Embed Size (px)

Citation preview

May 2006

Document of the World BankR

eport No. 36327-IN

India – PunjabN

ote on the Workings of the State Public Financial M

anagement System

Report No. 36327-IN

India – PunjabNote on the Workings of theState Public Financial Management System

Financial Management UnitSouth Asia Region

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

INDIA . PUNJAB

STATE PUBLIC FINANCIAL MANAGEMENT SYSTEM NOTE ON THE WORKINGS OF THE

CONTENTS PAGE

Executive Summary ....................................................................................................................... 1

Chapter 1 . Introduction and Background .................................................................................. 6 A . Introduction .................................................................................................................... 6 B . Background .................................................................................................................... 7 C . Structure of the Report ................................................................................................... 9

Chapter 2 . Budget Formulation and Budget Execution .......................................................... 10 A . Legislative Framework ................................................................................................ 10 B . Budget Formulation ...................................................................................................... 11 C . Budget Execution ......................................................................................................... 14 D . Recommendations for Action ...................................................................................... 22

Chapter 3 . Accounting and Financial Reporting ..................................................................... 23 A . Institutional Arrangements for Accounting in Punjab ................................................. 23 B . Computerization ........................................................................................................... 25 C . Drawing and Disbursing Officers ................................................................................ 25 D . Fragmentation o f Accounting Responsibility .............................................................. 26 E . Capacity Building ......................................................................................................... 27 F: Financial Reporting ...................................................................................................... 27 G . Recommendations for Action ...................................................................................... 28

Chapter 4 . Accountability .......................................................................................................... 29 A . Internal Control System ............................................................................................... 29 B . State Audit Organizations ............................................................................................ 29 C . External Audit .............................................................................................................. 31 D . Legislative Scrutiny ..................................................................................................... 34 E . Recommendations for Action ...................................................................................... 35

Chapter 5 . Local Bodies ............................................................................................................. 36 A . Local Bodies ................................................................................................................ 36 B . Urban Local Bodies ...................................................................................................... 36 C . Rural Local Bodies ....................................................................................................... 38 D . Recommendations for Action ...................................................................................... 40

Chapter 6 . Public Enterprises .................................................................................................... 41 A . Accumulated Loss ........................................................................................................ 41 B . Six Key Issues .............................................................................................................. 42

. ....................................................................................... C Recommendations for Action 43

Chapter 7 . Conclusion ................................................................................................................ 45

Annexes Annex A . Recent Reports on Public Financial Managemen b ...................................................... 47 Annex B . GoI’s Characteristics o f Good Accounting Systems for States .................................... 48 Annex C . Institutional Trends in Accounting Across India .......................................................... 49 Annex D . Comptroller and Auditor General Audit Reports ........................................................ 51 Annex E . Financial Performance o f GoP Public Sector Enterprises ............................................ 54

Figures Figure 1 . Public Financial Management System in Punjab ............................................................ 7 Figure 2 . Structure o f Government Accounts ............................................................................... 10 Figure 3 . Budget Realism in Selected Indian States ..................................................................... 19 Figure 4 . Accounting Model for Gram Panchayats ...................................................................... 39

Tables Table 1 . Supplementary Expenditure in Punjab ........................................................................... 14 Table 2 . Salary. Pension. and Interest Expenses ........................................................................... 15 Table 3 . Budget Execution Data for Selected Sectors. Annual Plan 2002-2003 .......................... 17 Table 4 . Release o f Funds to Local Bodies ................................................................................... 17 Table 5 . GoP’s Diversion o f Food Procurement Funds ................................................................ 18 Table 6 . Budget vs . Actuals: Tax and Non-Tax Revenue ............................................................. 19 Table 7 . Fiscal Marksmanship ...................................................................................................... 20 Table 8 . Share o f Non-Plan Expenditure ...................................................................................... 20

Table 10 . Personal Ledger Accounts ........................................................................................... 21 Table 9 . End o f Year Expenditures ............................................................................................... 21

Table 11 . Local Audit Department: Age Profile o f Outstanding Audit Objections ..................... 30 Table 12 . Internal Audit Organization: Summary o f Activities ................................................... 31 Table 13 . AG (Audit) Punjab: Outstanding Audit Objections ...................................................... 32

Table 15 . N e t Worth o f Selected PSUs ......................................................................................... 42 Table 14 . Operating Income and Profit/Loss & Accumulated Losses o f GoP’s PSUs/ACIs ....... 41

Table 16 . Explicit Guarantees issued by GoP ............................................................................... 43

ACKNOWLEDGEMENTS

This report was prepared by Parminder P.S. Brar, Lead Financial Management Specialist (Task Team Leader for this study). I t incorporates contributions from Donna Thompson (SARFM), Vinod Sahgal (SARFM), Papia Bhattacharya (SARFM), R. Ramanathan, (Consultant) and Hemant Chadha (Consultant). The analysis was undertaken over the period October 2003 to June 2004. A draft report was submitted in July 2004. I t was finalized after comments were received from the Accountant General in January 2005 and from the state government in May 2005. The report was updated by Ivor Beazley (SARFM) and Tanuj Mathur (SARFM) in 2006 to reflect subsequent developments.

This study has benefited greatly from the support and active cooperation o f the Government o f Punjab, especially from discussions with Captain Amarinder Singh, Chief Minister, Punjab and his team o f officials led by Jai Singh Gill, Chief Secretary, Punjab. We are particularly grateful to the following officials o f the Finance Department: B.R. Bajaj (Principal Secretary, Finance), G. Vajralingam (Secretary, Expenditure and Director o f Treasury), Vini Mahajan (Director, Disinvestment), Ravneet Kaur (Secretary, Finance) and S.P.Singh (Deputy Director, Financial Resources). The team also benefited from discussions with several other officials: A.K.Dubey (Principal Secretary, Local Self-Government), K.R.Lakhanpa1 (Principal Secretary, Irrigation & Finance), J.S.Kesar (Financial Commissioner, Cooperation) Tej inder Kaur (Principal Secretary, Education), Dr. B.C.Gupta (Financial Commissioner), J.R.Kunda1 (Secretary, Panchayats), Kusumjit Sidhu (Secretary, Power), R.S.Sandhu (Secretary, PWD), N.S.Kalsi (Secretary, Information Technology), A. Venu Prasad (Secretary, Mandi Board), Seema S. Jain (Deputy Commissioner, Roopnagar), S.R.Ladher (Director, Rural Development and Panchayats), and A.P.S. Virk (Joint Secretary, Planning).

The team would also l ike to record i ts appreciation for the excellent cooperation received from the officers o f the Comptroller and Auditor General o f India in Chandigarh, Principal Accountant General, Satyawadi , and Accountant General, Nand Lal.

The SARFM team led by Ian Mackintosh provided overall guidance. The peer reviewers were Gert Van Der Linde, Anand Rajaram, T.K.Balakrishnan, Nicola Smiters, and Rajat Narula. Comments were also received from Vikram Chand, Ivor Beazley, Sanjay Vani, Mohan Gopalakrishnan, Priya Goel, and Deepa Chakrapani.

Thanks are due to Pauline Chin Mor i for administrative and editorial support.

EXECUTIVE SUMMARY

A. Introduction

1. The purpose o f this note is to provide a preliminary assessment o f fiduciary risk' associated with the use o f public funds in Punjab and to identify areas for more effective financial control over scarce public resources. This note focuses on the performance o f the public financial management (PFM) system in Punjab. It covers the fol lowing f ive broad areas: (i) Budget Formulation and Execution; (ii) Accounting and Financial Reporting; (iii) Accountability -- Internal and External Audit and Legislative Oversight; (iv) Urban and Rural Local Bodies; and (v) Public Enterprises.

B. M a i n Observations

2. Consistent with other Indian states, the Government o f Punjab ( GoP) has a reasonable framework o f general financial rules, treasury codes, rules o f procedure, and related regulations governing public financial accountability and management. Monthly accounts are produced on time and annual accounts are produced within five months o f the end o f the financial year.

3. Recently, budget formulation has improved-there was a marked improvement in the estimation o f tax revenues during 2002-03. Other indications o f improvements underway are also visible-computerization in the 17 main treasuries i s complete, guarantees are subject to greater scrutiny than in the past, the GoP has indicated i t s resolve to establish a Guarantee Redemption Fund, and the practice o f parking lapsing appropriations has reduced dramatically. Almost half o f the personal ledger accounts (PLAs) have been closed. An active debt swap program has reduced the interest burden o n the state.

