Embed Size (px)

DESCRIPTION

TA

Citation preview

GROUP PARTICIPATION INGOVERNMENTAL ACCOUNTINGSTANDARDS SETTING: ACLUSTER ANALYSIS

EHSAN H. FEROZState University of New York at Buffalo

INTRODUCTIONAccounting rule-making bodies have often solicited opinions

their proposed standards. [1] The Governmental AccountingStandards Board (GASB) recently announced that it will conductards Board (GASB) recently announced that it will conductpublic hearings around the country based on a discussionmemorandimi that relates to the timing and measiu^ment ofgovernmental type funds. <GASB, 1985) While the preciseimpact of these solicited opinions upon the final policy outcomesis hard to document, it is possible to discern areas of agreement(disagreement) between the policy-makers' preferences andthose of their constituencies. Brown (1981) and Haring (1979)examined the association between the position of the FinancialAccounting Standards Board (FASB) and the expressedpreferences of their constituencies on a subset of proposedstandards.

The present study focuses on groups who responded to theGovernmental Accounting Standards Board OrganizationCommittee (GASBOC) Exposure Draft 1981 in order to examinethe level of agreement (disagreement) between the GASBOCrecommendations and the expressed preferences of theconstituents. The GASBOC recommended, among others, thatan independent and full-time GASB be established. It alsorecommended that an independent Governmental AccountingFoundation (GAF) be established to have oversight and funding

PAQ WINTER 1986 (471)

responsibilities. The committee particularly emphasized theindependence of the GASB as a rule-making body separate fromthe FASB.

Although the establishment of the GASB has clearly signaledthe victory for those who argued a case for a standards-settingbody designed exclusively to meet the requirements of thegovernmental entities, looking at the recent past record ofsupport might help the GASB identify the constituencies that itneed be concerned with. It is also expected that themethodology used in this article could be applied to analyze theconstituents' support for (opposition to) one or more recentGASB pronouncements.

The remainder of this article is organized as follows: Part Ioutlines the basic ptui icipation model; Part II provides back-ground information; Part m analyzes the actual participationdata using a clustering device; and the final section draws sometentative conclusions.

PARTICIPATING MODEL

Participation is an expression of one's preference withreference to a given set of alternatives before a decision-maker.Although participation can presumably be both overt andcovert, most participation models focus on overt participationand are framed in terms of the relative costs and benefits ofovert participation in a decision-making arena. While thespecific contexts of costs and benefits may vary, most theoristsagree that overt participation is preceded by a decision wherethe benefits of such participation substantially outweigh thecosts. A rational participant would rarely undertake the costs ofparticipation unless the expected utility of such costs is greaterthan the costs of participation. The costs that have frequentlybeen referred to are those of gathering information andanalyzing the impact of alternative decisions upon self as well asothers whose arguments one may encounter. In addition, asDowns (1957) argues, a rational participant will consider theopportunity costs of time spent lobbying the decision-makerwhich may well exceed the total information gathering andprocessing costs.

(472) PAQ WINTER 1986

We may begin with the simplistic notion that a rational actorbelieves that the benefits of overt participation (Bi) exceeds itscosts (Ci) or overt participation is preceded by the followingperceived inequality:

Bi>Ci (1)

This formulation suggested by Riker and Ordeshook (1973)assumes that Bi includes opportunity costs of participation aswell. In other words, the (^portunity costs of alternative i arethe benefits of the next best alternative that must be foregone ifalternative i is chosen. Thus if k is the next best alternative to ithen one can rewrite the expression (1) as follows:

Bi>Ci (1.1)

where:

Hence the condition becomes:

or simply:

B i - C i > Bk-Ck (1.2)

Note that the above expression (1.2) allows for non-participa-tion in which case no action—doing nothing—yields a netprofit. Since the expected utility in this formulation is a functionof perceived inequality between benefits and costs, an expectednegative utility will justify non-participation or no-action. Suchan action is both rational and expected since non-participationor doing nothing is then the most preferred alternative.

