Embed Size (px)

Citation preview

Market Analysis | Forecasting | Price Movements | Archive | Breaking Views | 24/7 Online Access

©2013 Metal Bulletin Research www.metalbulletinresearch.com 1

Robert Cartman Senior Metals Analyst

10-11 September 2013

18th Galvanizing & Coil Coating Conference

Addressing European overcapacity

Market Analysis | Forecasting | Price Movements | Archive | Breaking Views | 24/7 Online Access

©2013 Metal Bulletin Research www.metalbulletinresearch.com 2

Disclaimer:

Prices and other information contained in this presentation have been obtained by us from various sources believed to be reliable. This

information has not been independently verified by us. Those prices and price indices that are evaluated or calculated by us represent an

approximate evaluation of current levels based upon dealings (if any) that may have been disclosed prior to publication to us. Such prices are

collated through regular contact with producers, traders, dealers, brokers and purchasers although not all market segments may be contacted

prior to the evaluation, calculation, or publication of any specific price or index. Actual transaction prices will reflect quantities, grades and

qualities, credit terms, and many other parameters. The prices are in no sense comparable to the quoted prices of commodities in which a

formal futures market exists.

Evaluations or calculations of prices and price indices by us are based upon certain market assumptions and evaluation methodologies, and

may not conform to prices or information available from third parties. There may be errors or defects in such assumptions or methodologies

that cause resultant evaluations to be inappropriate for use. Your use or reliance on any prices or other information published by us is at your

sole risk. Neither we nor any of our providers of information make any representations or warranties, express or implied as to the accuracy,

completeness or reliability of any advice, opinion, statement or other information forming any part of the published information or its fitness or

suitability for a particular purpose or use. Neither we, nor any of our officers, employees or representatives shall be liable to any person for any

losses or damages incurred, suffered or arising as a result of use or reliance on the prices or other information contained in this publication,

howsoever arising, including but not limited to any direct, indirect, consequential, punitive, incidental, special or similar damage, losses or

expenses.

We are not an investment advisor, a financial advisor or a securities broker. The information published has been prepared solely for

informational and educational purposes and is not intended for trading purposes or to address your particular requirements. The information

provided is not an offer to buy or sell or a solicitation of an offer to buy or sell any security, commodity, financial product, instrument or other

investment or to participate in any particular trading strategy. Such information is intended to be available for your general information and is

not intended to be relied upon by users in making (or refraining from making) any specific investment or other decisions. Your investment

actions should be solely based upon your own decisions and research and appropriate independent advice should be obtained from a suitably

qualified independent advisor before making any such decision.

Market Analysis | Forecasting | Price Movements | Archive | Breaking Views | 24/7 Online Access

©2013 Metal Bulletin Research www.metalbulletinresearch.com 3

Europe’s overcapacity problem – how bad?

The effects of overcapacity

Solutions – wait it out or time to act?

Conclusions

Market Analysis | Forecasting | Price Movements | Archive | Breaking Views | 24/7 Online Access

©2013 Metal Bulletin Research www.metalbulletinresearch.com 4

Europe’s overcapacity problem – how bad?

The effects of overcapacity

Solutions – wait it out or time to act?

Conclusions

Market Analysis | Forecasting | Price Movements | Archive | Breaking Views | 24/7 Online Access

