Embed Size (px)

Citation preview

2EIRC Newsletter | March 2013 Volume 39 | Issue No. 02

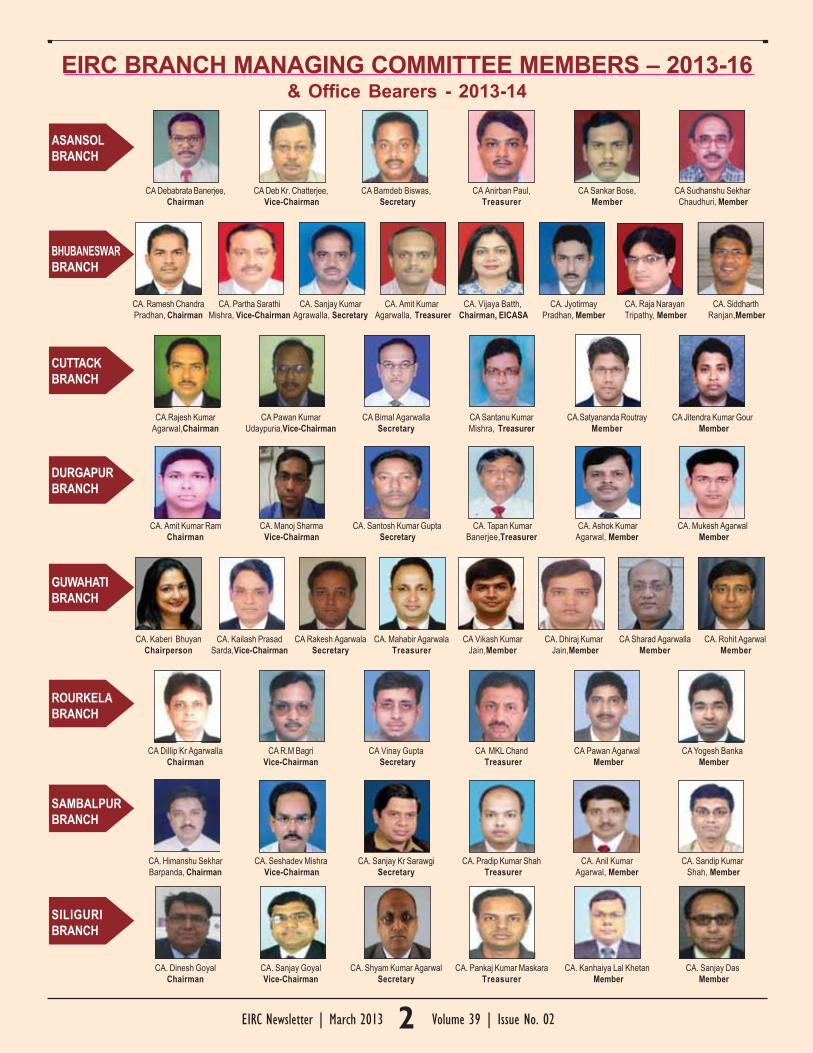

EIRC BRANCH MANAGING COMMITTEE MEMBERS – 2013-16& Office Bearers - 2013-14

CA Debabrata Banerjee, CA Deb Kr. Chatterjee, CA Bamdeb Biswas, CA Anirban Paul, CA Sankar Bose, CA Sudhanshu SekharChairman Vice-Chairman Secretary Treasurer Member Chaudhuri, Member

CA. Ramesh Chandra CA. Partha Sarathi CA. Sanjay Kumar CA. Amit Kumar CA. Vijaya Batth, CA. Jyotirmay CA. Raja Narayan CA. SiddharthPradhan, Chairman Mishra, Vice-Chairman Agrawalla, Secretary Agarwalla, Treasurer Chairman, EICASA Pradhan, Member Tripathy, Member Ranjan,Member

CA.Rajesh Kumar CA Pawan Kumar CA Bimal Agarwalla CA Santanu Kumar CA.Satyananda Routray CA Jitendra Kumar GourAgarwal,Chairman Udaypuria,Vice-Chairman Secretary Mishra, Treasurer Member Member

CA. Amit Kumar Ram CA. Manoj Sharma CA. Santosh Kumar Gupta CA. Tapan Kumar CA. Ashok Kumar CA. Mukesh AgarwalChairman Vice-Chairman Secretary Banerjee,Treasurer Agarwal, Member Member

CA. Kaberi Bhuyan CA. Kailash Prasad CA Rakesh Agarwala CA. Mahabir Agarwala CA Vikash Kumar CA. Dhiraj Kumar CA Sharad Agarwalla CA. Rohit AgarwalChairperson Sarda,Vice-Chairman Secretary Treasurer Jain,Member Jain,Member Member Member

CA Dillip Kr Agarwalla CA R.M Bagri CA Vinay Gupta CA MKL Chand CA Pawan Agarwal CA Yogesh BankaChairman Vice-Chairman Secretary Treasurer Member Member

CA. Himanshu Sekhar CA. Seshadev Mishra CA. Sanjay Kr Sarawgi CA. Pradip Kumar Shah CA. Anil Kumar CA. Sandip KumarBarpanda, Chairman Vice-Chairman Secretary Treasurer Agarwal, Member Shah, Member

CA. Dinesh Goyal CA. Sanjay Goyal CA. Shyam Kumar Agarwal CA. Pankaj Kumar Maskara CA. Kanhaiya Lal Khetan CA. Sanjay DasChairman Vice-Chairman Secretary Treasurer Member Member

2EIRC Newsletter | March 2013 Volume 39 | Issue No. 02

GUWAHATIBRANCH

SILIGURIBRANCH

SAMBALPURBRANCH

ROURKELABRANCH

DURGAPURBRANCH

CUTTACKBRANCH

BHUBANESWARBRANCH

ASANSOLBRANCH

3EIRC Newsletter | March 2013 Volume 39 | Issue No. 02

Chairman Writes

CA Ranjeet Kumar AgarwalChairman,EIRC

The EIRC News letter can be downloded from EIRC Website : eircicai.org

�Dear Friends & Professional Colleagues,It has been exactly a month, that I have taken over as theChairperson of the Eastern Region – a post – which carries withit expectations and responsibilities, which I am only beginning torealize. Yet, as one knows, “With increases powers comesincreased responsibilities,” and I have endeavored during thepast thirty days tried to do exactly that.Activities at a glance performed in last month:1. Seminars/Symposia

With every support help and support from mycouncil members, staff of ICAI and studentsat every level and a host of dynamicspeakers,I have during the past month beenable to organize the following:1. Live Budget at Palladian Lounge wherein

more than 161 members participated;2. A Budget Seminar at Kalamandir, where

the total registrations crossed 1700members;

3 Held a National Seminar on CompaniesBill,2012 at Hotel HindustanInternational;

4. Held a National Seminar on TransferPricing (International & National) atGolden Park Hotel;

5. A Bank Audit Seminar at Park Hotel.2. Meeting with President and Vice-PresidentOn 20th March I had a meeting with President and Vice Presidentat New Delhi along with all the other Regional Chairpersons, inwhich all the pertinent issues of Region were discussedthreadbare and deadlines were fixed to monitor the resolutionarrived upon the issues discussed therein. I believe this will go along way in making the performance of every region both efficientand effective. As far as the Eastern Region is concerned, I havetaken upon myself to address matters which directly concernboth the students and members, and their overall academic andprofessional development.I have also made it clear that I ammost open to suggestions and advices, by anyone who has apositive thought or initiative in mind so that the Eastern Regiongains mileage in terms of performance and attainmentspredetermined landmarks.3. Holi and Dol Jatra Get-togetherThis month, the Festival of Colors beckons, and considering thatwe need to add some fun, joy and humour to our lives; on 23rdMarch,EIRC organized a Holi Get-Together at EZCC along withAll the Study Circles where in more than 1200 members enjoyedthe Kavi Sammelan performed by Padamshree Surendra Sharmaand group. This laughter therapy, I know will go a long way inmaking our community happier and bring joy to our families, whoare often at the receiving end of our scant social commitmentand time.I also thanks conveners of All Study Circles for theiractive participation and support.4. Campus Placements for Newly Qualified CAsThe campus interviews for fresh Chartered Accountants of thiszone was held and 10 best companies had participated, recruitingalmost 91 graduates.I understand the numbers are minisculeas compared to the numbers who had enrolled for campus. Yet,it is by far higher than that in the previous years. I also feel that for

the ones who have not been selected, there will be no dearth ofemployment opportunities, if they are diligent and have faith intheir abilities;5. Meeting with Hon’ble Minister Sachin PilotOn 23rd March the undersigned along with EIRC Secretary CAP.D.Rungta and EIRC Treasurer CA Anirban Datta had theopportunity to meet Hon’ble Minister of State for Corporate Affairs

(I/C) Mr Sachin Pilot at Grand Hotel in Kolkata.6. Bank AuditThe final list of Bank wise Statutory Auditors ofBank Branches has been hosted on the websiteof RBI. Our ICAI has also formed a group to clearthe queries and grievances of Auditor of BankBranches.Please call CA AbhijitBandhopadhyay,our Central Council Member inthis regard.7. 31st March ClosingThe month of March, brings us close to all kindsof deadlines, particularly for us CharteredAccountants, more so on the issues of DirectTaxes. In this connection, I would like membersto note that the dates has been extended inIncome Tax Department and returns will be

submitted on 29th, 30th and 31st March, the entire day.

I am also endeavoring with initiatives for the development andbenefit of members:A) Improving the quality and content of the EIRC Magazine,

thereby making it more reader friendly and interesting for itsreaders both – members and students;

B) Seeking out avenues for new members, and enabling themto set-up practice, where they so desire and also makingprovision for their employment, in case they have a servicemotive;

C) On 8th April,2013 we have planned an orientation meeting ofAll Managing Committee Members of Branches and Regionalcouncil with President and Vice-President in Kolkata.

We look forward to a new financial year with hope, renewed zestand expectations that it would be better than the previous one. Aswe all know that change is inevitable and every situation, no matterwhat it is, will change. I say this keeping a watch on our economyand present developments, which has been sluggish but I havereasons to believe that the initiatives of the present government,a diligent budget, better performances of the agricultural andindustrial sectors would contribute to our growth.The Festival of Colors and Good Friday, promise joy, a resurgenceof faith and belief that good would prevail over bad and thatSummers’ would be more bearable than we can imagine. Onthis note, I would end, wishing each one of you and your familiesthe best for HOLI and a Prayerful Easter. May the festivities showeryou all with the best life has to offer.