BACKGROUND

In 1980 the National Council on Governmental Accounting

PAQ WINTER 1986 (473)

(NCGA), in collaboration with several other sponsoring bodies[2], established an ad hoc working committee (GASBOC) toconsider whether there was a need for a new structure toestablish accounting and reporting requirements for state andlocal government and if so to develop detailed recommendationsregarding the structure, funding, compliance, and the interfacewith the Financial Accounting Foundation (FAF) and the FASB.The committee (GASBOC) recommended a new structure forpromulgating standards for accounting and reporting bygovernmental units and solicited vndtten comments from allinterested groups. (GASBOC, 1981) The principal recommenda-tions of the committee on which the respondents were asked tocomment were as foUows:

Recommendation #1. A separate and independent GASB beestablished.Recommendatioii #2: Govenunental accounting standards beestablished by an independent body that includes govern-ment representation rather than solely by government.Recommendation #3: An independent Governmental Ac-counting Foundation (GAF) be established to have oversightand funding responsibility.Recommendation #4: The GASB should be a full-timeorganization.

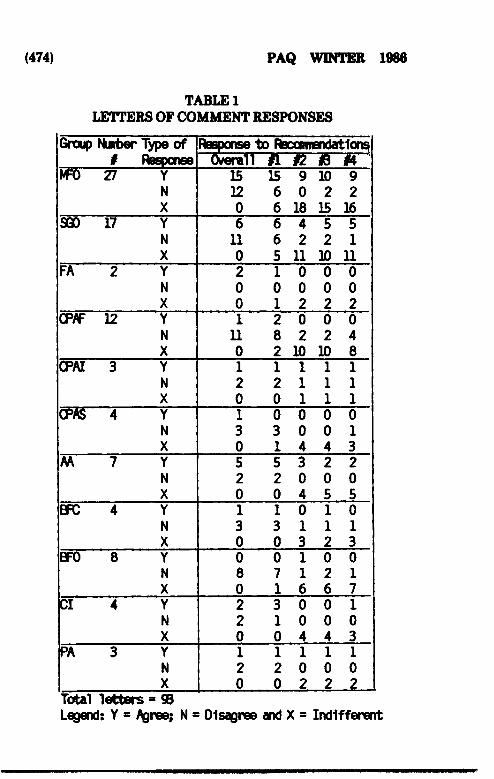

The GASBOC received a total of 93 letters commenting onthese recommendations. Following the letters of comment, theGASBOC convened public hearings on May 4 and 5, 1981 toprovide another opportunity to interested groups to expresstheir views regarding the recommendations of the committee.The number of participants in the public hearings was onlyone-fifth of those who wrote letters of comment. The gradualnarrowing of the number of participants may be a function of therelative costs involved in writing a letter and in appearingbefore the GASBOC. If writing a letter involves time andresearch (both of which are scarce commodities), appearingbefore the GASBOC involves an added component of theopportunity costs of time spent lobbjring the GASBOC.

Tables 1 and 1 list the participants who wrote letters of

<474) PAQ WINTER 1986

TABLE 1LETTERS OF COMMENT RESPONSES

Group Nunber Type o f1 Response

MFO 27 YNX

9QD 17 YNX

FA 2 YNX

CPAF 12 YNX

CPAI 3 YNX

CPAS 4 YNX

AA 7 YNX

BFC 4 YNX

BFO 8 YNX

CI 4 YNX

PA 3 YNX

^Bsponse t o RBcornnenddtionsiOm^^^ fi f2 i3 tA

15 15 9 10 912 6 0 2 20 6 18 15 166 6 4 5 5

11 6 2 2 10 5 11 10 112 1 0 0 00 O O O O0 1 2 2 21 2 0 0 0

11 8 2 2 40 2 K) ID 81 1 1 1 12 2 1 1 10 0 1 1 11 O O O O3 3 0 0 10 1 4 4 35 5 3 2 22 2 0 0 00 0 4 5 51 1 0 1 03 3 1 1 10 0 3 2 30 0 1 0 08 7 1 2 10 1 6 6 72 3 0 0 12 1 0 0 00 0 4 4 31 1 1 1 12 2 0 0 00 0 2 2 2

Total letters » 9BLegend: Y >= ree; N Disagree and X = Indiffererrt

PAQ WINTER 1986 (475)

