Embed Size (px)

Citation preview

PricewaterhouseCoopers 1

2005 Budget Memorandum

Managing Our Resources

National Budget 2005

We are pleased to set out in this Memorandum our commentary on the National Budget 2005with particular reference to the Fiscal Measures contained therein which was presented by theHonourable Prime Minister and Minister of Finance, Mr Patrick Manning on Friday,October 8, 2004.

PricewaterhouseCoopers 2

2005 Budget Memorandum

Table of Contents

Senior Partner’s Message

Executive Commentary

Snapshot of 2004 Fiscal Performance

Summary of 2005 Fiscal Measures

Detailed Measures

- Corporation Tax- Business Levy- Green Fund Levy- Withholding Tax- Income Tax- Value Added Tax- Petroleum Tax- Miscellaneous Provisions

Commentary by Sector

- Energy- Financial Services- Manufacturing- Construction- Agriculture- Tourism- Technology

Appendices

1. Fiscal Revenue and Expenditures2. 2004 Budget Deliverables - Delivered or Not ?3. Tax Facts4. Computations

Website: http://www.tttax.com

PricewaterhouseCoopers 3

2005 Budget Memorandum

Senior Partner’s MessageIt gives me great pleasure to communicate to you for the first time as Senior Partner.

As outlined by the Honourable Prime Minister Patrick Manning as part of the 2020 vision, “Trinidadand Tobago will be a society of creative thinkers, innovators and entrepreneurs engaged in a process oflifelong learning. All citizens will be given equal opportunity for personal growth, self-expression andactive participation in their own development. We will be a society that will look after our elderly andour less fortunate. In the society of 2020, poverty and unemployment will have been significantlyreduced to minimal levels, if not eliminated.”

That said, 2003/4 has been a period of anxiety where despite record energy prices the challenges facingthe country have been in stark focus.

Violent crime and kidnapping have been a major concern to us all. This focuses our attention onthe inadequate performance of the protective services and the legal system. We need long termsolutions that improve the quality and status of these services.

Despite high oil prices it appears government does not have a massive surplus. For many yearswe have been promised fiscal reform, especially in the Energy Sector but we have yet to see it.

The government’s focus on large projects (e.g. aluminium smelters and petrochemical plants) hasto some extent been at the expense of essential infrastructure. Education, health care and thetransportation network need significant investment.

We already have a favourable investment tax regime i.e. no estate duty, no capital gains tax, notax on interest or dividends and 30% income tax and corporation tax. There really is little scopefor further tax reductions while there are shortcomings in basic services and infrastructure.

In these circumstances the budget speech was not expected to produce major surprises and we had notanticipated tax reductions. Education, housing, health care, security and the transportation networkreceived considerable attention and it is hoped that the proposed actions will have the desired effect.

On a more positive note the economic indicators for Trinidad and Tobago remain strong and I continueto be optimistic about our future prospects. I look forward to the upcoming year with a sense ofanticipation both for the Country and for PricewaterhouseCoopers as we continue to serve the needs ofour clients.

I must take this opportunity to thank our dedicated tax staff for their outstanding effort in making thisreview available to clients only hours after the budget. I also thank the support staff who deal withprinting and delivering outside normal business hours with a quiet efficiency that we take for granted.

Should you have any queries about this memorandum and tax issues in general do not hesitate tocontact one of our two tax partners Peter Inglefield and Allyson West, or any of the senior staff listed atthe end of this review.

Graham L MitchellSenior Partner

PricewaterhouseCoopers 4

2005 Budget Memorandum

Executive Commentary

2005 Executive Overview

“Vision 2020: Ensuring Our Future Survival”

The Honourable Prime Minister and Minister of Finance introduced the theme of his 2005Budget presentation noting that his Government’s “unwavering focus” was on the attainmentof the 2020 Vision and that consistent with that focus the budget represented another buildingblock towards the social and economic development of Trinidad and Tobago.

He made it clear that the objectives were not short-term but were an integral part of hisGovernment’s long term vision and were “attainable over the next few years”.

The three pillars of economic strategy identified were:

1. Maximising returns for the energy sector;

2. Diversification of the economy to reduce dependence on the energy sector;

3. Ensuring that the benefits of economic growth and development are shared by all sectionsof the population.

These pillars have been identified as critical to the future of Trinidad and Tobago for as long asone can remember. The Honourable Prime Minister has gone one step further to identify thestrategy to be employed. In this regard we note with particular concern the Honourable PrimeMinister’s pronouncements with regard to the Energy Sector:- Government intends to raise its tax-take from the sector.

There is however a strong (and learned) school of thought which maintains that the tax-take is already at the higher end of the global scale. Great care must be taken so as not todis-incentivise the sector;

Government intends to review and re-negotiate all existing Production Sharing Contracts(PSCs). A very positive feature of the Trinidad and Tobago investment landscape has beenGovernment’s adherence to the sanctity of contracts. This rather casual reference to the re-negotiation of the PSCs will thus be received with shock by some and could doimmeasurable harm to our international reputation.

PricewaterhouseCoopers 5

2005 Budget Memorandum

Government intends to increase its participation in the natural gas value chain by(presumably) pursuing investments in shipping, re-gasification terminals and pipelinesystems.

The business risks associated with such investments must be substantial and notsurprisingly major players in the sector are seldom found to participate in all segments ofthis value chain. Government should move very cautiously in this area.

Government intends to review the tax liability of the oil companies over the last six (6)years as provided for in the current tax law.

This is a potentially dangerous precedent insofar as the Board of Inland Revenue is astatutory body that should and must act independently of any political interference.Furthermore it is an unwritten policy of the Board that the tax returns of these companiesare in fact audited on an annual basis to ensure that they are fully compliant with the taxlaws currently in force.

In formulating his 2005 Budget the Honourable Minister was in the fortunate position ofmanaging an economy that in his own words was “in excellent health”. Whether or not thisresulted from his “enlightened economic management” or the near fact that God is indeed aTrinbagonian is not yet clear. Nonetheless all indicators are noted to be very positive:-

Growth - consistent increases over the past 10 years;

Inflation – under control at below 4 percent (The rate for food prices is over 10% for 2004);

Unemployment – down to the lowest rate since 1956 at 7.8% (Is this due in part to CEPEP ortruly long term employment opportunities?);

Trade Surplus – US$1.6 billion recorded in 2003;

External Reserves – US$2.7 billion;

Estimated Budget Surplus - $437.1 million after transferring $1.263 billion to the RevenueStabilisation Fund;

External Debt – declined from 16.2% to 13.8% of GDP;

Oil Price – at record high levels giving rise to $6.916 billion of petroleum revenues (or 1/3 oftotal revenue).

PricewaterhouseCoopers 6

2005 Budget Memorandum

It is therefore not surprising that the Honourable Prime Minister was able to deliver aMarathon (almost) three hour presentation during which he outlined the extensive array ofplans and programmes that are intended to take Trinidad and Tobago further down the roadtowards developed country status. Few would challenge the Honourable Prime Minister on theareas that have been identified as integral to that objective, including:

Energy Sector growth;

Manufacturing Sector expansion;

Renewed emphasis on the Tourism Sector;

Another commitment to development of the Agricultural Sector;

Financial Sector to become the Pan Caribbean Financial Centre;

Wallerfield Industrial Park development for Information Technology.

What was absent however were the specific measures that are to be taken to bring about thedevelopment/expansion of those sectors on which our future well being, post oil and naturalgas, will be based.

There has been much heralded and promised in the past but the delivery of the promiseremains the challenge.

The Honourable Prime Minister proceeded to identify the many other areas that Governmenthad identified as critical to the attainment of its vision. These areas were:-

Investment in Human Capital: which included the construction of child care centres, newsecondary schools and the expansion of the University of Trinidad and Tobago all gearedto achieve a participation rate in post secondary and tertiary education of 60% by 2015.

Health Care: which includes construction and upgrade of several new facilities and therecruitment and training of medical personnel;

Infrastructure Development: which includes a comprehensive review of the sea, air andland transportation needs of the country along with the proposed construction of a roadsnetwork linking all parts of Trinidad.

National Security: which includes a wide ranging series of initiatives with newlegislation, new facilities, improved manpower and technology being earmarked as thetools that will be provided to curb the “unprecedented” level of criminal activity”.

PricewaterhouseCoopers 7

2005 Budget Memorandum

In the area of the Social Agenda the Honourable Prime Minister identified the provision ofhousing as the principal initiative in ensuring the social progress of the population. He notedthat Government intends to construct on average 10,000 homes per year over the next tenyears. He also noted that the squatter regularization programme was continuing.In outlining the Government’s Social Programmes for 2005 the Honourable Prime Ministerpointed out that in the last year $2.7 billion had been spent on its Social Programmes whichincluded developmental programmes; remedial programmes; and preventive programmes.

He noted that special emphasis was placed on eradicating poverty and inequality ofopportunities, increasing investments in human and social capital and promoting socialinclusion. References to several programmes and initiatives were made and only time will tellas to how successful these will be but details were sparse as to the mechanisms to beemployed.

In the short term measures were announced geared towards easing the plight of the poor andneedy in the form of increased financial assistance, increased pensions for public servants,reduction in import surcharge and CET on some essential foodstuffs (ie. chicken parts,powdered milk, split peas and cheese). Certain products were also zero rated for VATpurposes.

