Embed Size (px)

Citation preview

20

Financing with Derivatives

©2006 Thomson/South-Western

2

Introduction

This chapter examines the characteristics and valuation of options and option-related financing.

It explores the concepts necessary to evaluate the impact that decisions to issue or purchase these type of securities have on shareholder wealth.

3

Classes of Derivatives Securities

Options

Futures and forwards

Swaps

4

Options exist in many forms

S-T options on common stock Convertible fixed-income securities Warrants Rights Bonds with redemption provisions

5

Option Exchanges

http://www.aantix.com/

http://www.cboe.com/

http://www.cbot.com/

http://www.cme.com/

6

Option

CallCall

PutPut

Option to buybuy

Option to sell

Call and put options

7

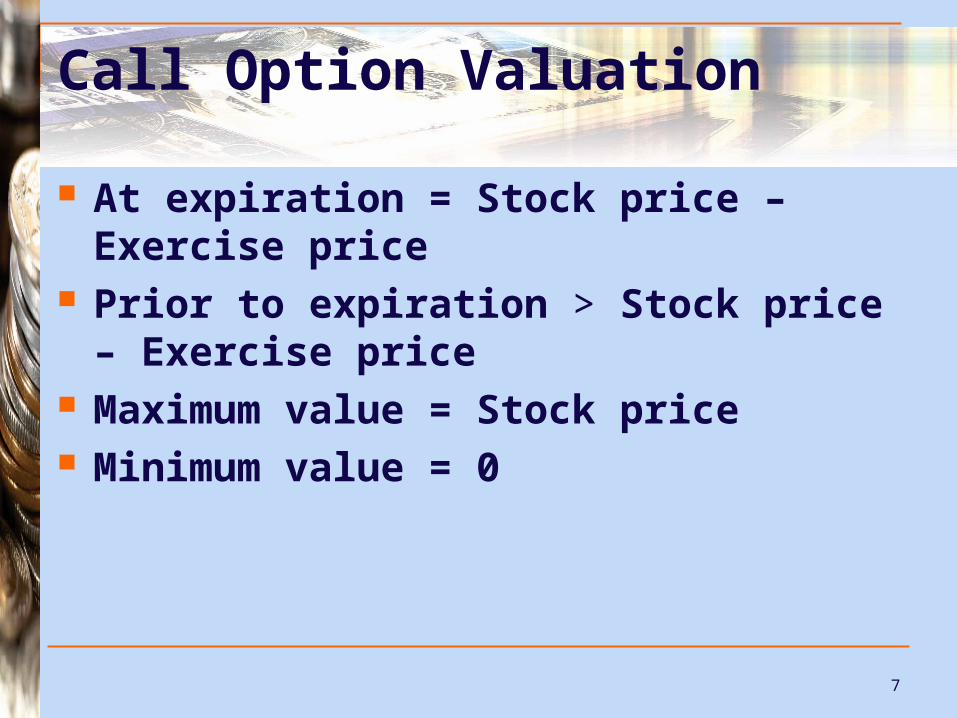

