Embed Size (px)

Citation preview

1875 MAP

MARKET ALLOCATION PROCESS

Investment Strategy August 2017

2

1875 FINANCE SA • 40, rue du 31 Décembre • PO Box 6208 • CH- 1211 Geneva 6 • Tel. +41 (0)22 595 18 75 • Fax +41 (0)22 595 18 00 • www.1875.ch

1875 FINANCE SA • Bleicherweg 7 • PO Box • CH- 8002 Zurich • Tel. +41 (0)44 355 18 75 • Fax +41 (0)44 355 18 00 • www.1875.ch

1875 FINANCE (Luxembourg) • Bd. Prince Henri 41 • L-1724 Luxembourg • Tél. +(352) 27 99 1875 • Fax + (352) 27 99 1875-75 • www.1875.lu

TABLE OF CONTENTS

Investment Policy

Economic Environment 3

Financial Environment 11

Investment Strategy 15

3

1875 FINANCE SA • 40, rue du 31 Décembre • PO Box 6208 • CH- 1211 Geneva 6 • Tel. +41 (0)22 595 18 75 • Fax +41 (0)22 595 18 00 • www.1875.ch

1875 FINANCE SA • Bleicherweg 7 • PO Box • CH- 8002 Zurich • Tel. +41 (0)44 355 18 75 • Fax +41 (0)44 355 18 00 • www.1875.ch

1875 FINANCE (Luxembourg) • Bd. Prince Henri 41 • L-1724 Luxembourg • Tél. +(352) 27 99 1875 • Fax + (352) 27 99 1875-75 • www.1875.lu

INVESTMENT POLICY

Global economic environment

The latest economic statistics released confirmed the

robustness of the expansion of the global economic cycle in

the second quarter, with a growth of close to 3.5%. The

slowdown in the emerging zone, particularly in Brazil, was largely

offset by stronger activity in developed countries, particularly in

Europe, while the economy remained more robust than expected

in China.

Contrary to the majority of forecasts, the economic situation in

the advanced nations will not decline during the second half

of the year, despite the uncertainties arising from the evolution

of American economic policy. It will benefit both from the

continuation of expansive financial conditions and the recovery

of productivity. By improving corporate profits, the constraints

imposed by the legacy of the strong contraction of investment

will dissipate and allow for a more intense fixed capital formation.

4

1875 FINANCE SA • 40, rue du 31 Décembre • PO Box 6208 • CH- 1211 Geneva 6 • Tel. +41 (0)22 595 18 75 • Fax +41 (0)22 595 18 00 • www.1875.ch

1875 FINANCE SA • Bleicherweg 7 • PO Box • CH- 8002 Zurich • Tel. +41 (0)44 355 18 75 • Fax +41 (0)44 355 18 00 • www.1875.ch

1875 FINANCE (Luxembourg) • Bd. Prince Henri 41 • L-1724 Luxembourg • Tél. +(352) 27 99 1875 • Fax + (352) 27 99 1875-75 • www.1875.lu

INVESTMENT POLICY

The increase in expenditure on capital goods will combine

with a more vigorous consumption due to improvement in

the labour market.

In emerging countries, economic activity will accelerate as

a result of the recovery in global trade, but also the rise in

commodity prices. It will also be supported by robust

domestic demand in China.

As for inflation, it remains particularly moderate and is

still below the targets set by the central banks. Due to the

very gradual reduction in surplus production capacity

induced by the creation of new productive resources, price

indices will only increase gradually during the second half

of the year.

5

1875 FINANCE SA • 40, rue du 31 Décembre • PO Box 6208 • CH- 1211 Geneva 6 • Tel. +41 (0)22 595 18 75 • Fax +41 (0)22 595 18 00 • www.1875.ch

1875 FINANCE SA • Bleicherweg 7 • PO Box • CH- 8002 Zurich • Tel. +41 (0)44 355 18 75 • Fax +41 (0)44 355 18 00 • www.1875.ch

1875 FINANCE (Luxembourg) • Bd. Prince Henri 41 • L-1724 Luxembourg • Tél. +(352) 27 99 1875 • Fax + (352) 27 99 1875-75 • www.1875.lu

INVESTMENT POLICY

Regional economic environment

USA

In line with our expectations, US gross domestic product has

recovered in the last 3 months to enter the third longest

expansion in its history since 1850. Having been affected by

the constricting effects of rising bond yields and the strengthening

of the dollar, the US economy will be supported by rising real

household incomes and a recovery in productive investment.

The delay in the implementation of the US tax reform is expected

to have only a limited impact on US economic development, with

the likelihood of an upcoming US tax reduction still remaining

high.

