationinSouthAfricatoanemployeeawayfromhis usualplaceofresidenceoutsideSouthAfricaforatwoyearperiod.This concessiondoesnotapplyiftheemployeewaspresentinSouthAfricafor morethan90daysinthetaxyearpriortothedateofarrivalforthepurpose ofhisduties.ThereisamonthlymonetarycapofR25000.

8/8/2019 (2010 - 2011) Pastel Tax Guide

http://slidepdf.com/reader/full/2010-2011-pastel-tax-guide 20/44

18

Asset type Conditions or annual allowance Annual allowance

Residential Buildingprojectserectedonorafter1April1982 2%ofcostandan buildings andbefore21October2008consistingofatleastinitialallowanceof veunitsofmorethanoneroomintendedfor 10%ofcost

letting,oroccupationbybonadefull-time employees

Newandunusedbuildingsacquired,erectedor 5%ofcostor10% improvedonorafter21October2008ifsituated ofcostforlowcost anywhereinSouthAfricaandownedbythetax- residentialunitsnot payerforuseinhistradeeitherforlettingoras exceedingR200000 employeeaccommodation.Enhancedallowances forastandaloneunit areavailablewherethelowcostresidentialunit orR250000inthe issituatedinanurbandevelopmentzone caseofanapartment

Employee 50%ofthecostsincurredorfundsadvancedor R6000priorto housing donatedtonancetheerectionofhousingfor 1March2008

employeesonorbefore21October2008 R15000between subjecttoamaximumperdwelling 1March2008and 20October2008

Employee Allowanceonamountsowingoninterestfree 10%ofamount housing loanaccountinrespectoflowcostresidential owingattheend loans unitssoldatcostbythetaxpayertoemployees ofeachyearof andsubjecttorepurchaseatcostonlyincaseof assessment repaymentdefaultorterminationofemployment

Thefollowingitemsofexpenditurebornebytheemployerforrelocation, appointmentorterminationareexemptfromtax:• transportationoftheemployee,membersofhishouseholdandpersonal

possessions• hiringtemporaryresidentialaccommodationfortheemployeeand

membersofhishouseholdforupto183daysaftertransfer• suchcostsasSARSmayallow,e.g.newschooluniforms,replacementof curtains,bondregistrationandlegalfees,transferduty,motorvehicle registrationfees,cancellationofbondandagent’sfeeonsaleofprevious residenceExpenseswhichdonotqualifyarelossonsaleofthepreviousresidenceandarchitect’sfeesfordesignoforalterationstoanewresidence.

RELOCATION OF ANEMPLOYEE

AnorganisationwillqualifyasaPublicBenetOrganisation(PBO)ifitcarriesoutoneormorepublicbenetactivitiesinanon-protmannersubstantiallyinSouthAfrica.ApublicbenetactivityincludestheactivitiesassetoutintheNinthScheduletotheAct,aswellasactivitiesapprovedbytheMinisterofFinanceintheGazette.

DonationstocertaindesignatedPBO’swillqualifyforataxdeductionIndividuals-limitedto10%(2007:5%)oftaxableincomebeforethe

deductionofdonationsandmedicalexpensesCompanies-limitedto10%(2007:5%)oftaxableincomebeforethe deductionofdonations.

PUBLIC BENEFITORGANISATIONS

DEDUCTIONS DONATIONS

RESIDENTIAL BUILDING ALLOWANCES

8/8/2019 (2010 - 2011) Pastel Tax Guide

http://slidepdf.com/reader/full/2010-2011-pastel-tax-guide 21/44

Asset type Conditions or annual allowance Annual allowance

Industrialbuildings Constructionofbuildingsorimprovementson 5%ofcost orimprovements orafter1January1989,providedbuilding (previously2%) isusedwhollyormainlyforcarryingon (note3) processofmanufactureorsimilarprocess

Constructionofbuildingsorimprovementsonor 10%ofcost after1July1996to30September1999andthe (note3) buildingsortheimprovementsarebroughtinto usebefore31March2000andusedinaprocess ofmanufactureorsimilarprocess

Newcommercial Anycostincurredinerectinganynewand 5%ofcost buildings(otherthan unusedbuilding,orimprovinganexistiing residential buildingonorafter1April2007whollyormainly accommodation) usedforthepurposesofproducingincomeinthe (note1) courseoftrade

Buildinginanurban Costsincurredinerectingorextendingabuilding 20%inrstyear

developmentzone inrespectofdemolishing,excavatingtheland,or 8%ineachofthe (note1) toprovidewater,powerorparking,drainageor 10subsequentyears security,wastedisposaloraccesstothebuilding Improvementstoexistingbuildings 20%ofcost

Hotelbuildings Constructionofbuildingsorimprovements, 5%ofcost providedusedintradeashotelkeeperorused

by lessee in trade as hotelkeeper Refurbishments(note2)whichcommenced 20%ofcost onorafter17March1993

Hotelequipment Machinery,implements,utensilsorarticles 20%ofcost broughtintouseonorafter16December1989

Aircraft Acquiredonorafter1April1995 20%ofcost(note3)

Farmingequipment Machinery,implements,utensilsorarticles 50%inrstyear (otherthanlivestock)broughtintouseonor 30%insecondyear after1July1988.Biodieselplantandmachinery 20%inthirdyear broughtintouseafter1April2003

Ships SouthAfricanregisteredshipsusedfor 20%ofcost prospecting,miningorasaforeign-going (note3) ship,acquiredonorafter1April1995

Plantandmachinery Neworunusedmanufacturingassetsacquired 40%in1styear onorafter1March2002willbesubjecttowear 20%ineachofthe

andtearallowancesoverfouryears 3subsequentyears(note 4)

Plantandmachinery Newandunusedplantormachinerybroughtinto 100%ofcost (smallbusiness useonorafter1April2001andusedbythetax- corporationsonly) payerdirectlyinaprocessofmanufacture

Non-manufacturing Acquiredonorafter1April2005 50%inrstyear assets(smallbusiness 30%insecondyear corporationsonly) 20%inthirdyear

Licences Expenditure,otherthanforinfrastructure, Evenlyoverthe toacquirealicencefromagoverment periodofthelicence, bodytocarryontelecommunicationservices, subjecttoa

exploration,productionordistributionof maximumof petroleumortheprovisionofgamblingfacilities 30years

Notes:1 Allowancesavailabletoownersasusersofthebuildingoraslessors/nanciers2 Refurbishmentisdenedasanyworkundertakenwithintheexistingbuildingframework3 Recoupmentsofallowancescanbedeductedfromthecostofthereplacementasset4 Whereplantandmachineryisusedinaprocessofmanufactureorasimilarprocess, thetaxpayerisobligedtomakeuseoftheallowancesandnotthewearandtearrates

CAPITAL INCENTIVE ALLOWANCES

19

8/8/2019 (2010 - 2011) Pastel Tax Guide

http://slidepdf.com/reader/full/2010-2011-pastel-tax-guide 22/44

20

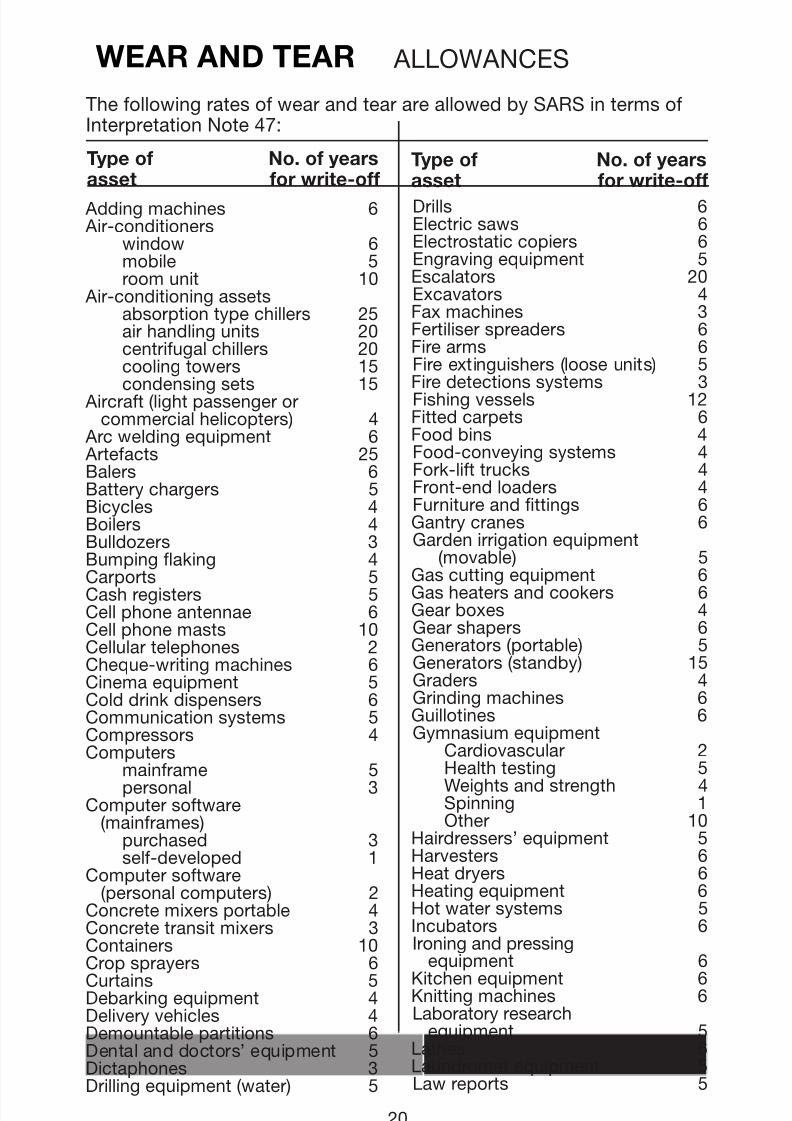

ThefollowingratesofwearandtearareallowedbySARSintermsofInterpretationNote47:

