Embed Size (px)

DESCRIPTION

1st National Bank Teller Newsletter 12

Citation preview

1st NatioNal BaNk's official Bi-MoNthly NewsletterIssue 12 • Jul/Aug 2011

The

Funny MoneyLighten up For a whiLe, spare

a MoMent For a chuckLe

THE VALUEOF HOME EQUITY

GET YOUR KEYSTO FINANCIAL

SUCCESS

1ST NATIONAL BANK PROUDLY ANNOUNCES THE OPENING OF OUR

FIFTH FULL SERVICE BRANCHWHAT'S INSIDE

the Big story

TELLER

HELLO ONCE AGAIN!

In this issue of the Teller we focus on the 1st National Bank’s la tes t n e t w o r k e xpan s i on . We are very proud to be se r v i ng t he communi t ies w i t h i n t h e v i c i n i t y o f

Choc from our newly opened

C h o c B a y Branch.

This new branch, brings to seven (7) our strategic locations in the marketplace and we have plans to continue branching out. 1st National Bank now serves Saint Lucia directly at Rodney Bay, Choc Bay , Castries, George FL Charles Airport, Ferry Terminal Faux-a-Chaux, Marigot and Vieux-Fort. Our bricks and mortar presence is supported by a full suite of SmartBanking services such as Mobanking, 1st Online Banking, our 1st Debit Card and seven (7) ATMS.

Our Bank’s decision to increase our physical presence across Saint Lucia is part of our strategy to meet our customers where they are. We understand the changing times and how these create shifts in consumer behaviour. Additionally, as the country’s Community Bank we see ourselves playing a critical role in the development of those communities and by association the Country.

We believe that we need to be in more places, serving more people, more often, more effectively. This is why we are the only financial institution with branches and sub branches opened on more days per week and delivering more hours of service.

Our dedicated staff share our vision and understand the needs of our cus tomers. They remain the backbone of the Bank and we remain appreciative of their hard work and loyalty. It is also opportune to commend the Team that has been directly involved in making the Choc Bay branch a reality.

I invite our customers, friends and potential clients from the environs of this new Choc Bay branch – Marisule,

Grande Riviere, Babonneau, Union, and Sunny Acres – to visit us to experience full service banking.

Our Drive-Up ATM is available every day and there is ample parking at all times. We look forward to seeing you!

Managing Director's Letter

G. Carlton GlasgowManaging Director

Bank branches are great! We all wish there was one in our living room sometimes. But with Online banking, ATMs and MoBanking at our finger-tips, why do we still love “going to the bank”? And, why would a Bank keep opening new branches in communities across the country?

Industry discussions raise that:Concerns have been voiced for some time about the high cost of branching and the potential over- branching of certain markets, especially with the availability of alternative banking technology. For example, a book published in 1996 predicted significant branch closings due to an increase in ATM, telephone, computer and direct deposit services, indicating that “The expense of maintaining bank branches has increased while the importance of branches to customers has declined.”

And yet, the same study later states:However, despite technological advances that have made it easier to conduct financial services activities without physically entering a bank branch, it seems that banking consumers like the convenience of bank branches. Surveys conducted recently indicate that the single most important factor influencing a customer’s choice of banks is the location of the institution’s branches.

This reality is strikingly reflected in new branch openings such as the recent branch in Choc serving the bustling and growing surrounding

communities. This branch is a perfect example of the bank recognising a need and moving to meet it with local knowledge, local experience and convenience in a branch that meets our customers where they are with what they need, yet every customer of this and every branch of 1st National Bank has access to the hottest and most convenient technology to make branch banking a supposed thing of a bygone era to be missed but easily replaced.

But a successful bank is not run by emotion and casual decision-making and much thought has gone into offering both the convenience of techno-banking, as well as the intimacy of the local branch network, and there are very valid reasons behind that.