Sincerely yours,

4EIRC Newsletter | March 2013 Volume 39 | Issue No. 02

Forthcoming Programme

EIRCDay and Date Programme Speakers Coordinator Venue Duration CPE Delegate

Hours FFFFFees `ees `ees `ees `ees `

Friday 12th Valuation of Equity shares CA S.S.Gupta CA Manish R.Singhi Hall, 5.15 pm to 3 150April, 2013 using DCF Method Goyal EIRC Premises 8.30 pmThursday 18th Effective Public Speaking & Mr Shekar Shukla, CA Sunil Kr R.Singhi Hall, 5.15 pm to 3 150April, 2013 Leadership Certified John Maxwell Sahoo EIRC Premises 8.30 pm

Team TrainerFriday 19th & Two Day Conference Eminent Speakers EIRC Vidya mandir 10.00 am to 12 1000Saturday 20th on Service Tax Hall 5.00 pmApril, 2013 (Details in pg 10)Wednesday 24th Share Capital Vs Sec 263 Adv. Paras Kochar CA Subhash R.Singhi Hall, 5.15pm to 3 150April, 2013 of the IT Act Ch Saraf EIRC Premises 8.30pmSaturday 27th Seminar on VAT Audit Eminent Speakers EIRC R.Singhi Hall, 10.00 am to 6 600April, 2013 EIRC Premises 5.00 pmMonday 29th TDS Return, Assessment CA Mayank Chamaria CA Pramod R.Singhi Hall, 5.15pm to 3 150April, 2013 Procedure & Issues CA Lalit Agarwal Dayal Rungta EIRC Premises 8.30pmThursday 2nd Concurrent Audit of Banks Eminent Speakers CA Anirban R.Singhi Hall 5.15pm to 3 150May, 2013 Datta EIRC Premises 8.30pmNote: (1) Seminar on 2nd and 5th April, 2013 has been cancelled due to the engagement of members for Bank Audit. (2) The above Seminar (except full day seminar) can be attended by the student Rs. 50/-

Study CircleStudy Circle Day & Date Programme Speakers Co- Venue Duration CPE

ordinator Hour

Vitta Salahkar Saturday, Provisions Relating Dr. Debasish Mitra CA.Hari Ram Agarwal Barabazar Library 3.00 P.M. 3Chartered 20th April,2013 To Directors & CA. Vinod Kothari 098306 30386 Bhawan to 6.00 P.M.Accountants study Meetings, under [email protected] 10/1/1, Syed Salleycircle - EIRC Companies Bill, 2012 Lane, Kolkata - 73Vitta Salahkar Sunday, Training Session On Mr. Ajay Agarwal CA.Hari Ram Agarwal Barabazar Library 9.00 A.M. to 4Chartered 28th April,2013 The Art Of Public 098306 30386 Bhawan, 1.00 PMaccountants study Speaking [email protected], 10/1/1, Syed Salleycircle - EIRC Lane, Kolkata - 73

CONTENTS

PARTICULARS Pg No.PARTICULARS Pg No.

EIRC of ICAI����� Chairman Writes 3����� Forthcoming Programme for Members 4����� EICASA Column 5����� EIRC Programme Details 9Articles����� Analysis of Budgetry Proposals on Direct Taxes 11����� Finance Budget 2013 – Indirect Taxes 14News����� Recent Judicial Pronouncements - Direct Tax 12-13

����� Recent Judicial Pronouncements - Indirect Tax 14����� Notification /Circulars 15-18����� Study Circle News 19-20����� Crossword 21-22Announcement����� Work Disposal Position 18����� Library News 19����� Empanelment 17

On the Cover – CA Ranjeet Kumar Agarwal , Chairman, EIRC, CA Pramod Dayal Rungta, Secretary, EIRC & CA Anirban Datta, Treasurer, EIRC meetsMr Sachin Pilot, Hon’ble Minister of Corporate Affairs, Govt of India.

5EIRC Newsletter | March 2013 Volume 39 | Issue No. 02

CA Subhash Chandra SarafChairman, EICASA, Vice Chairman-EIRC

EICASA

Campus Orientation Programme On 7th March, 2013 at Swabhumi, Kolkata

L to R: CA Abhijit Bandyopadhyay, Central CouncilMember, ICAI, CA Ranjeet Kr Agarwal, Chairman,

EIRC & CA Atis Basu, DCO Head of EIRC.

CA Saradindu Datta, CA Pramod Dayal Rungta,Secretary, EIRC, Mr Jai Shankar Gopalan.

CA Saugata Sen, CA Rishi Khator

CA Anupam Agarwal & CA Abdul Rahim Abhas Luharuwalla, President, Poddar Chhatra Niwas; CASubhash Ch. Saraf,Chairman, EICASA & Vice Chairman, EIRC;Navin Begwani,Vice Chairman, EICASA,CA Ayush Jain

Vivek Agarwal, Member EICASA; CA Subhash Ch. Saraf ,Chair-man, EICASA & Vice Chairman, EIRC; Abhas Luharuwalla;Navin Begwan,ViceChairman, EICASAi, CA Ayush Jain

Dear Students,Achieve more & more …I am highly elated in having the opportunityto communicate with my beloved students,being the Chairman of EICASA of EIRC. Lifeis nothing but a continuous process ofhigher learning and during this period of oneyear, I would be experiencing my studentlife through you and would be learning morethrough interaction with you.

During my one month in office, there has been many activities forstudents as detailed hereunder:Campus placement interview was completed wherein 10companies participated and 42 candidates were selected by 8companies and 2 companies shortlisted 50 candidates for finalinterview.Mock Test for IPCC and Final Students were held on 11th March2013.Revision classes for IPCC and Final students were held from12th to 24th March 2013.A visit to ‘Poddar Chhatra Niwas’ was done by me on 14th March2013 and interaction was done with approximate 100 boarder CAstudents.You are requested to note the following events for coming monthsdetailed as under:-1. An Industrial Visit has been organized to the shirt

manufacturing corporate namely ‘Turtle Limited’ Howrah on30th March 2013. Maximum registration 50 Students.

2. A Students’ Seminar on “How to pass CA Examinations” hasbeen fixed at Rotary Sadan on 4th April 2013. Registration areon first come first served basis.

3. Second Mock Test for IPCC / Final Students has beenorganized on 8th April 2013 at ‘Anglo Arabic Secondary School’.

4. A visit to Rajendra Chhatra Niwas has been organized on 20th

April 2013 for interaction with boarders of the hostel.5. An Education Boutique – 2013 has been organized by the

Times of India on 11th & 12th May 2013 at Park Hotel, Kolkata.I would like to place following important information for thebenefit of students :-(a) Last date for registration for CPT Course for June 2013

term is on or before 2nd April 2013.(b) CPT Exam – June 2013 form filling dates are from 3rd to

25th April 2013. No submission of form with late fee isallowed.

(c) “Students Special Grievance Cell” is operative every ThirdFriday of the month from 4.00 PM to 6.00 PM in EICASARoom.

It is advised to regularly visit the Institute’s Website www.icai.organd EIRC Website www.eircicai.org for latest update. It is alsoadvised to check Students’ Notice Board at EIRC from time totime for various activities and events. I also strongly recommendyou to read Students’ Journal (The Chartered Accountant Student)issued by the ICAI for current valuable topics and updates.I am happy to inform you that 1st International Students’ Conventionhas been scheduled to be held at Science City, Kolkata on 13th &14th August 2013 and I expect your whole hearted cooperation tomake it a grand success.You are requested to send your views and / or suggestions forimprovement, correction or modification in Students’ activities andespecially EICASA activities which you may send directly to me [email protected] while marking a copy toeicasakolkata@ gmail.comLooking forward for an eventful year.

Interaction of ICASA Chairman with CA Student of Poddar Chhatra Niwas

6EIRC Newsletter | March 2013 Volume 39 | Issue No. 02

BUDGET PROPOSALS - DIRECT TAXESCA K. K. Chhaparia

1. DEEMED SALES CONSIDERATION ON TRANSFER OFIMMOVABLE ASSETS (HELD AS BUSINESS ASSET)

1.1 It is proposed to provide by inserting a new section 43CAthat where the consideration for the transfer of an asset(other than capital asset), being land or building or both,is less than the stamp duty value, the value so adoptedor assessed or assessable shall be deemed to be thefull value of the consideration for the purposes ofcomputing income under the head “Profits and gains ofbusiness of profession”.

1.2 It is also proposed to provide that where the date of anagreement fixing the value of consideration for the transferof the asset and the date of registration of the transfer ofthe asset are not same, the stamp duty value may betaken as on the date of the agreement for transfer andnot as on the date of registration for such transfer. However,this exception shall apply only in those cases whereamount of consideration or a part thereof for the transferhas been received by any mode other than cash on orbefore the date of the agreement.

1.3 These amendments will take effect from assessment year2014-15 and subsequent assessment years.

1.4 Currently, when a capital asset, being immovableproperty, is transferred for a consideration which is lessthan the value adopted, assessed or assessable by anyauthority of a State Government for the purpose ofpayment of stamp duty in respect of such transfer, thensuch value (stamp duty value) is taken as full value ofconsideration under section 50C of the Income-tax Act.These provisions do not apply to transfer of immovableproperty, held by the transferor as stock-in-trade. Thisview has been held in several cases such as :� CIT v. M/S Kan Construction And Colonizers (P)

Ltd [2012] 20 taxmann.com 381 (Allahabad)� K.R. Palanisamy v. Union of India [2009] 180 Taxman

253 (Mad.)� Asst CIT v. Excellent Land Developers (P.)