4. There have been improvements in public enterprises and local government as well. Regarding public enterprises, the GoP has also indicated i t s resolve to have independent audits conducted o f some large enterprises that could pose significant risks. At the village level, the GoP's initiative to computerize land records is facilitating transparency and improving the record o f publicly-owned assets. In addition, the GoP has signed a memorandum o f understanding (MoU) with the Government o f India (GoI), a Fiscal Responsibility and Budget Management (FRBM Act) has been passed, and a Medium-Term Fiscal Plan (MTFP) has been prepared.

5. The main challenge in Punjab i s to improve compliance with rules and regulations and to strengthen transparency and accountability. Modernization o f rules and procedures i s required together with more effective compliance monitoring and sanctions to deter poor performance.

6, In the past, there have been concerns in the areas o f cash management, and timely release o f funds. The treasury has not always been able to live up to its obligations o f making timely payments. Severe cash rationing has led to discretionary and non-transparent spending decisions have severely limited funds available for poverty-reducing programs and local bodies. Crucial

' Fiduciary risk i s the risk that funds appropriated will not be used for the purpose intended.

2

programs in education, health, and nutrition regularly receive less than half their appropriations. During the period 1996-2004, local bodies received only 3 1 percent o f their allocations.

7. Some other key challenges that need to be addressed include:

0 Budgetary Issues: Budget formulation and implementation challenges in Punjab are quite similar to those faced by Go1 as well as other states. There are myriad reasons: (i) Resources are spread too thin over existing schemes; (ii) there are large extra- budgetary funds (EBF); (iii) project evaluation i s poor; (iv) new schemes are announced even though old schemes cannot be adequately funded; (v) budget execution i s poor; and (vi) there i s bunching o f expenditures at the end o f the year.

0 Accounting System: The responsibility for accounting i s divided between the l ine department and the finance department (FD) o f the GoP and the Comptroller and Auditor General (C&AG) o f India. The accounting system being followed i s such that the three entities maintain three separate sets o f accounting records for the bulk o f transactions. Line departments prepare bills, the treasury makes the payments, and the accounts are prepared by the C&AG.

0 Accountability: The agency responsible for implementing programs has no authority for making payments; the one responsible for payment i s not responsible for accounting; and the one responsible for accounting i s neither responsible for implementing programs nor making payments and also reports to an extra-state authority. This overlap o f jurisdictions i s functionally inefficient because work i s done in triplicate and significant problems o f reconciliation exist. Most importantly, l ine departments do not receive accurate or timely information regarding progress o f expenditure on schemes, with the delays being as long as six months.

0 Internal Controls: The internal control environment i s weak and there are frequent instances o f non-compliance with rules and regulations. There i s a state audit organization with 12 field offices responsible for internal and statutory audit o f GoP receipts, expenditures, and provident fund accounts. But the impact o f this organization i s marginal. The local fund audit (LFA) unit has 562 employees, i s responsible for audit o f 17,382 organizations, and also has l i t t le impact. The LFA’s annual report for 2000-01 states that more than 1,03,000 o f i t s audit objections had not been complied with. Almost half o f them are more than 10 years old.

0 External Audit: There i s clearly a disconnect between the auditor and the auditee. The C&AG’s report for 2001-02 states that excess expenditures over grants have not been regularized since 1 996-97.2 The annual appropriation accounts for 200 1-02 records that “explanations for variations were not received from any o f the controlling officers.yy3 The government did not respond to reviews noting important

It i s understood that four years’ excess expenditure was recently regularized in March 2004, and the excess expenditure for 2002-03 i s s t i l l to be regularized.

C&AG Audit Report (Civil) for the year ended March 31,2002; p. 30, para 2.5.

3

issues such as systems failures, mismanagement, and misappropriation o f government money.4 Similarly, the C&AG Audit Report (Revenue Receipts) states that none o f the secretaries replied to the audit objections raised by the C&AG.’

0 Legislative Oversight: Eighteen Public Accounts Committee (PAC) re orts since 1993 are s t i l l to be replied to and complied with by the state government. I!

0 Urban Local Bodies (ULBs): Accounting and reporting in municipalities is poor and compliance with audit requirements has been weak. Even though GoP has issued instructions to municipalities to shift over to accrual accounting, these undertakings are not even maintaining satisfactory cash accounts. The Municipal Corporation o f Ludhiana has been attempting to introduce accrual accounting but process controls remain weak. Basic accounting functions such as bank reconciliations have not been completed for the last four years.

,

0 Rural Local Bodies (RLBs): There is weak capacity and poor record keeping at more than 12,000 gram panchayats. This is a major challenge because there is an important initiative underway to devolve additional powers to the three tiers o f panchayati raj institutions (PRIs). Even though these bodies are struggling to maintain rudimentary cash accounts, the GoP i s now in the process o f introducing accrual accounting at the village level. This could prove to be premature.

0 Public Enterprises: There is a weak regulatory environment governing public enterprises. Accounting standards are not rigorously enforced. Due to this, public enterprises were able to convert their biggest ever operating loss into their biggest ever operating profi t in the same financial year.7 Managerial ‘control and accountability i s weak and there is no dedicated cadre o f public sector managers in the state. Thus there are no systems o f incentives or disincentives to improve the performance o f these enterprises.

8. Although signing the M o U with Go1 and the passage o f the FRBM Act are steps in the right direction, what i s needed i s compliance with the agreed conditions. The state government has committed that i t will: (i) contain the rate o f growth o f fiscal deficit to 2 percent per annum in nominal terms; (ii) reduce revenue deficit as percent o f total revenue receipts by at least 5 percent points from the previous year until fiscal balance is achieved; (iii) cap the ratio o f debt to GSDP at the level achieved in the previous year subject to an absolute ceiling o f 40percent to be achieved by 2006/7 (28 percent by 2009/10); and (iv) cap outstanding guarantees o n long-term debt to 80 percent o f revenue receipts o f the previous year. Meeting these targets will be a challenge for Punjab.

Ibid. p. 54.

C&AG Audit Report (Civil) for the year ended March 3 1,2002; p. 54. ’ C&AG Audit Report (Revenue Receipts) for the year ended March 3 1, 2002, p. 12.

’ See Annex E for the Markfed example.

4

9. The overall conclusion o f this note i s that there i s a need to improve compliance with the rules and regulations laid down. The processes o f budget formulation, budget execution, expenditure control, internal and external audit, and legislative oversight need significant revamping and strengthening to achieve the objectives o f public financial accountability.

10. Transparency and accountability o f decision-making processes at the governmental level would significantly increase as Punjab effectively implements the Right-to-Information (RTI) Act, 2005. Such legislation could act as an instrument o f public accountability and improve the workings o f the overall PFM system.

11. Some o f the core P F M issues that need to be addressed in Punjab are: (i) improved revenue management and collections; (ii) ownership o f the budget by l ine departments; (iii) improved cash management; (iv) reduced EBF; (v) tighter expenditure controls; (vi) effective monitoring and evaluation o f public expenditure; (vii) more effective departmental accounting; (viii) improved accountability through timely response to internal and external audit findings and P A C oversight; and (ix) improved regulatory and corporate governance environment o f public sector undertakings ( PSUs).

12. The PFM reforms need to address these issues in order to minimize the risk to public funds in Punjab. This note suggests several recommendations for action. These actions are aimed at; (i) improving the capacity for public financial accountability; (ii) enhancing the quality o f management information; and (iii) strengthening resource management for better control o f the public purse.

C. Recommendations for Action

13. The GoP has expressed a desire to strengthen PFM and accountability systems in the state in line with best Indian practices. In this context, both short-term actions (August 2005 to July 2007) and medium-term actions (August 2005 to January 2009) are proposed. These recommendations are divided into the five sections discussed in this paper.

Functional Short- Term Action Area (August 2005 to July 2007)

revenues with fixed costs and priority expenditures. 1. Overall 1. Develop a realistic long-term plan to balance

......................... ........................................ .. . ........... .................. .....................,,,,,.............. . ................................................................................... " ................ ... ... .. ,... .........,. .. .,......... 2. Budget 2. Induct a core team o f professionally qualified

Manage- ment improving treasury operations.

accountants (at least 5) to support the FD in

Obtain professional advice on treasury operations. Improve predictability o f funds flow through treasuries. Sequence payments in a transparent manner. Require treasuries to publish aging profile and lists o f bills pending. Merge EBF into the budget.

quality o f revenue forecasting.

3 . 4.