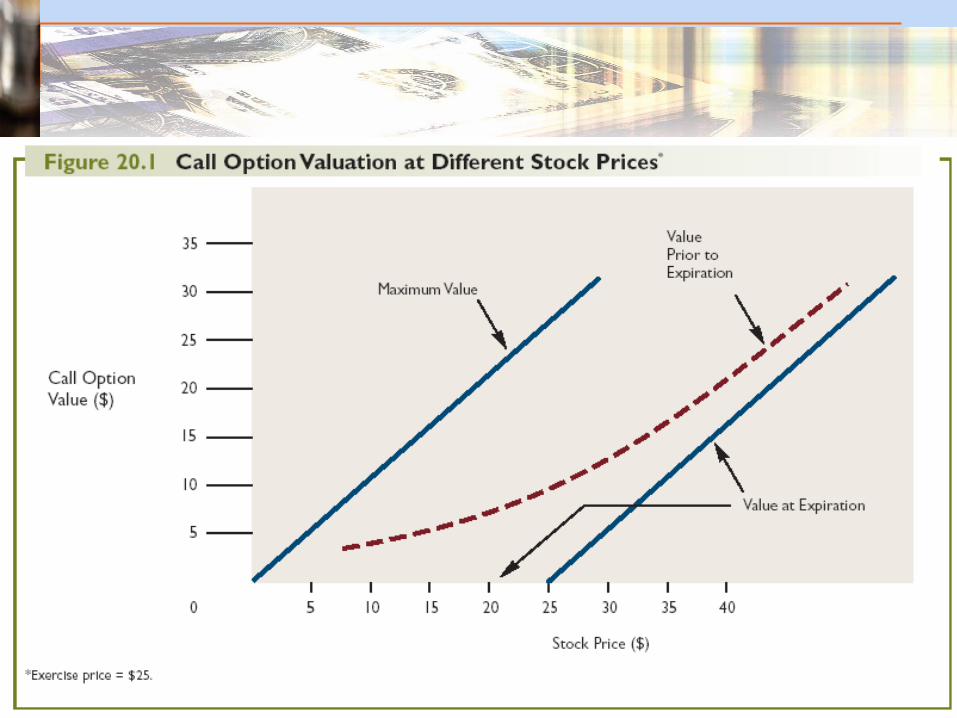

Call Option Valuation

At expiration = Stock price – Exercise price

Prior to expiration > Stock price – Exercise price

Maximum value = Stock price Minimum value = 0

8

9

Variables Affecting Option Values

VariablesVariablesaffectingaffecting

the value ofthe value ofan optionan option

Time to Time to expiration dateexpiration date

Interestrates

Expected stockprice volatility

Exercise priceExercise priceStock priceStock price

10

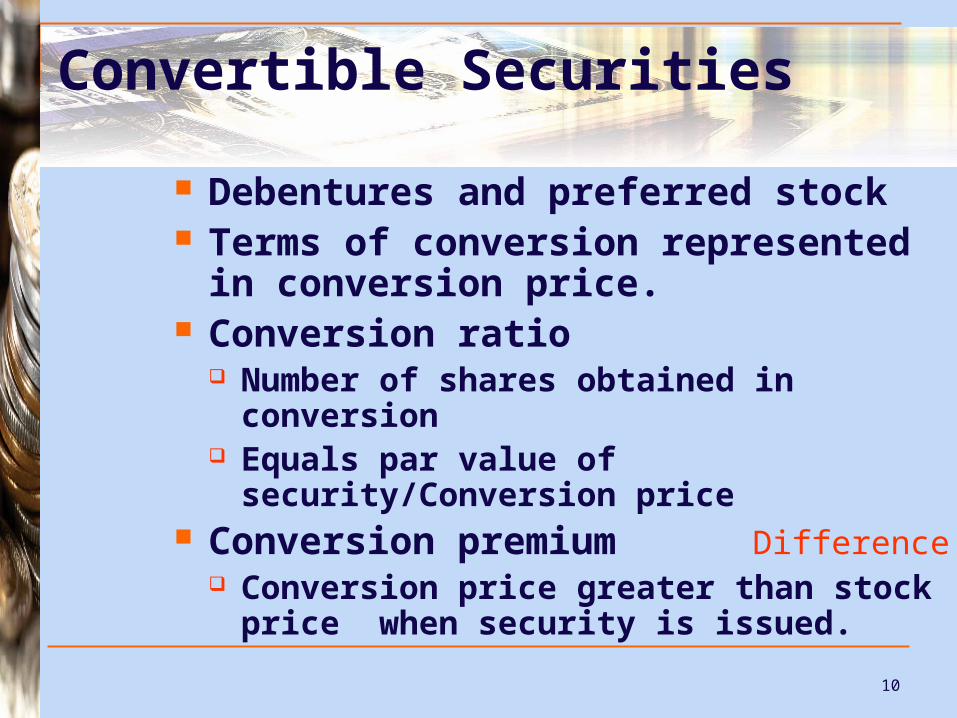

Convertible Securities

Debentures and preferred stock Terms of conversion represented in

conversion price. Conversion ratio

Number of shares obtained in conversion Equals par value of security/Conversion

price Conversion premium Difference

Conversion price greater than stock price when security is issued.