Ltd. [2010] 1 ITR (TRIB.) 563 (Delhi)Since Section 50C uses the word ‘capital asset’, itsprovisions can be invoked only if the land or buildingssold during the year is a capital asset. Stock in tradehas been excluded from the definition of capital assetby sec. 2(14). As a result, the flats/building constructedand sold by builders and developers which are theirbusiness activity, and their ‘stock-in-trade’, could not bebrought into Sec. 50C. Therefore the valuation done bystamp valuation authorities could not be substituted forapparent sale consideration in case of the transfer offlats/buildings even if such valuation by stamp valuationauthorities was more than apparent sale consideration.The new provision has been introduced to bring thetransfer of land or building or both (being stock in trade)at par with section 50C and now the valuation done bystamp valuation authorities could be substituted for

apparent sale consideration.1.5 To simplify this provision assuming a builder starts

booking flats in a residential project at ‘ 2,000/- per sqft. (assuming the Stamp Duty Value of that area is ‘1,900/- per sq. ft.). He offers 20% discount (i.e., he booksat ‘ 1,600/- per sq. ft.) to such persons who makes 90%down payment of the entire consideration at the time ofbooking of the flat. In the given circumstance, for flatsbooked under installment scheme for ‘ 2,000/- per sq.ft., the sale consideration to be deemed to be ‘ 2,000/-per sq. ft. and for the flats booked under down paymentscheme the sale consideration will be deemed to be ‘1,900/- per sq. ft. (being the Stamp Duty Value) insteadof ‘ 1,600/- per sq. ft. Thus, the builder is liable to betaxed even for discount of ‘ 300/- (i.e., ‘ 1,900 - ‘ 1,600)which in other way represents his notional finance cost.

1.6 Practically, most of the builders follow ‘PercentageCompletion Method’ whereby sale consideration isrecognized in the accounts in more than one accountingyear for the sale of the same flat. It will be herculeantask for the Assessing Officer to calculate apparent salesconsideration as he has to not only refer to the recordsof the instant year but also of the earlier years in whichbooking was done, in order to find out the taxable incomeunder this provision.

1.7 Now let us come to another situation where a flat isbooked by the builder before 31st March 2013, i.e., beforethe date of applicability of proposed amendment and herecognize the corresponding revenue in assessment year2014-15, i.e., assessment year covered by the aforesaidamendment proposal. Now, whether this proposal willapply on such transfer also? This needs to beclarified before passing the Finance Bill 2013.

1.8 This proposal alongwith other proposals pertaining totransactions in immovable property will have far reachingimpact and may in the long run affect all real estatetransactions.

2. DEEMED INCOME ON IMMOVABLE PROPERTYRECEIVED FOR INADEQUATE CONSIDERATION

2.1 The existing provisions of Section 56(2)(vii)(b), inter alia,provide that where any immovable property is receivedby an individual or HUF without consideration, the stampduty value of which exceeds fifty thousand rupees, thestamp duty value of such property would be charged totax in the hands of the individual or HUF as income fromother sources.

2.2 The existing provision does not cover a situation wherethe immovable property has been received by an individualor HUF for inadequate consideration. It is proposed toamend Section 56(2)(vii)(b) so as to provide that whereany immovable property is received for a considerationwhich is less than the stamp duty value of the propertyby an amount exceeding fifty thousand rupees, the stampduty value of such property as exceeds such

7EIRC Newsletter | March 2013 Volume 39 | Issue No. 02

consideration, shall be chargeable to tax in the hands ofthe individual or HUF as income from other sources.

2.3 Considering the fact that there may be a time gap betweenthe date of agreement and the date of registration, it isproposed to provide that where the date of the agreementfixing the amount of consideration for the transfer of theimmovable property and the date of registration are notthe same, the stamp duty value may be taken as on thedate of the agreement, instead of that on the date ofregistration. This exception shall, however, apply only ina case where the amount of consideration, or a partthereof, has been paid by any mode other than cash onor before the date of the agreement fixing the amount ofconsideration for the transfer of such immovable property.

2.4 This amendment will take effect from assessment year2014-15 and subsequent assessment years.

2.5 To simplify, let us again refer to example in the para 1.5above. Thus, for flats booked under down paymentscheme an assessee may be liable to tax on income of ‘300/- per sq. ft. being the difference between the StampDuty Value and the sale consideration. Though thedifference is merely because he is making payment earlierand it merely represents notional financial opportunity cost.

2.6 The term ‘Transfer’ in relation to capital asset includeany transaction involving possession of immovableproperty in part performance of contract as referred to inSection 53A of Transfer of Property Act 1882. As perthe said section the date of possession is an importantcriterion to determine when immovable property isacquired in relation to a capital asset. Now, coming toabove instance wherein immovable property is bookedin March 2013 but possession is received in April 2014a question may emerge whether the aforesaid provisionshall apply, as on the date of booking this proposal isnot in the statue book while on the date of possessionthis proposal has become a part of statue book.

2.7 Thus, for transaction in immovable property there is atwo way sword, both in the case of transferor (Section43CA) and in the case of transferee being an Individualor HUF (Section 56).

2.8 However, this provision does not apply where there is atransfer of immovable property to a relative as defined inSection 56.

2.9 Similar amendment was made in the past by the FinanceAct 2009 with effect from 1st October 2010. However, inFinance Act 2010, by way of retrospective effect, thisamendment was deleted.

3. TDS ON TRANSFER OF CERTAIN IMMOVABLEPROPERTIES

3.1 It is proposed to insert a new section 194-IA to providethat in case of transfer of immovable property (other thanagricultural land) by a resident, every transferee shalldeduct TDS at the rate of 1% of the consideration amountat the time of payment or credit whichever is earlier.

3.2 It is further proposed that no deduction of tax under thisprovision shall be made where the total amount ofconsideration for the transfer of immovable property, isless than ‘ 50 lakh.

3.3 This Amendment is proposed to take effect from 1st June2013.

4. ADDITIONAL INCOME TAX ON BUY BACK OFSHARES BY UNLISTED ENTITIES

4.1 As per present provisions, the consideration received bya shareholder on buy-back of shares by the company isnot treated as dividend but is taxable as capital gainsunder Section 46A. A Company, having distributablereserves, has two options to distribute the same to itsshareholders either by declaration and payment ofdividends to the shareholders, or by way of purchase ofits own shares (i.e. buy back of shares) at a considerationfixed by it. In the first case, payment by the Company issubject to Dividend Distribution Tax (DDT) and income inthe hands of shareholder is exempt. In the second casethe income is taxed in the hands of shareholders ascapital gains.

4.2 Unlisted Companies, having surplus funds, are generallyresorting to buy back of shares instead of payment ofdividends in order to avoid payment of tax by way of DDTparticularly where the capital gains arising to theshareholders are either not chargeable to tax or aretaxable at a lower rate.

4.3 In order to curb such practice it is proposed to amendthe Act, by insertion of new Chapter XII-DA, to providethat the consideration paid by the unlisted company forpurchase of its own shares which is in excess of thesum received by the company at the time of issue ofsuch shares shall be treated as ‘distributed income’ andthe company shall be liable to pay additional income-tax @ 20% of the distributed income paid to theshareholder. The additional income-tax payable by thecompany shall be the final tax on similar lines as dividenddistribution tax (DDT). The income arising to theshareholders in respect of such buy back by the companywould be exempt where the company is liable to pay theadditional income-tax on the buy-back of shares.

4.4 These amendments will take effect from 1st June 2013.4.5 The proposal in the present form may create lot of

litigations. Assuming the consideration paid by theshareholder is ‘ 100/- per share at the time of allotment,then there can be three situations :(i) The buy-back is made at a price of ‘ 100/-.(ii) The buy-back is made at a price less than ‘ 100/-.(iii) The buy-back is made at a price more than ‘ 100/-Prima facie, the instances mentioned in point (i) & (ii)above are irrelevant here because the proposed provisionis applied only when the consideration paid by thecompany for buy back of shares is in excess of sumreceived at the time of issue of the shares. In the firsttwo situations, the consideration received for buy backis less than or equal to the sum received at the time ofallotment.So, only in the third situation this provision may applywhen buy back price is more than the issue price of theshares.Now, let us come to a hypothetical situation. In betweenthe allotment and buy back of shares, the original allotteetransfers the shares to another person at ‘ 20/- and suchother person lodges for buy back of shares at ‘ 110/-.

8EIRC Newsletter | March 2013 Volume 39 | Issue No. 02

The proposal in the present form will make only ‘ 10/-liable to tax as Dividend Distribution Tax (DDT) in thehands of the company under the proposed provisions. Inthat case, the income of ‘ 80/- in the hands of shareholdershall be fully exempt, in the view of proposed insertionof section 10(34A) read with Section 115QA.

5. APPLICATION OF SEIZED CASH UNDER SECTION132B

5.1 The existing provisions contained in Section 132B, interalia, provide that seized assets may be adjusted againstany existing liability under the Income-tax Act, Wealth-tax Act, the Expenditure-tax Act, the Gift-tax Act and theInterest-tax Act and the amount of liability determined oncompletion of assessments pursuant to search, includingpenalty levied or interest payable and in respect of whichsuch person is in default or deemed to be in default.

5.2 It is proposed to amend the aforesaid section so as toclarify that the existing liability does not include advancetax payable.

5.3 This amendment will take effect from 1st June 2013.5.4 In the case of search u/s 132, when cash is seized, it is

kept in P.D. account of CIT. This cash is not adjustedagainst the advance tax inspite of specific request madeby the assessee for such adjustment. Even in caseswhen assessee makes declaration of undisclosedincome, the amount of seized cash is not adjustedagainst the tax liability relating to undisclosed incomepaid by the assessee.

5.5 The provision of clause (i) of Section 132B(1) regardingapplication of seized assets is not very clear in thisregard. It requires seized assets to be applied firsttowards the amount of the existing tax liability, if any,and thereafter towards the amount of tax liability to bedetermined on completion of the assessment relating tosearch years including any penalty levied or interestpayable in connection with such assessment. Theprovision is not clear as to what would happen to cashseized till completion of assessment or penaltyproceedings.

5.6 The provision of sub-section (4) of Section 132B regardingpayment of interest is also not clear as to whether interestis payable on surplus money after adjusting the liabilityarising on assessment u/s 153A or on the total amountof cash seized from the date of seizure till adjustmentof the same towards tax liability arising on assessment.

5.7 Accordingly, in the Pre-Budget Memorandum sent byICAI, it was suggested for amendment in Section 132B,clarifying the amount of cash seized to be permitted foradjusting against the advance tax liability of the assesseewhere specific request is made for such adjustment. Thiswould help in early realization of tax, avoid litigation andsave the assessee from mandatory interest charged u/s234B and 234C.