In terms of inflation, price indices will continue to progress in a

contained manner, with inflationary expectations remaining

moderate.

Source : 1875 MAP

6

1875 FINANCE SA • 40, rue du 31 Décembre • PO Box 6208 • CH- 1211 Geneva 6 • Tel. +41 (0)22 595 18 75 • Fax +41 (0)22 595 18 00 • www.1875.ch

1875 FINANCE SA • Bleicherweg 7 • PO Box • CH- 8002 Zurich • Tel. +41 (0)44 355 18 75 • Fax +41 (0)44 355 18 00 • www.1875.ch

1875 FINANCE (Luxembourg) • Bd. Prince Henri 41 • L-1724 Luxembourg • Tél. +(352) 27 99 1875 • Fax + (352) 27 99 1875-75 • www.1875.lu

INVESTMENT POLICY

Canada

After progressing strongly throughout the previous quarter, Canadian

growth will continue to solidify, remaining close to its 3% trend

level. In the absence of a major price increase in energy prices, the

Canadian inflation rate will remain below 2%.

Eurozone

In light of the evolution of our models, economic expansion in the

Eurozone will continue to increase to 2.5% again in the next 3 to

6 months. Following the rise in the Euro, it will be supported further

by domestic demand, namely consumption and investment.

Considering the trend towards inflation shown by our indicators and

the recent gains on the Euro, the price index in the Eurozone will

increase only slightly in 2017 and will not reach the target level

of two per cent before 2018.

Source : 1875 MAP

7

1875 FINANCE SA • 40, rue du 31 Décembre • PO Box 6208 • CH- 1211 Geneva 6 • Tel. +41 (0)22 595 18 75 • Fax +41 (0)22 595 18 00 • www.1875.ch

1875 FINANCE SA • Bleicherweg 7 • PO Box • CH- 8002 Zurich • Tel. +41 (0)44 355 18 75 • Fax +41 (0)44 355 18 00 • www.1875.ch

1875 FINANCE (Luxembourg) • Bd. Prince Henri 41 • L-1724 Luxembourg • Tél. +(352) 27 99 1875 • Fax + (352) 27 99 1875-75 • www.1875.lu

INVESTMENT POLICY

Great Britain

The latest statistics confirm the weakening of the British

economy. After the slowdown in consumer spending, which has been

affected by the decline in real incomes, the expansion of business

activity in the United Kingdom is now also affected by Brexit. As a

result, Britain's gross domestic product will grow more moderately in

the second half of the year to fluctuate at best between 1% and 1.5%.

After rising to 2.8% as a result of the decline in sterling, British

inflation will increase more modestly in the second half of the

year. In light of the evolution of our indicators relating to inflationary

conditions, the Bank of England's objective of price stability appears

to be weakened, increasing the risks of stagflation in the medium

term.

Source : 1875 MAP

8

1875 FINANCE SA • 40, rue du 31 Décembre • PO Box 6208 • CH- 1211 Geneva 6 • Tel. +41 (0)22 595 18 75 • Fax +41 (0)22 595 18 00 • www.1875.ch

1875 FINANCE SA • Bleicherweg 7 • PO Box • CH- 8002 Zurich • Tel. +41 (0)44 355 18 75 • Fax +41 (0)44 355 18 00 • www.1875.ch

1875 FINANCE (Luxembourg) • Bd. Prince Henri 41 • L-1724 Luxembourg • Tél. +(352) 27 99 1875 • Fax + (352) 27 99 1875-75 • www.1875.lu

INVESTMENT POLICY

Switzerland

Recent cyclical data advocates for a gradually more robust

expansion in Switzerland over the next six to nine months. The

Swiss economy will be favoured by an external demand which is

supported by the increased dynamism of the Eurozone and the

decline of the franc. It will also benefit from a gradual increase in

investment. In terms of inflation, price indices will increase only very

gradually, despite the rise in import prices.

Japan

Economic activity in Japan continued to accelerate during the

second quarter to reach an expansion rate of 2.5%. As a result of

the recovery in productive investment and of stronger consumption,

Japan's gross domestic product will continue to progress at a rate of

close to 2%. Despite the structural reforms put in place by the

government, however, Japanese growth will remain structurally

constrained by the ageing of the population.