11

Reasons for Issuing Convertibles Make security more attractive Sell C/S in the future at higher price Allow time for investments to pay benefits Allows smaller, risky firms to acquire

capital Reduces agency conflicts

12

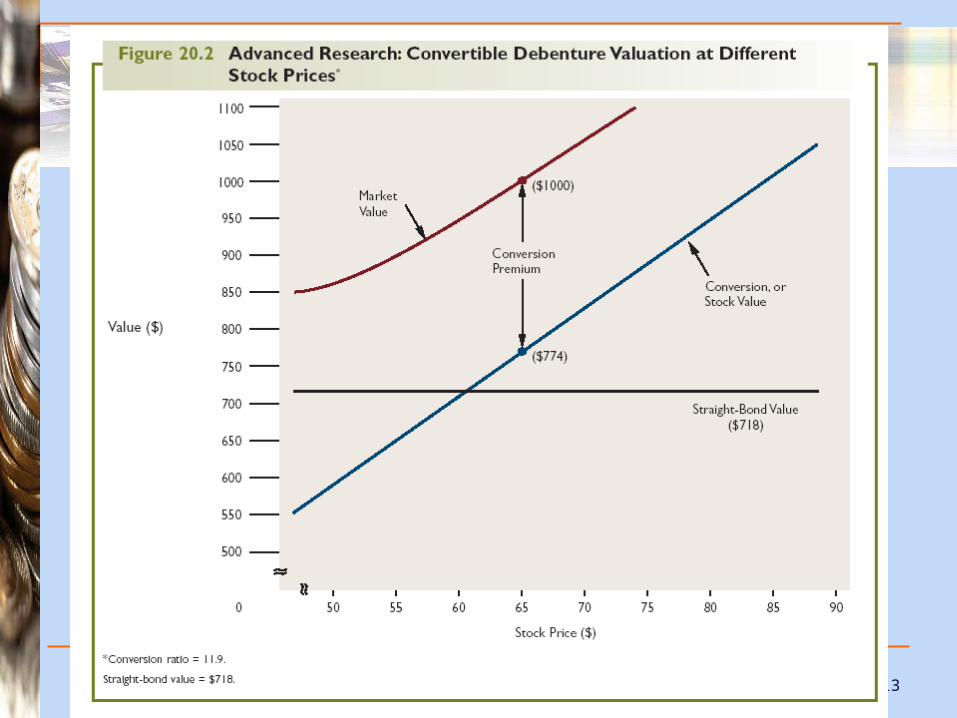

Valuation of convertibles

Conversion value Equals Conversion ratio times the Stock

price Market value

Equals the price the security trades for on the market

Usually slightly above the higher of the conversion value or the investment value