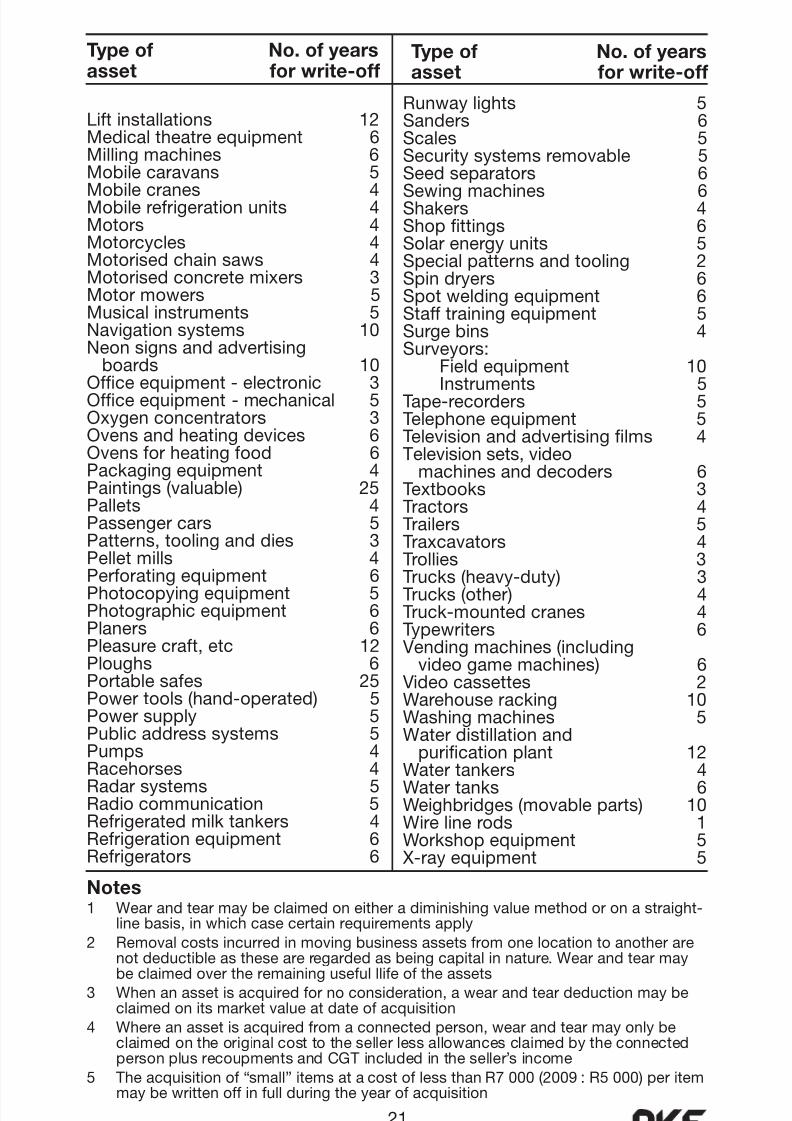

Type o No. o yearsasset or write-o

Type o No. o yearsasset or write-o

Addingmachines 6 Air-conditioners window 6 mobile 5 roomunit 10 Air-conditioningassets absorptiontypechillers 25 airhandlingunits 20 centrifugalchillers 20 coolingtowers 15

condensingsets 15 Aircraft(lightpassengerorcommercialhelicopters) 4 Arcweldingequipment 6 Artefacts 25Balers 6Batterychargers 5Bicycles 4Boilers 4Bulldozers 3Bumpingaking 4

Carports 5Cashregisters 5Cellphoneantennae 6Cellphonemasts 10Cellulartelephones 2Cheque-writingmachines 6Cinemaequipment 5Colddrinkdispensers 6Communicationsystems 5Compressors 4Computers

mainframe 5 personal 3Computersoftware(mainframes) purchased 3 self-developed 1Computersoftware(personalcomputers) 2Concretemixersportable 4Concretetransitmixers 3Containers 10Cropsprayers 6Curtains 5Debarkingequipment 4Deliveryvehicles 4Demountablepartitions 6Dentalanddoctors’equipment 5Dictaphones 3Drillingequipment(water) 5

Drills 6Electricsaws 6Electrostaticcopiers 6Engravingequipment 5Escalators 20Excavators 4Faxmachines 3Fertiliserspreaders 6Firearms 6Fireextinguishers(looseunits) 5

Firedetectionssystems 3Fishingvessels 12Fittedcarpets 6Food bins 4Food-conveyingsystems 4Fork-lifttrucks 4Front-endloaders 4Furnitureandttings 6Gantrycranes 6Gardenirrigationequipment(movable) 5

Gascuttingequipment 6Gasheatersandcookers 6Gearboxes 4Gearshapers 6Generators(portable) 5Generators(standby) 15Graders 4Grindingmachines 6Guillotines 6Gymnasiumequipment Cardiovascular 2

Healthtesting 5 Weightsandstrength 4 Spinning 1 Other 10Hairdressers’equipment 5Harvesters 6Heatdryers 6Heatingequipment 6Hotwatersystems 5Incubators 6Ironingandpressing

equipment 6Kitchenequipment 6Knittingmachines 6Laboratoryresearchequipment 5Lathes 6Laundromatequipment 5Lawreports 5

ALLOWANCESWEAR AND TEAR

8/8/2019 (2010 - 2011) Pastel Tax Guide

http://slidepdf.com/reader/full/2010-2011-pastel-tax-guide 23/44

21

Liftinstallations 12Medicaltheatreequipment 6Millingmachines 6Mobilecaravans 5

Mobilecranes 4Mobilerefrigerationunits 4Motors 4Motorcycles 4Motorisedchainsaws 4Motorisedconcretemixers 3Motormowers 5Musicalinstruments 5Navigationsystems 10Neonsignsandadvertisingboards 10

Ofceequipment-electronic 3Ofceequipment-mechanical 5Oxygenconcentrators 3Ovensandheatingdevices 6Ovensforheatingfood 6Packagingequipment 4Paintings(valuable) 25Pallets 4Passengercars 5Patterns,toolinganddies 3Pelletmills 4

Perforatingequipment 6Photocopyingequipment 5Photographicequipment 6Planers 6Pleasurecraft,etc 12Ploughs 6Portablesafes 25Powertools(hand-operated) 5Powersupply 5Publicaddresssystems 5Pumps 4

Racehorses 4Radarsystems 5Radiocommunication 5Refrigeratedmilktankers 4Refrigerationequipment 6Refrigerators 6

Type o No. o yearsasset or write-o

Type o No. o yearsasset or write-o

Runwaylights5Sanders 6Scales 5Securitysystemsremovable 5Seedseparators 6

Sewingmachines 6Shakers 4Shopttings 6Solarenergyunits 5Specialpatternsandtooling 2Spindryers 6Spotweldingequipment 6Stafftrainingequipment 5Surgebins 4Surveyors: Fieldequipment 10

Instruments 5Tape-recorders 5Telephoneequipment 5Televisionandadvertisinglms 4Televisionsets,videomachinesanddecoders 6Textbooks 3Tractors 4Trailers 5Traxcavators 4Trollies 3

Trucks(heavy-duty) 3Trucks(other) 4Truck-mountedcranes 4Typewriters 6Vendingmachines(includingvideogamemachines) 6Videocassettes 2Warehouseracking 10Washingmachines 5Waterdistillationandpuricationplant 12