Source : 1875 MAP

9

1875 FINANCE SA • 40, rue du 31 Décembre • PO Box 6208 • CH- 1211 Geneva 6 • Tel. +41 (0)22 595 18 75 • Fax +41 (0)22 595 18 00 • www.1875.ch

1875 FINANCE SA • Bleicherweg 7 • PO Box • CH- 8002 Zurich • Tel. +41 (0)44 355 18 75 • Fax +41 (0)44 355 18 00 • www.1875.ch

1875 FINANCE (Luxembourg) • Bd. Prince Henri 41 • L-1724 Luxembourg • Tél. +(352) 27 99 1875 • Fax + (352) 27 99 1875-75 • www.1875.lu

INVESTMENT POLICY

According to our inflationary indicators, price indices will increase during the

2nd quarter, while still remaining below the trend defined by the Bank of

Japan.

Australia

After being constrained by the decline in base metals, Australian growth

will strengthen, in line with the acceleration in the global economic

cycle. Regarding inflation, the increase in prices will remain contained

and will grow in a more limited manner in international comparison.

Emerging countries

The moderation of the expansion of emerging countries was less

pronounced than expected in the second quarter, due to the robustness of

the Asian economies and the marked recovery of production in Russia. A

more sustained activity in developed countries, as well as a domestic

demand which is stronger in India and still firm in China, will support

growth in developing nations in the second half of the year, in

conjunction with rising commodity prices.Source : 1875 MAP

10

1875 FINANCE SA • 40, rue du 31 Décembre • PO Box 6208 • CH- 1211 Geneva 6 • Tel. +41 (0)22 595 18 75 • Fax +41 (0)22 595 18 00 • www.1875.ch

1875 FINANCE SA • Bleicherweg 7 • PO Box • CH- 8002 Zurich • Tel. +41 (0)44 355 18 75 • Fax +41 (0)44 355 18 00 • www.1875.ch

1875 FINANCE (Luxembourg) • Bd. Prince Henri 41 • L-1724 Luxembourg • Tél. +(352) 27 99 1875 • Fax + (352) 27 99 1875-75 • www.1875.lu

INVESTMENT POLICY

Inflationary pressures in developing countries will remain

moderate overall, while remaining heterogeneous depending on

exchange rate trends.

China

During the second quarter, economic growth in China remained

higher than expected, reaching 7% once more. As some

advanced leading indicators seem to anticipate, the Chinese

economy will remain firm in the coming months as foreign

demand strengthens and the domestic economy remains solid.

In the medium term, however, the Chinese economy will face

a controlled decline in its growth. On the one hand, the ageing

of the population will lead to a decline in labour productivity. On

the other hand, the new mode of development, which favours

consumption at the expense of exports and privileges services

over the manufacturing sector, will hinder the accumulation of

capital.

Source : 1875 MAP

11

1875 FINANCE SA • 40, rue du 31 Décembre • PO Box 6208 • CH- 1211 Geneva 6 • Tel. +41 (0)22 595 18 75 • Fax +41 (0)22 595 18 00 • www.1875.ch

1875 FINANCE SA • Bleicherweg 7 • PO Box • CH- 8002 Zurich • Tel. +41 (0)44 355 18 75 • Fax +41 (0)44 355 18 00 • www.1875.ch

1875 FINANCE (Luxembourg) • Bd. Prince Henri 41 • L-1724 Luxembourg • Tél. +(352) 27 99 1875 • Fax + (352) 27 99 1875-75 • www.1875.lu