The above measures are certainly to be commended and hopefully will be extended in thefuture. The Honourable Prime Minister also made it clear that he EXPECTED to see areduction in poultry prices and threatened further action if these did not materialize.

Not to be overlooked is the proposed increase in the minimum wage from $8.00 to $9.00 perhour with effect from January 1, 2005. This modest increase will certainly find favour with theprivate sector which may have had reason to be fearful of a far more dramatic increase.The Honourable Prime Minister has identified three (3) important areas of reform that are on-going namely in the areas of:

Pensions Non-Energy Tax Regime Local Government

These are all important elements of the overall development plan but the process is notexpected to be a “quick- fix”, as evidenced by the fact that these exercises have already been inprogress for some time. We can only await the outcome.

Tobago is continuing to receive substantial support from the Central Government as efforts aremade to ensure that it “catches up” with the rest of the country. Substantial allocations havebeen provided in excess of $1.0 billion to finance its programmes with the principal focusbeing its tourism sector.

PricewaterhouseCoopers 8

2005 Budget Memorandum

Of significant importance to the national community is Government’s commitment to goodgovernance which is reflected in its plans to enhance:

- transparency;

- accountability;

- highest level of efficiency andeffectiveness;

- equity; and

- adherence to the rule of law.

Three specific areas were identified which included the formalization of the revenuestabilization fund with a quarterly public report being produced; the reform of Government’sprocurement process and the State Enterprise Sector. These initiatives will undoubtedly bewell received but as usual there will remain a high level of skepticism until government showsby its actions that it is committed to such reforms.

Having outlined the various policies and programmes the Honourable Prime Ministerproceeded to detail his fiscal measures for 2005, the details of which are provided later in thisMemorandum. Little was made of the mixed signals previously received regarding the“windfall revenues” or lack thereof from the petroleum sector albeit a not insubstantial surpluswas achieved in 2004 and a healthy $1.3 billion transferred to the Revenue Stabilisation Fund.The 2005 revenue estimate is being based on a US$32.80 barrel of crude but a moreconservative price of US$25 per barrel has been used for the expenditure budget. The latterapproach is to be commended as Government strives to maintain the fiscal discipline to whichit subscribes.

The focus of the 2005 budget is undoubtedly the long term development of the country as awhole and few would challenge the Honourable Prime Minister on the areas that have beenidentified as critical to the future of Trinidad and Tobago. The challenge however remains inthe implementation and delivery on the promises. The programme outlined by the HonourablePrime Minister will demand a level of management and control that would ‘tax’ even the bestand brightest in the private sector. We can but lend our support and wish him well. Our wellbeing and the well being of future generations of Trinidad and Tobago depend on him and hisGovernment.

PricewaterhouseCoopers 9

2005 Budget Memorandum

Snapshot of 2004 Fiscal Performance

$m $m $m

Estimate 2004Revised Estimate

2004 VarianceRevenue

The government’s revenue for the period included taxes from the following sources

Tax on Income/ProfitsPetroleum Companies 4,962.6 5,405.9 443.3Income Tax excluding Oil Companies 5,072.1 5,945.1 873.0Value Added Tax 2,754.7 2,864.0 109.3Taxes on International Trade 1,001.9 1,158.6 156.7

Expenditure

Recurrent Expenditure 17,623 18,478 (885)

Government’s recurrent expenditure program included spending in the following categories:

Personnel Expenditure 4,923.3 4,466.5 456.8Goods and Services 2,354.0 2,131.1 222.9Minor Equipment 171.1 93.4 77.7Current Transfers and Subsidies 4,830.5 6,701.2 (1,870.7)Transfers to Statutory Bodies 2,166.6 2,219.6 (53)Acquisition of Physical Assets 0.0 23.6 (23.6)

Government’s capital program included the following areas of expenditure :

Development Program 1,677.5 1,691.5 (14.0)Capital Repayment & Sinking FundContributions 3,226.6 2,353.0 873.6Interest and Other Debt Charges 2,612.0 2,374.6 237.4

Government’s expenditure priorities were reflected in the allocation to the following ministries:

Ministry of Education 2,491.1 2,134.6 356.5Ministry of Health 1,441.9 1,420.4 21.5Ministry of National Security 1,816.5 1,763.0 53.5

Source: Draft estimates of Revenue and Expenditure for 2005

PricewaterhouseCoopers 10

2005 Budget Memorandum

Summary of 2005 FiscalMeasures

1. Revenues

Total revenues are budgeted at $24,015.5Mcomprising petroleum revenues of$9,580.5M, taxes on non-petroleum incomeof $6,112.4M, VAT of $3,045M and taxeson international trade of $1,200.4M.

2. Expenditure

Central Government expenditure isbudgeted at $27,917.9M of which$20,769.4M will be provided by way of theAppropriation Bill, $6,798.4M will be adirect charge on the Consolidated Fund,$300M will come from the UnemploymentLevy Fund and $50M from the RoadImprovement Fund.

3. Oil Price and Stablisation Fund

While the revenue estimates are based onan average oil price of US$32.80 per barrel(Galeota mix) and a netback gas price ofUS$1.50 per cubic foot, the expenditureprogramme is based on a price of US$25per barrel. Any difference realized betweenthe two prices will be transferred to theRevenue Stablisation Fund.

4. Relief to Pensioners and PublicAssistance Recipients

There are proposed increases as follows:

a) maximum old age pension to beincreased from $1,000 to $1,150 permonth;

b) public assistance to be increased by$150 per month;

c) disability assistance grants to beincreased from $650 to $800 permonth;

all with effect from October 1, 2004.

5. Food Price Reduction Measures

These are as follows:

a) the surcharge on imported chickenand turkey is to be reduced from 86%to 40%;

b) the common external tariff onimported powdered milk, split peas,black eye beans and cheese is to beremoved;

c) Brown sugar, cocoa powder, coffee,mauby and orange juice are to bezero-rated.

6. Food Distribution

The SHARE Programme is to be expandedto provide an additional 5,000 foodhampers per month at an increased value of$250 per hamper up from $15,000 hampersat $200 per hamper.

PricewaterhouseCoopers 11

2005 Budget Memorandum

7. Relief to Low Income Wage Earners

The minimum wage is to be increased from$8 - $9.00 per hour and registered smallbusinesses will enjoy relief from businesslevy.

8. Increase in the Personal Allowance

Persons earning up to $30,000 per annumwill be granted an increased personalallowance of $30,000 rather than the$25,000 to which they are now entitled.Persons earning in excess of $30,000 perannum will lose a dollar of this additional$5,000 allowance for every dollar they earnin excess of $30,000.

9. Public Service Pensions

These pensions will be increased effectiveOctober 2004 as follows:

a) Public Service officers who retiredby December 1984 will receive anex gratia payment of $400 permonth;

b) Public Service officers who retiredbetween 1985 and 1994 will receivean ex gratia payment of $300 permonth;

c) Public Service officers who retiredbetween 1995 and 1999 will receivean ex gratia payment of $150 permonth;

d) Widows of public service officerswill receive an ex gratia payment of$150 per month.

10. Duty Free Allowance

The Duty Free Allowance from customsduty in respect of personal items importedby a traveller will be increased from $1,200to $3,000 per annum.

11. Set Off of Losses

Individuals will no longer be able to offsetagainst their income from employment,office or profession losses incurred fromother sources of income such as propertyrental.

12. Taxation of Benefits in Kind

Employees of educational and charitableinstitutions and companies not carrying ona trade will no longer be able to enjoy relieffrom tax on benefits in kind earned inrespect of their employment.

13. One Year Deeds of Covenant

The Act is to be amended to regularize thepractice of allowing companies to claim adeduction in respect of a one-time donationmade to an approved charitable institution.

14. Stamp Duty Waiver

The power to waive stamp duty, which nowresides with the Minister of Finance, willbe conferred on the Board of InlandRevenue.

15. Sports Allowance for PetroleumCompanies

Petroleum companies will be allowed toclaim the 150% allowance in respect ofcontributions made to sporting activitiesand sportsmen.

PricewaterhouseCoopers 12

2005 Budget Memorandum

Detailed MeasuresThe only fiscal measure of significancewhich was expected to be addressed in theBudget Statement for 2005 was a revisionof the petroleum tax regime to give effectto the Government’s stated desire to reviewand modernize the tax system to reflect thesignificant changes that have taken place inthe energy industry since 1992 when thelast comprehensive review and revisionwas undertaken. It was also expected thatsignificant amendments would have beenintroduced to address the issue of taxrevenues from the rapidly expandingnatural gas industry. However, those muchanticipated amendments were notforthcoming in the Statement delivered bythe Honourable Prime Minister. To itscredit the Government acknowledged thesignificance of this proposed reform andthe need to take the time required to consultwith the stakeholders and to get it right.

Instead the Budget contained a mishmashof relatively minor amendments with atwo-fold objective

promoting one of the Government’smain goals of poverty reduction and

closing some existing loopholes in thetax legislation.

We have outlined below the proposedmeasures as well as a couple of areas thatwarranted attention.

