Embed Size (px)

Citation preview

2006 Lawn & garden Market 2006 Lawn & garden Market DataData

GREEN CIRCLE GROWERSGREEN CIRCLE GROWERS

-AN Analysis of industry, product, Consumer & marketplace Trends-

Industry TrendsIndustry TrendsAlthough 2005 Floriculture sales leveled off (Up 1.48%), industry growth has been steady for the past few years with sales growing 77% since 1995.

Source: USDA Floriculture Crops Summary

Despite aggressive industry growth over the past 10 years, numbers of growers decreased 7% from 2004 to 2005 (11,385 in 2004 – 10,563 in 2005)

Combination of above data is indicative of gradual centralization of consumer purchases. . .

NET >>>NET >>>

Industry formerly built on Ma & Pa outlets is now dominated by high-traffic mass merchants with consistent execution of programs & products. . .

Floriculture GrowthFloriculture Growth

Foliage16.2%

Cut Greens3.7%

Cut Flowers13.8%

Pots22.2%

Bedding / Garden44.1%

Foliage15.5%

Bedding / Garden56.3%

Cut Greens2.3%

Cut Flowers8.5%

Pots17.4%

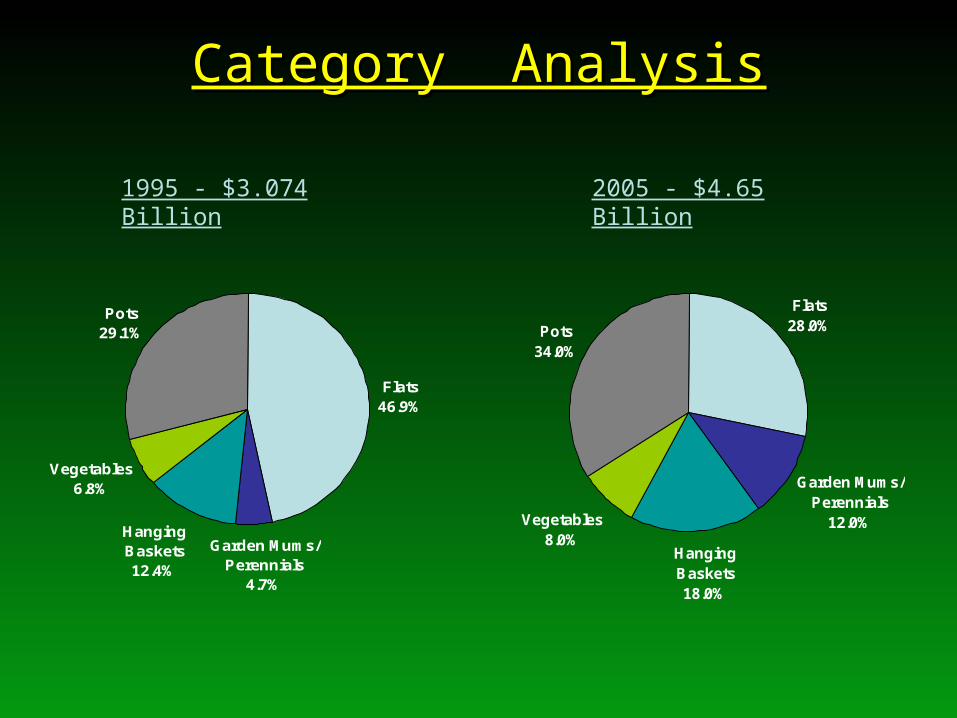

2005 - $4.65 Billion1995 - $3.074 Billion

Bedding & Garden category experiencing most aggressive growth over last 10 years.

Floriculture Growth – cont’dFloriculture Growth – cont’d

Overall Floriculture sales grew 51.1% over 10 year time period. . .

NET >>>NET >>>

Bedding & Garden has seen most aggressive growth in this time frame: B & G accounted for 44.1% of total in 1995 . . .By 1998 B & G took over a majority share of the market as sales accounted for 51.4% of the total. . .