Here's what the Richmond Fed wrote in its report on branch banking dated Aug. 4 2011:Unlike cars or groceries, loan products are special in that pricing them properly in low- and moderate-income areas may require an intimate knowledge of the community and its people. The lending market in these neighborhoods can fail without a lender with local experience; that is, some creditworthy people may not be able to get credit even if they travel to the next bank branch miles away. Thus, brick-and-mortar branches provide tangible benefits to consumers, especially in low- and moderate-income and developing neighborhoods. A physical bank presence leads to at least two measurable benefits: It makes it possible for creditworthy borrowers living there to obtain loans, and it leads to lower rates of default among them.

WIDENING THE BRANCH NETWORK costly brick and mortar, or good

local banking sense?

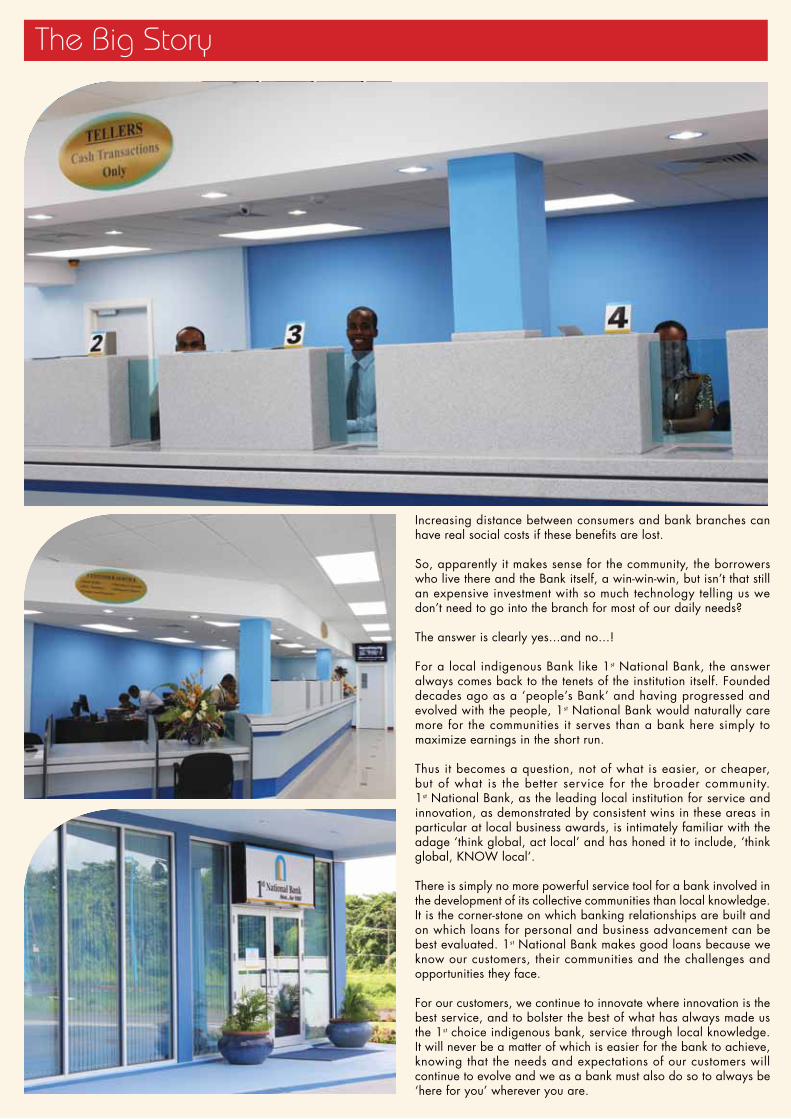

The Big Story

The Big Story

Increasing distance between consumers and bank branches can have real social costs if these benefits are lost.

So, apparently it makes sense for the community, the borrowers who live there and the Bank itself, a win-win-win, but isn’t that still an expensive investment with so much technology telling us we don’t need to go into the branch for most of our daily needs?

The answer is clearly yes...and no...!

For a local indigenous Bank like 1st National Bank, the answer always comes back to the tenets of the institution itself. Founded decades ago as a ‘people’s Bank’ and having progressed and evolved with the people, 1st National Bank would naturally care more for the communities it serves than a bank here simply to maximize earnings in the short run.