Corporation Tax

The corporation tax regime was left largelyuntouched which means that once again wego into a new fiscal year with a two-tieredcorporation tax rate, one for petroleumrelated companies not caught by thePetroleum Taxes Act and one for othercompanies. This certainly is not conduciveto the simplicity of the tax regime to whichthe Honourable Prime Minister referred.However, it is hoped that this issue, whichwas clearly intended to be a short-termstop-gap measure, will be addressed duringthe course of the next fiscal year as part ofthe review of the taxation of the energysector.

Measure

The Corporation Tax Act is to be amendedto regularize the existing practice ofallowing companies to claim deductions forcontributions made under a one-year deedof covenant to an approved charitableinstitution or sporting body.

Commentary

The Act currently allows a companymaking an annuity or other annual paymentunder a deed of covenant or othersettlement to an approved charitableinstitution or sporting body to deduct thatpayment up to a maximum of 15% of theCompany’s total income in arriving at itschargeable profits. The term annuity orannual payment connotes an event thatoccurs over the course of years and as suchdoes not contemplate or sanction adeduction in respect of a singlecontribution.

PricewaterhouseCoopers 13

2005 Budget Memorandum

The section of the Income Tax Act whichpreviously allowed such a deduction wasdeleted when the Act was changed to denyindividuals a deduction of contributionswhich they made to charity. Theamendment is merely to allow companies adeduction of a one-time payment to anapproved charity or sporting body.

Business Levy

Measure

The Business Levy provisions are to beamended to exempt registered smallbusinesses from the payment of the levy.

Commentary

This measure is an amendment intended togive relief to small businesses likely to beadversely affected by the proposed increasein the minimum wage from $8.00 to $9.00per hour. Understandably, in an effort tosimplify the administration of this relief itis to be limited to small businesses dulyregistered (presumably with theDevelopment Company Limited) whichundoubtedly many of our small businessesare not. While this measure may lead someof those businesses to seek registration,many more of them, along with their largercounterparts, are likely to seek to flout theminimum wage legislation which requiresgreater policing.

Green Fund Levy

No amendments are proposed to the GreenFund Levy provisions which once againleaves the following issues unresolved:

The equity of a single rate for thelevy when some industriesobviously contribute significantlymore than others to the destructionbeing wrought on the environment.

The applicability of the levy tocapital receipts;

The multiple taxation effect of thelevy on dividends in a multi-tieredcorporate structure.

Withholding Tax

This tax, which is a charge on non-residents earning income in T&T, remainsunchanged and continues to apply at thestandard rates of 10% & 15% on dividendsand 20% on other payments such as interestand fees.

Income Tax

Few changes were made to the Income TaxAct and with the exception of the onemeasure introduced to promoteGovernment’s stated objective of povertyalleviation, the measures announced aremainly aimed at addressing what have beenreferred to as loopholes in the legislation.

Measure

The personal allowance is to be increasedby $5,000 from $25,000 to $30,000 for aresident individual whose gross incomedoes not exceed $30,000 per annum. For aresident individual with gross income inexcess of $30,000, the $5,000 increase inthe allowance is reduced by $1.00 for every$1.00 of income in excess.

PricewaterhouseCoopers 14

2005 Budget Memorandum

As such this $5,000 increase will providefull relief to persons earning between$25,000 and $30,000, and partial relief on areducing basis to persons earning between$30,000 and $35,000 per annum. Personsearning $35,000 or more will continue tobe entitled to the $25,000 allowance whichnow applies.

Commentary

While this will provide much needed reliefto low income earners, it certainly iscontrary to the Government’s statedobjective of promoting simplicity in the taxsystem. The same objective could havebeen achieved while maintaining simplicityif the personal allowance for persons under60 years of age was increased by $5,000 to$30,000 although this would also haveresulted in conferring a benefit on middleand higher income earners.

Measure

The Act is to be amended to preventindividuals from offsetting against theirincome from employment or professionlosses from any other source.

Commentary

As the Act is currently drafted individualsare not allowed to offset gains fromemployment or profession against lossesfrom any trade or business includingagriculture, farming or fishing. However, ifan individual incurs a loss in respect of anyother income earning activity, such asproperty rental, he is allowed to offset thatloss against his income from employment,office or profession and thereby reduce thetax that he would otherwise pay on thatincome.

The benefit would have been enjoyed forexample by those persons who acquiredproperty during 1992 and 1997 whichqualified for exemption under the Act butin respect of which those individualscontinued to be entitled to deduct theirexpenses for tax purposes. All of thoseexpenses were allowed to be offset againstthe income earned by these individualsfrom their employment or profession. Itseems that once again an attempt is beingmade to close the stable door after thehorse has bolted.

It should also be noted that no suchrestriction in respect of the offset of lossesapplies to a company and as such a personearning professional fees as well as rentalincome as an individual will be at an unfairadvantage vis a vis a person earning theidentical forms of income through acompany.

Measure

The Act is to be amended to delete thoseprovisions that relieve employees ofschools and other educational institutions,charitable institutions and other companiesnot carrying on a trade from tax on theirbenefits in kind from employment.

Commentary

The Income Tax Act taxes not only salaryand other remuneration earned by anemployee or the holder of an office, butalso brings into the charge benefits in kindreceived by an employee or director. Thosebenefits in kind include the value of amotor vehicle or other asset made availableto the employee or director for his privateuse, residential accommodation provided

PricewaterhouseCoopers 15

2005 Budget Memorandum

for him or any expense incurred to providehim with a benefit. However, as currentlydrafted the provisions extending the chargeto tax on employees to the benefits in kindreceived from their employers do not applyto employees of schools, charities and othernon-trade companies. This exclusion is tobe removed to render those persons taxableon their benefits. It should be noted thatwhile the Honourable Prime Minister statedrather dismissively that there exist “nojustification for this exemption” it is clearthat contrary to the above there clearly wasa sound rational for this provision that thathas been in effect for over forty years.Whether recognised or not this provisionwill affect persons such as priests and otherreligious personnel many of whom receivesmall stipends, but who are generallyhoused and sometimes provided withtransportation.

Value Added Tax

In keeping with its stated objective ofpoverty relief, the Government proposes tointroduce measures to reduce the cost ofcertain food items.

Measure

With immediate effect, the following goodsare to be zero-rated:

Brown sugar Cocoa powder Coffee Mauby Orange juice

Commentary

This is a further erosion of the once verybroad-based VAT regime and again goesagainst the stated intention of promotingsimplicity in the tax regime. However, theobjective is laudable and should certainlybe welcome especially by the lower incomeearners who have been suffering the effectsof rapidly rising food prices. However, itbegs the question why orange juice and notall juices, especially since some childrenand adults cannot drink the former.

Petroleum Tax

We continue to await the long promisedrevision of the taxes in this sector which wecontinue to hope will be preceded andinfluenced by meaningful discussion withthe stakeholders. In the interim the onemeasure introduced appears to be anattempt to address an oversight in the lastBudget presentation.

Measure

The 150% sporting allowance currentlyavailable to all companies, other thanpetroleum companies, that make acontribution to a sporting activity orsportsman, will be extended to companiestaxable under the Petroleum Taxes Act.

Commentary

This is a welcome amendment since thereseemed no logical reason to excludepetroleum companies, which often makesignificant contributions to thedevelopment of sport locally, fromenjoyment of this relief.

PricewaterhouseCoopers 16

2005 Budget Memorandum

Miscellaneous Provisions

Measure

The Common External Tariff is to beremoved from powdered milk, split peas,black eye beans and cheese.

Commentary

It expected that this will result in areduction in the price of these items whichare all seen to be basic food items.

Measure

The duty free allowance from customs dutyon personal items imported into the countrywill be increased from $1,200 to $3,000 perannum.

Commentary

This is a welcome increase in an allowancewhich has remained unchanged for yearsnotwithstanding the several devaluationsand subsequently floating of the T&Tcurrency not to mention the impact ofinflation on the value of money.

Measure

The Board of Inland Revenue is to be giventhe power to waive stamp duty penalties.

Commentary

This is a sensible approach to theadministration of this relief which iscurrently only available through anapplication to the Minister.

PricewaterhouseCoopers 17

2005 Budget Memorandum

Commentary by Sector

Energy

As in previous years the energy sectorcontinues to be the “engine of growth”.The 2005 revenue estimate is based on anaverage oil price of US$32.80 per barrel“Galeota Mix” along with a netback gasprice of US$1.50 per cubic foot while theexpenditure is based on an oil-planningprice of US$25 per barrel with a netbackgas price of US$1.50 per cubic foot.

The Honourable Prime Minister – MrPatrick Manning identified the first pillarfor our economic strategy as being directedtowards maximising returns from theenergy sector, through increasing ourparticipation in the value chain and raisingGovernment’s tax take in a manner that isconsistent with promoting a high level ofinvestment in the sector.

The continued development of this sector istherefore critical to the attainment ofdeveloped country status.

The plan outlined in the budget to leveragethe energy sector to create conditions forsustainable growth and development are:-

To attract investment in explorationactivities so as to increase hydrocarbonreserves;

To increase the value added from ournatural gas production capacity whichinvolves participation at every stage ofthe value chain including shipping,regasification terminals, the pipelinesystem and even the market place; and

To increase the revenue take throughthe introduction of a new energy taxregime for oil and gas.