INVESTMENT POLICY

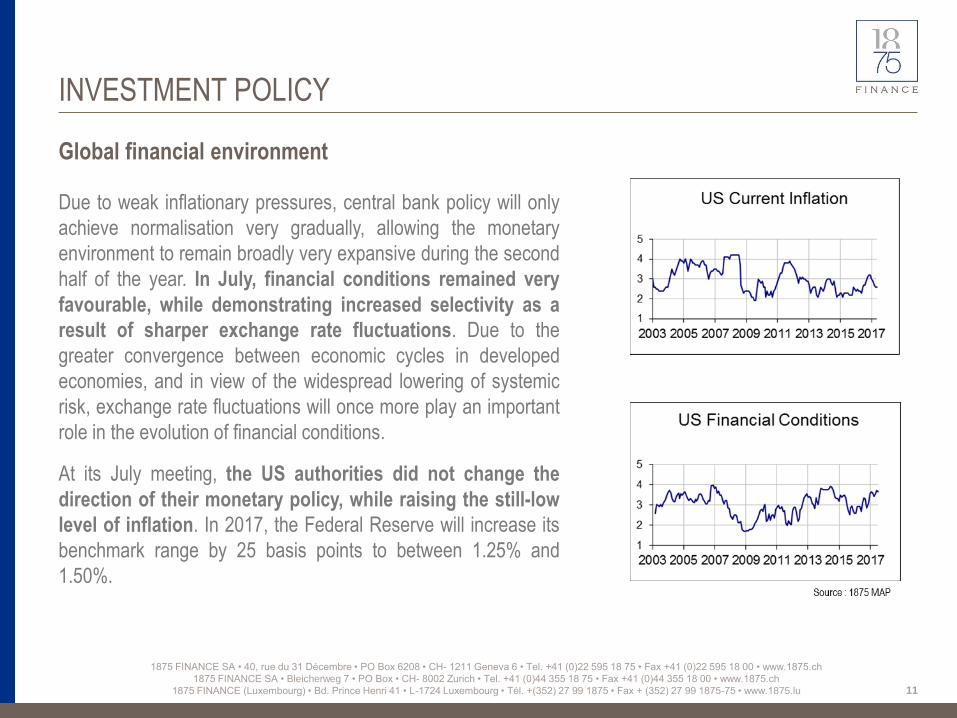

Global financial environment

Due to weak inflationary pressures, central bank policy will only

achieve normalisation very gradually, allowing the monetary

environment to remain broadly very expansive during the second

half of the year. In July, financial conditions remained very

favourable, while demonstrating increased selectivity as a

result of sharper exchange rate fluctuations. Due to the

greater convergence between economic cycles in developed

economies, and in view of the widespread lowering of systemic

risk, exchange rate fluctuations will once more play an important

role in the evolution of financial conditions.

At its July meeting, the US authorities did not change the

direction of their monetary policy, while raising the still-low

level of inflation. In 2017, the Federal Reserve will increase its

benchmark range by 25 basis points to between 1.25% and

1.50%.

12

1875 FINANCE SA • 40, rue du 31 Décembre • PO Box 6208 • CH- 1211 Geneva 6 • Tel. +41 (0)22 595 18 75 • Fax +41 (0)22 595 18 00 • www.1875.ch

1875 FINANCE SA • Bleicherweg 7 • PO Box • CH- 8002 Zurich • Tel. +41 (0)44 355 18 75 • Fax +41 (0)44 355 18 00 • www.1875.ch

1875 FINANCE (Luxembourg) • Bd. Prince Henri 41 • L-1724 Luxembourg • Tél. +(352) 27 99 1875 • Fax + (352) 27 99 1875-75 • www.1875.lu

INVESTMENT POLICY

In addition, during the second half of the year, it will begin to reduce its

balance sheet assets in accordance with the terms laid out in its June

press release.

Having left its policy unchanged in June, the European Central Bank

will keep its key interest rates at a low level until the end of the

year in consideration of a too-low general price level. The reduction in

cyclical risk and the acceleration of the reflation process will

nonetheless allow it to clarify the plan for its tapering off of bond

purchases, which will be implemented from 2018. The monetary

environment has deteriorated marginally following the

strengthening of the Euro, while still remaining very expansive,

thanks in particular to the especially low level of interest rates

relative to the recovery in nominal growth.

In its last review of the economic and monetary situation, the Swiss

National Bank maintained its expansionary monetary policy unchanged.

The decline in the Euro over the past few months will allow the

Swiss authorities to gradually put a brake on the strong growth of

their balance sheet without challenging the significant expansion

of financial conditions.

Source : 1875 MAP

13

1875 FINANCE SA • 40, rue du 31 Décembre • PO Box 6208 • CH- 1211 Geneva 6 • Tel. +41 (0)22 595 18 75 • Fax +41 (0)22 595 18 00 • www.1875.ch

1875 FINANCE SA • Bleicherweg 7 • PO Box • CH- 8002 Zurich • Tel. +41 (0)44 355 18 75 • Fax +41 (0)44 355 18 00 • www.1875.ch

1875 FINANCE (Luxembourg) • Bd. Prince Henri 41 • L-1724 Luxembourg • Tél. +(352) 27 99 1875 • Fax + (352) 27 99 1875-75 • www.1875.lu

INVESTMENT POLICY

During its July session, the Bank of England maintained its base rate at

0.25% as well as its program of corporate loan purchases at GBP 10

billion and its stock of government bonds at GBP 435 billion. It has

shown a more accommodating tone for the coming months due to the

uncertainties associated with Brexit, but a more restrictive one for the long

term, considering that expectations of rising interest rates are too gradual.

Regarding its projections, it has maintained its inflation estimates

unchanged at 2.8% for 2017, but has reduced growth forecasts to 1.6%.