©2013 Metal Bulletin Research www.metalbulletinresearch.com 5

0

5

10

15

20

25

30

35

40

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

ArcelorMittal ThyssenKrupp Riva Tata Steel

voestalpine Marcegaglia Salzgitter Arvedi

Ruukki US Steel Other

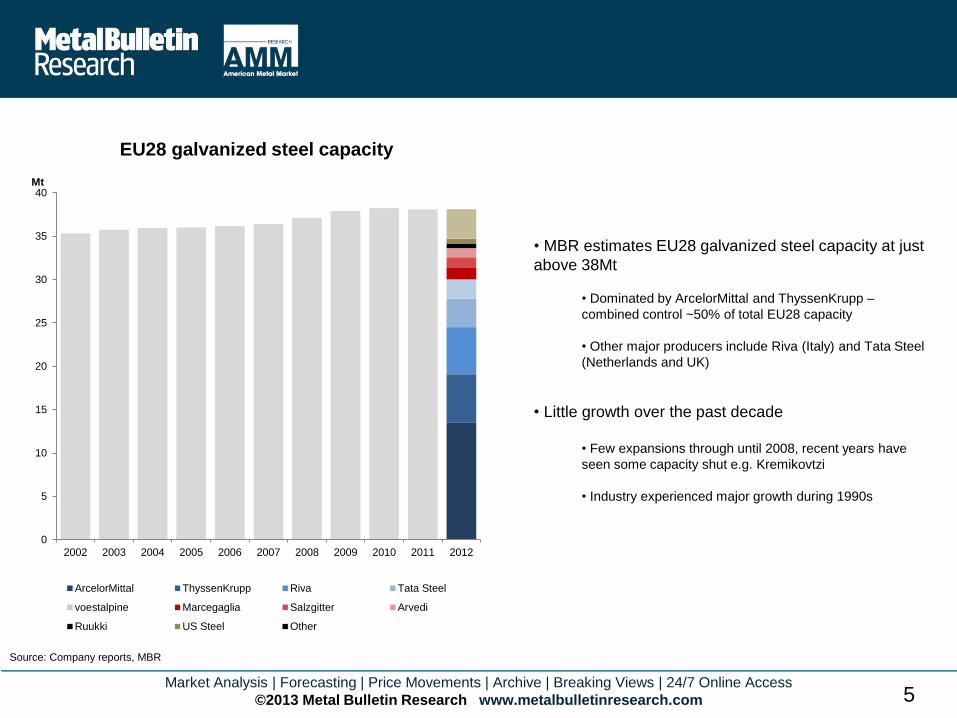

EU28 galvanized steel capacity

Mt

• MBR estimates EU28 galvanized steel capacity at just

above 38Mt

• Dominated by ArcelorMittal and ThyssenKrupp –

combined control ~50% of total EU28 capacity

• Other major producers include Riva (Italy) and Tata Steel

(Netherlands and UK)

• Little growth over the past decade

• Few expansions through until 2008, recent years have

seen some capacity shut e.g. Kremikovtzi

• Industry experienced major growth during 1990s

Source: Company reports, MBR

Market Analysis | Forecasting | Price Movements | Archive | Breaking Views | 24/7 Online Access

©2013 Metal Bulletin Research www.metalbulletinresearch.com 6

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

5

10

15

20

25

30

35

40

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Capacity Production Capacity utilization (RHS)

EU28 galvanized steel capacity vs. production

Mt

• Capacity utilization since 2008 has fallen below 80%

• As low as 60% in 2009 before recovering in 2010 and

2011 but fell again last year to 70%

• Production likely to fall again this year but capacity also

falling further (discussed later)

• Long-term breakeven level around 70% so current

situation unsustainable for some mills

• What effects has this overcapacity had on Europe’s

galvanized steel producers?

• Will the market improve back to pre-crisis levels or are

capacity cuts needed?

Source: Company reports, MBR

Market Analysis | Forecasting | Price Movements | Archive | Breaking Views | 24/7 Online Access

©2013 Metal Bulletin Research www.metalbulletinresearch.com 7

Europe’s overcapacity problem – how bad?

The effects of overcapacity

Solutions – wait it out or time to act?

Conclusions

Market Analysis | Forecasting | Price Movements | Archive | Breaking Views | 24/7 Online Access

©2013 Metal Bulletin Research www.metalbulletinresearch.com 8

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

100

200

300

400

500

600

700

800

900

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Average EU HDG price Capacity utilization (RHS)

EU28 HDG prices vs. capacity utilization

€/tonne

• Apparent effect on prices from low capacity utilization

• Before 2008, healthy utilization levels, in some years

pushing 90% gave producers ability to raise prices

• Since 2008, lower utilization rates have made it difficult

for producers to raise prices significantly or for a sustained

period

• With larger amounts of spare capacity, producer power

now much weaker than it was through until 2008

• Price increases now very fragile, tend to only last 2-3

months

Source: SteelFirst, Company reports, MBR

Market Analysis | Forecasting | Price Movements | Archive | Breaking Views | 24/7 Online Access