Thus it becomes a question, not of what is easier, or cheaper, but of what is the better service for the broader community. 1st National Bank, as the leading local institution for service and innovation, as demonstrated by consistent wins in these areas in particular at local business awards, is intimately familiar with the adage ‘think global, act local’ and has honed it to include, ‘think global, KNOW local’.

There is simply no more powerful service tool for a bank involved in the development of its collective communities than local knowledge. It is the corner-stone on which banking relationships are built and on which loans for personal and business advancement can be best evaluated. 1st National Bank makes good loans because we know our customers, their communities and the challenges and opportunities they face.

For our customers, we continue to innovate where innovation is the best service, and to bolster the best of what has always made us the 1st choice indigenous bank, service through local knowledge. It will never be a matter of which is easier for the bank to achieve, knowing that the needs and expectations of our customers will continue to evolve and we as a bank must also do so to always be ‘here for you’ wherever you are.

1st National Bank St. Lucia Limited, P.O. Box 168,#21 Bridge Street, Castries, St. LuciaTel: +758 455 7000 | Fax: + 758 453 1630Email: manager@1st nationalbankslu.comWebsite: www.1stnationalbankonline.com

1ST National Bank has been here for our local staff, their families and communities, sharing in their aspirations and giving them fertile ground on which to grow.We know that our customers are our neighbors and that our futures will always be tightly linked. Proud, bright futures, built on a history of performance and respect.

A HISTORY OF BUILDING FUTURES

Home GrownThrough a simple blessing by Father Michel Francis the newest branch of the 1st National Bank began its first year of business. It is located opposite the Caribbean Cinemas building at Choc Bay. The branch opening forms part of the carefully calculated expansion of St.lucia’s first indigenous bank, its products and services to the St.lucian public. Father Michel emphasized that Monday’s activity was to ensure a providential start to the Bank’s operations.

For the first part we want to show our gratitude because the Psalmist says that of the lord that if He does not build the labourers labour in vain. So our first action is one of gratitude for what God has given to us.

The new Choc Bay Branch offers all of the services that can be found at any other branch of 1st National Bank island wide including night deposit, 1st CashPoint 24-Hr ATM Services, plus the added convenience of Saturday opening from 8:30pm to 12 noon. Father

Michel also praised 1st National Bank for its demonstrated corporate social responsibility in the communities around St.Lucia.

“Certainly Kudos to 1st National Bank for really responding to initiatives that seek to help people develop. Anything that is encouraging you can expect 1st National Bank to make itself part of that. It is my pleasure to say that,” stated Father Michel.

The staff were grateful for yet another opportunity to serve the public.

“We want to also pray that we will be able to work as a team and that we will be able to give the bank and customers satisfaction in our duties,” claimed one staff member.

The Choc Bay is now open from 8:00am to 2pm Mondays to Thursdays and 8:00am to 5pm on Fridays.

Mega J

MegaPlex 8

Cas

trie

s -

Gro

s Is

let

Hw

y

ChocBay

Choc Round- about

Casties Gros Islet

Hw

yC

astie

s G

ros

Isle

t Hw

y

Cas

ties

Gro

s Isl

et H

wy

Casties Gros Islet Hwy

Sandals HalcyonBeach Resort

SagicorLife Inc

JQ MotorsLtd

Castries - Babonneau

Home Grown

Levern Looks to London 2012 wIth 1st nAtIonAL BAnk’s support.St.Lucia’s world class high jumper Levern Spencer has much to celebrate after qualifying for the summer Olympic games to be held in London next year. Levern last month cleared the qualifying mark of 1.92 meters, placing second in the rankings. This latest accomplishment continues to prove Levern’s worth as a national athlete and for this reason a special management committee has been formed to assist the high jumper. Manager Gregory Dickson says Levern has been steadfast in her quest to bring glory to St.Lucia.

“The goal was always to ensure that it would not be just a time for her to receive an education or to just go out there and participate in sports but to be out there on the international scene and to be one of those individuals that we would be viewing on television as we do with the Jamaicans and the Trinidadians, cheering for her.”- Gregory Dickson.