At its last monetary committee, the Bank of Japan left the direction of its

policy unchanged, reaffirming its diagnosis of moderate expansion

and still too-weak inflation. The base rate was kept at -0.1% and the

government bond purchasing program remained at around 80 trillion yen,

modulated so that the target 10-year government yield stays at around

zero. It has also decided to increase purchases of ETFs on equities and on

REITs by 6 trillion and 90 billion yen per year respectively. The amount held

in private bonds remained unchanged at 5.4 trillion yen. In the absence of

a significant increase in the yen, the Japanese monetary environment

will continue to be expansive in the short and medium term.Source : 1875 MAP

14

1875 FINANCE SA • 40, rue du 31 Décembre • PO Box 6208 • CH- 1211 Geneva 6 • Tel. +41 (0)22 595 18 75 • Fax +41 (0)22 595 18 00 • www.1875.ch

1875 FINANCE SA • Bleicherweg 7 • PO Box • CH- 8002 Zurich • Tel. +41 (0)44 355 18 75 • Fax +41 (0)44 355 18 00 • www.1875.ch

1875 FINANCE (Luxembourg) • Bd. Prince Henri 41 • L-1724 Luxembourg • Tél. +(352) 27 99 1875 • Fax + (352) 27 99 1875-75 • www.1875.lu

INVESTMENT POLICY

A contained inflation rate and the firmness of the AUD prompted the

Australian central bank to keep its benchmark rate unchanged,

favouring a continuing loosening of financial conditions.

Due to the weakness of the greenback and the selective decline

in returns, the monetary environment in the emerging area

remained moderately expansive overall. Depending on exchange

rate fluctuations and the evolution of inflation, it is however still

heterogeneous. It continues to be accommodating in Brazil, where

monetary authorities further lowered their base rate by 100 basis

points to 9.25% at the end of July, while it tightened in Mexico through

a raise in the repo rate from 0.25% to 7%. In Southeast Asia,

monetary policies are also on a trend towards flexibility, while

remaining less expansionary in China since the People's Bank of

China has tightened its conditions on certain loans.

Source : 1875 MAP

15

1875 FINANCE SA • 40, rue du 31 Décembre • PO Box 6208 • CH- 1211 Geneva 6 • Tel. +41 (0)22 595 18 75 • Fax +41 (0)22 595 18 00 • www.1875.ch

1875 FINANCE SA • Bleicherweg 7 • PO Box • CH- 8002 Zurich • Tel. +41 (0)44 355 18 75 • Fax +41 (0)44 355 18 00 • www.1875.ch

1875 FINANCE (Luxembourg) • Bd. Prince Henri 41 • L-1724 Luxembourg • Tél. +(352) 27 99 1875 • Fax + (352) 27 99 1875-75 • www.1875.lu

INVESTMENT POLICY

Global Tactical Allocation (asset classes):

The investment strategy recommended in July has been kept

unchanged for the month of August. In order to benefit from

continued reflation processes and the expected recovery in global

growth, equities remain significantly overweight and the sensitivity of

portfolios to interest rates is strongly reduced so as to increase

cyclicality.

In terms of tactical allocation, the following positioning is

recommended:

• Maintain a minimal exposure to short-term investments

• Increase the bond underweighting by additionally reducing

durations

• Remain overweight on equities

• Take profits on investments in international real estate to

overexpose them more moderately

• Maintain a minimal diversification on gold commitments and stay

overweight on productive materials

Source : 1875 MAP Wealth Management CHF

16

1875 FINANCE SA • 40, rue du 31 Décembre • PO Box 6208 • CH- 1211 Geneva 6 • Tel. +41 (0)22 595 18 75 • Fax +41 (0)22 595 18 00 • www.1875.ch

1875 FINANCE SA • Bleicherweg 7 • PO Box • CH- 8002 Zurich • Tel. +41 (0)44 355 18 75 • Fax +41 (0)44 355 18 00 • www.1875.ch

1875 FINANCE (Luxembourg) • Bd. Prince Henri 41 • L-1724 Luxembourg • Tél. +(352) 27 99 1875 • Fax + (352) 27 99 1875-75 • www.1875.lu

INVESTMENT POLICY

Bonds

During July, government bond markets in developed countries

have generally moved sideways, while emerging debt has

continued on its upwards trend. The markets benefited both

from the decline in USD-denominated yields and from higher

commodity prices. Within advanced nations, dollar investments

(0.2%) continued to outperform due to the narrowing of the

cyclical gap between the United States and the rest of the

world. CAD (-0.3%) and to a lesser extent CHF (-2%) bonds

corrected the most.

Under the influence of better-than-expected earnings

announcements, credit premiums tightened further, as Euro-

denominated bonds posted excess returns relative to their

counterparts denominated in USD. The high-yield borrowing

segment consolidated, penalized by the energy sector.