©2013 Metal Bulletin Research www.metalbulletinresearch.com 9

-150

-100

-50

0

50

100

150

200

2005 2006 2007 2008 2009 2010 2011 2012

USSK profit after tax

ArcelorMittal (Flat Carbon Europe) operating income

TKS Steel Europe EBIT

voestalpine steel EBIT

Indexed financial indicators for Europe’s

major galvanized steel producers (2005=100)

• Financial impact of market weakness and

overcapacity is evident

• Before 2008, healthy utilization levels and associated

higher prices helped producers to perform better financially

• Since 2008, earnings down, losses in some cases

(associated with wider writedowns) and European

producers have been suffering for past 4-5 years

• How much longer can Europe’s producers continue

like this?

• Will galvanized steel demand finally pick up and head

back to pre-crisis levels?

• Will Europe’s producers continue to wait or look for other

solutions?

Source: Company reports, MBR

Market Analysis | Forecasting | Price Movements | Archive | Breaking Views | 24/7 Online Access

©2013 Metal Bulletin Research www.metalbulletinresearch.com 10

Europe’s overcapacity problem – how bad?

The effects of overcapacity

Solutions – wait it out or time to act?

Conclusions

Market Analysis | Forecasting | Price Movements | Archive | Breaking Views | 24/7 Online Access

©2013 Metal Bulletin Research www.metalbulletinresearch.com 11

0

5

10

15

20

25

EU28 motor vehicle production

million units

• Automotive sector accounts for ~50-60% of EU28

galvanized steel consumption

• Vehicle output remains far below pre-crisis peaks, with

falls last year and forecast this year too

• 2013 vehicle output forecast to be some 20% below 2007

levels

• Demand growth likely to be slow, particularly with

regard to galvanized steel consumption

• Per-vehicle use of galvanized steel has little further

headroom to grow compared to past, already in

widespread use

• Increased focused on light-weighting, due to

environmental restrictions,/fuel costs, may see per-

vehicle use of galvanized steel fall or see it replaced by

other materials e.g. aluminium

Source: ANFAC, ANFIA, CCFA, SMMT, VDA, OICA, MBR

Market Analysis | Forecasting | Price Movements | Archive | Breaking Views | 24/7 Online Access

©2013 Metal Bulletin Research www.metalbulletinresearch.com 12

60

70

80

90

100

110

120

130

140

Jan

-96

Se

p-9

6

Ma

y-9

7

Jan

-98

Se

p-9

8

Ma

y-9

9

Jan

-00

Se

p-0

0

Ma

y-0

1

Jan

-02

Se

p-0

2

Ma

y-0

3

Jan

-04

Se

p-0

4

Ma

y-0

5

Jan

-06

Se

p-0

6

Ma

y-0

7

Jan

-08

Se

p-0

8

Ma

y-0

9

Jan

-10

Se

p-1

0

Ma

y-1

1

Jan

-12

Se

p-1

2

Ma

y-1

3

EU28 production in construction index

(2010 = 100)

Source: Eurostat, MBR

0

100

200

300

400

500

600

700

800

900

1,000

Q1 1

994

Q4 1

994

Q3 1

995

Q2 1

996

Q1 1

997

Q4 1

997

Q3 1

998

Q2 1

999

Q1 2

000

Q4 2

000

Q3 2

001

Q2 2

002

Q1 2

003

Q4 2

003

Q3 2

004

Q2 2

005

Q1 2

006

Q4 2

006

Q3 2

007

Q2 2

008

Q1 2

009

Q4 2

009

Q3 2

010

Q2 2

011

Q1 2

012

Q4 2

012

Building permits granted, all buildings, sa Germany

No of new buildings approved Spain

New construction orders value, 2005p, sa UK

Selected construction indicators

(2010 = 100)