5. 6. Establish a tax research unit in the FD to enhance the

Medium-Term Action (August 2005 to Januarv 2009)

1. Transition to proactive fixed-cost management in salaries, pensions, and interest with a time-bound

2. Ab initio review of all state plan and non-plan schemes; reduce and consolidate existing schemes; strengthen review processes for proposed new schemes; priority funding for schemes nearing completion; and improved monitoring system.

3. Ownership of the budget by line departments.

. ... ................ action ........ ..................................... plan. ............................ ....... .. ............. ... ......,..,.,....... .

.. . , .. , . . , .. ... .... , .. . ....... . ..... . . .................. ............ . ............ . ............ .... ... . ..... ....... . .... . ................ . . .. . .... .... . ......... .. .. .. ....... . . ............................. .. , .. . ... ........ ..... (.,, .. .. ..... , ........... ... ......... .... , .. ... .... .......................... ......... ....... ...... .... .. .. . .. , ,,..

5

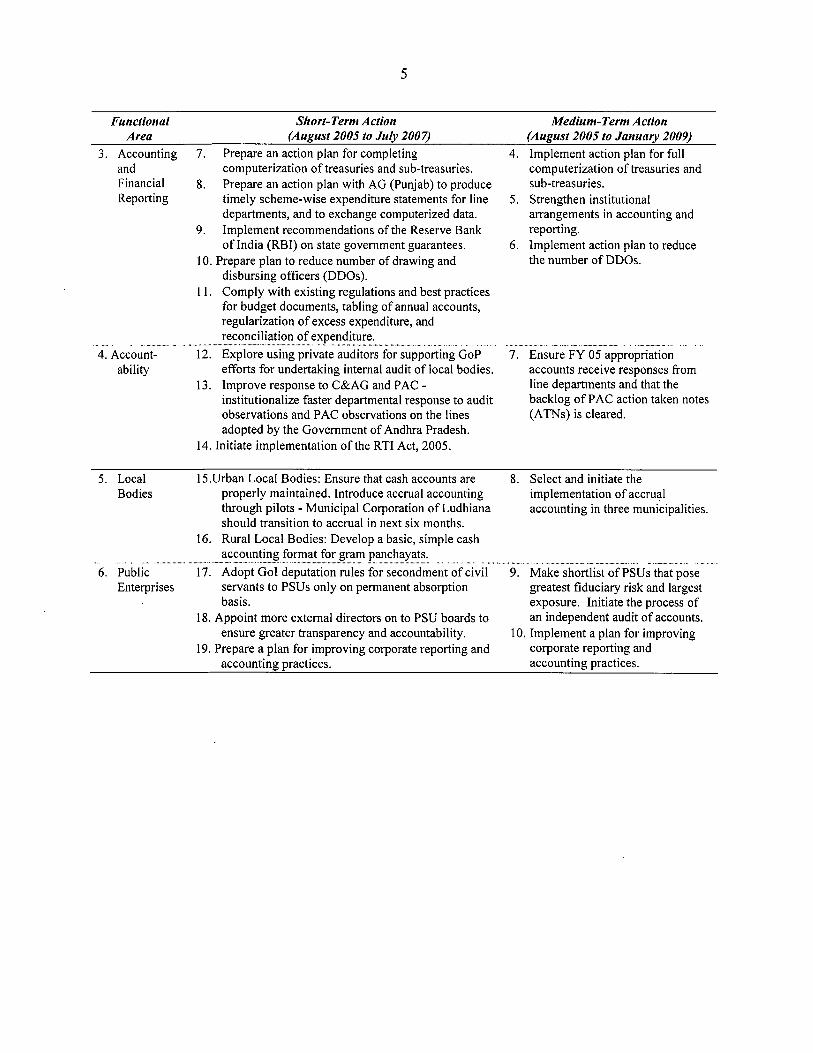

Functional Short-Term Action

3. Accounting 7. Prepare an action plan for completing Area (August 2005 to July 2007)

and Financial Reporting

computerization o f treasuries and sub-treasuries. Prepare an action plan with AG (Punjab) to produce timely scheme-wise expenditure statements for line departments, and to exchange computerized data.

9. Implement recommendations o f the Reserve Bank o f India (RBI) on state government guarantees.

10. Prepare plan to reduce number o f drawing and disbursing officers (DDOs).

1 1. Comply with existing regulations and best practices for budget documents, tabling o f annual accounts, regularization o f excess expenditure, and reconciliation o f expenditure.

efforts for undertaking internal audit o f local bodies. 13. Improve response to C&AG and PAC -

institutionalize faster departmental response to audit observations and PAC observations on the lines adopted by the Government o f Andhra Pradesh.

8.

.......................................................................................................................................................................................................................................................... 4. Account- 12. Explore using private auditors for supporting GoP

ability

14. Initiate implementation o f the RTI Act, 2005.

Medium-Term Action (August 2005 to January 2009)

4. Implement action plan for full computerization o f treasuries and sub-treasuries.

arrangements in accounting and reporting.

6. Implement action plan to reduce the number o f DDOs.

5. Strengthen institutional

............................................................................................................... 7. Ensure FY 05 appropriation

accounts receive responses from line departments and that the backlog o f PAC action taken notes (ATNs) i s cleared.

5. Local 15.Urban Local Bodies: Ensure that cash accounts are 8. Select and initiate the Bodies properly maintained. Introduce accrual accounting implementation o f accrual

through pilots - Municipal Corporation o f Ludhiana should transition to accrual in next six months.

16. Rural Local Bodies: Develop a basic, simple cash accounting format for gram panchayats.

servants to PSUs only on permanent absorption basis.

18. Appoint more external directors on to PSU boards to ensure greater transparency and accountability.

19. Prepare a plan for improving corporate reporting and accounting practices. accounting practices.

accounting in three municipalities.

................................................................................................................................................................................................................................................................n� 6. Public 17. Adopt Go1 deputation rules for secondment of civil 9. Make shortlist o f PSUs that pose

greatest fiduciary risk and largest exposure. Initiate the process o f an independent audit o f accounts.

10. Implement a plan for improving corporate reporting and

Enterprises

CHAPTER 1. INTRODUCTION AND BACKGROUND

A. Introduction

The purpose o f this note i s to provide a preliminary assessment o f the P F M arrangements in the state and the fiduciary risk associated with the use o f public funds in Punjab. It also identifies areas for improvement o f financial management o f scarce public resources and offers recommendations o n specific actions.

There i s a large body o f reports o n the functioning o f the financial management system in various states in India. Some o f these diagnostics have been completed by the state government i tself while other reports have been prepared by agencies such as the World Bank and the International Monetary Fund (IMF). The findings are remarkably similar in many o f the reports. (See Annex A for a listing o f the recent reports.)

The components o f the P F M system examined in this note are listed below and depicted in Figure 1:

Budget Formulation Budget Execution Accounting Financial Reporting Internal Controls and External Audit Legislative Scrutiny Urban Local Bodies Rural Local Bodies Public Enterprises

Internal Audit

7

Figure 1. Public Financial Management System in Punjab h

Budget Execution

External Audit Urban Local Bodies

Internal Controls & Internal Audit

4. This review o f the overall control environment as well as the workings o f the primary institutions o f financial accountability at the level o f the state government was undertaken over the period October 2003 to June 2004 by a World Bank team’ with the full support o f the GoP and the Accountant General (Accounts), Punjab. It was updated in 2006 to reflect subsequent developments.

B. Background

5. Punjab has the highest per capita income and is the most prosperous state in the country. I t has achieved the steepest decline in poverty over the past three decades among the major Indian states and in several areas it has already achieved the Mi l lennium Development Goals (MDGs). I t can be justifiably proud o f the fact that 99 percent o f rural households have access to safe drinking water, 94 percent o f six year olds are enrolled in primary schools, 72 percent o f children under twelve are immunized, 70 percent o f citizens are literate, 94percent o f Punjab’s citizens are above the poverty line, and the average l i f e expectancy is 68 years. These are standards that most other states in India are striving to achieve.2

6. After having achieved record growth rates in the 1960s and 1970s, growth perceptibly slowed down in the 1980s and 1990s. During the 1990s Punjab’s growth rate was 2.1 percent, the third lowest among India’s major states. A major contributor to this was the decade and a ha l f o f militancy and the impact i t had on growth and state finances. The industrial growth rate halved f rom 8 percent to 4 percent; the growth rate o f the services sector decelerated as well, and fel l by half, between 1987/88 and 1992/93. Even the

’ The World Bank team comprised Parminder Brar, Operations Policy & Country Services (OPCFM), Task Team Leader), Papia Bhattacharya, South Asia Region Financial Management (SAFWM), Hemant Chadha (Consultant), and R.Ramanathan (Consultant).