In addition to the above the Governmenthas employed a sustained policy ofattracting foreign investment to explore andincrease hydrocarbon reserves, as well as,continued its policy of diversification byencouraging a deepening and broadening ofthe domestic gas processing industry.

New petrochemical plants namely CNC IIAmmonia and Atlas Methanol came onstream. M5 methanol is scheduled forcompletion in June 2005.

Steps are being taken to construct anethylene petrochemical complex with aminimum of four plants and a gas refinerycomplex comprising five plants.

The focus is no longer on first stageprocessing in the natural gas industry butinstead promoting second stage processingof petrochemicals. To this end thefollowing are worth noting:-

NEC and ALCOA signed a MOU forthe construction of an aluminiumsmelter including and anode plant andassociated facilities.

The construction of the aluminiumsmelter is predicated on the sourcing ofalumina from both Jamaica andSuriname.

PricewaterhouseCoopers 18

2005 Budget Memorandum

The project has implications for theexpansion of intra Caribbean businessactivity as it is anticipated that it willgenerate trade in the order of US200m on ayearly basis.

Other projects include:-

The expansion of the local iron andsteel industry;

Refinery upgrade programme atPetrotrin;

Gas to liquids plant;

Caribbean Gas Pipeline.

In the 2004 budget the Minister indicatedthat given the changing internationalpetroleum environment, Government willseek a revision of the existing oil and gastaxation regime and that was expected tocome into effect on January 1, 2004. Todate there has been no change and theMinister indicated that discussions havealready begun with the oil producingcompanies.

Given the highly complex and technicalissues that need to be resolved it isanticipated that these discussions will takeupwards of six (6) months before the newregime is hammered out. Past experiencesuggests that this process could takeconsiderably longer but we wouldnonetheless urge Government to ensure thatadequate time is provided for meaningfulconsultation with stakeholders.In the interim it is proposed to:-

Review and renegotiate all existingProduction Sharing Contracts (PSC’s);

Re-activate the Petroleum Crude OilPricing Committee;

Monitor export of crude on adestination basis;

Review the tax liability of the oilcompanies over the last six (6) years asprovided for in the current laws.

What does this mean for operators ofexisting PSC’s? Will they find that thereare suddenly new terms and conditionsimposed upon them?

Onshore producers will be disappointed atthe fact that no relief has been provided inthis Budget as they are currently operatingunder very marginal conditions.

What about those producers of crude oiland natural gas who are currently operatingunder an Exploration and ProductionLicence or as a sub-licencee? Will they befaced with an additional tax burden by theimposition of new taxes or higher rates ofPetroleum Profits Tax and SupplementalPetroleum Tax or even increased royalties?

Trinidad and Tobago continues to betargeted as a high priority market for the oiland gas sector.

A high level of investment exists now andmore is expected in the future as large gasreserves and favourable economic andsocio political factors make it attractive forlong term investment.

Will the new petroleum tax regime serve asa disincentive to such investment?

PricewaterhouseCoopers 19

2005 Budget Memorandum

No doubt these are questions that have beenraised over the last year and will continueto occupy the minds of these companies asthe Government seeks to revise the existingregime.

Financial Services

The strides being made by the FinancialServices sector mirrors the strongperformance of the Trinidad and Tobago(T&T) economy as a whole with all the keyindicators showing consistent economicgrowth, a deceleration in the inflation rate,balance of payments surpluses in 2004,gross reserves which now coverapproximately five and a half monthsimports and an upgrade in the credit ratingof the T&T long-term local currency fromA- to A, short-term local currency from A-2 to A-1 and long-term foreign currencyfrom BBB to BBB+ by Standard andPoor’s in June 2004.

The Trinidad and Tobago financial servicessector underwrote bond issues for regionalgovernments in excess of US$500 millionwhile its investment in the region amountedto US$250 million. The sector nowaccounts for 12.5% of T&T’s GrossDomestic Product and employs 7.5% of thelabour force.

Banking Sector

While the economy is out-performing theexpectations of even its greatest skeptics,the issue now is whether the financialservices sector can proficiently play therole of the ‘batsman at the non-striker’send’ as the energy sector plays its muchneeded knock.

This is critical if the country is to achievethe goal of becoming a developed nation bythe year 2020 as articulated in theGovernment’s vision. Proposedamendments to the Venture Capital Act andthe establishment of a Development Bankto service the requirements of the smallbusiness sector are but two of the manyareas of this sector that the Government isseeking to address.

There are a number of challenges facing theGovernment and the stakeholders in thissector which must be conquered. It islaudable that the Government hasrecognized a number of factors which arerequired to achieve its objective such as:

An integrated legislative, regulatoryand supervisory framework for theentire sector;

The application of internationalfinancial standards for transactionsand business conduct, informationdisclosure and corporate governance;

A competitive tax regime and policyfor the regulation of cross-bordertransactions;

A competition and take-over policyfor business transactions;

A system for the certification andaccreditation of individuals andcompanies with the requirementsnecessary for operating in the sector;

A framework for the identificationand assessment of the risks associatedwith capital markets in our region;

PricewaterhouseCoopers 20

2005 Budget Memorandum

A methodology for the pricing ofbonds and other instruments;

The existence of information vendors(such as credit rating agencies, riskassessment advisors, external ratingagencies);

Accurate and timely data from theCentral Statistical Office (CSO) andother government agencies;

Policy framework for operationalrisks such as the collapse of financialinstitutions, mismanagement andcorporate governance.

The sector has continued to grow bothlocally and regionally. However, with theanticipated advent of the Caricom SingleMarket and Economy (CSME) and the FreeTrade Area of the Americas (FTAA), itmust prepare for globilisation.

If our financial services sector is to becompetitive in the global market revisionsto the current T&T tax regime are critical.Such revisions may include but are notlimited to the following:

Reduction or removal of withholdingtax on interest payable by localfinancial institutions raising financingfor local industry. This should resultin cheaper financing which wouldenhance the competitive edge of thelocal institutions;

Development of tax legislation inrelation to financial products andtransactions;

Removal of financial services taxwhich is a nuisance tax both for thecustomers who bear it and for theinstitutions that are required to collectand account for it;

Tax incentives for entities seeking tosecure certification and accreditation.

The White Paper on the Reform of theFinancial System of Trinidad and Tobagoencapsulates Governments vision asfollows:-

“A Pan-Caribbean Financial Centre whichis globally competitive, well-diversified,responsive and market-driven providing thewidest possible range of financial productsand services to international and regionalbusinesses, small and large enterprises inthe public and private sector.” Theattainment of this vision is possible but itcalls for a structured and logical approachto identifying the current deficiencies andmitigating such. It is comforting to knowthat the Government, CBTT and otherstakeholders are actively seeking to put aframework in place for the achievement ofthis objective.

Insurance Sector

Supervision and Regulation

Effective May 25, 2004, all entitiesformally under the purview of theSupervisor of Insurance have been deemedto be registered under the regulatorycontrol of the Central Bank of Trinidad andTobago. The new department responsiblefor Insurance companies and Bankregulation will be called the FinancialInstitutions Supervision Departmentheaded by Mrs Catherine Kumar.

PricewaterhouseCoopers 21

2005 Budget Memorandum

In keeping with the Honourable PrimeMinister’s intention to maintain Trinidadand Tobago as the financial centre of theCaribbean the Insurance Act is to beamended in 2005.

Regional Integration in Financial Services

On the regional front the Honourable PrimeMinister did emphasise the importance ofthe Caricom market to Trinidad andTobago. In the context of insuranceservices trade integration the impact of theCSME and FTAA are likely to be slow butsteady.

The proposed changes to the Insurance Acttherefore need to take account of the verysignificant regional trade agreements thatwill eventually affect our local insuranceindustry.

General (P&C) Insurance

The financial costs associated with thecurrent hurricane season which preliminaryestimates forecast to be in excess of US$15billion will no doubt cause of many of ourTrinidad and Tobago based GeneralInsurance Companies to report significantlosses. The Honourable Prime Ministermay therefore wish to consider extendingthe amendments proposed to the tax lossrelief regime to include provisions whichwill make the existing corporate tax lossprovisions more flexible and thus beneficialto General Insurance Companies. The lackof an appropriate tax regime for thisindustry given recent events could add tothe operating costs of the industry and byextension the cost of doing business inTrinidad and Tobago and the region.

Alternatively, Trinidad and Tobago basedGeneral Insurance Business could becomeless competitive.

Life Insurance

The Honourable Prime Minister referred toproposals for a review of taxation in thenon-energy sector. There has also beensome debate from within the Life InsuranceIndustry as to the appropriateness of theexisting regime of taxation.

Any initiative to alter the basis or rate oftax of the existing regime must consider thefollowing issues: -

i. The shift in customer focus from deathbenefits, like whole life insurance toliving benefits such as annuityproducts;

ii. The current effective rate of tax on lifeproducts given the existing tax reliefs,tax deferrals, allowances anddeductions;

iii. The fundamental issue of the incidenceof taxation, i.e. who bears the actualburden of tax currently in the lifeinsurance business;

iv. The impact (whether positive ornegative) of any new tax measures onthe investment decisions ofpolicyholders and/or insurancecompanies;

v. The current and future rates of effectivetaxation on financial products whichcompete with products offerings of thelife insurance business.