TABLE 2PUBUC HEARING RESPONSES

Respondent

RACNYCSAIONYSDCFASBE&WPWC&LOH&SNACUBOAAACSGNAAPICPAsNACAGAMFOAHFMASCCGNCSL

ResponseOverall

NYNYNNNNNNNYNNNNYNYN

to Recommendation#1

NYNYNNNXNNXYNNNNYNYN

#2

XYXYXXXXXXXYXXXYYXXX

#3

XYXYXXXXXXXYXXXXYXXX

#4

XXXYXXXXXXXYXXXYYXXX

Total submissions " 20

Legend: Y « Agree; N " Disagree;X « Indifferent

(476) PAQ WINTER 1986

comment and/or appeared before the public hearings. Table 1classifies the participants in terms of their professionalaffiliations into eleven groups: Municipal Financial Officers(MFO); State Governmental Officers (SGO); Federal Agencies(FA); CPA-Firm (CPAF); CPA-Individual (CPAI); CPA-Society(CPAS); Accounting Academicians (AA); Business Firms-Creditors (BFC); Business Firms-Others (BFO); ConcernedIndividuals (CI); and Professional Associations excluding CPAsocieties (PA). These groups could also be conceived assubgroups of broader denominations such as the profession,management, and users. While classifying the groups undercategories such as profession and users may be useful for somepurposes, in the present case they seem to be too broad toprovide any meaningful information for comparative analysis.

Table 2 defies any natural grouping and hence presents theindividual participant as the unit of analysis. These participantswere: Professor Robert Anthony (RA); Comptroller of New YorkCity (CNYC); State Auditor and Inspector, Oklahoma (SAIO);New York State Deputy Comptroller (NYSDC); FinancialAccounting Standards Board (FASB); Ernst & Whinney (E&W);Price-Waterhouse (PW); Cooper and Lybrand (C&L); DeloitteHaskins and Sells (DH&S); National Association of College andUniversity Business Officers (NACUBO); American AccountingAssociation (AAA); Council of State Governments (CSG);National Association of Accountants (NAA); PennsylvaniaInstitute of CPAs (PICPAs); National Association of Counties(NAC); Association of Government Accountants (AGA);Municipal Finance Officers Association (MFOA); HospitalFinancial Management Association (HFMA); State, County,and City Government (SCCG); and National Conference of StateLegislators (NCSL).

Both in the letters of comment groups and in the publichearings, state and local government officials (MFO and SGO)and auditors (CPAF, CPAI, and CPAS) seem to be overrepre-sented. On the other hand, the creditors (BFC) and ConcernedIndividuals (CI) are conspicuous by their absence in publichearings. One explanation for this skewed representation couldbe the low ' 'transfer costs'' for creditors as against the state andlocal government officers who have invested their human capital

PAQ WINTER 1986 (477)

in the governmental entities (see Sunder, 1981). Theopportunity to diversify without significant transaction costsrenders the creditors less dependent upon the future of govern-mental accounting.

Concerned Individuals (CI) include those categories ofindividuals whose interest in governmental accounting stemsprimarily from monitoring or citizenship interest (as againstprofessional interest). Participation of this group may beexpected due to the potential negative impacts of localgovernmental decision on the constituents' well-being, such asincreased taxes or reduced services for segments of theconstituency. However, as Copeland and Ingram (1983:63)argue, these costs, spread over a large number of individuals,generally constitute a public good (bad) and their per capitaimpact is likely to be minimal. In the absence of an entrepre-neureal personality, such large groups are likely to be dormantor inactive.

DIFFERENTIAL SUPPORT FOR THE RECOMMENDATIONS

As mentioned previously, when the GASBOC invited lettersof comment and public hearing submissions, it solicitedopinions on specific recommendations related to the proposedGASB. In order to determine the level of support for (oppositionto) the GASBOC recommendations, each of the letters ofconunent and public hearing submissions was read to determinewhether the respondent agreed with the GASBOC proposals ingeneral and each of the four recommendations in particular. [3]Letters and submissions were classified as being either favorable(Agree) or unfavorable (Disagree) or Neutral (Indifferent). [4]The same set of letters and submissions was reread by a secondreader to ensure the reliability of the coding. The correspond-ence between the first and second reading was rather high (.87)although there was a high level of indifference on each of thefour recommendations. [5] The large number of neutrals isattributable to the lack of specificity and articulation in most ofthe letters and submissions.