Watertankers 4Watertanks 6Weighbridges(movableparts) 10Wirelinerods 1Workshopequipment 5X-rayequipment 5

Notes1 Wearandtearmaybeclaimedoneitheradiminishingvaluemethodoronastraight- linebasis,inwhichcasecertainrequirementsapply2 Removalcostsincurredinmovingbusinessassetsfromonelocationtoanotherare

notdeductibleastheseareregardedasbeingcapitalinnature.Wearandtearmay beclaimedovertheremainingusefulllifeoftheassets3 Whenanassetisacquiredfornoconsideration,awearandteardeductionmaybe claimedonitsmarketvalueatdateofacquisition4 Whereanassetisacquiredfromaconnectedperson,wearandtearmayonlybe claimedontheoriginalcosttothesellerlessallowancesclaimedbytheconnected personplusrecoupmentsandCGTincludedintheseller’sincome5 Theacquisitionof“small”itemsatacostoflessthanR7000(2009:R5000)peritem maybewrittenoffinfullduringtheyearofacquisition

8/8/2019 (2010 - 2011) Pastel Tax Guide

http://slidepdf.com/reader/full/2010-2011-pastel-tax-guide 24/44

22

Asset type Conditions or annual allowance Annual allowance

Strategicprojects Anadditionalindustrialinvestmentallowanceis 100%ofcost (note) allowedonnewandunusedassetsusedforpre- ferredqualifyingstrategicprojectswhichwere approvedbetween31July2001and31July2005

Anyotherqualifyingstrategicprojects 50%ofcost Pipelines Newandunusedstructurescontractedfor 10%ofcost andconstructioncommencedonorafter 23February2000

Electricityand Newandunusedstructurescontractedfor 5%ofcost telephonetrans- andconstructioncommencedonorafter missionlinesand 23February2000 railwaytracks

Airporthangars Constructioncommencedonorafter 5%ofcost andrunways 1April2001

Rollingstock Broughtintouseonorafter1January2008 20%ofcost

Portassets Broughtintouseforthersttimebythetaxpayer 5%ofcost onorafter1January2008

Environmental Asfrom8January2008fornewandunusedassets 40%in1styear assets Environmentaltreatmentandrecyclingassets 20%ineachofthe 3subsequentyears Environmentalwastedisposalassetsofa 5%ofcost permanentnature

Energyefciency Allformsofenergyefciencysavingsasreected Determinedin savings onanenergysavingscerticateinanyyearof accordancewitha assessmentendingbefore1January2020 formula

Note:• Theallowanceislimitedtotheincomederivedfromtheindustrialprojectandtheexcessis deductibleintheimmediatelysucceedingyearofassessment,subjecttocertainotherlimits

CapitalGainsTax(CGT),applicablesince1October2001,appliestoaresident’sworldwideassetsandtoanon-resident’simmovablepropertyorassetsofapermanentestablishmentintheRepublic.

DisposalsCGTistriggeredondisposalofanasset.• Importantdisposalsinclude: - abandonment,scrapping,loss,etc - vestingofaninterestinanassetofatrustinthebeneciary - distributionofanassetbyacompanytoashareholder - granting,renewal,extensionorexcerciseofanoption• Deemeddisposalsinclude: - terminationofSouthAfricanresidency - achangeintheuseofassets - thetransferofanassetbyapermanentestablishment

- thereductionorwaiverofadebtbyacreditorwithoutfull consideration,subjecttocertainexclusions• Disposalsexclude: - thetransferofanassetassecurityforadebtorthereleaseof suchsecurity - issueof,orgrantofanoptiontoacquire,ashare,debentureor

unit trust - loansandthetransferorreleaseofassetsecuringdebt

STRATEGIC ALLOWANCES

CAPITAL GAINSTAX

8/8/2019 (2010 - 2011) Pastel Tax Guide

http://slidepdf.com/reader/full/2010-2011-pastel-tax-guide 25/44

23

Calculation o a Capital Gain/Loss• Acapitalgainorlossisthedifferencebetweentheproceedsandthe basecost

Base Cost• Expenditureincludedinthebasecost: - costofacquisition,transfer,stampdutyandsimilarcosts - remunerationofadvisors,consultantsandagents

- costsofmovinganassetandimprovementcosts• Expenditureexcludedfromthebasecost: - expensesdeductibleforincometaxpurposes - interestpaid,raisingfees(exceptinthecaseoflistedsharesand

business assets) - expensesinitiallyrecordedandsubsequentlyrecovered• Methodsfordeterminingbasecost: - Timeapportionmentbasecost

Example: IfanassetcostR250000on1October1998andwassoldon

30September2002forR450000,asCGTwasimplementedon 1October2001,thebasecostis:

Originalcostexpenditure R250000

Add: R150000*

*Proceedsfromdisposal R450000

Less:Basecostexpenditure (R250000)

Timeapportionmentbasecost R400000

Note 1:Whendeterminingthenumberofyearstobeincludedinthetime

apportionmentcalculation,apartoftheyearistreatedasafullyear. Note 2:Whereexpenditureinrespectofapre-valuationdateassetwasincurred onorafter1October2001andanallowancehasbeenallowedinrespectofthat asset,asecondtimeapportionmentformulaisapplied.

- Valuationasat1October2001 - 20%oftheproceeds

Proceeds• Thetotalamountreceivedoraccruedfromthedisposal

• Excluded: - amountsincludedingrossincomeforincometaxpurposes - amountsrepaidorrepayableorareductioninthesaleprice• Specictransactions: - connectedpersons-deemedtobeatmarketvalue - deceasedpersons-marketvalueasatdateofdeath - deceasedestates-thedisposalisdeemedtobeatthebasecost i.e.marketvalueatdateofdeath

Inclusion Rates And Eective Rates

Inclusion rate Max eective rateIndividualsandspecialtrusts 25% 10%Companies 50% 14%Trusts 50% 20%

UnitTrusts(CIS):theunitholderistaxable

RetirementFunds:nottaxable

} x 34 /

8/8/2019 (2010 - 2011) Pastel Tax Guide

http://slidepdf.com/reader/full/2010-2011-pastel-tax-guide 26/44

24

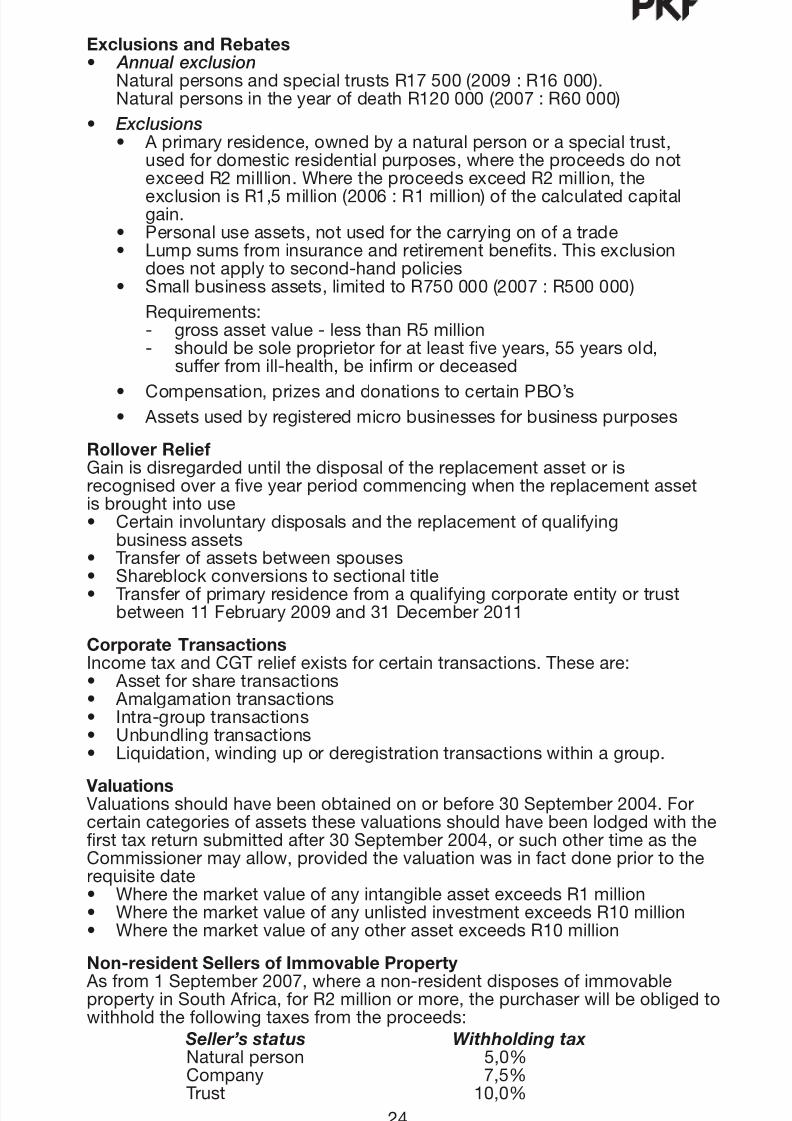

Exclusions and Rebates• Annual exclusion

NaturalpersonsandspecialtrustsR17500(2009:R16000). NaturalpersonsintheyearofdeathR120000(2007:R60000)