PricewaterhouseCoopers 22

2005 Budget Memorandum

The very long term nature of life insuranceproducts exposes these companies to beingcharged tax on profits of products whichmay subsequently prove to be unprofitablewith its consequent negative effects.Accordingly, change in the tax regimeought to be carefully considered.

Pension Reform

Public Service Pensions

The Honourable Prime Minister’s statedintention to change the national publicservice pensions from a Pay as You Go(PAYG) system to a contributory system islaudable given the parlous state of mostsuch systems in other countries.

Moreover the need for employees of thestate to gradually take greater responsibilityfor the management of their pension affairswill help to reduce if not eliminate the“retirement rage” phenomenon currently onthe rise in many first world countries.

Corporate Pensions

Mention was also made of the intention todeal with the following issues affecting thecorporate pension sector:-

Taxation issues in the pensionindustry;

Treatment of pension fund surpluses; Minimum levels of income

maintenance in retirement; Minimum income replacement ratios; Indexation of pension benefits

all of which will help to improve corporatepension benefits.

State Pensions

The old age pension and national insuranceschemes (NIS) are to be integrated and amodernization plan formulated for the NISin particular.

Worldwide, the burden of pensionmanagement has been shifting irretrievablyfrom the state to the corporate sector, andnow finally to the individual. Thestatements made in the year’s Budgetpresentation mirror this trend.

Only time will tell whether these plans willbe transformed into concrete action.

Manufacturing

There is no disputing that T&T is theregion’s leading manufacturing nation.

Currently the sector enjoys tax reliefs invarious forms including an initialallowance (60%) on asset purchases, 150%promotional expense uplift, import dutyconcessions, tax holidays under the FiscalIncentives Act and export incentives underthe Free Zones Act.

However, the sector is facing manychallenges:-

1) Lack of investor confidence due toescalation of crime and industrialactions;

2) The anticipated saturation of both thelocal and regional markets due to theinflux into the region of products madein the US, Mexico and the Far East;

PricewaterhouseCoopers 23

2005 Budget Memorandum

3) The prospect of the Free Trade Area ofthe Americas (FTAA) and the CaricomSingle Market and Economy cominginto being.

Our manufacturers will need to divertresources into research and development(R&D) and invest in technology tofacilitate expansion and maintain theirdominance in the region.

In his Budget Speech the HonourablePrime Minister made reference to thefollowing measures intended to furtherdevelop the sector. Some are a continuationfrom the previous years as development isplanned on a phased basis:-

1) Penetrating new markets withfavourable bi-lateral tradingagreements. Some were signed in 2004(e.g. Cuba and Costa Rica) but we lookforward to tax treaties signed with LatinAmerican territories as this is GOTT’sfocus.

2) The development of the WallerfieldBusiness Park designated for lightmanufacturers and services.Infrastructure work began in 2004 andwe hope that the planned NEL/SURALjoint venture will come on stream in2005.

3) The development of the R&D fundintended to finance development inunique products. It is hoped that thiswill become a reality particularly forlight manufacturers and increasedemployment.

4) Establishment of the Ammonia andUrea plants at Union Estate, La Brea,expected to come on stream in 2008.This should lead to job-creation in themedium term.

It is of note that the inability to write-offstart up costs could be a disincentive topotential investors in light manufacturing.

T&T manufacturers may be cautiouslyoptimistic that the thrust to further developthe downstream (petrochemical) sector willserve as the catalyst to the development ofthe light manufacturing sector.

Despite their regional superiority our localmanufacturers will be forced to take stockof their circumstances and determinewhether given the economic environment itis feasible to continue operating in thesector. Several of the multi-nationalmanufacturers have already made thatdecision based on their own circumstances.

The 2005 Budget contains no measuresdesigned to give our manufacturers anylevel of comfort that their needs are beingaddressed. A simple example is theabsence of any mention of the much neededcustoms reform or improvements at theports of entry.

Maybe we as consumers also have a part toplay to ensure the survival of the sector bychanging our focus and buying locallymanufactured products.

PricewaterhouseCoopers 24

2005 Budget Memorandum

Construction

In spite of the importance of theconstruction sector to the government’splans to improve the country’sinfrastructure, construct new homes andcreate a large number of jobs, no specificincentives or concessions impacting thissector were introduced. Several majorconstruction and road expansion projectswere however outlined with thegovernment being the main player.

Projects already on stream or expected tocome on stream include the new headoffice for the Customs and Excise Divisionin Port of Spain, the new wing at the SanFernando General Hospital, theScarborough Regional Hospital and theScarborough Library, the Point FortinHospital, construction and upgrade ofprimary and secondary schools as well asEarly Childhood Care and EducationCentres, Expansion of the Crown PointAirport Terminal, the National OncologyCentre at Mt Hope and District HealthFacilities.

The government’s stated housing policy ofconstructing 100,000 houses over a ten yearperiod has also impacted the industry withseveral projects having been completed andseveral others being underway. This policywill involve heavy private sectorinvestment as well as funding frominternational funding agencies like theIADB.

Road expansion projects have also beenunder highlighted including the extensionof the Churchill-Roosevelt Highway, DiegoMartin Highway, construction of a SanFernando-Point Fortin Highway and thelong overdue Interchange at the ButlerIntersection.

The industry has also been kept afloat bymajor projects in the energy sector whereworld scale plants have been constructed totake advantage of increased natural gasreserve finds. There is therefore muchanticipation regarding the future prospectsby the players in this industry that providesa livelihood for approximately 80,000persons.

The sector is a significant player in theattainment of the government’s target ofcreating a large number of new jobs. In thatregard some specific measures are requiredto provide the skilled personnel required bythe sector and also to provide the necessaryimpetus including:-

Simplification of the process forapproval of ApprenticeshipProgrammes qualifying for tax relief;

Removal of Stamp Duty for first timehome owners;

Incentives to lending institutionsgranting loans for construction projects;

Simplification of the approval processfor houses converted to ApprovedGuest Houses and thereby qualifyingfor tax relief.

Agriculture

Agriculture is in transition.

As expected the agricultural sector hasdeclined by over 10%, a direct result ofGovernment shutdown of Caroni (1975)last year and the displacing of 9000workers.

PricewaterhouseCoopers 25

2005 Budget Memorandum

The government restructuring of Caroni(1975) Ltd and the agricultural sector as awhole include the following:-

the stimulation of economic activitieson lands which were no longer undersugar cultivation ; and

the preparation of the displacedworkers for the new environment ofwork which involves retraining andretooling of employees to takeadvantage of opportunities especiallythose emerging in the manufacturingindustry.

To this end the government has announcedthe following initiatives:-

making more lands and the necessaryinfrastructure available for agriculturalproduction;

youth training in farm management,production, marketing , post harvestmanagement and food processing;

increasing access to agricultural creditand protection for domestic producersthrough the CET and increased importsurcharges;

implementing a food packaging andwarehousing facility for the effectivepreservation of food products;

introducing of the National AgricultureInformation System;

developing and enforcing grades andstandards to international standards;and

promoting fish production byintroducing sustainable managementtechniques for renewable marine andinland fisheries.

While these are all laudable goals thegovernment must seriously also considerreintroducing tax incentives for the sector.

Agriculture provides an important avenuefor diversification, employment and selfreliance and must be given the support itrequires to achieve these objectives whichmust be seen as integral to the 20/20Vision.

Tourism

The Honourable Prime Minister in his 2005Budget presentation has again identifiedTourism as a high potential sector for GDPgrowth and featured as part of theMinister’s “3 main pillars” of GOTT’sdiversification strategy. GOTT’s focus forexpansion of the sector includes:-

1) Creation of the Tourism DevelopmentCorporation with the responsibility fortourism investment, promotion, productdevelopment and marketing.

2) Marketing T&T internationally;

3) Attraction of major hotel chains;

4) Providing for a Tourism Rolling Planspecifically for Tobago

5) Providing enhanced Human ResourceTraining and Development

PricewaterhouseCoopers 26

2005 Budget Memorandum

The Tourism Development Act, 2000provides specific incentives andconcessions for entities operating in thesector but they are faced with challenges tosatisfy cumbersome qualifying criteria inorder to take advantage of these incentivesand concessions, not to mention a poorlydrafted Act which resulted in the promisedincentives incapable of being granted.

It is interesting to note that while the sectoris earmarked for continued expansion, localprivate investment dropped from $268m to$98m in 2004 while foreign privateinvestment dropped from $53m to $37m.Based on these statistics it appears that theplanned thrust in the sector may notbecome a reality due to lack of investorconfidence.

If the passive approach to promoting thesector continues, it will be a case of toolittle, too late especially if as a nation weare to achieve our vision for 2020 ofdeveloped nation status.

Fiscal incentives that may give this sectorthe boost and encouragement it needs are:-

Ensure that our package of incentivesare ‘better that the rest’ of the region;

Simplify the regulatory frameworksuch that qualifying for tax exemptionsand allowances/deductions are easy toaccess;

Exemption or reduction in the HotelAccommodation tax for new hotels toenable them to competitively pricerooms;

Extend the business levy exemption to5 years from the commencement oftrade for qualifying tourism projects.The removal of business levy forregistered small businesses in thissector is a positive step;

Introduce a minimum income levelbefore a qualifying individual or entitybecomes taxable on income earned inthis sector;

Monitor and assist in the raising offinance for qualifying tourism projects;

Continue to protect the image of T&Twith measures intended to reduce andcontrol crime;

Guidance for the orderly developmentof the industry particularly inprotection of our eco-systems.