One important issue in analyzing the letters and submissionswas: how much weight should be assigned to each of the letters

(478) PAQ WINTER 1986

and submissions coming from professional associations (CPAs,NAA, NCSL, etc.) relative to individuals. [6] A letter or asubmission from a professional association presumably repre-sents the views of more than one member of that association.However, it is not evident from those letters or submissionswhether they represent the views of all the members of theassociation or only some members. In the absence of suchinformation, does the submission represent the views of itsendorser only?

Table 1 indicates that there were significant differences in theresponses of the eleven groups as to the four recommendationsmade by the GASBOC. A rank ordering of the various groups indescending order of support is in Table 3. [7] The level ofsupport was measured by subtracting the percentage of groupmembers agreeing with a recommendation (or overall) from thepercentage of members disagreeing. Support for a recom-mendation (or overall) can range between -1-100% to -100%.

Table 3 also identifies five support (agree) clusters (A throughE) and five oppose (disagree) clusters (F through J) from thedata presented in Table 1. [8] Groups with a 0% support are inthe neutral zone since the percentage of members agreeing ineach of these groups equals the percentage disagreeing. Whilethe neutrals constitute an interesting subset, this analysisfocuses on support and oppose clusters since potentially theyare the ones that the GASB needs to be most concerned with.The frequencies of each of the groups appearing in the supportor oppose dusers are as foUows:

Support Clusters Oppose Clusters

MFO 5 CPAF 5AA 5 BFC 4PA 3 BFO 4SGO 3 CPAS 3FA 2 CPAI 2CI 1 PA 2

SGO 1

PAQ WINTER 1986 (479)

00 cr\ M

UJ-no

T»-•oo^^nC l

' " '

1

1

1

1

OT)

^^100

LA)

LO

1

1

1

o

TLOLO

LO

n• n

CDFC/

oTJgTU lo

o1

0 0- J

Ln

p - i

i _ i

1

CO-noTN>U l

CD

O

125)

T3

>t~i

1LOocft

>

1

U l

CD

TLn

I

(^

1

•

CD

O

CO

gTN)^O

U l

T

OT

1LO

•LT

C2Jj1

(-•

•

CD-nooTJ>t—1(0

)

o

t—i^••^o

ooo ^

CO

oo

oLO1 ttJ.3)

nCD

\(42. >

LT

a

BFO/

^1^^

o

(/>o

ICD

]

SGO<

!_•

•0 0

nO

>

ISJ00

O l

MFO/

TJ>

LO

LO

O

Is)ft

>

QC

T:

LkiLtl

Lkl

ft6)CE] J

:)vv

ODftU l

MFO

rs)Lnft

VO

1

uft

u

f

LO

(480) PAQ WINTER 1966

I

PAQ WINTER 1986 (481)

Each group may appear a maximum of five times (andminimum zero) in the support (or oppose) clusters. Assigning avalue of -f-1 for a group's appearing once in one of the supportclusters and -1 for appearing in one of the oppose clusters once,the following is the cumulative rank ordering of the groups inorder of descending level of support:

tank

1.2.3.4.5.6.7.

Group

MFO/AASGOPA/CICPAICPASBFC/BFOCPAF

Support/Oppose

+ 5+2+ 1-2-3-4-5

The above analysis indicates that, among those whosubmitted letters of comment. Municipal Financial Officers(MFO) and Accounting Academicians (AA) agreed with theGASBOC recommendations most. Other groups lending varyingdegrees of support are the State Grovenunental Officers (SCKD),Professional Associations (PA), and Concerned Individuals (Cl).CPA-Firms (CPAF) were in most complete or nearly completedisagreement with the GASBOC recommendations. While theCPA Societies (CPAS) and CPA-Individuals (CPAI) varied intheir level of disagreement with the GASBOC, it is noteworthythat the auditors offered a concerted opposition to theGASBOC recommendations.