• Exclusions

• Aprimaryresidence,ownedbyanaturalpersonoraspecialtrust, usedfordomesticresidentialpurposes,wheretheproceedsdonot exceedR2milllion.WheretheproceedsexceedR2million,the

exclusionisR1,5million(2006:R1million)ofthecalculatedcapital gain. • Personaluseassets,notusedforthecarryingonofatrade • Lumpsumsfrominsuranceandretirementbenets.Thisexclusion doesnotapplytosecond-handpolicies • Smallbusinessassets,limitedtoR750000(2007:R500000)

Requirements: - grossassetvalue-lessthanR5million - shouldbesoleproprietorforatleastveyears,55yearsold, sufferfromill-health,beinrmordeceased

• Compensation,prizesanddonationstocertainPBO’s

• Assetsusedbyregisteredmicrobusinessesforbusinesspurposes

Rollover RelieGainisdisregardeduntilthedisposalofthereplacementassetoris recognisedoveraveyearperiodcommencingwhenthereplacementassetisbroughtintouse• Certaininvoluntarydisposalsandthereplacementofqualifying

business assets• Transferofassetsbetweenspouses

• Shareblockconversionstosectionaltitle• Transferofprimaryresidencefromaqualifyingcorporateentityortrust between11February2009and31December2011

Corporate TransactionsIncometaxandCGTreliefexistsforcertaintransactions.Theseare:• Assetforsharetransactions• Amalgamationtransactions• Intra-grouptransactions• Unbundlingtransactions• Liquidation,windinguporderegistrationtransactionswithinagroup.

ValuationsValuationsshouldhavebeenobtainedonorbefore30September2004.Forcertaincategoriesofassetsthesevaluationsshouldhavebeenlodgedwiththersttaxreturnsubmittedafter30September2004,orsuchothertimeastheCommissionermayallow,providedthevaluationwasinfactdonepriortotherequisitedate• WherethemarketvalueofanyintangibleassetexceedsR1million• WherethemarketvalueofanyunlistedinvestmentexceedsR10million• WherethemarketvalueofanyotherassetexceedsR10million

Non-resident Sellers o Immovable Property Asfrom1September2007,whereanon-residentdisposesofimmovablepropertyinSouthAfrica,forR2millionormore,thepurchaserwillbeobligedtowithholdthefollowingtaxesfromtheproceeds: Seller’sstatus WithholdingtaxNaturalperson 5,0%Company 7,5%Trust 10,0%

8/8/2019 (2010 - 2011) Pastel Tax Guide

http://slidepdf.com/reader/full/2010-2011-pastel-tax-guide 27/44

25

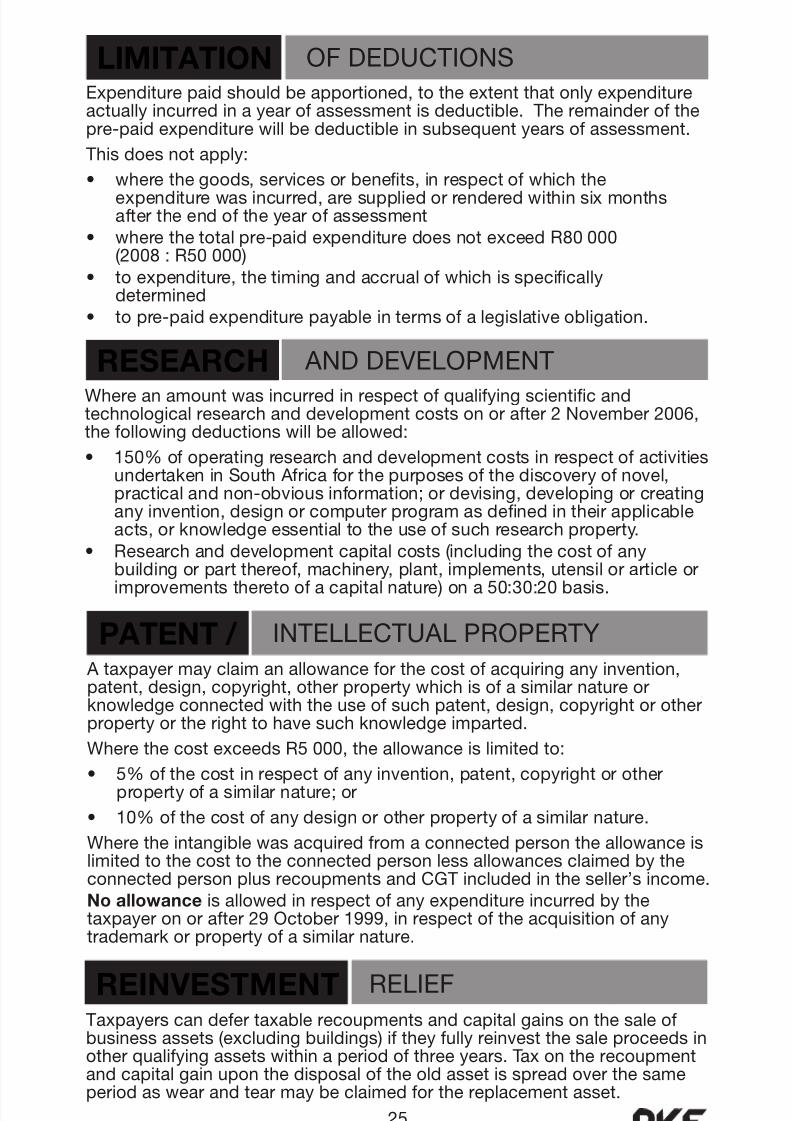

Expenditurepaidshouldbeapportioned,totheextentthatonlyexpenditureactuallyincurredinayearofassessmentisdeductible.Theremainderofthepre-paidexpenditurewillbedeductibleinsubsequentyearsofassessment.

Thisdoesnotapply:

• wherethegoods,servicesorbenets,inrespectofwhichthe expenditurewasincurred,aresuppliedorrenderedwithinsixmonths aftertheendoftheyearofassessment• wherethetotalpre-paidexpendituredoesnotexceedR80000 (2008:R50000)• toexpenditure,thetimingandaccrualofwhichisspecically determined• topre-paidexpenditurepayableintermsofalegislativeobligation.

LIMITATION OFDEDUCTIONS

PATENT / INTELLECTUALPROPERTY

Ataxpayermayclaimanallowanceforthecostofacquiringanyinvention, patent,design,copyright,otherpropertywhichisofasimilarnatureorknowledgeconnectedwiththeuseofsuchpatent,design,copyrightorotherpropertyortherighttohavesuchknowledgeimparted.

WherethecostexceedsR5000,theallowanceislimitedto:

• 5%ofthecostinrespectofanyinvention,patent,copyrightorother propertyofasimilarnature;or

• 10%ofthecostofanydesignorotherpropertyofasimilarnature.

WheretheintangiblewasacquiredfromaconnectedpersontheallowanceislimitedtothecosttotheconnectedpersonlessallowancesclaimedbytheconnectedpersonplusrecoupmentsandCGTincludedintheseller’sincome.No allowance isallowedinrespectofanyexpenditureincurredbythetaxpayeronorafter29October1999,inrespectoftheacquisitionofanytrademarkorpropertyofasimilarnature.

Whereanamountwasincurredinrespectofqualifyingscienticandtechnologicalresearchanddevelopmentcostsonorafter2November2006,thefollowingdeductionswillbeallowed:

• 150%ofoperatingresearchanddevelopmentcostsinrespectofactivities undertakeninSouthAfricaforthepurposesofthediscoveryofnovel, practicalandnon-obviousinformation;ordevising,developingorcreating anyinvention,designorcomputerprogramasdenedintheirapplicable acts,orknowledgeessentialtotheuseofsuchresearchproperty.• Researchanddevelopmentcapitalcosts(includingthecostofany

buildingorpartthereof,machinery,plant,implements,utensilorarticleor improvementstheretoofacapitalnature)ona50:30:20basis.

RESEARCH ANDDEVELOPMENT

Taxpayerscandefertaxablerecoupmentsandcapitalgainsonthesaleofbusinessassets(excludingbuildings)iftheyfullyreinvestthesaleproceedsinotherqualifyingassetswithinaperiodofthreeyears.Taxontherecoupmentandcapitalgainuponthedisposaloftheoldassetisspreadoverthesameperiodaswearandtearmaybeclaimedforthereplacementasset.