Source: CEIC, MBR

Market Analysis | Forecasting | Price Movements | Archive | Breaking Views | 24/7 Online Access

©2013 Metal Bulletin Research www.metalbulletinresearch.com 13

ArcelorMittal planning cuts of ~700kt across 4 lines at

their Liège works, Belgium

Still to be finalized following discussions with unions

Possibility of 1 line remaining open, another only

‘mothballed’ and could be re-opened based on market

conditions

Source: ILZSG, MBR

Planned galvanized steel capacity closures

ThyssenKrupp to divest/close 4 lines too in Germany

and Spain, amounting to ~1.4Mt

Galmed line in Spain (~400kt) already closed

Neuwied, Dortmund sites likely to be closed over coming

months

Market Analysis | Forecasting | Price Movements | Archive | Breaking Views | 24/7 Online Access

©2013 Metal Bulletin Research www.metalbulletinresearch.com 14

0

5

10

15

20

25

30

35

40

2012

ArcelorMittal ThyssenKrupp Other

EU28 galvanized steel capacity

Mt

• ArcelorMittal and ThysennKrupp cutbacks amount to

5-6% of total EU galvanized steel capacity

• ArcelorMittal capacity to fall to ~12.8Mt

• ThyssenKrupp capacity to fall to ~4.2Mt

• Total EU capacity will fall to around 36Mt, a similar level

to that of 2004/05

• Will this be sufficient or are further cutbacks likely to be

necessary?

Source: Company reports, MBR

Market Analysis | Forecasting | Price Movements | Archive | Breaking Views | 24/7 Online Access

©2013 Metal Bulletin Research www.metalbulletinresearch.com 15

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

5

10

15

20

25

30

35

40

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 Med.term

Longterm

Capacity Production Capacity utilization (RHS)

EU28 galvanized steel capacity vs. production,

including forecastsMt

• Announced capacity cuts not overly drastic

• Should see utilization rise back toward sustainable and

profitable levels in the next few years and over the long

term

• Assumes capacity cutbacks enacted in full, with no further

expansions

• ArcelorMittal concessions to unions would alter the

numbers slightly

• Also assumes import penetration remains similar to

existing levels (about 8-10% in 2012) and that European

producers remain competitive

• Price levels likely to improve, along with profitability

Source: Company reports, MBR

Market Analysis | Forecasting | Price Movements | Archive | Breaking Views | 24/7 Online Access

©2013 Metal Bulletin Research www.metalbulletinresearch.com 16

Europe’s overcapacity problem – how bad?

The effects of overcapacity

Solutions – wait it out or time to act?

Conclusions

Market Analysis | Forecasting | Price Movements | Archive | Breaking Views | 24/7 Online Access

©2013 Metal Bulletin Research www.metalbulletinresearch.com 17

• EU28 galvanized steel capacity has steadily built up over past two decades to

some 38Mt

• Utilization levels since 2008 have barely hit 70% and have fallen back in 2012 and

expected to again in 2013

• Last four years have seen prices slide and, with that, profitability

• Producers have already tried to wait it out, hoping for demand levels to return to

pre-2008 levels

• Automotive and construction sectors either down sharply or showing scant signs of growth

• Other dynamics, such as vehicle light-weighting, also acting against demand growth for galvanized steels

• Capacity cutbacks hence needed and they are now arriving, largely via

ArcelorMittal and ThyssenKrupp – the EU28’s two major galvanized steel producers

• Plans announced appear measured and should help the industry move to stronger ground over the next few years

Market Analysis | Forecasting | Price Movements | Archive | Breaking Views | 24/7 Online Access

©2013 Metal Bulletin Research www.metalbulletinresearch.com 18

Market Analysis | Forecasting | Price Movements | Archive | Breaking Views | 24/7 Online Access

©2013 Metal Bulletin Research www.metalbulletinresearch.com 19

Contact details for further information:

Metal Bulletin Research

Nestor House, Playhouse Yard, London EC4V 5EX

+44 (0)20 7779 7999

Robert Cartman

Senior Metals Analyst

+44 (0)20 7827 6422