5.8 This amendment has been proposed, prima facie, tonullify the views taken by various courts/tribunals thatthe term “existing liability” include advance tax liabilityof the assessee.In the following judgements, it has been held that amount

of cash seized from assessee in search proceedingsunder section 132 can be adjusted against his advancetax liability :� Nikka Mal Babu Ram v. Asstt. CIT [2010] 41 SOT

407 (CHD.)� Ram S. Sarda v. DCIT [2012] 25 taxmann.com 455

(Rajkot)� ACIT v. Vaibhav Tylsyan [ITA No. 1695/Kol/2011]� Siddharth Jain v. ACIT [ITA No. 2166/Kol/2009]

5.9 An assessee from whose possession, cash has beenseized will not be able to claim adjustment of suchretained/seized cash against his liability for advance taxand he would be liable to pay interest due under Sections234A, 234B and 234C as per proposed amendment.

5.10 This proposal is prospective and is stated to beclarificatory. In legal parlance, clarificatory amendmentsare generally deemed to be retrospective.

6. DIRECTION FOR SPECIAL AUDIT UNDER SECTION142 (2A)

6.1 The existing provisions contained in sub-section (2A) ofSection 142, inter alia, provide that if at any stage of theproceeding, the Assessing Officer having regard to thenature and complexity of the accounts of the assesseeand the interests of the revenue, is of the opinion that itis necessary so to do, he may, with the approval of theChief Commissioner or Commissioner, direct theassessee to get his accounts audited by an accountantand to furnish a report of such audit.

6.2 It is, therefore, proposed to amend the aforesaid sub-section so as to provide that if at any stage of theproceedings before him, the Assessing Officer, havingregard to the nature and complexity of the accounts,volume of the accounts, doubts about the correctness ofthe accounts, multiplicity of transactions in the accountsor specialized nature of business activity of the assessee,and the interests of the revenue, is of the opinion that itis necessary so to do, he may, with the previous approvalof the Chief Commissioner or the Commissioner, directthe assessee to get his accounts audited by anaccountant and to furnish a report of such audit.

6.3 This amendment will take effect from 1st June 2013.6.4 The expression “nature and complexity of the accounts”

has been interpreted in a very restrictive manner in severalcases such as :� Gurunanak Enterprises v. Commissioner of Income-

Tax and Anr. [2003] 259 ITR 637� Yum! Restaurants India Pvt. Ltd v. Commissioner of

Income-Tax [2005] 278 ITR 401� Peerless General Finance and Investment Co. Ltd

v. Dy. CIT [1999] 236ITR 671 (Cal.)� Muthoottu Mini Kuries v. Dy. CIT [2001] 250 ITR 455

(Ker.)6.5 Now the Assessing Officer can call for Special Audit in

a number of circumstances such as volume of theaccounts, doubts about the correctness of accounts,specialized nature of business activities etc. Till datevery few cases have been referred for special audit, wemay find more cases being referred to special audit inthe days to come.

9EIRC Newsletter | March 2013 Volume 39 | Issue No. 02

A. Service TaxI. Vocational Training – Service tax exemption on NSDC

affiliated Institutes removedNSDC is pioneering public private partnership tocatalyzeinitiatives to involve the industry in all aspects of skilldevelopment through ultra - low cost, high-quality, innovativebusiness models. It’s really so unfortunate that governmenthas withdrawn Service Tax exemption on institutes affiliatedto NSDC. On one hand, government is spending Crore ofrupees to train unemployed youth, by various schemes runby Central and State government for skill development. Thisincludes not only training, but also expenses for food andresidential facilities, transportationetc. On the other hand,Government is levying service tax on all those vocationaltraining institutes, except those affiliated to NCVT or SCVT,who are already working for the mission “employment for youththrough vocational training” for years, thereby ultimatelysaddling the lower and middle class strata of students withextra burden of service tax.II. Service Tax Voluntary Compliance Encouragement

Scheme 2013 – Will it rake the Moolah?Under the scheme you can get a complete waiver or immunityfrom interest, penalty and prosecution with respect to theservice tax liability declared under the scheme. Further, thematters declared under the scheme cannot be reopened laterin any department or court proceedings. Eligibility to participatein this scheme is seriously limited. Following set of assessecannot participate:

a) An assesse who has declared true liability in his returnbut has not paid the dues.

b) A notice or order for any period in respect of a particularissue already exists, disclosure cannot be made for asimilar issue for any subsequent period

c) An inquiry, investigation or an audit is pending as on01-03-2013

The only assesse, therefore, eligible to participate are oncewho have not paid tax and are not yet put on notice by thedepartment.For those who are eligible, you can also explore the followingpossibilities to save on the existing or future cash outflowswith respect to the tax required to be deposited under thescheme:

1. Payment of tax declared through existing CENVATcredit balance.

2. Claiming of CENVAT credit for the amounts depositedfor reverse charge mechanism.

III Abatement on construction of complex services –Complex is the new simple

Effective rate of service tax increased to 3.618% from 3.09%in case of construction of complex other than residential units

having carpet area upto 2000 sq. ft. or where the amountcharged is less than rupees one crore.IV Limitation period of 18 months in Service taxEarlier, department could issue SCN for a period of 5 yearswhere service tax has not been paid or levied owing to reasonsof fraud, collusion, willful misstatement or suppression of facts.Where these elements are not present, SCN could be issuedonly for a period of 1 year. After the amendment, where theseelements are not present SCN could be issued for a period of18 months.A further amendment has been made whereina demand raisedby the department by invocation of extended period of limitationof 5 years has been struck down by an appellate authority,tribunal or court on grounds of absence of elements of fraud,collusion, willful misstatement or suppression of facts butnevertheless service tax is payable otherwise on merits, thedepartment can still proceed to determine demand for 18months as if the SCN was issued for those 18 months.

B. Central ExciseI. Relief for ready-made garmentsBRANDED readymade garments, falling under Chapters 61,62 and 63 of the Central Excise Tariff were liable to 12 %Excise duty so far. The tariff value for the same has been fixed30 % of the Retail Sale Price of the garments. All goods fallingunder these chapters, not bearing any brand name, wereentitled for full exemption as per S.No. 16 of Notification 30/2004. Now, this S.No. 16 of Notification 30/2004 has beenamended to the effect that even branded garments would alsobe entitled to claim full exemption. The option of paying 6 %duty is now made available under S.No. 7 of Notification 7/2012 even for branded garments.Now, all branded readymade garments manufacturers, whowere hitherto paying 12 % on 30 % of MRP, can opt for fullexemption under S.No. 16 of Notification 30/2004, with effectfrom 01.03.2013.II 365 is total period for which a Stay order granted by

CESTAT will be operationalThe Appellate Tribunal shall, where it is possible to do so,hear and decide every appeal within a period of three yearsfrom the date on which such appeal is filed :Provided that where an order of stay is made in any proceedingrelating to an appeal filed under sub-section (1) of section35B, the Appellate Tribunal shall dispose of the appeal withina period of one hundred and eighty days from the date of suchorder:Provided further that if such appeal is not disposed of withinthe period specified in the first proviso, the stay order shall,on the expiry of that period, stand vacated.”In view of the proposed amendment, one thing is clear. CESTATcan grant stay for a total period of One year from the date offiling the appeal.This provision, in terms of which, theDepartment can take recovery action after 365 days from the

BUDGET PROPOSALS - INDIRECT TAXESBy CA Rohit Surana

10EIRC Newsletter | March 2013 Volume 39 | Issue No. 02

FORM IVStatement about ownership and other particulars aboutnewspaper EIRC NEWSLETTER to be published inthe firstissue every year after the last day of February1. Place of publication KOLKATA2. Periodicity of its publication MONTHLY3. Printer’s Name ATIS BASU

Nationality INDIANAddress 7, AnandilalPoddarSarani

(Russell Street) Kolkata - 7000714. Publisher’s Name ATIS BASU

Nationality INDIANAddress 7, AnandilalPoddarSarani

(Russell Street) Kolkata - 7000715. Editor’s Name CA. RANJEET KUMAR AGARWAL

Nationality INDIANAddress 7, AnandilalPoddarSarani

(Russell Street) Kolkata - 7000716. Names and addresses of Eastern India Regional

individuals who own the Council Of The Institute ofnewspaper and partners or Chartered Accountantsshareholders holding (More of Indiathan one per cent of the totalcapital)

I, ATIS BASU hereby declare that the particulars given aboveare true to the best of myknowledge and belief.Date: 27th March 2013 Signature of Publisher

date of the stay order would seem to be unconstitutional, inas much as, the appellant cannot be faulted for any delay onthe part of the CESTAT.III Disposal of appeal involving amounts upto Rs. 50 lacs

by Single member bench of CESTATIN what could be seen as a major development in terms ofhandling of appeals by the CESTAT Benches, Section 129Cof the Customs Act, 1962 is proposed to be amended to allowSingle Members of the CESTAT Benches to dispose of,appeals, involving amounts of up to Rs 50 lakhs, as againstthe current limit of Rs 10 lakhs, except in cases involvingdisputes related to classification or valuation of goods orservices. As we know, Section 129C has been made applicableto central excise appeals in terms of Section 35D of the CentralExcise Act, 1944.IV FM addresses issue of bailability - 6 offences made

non-bailable under indirect taxesTHE Offences under the Customs Act and the Central ExciseAct were treated as non-bailable till October, 2011 when theApex Court in the case of Om Prakash (2011-TIOL-95-SC-CX-LB) held that the offences under both these acts are bailable.This led to serious erosion of the enforcement ability of theRevenue Machinery.These proposed non-bailable offences are:

Customs Act(a) evasion or attempted evasion of duty exceeding fifty lakh

rupees; or(b) prohibited goods notified under section 11 which are also

notified under sub-clause (C) of clause (i) of sub-section(1) of section 135; or

12 HrsCPE

Fees1000/-

Registration for Seminars will be done on first cum first serve basis. Members arerequired to contact below for registration. The cheque shoud be drawn in favour of‘The Institute of Chartered Accountants of India-EIRC’

The Institute of Chartered Accountants of India, ICAI Bhawan,7, Anandilal Poddar Sarani (Russell Street), Kolkata – 700071

Ph- 30211104,33,34 Mob: 9674073910, 9831384972Email : [email protected], [email protected]

SEMINAR ON SERVICE TAXOrganized by

EASTERN INDIA REGIONAL COUNCIL, ICAIOn

Friday 19th & Saturday 20th April, 2013Venue: Vidya Mandir,Kolkata

Time : 10am to 5 pm

Topics1. Reverse Charge Mechanism 2. Various New Provisions affecting CAs3. Definition of Service - Concept of

negative list 4. Cenvat Credit5. Valuation of Bundled Service 6. Declared list of Services7. Latest Ammendments with respect 8. How to deal with Departmental

to Penalty and Prosecution Enquiry & AuditSpeakers

1. CA Ashok Batra, New Delhi 3. CA Rajesh Kumar T.R, Bangalore2. CA Madhukar Hiregange, Bangalore 4. CA J.K.Mittal, New Delhi

(c) import or export of any goods which have not been declaredin accordance with the provisions of this Act and the marketprice of which exceeds one crore rupees; or

(d) fraudulently availing of or attempt to avail of drawback orany exemption from duty provided under this Act, if theamount of drawback or exemption from duty exceeds fiftylakh rupees, shall be non-bailable.