The World Bank (June 2004), “ Punjab Development Report.” 2

8

agricultural growth rate plummeted from around 6 percent per year to 2 percent per year during this period due to a decline in long-term investment associated with the uncertainty surrounding militancy activities.

Currently Punjab’s economy i s growing at a rate o f 4 percent against a national average o f 6 percent per annum. The Finance Minister o f Punjab in his 2004 Budget Speech noted that projections prepared by India’s Planning Commission for the Tenth Five Year Plan period (2002-07) indicate that Punjab will be among the four slowest growing o f the 28 states in the ~ o u n t r y . ~ The state has faced sluggish revenue growth and escalating expenditures over the past decade. Recently, there has been improvement in the fiscal situation as a result o f increased central government support, higher collection o f state taxes etc. However, i t i s unclear whether this improvement can be sustained in the long term.

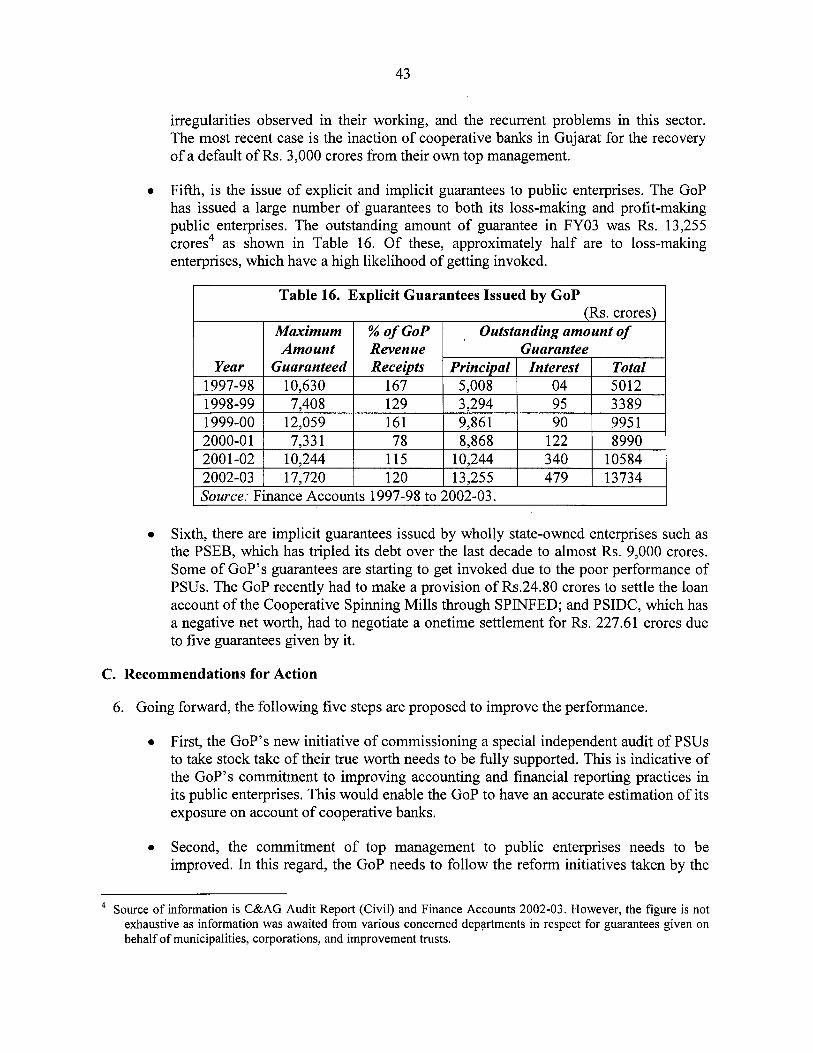

8. High fiscal deficits and weak management o f public finances have contributed to Punjab having a debdgross state domestic product (GSDP) ratio o f more than 50 percent-one o f the highest in the c0unt1-y.~ Punjab’s debt burden o f more than Rs. 40,000 crores has built up during the past decade as Punjab borrowed heavily to finance current consumption (i.e., to pay for growing salary, pension, interest, and subsidies). This i s more than 163 percent o f Haryana’s debt level and 235 percent o f Maharashtra’s, two states with similar per capita income to Punjab. The annual cost o f servicing debt (Rs. 3,500 crores) represents an increase o f 50 percent over the past five years. I t s hidden liabilities-arrears, delayed payments, unfunded liabilities, and contingent liabilities-are estimated to be approximately 20 percent o f GSDP.

9. Salary, pension, and interest payments have together amounted to more than 100 percent o f revenue receipts since 1996-97.’ In addition, subsidies paid out o f GoP’s budget, mainly for power and irrigation, have increased from Rs. 409 crores in 1990/91 to more than Rs. 2,000 crores a decade later. This i s in spite o f the fact that the state benefits from approximately Rs. 3,000 crores o f subsidies from Go1 as price support for foodgrain and fertilizers.

10. During the past decade the GoP experienced a prolonged cash crisis, due to which Punjab was unable to adequately fund capital and operation and maintenance expenditures essential for service delivery. Although this i s partly attributable to costs associated with the period o f insurgency, weak controls over revenue and expenditure also played an important role. Improvements in the state’s financial management practices will be critical in ensuring that recent improvements in the state’s fiscal position are translated into improved service delivery, poverty reduction, and economic growth.

GoP, Budget Speech o f Finance Minister, June 2 1,2004, para. 9. The two other states in this category are Bihar and Orissa. (“RBI Report on State Finances,” 2003-04, p. 22). Crisil had estimated that Punjab has the largest exposure in the county on the basis o f debt plus guarantees divided by revenue receipts. (Crisil Presentation on “State Government Guarantees,” 200 1). Revenue receipts excluding notional receipts such as interest receipts from the Punjab State Electricity Board

(PSEB) adjusted against rural electrification subsidy, net receipts from lotteries, and notional grants under waiver o f special term loans.

’

9

1 1. Tax performance is an important area to work on. Punjab’s tax-to-GSDP ratio i s lower than the average for high- and middle-income states and i t s tax buoyancy i s low. The World Bank recently estimated that the extent o f under-taxation in Punjab could be as high as Rs.1500 crores per annum. Growth i s l o w also due to the fact that the state’s share o f foreign direct investment (FDI) is only 0.7 percent.

12. Punjab performs less wel l in service delivery than other major states. A recent survey placed Punjab eleventh out o f sixteen major states surveyed. Reports f rom the Accountant General (AG) point to frequent instances o f non-compliance with financial rules and regulations, corruption, and weak enforcement o f sanctions against individuals who abuse public trust.

13, In the above background, an effective system o f public financial accountability and an informed public can help to promote effective financial management and spur demand for good governance and fiscal discipline. This is even more important at a time when further devolution o f authority and finances to local bodies and community organizations i s being planned.

C. Structure o f the Report

14. This report i s organized as follows:

o Chapter 1 provides a background on Punjab and a br ief description o f the state’s key indicators and fiscal situation.

o Chapter 2 focuses on the process o f budget formulation and execution, including the legislative framework.

o Chapter 3 focuses o n accounting and financial reporting and covers institutional arrangements for: accounting; computerization o f the treasury and financial reporting; DDOs; fragmentation o f accounting responsibility; and measures required for capacity building.

o Chapter 4 focuses o n accountability issues, including internal control and internal audit, external audit, and legislative scrutiny.

o Chapter 5 focuses o n financial management issues in local bodies.

o Chapter 6 focuses o n financial management issues in public enterprises.

o Chapter 7 provides a conclusion.

The World Bank (June 2004), “Punjab Development Report,” p. 8. The comparator for this estimation was Karnataka. ’ Survey conducted by the Public Affairs Centre. See The World Bank (June 2004), “Punjab Development Report, “p. 8, para. vii.

CHAPTER 2. BUDGET FORMULATION AND BUDGET EXECUTION

A. Legislative Framework

1. The framework for budget formulation and the P F M system is prescribed by the Indian Constitution in great detail.’ At the state level, the legislature is responsible for approving the budget and overseeing the use o f public funds. The Constitution also prescribes the overall structure o f the accounts that are to be maintained:2

0 Consolidated Fund: All revenues received, the proceeds from al l loans raised, and al l repayments f rom loans and advances are to be deposited into this fund. There are three types o f transactions in the Consolidated Fund: (i) receipts and expenditures of a current nature; (ii) receipts and expenditures o f a capital nature; and (iii) loans.