Technology

In this year’s Budget the Honourable PrimeMinister sharpens the focus on technologyas a means towards achieving the vision for2020.

Indeed technology features prominently inmany of the measures mentioned forimplementation. The Ministry of NationalSecurity will be provided with cutting-edge technology and an expandedCommunications Network to assist in thefight against crime.

PricewaterhouseCoopers 27

2005 Budget Memorandum

The thrust into the knowledge-basedindustries is to be strengthened by theacquisition of 3,000 computers for primaryschools, IT units in each educationaldistrict and a Wide Area Networkconnecting all schools.

The Minister also refers to ElectronicGovernment whereby all GovernmentMinistries and Departments will beconnected.

In addition a TelecommunicationsAuthority has been established to facilitatecompetition in this sector. We trust that itwill be effective in making broad bandinternet access available and affordable foreveryone.

Most significantly the development of anInformation Technology/Industrial Sectorat the Wallerfield Industrial Park isproposed. The earmarked zones of activityinclude technology and softwaredevelopment and incubation facilities. TheUniversity of Trinidad & Tobago with belocated in the park and emphasis will beplaced on its on-line distance learningcapability.

No specific tax incentives were stated inthe Budget to motivate development of thissector. However tax reliefs currentlyavailable include:-

1) 10% wear and tear allowance on theconstruction of the infrastructure;

2) 150% training allowance for training todevelop the expertise in this specialisedarea.

3) 200% employment allowance wherenew jobs are created, albeit theminimum wage has increased from $8to $9.

4) Zero-rated VAT on computingequipment;

It is hoped that these reliefs will initiatedevelopment of this “new” sector butthe expectation is that aggressiveincentives must be provided in order toattract the investment required tojumpstart this fledging industry.

PricewaterhouseCoopers 28

2005 Budget Memorandum

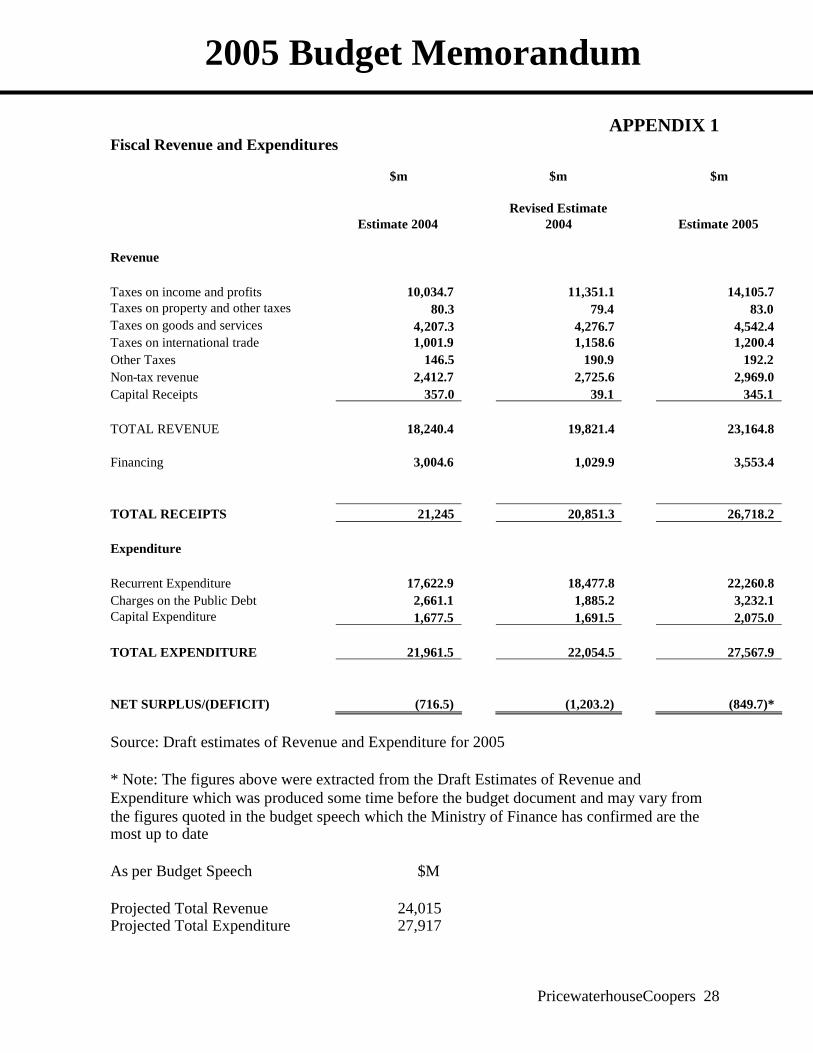

APPENDIX 1Fiscal Revenue and Expenditures

$m $m $m

Estimate 2004Revised Estimate

2004 Estimate 2005

Revenue

Taxes on income and profits 10,034.7 11,351.1 14,105.7Taxes on property and other taxes 80.3 79.4 83.0Taxes on goods and services 4,207.3 4,276.7 4,542.4Taxes on international trade 1,001.9 1,158.6 1,200.4Other Taxes 146.5 190.9 192.2Non-tax revenue 2,412.7 2,725.6 2,969.0Capital Receipts 357.0 39.1 345.1

TOTAL REVENUE 18,240.4 19,821.4 23,164.8

Financing 3,004.6 1,029.9 3,553.4

TOTAL RECEIPTS 21,245 20,851.3 26,718.2

Expenditure

Recurrent Expenditure 17,622.9 18,477.8 22,260.8Charges on the Public Debt 2,661.1 1,885.2 3,232.1Capital Expenditure 1,677.5 1,691.5 2,075.0

TOTAL EXPENDITURE 21,961.5 22,054.5 27,567.9

NET SURPLUS/(DEFICIT) (716.5) (1,203.2) (849.7)*

Source: Draft estimates of Revenue and Expenditure for 2005

* Note: The figures above were extracted from the Draft Estimates of Revenue andExpenditure which was produced some time before the budget document and may vary fromthe figures quoted in the budget speech which the Ministry of Finance has confirmed are themost up to date

As per Budget Speech $M

Projected Total Revenue 24,015Projected Total Expenditure 27,917

PricewaterhouseCoopers 29

2005 Budget Memorandum

2004/2005 BUDGETED EXPENDITURE

Expenditure Head Personnel Other DevelopmentProgramme 2005 Estimates

President 1,283,068 10,695,857 $11,978,925Auditor General 16,101,875 3,318,350 $19,420,225Judiciary 90,246,000 111,948,000 37,800,000 $239,994,000Industrial Court 12,430,000 14,988,000 510,000 $27,928,000Parliament 13,390,931 31,428,804 1,040,000 $45,859,735Service Commissions 20,616,600 23,744,645 900,000 $45,261,245Statutory Authorities' Service Commissions 2,616,600 1,401,316 $4,017,916Election & Boundaries Commission 17,838,616 16,617,917 6,700,000 $41,156,533Tax Appeal Board 2,441,400 1,767,500 $4,208,900Registration, Recognition & Certification Board 1,853,888 621,760 $2,475,648Public Service Appeal Board 970,000 255,472 $1,225,472Office of the Prime Minister 37,731,900 1,385,592,971 35,700,000 $1,459,024,871Tobago House of Assembly 822,900,000 200,000,000 $1,022,900,000Central Administrative Services, Tobago 7,760,800 3,997,490 $11,758,290Personnel Department 12,811,250 7,081,030 5,871,000 $25,763,280Ministry of Finance 215,505,021 3,537,673,763 30,420,000 $3,783,598,784Charges on Account of Public Debt 5,280,619,004 $5,280,619,004Pensions and Gratuities 1,022,761,804 $1,022,761,804Ministry of Planning and Development 38,398,455 29,194,249 28,065,000 $95,657,704Ministry of National Security 1,415,069,456 775,136,273 141,340,000 $2,331,545,729Ministry of the Attorney General 38,101,000 120,736,175 20,100,000 $178,937,175Ministry of Legal Affairs 27,110,000 46,818,500 13,490,000 $87,418,500Ministry of Agriculture, Land and Marine Resources 172,966,670 227,824,562 52,170,000 $452,961,232Ministry of Education 1,939,152,000 907,181,843 294,000,000 $3,140,333,843Ministry of Health 448,976,000 1,132,398,600 280,000,000 $1,861,374,600Ministry of Labour and Small & Micro Enterprise Deve 23,092,300 115,807,890 14,800,000 $153,700,190Ministry of Public Administration and Information 51,452,200 297,841,360 76,850,000 $426,143,560Ministry of Culture and Tourism 16,502,800 93,910,855 15,280,000 $125,693,655Ministry of Housing 5,548,500 139,054,800 161,700,000 $306,303,300Integrity Commission 1,299,600 6,046,350 3,000,000 $10,345,950Environmental Commission 1,854,500 2,418,150 $4,272,650Ministry of Public Utilities & the Environment 80,072,900 794,570,551 80,000,000 $954,643,451Ministry of Energy and Energy Industries 22,354,700 364,421,100 $386,775,800Ministry of Local Government 60,688,000 763,733,526 43,070,000 $867,491,526Ministry of Works & Transport 384,899,000 696,247,082 194,070,000 $1,275,216,082Ministry of Sport & Youth Affairs 33,769,320 129,497,592 31,980,000 $195,246,912Ministry of Foreign Affairs 74,678,400 145,052,870 12,974,000 $232,705,270Ministry of Trade & Industry 14,940,300 69,916,750 61,770,000 $146,627,050Ministry of Science, Technology & Tertiary Education 42,701,000 808,699,000 160,000,000 $1,011,400,000Ministry of Community Development & Gender Affairs 18,667,805 147,678,340 67,200,000 $233,546,145Ministry of Social Development 6,215,600 29,143,390 4,200,000 $39,558,990