Central Excise Act(e) The offences relating to excisable goods where the duty

leviable exceeds fifty lakh rupees and is punishable underclause (b) {evasion of duty} or clause (bbbb) {wrongfulavailment of Cenvat Credit} of sub-section (1) of section 9,shall be cognizable and non-bailable.

Service Tax(f) failure to pay any amount {in excess of Rs 50 lakhs}

collected as service tax to the credit of the CentralGovernment beyond a period of six months shall becognizable offence.

V. Holdingmoney for or on account of a defaulter, thetaxman can knock your doors too for recoverySECTION 11 of the CEA, 1944 is being amended so as toprovide for -

(i) Recovery of money due to the Government from any personother than from whom money is due after giving a propernotice, if that other person holds money for or on accountof the first person;

(ii) The other person to whom such notice has been issuedis bound to comply and

(iii) If the other person to whom the notice is served fails tocomply, he shall face all the consequences under thisAct.

11EIRC Newsletter | March 2013 Volume 39 | Issue No. 02

1. Whether the Assessees are entitled to the benefit ofimmunity arising out of Explanation-5 to Section271(1)(c ) of the Income Tax Act (CIT, Central-I/Kolkatavs. Amardeep Singh Dhanjal [ITA No. 39 of 2010] (CalcuttaHigh Court)]).Whether the assessee would have disclosed the incomeor would not have disclosed the income had the searchnot been conducted is not a question which falls for ourdetermination. The question for determination is whetherthe Tribunal was right in allowing the immunity underExplanation-5 to Section 271 of the Income Tax. All therequirements of the clause quoted above were met by theassessee and, therefore, the Tribunal took the correct viewof the matter in allowing the immunity and upholding theview of the Commissioner of Income Tax appeals and settingaside the order of penalty passed by assessing officer.

2. Whether the seized cash could be adjusted against aliability which arose subsequent thereto (CIT, Central-III vs. M/S. BLB securities (P) LTD. [ITAT 274 of 2012 &GA 3245 of 2012 (Calcutta High Court)]).If the seized cash can be adjusted against an existingliability, there is no reason why the seized cash cannotbe adjusted against a liability which arose in futurebecause in that case the seized cash would amount tosome sort of advance payment.Comment: The case law has been proposed to berendered ineffective vide Finance Bill, 2013.

3. Whether the order of the Appellate Authority was badbecause it violated Rule 46A of the Income Tax Rulesin allowing the assessee an opportunity for adducingadditional evidence (CIT, Kolkata-II vs. M/S. PrudentialEquity Fund Ltd. [ITAT No. 251 of 2012 & GA No. 3078 of2012 (Calcutta High Court)]).The aforesaid order passed by the ITAT allowing theassessee to file additional evidence before the AppellateAuthority was not challenged by the department.Therefore, that order became final. Based on suchpermission, the assessee adduced additional evidenceand got the relief from CIT(A) which has been upheld bythe Tribunal. Department is now aggrieved and is seekingto raise the point as regards violation of Rule 46A. Thissubmission can no longer be countenanced because noobjection was taken at the appropriate time.

4. Whether the addition of 1% of dividend income u/s14A of the Income-tax Act is proper when the assesseedid not show any expenditure incurred by him for thepurpose of earning exempted income (CIT, Kolkata-IV vs. M/s. R. R. Sen & Brothers (P) Ltd. [GA No. 3019of 2012 & ITAT No. 243 of 2012 (Calcutta High Court)]).The assessee did not show any expenditure incurred byhim for the purpose of earning the money which isexempted under the income tax.

RECENT JUDICIAL PRONOUNCEMENTS (DIRECT TAX)CA. Manoj K Tiwari

The Tribunal has computed expenditure at 1 per cent ofsuch dividend income which, according to them, is thethumb rule applied consistently. We find no reason tointerfere.

5. Strict guidelines issued to end Dept’s TDS credit &refund adjustment harassment (Court on its ownmotion vs. CIT [Writ Petition No. 2659/2012 (Delhi HighCourt)])(i) Re Uploading of wrong or fictitious demand: The

CBDT has accepted that incorrect and wrong demandshave been uploaded on the CPC arrears portal. In hisletter dated 21.08.2012, the CIT, CPC, has expressedhis concern and anguish on account of uploading ofincorrect and wrong data in the CPU and the problemfaced by them and by the assesses. To ensuretransparency (and accountability), a register must bemaintained with details and particulars of eachapplication made u/s 154, the date on which it wasmade, date of disposal and its fate. The Sec. 154application has to be disposed of by a speaking orderand communicated to the assessee. There must befull compliance of the said requirements;

(ii) Re Adjustment of refund contrary to Section 245:Sec. 245 postulates two stage action; first a priorintimation to the assessee and then, if warranted, thesubsequent adjustments of the refund towards arrears.This is not being followed by the CPC because thecomputer itself adjusts the refund due against theexisting demand. To prevent this breach of the law, thedepartment must follow the procedure prescribed u/s245 and give the assessee an opportunity to file a replywhich should be considered by the AO before givingthe direction for adjustment. As regards the cases wheresuch (illegal) adjustment has been made in the past,the cases must be transferred to the AOs for issue ofnotice to the assessee seeking adjustment of refund.False uploading of past arrears and failure to follow themandate of Sec. 245 is a lapse on the part of the AO;

(iii) Re non-communication of adjusted Section 143(1)intimations: The non-communication of Sec. 143(1)intimations, where adjustments on account of rejectionof TDS or tax paid has been made is a matter of graveconcern. When there is failure to dispatch theintimation within a reasonable time to the assessee,the return shall be deemed to have been acceptedand the intimation will be treated as non est or invalidfor want of service. The onus to show that the orderwas served on the assessee is on the Revenue andnot upon the assessee. If a TDS or tax credit claimhas been rejected on a technicality but there is nocommunication to the assessee of the order/intimationu/s 143(1), the AO cannot enforce the demand createdby the said order/intimation;

12EIRC Newsletter | March 2013 Volume 39 | Issue No. 02

(iv) Re non-grant of credit for TDS: The problemregarding rejection of TDS credit is in two categories.The first is those where the deductors fail to uploadthe correct particulars of the TDS which has beendeducted and paid and the second is where there is amismatch between the details uploaded by thedeductor and the details furnished by the assessee inthe ROI. The CBDT must re-examine this aspect andtake suitable remedial steps if they feel thatunnecessary burden or harassment will be caused tothe assessees. As regards cases of mismatchbecause of different methods of accounting, or offeringincome in different years, the department must takeremedial steps and ensure that in such cases TDS isnot rejected on the ground that the amounts do nottally. The AO must use his power and authority toensure that the deductor complies with the law.

6. Explanation to Section 37(1): No disallowance forcompensatory payments (CIT-9 vs. Regalia ApparelsPvt Ltd [ITA No. 88 of 2013 (Bombay High Court)]).The assessee took a business decision not to honour itscommitment of fulfilling the export entitlement in view of lossbeing suffered by it. The genuineness of the claim ofexpenditure being for business purpose is not disputed. Theassessee has not contravened any provision of law and theforfeiture of the bank guarantee is compensatory in natureand does not attract the Explanation to Sec. 37(1).

7. Rule 8D(2)(ii) & (iii) do not apply to shares held asstock-in-trade (DCIT vs. Gulshan Investment Co. Ltd.[ITA No. 666/Kol/2012 (ITAT Kolkata)] )Though Sec. 14A applies to shares held as stock-in-trade,Rule 8D (2)(ii) & (iii) cannot apply if the shares are heldas stock-in-trade because one of the variables on thebasis of which disallowance under rules 8D(2)(ii) & (iii) isto be computed is the value of “investments, income fromwhich does not or shall not form part of total income”. Ifthere are no such “investments”, the rule cannot haveany application. When no amount can be computed underthe formula given in rule 8 D(ii) and (iii), no disallowancecan be made under rule 8D (2)(ii) & (iii) either. As held inB. C. Srinivas Shetty 128 ITR 294 (SC), when thecomputation provisions fail, the charging provisions cannotbe applied, and by the same logic, when the computationprovisions under rule 8 D (2) (ii) and (iii) fail, disallowancethere under cannot be made either as the said provisionis rendered unworkable. However, this does not excludethe application of rule 8 D(2)(i) which refers to the “amountof expenditure directly relating to income which does notform part of total income”. Accordingly, in a case whereshares are held as stock-in-trade and not as investments,the disallowance even under rule 8 D is restricted to theexpenditure directly relatable to earning of exempt income.The result is that the scope of disallowance under Rule8D is narrower than that of Sec. 14A.

8. No Section 271(1)(c) penalty if income not offered totax due to “inadvertent mistake” (CIT-I, Mumbai vs.M/s Bennett Coleman & Co. Ltd. [ITA No. 2117 of 2012(Bombay High Court)])The assessee claimed deduction/ exemption of interest

on tax-free bonds of Rs.5.60 crores. When the AO askedthe assessee to give details of the interest on tax-freebonds, the assessee stated that it had inadvertently treatedtaxable interest of Rs. 75 lakhs as being tax-free and offeredthe said sum to tax. The AO levied penalty u/s 271(1)(c)for concealment of income/ filing inaccurate particulars ofincome. This was upheld by the CIT(A) though deleted bythe Tribunal on the ground that there was an “inadvertentmistake” by which the taxable bonds were classified astax-free and that there was “no desire” on the part of theassessee to hide or conceal its income so as to avoidpayment of tax on interest from the bonds. On appeal bythe department, HELD dismissing the appeal:‘The decision of the Tribunal is based on finding of factthat there was an inadvertent mistake on the part of theassessee in including the interest received of 6% on theGOI Capital Index Bonds as interest received on tax freebonds. It is not contended by the Revenue that abovefinding of fact by the Tribunal is perverse. In thesecircumstances, there is no reason to entertain theproposed question’.