0 Contingency - Fund: Small corpus to be utilized in unforeseen circumstances.

0 Public Account: This primarily includes transactions where the government acts l ike a trustee or banker. It identifies claims on the resources o f the state (e.g., deposits and advances received by the state, employee provident funds, employee insurance schemes, and reserve or sinking funds). Although accounting records o f this fund are maintained separately, in practice these funds are freely pooled with the funds in the Consolidated Fund, as the state government’s banker --the RBI -- maintains one single account for a l l transactions pertaining to the state government. Figure 2 presents a diagram o f the accounts.

Figure 2. Structure of Government Accounts

I Government Accounts I

Deposits & Advances Reserve Funds

General Services Social Services Cash Balance Economic Services Grants in Aid & Contributions

Loans & Advances

Non Tax Revenue Grants in Aid & Contributions

Expenditure P General Services Social Services Economic services Grants in Aid & Contributions

’ This i s described in Articles 148-151, 166, 202-209,266-267, 282-284, and 293.

Structural Changes in the Classification System.” The schematic i s from CGA (October 2003), “Classification o f Government Transactions-Sub-Group’s Report on

11

2.

3 .

Monies f rom the Consolidated Fund can only be drawn and accounted for based upon appropriations approved by the legislature (Annual Financial Statement). Under Article 150, the accounts o f the union and o f the states are to be kept in such form as the President may, on the advice o f the C&AG o f India, prescribe. Detailed accounting instructions regarding the form in which the accounts are to maintained are prescribed by the Controller General o f Accounts (CGA), Ministry o f Finance, GoI, who exercises these powers on behalf o f the P r e ~ i d e n t . ~

The annual appropriation accounts and finance accounts are audited by the C&AG who submits the audit reports to the governor for onward transmittal to the legislature. These are examined by the P A C and the Committee on Public Undertakings (COPU) for follow- up action.

B. Budget Formulation

1. Process

4.

5.

6.

7.

As per the constitution, withdrawals from the Consolidated Fund must f i rs t be authorized by the legislature. The legislative assembly provides this authorization v ia an annual Appropriation Act. Supplementary or additional grants are approved by subsequent Appropriation Acts. The budget is examined and approved by the legislature. A vote on account provides temporary authorization pending the enactment o f the Appropriation Act (approximately two months after the start o f the financial year). Unl ike the GoI, in several states such as Punjab, there is no system o f intensive budget scrutiny by a Standing Committee o f the Legislature o f budget proposals.

The Punjab state budget, l ike the GoI’s budget, i s prepared o n a cash basis and therefore does not reflect arrears or receipts due. Contingent liabilities (e.g., guarantees which are likely to become actual liabilities), pension liabilities, non-performing assets, bad debts, and existing commitments made for projects for future years also do not find place in the budget. Due to the large number o f EBF, the budget presents an incomplete picture o f the financial position and resource use by the GoP.

The budget i s input based, showing provision o f h n d s for commitment to deliver services but not linking inputs to outputs or to deliverables. Performance i s currently measured in terms o f expenditures incurred and not in the quality or timeliness o f services delivered. Before Punjab considers moving toward performance-based budgeting it needs to “get the basics right.”4

The budget becomes a public document after it i s presented in the legislature. I t is available on the GoP website. Although budget information i s widely disseminated, its impact could

http://www.finmin.nic.in/the--niinistrv/dept expenditure/controIler zeneral-accounts/index.htmJ.CGA’s manual “Government Accounting Rules 1990” prescribes the format o f accounts to be adopted by state governments / accountant generals.

Professor Allan Schick (200 l), “Why most developing countries should not try New Zealand Reforms,” World Bank Research Observer, pp 123-13 1. See also “Budget Management in Developing Countries,” World Bank Seminar on Public Financial Management (2004).

4

12

8.

9.

be increased greatly if the budget was presented in an easier to understand and user- friendly format. The complexity and volume o f budget documents make transparency a major challenge for legislative scrutiny and public participation. Access alone i s insufficient to fulfill disclosure requirements if the documents are not clear and understandable by the intended audiences.

“Budget at a Glance”, a document presented by the GoP along with the budget, provides an overview o f the budget. I t i s a concise summary that i s wel l presented. However i t s utility would be greatly enhanced if it included additional information on aspects such as contingent liabilities and risk rating o f guarantees. This document needs to be improved for increased transparency. The GoP needs to adopt best practices o f the GoI, and states such as Karnataka, Andhra Pradesh, and Tamil Nadu.

Many o f the loans given to state-owned public sector undertakings (PSUs) are in fact bad debts and need to be written off. There i s no indication o f the overall extent o f non- performing assets. Many payments are carried forward to the next year due to lack o f funds. These liabilities are not mentioned in the budget documents. Regular use o f extra- budgetary resources also undermines the integrity o f the budget so that the budget document does not provide a full picture o f the financial position o f the state.

2. Allocation of Resources

10. Poor budget formulation is also the result o f weak capacity to appraise and prioritize schemes as wel l as the tendency to increase the size o f the annual plan to reflect increased development. In the GoP budget there is:

0 Pressure to announce new capital schemes even though existing ones are inadequately funded. Punjab has 600 state schemes with inadequate funding and little monitoring o f results or impact.

0 Inadequate scrutiny o f new schemes.

0 Pressure on states to take on new schemes in order to increase funding from the GoI.

11 There is poor allocation o f resources due to excessive number o f schemes, incremental budgeting, l i t t le f lexibi l i ty to line departments, and a systemic bias in favour o f capital expenditure over operation and maintenance expenditures. In order to improve the overall scheme performance, schemes should be prioritized. High-priority schemes should include those, which are critical for development and/or close to completion. The remaining schemes should be grouped into medium and l o w categories and should receive funding only if resources are available. New schemes should be considered only if they are o f high priority and adequate resources are available.

12. The GoP advised the Wor ld Bank in M a y 2005 that it has initiated the plan for categorization o f schemes and that high-priority schemes would receive priority funding and be monitored on a monthly basis by the Chief Secretary and the Chief Minister on a

13

quarterly b a s k 5 The GoP needs to publish the list o f high-priority schemes early so that the beneficiaries could become aware that these are l ikely to get completed in the near future, while schemes on other l i s ts are likely to be substantially delayed.

13. Incremental budgeting has resulted in less than optimal allocation o f resources. The GoP’s “Guidelines for the preparation o f R.E. for the current year and budget estimate (B.E.) for the ensuing year” provide for an incremental increase o f up to 5 percent per annum and additional justifications for increases exceeding that. Highly detailed line-item budgeting for thousands o f l ine items provides little flexibility to l ine departments as wel l as little information about results achieved. Input-based budgeting results in a poor performance orientation.

3. Revenue Estimation

14. An important issue that needs to be addressed in budget formulation is poor tax performance. Even though tax estimation improved in 2002-03, poor tax performance and large-scale tax evasion has resulted in inadequate resources being available to the state. This impacts budget formulation because the state does not have the resources necessary to meet its committed and developmental expenditures.

15. The tax performance o f two agricultural-based states - Punjab and Kerala -- i s widely divergent. In 1995-96 both states had tax collections o f approximately Rs. 1,500 crores per annum. Both have strong inward remittances from the diaspora abroad and have similar GSDPs. Punjab has a GSDP o f Rs.55, 000 crores, while Kerala has one o f Rs. 57,000 crores. In 2003-04, Kerala’s sales tax collection was Rs. 6,418 crores while Punjab’s was Rs. 3,575 crores despite Punjab having a higher proportion o f consumption expenditure.

4. Extra-BudgetaryFunds

16. Budget formulation i s a challenge partly due to the existence o f a large number o f EBF. The two main ones are:

0 Puniab Mandi Board and the Rural Development Board: These funds receive income from levy on sale o f agricultural produce. Last year the income o f these two funds was Rs. 600 crores.

0 Puniab Infrastructure Development Board: This fund receives income from levy o n the sale o f diesel. I ts income last year was Rs. 137 crores.6

17. Even though these revenues are raised by the state, the resources are outside the Consolidated Fund. There are weak oversight and governance structures, and these funds are not available to the treasury for meeting committed monthly expenditures.

’ GoP (May 2005), Comments of the GoP on the draft Report o f the World Bank on the PFM system in Punjab (July 2005).

In addition, these two bodies raised market loans o f more than Rs. 900 crores.

14

Year 1997-1998

18.

19.

20.

21.