Source : 1875 MAP

17

1875 FINANCE SA • 40, rue du 31 Décembre • PO Box 6208 • CH- 1211 Geneva 6 • Tel. +41 (0)22 595 18 75 • Fax +41 (0)22 595 18 00 • www.1875.ch

1875 FINANCE SA • Bleicherweg 7 • PO Box • CH- 8002 Zurich • Tel. +41 (0)44 355 18 75 • Fax +41 (0)44 355 18 00 • www.1875.ch

1875 FINANCE (Luxembourg) • Bd. Prince Henri 41 • L-1724 Luxembourg • Tél. +(352) 27 99 1875 • Fax + (352) 27 99 1875-75 • www.1875.lu

INVESTMENT POLICY

With a still very expensive valuation, government bonds will

continue on their downwards trend for the next 6 months. In

the short term, bond markets will be affected by the increase in

real yields linked to a more intensive use of inputs. In the longer

term, they will be penalized by rising inflationary pressures. It is

therefore necessary to reduce exposure to reach a more

significant underweighting, and to further reduce durations.

During the second half of the year, inflation-linked bonds will

remain underweight. Conversely, variable-rate borrowings will be

privileged.

In terms of monetary allocation, assets denominated in AUD

remain overweight due to the limited short-term economic

recovery and low inflationary pressures in Australia. Investments

in USD and NOK should be reduced to be moderately

underweight, with the former being affected by higher valuations

and the latter by the expected recovery of growth in Norway.

1

2

3

4

5

2003 2005 2007 2009 2011 2013 2015 2017

EU Bonds Valorisation

18

1875 FINANCE SA • 40, rue du 31 Décembre • PO Box 6208 • CH- 1211 Geneva 6 • Tel. +41 (0)22 595 18 75 • Fax +41 (0)22 595 18 00 • www.1875.ch

1875 FINANCE SA • Bleicherweg 7 • PO Box • CH- 8002 Zurich • Tel. +41 (0)44 355 18 75 • Fax +41 (0)44 355 18 00 • www.1875.ch

1875 FINANCE (Luxembourg) • Bd. Prince Henri 41 • L-1724 Luxembourg • Tél. +(352) 27 99 1875 • Fax + (352) 27 99 1875-75 • www.1875.lu

INVESTMENT POLICY

Conversely, CAD and JPY commitments can be increased due to a

more favourable monetary environment. Investments in EUR, and to

a lesser extent in CHF and GBP, are still highly overvalued and must

be further reduced in order to be more strongly underexposed and

with durations close to their minimum level.

Regarding debtor categories, corporate bonds remain overweight

in view of the continued improvement in the financial health of

companies. Private issuers in EUR continue to be privileged in view

of the more marked improvement in their margins and their very low

level of debt.

19

1875 FINANCE SA • 40, rue du 31 Décembre • PO Box 6208 • CH- 1211 Geneva 6 • Tel. +41 (0)22 595 18 75 • Fax +41 (0)22 595 18 00 • www.1875.ch

1875 FINANCE SA • Bleicherweg 7 • PO Box • CH- 8002 Zurich • Tel. +41 (0)44 355 18 75 • Fax +41 (0)44 355 18 00 • www.1875.ch

1875 FINANCE (Luxembourg) • Bd. Prince Henri 41 • L-1724 Luxembourg • Tél. +(352) 27 99 1875 • Fax + (352) 27 99 1875-75 • www.1875.lu

INVESTMENT POLICY

Equities

Stock market indices continued to progress selectively in August,

strongly influenced by interest rate and currency movements.

Fuelled by improved financial conditions caused by lower USD

bond yields and a lower greenback, emerging markets (5.5%) and

the US (1.9%) performed the best, with the former also profiting

from rising commodity prices. Penalised by the rise in their

respective currencies, European (-0.40%) and Canadian (-0.25%)

securities temporarily declined. Thanks to the weakness of the

Swiss franc, Swiss values were very strong, rising by 1.8%.

At a sectoral level, the environment was marked by the recovery

of energy stocks (2.3%) and base materials (2.8%), which

benefited from the rise in commodity prices.

Source : 1875 MAP

20

1875 FINANCE SA • 40, rue du 31 Décembre • PO Box 6208 • CH- 1211 Geneva 6 • Tel. +41 (0)22 595 18 75 • Fax +41 (0)22 595 18 00 • www.1875.ch

1875 FINANCE SA • Bleicherweg 7 • PO Box • CH- 8002 Zurich • Tel. +41 (0)44 355 18 75 • Fax +41 (0)44 355 18 00 • www.1875.ch

1875 FINANCE (Luxembourg) • Bd. Prince Henri 41 • L-1724 Luxembourg • Tél. +(352) 27 99 1875 • Fax + (352) 27 99 1875-75 • www.1875.lu

INVESTMENT POLICY

Technology (3.7%) and telecommunications (2.9%) also

advanced strongly due to better-than-expected results and

favorable strategic announcements. Defensive sectors such as

healthcare (-0.5%) and consumption of non-durable goods (-

0.4%) underperformed.

