Embed Size (px)

Citation preview

PAN AMERICAN SILVER CORP. ANNUAL REPORT 2010

15 Years of Harvesting Silver

VANCOUVER OFFICECORPORATE HEADQUARTERS

Pan American Silver Corp.1500 – 625 Howe StreetVancouver, British ColumbiaCanada, V6C 2T6

T. 604-684-1175 F. [email protected]

www.panamericansilver.com

MEXICO OFFICE

Plata Panamericana S.A. de C.V.T. 52-618-128-0709 x 101F. 52-618-128-0692 x 102Country Manager – Chris Warwick

PERU OFFICE

Pan American Silver Peru S.A.C.T. 51-1-618-9700 F. 51-1-618-9729Country Manager – Jorge Ugarte

ARGENTINA OFFICE

Pan American Silver ArgentinaT. 54-11-4816-3220F. 54-11-4816-3227Country Manager – Bret Boster

BOLIVIA OFFICE

Pan American Silver (Bolivia) S.A.T. 59-1-2-279-6690 F. 59-1221-54216Country Manager – Andres Gonzales

PAN

AM

ER

ICA

N S

ILVE

R C

OR

P. A

NN

UA

L RE

POR

T 2010

DIRECTORSRoss J. Beaty – ChairmanGeoff Burns – President & Chief Executive Officer Michael Carroll (Independent)Bill A. Fleckenstein (Independent)Michael J.J. Maloney (Independent)Robert Pirooz – General CounselDavid Press (Independent)Walter Segsworth (Independent)Paul B. Sweeney (Independent)

EXECUTIVE MANAGEMENT – VANCOUVERGeoff Burns – President & Chief Executive OfficerSteven Busby – Chief Operating Officer Andres Dasso – Sr. VP, Mining OperationsRob Doyle – Chief Financial Officer Delaney Fisher – Corporate Secretary & Legal CounselGeorge Greer – VP, Project DevelopmentSean McAleer – VP, Human Resources & SecurityRobert Pirooz – General CounselMichael Steinmann – Executive VP, Geology & ExplorationWayne Vincent – VP, Accounting & Financial ReportingMartin Wafforn – VP, Technical Services

AUDITORSDeloitte & Touche LLP, Chartered Accountants2800 – 1055 Dunsmuir StreetVancouver, British ColumbiaCanada, V7X 1P4

LEGAL COUNSELBorden Ladner Gervais1200 – 200 Burrard StreetVancouver, British Columbia,Canada, V7X 1T2

AUTHORIZED CAPITAL200,000,000 common shares without par value

ISSUED CAPITALDecember 31, 2010: 107,791,368 common shares

TRADING INFORMATIONNASDAQ: PAASTSX: PAA

REGISTRAR & TRANSFER AGENTComputershare Investor Services Inc.510 Burrard Street, 3rd FloorVancouver, British ColumbiaCanada, V6C 3B91-800-564-6253

ANNUAL GENERAL MEETINGWednesday, May 18, 2011Four Seasons Hotel, Seasons Ballroom 791 West Georgia St. Vancouver, BC

EXECUTIVE MANAGEMENT – VANCOUVER (L to R) Wayne Vincent, Sean McAleer, Delaney Fisher, Steve Busby, George Greer, Geoff Burns, Rob Doyle, Martin Wafforn, Michael Steinmann, Robert Pirooz, Andres Dasso.

DIRECTORS (L to R) Bill A. Fleckenstein, David Press, Robert Pirooz, Ross Beaty, Geoff Burns, Walter Segsworth, Michael Carroll, Paul Sweeney. Not pictured: Michael Maloney.

TABLE OF CONTENTS

Financial Highlights 02

Operations/Projects Map 03

Chairman’s Message to the Shareholders 04

President’s Message to the Shareholders 06

The Silver Market 2010 08

Exploration 10

Project Development: Navidad 13

Social Responsibility 16

Cautionary Note to US Investors 20

Properties at a Glance 21

Financial Statements 22

Corporate Information IBC

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

CERTAIN OF THE STATEMENTS AND INFORMATION IN THIS ANNUAL REPORT CONSTITUTE “FORWARD-LOOKING STATEMENTS” WITHIN THE MEANING OF THE UNITED STATES PRIVATE

SECURITIES LITIGATION REFORM ACT OF 1995 AND “FORWARD-LOOKING INFORMATION” WITHIN THE MEANING OF APPLICABLE CANADIAN PROVINCIAL SECURITIES LAWS RELATING

TO THE COMPANY AND ITS OPERATIONS. ALL STATEMENTS, OTHER THAN STATEMENTS OF HISTORICAL FACT, ARE FORWARD-LOOKING STATEMENTS. WHEN USED IN THIS ANNUAL

REPORT THE WORDS, “BELIEVES”, “EXPECTS”, “INTENDS”, “PLANS”, “FORECAST”, “OBJECTIVE”, “OUTLOOK”, “POSITIONING”, “POTENTIAL”, “ANTICIPATED”, “BUDGET”, AND OTHER SIMILAR

WORDS AND EXPRESSIONS, IDENTIFY FORWARD-LOOKING STATEMENTS OR INFORMATION. THESE FORWARD-LOOKING STATEMENTS OR INFORMATION RELATE TO, AMONG OTHER

THINGS: FUTURE PRODUCTION OF SILVER, GOLD AND OTHER METALS; FUTURE CASH COSTS PER OUNCE OF SILVER; THE PRICE OF SILVER AND OTHER METALS; THE EFFECTS OF LAWS,