Supplementary (% B. E.) No. of Cases

21.45 33

In 2002 when it prepared the “White Paper on State Finances”, the GoP proposed the merger o f these funds into the budget and the treasury single account because the “incorporation o f these fees into the budget would make them subject to the full rigors o f the budgeting and public expenditure management. They would also augment revenues o f the ~ t a t e . ” ~

1999-2000 2000-200 1

Table 1. Supplementary Expenditure in Puniab

19.82 34 3.54 26

200 1-2002 2002-2003

20.16 23 2.55 24

2003-2004 I 4.86 22

“restoration o f fiscal discipline would call for bringing in all extra-budgetary transactions into the Consolidated Fund.”8

However, in May 2005 the GoP expressed the view that i t had no intention o f merging these funds into the budget since “extra-budgetary funds are working well. If we merge funds into the budget the additional resources are likely to be used for committed and non- essential expenditure. Therefore there i s no need to merge extra-budgetary funds into the budget.” The solution i s not to keep public resources out o f the budget but to f ix the shortcomings in the core process itself.

5. Supplementary Demands

Due to poor budget formulation, Punjab also follows the trend o f other states in supplementary demands. On average, Punjab has sought a 19 percent increase in the budget through supplementary demands, which i s close to the norm for all states (See Table 1).

C. Budget Execution

1. Committed Expenditures

22. In Punjab from 1996-97 to the present, salary, ension, and interest have accounted for more than 100 percent o f total revenue receipts.” As shown in Table 2, the salary burden increased markedly after 1995. This was after the GoP adopted the recommendations o f GoI’s Fifth Pay Commission for increasing the salaries o f civil servants and pension payments.

23. Punjab’s wage and pension payments more than doubled between 1995-96 and 2000-01 from Rs. 2,180 crores to Rs. 5,426 crores in 2000-01. The severity o f the fiscal stress was

GoP (March 2002), “White Paper on State Finances,” p. 33. GoP (October 14,2002), “Report of the Public Expenditure Reform Commission, Punjab,” p. 29, para III.2.(a). GoP (May 2005), Comments o f the GoP on the draft Report o f the World Bank on the PFM system in Punjab (July 2004).

lo Excluding interest receipts from the PSEB adjusted against rural electrification subsidy, net receipts from lotteries and notional grants under waiver o f special term loans. Source: GoP (March 2002), “White Paper on State Finances,” and GoP Budget Documents, June 2004.

15

particularly acute due to Punjab having one o f the highest proportion o f civil servants per head in the country as well as pegging civil service salaries at a rate higher than the already high scales proposed by the GoI.

Table 2. Salary, Pension, and Interest Expenses (Rs. crores) I

SPI / 1 Salary I Pension 1 Interest I Total I Revenue I RR I

24.

25.

26.

Poor tax performance combined with escalating non-developmental expenditure has resulted in Punjab’s debt stock increasing from Rs. 15,250 crores in 1996-97 to Rs. 38,315 crores in 2002-03. Between 1998-99 and 2002-03, Punjab’s fiscal liabilities increased at an average annual rate o f over 16 percent. Punjab i s one o f the most highly-indebted states in the country with a debt to GSDP ratio o f 50.41 percent at the end o f 2002-03.’’

The GoP recently announced that during the past two years it swapped high-cost debt o f Rs. 3,400 crores carrying an interest rate o f 13.5 percent for lower-cost debt. During the current fiscal year (2004-05) it intends to a swap debt o f Rs. 2,800 crores. These efforts helped reduce the interest burden by Rs. 217 crores in the past two years. During the current year the interest liability i s expected to be reduced by an additional Rs. 179 crores. 12

Although additional savings o f Rs. 179 crores i s certainly helpful, it i s unlikely to have a major impact on reducing the fiscal stress in a state with projected fiscal deficits o f Rs. 6,118 crores or 6.79 percent o f GSDP during the current year.

‘I GoP, Budget Documents, June 21,2004, “Medium -Term Fiscal Reform Program.” l 2 GoP, Budget Speech o f the Finance Minister ( June 21,2004), para. 19.

16

2. Cash Management

27, The one single factor that has had the greatest impact on budget execution i s the severe cash constraint the state has been operating under. The GoP’s finances had been gradually deteriorating since the mid-1980s due to sluggish revenue growth and escalating expenditures. The RBI’s move for enforcing strict ways and means limits, combined with an escalating interest liability, has resulted in GoP finding that one o f i t s biggest challenges is making monthly salary, pension, and interest payments. As a result, the GoP has had to resort to irregular cash management practices and fire fighting o n a daily basis in order to manage competing demands. Recently, there has been an improvement in the fiscal situation as a result o f increased central government support, and higher collection o f state taxes etc.. However it i s unclear whether this improvement can be sustained in the long term.

28. The process o f cash management is through preparation o f a daily report o f collections and matching resources available with pending bills. With payments due regularly exceeding resources available, there i s an informal process o f prioritizing payments. In the past (up to FY 2004-05) there have been instances o f treasuries receiving telephonic instructions for releasing individual payments, which created an additional approval process that was non- transparent l3 and time consuming.

29. Due to the cash constraint there has been a large build up o f arrears. In March 2002 the level o f arrears was Rs. 315.39 crores. The position worsened in 2002-2003 with arrears more than doubling to Rs. 649.1 crores. Since then the problem seems to be pe rsisting. In October 2003 the Chandigarh treasury (largest o f the 17 treasuries in the state) had arrears o f Rs. 303.42 crores.

30. The cash crunch has resulted in the GoP delaying and reducing release o f funds for development schemes despite the appropriations having been approved by the legislature. Non-release o f funds by the FD resulted in critical pro rams in education, nutrition, and health sectors receiving only a fraction o f their allocation (See Table 3). 5

l3 The telephonic cash management system while completely non- transparent may have had the effect o f reducing the days o f overdraft with the RBI. In 2002-03 the number o f days o f overdraft came down to 53 from 120 in the previous year. (Source: RBI Report on State Finances, 2004). Program implementation i s also constrained due to excessive process controls imposed by the GoP on new schemes. Even after the budget i s approved by the legislature, new schemes must undergo authorization by the planning department and the FD, before funds can be released.

l4

17

Year

1996-97

Table 3. Budget Execution Data for Selected Sectors, Annual Plan 2004-05

(Rs. in Lakhs) Approved Revised Percent

Outlay Outlay utilized Expenditure

Agriculture and Allied Activities Animal Husbandry 1,199 327 0% Cooperation 926 326 0 Yo

Industry and Minerals 1,294 244 0% Rural Development 25,863 31,911 25,940 81%

Social Services

20% share of Original budget Revised budget net tax receipts outlay outlay

22.27 11.89

General Education Technical Education Medical and Public Health Water Supply and Sanitation Urban Development Labour and Labour Welfare

Amount actually

transferred

63.18

29,445 826

7,509 19,117 6,393

594

Percent transferred compared to share entitled

0%

67%

0,227 55% 217 64%

2,133 24% 7,289 62%

439 5% 0%

Nutrition 2,596 6,572 1,736 26% General Services Jails 100 33 1 70 21% Public Works 3,325 3,685 1,120 30% Treasury and Accounts 3 19 319 100% Source : Department o f Planning, GoP

31.

8,673 337

8,766 1,728 9,225

593

From 1996-2004, local bodies have received only 3 1 percent of their allocations as shown in Table 4.

Table 4. Release of Funds to Local Bodies (Rs. crores)

1997-98 I 94.11 I 106.74 I 66.12

18

32. In addition, to cope with the cash constraint the GoP took a “temporary” loan o f Rs. 165.3 1 crores from six state-level enterprises that has not been repaid.15 Incentives o f Rs. 470 crores committed under the State Industrial Policy have not been released. Funds earmarked by the Go1 for specific purposes have been diverted regu1arly.l6 Some examples are given below:

0 More than Rs. 4,500 crores (approx. $900 million) received f rom the federal food procurement agency for repayment o f commercial bank credit was diverted between 1996-2003.

0 Incentives for entrepreneurs under various schemes have not been released.

0 Arrears are regularly built up.

0 Individual payments are released on the basis o f telephonic instructions.

0 “Borrowings” f rom public enterprises are overdue and have not been repaid.