GRAND TOTAL $5,372,108,455 $20,120,743,491 $2,075,000,000 $27,567,851,946

2004/2005 20% 73% 8% 100%

NATIO

Est

Incrthei

Instauto

AcqPris

Estagathtech

Ena

Acqatta

Coninfr

Esta

Impand

Intr

2004Deliv

PricewaterhouseCoopers 30

2005 Budget Memorandum

APPENDIX 2

NAL SECURITY - $1.674 B

ablish Special Crime Fighting Unit

ease police patrols and presence in the main business areas and in communities, and improver response time by

- increasing the fleet of vehicles- constructing police stations in 14 communities- recruiting 1,000 additional police officers

all police computer system to transmit voice, data and video to police vehicles, expandmated fingerprint and mugshot systems to sub-divisional headquarters

uire reporting and analytical tools, including GIS linkages to the Magistracy, High Courts,ons and other agencies

blish an Officer’s Training School to cover areas such as narcotics investigations, intelligenceering and analysis, money laundering, drug enforcement, forensic training and bomb disposalniques

ct new legislation to improve the management of the Police Service and to combat crime

uire patrol vessels, with capability to launch interceptor boats and carry a helicopter withck capability, to be operated in conjunction with an ultra-modern radar system

tinue comprehensive upgrading of Coast Guard and Defense Force facilities andastructure, and complete Global Maritime Distress and Safety System

blish a Special Security Commission to act as a Think Tank on crime prevention and detection

rove facilities at the Youth Training Centre, reconstruct Golden Grove Inmates’ Dormitorybegin construction of a new medium correctional facility for Tobago

oduce a parole system to promote rehabilitation

Budget Deliverablesered or Not ?

PricewaterhouseCoopers 31

2005 Budget Memorandum

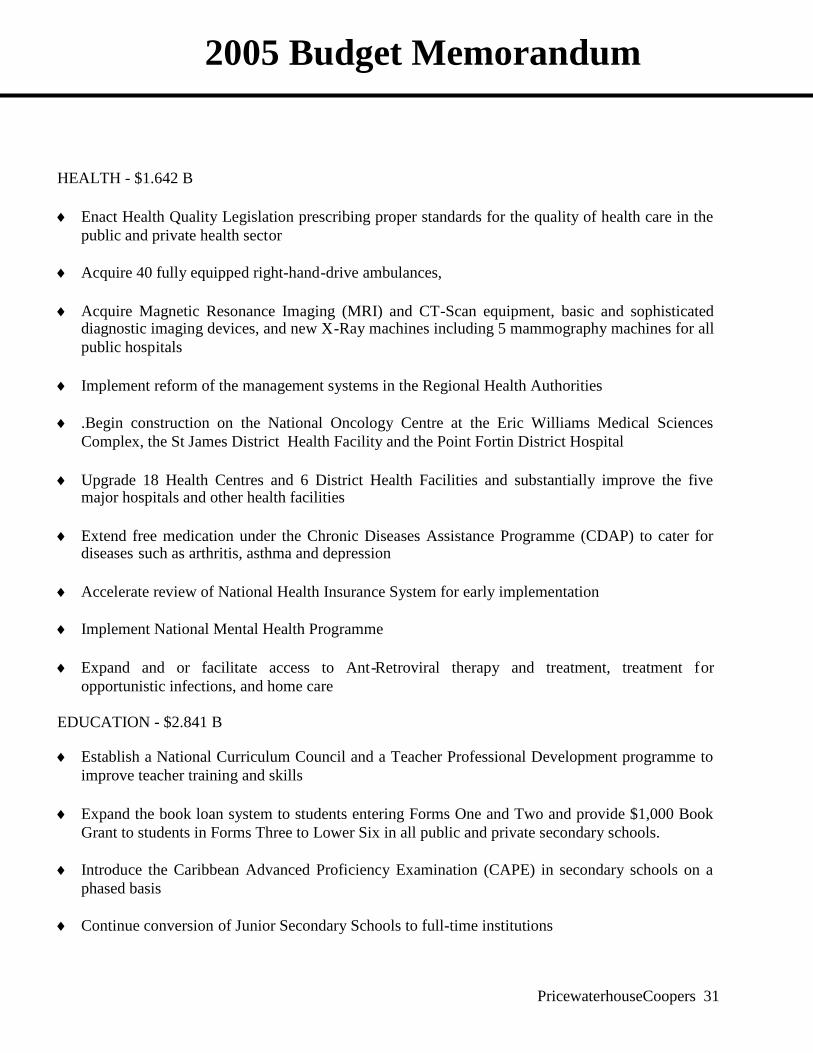

HEALTH - $1.642 B

Enact Health Quality Legislation prescribing proper standards for the quality of health care in thepublic and private health sector

Acquire 40 fully equipped right-hand-drive ambulances,

Acquire Magnetic Resonance Imaging (MRI) and CT-Scan equipment, basic and sophisticateddiagnostic imaging devices, and new X-Ray machines including 5 mammography machines for allpublic hospitals

Implement reform of the management systems in the Regional Health Authorities

.Begin construction on the National Oncology Centre at the Eric Williams Medical SciencesComplex, the St James District Health Facility and the Point Fortin District Hospital

Upgrade 18 Health Centres and 6 District Health Facilities and substantially improve the fivemajor hospitals and other health facilities

Extend free medication under the Chronic Diseases Assistance Programme (CDAP) to cater fordiseases such as arthritis, asthma and depression

Accelerate review of National Health Insurance System for early implementation

Implement National Mental Health Programme

Expand and or facilitate access to Ant-Retroviral therapy and treatment, treatment foropportunistic infections, and home care

EDUCATION - $2.841 B

Establish a National Curriculum Council and a Teacher Professional Development programme toimprove teacher training and skills

Expand the book loan system to students entering Forms One and Two and provide $1,000 BookGrant to students in Forms Three to Lower Six in all public and private secondary schools.

Introduce the Caribbean Advanced Proficiency Examination (CAPE) in secondary schools on aphased basis

Continue conversion of Junior Secondary Schools to full-time institutions

PricewaterhouseCoopers 32

2005 Budget Memorandum

Expand School Feeding Programme to provide 90,000 lunches daily and 25,000 breakfast mealsfive days a week

Expand school transport to 20,000 seats per day from PTSC and 21,500 from maxi taxis in ruralareas. Provide bus transportation for differently-abled students

Repair perimeter fences and security lighting at 28 high-risk secondary schools

Build 200 Early Childhood Care Centres over the next four years

HOUSING - $217 M

Shift the development and delivery of houses away from NHA to a new company

Introduce “rent to own” programme and develop standardized mortgage deed to facilitate andassist home ownership

Finance low cost housing by providing a subsidy of $36,000 or $24,000 to beneficiaries withspecified annual household incomes, for construction or purchase of a new house

AGRICULTURE – $448 M

Grant an initial allowance of 100 percent to be applied to capital expenditure in plant andequipment for approved agro-processing activities

Introduce tax credits and investment allowances to create a more effective fiscal regime

Develop the Agricultural Land Information System and Inventory of State Lands by updating thedatabase of 16,537 parcels of tenanted or occupied state agricultural lands and creating aninventory of privately owned and other state lands used for agriculture

Establish water management and flood control programmes at Duck Pond, Moruga, Carlsen Fieldand Depot Road

Assign agricultural leases and housing plots to former employees of Caroni (1975) Limited andseek private sector equity participation for Rum Distillers Limited

Make agricultural credit more accessible, provide appropriate crop insurance and strengthen andenforce measures aimed at combating praedial larceny

Develop the nation’s inshore and offshore fisheries resources

PricewaterhouseCoopers 33

2005 Budget Memorandum

TOBAGO Complete construction of Scarborough Hospital

Purchase a new passenger ferry to service the inter-island route

Begin the extension of the Crown Point Airport Terminal

Embark on projects such as the reconstruction of the Scarborough Library, the transportation hubin Scarborough, desilting of the Hilsborough Dam, expansion of the Scarborough jetty,construction of a new financial complex, the Roxborough Plaza and Market and of a number ofbridges and repairs to secondary roads