Despite expensive levels of valuation, stocks will continue on

their upwards trend over the next 3 to 6 months and must

remain overweight. They will continue to benefit from a

particularly favourable macro-financial environment which limits

the influence of their sometimes excessive valuation. The

expansion in financial conditions will support rising multiples, and

corporate profits will continue to progress over the next few

quarters. Companies will benefit from both increased business

volumes and improved margins through a recovery in productivity.

In 2017, they will achieve an overall growth estimated at 15%.

21

1875 FINANCE SA • 40, rue du 31 Décembre • PO Box 6208 • CH- 1211 Geneva 6 • Tel. +41 (0)22 595 18 75 • Fax +41 (0)22 595 18 00 • www.1875.ch

1875 FINANCE SA • Bleicherweg 7 • PO Box • CH- 8002 Zurich • Tel. +41 (0)44 355 18 75 • Fax +41 (0)44 355 18 00 • www.1875.ch

1875 FINANCE (Luxembourg) • Bd. Prince Henri 41 • L-1724 Luxembourg • Tél. +(352) 27 99 1875 • Fax + (352) 27 99 1875-75 • www.1875.lu

INVESTMENT POLICY

In terms of geographical diversification, the relative performance of

stock exchanges will continue to be partly influenced by exchange

rate developments. For the month of August, the strategy

recommends the following guidelines:

• Strengthen exposure to British and Canadian stocks to

overweight them more strongly due to the improved financial

environment and an attractive level of valuation in international

comparison

• Retain a significant excess weighting on the Swiss and

Australian markets

• Decrease stock market investments on the Eurozone, on

Japan as a result of the rise in its currency and on the

United States in view of the further deterioration in their

valuation levels. The former, however, remains highly

overexposed, the second markedly overweight and the last

moderately over-invested

• Continue to apply a more limited overweighting to emerging

markets

1

2

3

4

5

2003 2005 2007 2009 2011 2013 2015 2017

SZ Equities

1

2

3

4

5

2003 2005 2007 2009 2011 2013 2015 2017

UK Equities

22

1875 FINANCE SA • 40, rue du 31 Décembre • PO Box 6208 • CH- 1211 Geneva 6 • Tel. +41 (0)22 595 18 75 • Fax +41 (0)22 595 18 00 • www.1875.ch

1875 FINANCE SA • Bleicherweg 7 • PO Box • CH- 8002 Zurich • Tel. +41 (0)44 355 18 75 • Fax +41 (0)44 355 18 00 • www.1875.ch

1875 FINANCE (Luxembourg) • Bd. Prince Henri 41 • L-1724 Luxembourg • Tél. +(352) 27 99 1875 • Fax + (352) 27 99 1875-75 • www.1875.lu

INVESTMENT POLICY

Currencies:

In the previous month, foreign exchange markets were characterized

by the continuation of the decline of the USD against the EUR (-

3.4%), which was caused by the narrowing in cyclical spreads. The

currency environment was also marked by the overall strengthening

of emerging currencies and the sharp rise in currencies linked to

commodity price developments such as the CAD (3.3%), AUD (2.4%)

and NOK (3.1%). In Europe, we witnessed the pronounced decline of

the Swiss franc against the Euro (4.3%).

EUR/USD: burdened with a more expensive valuation following its

recent increases, the EUR can now be reduced. It must however

remain overweight due to the decrease in its risk premium and to the

continued narrowing in currency spreads between the United States

and the Eurozone.

1

2

3

4

5

2003 2005 2007 2009 2011 2013 2015 2017

USD/EUR

23

1875 FINANCE SA • 40, rue du 31 Décembre • PO Box 6208 • CH- 1211 Geneva 6 • Tel. +41 (0)22 595 18 75 • Fax +41 (0)22 595 18 00 • www.1875.ch

1875 FINANCE SA • Bleicherweg 7 • PO Box • CH- 8002 Zurich • Tel. +41 (0)44 355 18 75 • Fax +41 (0)44 355 18 00 • www.1875.ch

1875 FINANCE (Luxembourg) • Bd. Prince Henri 41 • L-1724 Luxembourg • Tél. +(352) 27 99 1875 • Fax + (352) 27 99 1875-75 • www.1875.lu

INVESTMENT POLICY

Currencies:

CHF/EUR: after depreciating in the previous month, the CHF is now

benefiting from a lower valuation. In view of the improved economic

fundamentals of the Eurozone, the Swiss currency will continue on its

downwards trend, but in a more limited way. It should therefore be

more moderately underweighted.