33. The implementation o f state programs i s crippled because the treasury does not release funds that have been duly approved by the legislature. The largest single diversion was that o f the cash credit limit (CCL) provided for food procurement. This diversion was through an “irregularity” o f Rs. 4,5 11 crores (US$ 900 million). Food procurement in Punjab i s funded through a C C L sanctioned by the RBI from a consortium o f public sector banks. The State Bank o f India i s the lead agency in the CCL for Punjab. The C C L is approved on a crop-to-crop basis, and both the C C L and the interest is to be paid when the procurement agency receives payment f rom the Food Corporation o f India.

iversion o rocurement Funds 34. Since 1996, the GoP’s “irregularity”

increased to more than Rs. 4,500 crores as the treasury regularly diverted funds received from the Food Corporation o f India while in transit for repayment o f the cash credit by commercial banks (see Table 5). This “irregularity” has since been converted into a term loan that the GoP has responsibility for discharging.

GoP (March 2002) “White Paper on State Finances,” p. 79. This was however repaid during FY 2002-04. 15

l6 Ibid. GoP (March 2002), “White Paper on State Finances” states that Rs.315 crores received from Go1 for specific programs was diverted by GoP.

19

35. These practices indicate that weaknesses in P F M system extend to lending and regulatory agencie~. ’~ This raises fundamental questions about governance and accountability arrangements as wel l as undermining the integrity o f the budget.

3. Fiscal Marksmanship

36. Punjab has in the past been over-estimating revenue receipts at twice the average o f the major states except Orissa (See Figure 3).

Figure 3. Budget Realism in Selected Indian States

Deficit Management FY 01 - 02 Actuals - % increase over budget estimates

-........... ................. _-lr ... 111 ..

37. A though there was an improvement in tax revenue estimation in 2002-03 as shown n Table 6, non-tax revenue was o f f the mark by 33 percent. This has improved in 2003-04, where tax and non-tax revenue were o f f the mark by 3 percent and 4 percent respectively.

Table 6. Budget vs. Actuals: Tax and Non-ax Revenue 1 Tax Revenue (Rs. crores) Non-tax Revenue (Rs. crores)

~ ! 1 j ! i I Estimate Actual I Shortjdl I Variation Estimate I Actual I Shortfnll 1 Variation I Budget / j I I Budget I i

Year 1999-00 , 4,166 1 3,947 .......... ........................................... , (-)219 1 ............................... -5% / i.. 2,221 .,” 1 2,326 ,. I (+)lo5 .i 5%

............................ 5 ’ (-)455 1 -9% I 3,656 2,935 / (-)721 I -20% .................................... ’ -8% i 3 535 1 2,960 (-)575 I -16% 2001-02 : 5,874 , 5,430 .i I (-

............................ 2002-03 i. ............... 6423 ?.. 1 6360 I (-)63 -1% 6046 I 4036 I (-)2010 I -33% .............. t........ .... b ............ i .................................. _ ..................................... i .................. 2 ............................. 4 ............. ?. ....................................................... 2003-04 / 6,332 1 6,146 I (-) 186 I -3% I 4,856 I 4,665 I (-) 191 1 -4%

......................... ..................................... .................................................. ...................................

............................ ~ ........................................ 1. ........................................... i .................................................. i... ........................... ...i... . . . ................................................ ..................... i ...................... .................................... ................................ ........... .......................................... ..! .............. .!... ................................................. .................................................. i . . . . . . . . . . . . . . . . . . .

.....................

Source: Budget at a Glance and Finance Accounts: 1999-2000 to 2003-04

” The GoP’s position i s that these funds were utilized for meeting the committed expenditures (salary, pension, and interest payments) o f the state. If so, then utilization o f the funds should have been reflected in the monthly accounts produced by the AG (Punjab) and would have resulted in excess expenditures under appropriations. However there were savings in expenditure in the years that the diversions took place.

20

39, A characteristic o f budget execution in India, both at the

38. Fiscal marksmanship needs to be improved. As shown in Table 7, there is large variability o f estimates; though forecast o f revenue receipts and expenditure shows an improvement in the accuracy in the last few years, the forecast for capital expenditure and net loans and advances needs further improvement.

Table 8. Share o f Non-Plan Expenditure

1997-98 , 13-57 18-82 I 20.1 1 , 47.5 1 I 1st Qu I 2nd Qu I 3rd Qu I 4th Qu

,_______________________________________--------------------------------------------------------.------.------.----------- Table 7 Fiscal Marksmanship (percent)

: 1997-98 : 1998-99 : 1999-00 :2000-01 :2001-02 :2002-03 :2003-04 : P

;Revenue Receipts

;BE-Actuals -10.07: 30.68; 5.30: -8.86; -20.98; -11.21; -11.25: :Revenue Expenditure ; -21.67; 3.12; -1 1.71 ; -3.51 ; -3.5 13 -3.91 ; 3.38;

i BE-RE ; 22.60; 14.733 -6.30; 9.82; -14.82; -2.82; 1.00;

; BE-Actuals ; -16.273 12.26; 0.86; -16.273 -6.93 ; -7.13: -8.80: ; BE-RE

!Capital Expenditure : BE-RE 1 . -5.30: -36.953 -38.59; -13.65; -13.65; -35.49; -25.64i

;Net Loans and Advances ; i BE-RE -3.71; 2.73; 77.533 54.763 45.24; -42.44; -351.953 ;BE-Actuals ; 95.14; 98.53; 83.59; 60.37; 33.333 8.163 834.04;

:Note: Positive numbers represent excess over original estimates, negative numbers represent savings over original estimates. 3

. :BE-Actuals 4.02; -5.66:: 80.53; -4.283 -32.34: -75.00: -55.90:

i f i y r ~ i punjab b ~ d ! t u r e !%OJES commiss!o?-Reg~~~<2~~?),page~0, Go!': - - - - - - -. - - - - - - - - - - - - - - - - - - - - - - - - - 1

state and national level, i s the seasonality o f spending. Approximately three-quarters o f total expenditure is classified as "non-planyy'8 as shown in Table 8. There i s large seasonality o f spending with a significant share o f expenditure being incurred in the last quarter.

I ............................. i ............................ i .............................................. i ...................................... 4 .................................................. I I. 1998-99 i 22.13 I 18.74 ' 27.94 I .......................................... : .................... .i. .................................... i ........... ..I? !..:? ..... i ........................................... 1999-00 16.19 I 18.08 I 28.53 I 37.2 2000-01 1 15.58 20.58 I 21.71 I 42.12

....................................... 4. .................................. !.., ............................................................................. .,.. ...............................................

.................................................................... i ....................... ............,.... .................................... "2001-02 1 16.3 i 23.82 21.98 / 37.9 ................. ................................ ........... *. ............................................. i .................................. 4 .................................................... 2002-03 1 15.64 1 16.24 I 22.02 I 46.1 2003-04 I 13.7 I 21.36 I 19.03 I 45.91

Source: GoP.

........................................................................................... i ................................................... i ..................................... i ..................................

'' While not strictly correct this i s broadly classified as non-developmental and developmental expenditure respectively.

21

Year 1997-1998

40. Not only i s there bunching in the last quarter, but also a large proportion o f spending takes place in the last month o f the financial year. Year after year a large proportion o f the GoP’s 30 grants i s spent in March, just before the funds are due to lapse as shown in Table 9. The percentage o f expenditure incurred in March 2003, as a proportion o f total expenditure for FY 2003 was 77 percent for rural development programs (MH 4515 and 4707), and 39 percent for local bodies and PRIs.

Grants March of F Y 17 36 to 100%

Table 9. End o f Year Expenditures Actual

Expenditure in

1998-1999 1999-2000

25 21 to 100% 15 37 to 100%

2000-2001 I 10 I 36 to 100% Source: C&AG.

5. Personal Ledger Accounts

41. Some o f this seasonality in expenditure trends i s due to actual spending, but also to book transfers to avoid lapse o f funds. The GoP institutions, l ike other states, transfer funds to personal ledger accounts (PLAs) in the public account (PA) in order to avoid funds lapsing.

42. A PLA i s a device intended to facilitate the account administrator to credit receipts into and effect withdrawals directly from the account, subject only to the condition that the withdrawals do not exceed the available balances. l 9

I Table 10. Personal Ledger Accounts Major Head Description 2000-01 2001-02 2002-03

8443- 106 Personal Deposit 3 66 366 3 69 8443- 1 10 PCEF 16 16 19

15 18 137

14 Total: 548 548 560

................................................................................................................................................................................................................................................................e�

................................................................................................................................................................................................................................................................F�

............................................................. ................................ ...................................................................................... ..........................................................

.................................................................................................................

.................................................. ................................. ............ ...........

No. o f PLA Accounts where balances were carried over: 548 548 560 Source: Accountant General, Punjab.