INFRASTRUCTURE

Extend the Churchill Roosevelt Highway to Wallerfield

Begin construction of the Mamoral Dam and Reservoir

Upgrade drainage works on the Marabella, Caroni, Cipero, Vistabella, North Oropouche rivers andthe Richplain Ravine

Undertake coastal protection works at Manzanilla/Mayaro

Begin restoration works on the President’s Residence and Office, Queen’s Royal College, HolyTrinity Cathedral and the associated Deanery, Mille Fleurs and Stollmeyer’s Castle

Reconstruct Berth 7 of the Port of Port of Spain

PricewaterhouseCoopers 34

2005 Budget Memorandum

TRANSPORTATION

Upgrade passenger accommodation at the ports of Port of Spain and Scarborough

Acquire a new navigational aid system for the Civil Aviation Authority

Implement a new Permits and Vehicle Registration Information System over the next two years

Introduce Breathalyser legislation

SOCIAL AND CULTURAL PROGRAMMES

Introduce the following new programmes

- Community Development Bursary Progamme- Geriatric Adolescent/Partnership Programme- Adolescent Mothers Programme- Community Improvement Services

PricewaterhouseCoopers 35

2005 Budget Memorandum

APPENDIX 3Tax Facts 2005

%Cumulative Tax

2005 %Cumulative Tax

2004 %Cumulative Tax

2003

1 PERSONAL INCOME TAX

TAXRATES

0-50,000 25 $12,500 25 $12,500 25 $12,500Over 50,000 30 30 30

ALLOWANCES/DEDUCTIONS

Severance Pay $100,000 $300,000 $300,000Alimony paid No limit No limit No LimitAlimony (per child) $1,200 $1,200 $1,200Personal allowance:Gross Income not exceeding $30,000Gross income $30,001-$34,999Gross income $35,000 and abovePersons over 60 years

$30,000$25,001-$29,999

$25,000$40,000

$25,000$25,000$25,000$40,000

$25,000$25,000$25,000$30,000

Mortgage interest (owner occupied)Tertiary education allowance $18,000 $18,000 $18,000Pension/Deferred AnnuityNational Insurance $12,000 $12,000 $12,000Credit Union DeductionHousing Allowance

$10,000$10,000

$10,000$10,000

$10,000$10,000

TAX CREDITS

TTMF Bonds (issued before 1.1.96) 50% of interest 50% of interest 50% of interest

2 COMPANY TAX

Corporate Tax Rate (energy related) 35.0 % 35.0 % 35.0 %Corporation Tax Rate (non-petroleum) 30.0 % 30.0 % 30.0 %Business Levy (on gross sales) 0.20 % 0.20 % 0.20 %Green Fund Levy (on gross sales) 0.10 % 0.10 % 0.10 %Small Business Tax Credit 25.0 % 25.0 % 25.0 %

3 PETROLEUM TAXES

Petroleum Profits Tax 50 % 50 % 50 %Unemployment Levy 5 % 5 % 5 %

4 INVESTMENT INCOME

Dividends received exempt exempt exemptInterest received (individuals) exempt exempt 5%Interest received (over 60’s) exempt exempt exempt

5 WITHHOLDING TAXES

Standard Rate 20 % 20 % 20 %Dividend - Parent 10 % 10 % 10 %

- Other 15 % 15 % 15 %

PricewaterhouseCoopers 36

2005 Budget Memorandum

Low Income Person I

2005 2004

Income 30,000 30,000Less:Personal Allowance 30,000 25,000

Credit Union Deduction - 3,000Pension/Annuity & NIS Contributions - 826

Taxable Income 0 1,174

Income Tax Thereon (25%) 0 293.50

Effective Tax Rate 0% 1.0%

Low Income Person II 2005

Income (Bands) 30,000 32,500 35,000

Less:Personal Allowance 30,000 27,500 25,000

Credit Union Deductions - 3,000 3,000Pension/Annuity & NISContribution - 826 826

Taxable Income 0 1,174 6,174

Income Tax Thereon (25%) - 294 1,543.50

Effective Tax Rates - 1% 4.40%

PricewaterhouseCoopers 37

2005 Budget Memorandum

CaveatThis Memorandum contains a summary ofthe main features of the proposedbudgetary measures and is intended toprovide readers with a general guidethereto. It is not intended to be acomprehensive statement of the law andshould therefore not be acted upon withoutprofessional advice.

While every effort has been made to ensurethe accuracy of information contained inthis document, no responsibility is acceptedfor any errors or omissions. No part of thispublication may be reprinted without ourprior permission.

Contacts for PricewaterhouseCoopers Ltd

Should you need further information pleasecontact:

Peter R InglefieldManaging DirectorTelephone: 1-868-623-1361, Ext 172E-mail: [email protected]

Allyson M WestDirector – Tax ServicesFSIPTelephone: 1-868-623-1361, Ext 173E-mail: [email protected]

Susan R MorganDirectorEnergy-DownstreamTax ServicesTelephone: 1-868-623-1361, Ext 174E-mail: [email protected]

Deborah Ragoonath-RajkumarSenior ManagerEnergy-UpstreamTax ServicesTelephone: 1-868-623-1361, Ext 145E-mail: [email protected]

Website: http://www.tttax.com

PricewaterhouseCoopers 38

2005 Budget Memorandum

PricewaterhouseCoopers Caribbean

Across the Caribbean, with over 80 partners and 1300 staff, PricewaterhouseCoopers providesa fully integrated range of professional services to local, regional and international clients fromoffices located in Antigua, Aruba, the Bahamas, Barbados, the Cayman Islands, Curacao,Grenada, Jamaica, the Dominican Republic, Puerto Rico, St Lucia, St Maarten , Trinidad &Tobago and the Turks & Caicos Islands.

In providing industry-focused assurance, tax and advisory services for public and privateclients, PricewaterhouseCoopers assists these clients primarily in four broad areas:corporate accountability, risk management, structuring/mergers and acquisitions, andperformance and process improvement. Our use of our networks, experience, industryknowledge and business understanding in each of these areas distinguishes the way wework – we call this “Connected Thinking”.

PricewaterhouseCoopers is a truly global organization with member firm offices in 768 citiesin 139 countries. Our primary purpose is to enhance value for our clients and theirstakeholders while setting high standards for the conduct of business and demonstratingleadership within our profession.

With unrivalled geographic coverage and human resources in the Caribbean, we seek toprovide services of consistently superior quality to all of our clients across the region.

PricewaterhouseCoopers 39

2005 Budget Memorandum

TRINIDAD & TOBAGOGraham L Mitchell – Senior PartnerPO Box 550Port-of-SpainTrinidad & Tobago

Telephone: [1] (868) 623 1361Telecopier: [1] (868) 623 6025

ARUBAEdsel N Lopez – PartnerPO Box 307Aruba

Telephone: [297] 582 1647Telecopier: [297] 582 4864

BAHAMASLenworth C Smith – Partner-in-ChargePO Box F 42682FreeportBahamas

Telephone: [1] (242) 352 8471Telecopier: [1] (242) 352 4810

CAYMAN ISLANDSChristopher D Johnson – Senior PartnerP.O. Box 258 GTGrand Cayman, BWICayman Islands

Telephone: [1] (345) 949 7000Telecopier: [1] (345) 949 7352

DOMINICAN REPUBLICFreddy Perez – PartnerPO Box 1286Santo DomingoDominican Republic

Telephone: [1] (809) 567 7741Telecopier: [1] (809) 541 1210

EASTERN CARIBBEANAntiguaCharles W A Walwyn – PartnerPO Box 1531St John'sAntigua

Telephone: [1] (268) 462 3000Telecopier: [1] (268) 462 1902

BarbadosAndrew J Marryshow – Senior PartnerPO Box 111BridgetownBarbados

Telephone: [1] (246) 431 2700Telecopier: [1] (246) 436 1275

GrenadaPO Box 124St George's, Grenada, WIGrenada

Telephone: [1] (473) 440 2127Telecopier: [1] (473) 440 4131

St LuciaAnthony D Atkinson – PartnerPO Box 195Castries, St Lucia

Telephone: [1] (758) 452 2511Telecopier: [1] (758) 452 1061

JAMAICAEverton L McDonald – Senior PartnerPO Box 372Kingston, Jamaica

Telephone: [1] (876) 922 6230Telecopier: [1] (876) 922 7581

NETHERLANDS ANTILLES

BonaireCees Rokx – PartnerKaya Isla Riba 1Kralendijk, BonaireNetherlands Antilles

Telephone: [599] (7) 17 4790Telecopier: [599] (7) 17 6592

CuracaoPeter Bolwerk – Senior PartnerPO Box 360Willemstad, CuraçaoNetherlands Antilles

Telephone: [599] (9) 4300000Telecopier: [599] (9) 4611118

PwC Caribbean Offices

2005 Budget Memorandum

St MaartenCees Rokx – PartnerPO Box 195Philipsburg, St MaartenNetherlands Antilles

Telephone: [599] (5) 4 22379Telecopier: [599] (5) 4 24788

TURKS & CAICOS ISLAN

Joseph P Connolly – ManaginPO Box 63Abacus House, ProvidencialeTurks & Caicos Islands

Telephone: [1] (649) 946 489Telecopier: [1] (649) 946 489

PricewaterhouseCoopers 40

DS

g Director

s

02

PwC Caribbean Offices