The management committee has launched a vigorous campaign dubbed “Levern London 2012”. The aim is to rally financial support for the St.lucian high jumper as well as technical and personal grooming to enhance Levern as a marketable sports celebrity. Committee member Rowston Taylor says Levern has worked hard enough under trying circumstances to deserve it.

“To the corporate entities and persons who have decided to do what is right, I thank you! Thank you on behalf of Levern, thank you on behalf of the next athlete who I hope will not have to endure what Levern has.”

Several corporate entities have given tangible support to the Levern London Campaign including 1ST National Bank.

“This is a new road, this is a new beginning and we accept along with our other sponsors and colleagues this new challenge because we take great pride in what Levern has become, we are overjoyed at what we see her doing and we are going to be with Levern all the way to London 2012.”

Levern for her part has welcomed the support.

“As a representative of my country for the past 13 unbroken years I must confess that it has not been all smooth sailing. There have been many potential pitfalls along the way. There were times when I felt like giving up. But I having surrounded my self with the right people and I having used my formula, I have kept on going today. I am glad I did continue!”

The High jumper who is ranked 7th in the world has also been given her own internet domain “levernspencer.com”

1st nAtIonAL BAnk shows Its support for the st. LucIA sIckLe ceLL AssocIAtIon

1st National Bank has committed to a three-year covenant with the St.lucia Sickle Cell Association. This week Bank representative Robert Fevrier paid a visit to the institution to check on its progress and to deliver another installment of its monetary support to president Paula Calderon.

“This morning I am pleased to be at the St. Lucia sickle cell association office and clinic to honor our commitment, the second installment of our 3 year covenant totaling $13,500. This morning on behalf the Board of Directors, management and staff of 1st National Bank St.Lucia limited I would like to present this cheque of $4500 to the St.Lucia Sickle Cell Association in support of all the good work they have been doing in St.Lucia.” –Mr. Robert Fevrier

In recent times the association has encountered several set backs including a long search for new headquarters and theft of equipment, computers and medical supplies. Donations like that of 1st National Bank help to sustain the daily operations vital to the health of people suffering from the sickle cell disease. President of the association Paula Calderon thanked 1st National Bank for its generosity.

“You are the only bank actually, that over the years has supported us through a covenant which gives us the ability to plan better and we would hope that at some time later on that more banks will learn from 1st National Bank’s efforts and find it necessary to support what we are doing.”

According to Mrs. Calderon, over the years the association has been able to achieve much, even with its limited resources.

“We have done such a lot of work and achieved so much that the work is consistent, and continuous. It might not be that somebody is getting a bone marrow transplant, like we have done in the past, but certainly the work continues. Our clinic is open. Our doctors, Dr. Bird and her team, are here every week dealing with our members and we continue to help those with ailments, those who need assistance in acquiring overseas medical help.

Spotlight on the Community

Spotlight on the CommunityMrs. Calderon says that’s she would like to see a regional approach to dealing with the disease at heads of government levels to effectively combat the negative effects on individuals and society.

1st nAtIonAL BAnk Is BAckIng Just us musIc

The evolution of the national youth choir into “Just Us” an assembly of young adult singers was inevitable as the level of commitment by members to the group seemed uneven.

A lot of the members of “Just Us” were former senior members of the National youth Choir. They have graduated through the National Youth Choir program. We were often called to perform at functions where there were problems with the whole choir turning up. So we found quite often that when we looked at who would actually be on the stage and who would be singing, it was “Just Us”.

The Choir began rehearsals of the special production sometime in January this year. The group’s musical arrangements were done by Director John Bailey and Jason Joseph, more popularly known as calypsonian “The Bachelor”. Choir members say that they quite enjoy the exploration of various musical genres.

“Oh it was great, I mean we have done Caribbean pieces while focusing more on the local pieces and that was a good experience for the choir. These are songs that we are more familiar with. The arrangements done by Mr.Joseph were just amazing. He is really good at his craft. The arrangement combined with his song choices just resulted in perfection.