9. Section 14A & Rule 8D: Expense specifically relatableto taxable income cannot be disallowed (JCIT vs.Pilani Investment & Industries Corpn. Ltd. [ITA No.653/Kol/2012(ITAT Kokatta)])Once it is found that an expense is specifically relatable toa taxable income, no portion of such an expense can bedisallowed u/s 14A. The allocation of general expensesvis-à-vis tax exempt income and taxable income can onlybe made in respect of expenditure which cannot either bewholly allocated to taxable income, then or which cannotbe wholly allocated to tax exempt income; the allocationcan be made, even on the basis of formula set out in Rule6D (iii) (should be Rule 8D (2)(iii)), in respect of suchexpenses which do not fall within any of these categories.

10. Compensation to CA Firm for loss of referral work isa non-taxable capital receipt (Khanna and Annadhanamvs. CIT [ITA No. 1286 of 2008(Delhi High Court)])On appeal by the assessee to the High Court HELDreversing the Tribunal:(i) There is a distinction between the compensation

received for injury to trading operations arising frombreach of contract and compensation received assolatium for loss of office. The compensation receivedfor loss of an asset of enduring value would be regardedas capital. If the receipt represents compensation forthe loss of a source of income, it would be capitaland it matters little that the assessee continues to bein receipt of income from its other similar operations(Oberoi Hotel & Kettlewell Bullen followed);

(ii) When that source was unexpectedly terminated, itamounted to the impairment of the profit-makingstructure or apparatus of the assessee. It is for thatloss of the source of income that the compensationwas calculated and paid to the assessee. Thecompensation was thus a substitute for the sourceand the Tribunal was wrong in treating the receipt asbeing revenue in nature”.

13EIRC Newsletter | March 2013 Volume 39 | Issue No. 02

1. Service Tax liability in case of mobilization advancesbetween two periods having different service taxrates(M/s Shapoorji Pallonji & Company Ltd Vs CST [2012-TIOL-1891-CESTAT- AHM])The Appellant was receiving mobilization advances fromclients and discharging service tax at the rate applicable.But at the time of raising running bills for services performedthe rate of service tax being reduced, the appellant adjustedthe same with service tax already paid at higher rate. TheHon’ble CESTAT hearing the stay petition has ordered apre deposit as the case of mobilization advance needs tobe detailed at the time of final hearing.

2. Determination of eligibility of Credit on Capitalgoods[CCE, Surat vs M/s Aneri Construction (2013-TIOL-477-CESTAT-AHM)]In this case, the Revenue went in to the appeal seekingdenial of Cenvat credit claimed on capital goods purchasedbefore the time the service itself become taxable. TheHon’ble Tribunal noted that CENVAT credit eligibility is tobe determined with reference to the taxability of the serviceon the date of receipt of capital goods. In the given case‘Commercial & Industrial Construction Service (PipelineService)’ was notified as taxable service under FA, 1994only on 16/06/2005 as such credit of capital goods viz. Aircompressor bought on 05/05/2005 cannot be claimed bythe assessee. Hence, the revenue appeal was allowed.

3. Duty hike proposed in Finance Bill- date of Effectwhen declaration under PCTA silent( Ultratech Cementv Commissioner[2013 (288)E.L.T. 438 (Tri- Kolkata)]Imposition or increase in duty through amendments byFinance Bill in the absence of declaration under ProvisionalCollection of Taxes Act, 1931 (PCTA) will not be effectiveimmediately. In this case, the department demanded dutyon Portland Pozzolana Cement for the intervening periodbertween the date of introduction of the Bill and itsenactment. The declaration under PCTA including theclauses in the Finance Bill which take immediate effectdid not mention the relevant clause on tariff change inrespect of the said item. It was therefore held that theeffective date of enhancement of duty would be date ofenactment and that no duty was payable for the interveningperiod.

4. Payment of service tax by contractor would notabsolve the liability of the builder- pre deposit of ‘ 50lacs ordered ( M/s. Cotton City Developers Pvt. Ltd. vsCCE (ST), Coimbatore [2013-TIOL-427-CESTAT-MAD]In this case, the developers were paying service tax oncontraction of complex service. However, on scrutiny oftheir service tax returns it was noted that the Appellanthad stopped payment of service tax for the period October2006 onwards. Thus, demand was raised for the periodJuly 2006 to September 2009 on the Appellants. TheAppellants contested that they had engaged contractorsfor the purpose of construction who have paid service tax.But the Hon’ble Tribunal held that such activity is only aninput service for providing the services rendered by theAppellants to the individual buyers of undivided share inland, for construction of the flats. Thus, a pre deposit wasordered.

5. Rule 6(1) of the Cenvat Credit Rules cannot be readin isolation. Plea of the appellant that they havemanufactured exempted goods in the nature of pipesas well as dutiable goods in the nature of scrapandthereby benefit of Rule 6(3) should be afforded to themrejected and differential demand confirmed (M/s.Ratnamani Metals and Tubes Ltd. Vs. CCE, Ahmedabad[2013-TIOL-432-CESTAT-AHM])In this case, the Appellant had availed credit of inputsused in manufacture of exempted goods after paying dutyto the tune of 8% on the value of exempted goodsmanufactured. The Revenue was of the view that the caseof the Appellant was not covered under Rule 6(3) of theCCR but it was squarely falling within the ambit of Rule6(1) of the CCR which demanded full reversal of the crediton inputs used in manufacture of exempted goods only.The Appellant contested the same by bringing in thecontention that they had manufactured dutiable scrap alsoand hence benefit of Rule 6(3) should not be denied tothem. The Tribunal held that since merely some wastearose and the same was cleared on payment of duty doesnot mean that both, dutiable and exempted goods werebeing manufactured out of the common input. Thus Rule6(1) of the CCR to be applicable and thereby the appealwas rejected by confirming the differential duty demand.

6. Benefit of interpretation of exemption notification tobe awarded to assessee. Penalty under Section 77and 78 of the Finance Act, 1994 not imposable. ( CCE,Indore Vs. M/s Jas Enterprises [2013-TIOL-440-CESTAT-DEL])Here, the Revenue went to the Hon’ble Tribunal beingaggrieved by the order passed by the Comr (Appeals) bywhich demand for service tax was dropped on the groundof interpretation of an exemption notification. The Hon’bleTribunal while allowing the appeal of the Revenue to theextent of confirmation of demand of duty and interestthereon against the respondents and dropping the penaltyheld that the complexity of the Notification which hasalready resulted in passing of a favourable order byCommissioner (Appeals), cannot be understood by acommon personnot very well conversant with the legalinterpretations. Commissioner (Appeals) being an appellateauthority has interpreted the Notification in favour of theassessee. We are of the view that when an expert officerhimself interprets the Notification in such a manner so asto extend the benefit to the assessee, no faults can befound on the part of the assessee to understand the law inthat particular manner. Thus, penalty under section 77 and78 of the Finance Act, 1994 is not imposable.

7. Cenvat Credit on capital goods used by a job workeravailing benefit of Notification No. 214/86- CE (M/sGaruda Cotex Shades Ltd. Vs CCE[2012-TIOL-1721-CESTAT-AHM])In this case, the Tribunal held that if an assessee isfunctioning under Notification No. 214/86-CE and if theultimate principal manufacturer is discharging CentralExcise Duty liability after consumption of job worked goods,it has to be held that the said notification does not exemptthe goods manufactured on job work by the assessee,there cannot be denial of cenvat credit of central exciseduty paid on the capital goods.

RECENT JUDICIAL PRONOUNCEMENTS (INDIRECT TAX)CA Ankit Kanodia

14EIRC Newsletter | March 2013 Volume 39 | Issue No. 02

A. DIRECT TAXESCompiled By CA. Debayan Patra

1. Interest rate on Small SAVING Scheme reduced by0.1% above 2 yrs time deposit w.e.f 01.04.2013(pressrelease on 25.03.2013)

2. Director, Financial Intelligence Unit India (FIUIND),MOF will be considered for Sec 138(1)(a)(ii) of the ITAct, 1961. ( NOTIFICATION NO. 19/2013 [F. NO. 225/38/2013-ITA. II], DATED 12-3-2013

3. Jurisdiction of Commissioner of Income Tax, CPC (TDS)notified by The Central Board of Direct Taxes to comeinto force from the date of its publication in the Offi-cial Gazette ( NOTIFICATION NO. 17/2013 [F. NO. 187/5/2013-ITA-I]/SO 461(E), DATED 26-2-2013 )

4. Director General of Income-tax (Systems) having hisheadquarters at New Delhi shall exercise the powersand perform the functions in respect of such cases orclasses of cases, in respect of which the Commissionerof Income-tax , Centralised Processing Cell (TDS) hasjurisdiction vested in him ( NOTIFICATION NO. 16/2013[F.NO. 187/5/2013-ITA-I]/SO 462(E), DATED 26-2-2013 )

5. Commissioner of Income-tax, Centralised ProcessingCell (TDS) shall be subordinate to the Director Gen-eral of Income-tax (Systems) ( NOTIFICATION NO. 15/2013 [F.No.187/5/2013-ITA.I]/460(E), DATED 26-2-2013)

B. SERVICE TAXCompiled by : CA Ankit Kanodia

1. Abatement for luxury flats reduced to 70% byamending notification No. 26/2012 (Notification no. 02/2013-ST dated 01.03.2013 w.e.f. 01.03.2013)

2. Mega exemption notification no. 25/2012 makenecessary amendments in the specified entriestherein. (Notification no. 03/2013-ST dated 01.03.2013w.e.f. 01.04.2013)

3. Residential Public Limited Company made eligiblefor Advance Ruling under Service tax(Notification no.04/2013-ST dated 01.03.2013 )

4. Central Board of Excise & Customs extends the dateof submission of the Form ST-3 for the period from1st July 2012 to 30th September 2012, from 25th March,2013 to 15thApril, 2013.( Order No. 01/2013-ST dated06.03.2013)