REINVESTMENT RELIEF

8/8/2019 (2010 - 2011) Pastel Tax Guide

http://slidepdf.com/reader/full/2010-2011-pastel-tax-guide 28/44

8/8/2019 (2010 - 2011) Pastel Tax Guide

http://slidepdf.com/reader/full/2010-2011-pastel-tax-guide 29/44

27

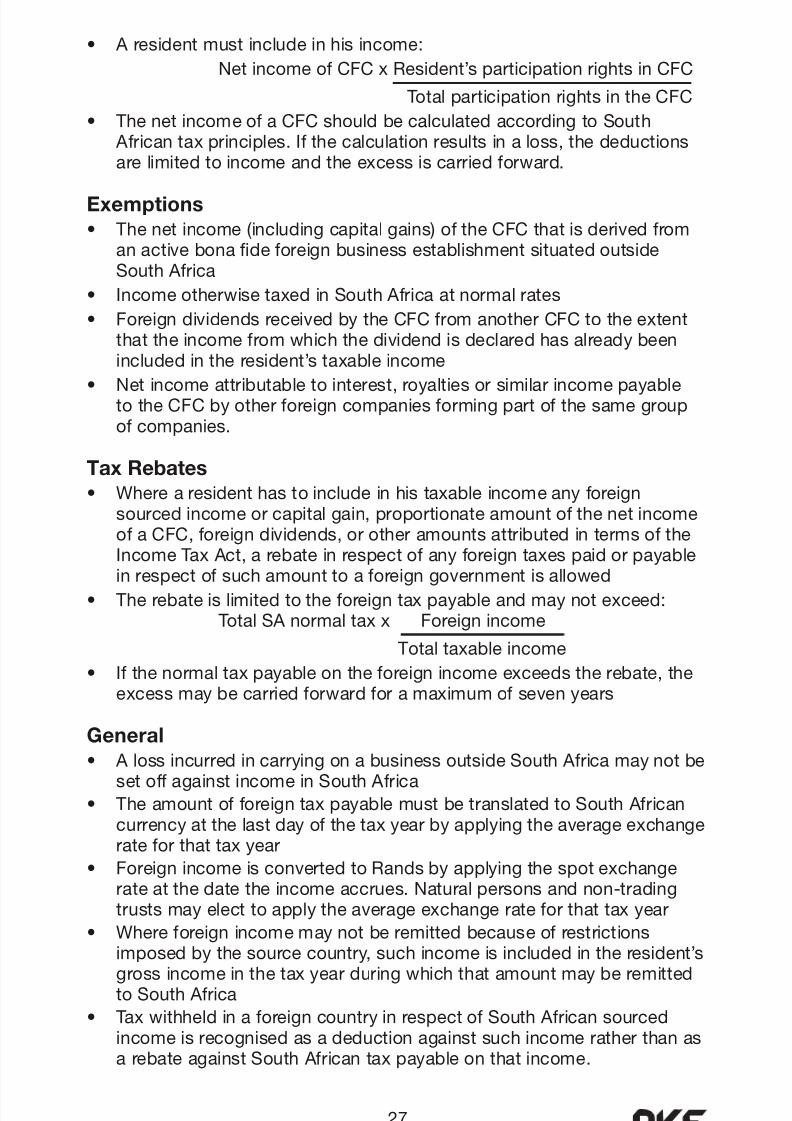

• Aresidentmustincludeinhisincome:

NetincomeofCFCxResident’sparticipationrightsinCFC

TotalparticipationrightsintheCFC

• ThenetincomeofaCFCshouldbecalculatedaccordingtoSouth Africantaxprinciples.Ifthecalculationresultsinaloss,thedeductions arelimitedtoincomeandtheexcessiscarriedforward.

Exemptions

• Thenetincome(includingcapitalgains)oftheCFCthatisderivedfrom anactivebonadeforeignbusinessestablishmentsituatedoutside SouthAfrica

• IncomeotherwisetaxedinSouthAfricaatnormalrates

• ForeigndividendsreceivedbytheCFCfromanotherCFCtotheextent thattheincomefromwhichthedividendisdeclaredhasalreadybeen includedintheresident’staxableincome

• Netincomeattributabletointerest,royaltiesorsimilarincomepayable totheCFCbyotherforeigncompaniesformingpartofthesamegroup ofcompanies.

Tax Rebates

• Wherearesidenthastoincludeinhistaxableincomeanyforeign sourcedincomeorcapitalgain,proportionateamountofthenetincome ofaCFC,foreigndividends,orotheramountsattributedintermsofthe IncomeTaxAct,arebateinrespectofanyforeigntaxespaidorpayable

inrespectofsuchamounttoaforeigngovernmentisallowed• Therebateislimitedtotheforeigntaxpayableandmaynotexceed: TotalSAnormaltaxxForeignincome

Totaltaxableincome

• Ifthenormaltaxpayableontheforeignincomeexceedstherebate,the excessmaybecarriedforwardforamaximumofsevenyears

General

• AlossincurredincarryingonabusinessoutsideSouthAfricamaynotbe setoffagainstincomeinSouthAfrica

• TheamountofforeigntaxpayablemustbetranslatedtoSouthAfrican currencyatthelastdayofthetaxyearbyapplyingtheaverageexchange rateforthattaxyear

• ForeignincomeisconvertedtoRandsbyapplyingthespotexchange rateatthedatetheincomeaccrues.Naturalpersonsandnon-trading trustsmayelecttoapplytheaverageexchangerateforthattaxyear

• Whereforeignincomemaynotberemittedbecauseofrestrictions

imposedbythesourcecountry,suchincomeisincludedintheresident’s grossincomeinthetaxyearduringwhichthatamountmayberemitted toSouthAfrica

• TaxwithheldinaforeigncountryinrespectofSouthAfricansourced incomeisrecognisedasadeductionagainstsuchincomeratherthanas arebateagainstSouthAfricantaxpayableonthatincome.

8/8/2019 (2010 - 2011) Pastel Tax Guide

http://slidepdf.com/reader/full/2010-2011-pastel-tax-guide 30/44

28

Thedeductionofexpenditureandlossesincurredinconnectionwith,butpriortothecommencementoftradeisallowed,providedtheexpenditureandlossesincludingsection24Jinterestcouldhavebeendeductiblehadthetradecommenced.However,suchexpenditureandlossesarering-fenced,inthattheycanonlybesetoffagainstincomefromthattrade.Thebalanceis

carriedforwardandcanbeclaimedinthenextyearofassessment.

EmployercompaniesmayissuequalifyingsharesuptoalimitofR50000(2008:R9000)peremployeeinthecurrenttaxyearandintheimmediatelyprecedingfour(2008:two)taxyears.AtaxdeductionlimitedtoamaximumofR10000(2008:R3000)perannumperemployeewillbeallowedintheemployer’shands.Providedtheemployeeholdsontothesharesforatleast

veyearstherewillbenotaxconsequencesfortheemployee,otherthanCGT.

PRE–TRADING EXPENDITURE

BROAD BASED EMPLOYEEEQUITY

RESTRAINT OFTRADE

Gross Income Anyamountreceivedbyoraccruedtoanynaturalperson,labourbrokerorpersonalserviceproviderforarestraintoftradeimposedonsuchperson, shouldbeincludedintherecipient’sgrossincomeintheyearofreceiptor accrual.

DeductionWhereanamountwasincurredinrespectofarestraintoftradeimposedonanyperson,thededuction,inayearofassessment,islimitedtothelesserof:• theamountapportionedovertheperiodforwhichtherestraintapplies;or• one-thirdoftheamountincurredperannumNodeductionisallowedwheretheamountdidnotconstituteincomeinthehandsoftherecipient.

Interestandrelatednancechargesincurredonanyborrowingforthe acquisition,installation,erectionorconstructionofanymachinery,plant,buildingorimprovementstoabuildingorotherassets,includingland,aredeductiblewhentheassetisbroughtintouseintheproductionofincome.

PRE–PRODUCTION INTEREST

BURSARIES ANDSCHOLARSHIPS

Bona fdescholarshipsorbursariesgrantedtoenableanypersontostudyatarecognisededucationalinstitutionareexemptfromfringebenettax.Wherethebenetisgrantedtoanemployee,theexemptionwillnotapplyunlesstheemployeeagreestoreimbursetheemployerintheeventthatthestudiesarenotcompleted.Wherethebeneciaryisarelativeoftheemployee,theexemptionwillonlyapplyiftheannualremunerationoftheemployeeislessthanR100000(2007:R60000)andtotheextentthatthe

bursarydoesnotexceedR10000(2007:R3000).