A similar analysis of the public hearing submissions in termsof level of agreement with the GASBOC recommendationsappears in Table 4. [9] Table 4 rank-orders the public hearingparticipants in Table 2 in descending order of support andidentifies two clusters: a support cluster (A) and an opposecluster (B). As with the letters of comment cluster appearing inTable 3, Municipal Financial Officers (MFOA) rank heavily inthe support cluster. Other members of this cluster are: Councilof State Governments (CSG); New York State Deputy Comptrol-ler (NTSDC); ComptroUer of New York City (CNYC); and the

(482) PAQ WINTER 1986

State, County, and City Governments (SCCG). The opposecluster may also be termed as the cluster of big auditing firms(C&L, DH&S, PW, and E&W). While their opposition isconsistent with their stance at the letters of comment stage,what is somewhat unexpected is the appearance of theAmerican Accounting Association (AAA) and the onlyaccounting academician (RA) in the oppose cluster. Theiropposition is perhaps more explainable in terms of thedissenting views of the individual presenter than that ofaccoimting academicians in general. Finally, the FinancialAccounting Standards Board (FASB) registered its disapprovalof the GASBOC recommendations.

SUMMARY AND CONCLUSIONSThis article analyzed the participation data with respect to the

four GASBOC recommendations. While there are variousmodes of participation, the present study is confined to thewritten and oral submissions made by various groups. Somemodes of participation, such as subtle influence upon thedecision-makers, can be real but not easily susceptible toempirical verification. In this sense, this study might have dealtwith the more obvious, but not necessarily the most important,modes of participation that are readily identifiable.

The pyramidic nature of participation with respect to the fourGASBOC recommendations generally conforms to the expecta-tions that, out of the total spectrum of interest groups, only asubset will take an interest in the process of accountingstandards setting (see Feroz, 1985). From a rational perspective,non-participation means an indifference stemming from well-articulated negative utilities of participation. Ontologically, thenon-participating subsets could be an important object of study.However, these subsets caimot be identified unless they maketheir preferences manifested in an observable fashion.

Of the groups participating, the local and state governmentofficials (MFO and SGO) and accounting academicians (AA)seem to have a more favorable view of the changes in govern-mental accounting than the rest of the constituents. Accountingacademicians have generally been considered to be "change

PAQ WINTER 1986 (483)

agents" in the accounting profession. (Hicks, 1978) Theirfavorable view of the GASBOC recommendations furtherreaffirms their progressive orientation. State and localgovernmental officials have long been arguing a case ofuniqueness of governmental accounting as distinct fromcorporate accounting. An independent GASB with an identityseparate from the FASB generally reinforces the case of govern-mental accountants for their separate identity.

The clustering of the state and local governmental officialsand accounting academicians on one side and the auditors andthe FASB on the other generally indicates a lack of consensusamong the GASB constituents. Success of the GASB in years tocome will depend to some extent upon how persuasively itresponds to the groups that were in various levels of agreement(disagreement) with the GASBOC recommendations. Ingeneral, group support for (or opposition to) the GASB policyinitiatives is likely to be issue-specific and transitory. In otherwords, the very same groups that supported (opposed) theGASBOC recommendations cmild find themselves in disagree-ment (agreement) with the GASB on some other issues in thefuture. However, as Gordon and Hammer (1983) suggest, ifseveral of these groups perceive a particular GASB pronounce-ment as being unreasonably costly to implement, these groupscould organize sufficient resistance to lead to the GASB'sdemise.

Finally, the findings of this study are strictly based upon thepopulation of respondents which may not represent all interestsor groups that might be potentially interested in the GASB. Thedelicate balance between the support for and opposition to theGASBOC recommendations could very well change if one couldincorporate all conceivable interests and groups that might beinterested in the GASB. To the extent that this failure biases thefindings, the conclusions are tentative and partial.

NOTES

1. The author wishes to thank Jim Chan for providing him with the data and initialencouragement; Nicii Dopuch, Sandy Gunn, and Paul Newman for comments andsuggestions and Kishwar Feroz for research assistance. None of them endorsesthe views expressed here.

(484) PAQ WINTER 1986

2. The other sponsoring organizations are: American Institute of Certified PublicAccountants (AICPA); Financial Accounting Foundation (FAFI; MunicipalFinancial Officers Association (MFOA); National Association of State Auditors,Comptrollers and Treasurers (NASACT); and General Accounting Office (GOA).