5. Service Tax Returns for the period 1st July-30th Sept 2012isnow available in a modified format for efiling in ACES. Onlyoffline version is available and there is no online version( for details visit www.aces.gov.in)

NOTIFICATIONS AND CIRCULARSC. CENTRAL EXCISE

1. Amends Notification No.17/2007-CE dated 1.3.2007 toincrease compound levy rate of stainless steel patties’pattas from Rs.30,000 to Rs.40,000 per cold rollingmachine per month (notification no. 05/2013-CE dated01.03.2013 )

2. Rescinds Notification No. 20/2011-CE dt. 24.03.2011specifying duty @1% on mobile phones(notification no.06/2013-CE dated 01.03.2013 )

3. Amends Notification No. 7/2012 dt. 17.03.2012-prescribing 6% excise duty for branded readymadegarments of cotton not containing any other textilematerials. (notification no. 08/2013-CE dated 01.03.2013)

4. Amends Notification No. 1/2011-CE dt. 1.03.2011 (duty@ 2%) omitting certain entries like handmade carpets,ships, tugs, vessels, which are now fully exempted.(notification no. 09/2013-CE dated 01.03.2013 )

5. Amends Notification No 49/2008 CE(NT) dated24.12.2008 - Medicaments exclusively used inAyurvedic, Unani, Siddha, Homeopathic systems andsold under a brand name brought under MRPassessment (notification no. 01/2013-CE(NT) dated01.03.2013 )

6. CE Rules amended to restrict interest on refund onfinalization of provisional assessment. (notification no.02/2013-CE(NT) dated 01.03.2013 )

7. Amends CENVAT Credit Rules, 2004 to provide forrecovery of amounts payable on inputs/capital goodscleared as such. (notification no. 03/2013-CE(NT) dated01.03.2013 )

8. Resident Public Limited Company made eligible forAdvance Ruling. (notification no. 04/2013-CE(NT) dated01.03.2013 )

D. CUSTOMS1. Amends Notification No. 9/2012-Cus dt. 9.03.2012- Cut

and polished diamonds to variation limitchanged.(notification no. 11/2013-Cus dated 01.03.2013)

2. Rescinds Notification No. 19/2012-Cus and 20/2012 bothdt. 17.03.2012- relating to exemption to dredgers.(notification no. 13/2013-Cus dated 01.03.2013 )

3. Amends Notification No. 146/94-Cus. Dt. 13.07.1994-Trophies imported by sports bodies exempted.(notification no. 14/2013-Cus dated 01.03.2013 )

4. Amends Notification No. 27/2011-Cus dt. 1.03.2011- Rawsugar, Rice bran oil cake, exempted from export duty-10% export duty on bauxite and ilmenite (processedilminite @ 5%).(notification no. 15/2013-Cus dated01.03.2013 )

5. Import of Hot rolled flat products of Stainless steelseries 300 from PR China – submission date of finalfindings on safeguard investigation extended up to25/05/2013. (notification no. 24/2013-Cus(NT) dated26.02.2013 )

6. Amends Baggage Rules, 1998 - duty free jewellerylimit enhanced to Rs 50,000/- and Rs 1,00,000/-

15EIRC Newsletter | March 2013 Volume 39 | Issue No. 02

respectively for gents and ladies. (notification no. 25/2013-Cus(NT) dated 01.03.2013 )

7. Govt lowers tariff value of gold & silver and also RBDPalmolein(notification no. 26/2013-Cus(NT) dated01.03.2013 )

8. CBEC amends rules of Origin of Goods for SAFTA(notification no. 27/2013-Cus(NT) dated 01.03.2013 )

9. CBEC notifies Customs Exchange Rates w.e.f08.03.2013 (notification no. 28/2013-Cus(NT) dated06.03.2013 )

10.Customs - Tariff Values of Gold, Silver & oilsreduced(notification no. 30/2013-Cus(NT) dated15.03.2013 )

11.CBEC notifies Customs Exchange Rates w.e.f22.03.2013(notification no. 31/2013-Cus(NT) dated21.03.2013 )

12.Information as regards norms for Execution of BankGuarantee in respect of Advance Authorization (AA) /Duty Free Import Authorization (DFIA) / ExportPromotion Capital Goods (EPCG)Schemes– (Circularno. 08/2013-Cus dated 04.03.2013 )

13.Information as regards Post Export EPCG duty creditscrip(s) Scheme and certain other changes related toForeign Trade Policy 2009-14(Circular no. 10/2013-Cusdated 06.03.2013 )

14.Information as regards Setting up of Public/PrivateBonded Warehouses for Gems & Jewellery Sector(Circular no. 11/2013-Cus dated 06.03.2013 )

E. FOREIGN TRADECompiled by : CA Kushal bhuwania

1. Export of Set Top Box/ Set Top Unit to attract reward/incentive of 5% under the Focus Product Scheme–(P.N no. 51 dtd 05/03/2013)

2. Import of Personal computer/laptops, photocopymachine, air conditioning machine all in SecondHand condition would require Import Authorisationas they are restricted items for import – (Notificationno. 35 dtd 28/02/2013)

3. Import of Used Rail including Cut Rail of all lengthsis ‘free’ subject to the Pre-inspection condition –(Notification no. 36 dtd 28/02/2013).

4. TED refund should not be provided by R.A of DGFTor by office of Development Commissioner in caseswhere supplies are ab-initio exempted from paymentof excise duty- (Policy Circular No. 16 dtd 15/03/2013)

F. CORPORATE LAW UPDATECompiled by CA. Ankita Agrawal,

[email protected]. Clarification for tax free government bonds authorized

under Union Budget 2013-14(General Circular No. 06/2013 dated 14/3/2013)

2. Relaxation of additional fees and extension of lastdate of submission of various forms(Circular No. 07/2013 dated 20/3/2013)

The Ministry of corporate affairs has extended the time limit ofdate filling of various forms till 31.3.2013 and has also relaxedthe additional fees thereon.The types on forms on which such relaxation has been givenare as under –(i) Wherein the due date for filling of forms was before

17.1.2013, the extended due date has been revised till31.3.2013 with an increase in additional fees for the periodof 17.1.2013 to 28.2.2013.

(ii) Wherein documents have expired on 17.1.2013 due to non-submission/ re-submission, the PUCL will be restored back.Tickets raised till 24.3.2013 will be valid for the period giventherein and users will be given a time of 7 days of intimationto file the documents.

This relaxation is only for fees payable on or after 17.1.2013.Fees payable till 16.1.2013 will remain payable.3. Amendment to Companies (Acceptance of Deposit)

Rules, 1975 (Notification dated 21.3.2013)Rule 2(b)(x) of the said rules excludes bonds and debenturesfrom the definition of deposits if the same is secured bymortgage of any immovable property. The said amendmentsubstitutes the words ‘fixed assets referred to in Schedule VIof the Act excluding intangible assets’ as against the words‘immovable property’.Therefore, bonds and debentures mortgaged against movablefixed assets are now also excluded from the definition ofdeposits.Also, the authority to file complaints under section 58AAA(2)has now been extended to the Registrar of Companies andany other officer of the Central Government.4. Companies Directors Identification Number

(Amendment) Rules 2013 (Notification dated 15.3.2013)In the Companies (Directors Identification Number) Rules,2006,after rule 7,the following rule shall be inserted, namely :Rule 8 - Cancellation or Deactivation of DIN.- The CentralGovernment or Regional Director (Northern Region), Noida orany officer authorised by the Regional Director, upon beingsatisfied on verification of particulars of proof attached withthe application received from any person seeking cancellationor deactivation of DIN, in case -(a) the DIN is found to be duplicate;(b) the DIN was obtained by wrongful manner or fraudulent

means;(c) of the death of the concerned individual;(d) the concerned individual has been declared as lunatic by

the competent Court;(e) if the concerned individual has been adjudicated an

insolvent;then the allotted DIN shall be cancelled or deactivated bythe Central Government or

Regional Director (NR), Noida or any other officer authorisedby the Regional Director (NR): Provided that before cancellationor deactivation of DIN under clause (b), an opportunityof being heard shall be given to the concerned individual.

16EIRC Newsletter | March 2013 Volume 39 | Issue No. 02

17EIRC Newsletter | March 2013 Volume 39 | Issue No. 02

Empanelment as a Technical Reviewer with theQuality Review Board

The Government of India has, in exercise of the powersconferred by Sec. 28A of the Chartered Accountants Act,1949, constituted a Quality Review Board to perform thefollowing functions:-

(1) to make recommendations to the Council with regardto the quality of services provided by the members ofthe Institute;

(2) to review the quality of services provided by themembers of the Institute including audit services; and

(3) to guide the members of the Institute to improve thequality of services and adherence to the variousstatutory and other regulatory requirements.

(4) Now, with a view to continue to carry out the work ofreview of quality of audit services of auditors/audit firmsin India, the Quality Review Board has decided to issuea revised announcement seeking the services ofmembers of the Institute to function as TechnicalReviewers for the Board in terms of the aforesaidProcedure for Quality Review of Audit Services of AuditFirms issued by it. A suitable amountranging uptoRs. 1 lakh or above, as may be fixed by the QualityReview Board depending upon the nature of workinvolved, may also be paid as honorarium. Thoseinterested may kindly apply in the revised‘Application Form for Empanelment as a TechnicalReviewer’ (available at its website http://www.qrbca.in).

EIRC DEEPLY MOURNS THE SAD DEMISE OF ...

We pray to the Almighty ‘May their soul rest in peace’

CA Om Prakash Goenka(Mem No – 013635 )Left us on 06.12.2012

CA Saibal Bhattacharyya(Mem No – 057811 )Left us on 13.01.2013

CA Binay Bhusan Das(Mem No – 016618 )Left us on 06.02.2013

CA Anil Kr ChattopadhyayPast Chairman (EIRC 1957-58)

(Mem No – 001332 )Left us on 06.02.2013

CA Dilip Chakraborty(Mem No – 015705 )Left us on 12.02.2013

Opportunity with Garden Reach ShipBuilders & Engineers Ltd.