8/8/2019 (2010 - 2011) Pastel Tax Guide

http://slidepdf.com/reader/full/2010-2011-pastel-tax-guide 31/44

29

FarmingincomeissubjecttotheprovisionsoftheFirstScheduletothe IncomeTaxAct.Farmerswhoarenaturalpersonsarealsoallowedto averagetheirfarmingincomeindeterminingtheirtaxliability.

Summary O The First Schedule’s Main Paragraphs

Rating Formula Applicable To FarmersBecauseafarmer’sincomeuctuatesfromyeartoyear,hemayelecttobetaxedinaccordancewitharatingformula.Theformulaisbasedonthe averagetaxablefarmingincomeinthecurrentandprecedingfouryears.Shouldheelecttomakeuseofthisformula,itisbindinguponhiminfutureyearsandheisnotpermittedtomakeuseoftheprovisionsrelatingto governmentlivestockreductionschemes,ratingformulaforplantation farmersandprovisionsrelatingtosugarcanefarmers.Forafarmercommencingfarmingoperationstheaveragetaxableincomefromfarmingintherstyearofassessmentendingonorafter1January2008willbetwothirdsofthetaxableincomeforthatperiod.

Capital Development Expenditure (Paragraph 12)

Thefollowingitemsofcapitalexpenditure,incurredduringayearof assessment,aredeductibleagainstfarmingincome:• expenditurewhichisnotrestrictedtotaxableincomefromfarming: - eradicationofnoxiousweedsandinvasivealienvegetationand preventionofsoilerosion• expenditurewhichisrestrictedtotaxableincomefromfarming: - dippingtanks,buildingofroadsandbridgesforfarmingoperations - dams,irrigationschemes,boreholes,pumpingplantsandfences - additions,erectionof,extensionsandimprovementstofarmbuildings notusedfordomesticpurposes - costsofestablishingtheareaforandtheplantingoftrees,shrubs

and perennial plants - carryingofelectricpowerfrommainpowerlinestofarmmachinery andequipment.Theexcessexpenditureovertaxableincomefromfarmingiscarriedforwardtothenextyearofassessment.Machinery,implements,utensilsandarticlesforfarmingpurposesarewrittenoffoverthreeyearsona50:30:20basis.Thisdoesnotapplytomotor vehiclesusedtoconveypassengers,caravans,aircraft(excludingcrop- sprayingaircraft)orofcefurnitureandequipment.Normalwearandtearmaybeclaimedontheseitems.

Non-arming IncomeIncomefromnon-farmingsourcesshouldbeshownseparately.Themostcommonexamplesofnon-farmingincomeare:• interestreceived• incomederivedbyafarmerfromcarryingonatradeotherthanfarming• annuities• rentalincomefromfarmland.

14–16 Plantationfarming17 Sugarcanedestroyedby re19 Ratingformulaforfarmers (whoarenaturalpersons)20 Expropriationoffarming

land

2–5&9 Valuationoflivestockandproduce6–7 Electionofstandardvalues8 Ring-fencingoflivestockacquisitions11 Donationsandinspeciedividends12 Capitaldevelopmentexpenditure13 Forcedsalesanddroughtrelief provisions

TAXATION OF FARMINGINCOME

8/8/2019 (2010 - 2011) Pastel Tax Guide

http://slidepdf.com/reader/full/2010-2011-pastel-tax-guide 32/44

30

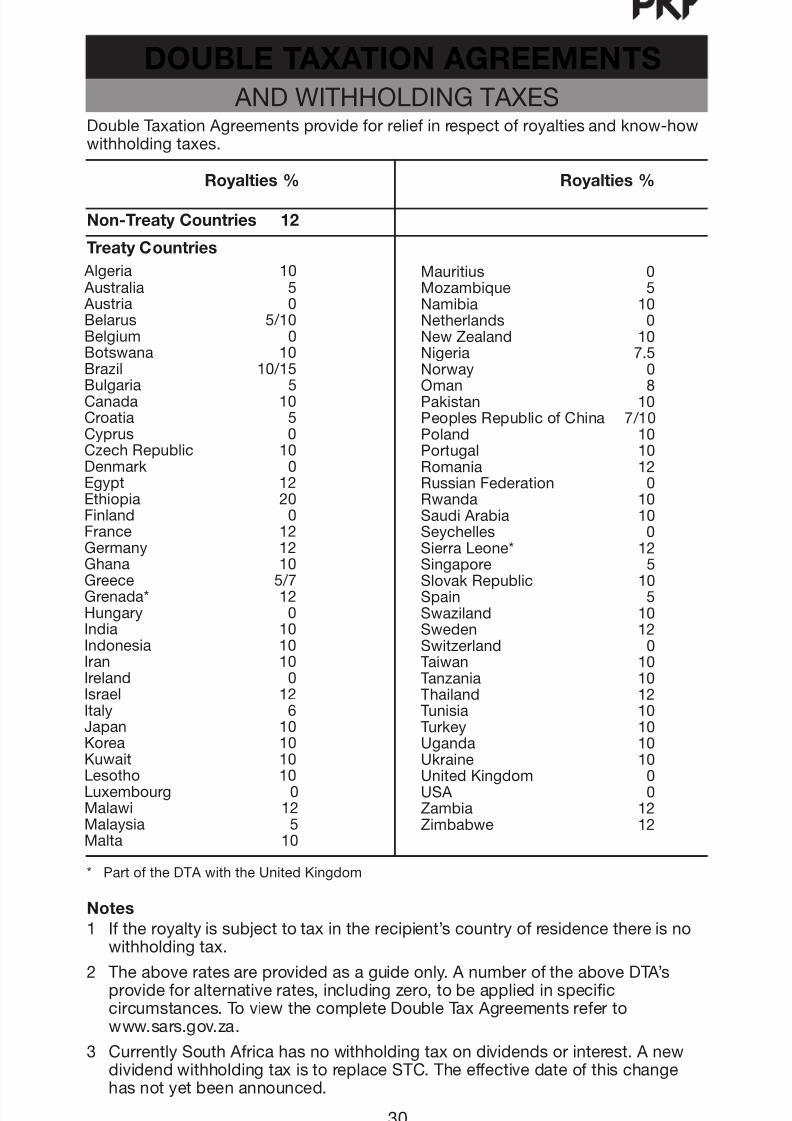

DoubleTaxationAgreementsprovideforreliefinrespectofroyaltiesandknow-howwithholdingtaxes.

Non-Treaty Countries 12

Treaty Countries

Algeria 10 Australia 5 Austria 0 Belarus 5/10 Belgium 0Botswana 10 Brazil 10/15

Bulgaria 5 Canada 10 Croatia 5 Cyprus 0CzechRepublic 10 Denmark 0 Egypt 12Ethiopia 20Finland 0 France 12 Germany 12 Ghana 10Greece 5/7 Grenada* 12 Hungary 0 India 10 Indonesia 10Iran 10Ireland 0 Israel 12 Italy 6Japan 10 Korea 10

Kuwait 10Lesotho 10Luxembourg 0Malawi 12Malaysia 5Malta 10

Mauritius 0Mozambique 5Namibia 10Netherlands 0NewZealand 10Nigeria 7.5Norway 0

Oman 8 Pakistan 10PeoplesRepublicofChina 7/10Poland 10Portugal 10Romania 12RussianFederation 0Rwanda 10SaudiArabia 10Seychelles 0SierraLeone* 12Singapore 5SlovakRepublic 10Spain 5Swaziland 10Sweden 12Switzerland 0Taiwan 10Tanzania 10Thailand 12Tunisia 10Turkey 10Uganda 10

Ukraine 10UnitedKingdom 0USA 0Zambia 12Zimbabwe 12

*PartoftheDTAwiththeUnitedKingdom

Notes

1 Iftheroyaltyissubjecttotaxintherecipient’scountryofresidencethereisno withholdingtax.

2 Theaboveratesareprovidedasaguideonly.AnumberoftheaboveDTA’s provideforalternativerates,includingzero,tobeappliedinspecic circumstances.ToviewthecompleteDoubleTaxAgreementsreferto www.sars.gov.za.

3 CurrentlySouthAfricahasnowithholdingtaxondividendsorinterest.Anew dividendwithholdingtaxistoreplaceSTC.Theeffectivedateofthischange hasnotyetbeenannounced.