Difference is the premium Investment value

Equals the straight bond value

13

14

Option Valuation Calculator

Check out the option valuation calculator at this Web site:http://www.numa.com/

15

Conversion

Conversion

Voluntary

Forced

Call privilegeCall privilege

Prior to expirationPrior to expiration

16

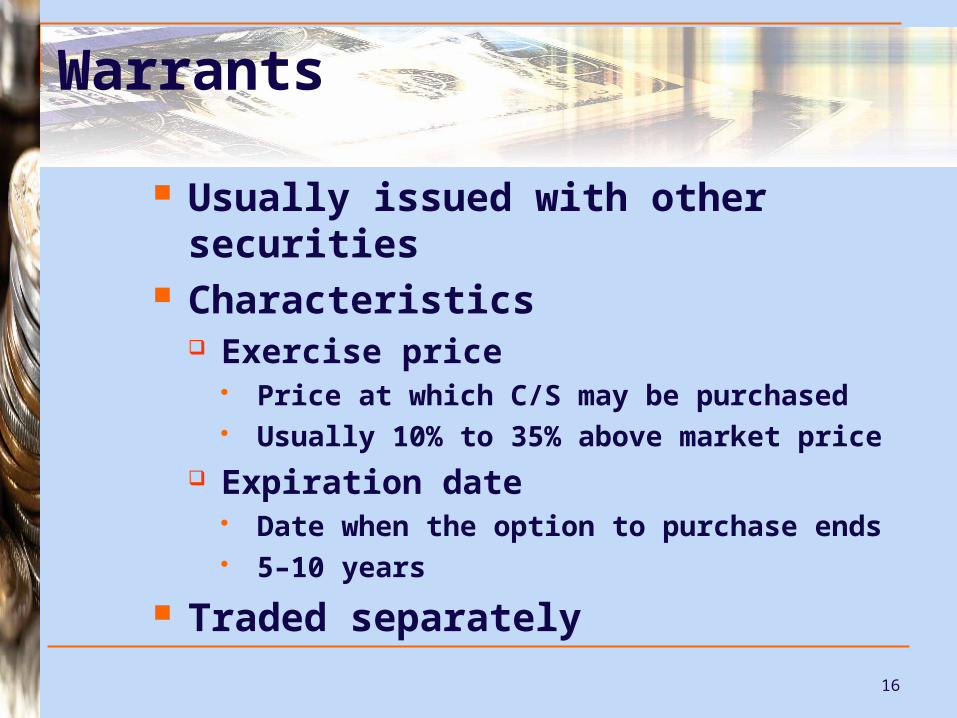

Warrants

Usually issued with other securities Characteristics

Exercise price Price at which C/S may be purchased Usually 10% to 35% above market price

Expiration date Date when the option to purchase ends 5–10 years

Traded separately

17

Warrants (continued)

Why issue warrants ? Sweetener

Provide leverage to investors

Market value of warrant Usually exceeds the formula value

The difference is called the premium

Warrants provide leverage to investors

18

Warrants (W) and Convertible Securities (C)

Characteristic W C

Lessen Agency Conflicts x x

Deferred Issuance of C/S x x

Savings of Interest or Dividends x x

Company Receives AdditionalFunds

x o

Two Securities on BooksMore Control

x o

o x

19

Rights Offering

A single right for each current share Subscription price is less than current

market price. Can sell rights Subject to a shareholder of record date

Rights-on Ex-rights

Rights trade for a price is greater than the theoretical value.

20

Economic Value

R =Mo – S

N + 1

Theoretical value of a right selling rights-on:

R =Me – S

N

Theoretical value of a right detached:

21

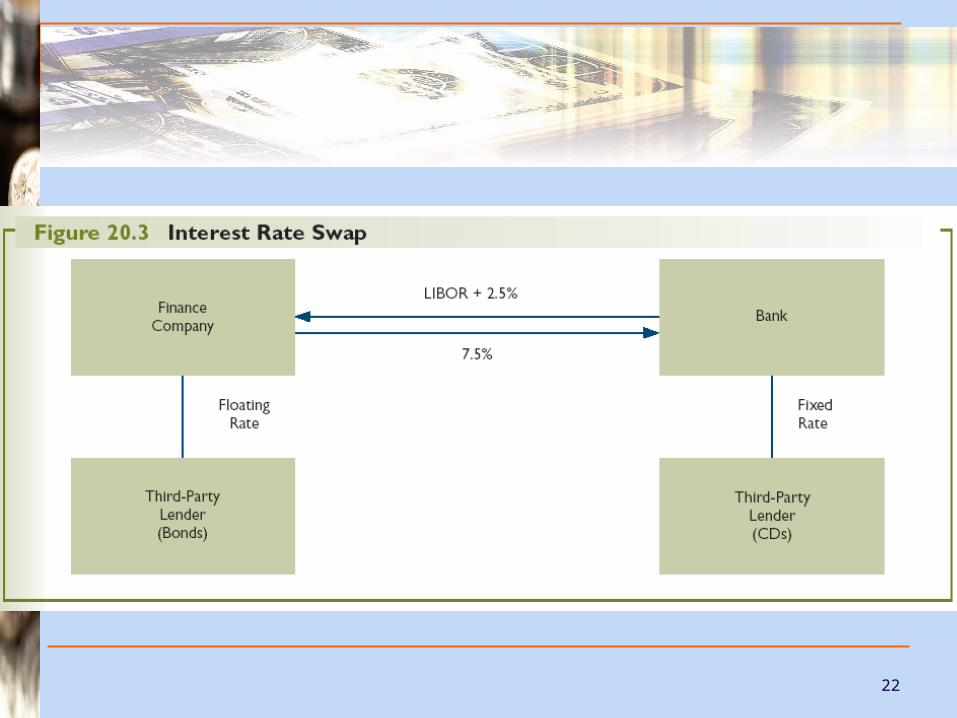

Interest Rate Swaps

Traded on the over-the-counter market Basic type

Exchange floating rate interest payments for fixed rate

Protects against fluctuations in interest rates Used to hedge against interest rate risk Longer-term risks – 10 years or more Parties to agreement

Finance company Bank Financial institutions

Floating Rate tied to LIBOR (Ch 2)

22

23

Information on Swaps

Check out the Chicago Board of Trade Web site as a source of information on swaps.http://www.cbt.com/