1st National Bank, sponsors of both the event and the choir were represented by Mr. Carlton Glasgow who expressed his delight at the presentation. Mr. Glasgow says that the bank is especially pleased to be involved with “Just Us” as it reflects the financial institutions commitment to national development through the arts.

We make it our business to do this because, it is all well and good to operate your institution within a society and being a business you

are entitled to generate your profits but you have got to plow it back into the society. Your aim is to bring out societal development. 1st National Bank believes that by supporting such activities we are really helping the country develop and that is what we are all about!

“Just Us” is due to travel to neighboring islands where they have been invited to put on musical performances at various public venues.

1st nAtIonAL BAnk AIds the entrepot secondAry schooL.

1st National Bank paid a special visit to the principal and staff of the Entrepot secondary school following a formal request by the teachers for assistance in a remodeling project. The teachers of the Entrepot Secondary school were determined to do something about the state of their staff room. The area was not the most conducive place to work or to meet the students or their parents.

For sometime the teachers have been complaining that the staff room is a bit congested and our teachers primarily from the business department, they came to me before going to the principal. They were looking at ways of putting up additional cupboards for storage of papers, books and so on. They put together a proposal.

Business teacher Maximilia Eudovic the initiator of the proposal decided to make an appeal for assistance from St.Lucia’s cooperate community. There was some response but in general not very encouraging as few of the school’s immediate needs were being met. We had already sent out letters to various corporations. We got money that covered labor costs to enhance the staff room whereby we could install some new cupboards and get some new fans for the staff room. We got the furniture, or you can say most of it from another corporation, but we were lacking finance to cover labor costs and fans.

That was when 1st National Bank stepped in to help with the rest of the teacher’s needs. The Bank believes that their contribution is an investment in education in St.Lucia.

As we know the staff room is a place of heavy teacher interaction. A lot of work happens in the staff room in terms of preparing schedules, homework, preparing and marking student examinations and so this room should be a room that is conducive to all this activity helping the teachers perform at their optimum. Many times we contribute towards student development, which is also very good, but often times we can tend to neglect the people in the background, the teachers and staff and those who administer the educative program.

Robert Fevrier, manager of projects and services of 1st National Bank paid a special visit to the Entrepot school to get a first hand look at the newly refurbished teacher’s staff room.

To define equity one must first define collateral. Collateral is property that you pledge as a guarantee that you will repay a debt. If you don't repay the debt, the lender can take your collateral and sell it to get its money back. With a home equity loan or line of credit, you pledge your home as collateral. You can lose the home and be forced to move out if you don't repay the debt.

After considering the definition of collateral, some may wonder, “Why take such a risk?” But in fact using home equity line of credit is among the most cost effective methods of financing individual pursuits. These include paying for university tuition, purchasing a car, renovating your home and for financing in general. However using it to finance everyday consumption is not advisable.

St. Lucians have only recently gained a fuller grasp of the tremendous value in home equity. A common misconception is that home value is equivalent to home value. Home value refers to how much a house would sell for, if put on the open market. Home equity refers to how much of your home’s value, you do not owe on the loan.

Home value is determined by many factors, including the size, quality of construction and even its proximity to schools, hospitals, recreational facilities etc.

Calculating equity value is quite simple. Subtract the amount you owe on your house loan from the value of your home. If your home value was $300,000, and you owed $130,000 in loans, your equity value would be $170,000.

What’s the difference between a Home equity line of credit (HELOC) and a home equity loan (HEL)? A HELOC allows you to draw funds, up to a predetermined limit, whenever you need money. There is generally a minimum payment due each month, with the option to pay off as much of the line as you want. The

way that you draw and repay funds for a HELOC is similar to the way you draw and repay funds for a credit card. With a HEL, you receive a lump sum of money and have a fixed monthly payment that you pay off over a predetermined time period. In each case, the amount you can borrow is based on factors such as your income, debts, the value of your home, how much you still owe on your mortgage and your credit history.

The appeal of both of these types of loans is their interest rates, which are almost always lower than those of credit cards or conventional bank loans because they are secured against your home. In addition, the interest you pay on a home equity line or loan is often tax deductible (consult a tax advisor about your particular situation).