43. Over the past three years PLAs increased from 548 to 560 as shown in Table 10. However, the GoP recently indicated i ts intention to both drastically reduce as well as monitor the performance o f PLAs. It i s understood that approximately 357 PLAs with an outstanding balance o f Rs. 24.57 crores have been closed recently. Given existing accounting rules and constitutional provisions, i t would be extremely difficult to close all these accounts, but their performance needs to be closely monitored.

l 9 Under Treasury Rules, these are authorized only in the following cases: (i).administration o f wards and attached estates and estates under government management; (ii) certain regulatory activities where government receipts are credited into and withdrawals directly from the P.L.A without any outgo from the consolidated fimd; and (iii) liabilities arising out o f any law or rule out o f any special enactments.

22

D. Recommendations for Action

44. Going forward, restoring the credibility o f treasury management needs to be a high priority for improvement. The credibility o f the treasury, and indeed o f the GoP, depends upon an assurance that funds will be used for the intended purposes, as voted in the budget. This has not been happening in Punjab for the past few years.

45. The treasury requires qualified staffing and specialized expertise to discharge its duties. The FD should revamp i t s treasury systems and procedures. This may require external advice f rom experts with extensive experience in treasury operations.

46. Because the treasury needs qualified accountants in the short term, it i s suggested that before longer-term capacity building takes place, a core team o f qualified finance professionals (e.g., chartered accountants, cost accountants, and MBA-finance) be inducted immediately. I t i s suggested that a core group o f five accounting professionals be made available to the Director o f Treasury to support this work.

47. This team could either be recruited or brought on a deputation basis and made responsible for supporting cash management and treasury operations. The same team could also be utilized for review o f selected plan schemes and improved budget monitoring. Strengthening the treasury needs to be accompanied by the assimilation o f EBF which can help ease the liquidity crisis the government is facing.

48. The longer-term solution i s clearly controlling expenditures and improving tax performance.

CHAPTER 3. ACCOUNTING AND FINANCIAL REPORTING

A. Institutional Arrangements for Accounting in Punjab

1. Complex institutional arrangements for accounting negatively affect the performance and impact o f the P F M system. Currently three sets o f accounts books are maintained for the bulk o f state government transactions. Despite al l this record keeping, there i s a large delay o f up to several months for line departments to receive accurate information regarding the progress o f expenditures on different schemes.

0 The first and init ial set o f accounting records is maintained by line de artments. These departments have DDOs who are only authorized to prepare bills. They are attached to specific treasuries or sub-treasuries to which they submit bi l ls for payment. They are required to maintain records o f a l l receipts and, expenditures and to submit periodic reports to their headquarters. In a cash-constrained state such as Punjab, where there are large amounts o f pending bills in the treasury, DDOs do not have accurate expenditure information.

P

0 The second set o f accounting records i s maintained for “conventional” departments by the, treasury or for “works” departments (public works and forests) by divisional accounting units.* Treasuries make payments, and prepare major head-wise summaries that provide information on a functional basis. They forward these summaries, along with original vouchers to the AG for compilation o f the monthly account.

0 The third set o f accounting records i s maintained by AG (Accounts). The AG i s the accounting authority for the state and it produces its own set o f accounting records based upon paid vouchers and revenue receipts received f rom the treasury. This i s merged with compiled accounts received from the public works department (PWD) and forest divisions, and RBI advice on inter-governmental transactions to produce the state government’s monthly account.

2. Line departments that are executing programs do not have the authority to make payment^.^ The treasury, which makes payments, i s not responsible for producing monthly accounts. The AG who produces the accounts does not make payments for schemes and does not report to the state government but to the constitutionally independent C&AG. This i s the “treasury” system o f accounting that the country inherited f rom colonial times.

’ There are a very large number o f DDOs in every state. Karnataka and Tamil Nadu have over 21,000. The level o f aggregation varies from state to state. In some states, consolidation i s done only at the f i rst- tier level

(major head - functional classification) while in states such as Andhra Pradesh and Tamil Nadu, treasuries prepare consolidated accounts.

Other than the “works” departments o f forests, irrigation, and PWD.

24

3.

4.

5.

6.

7.

8.

9.

This system entails that Punjab has approximately 7,800 DDOs who prepare bills in l ine departments and submit them to treasuries for payment. Depending upon cash availability, these bills are paid by the 18 district treasuries and 77 sub-treasuries.

The sub-treasuries render cash accounts duly supported by paid and receipt vouchers to the accredited treasury. Treasuries in turn also make payments and submit their documentation to AG (Accounts) for compilation. The AG (Accounts) Punjab also receives compiled accounts f rom 220 PWDs and 40 forest divisions. Based upon this, the AG enters al l the data f rom the vouchers into C&AG’s computerized system and compiles the state government’s monthly accounts.

The AG’s monthly account provides expenditure and receipts details at the major head level (functional classification). This is a very high-level aggregation that i s o f limited utility to l ine departments. It is not possible to monitor the progress o f individual programs or schemes at this level.

There is a large time lag-up to six months-for the f l ow o f reconciled program- wisehcheme-wise expenditure information to decision makers. In September 2003, the GoP was reviewing scheme-wise expenditure data for the previous financial year (i.e. for March 2003).

A s can be expected, keeping accounting results in triplicate poses serious problems for reconciling accounting records. Departmental figures o f expenditure need to be reconciled with those o f the AG (Accounts & Entitlements) every month. This is a challenge. In Punjab, 98 controlling officers have not reconciled their figures f rom 1992-93 to 2002-03 for an amount o f Rs. 6,265 crores, which affects the accuracy o f the annual accounts and budget execution information produced annually. 4

Despite an enormous amount o f effort expended to maintain accounting records and reconcile figures, in practice:

0 Line departments responsible for service delivery do not get timely revenue or expenditure information;

0 the treasury is only partially aware o f the budget execution progress because it does not receive budget execution data f rom the works departments or the RBI; and

0 the AGs prepare the monthly account through consolidating data at a major head (functional) level that is o f l imited utility to l ine departments and the state government.

These accounting arrangements need to be modernized. The Go1 is o f the view that accounting and service delivery need to be integrated into the same entity, as i s often the

During FY 2004-05, up to November 2004, o f the 209 major heads for which reconciliation was required to be done by controlling officers, in 58 cases there were no transactions, in 20 reconciliation had not even been started and in the remaining 13 1 cases it was incomplete.

Source: AG (Punjab), January 2005.

25

case worldwide. states.)

B. Computerization

(See Annex B for GoI’s characteristics o f good accounting systems for

10. Several states have addressed the challenge o f fragmentation o f accounting responsibility through computerization. The project report for treasury computerization was prepared almost eight years ago, in 1996-97. This envisaged an investment o f Rs. 270.74 crores for computerization o f a l l 17 treasuries and 68 sub-treasuries.

1 1. The project i s being implemented by a central government agency, the National Informatics Centre (NIC). The project has taken much longer than expected for a variety o f reasons, including inadequate allocation o f resources for the task, cash constraints, and high turnover o f the N I C staff. However, significant progress has been made recently and computerization has been extended to 17 treasuries and 52 sub-treasuries and i s being closely monitored to ensure long-term stability.

12. The GoP’s experience is in contrast to states such as Karnataka where in less than three years al l 215 treasury offices were computerized at a cost o f less than Rs. 40 crores. All treasury offices are networked through a dedicated satellite-linked communications system and online information i s available at a central location. The system provides for online data entry and cheque writing, classification o f receipts and expenditures, generation o f the management information system (MIS) reports, and effective budgetary controls before payments are made. After having successfully completed this phase, the computerization project is now focusing on payroll, pensions, capital project budget cycle, and extension o f the network to cover DDOs. 5

13. The GoP should complete the computerization process by extending coverage to the remaining sub-treasuries and fully testing the networking functionalities. This could have a significant positive impact o n overall financial control in a relatively short time.

C. Drawing and Disbursing Officers

14. Punjab has approximately 7,800 DDOs who add enormously to the accounting task. These DDOs need to reconcile their accounts on a regular basis with both the treasury and the AG (Accounts). This by itself i s a huge task.

15. There is clearly a need to reduce the number o f DDOs. The GoP could fo l low the example o f Uttar Pradesh, which had more than 30,000 DDOs at one time. Uttar Pradesh took the decision to rationalize the number o f DDOs through applying the principle: “one DDO per department per district” and acted to reduce their number by more than two-thirds to less than 10,000.6

See World Bank (April 2004), “India: Karnataka State Public Financial Management and Accountability Study,” pp. 31 and 32.

Government o f India, Ministry o f Finance, CGA (1998), “Accounting in State Governments: Need for Reorganization and Options,”, para. 3.13.

26