By 2005, B & G sales were reported at $2.613 Billion, an increase of $92.6% fro 1995, and they accounted for 56.3% of the pie. . .

Cut flower, cut greens, and potted flowering plant segments have all relinquished share to the B & G plant slice over the last decade. . .

Vegetables6.8%

Pots 29.1%

Flats 46.9%

Hanging Baskets12.4%

Garden Mums/ Perennials

4.7%

2005 - $4.65 Billion1995 - $3.074 Billion

Flats28.0%

Hanging Baskets18.0%

Vegetables8.0%

Pots 34.0%

Garden Mums/ Perennials

12.0%

Category AnalysisCategory Analysis

Category Analysis – cont’dCategory Analysis – cont’d

Biggest fluctuation in sub-categories has occurred in flats. Impact on the overall mix has dropped 67.5% over the past decade.

NET >>>NET >>>

Decreased flat business has been spread over many segments of the business, including Potted Annuals, Hanging Baskets, and Mums & Perennials.

Significant growth represented in each of these segments indicative not only of market trends, but also rising price points and overall product sizes (i.e. 16” Coco HB’s, 14” Mums, 10” Poinsettias).

Although not shown, much of the flat business today is comprised of multi-packs, handle-packs, etc. Consumer is still planting, but ease of purchase and success with project is essential going forward.

What’s Selling?What’s Selling?

Geraniums-seed

Geraniums-Vegetative

Marigolds

3.3%

Impatiens

8.0%

2.3%

New Guinea Impatiens

4.2%

Pansies & Violas8.7%

Begonias5.3%

9.0%

Petunias8.7%

Vegetables7.4%

Other Flowering Annuals

43%

While breeding and plant innovation will continue to be important, product ideas and packaging will become paramount. Development of alternative packaging and price points is crucial as competition is fierce for these top items.

Consumer TrendsConsumer Trends

Unity Marketing Survey Gardening Results

““Simple is in, clutter is out”Simple is in, clutter is out”

Implication:Implication: Simple, big blocks of color in stores is key to attract customer & drive sales

““Do some of it for me” is in, “Do it all yourself “ Do some of it for me” is in, “Do it all yourself “ is outis out

Implication:Implication: More “Garden-Ready” material is required

Implication:Implication: Instant gratification is key, consumer needs early success to believe

Implication:Implication: Make it easier for consumer to find

success

Consumer TrendsConsumer Trends

October 2005 Garden Writer’s Survey:

Consumer’s primary purchase goal is color & Consumer’s primary purchase goal is color & decorationdecoration

Implication:Implication: Consistent product presentation is critical

Critical Factor’s in Consumers’ plant selections:Critical Factor’s in Consumers’ plant selections:

Color:Color: 51%

Size:Size: 30%

Cost:Cost: 31%

Brand:Brand: 7%

Source: Garden Writer’s Fall 2005 Survey

Wall Street Journal Survey:

Consumer is looking for “upscale experience Consumer is looking for “upscale experience with downscale prices”with downscale prices”

Consumer Trends - ContinuedConsumer Trends - ContinuedContainer Gardening continues to grow at Container Gardening continues to grow at fast pacefast pace

Growing at nearly a 20% annual rate

Ease of designing and planting an entire flower garden in an afternoon

Includes lower income demographic also . . .Great item for smaller yards, porches and apartment balconies

Much less maintenance (weeding, watering, etc) than conventional flower beds

Consistent growth in container components Consistent growth in container components

More avid gardener creates their own combinations

Strong sales of component plants in color (Gerbera Daisy, Dahlia, New Guinea, etc) and accents (Spikes, Bacopa, Vinca Vine, Coleus, etc)

Marketplace TrendsMarketplace Trends

Home Depot – Pay By Scan initiative continues to Home Depot – Pay By Scan initiative continues to produce varied results across countryproduce varied results across country