3. Although it is arguable that Recommendation 01 was the principalrecommendation of the GASBOC, the stance here is that a well-articulatedresponse will he consistent with respect to all the four recommendations. Res-pondents often agree in general terms but disagree in specifics. It is the paradoxof this type that led to a coding scheme embracing all four specific recommenda-tions.

4. Coders were directed to record an agreement with a recommendation (or overall)only if there was an explicit statement to that effect. Disagreement was similarlyonly on the basis of an explicit dissenting statement.

5. When there was a disagreement between two coders, the author himself read theletter of comment or submission and decided according to the majority rule (2 outof 3 readers).

6. Almost any weighting scheme is bound to be distorted in the absence of a clearindication of the internal decision-making process of the entities or groupsinvolved. While it is possible to perceive some actors or groups as being moreinfluential than others on an anecdotal basis, the problem is to convert theseperceptions into numerical weights. The author is unaware of any weightingscheme that is both objective and reliable.

7. The computations for Table 3 can be illustrated as follows: Take the case of MFOin Table 1 with respect to GASBOC Recommendation #1. Fifteen (6S.6%)members of MFO agreed with the recommendation; six (22.2%) disagreed; andsix (22.2%) were indifferent. In order to compute the support score for MFO,subtract the percentage of members disagreeing (22.2%) h'om the percentage ofmembers agreeing (65.5%) and get the MFO support score of 33.3%. Note thatthe author ignored the percentage of members indifferent (22.2%) for thepurposes of these computations. Once the support score for each group iscomputed on each recommendation and overall, the groups are rank-ordered interms of descending level of support. MFO, for example, ranked third indescending order of support on Recommendation ifl in Table 1.

8. The basis of these clusters is the group's aggregate support for (or opposition to)each of the four GASBOC recommendations (or overall) outlined in Table 1.

9. Support scores in Table 4 were calculated by subtracting the number of Ns fromthe number of Ys in Table 2 and assuming N or Y = 1. Xs were ignored in thiscalculation.

REFERENCESBrown, Paul R. (1981). "A Descriptive Analysis of Select Input Bases of the

Financial Accounting Standards Board." Journal of Accounting Research 19(Spring):232-246.

Copeland, Ronald M. and Robert Ingram (1983). Municipal Financial Accountingand Disclosure Quality. Reading, Mass.: Addiaon-Wesley.

Downs, Anthony (1957). .4n Economic Theory of Democracy. New York: Harper andRow.

Feroz, Ehsan H. (1985). "A Group Theory Approach to the Process of FinancialAccounting Standards Setting," in Heidi Vernon-Wortzel and Carolyn Dexter(eds.). Management in the 199O's: Perspectives from Business, Government andEducation. Eastern Academy of Management.

Gordon, Lawrence and Michelle W. Hammer (1983). "GASB's Survival Potential:An Agency Theory Perspective." Public Budgeting and Finance 3 (Spring):103-112.

PAQ WINTER 1986 (485)

Governmental Accounting Standards Board (1986). Governmental AccountingStandards Series: Discussion Mtmorandum, An Analysis of Issues Related toMeasurement Focus and Basis of Accounting — Oovemment4U Funds. Stamford,Conn.: Financial Accounting Foundation.

Governmental Accounting Standards Board Organization Committee (1981). Reportof the Oovernmental Accounting Standards Board Organization Committee:Exposure Draft. Stamford, Conn.: Financial Accounting Foundation.

Haring, John R. (1979). "Accounting Rules and the Accounting Establishment."Journal of Business 62 (October):507-619.

Hicks, James O. (1976). "An Examination of Accounting Interest Groups' Differ-ential Perception of Innovation." Accounting Review 63 (April):371-3S8.

Rilcer, William H. and Peter C. Ordeshook (1979). An Introduction to PositivePolitical Theory. Englewood Cliffs, N.J.: Prentice-Hall.

Sunder, Shyam (1981). "Toward a Ttheory of Accounting Choice: Private and SocialDecisions." Working Paper. Chicago: University of Chicago.

![Constraints Impacting Minority Swimming Participation ... · media exposure on the issue of minority swimming (in)ability; and, [3] resulted in action by community and governmental](https://img.dokumen.tips/doc/110x75/5e459695f8a0842fab5305db/constraints-impacting-minority-swimming-participation-media-exposure-on-the.jpg)