DOUBLE TAXATION AGREEMENTS

ANDWITHHOLDINGTAXES

Royalties % Royalties %

8/8/2019 (2010 - 2011) Pastel Tax Guide

http://slidepdf.com/reader/full/2010-2011-pastel-tax-guide 33/44

31

Taxpayerswhoaremarriedincommunityofpropertyaretaxedonhalfoftheirowninterest,dividend,rentalincomeandcapitalgainandhalfoftheirspouses’interest,dividend,rentalincomeandcapitalgain,nomatterinwhosenametheassetisregistered(exceptforassetsexcludedfromthejointestate).Allothertaxableincomeistaxedonlyinthehandsofthespousewho

receivesthatincome.

MARRIED INCOMMUNITYOFPROPERTY

LEARNERSHIP ALLOWANCE

Asfrom1July2009ataxpayerwillbeentitledtoadeductionof100%ofthecostofsharesissuedbyaventurecapitalcompanysubjecttothefollowing limitations:• anaturalpersonmaydeductR750000inayearofassessmentanda totalofR2250000• alistedcompanyandanycompanyheld70%directlyorindirectlyby thatlistedcompanycandeductamaximumofthecostofupto40%of

thetotalequityinterestintheventurecapitalcompany• theventurecapitalcompanymustbeapprovedbySARSasaqualifying companyandfullanumberofpre-conditions.

VENTURE CAPITALINVESTMENTS

Employersareallowedtoclaimlearnershipallowancesinrespectofregisteredlearnershipsoverandabovethenormalremunerationdeduction.Foryearsofassessmentendingonorafter1January2010:• Whereanemployerispartytoalearnership,thelearnershipallowance

consistsoftwobasicthresholds,namelyarecurringannualcommence- mentallowanceofR30000andacompletionallowanceofR30000for eachyearofthelearnership,claimablecumulativelyattheendofthe learnership.• Forlearnerswithdisabilitiestherelevantallowancesareincreasedto R50000• Learnershipsoflessthan12fullmonthswillbeeligibleforapro-rata amountofthecommencementallowance(regardlessofthereasonthat thelearnershipfallsshortofthe12monthperiod).Ifalearnershipfalls overtwoyearsofassessment,thecommencementallowanceisallocated

pro-ratabetweenbothyearsbasedonthecalendarmonthsapplicableto eachyearbymultiplyingthecommencementamountbythetotalcalendar monthsofthelearnershipover12.Foryearsofassessmentendingbefore1January2010thelearnership allowanceregimewasasfollows:• Commencementallowance: - Thelesserof70%oftheprescribedremunerationofthelearneror R20000(forexistingemployees) - ThelesseroftheprescribedremunerationofthelearnerorR30000 (fornewemployees)

• Completionallowance:Thelesseroftheprescribedremunerationofthe learnerorR30000• Fordisabledpersonsemployedaslearnerstheinitialallowanceisequal to150%oftheannualsalaryofanexistinglearner(uptoamaximumof R40000)and175%foranewlyemployedlearner(uptoamaximumof R50000).Thecompletionallowanceforadisabledlearneris175%of annualsalary(uptoamaximumofR50000)• Specialprovisionsappliedtomultipleyearapprenticeshipcontracts

8/8/2019 (2010 - 2011) Pastel Tax Guide

http://slidepdf.com/reader/full/2010-2011-pastel-tax-guide 34/44

32

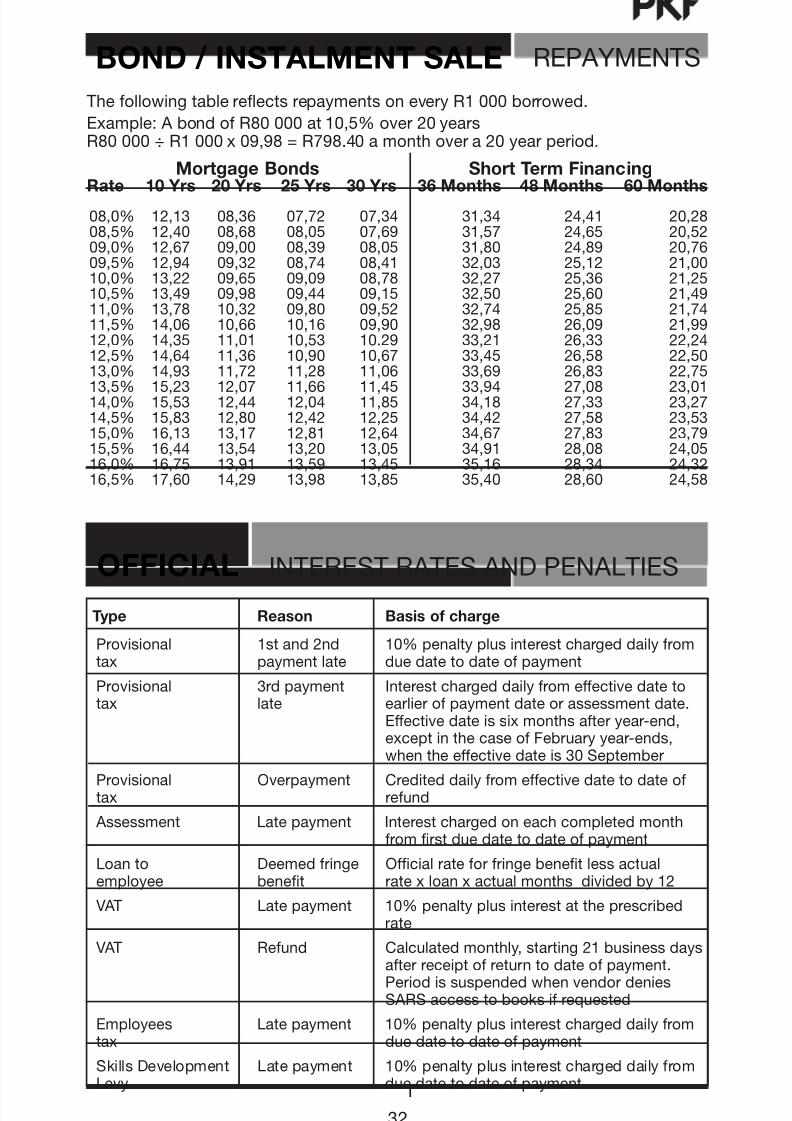

ThefollowingtablereectsrepaymentsoneveryR1000borrowed.

Example:AbondofR80000at10,5%over20yearsR80000÷R1000x09,98=R798.40amonthovera20yearperiod.

Mortgage Bonds Short Term Financing

Rate 10 Yrs 20 Yrs 25 Yrs 30 Yrs 36 Months 48 Months 60 Months08,0% 12,13 08,36 07,72 07,34 31,34 24,41 20,2808,5% 12,40 08,68 08,05 07,69 31,57 24,65 20,5209,0% 12,67 09,00 08,39 08,05 31,80 24,89 20,7609,5% 12,94 09,32 08,74 08,41 32,03 25,12 21,0010,0% 13,22 09,65 09,09 08,78 32,27 25,36 21,2510,5% 13,49 09,98 09,44 09,15 32,50 25,60 21,4911,0% 13,78 10,32 09,80 09,52 32,74 25,85 21,7411,5% 14,06 10,66 10,16 09,90 32,98 26,09 21,9912,0% 14,35 11,01 10,53 10.29 33,21 26,33 22,2412,5% 14,64 11,36 10,90 10,67 33,45 26,58 22,5013,0% 14,93 11,72 11,28 11,06 33,69 26,83 22,75

13,5% 15,23 12,07 11,66 11,45 33,94 27,08 23,0114,0% 15,53 12,44 12,04 11,85 34,18 27,33 23,2714,5% 15,83 12,80 12,42 12,25 34,42 27,58 23,5315,0% 16,13 13,17 12,81 12,64 34,67 27,83 23,7915,5% 16,44 13,54 13,20 13,05 34,91 28,08 24,0516,0% 16,75 13,91 13,59 13,45 35,16 28,34 24,3216,5% 17,60 14,29 13,98 13,85 35,40 28,60 24,58

BOND / INSTALMENT SALE REPAYMENTS

Type Reason Basis o charge

Provisional 1stand2nd 10%penaltyplusinterestchargeddailyfromtax paymentlate duedatetodateofpayment

Provisional 3rdpayment Interestchargeddailyfromeffectivedatetotax late earlierofpaymentdateorassessmentdate. Effectivedateissixmonthsafteryear-end, exceptinthecaseofFebruaryyear-ends, whentheeffectivedateis30September

Provisional Overpayment Crediteddailyfromeffectivedatetodateoftax refund

Assessment Latepayment Interestchargedoneachcompletedmonth fromrstduedatetodateofpayment

Loanto Deemedfringe Ofcialrateforfringebenetlessactualemployee benet ratexloanxactualmonthsdividedby12

VAT Latepayment 10%penaltyplusinterestattheprescribedrate

VAT Refund Calculatedmonthly,starting21businessdays afterreceiptofreturntodateofpayment. Periodissuspendedwhenvendordenies SARSaccesstobooksifrequested