Strong move away from OPP strategy and to higher end material

Very container driven in percentages of Hanging Baskets & Patio Pots

Lowe’s – Continues to be favored destination Lowe’s – Continues to be favored destination of female consumerof female consumer

Economic downturn worked to their advantage

OPP strategy supplemented by big baskets and containers

Nursery was one of Top 5 categories in 2nd Quarter 2005

Marketplace Trends - Marketplace Trends - ContinuedContinuedWal-Mart Wal-Mart –– Continues low price push Continues low price push

Continues to go after narrow selection and large levels of stock

Mainly OPP driven with some markets experimenting with higher – ticket items

Independent Garden Centers – Continue to lose Independent Garden Centers – Continue to lose overall market shareoverall market share

I.G.C.’s have dropped from 14% of market in 1997 to less than 10% in 2004

Large chain retailers hold 71.2% share of live goods market in U.S. (and growing)

Overall business philosophy of attempting to include higher demographics slowly moving to Garden Center

Marketplace Trends - Marketplace Trends - ContinuedContinuedGardening will continue to grow as the #1 Outdoor Leisure Gardening will continue to grow as the #1 Outdoor Leisure

Activity in the U.S.Activity in the U.S.

Over 60 crowd – fastest growing demographic – Gardens at 46% level!!

80% of consumers report some involvement in Lawn & Garden

Home ownership is up to 68% (from 62% in 1997)

Largest outdoor leisure activity in U.S. (34% participate regularly)

In 2004, 86 Million households worked in their gardens, up from 67 Million in 1997

Home owners garden at 4 times the rate of non–home owners!!

Marketplace Trends - Marketplace Trends - ContinuedContinued

Consumers spent an average of $461 on Lawn & Garden supplies in 2004 – Double the 1994 figure

2000 $6.3 Billion

2004 $11.1 Billion

Landscaping/Gardening is the 3rd highest ranked home improvement project

Professional landscaping and garden installation in last four years has grown nearly 80%

Consumers are willing to spend on their gardening needs Consumers are willing to spend on their gardening needs rather than their lawnsrather than their lawns

Marketplace Trends - Marketplace Trends - ContinuedContinued

57% of women plant gardens themselves vs only 32% of men

Women lead the buying and implementation of most Women lead the buying and implementation of most Home Garden designsHome Garden designs

#1 use for a garden by consumers is “relaxation” (55% of consumers)#2 use for a garden by consumers is “entertainment” (32% of consumers)

Source: Home Channel News Trend Surveys

Where do you buy your outdoor garden supplies?

Consumers are looking to Chain Store Retailers as Consumers are looking to Chain Store Retailers as their primary destination for Lawn & Garden needstheir primary destination for Lawn & Garden needs

Source: National Garden Association Survey

79% say they have bought at large chain retailers

Marketplace Trends - Marketplace Trends - ContinuedContinued

2004 Floral Purchases for Mother’s Day Gifts:2004 Floral Purchases for Mother’s Day Gifts:

As of 2O04 Outdoor Garden items are now #1 gift As of 2O04 Outdoor Garden items are now #1 gift for Mother’s Day – FIRST TIME EVER!!!for Mother’s Day – FIRST TIME EVER!!!

40%40% Outdoor Garden Item (i.e. Hanging Outdoor Garden Item (i.e. Hanging Basket)Basket)

37%37% Cut FlowersCut Flowers

23%23% Flowering or Green Foliage HouseplantsFlowering or Green Foliage Houseplants

Keys to Success . . .Keys to Success . . .

High Foot – Traffic areas drive impulse . High Foot – Traffic areas drive impulse . . .. .

High Visibility & Display are critical to High Visibility & Display are critical to grab customer . . .grab customer . . .

80% of Floral Purchases are impulse driven 80% of Floral Purchases are impulse driven . . .. . .