GBP/EUR: The narrowing of currency spreads and the

undervaluation of the GBP will continue to allow the English

currency to rise against the EUR and be overweight.

1

2

3

4

5

2003 2005 2007 2009 2011 2013 2015 2017

GBP/EUR

1

2

3

4

5

2003 2005 2007 2009 2011 2013 2015 2017

CHF/EUR

24

1875 FINANCE SA • 40, rue du 31 Décembre • PO Box 6208 • CH- 1211 Geneva 6 • Tel. +41 (0)22 595 18 75 • Fax +41 (0)22 595 18 00 • www.1875.ch

1875 FINANCE SA • Bleicherweg 7 • PO Box • CH- 8002 Zurich • Tel. +41 (0)44 355 18 75 • Fax +41 (0)44 355 18 00 • www.1875.ch

1875 FINANCE (Luxembourg) • Bd. Prince Henri 41 • L-1724 Luxembourg • Tél. +(352) 27 99 1875 • Fax + (352) 27 99 1875-75 • www.1875.lu

INVESTMENT POLICY

Currencies:

USD/JPY: The lowering of risk premiums triggered by the improved

economic outlook and the still highly expansive monetary policy

conducted by the Bank of Japan will lead to a further decline in the yen,

requiring that its strong underweighting be maintained in the short

term.

AUD/USD: Due to the acceleration of global growth and the resumption

of the rise in base metal prices, the Australian currency, which is still

undervalued, will continue to appreciate, justifying its overweighting.

USD/CAD: Due to its strong recovery, the CAD is now less undervalued.

It will progress in a more contained manner and must therefore be

less highly overexposed.

1

2

3

4

5

2003 2005 2007 2009 2011 2013 2015 2017

USD/YEN

1

2

3

4

5

2003 2005 2007 2009 2011 2013 2015 2017

USD/CAD

25

1875 FINANCE SA • 40, rue du 31 Décembre • PO Box 6208 • CH- 1211 Geneva 6 • Tel. +41 (0)22 595 18 75 • Fax +41 (0)22 595 18 00 • www.1875.ch

1875 FINANCE SA • Bleicherweg 7 • PO Box • CH- 8002 Zurich • Tel. +41 (0)44 355 18 75 • Fax +41 (0)44 355 18 00 • www.1875.ch

1875 FINANCE (Luxembourg) • Bd. Prince Henri 41 • L-1724 Luxembourg • Tél. +(352) 27 99 1875 • Fax + (352) 27 99 1875-75 • www.1875.lu

Important Legal Information

This publication is intended for information purposes only, and should not be construed as an offer, recommendation or solicitation for sale, purchase or engagement in any other transaction.

Furthermore, by offering information, products or services via this publication, no solicitation is made to any person to use such information, products or services in jurisdictions where the provision of

such information, products or services is prohibited by law or regulation. All material is provided without express or implied warranties or representations of any kind and no liability for any direct or

indirect damages arising out of the use of this information is accepted.

All information contained in this publication has been prepared by 1875 FINANCE SA on the basis of publicly available information, internally developed data and other sources believed to be reliable.

It is for general informational purposes only and should not be construed as an individualised recommendation or personalised investment, tax or legal advice. The information is subject to change

without notice. Reasonable care has been taken to ensure that the materials are accurate and that the opinions stated are fair and reasonable. All opinions and estimates constitute our judgment as

of the date of publication and do not constitute general or specific investment advice.

Investments in the asset classes mentioned herein may not be suitable for all recipients. Past performance is no guarantee or indication for future results. The price, value of, and income from

investments in any asset class mentioned in this publication may experience upward and downward movement and investors may not get back the amount invested. International investing includes

risks related to political and economic uncertainties in foreign countries, as well as currency risk. Any investment should be made only after thoroughly reading the current prospectus and/or other

documentation/information available. Nothing contained in this document constitutes legal, tax or other advice, nor should any investment or any other decisions be made solely based on this

document.

This publication is not intended for distribution to, or use by, any person or entity in any country or jurisdiction where such distribution or use would be contrary to applicable local laws or regulations

or would subject 1875 FINANCE SA to any registration requirement within such country or jurisdiction. Persons or entities in respect of whom such prohibitions apply must not use this publication.

This document is not intended for distribution in the U.S. or to U.S. persons.