Employees Latepayment 10%penaltyplusinterestchargeddailyfromtax duedatetodateofpayment

SkillsDevelopment Latepayment 10%penaltyplusinterestchargeddailyfromLevy duedatetodateofpayment

OFFICIAL INTERESTRATESANDPENALTIES

8/8/2019 (2010 - 2011) Pastel Tax Guide

http://slidepdf.com/reader/full/2010-2011-pastel-tax-guide 35/44

33

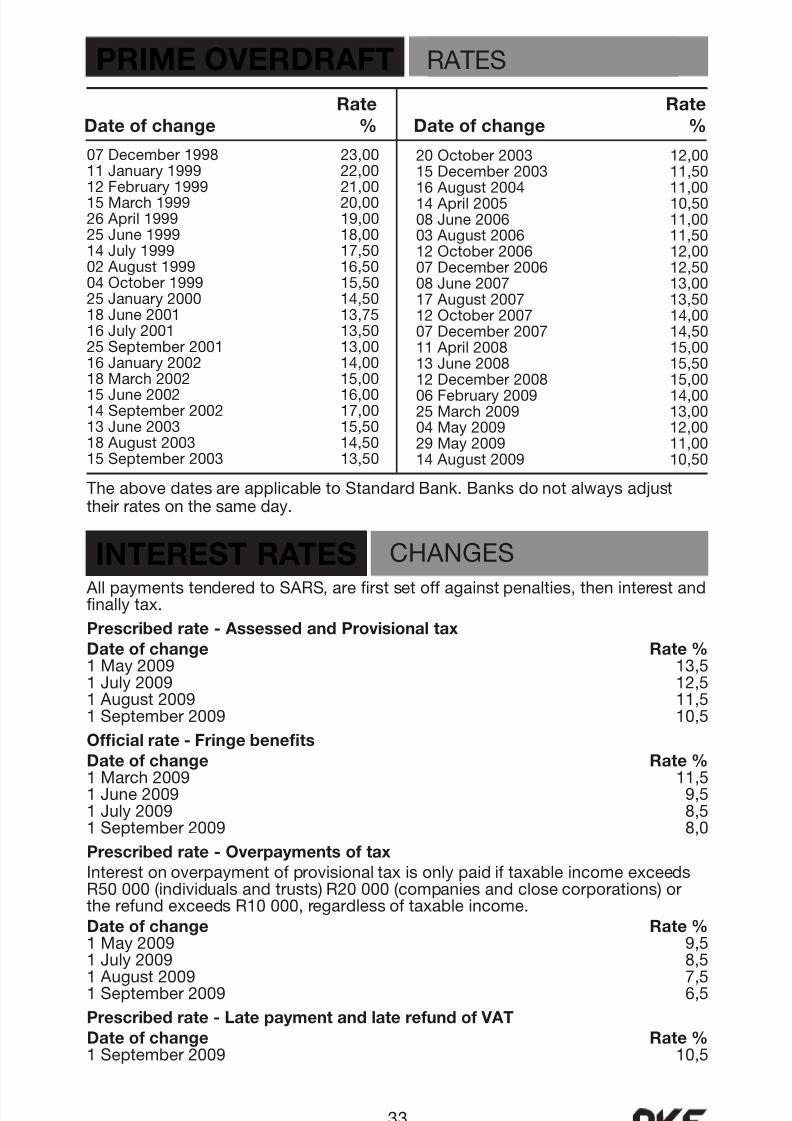

AllpaymentstenderedtoSARS,arerstsetoffagainstpenalties,theninterestandnallytax.

Prescribed rate - Assessed and Provisional tax

Date o change Rate %1May2009 13,51July2009 12,51August2009 11,51September2009 10,5

Ofcial rate - Fringe benefts

Date o change Rate %1March2009 11,51June2009 9,51July2009 8,51September2009 8,0

Prescribed rate - Overpayments o tax

InterestonoverpaymentofprovisionaltaxisonlypaidiftaxableincomeexceedsR50000(individualsandtrusts)R20000(companiesandclosecorporations)ortherefundexceedsR10000,regardlessoftaxableincome.Date o change Rate %1May2009 9,5

1July2009 8,51August2009 7,51September2009 6,5

Prescribed rate - Late payment and late reund o VAT

Date o change Rate %1September2009 10,5

INTEREST RATES CHANGES

Rate Rate

Date o change % Date o change %

20October2003 12,0015December2003 11,50

16August2004 11,0014April2005 10,5008June2006 11,0003August2006 11,5012October2006 12,0007December2006 12,50 08June2007 13,00 17August2007 13,50 12October2007 14,00 07December2007 14,5011April2008 15,0013June2008 15,50

12December2008 15,00 06February2009 14,0025March2009 13,0004May2009 12,0029May2009 11,0014August2009 10,50

07December1998 23,0011January1999 22,00

12February1999 21,0015March1999 20,0026April1999 19,0025June1999 18,0014July1999 17,5002August1999 16,5004October1999 15,5025January2000 14,5018June2001 13,7516July2001 13,5025September2001 13,0016January2002 14,00

18March2002 15,0015June2002 16,0014September2002 17,0013June2003 15,5018August2003 14,5015September2003 13,50

TheabovedatesareapplicabletoStandardBank.Banksdonotalwaysadjusttheirratesonthesameday.

RATESPRIME OVERDRAFT

RATES

8/8/2019 (2010 - 2011) Pastel Tax Guide

http://slidepdf.com/reader/full/2010-2011-pastel-tax-guide 36/44

34

On Immovable Property (on or ater 1 March 2006 )Transferduty,ifpropertyispurchasedbynaturalpersons:

Transferduty,ifpropertyispurchasedbycompanies,closecorporationsortrusts,isataatrateof8%onfullpurchaseconsideration

Notes• NotransferdutyispayableifthetransactionissubjecttoVAT•Wherearegisteredvendorpurchasespropertyfromanon-vendor,theVAT notionalinputtaxcreditislimitedtothequantumoftransferdutypayable.

Anotionalinputtaxcreditisonlyclaimabletotheextenttowhichthe purchasepricehasbeenpaid• Certainexemptionsapplytocorporaterestructuring• Theacquisitionofacontingentrightinatrustthatholdsaresidential propertyorthesharesinacompanyorthemember’sinterestinaclose corporation,whichownsresidentialproperty,comprisingmorethan50% ofitsCGTassets,issubjecttotransferdutyattheapplicablerate• Liabilitiesoftheentityaretobedisregardedwhencalculatingthefair valueofthecontingentrightinthetrust,thesharesinthecompanyorthe member’sinterestintheclosecorporation

• Residentialpropertyincludesdwellings,holidayhomes,apartmentsand similarabodes,improvedandunimproved,zonedforresidentialpurposes. Itexcludesastructureofveormoreunits,rentedbyveormore unconnectedpersons.Italsoexcludesxedpropertyformingpartofthe enterpriseofaVATvendor• Anypersonwhodoesoromitstodoanythingwiththeintenttoevade transferdutymaybechargedwithadditionaldutyuptotwicetheamount ofdutypayable.Suchapersonisguiltyofanoffenceandliableon convictiontoaneorimprisonmentforaperiodnotexceeding60months.• Notransferdutyispayableinrespectoftheacquisitionbyaqualifying naturalpersonofaprimaryresidencefromaqualifyingcorporateentity

ortrustbetween11February2009and31December2011.

Property value Rates o tax

R0-R500000 0% R500001-R1000000 5%onthevalueaboveR500000

R1000001andabove R25000plus8%onthevalueaboveR1000000

Themaximumlendingratesofinterestarecalculatedasfollows:

TRANSFER DUTY

NATIONAL CREDIT ACT

TheNationalCreditActdoesnotapplytolargeagreementsasdened,ortocreditagreementswheretheconsumerisajuristicpersonwithaturnoveraboveadenedthreshold,thestateoranorganofstate,orwherethelenderistheSouth AfricanReserveBankoraforeigner.

Mortgageagreements {(Reporatex2.2)+5%}peryearCreditfacilities {(Reporatex2.2)+10%}peryear

Unsecuredcredittransactions {(Reporatex2.2)+20%}peryearShorttermcredittransactions 5%permonthOthercreditagreements {(Reporatex2.2)+10%}peryearIncidentalcreditagreements 2%permonth

8/8/2019 (2010 - 2011) Pastel Tax Guide

http://slidepdf.com/reader/full/2010-2011-pastel-tax-guide 37/44

35

Nostampdutyispayableonleasesofimmovablepropertyenteredintoafter1April2009

STAMP DUTY

SECURITIES TRANSFERTAX