Applications are invite from CA Firms from Kolkata forcarrying out inventory verificationn exercise forCompany’s units located in Kolkata. Advertisement anddetails fro the above are available on the company’swebsite- www.grse.nic.in under ‘Applications Invitedsection, on and from 18.03.2013 . Last date forsubmission of applications is 02.04.2013 (14.00hrs); Bidsto be opened on 02.04.2013 at 15.00hrs. Details alsoavailable at EIRC website – www.eircicai.org.

EMPANELMENT OPPORTUNITY

Opportunity with Kolkata Port Trust

Applications are invited from professionals possessingqualification of Chartered Accountant / Cost Accountant/ Company Secretary for engagement of 8 (eight) no. ofAccounts / Audit Officers on contractual basis.

The selected candidate will be paid a fixed consolidateremuneration package of Rs 25,000 per month for KolkataDock System and Rs 38,500/- per month for Haldia DockComplex.

Applications (Hard copy) giving detailed bio-data withrecent passport size photograph & self attestedphotocopies of relevant certificates / testimonials fromthe willing candidates (25 – 62 Yrs of age) should reachthe office of the

Financial Adviser & Chief Accounts Officer at 15, StrandRoad, Kolkata – 700001 latest by 19th April 2013.

For further details please visit EIRC Websitewww.eircicai.org (Announcement)

18EIRC Newsletter | March 2013 Volume 39 | Issue No. 02

IT TRAINING AT DURGAPURBRANCH OF EIRC OF ICAI

Durgapur Branch of EIRC of ICAI has started anInformation Technology Training Class of 100hours at branch premises. Interested Studentsare requested to register their name with DD ofRs. 4000.00 (Rs. Four Thousand Only) in favorof “ ICAI DURGAPUR BRANCH “ payable atDURGAPUR. Registration is based on first comefirst serve basis.

Contact : Mr. Ayan MazumdarMob No : 7679404754

WORK DISPOSAL STATUS LIBRARY NEWS

1 Tax Shasta,2012 Parthasarathi BS books New Delhi,Shome 2012

2 Ending Corruption? How N Vittal Penguin New Delhi,to clean up INDIA, 2012 Group 2012

3 Markets Never Forget Ken Fisher Wiley India New Delhi,2012

4 Social Versus Corporate Kevin Palgrave UK,Welfare, 2012 Farnsworth Macmillan 2012

5 Foreign Direct Investment, Shahid Routledge New Delhi,Trade & Economic Ahmed 2013Growth

6 Corporation 2020, Pavan Portfolio New Delhi,Transforming Business Sukhdev Penguin 2012for Tomorrow’s World,2012

7 Debt The First 5000 David Penguin New Delhi,Years Graeber Allen Lane 2012

8 The Global Economic Jayshree Academic New Delhi,Meltdown Sengupta Foundation 2012

9 Tata Log Harish Bhat Portfolio New Delhi,Penguin 2012

10 Central Excise Tariff R K Jain’s Centax New Delhi,of India Publications 2013

Pvt Ltd11 Central Excise Law R K Jain’s Centax New Delhi,

Manual Publications 2013Pvt Ltd

12 Customs Law Manual R K Jain’s Centax New Delhi,Publications 2013Pvt Ltd

For further enquiry please call Library at 3021103/05 or [email protected]/[email protected]

Sl. Place &No. Year

Some of the latest and useful addition to the EIRC Library

Title & Edition Author Publisher

MEMBERS SECTION

Work Disposal Status of various Activities Related as on 25th

March , 2013

1) New Enrolment (for 2012-13 ) 14/03/20132) Grant of Certificate of Practice 20/03/20133) Grant of Fellow Admission 20/03/20134) Firm Registration / Constitution 20/03/20135) Reconstitution of Firms 20/03/20136) Restoration 20/03/20137) Change of address 20/03/20138) Permission of other engagement 20/03/2013

ARTICLES SECTION

The position of action taken on various matters relating tomembers and students of EIRC as on 22/03/2013

PARTICULARS DATE

Industrial training Registration 25/02/2013Re-registration 25/02/2013Termination 25/02/2013Completion 20/03/2013Permission to Study 14/03/2013Supplementary Registration 25/02/2013Change of Address 18/03/2013

BOARD OF STUDIES SECTION - AS ON 25/03/2013

CPT REGISTRATION 19-03-2013IPCC REGISTRATION 19-03-2013FINAL REGISTRAION 01-03-2013

By hand By postIssuance of study materials - Upto date 13-02-2013CPTIssuance of study materials - Upto date 18-02-2013IPCCIssuance of study materials - Upto date 21-02-2013FINALGmcs certificate issuance Upto dateOrientation certificate issuance Upto dateITT certificate issuance Upto dateChange of name/address Upto date

“CA. Bharat D Sarawgee (M.No.061505) has been Appointedas Member, Investor GrievancesRedressal Committee (IGRC) ofthe Bombay Stock Exchange andUnited Stock Exchange atRegional Arbitration Centre atKolkata”.

member at helm

19EIRC Newsletter | March 2013 Volume 39 | Issue No. 02

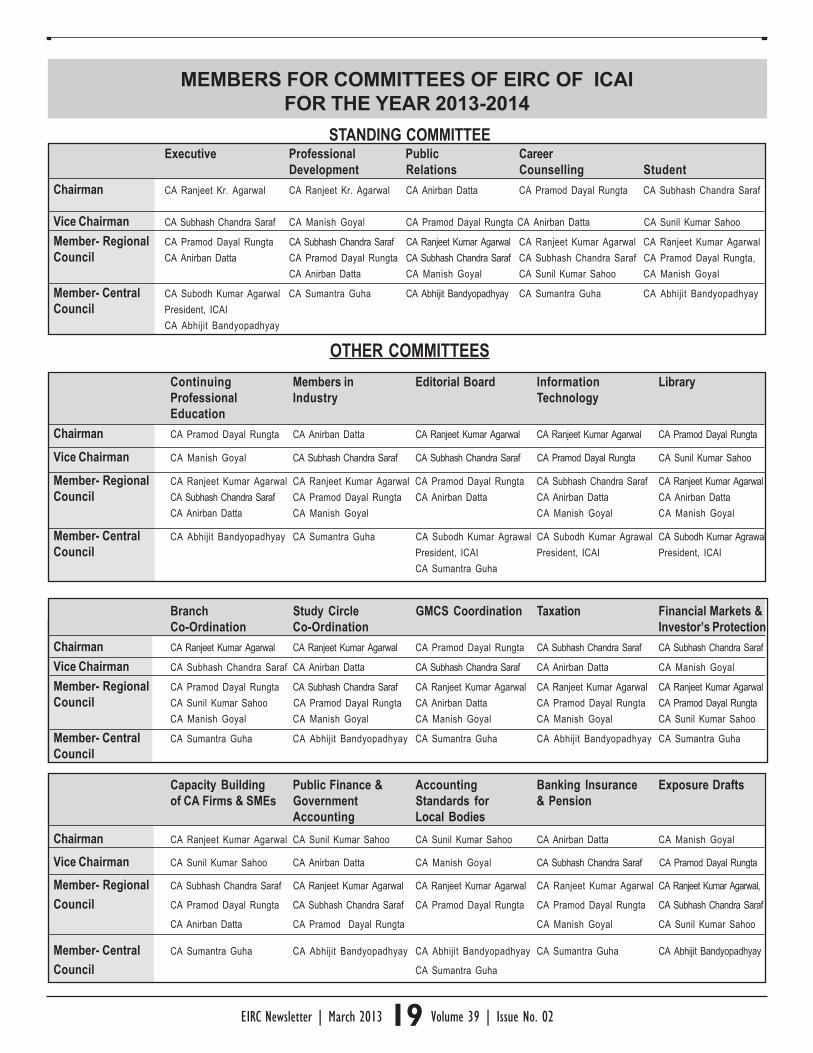

MEMBERS FOR COMMITTEES OF EIRC OF ICAIFOR THE YEAR 2013-2014

STANDING COMMITTEEExecutive Professional Public Career

Development Relations Counselling StudentChairman CA Ranjeet Kr. Agarwal CA Ranjeet Kr. Agarwal CA Anirban Datta CA Pramod Dayal Rungta CA Subhash Chandra Saraf

Vice Chairman CA Subhash Chandra Saraf CA Manish Goyal CA Pramod Dayal Rungta CA Anirban Datta CA Sunil Kumar Sahoo

Member- Regional CA Pramod Dayal Rungta CA Subhash Chandra Saraf CA Ranjeet Kumar Agarwal CA Ranjeet Kumar Agarwal CA Ranjeet Kumar AgarwalCouncil CA Anirban Datta CA Pramod Dayal Rungta CA Subhash Chandra Saraf CA Subhash Chandra Saraf CA Pramod Dayal Rungta,

CA Anirban Datta CA Manish Goyal CA Sunil Kumar Sahoo CA Manish Goyal

Member- Central CA Subodh Kumar Agarwal CA Sumantra Guha CA Abhijit Bandyopadhyay CA Sumantra Guha CA Abhijit BandyopadhyayCouncil President, ICAI

CA Abhijit Bandyopadhyay

OTHER COMMITTEESContinuing Members in Editorial Board Information LibraryProfessional Industry TechnologyEducation

Chairman CA Pramod Dayal Rungta CA Anirban Datta CA Ranjeet Kumar Agarwal CA Ranjeet Kumar Agarwal CA Pramod Dayal Rungta

Vice Chairman CA Manish Goyal CA Subhash Chandra Saraf CA Subhash Chandra Saraf CA Pramod Dayal Rungta CA Sunil Kumar Sahoo

Member- Regional CA Ranjeet Kumar Agarwal CA Ranjeet Kumar Agarwal CA Pramod Dayal Rungta CA Subhash Chandra Saraf CA Ranjeet Kumar AgarwalCouncil CA Subhash Chandra Saraf CA Pramod Dayal Rungta CA Anirban Datta CA Anirban Datta CA Anirban Datta

CA Anirban Datta CA Manish Goyal CA Manish Goyal CA Manish Goyal

Member- Central CA Abhijit Bandyopadhyay CA Sumantra Guha CA Subodh Kumar Agrawal CA Subodh Kumar Agrawal CA Subodh Kumar AgrawalCouncil President, ICAI President, ICAI President, ICAI

CA Sumantra Guha

Branch Study Circle GMCS Coordination Taxation Financial Markets &Co-Ordination Co-Ordination Investor’s Protection