Generally, a HELOC is a good choice to meet ongoing cash needs, such as college tuition payments or medical bills. A HEL is more suitable when you need money for a specific, one-time purpose, such as buying a car or a major renovation.

Both HELOCs and HELs usually carry a higher interest rate than that of a first mortgage. With a HEL, you may choose either an adjustable rate that fluctuates according to variations in the economy and other factors, or you may opt for a fixed rate. A fixed rate enables you to budget a set payment monthly without worrying about increasing costs should interest rates rise. You may miss out on payment reductions if interest rates were to lower. With a HEL, there are also closing costs that you should consider.HELOC’s generally carry a lower interest rate than HEL’s, however rates are fluid (cannot be fixed). HELOC’s also allow you to withdraw funds only when needed. One is also able tore pay as little as interest only monthly. There are no closing costs!

Keep in mind, your home is the collateral for both a HELOC and a HEL. Realize the value of your home equity and use it Responsibly!

Money Guide for Financial Success A communication of the National Savings and Investment Programme supported by 1st National Bank

Thevalue

of Home Equity

Money Jokes and Humour From Across the Globe

The most successful investor was Noah. He floated stock, while everything around him went into liquidation.

I saw a bank that said if offered 24 Hour Banking." But I didn’t go in. I didn’t have that much time.

The market is weird. Every time one guy sells, another one buys, and they both think they're smart.

Q: How to make a million in the stock market?A: Start with two!

At 18 years old, Rockfeller had no money. He found an apple in the street. The fruit was dirty he cleaned it and resold it 50 cents to a man walking in the street ... with his 50 cents he bought 2 apples 25 cents each, and resold them 1$ to another man walking in the street ... with his 1 dollar he bought 4 apples, and resold them of course 2$ ... at 19 years he inherited from his grandmother...

A preacher went into his church and he was praying to God. While he was praying, he asked God, "How long is 10 million years to you?" God replied, "1 second." The next day the preacher asked God, "God, how much is 10 million dollars to you?" And God replied, "A penny." Then finally the next day the preacher asked God, "God, can I have one of your pennies?" And God replied, "Just wait a sec."

Washington, D. C.A tour guide was showing a tourist around Washington, D. C. The guide pointed out the place where George Washington supposedly threw a dollar across the Potomac River. "That's impossible," said the tourist. "No one could throw a coin that far!" "You have to remember," answered the guide. "A dollar went a lot farther in those days."

Graduation DayIt was graduation day and Mom was trying to take a picture of their son in a cap and gown, posed with his father. "Let's try to make this look natural" she said. "Junior, put your arm around your dad's shoulder." The father answered, "If you want it to look natural, why not have him put his hand in my pocket?"

A market analyst is an expert who will know tomorrow why the things he predicted yesterday didn't happen today!

Saving moneyMother had decided to trim her household budget wherever possible, so instead of having a dress dry-cleaned she washed it by hand. Proud of her savings, she boasted to my father,Just think, Fred, we are five dollars richer because I washed this dress by hand. Good, my dad quickly replied. Wash it again!

Sometimes it’s hard to see the lighter side of money and personal finance. But here are some funny ones about money to lighten things up.

Pro

du

ce

d b

y O

ran

ge

Me

dia

Gro

up

1st National Bank St. Lucia Limited, P.O. Box 168,#21 Bridge Street, Castries, St. LuciaTel: +758 455 7000 | Fax: + 758 453 1630Email: manager@1st nationalbankslu.comWebsite: www.1stnationalbankonline.com

So you have time for everything else that matters in life!SMARTBANKING...

CashPointOnline

OPEN

Smart

Hours

![Nothing · 2014. 11. 20. · Teller, Janne, 1964– [Intet. English] Nothing / Janne Teller; translated by Martin Aitken. — 1st ed. p. cm. Danish Cultural Ministry Prize for best](https://img.dokumen.tips/doc/110x75/614041231664f1518558a325/nothing-2014-11-20-teller-janne-1964a-intet-english-nothing-janne.jpg)