REGULATIONS AND GOVERNMENT POLICIES AFFECTING PAN AMERICAN’S OPERATIONS OR POTENTIAL FUTURE OPERATIONS, INCLUDING BUT NOT LIMITED TO, LAWS IN THE PROVINCE

OF CHUBUT, ARGENTINA, WHICH, CURRENTLY HAVE SIGNIFICANT RESTRICTIONS ON MINING; FUTURE SUCCESSFUL DEVELOPMENT OF THE NAVIDAD PROJECT, THE LA PRECIOSA

PROJECT, AND OTHER DEVELOPMENT PROJECTS OF THE COMPANY; THE SUFFICIENCY OF THE COMPANY’S CURRENT WORKING CAPITAL, ANTICIPATED OPERATING CASH FLOW OR ITS

ABILITY TO RAISE NECESSARY FUNDS; THE ACCURACY OF MINERAL RESERVE AND RESOURCE ESTIMATES; ESTIMATED PRODUCTION RATES FOR SILVER AND OTHER PAYABLE METALS

PRODUCED BY THE COMPANY; TIMING OF PRODUCTION AND THE CASH AND TOTAL COSTS OF PRODUCTION AT EACH OF THE COMPANY’S PROPERTIES; THE ESTIMATED COST OF

AND AVAILABILITY OF FUNDING NECESSARY FOR SUSTAINING CAPITAL; ONGOING OR FUTURE DEVELOPMENT PLANS AND CAPITAL REPLACEMENT, IMPROVEMENT OR REMEDIATION

PROGRAMS; THE ABILITY OF THE COMPANY TO REDUCE ENVIRONMENTAL IMPACTS, INCLUDING A REDUCTION IN GREENHOUSE GAS EMISSIONS, AND TO IMPROVE SUSTAINABILITY IN ITS

OPERATIONS AND PROJECTS; THE ESTIMATES OF EXPECTED OR ANTICIPATED ECONOMIC RETURNS FROM THE COMPANY’S MINING PROJECTS, AS REFLECTED IN TECHNICAL REPORTS

OR OTHER ANALYSES PREPARED IN RELATION TO DEVELOPMENT OF PROJECTS; ESTIMATED EXPLORATION EXPENDITURES TO BE INCURRED ON THE COMPANY’S VARIOUS PROPERTIES;

FORECAST CAPITAL AND NON-OPERATING SPENDING; FUTURE SALES OF THE METALS, CONCENTRATES OR OTHER PRODUCTS PRODUCED BY THE COMPANY; AND THE COMPANY’S PLANS

AND EXPECTATIONS FOR ITS PROPERTIES AND OPERATIONS.

THESE STATEMENTS REFLECT THE COMPANY’S CURRENT VIEWS WITH RESPECT TO FUTURE EVENTS AND ARE NECESSARILY BASED UPON A NUMBER OF ASSUMPTIONS AND ESTIMATES

THAT, WHILE CONSIDERED REASONABLE BY THE COMPANY, ARE INHERENTLY SUBJECT TO SIGNIFICANT BUSINESS, ECONOMIC, COMPETITIVE, POLITICAL AND SOCIAL UNCERTAINTIES

AND CONTINGENCIES. MANY FACTORS, BOTH KNOWN AND UNKNOWN, COULD CAUSE ACTUAL RESULTS, PERFORMANCE OR ACHIEVEMENTS TO BE MATERIALLY DIFFERENT FROM

THE RESULTS, PERFORMANCE OR ACHIEVEMENTS THAT ARE OR MAY BE EXPRESSED OR IMPLIED BY SUCH FORWARD-LOOKING STATEMENTS CONTAINED IN THIS ANNUAL REPORT

AND THE COMPANY HAS MADE ASSUMPTIONS AND ESTIMATES BASED ON OR RELATED TO MANY OF THESE FACTORS. SUCH FACTORS INCLUDE, WITHOUT LIMITATION: FLUCTUATIONS

IN SPOT AND FORWARD MARKETS FOR SILVER, GOLD, BASE METALS AND CERTAIN OTHER COMMODITIES (SUCH AS NATURAL GAS, FUEL OIL AND ELECTRICITY); FLUCTUATIONS IN

CURRENCY MARKETS (SUCH AS THE PERUVIAN SOL, MEXICAN PESO, ARGENTINE PESO, BOLIVIAN BOLIVIANO AND CANADIAN DOLLAR VERSUS THE U.S. DOLLAR); RISKS RELATED

TO THE TECHNOLOGICAL AND OPERATIONAL NATURE OF THE COMPANY’S BUSINESS; CHANGES IN NATIONAL AND LOCAL GOVERNMENT, LEGISLATION, TAXATION, CONTROLS OR

REGULATIONS AND POLITICAL OR ECONOMIC DEVELOPMENTS IN CANADA, THE UNITED STATES, MEXICO, PERU, ARGENTINA, BOLIVIA OR OTHER COUNTRIES WHERE THE COMPANY MAY

CARRY ON BUSINESS IN THE FUTURE; RISKS AND HAZARDS ASSOCIATED WITH THE BUSINESS OF MINERAL EXPLORATION, DEVELOPMENT AND MINING (INCLUDING ENVIRONMENTAL

HAZARDS, INDUSTRIAL ACCIDENTS, UNUSUAL OR UNEXPECTED GEOLOGICAL OR STRUCTURAL FORMATIONS, PRESSURES, CAVE-INS AND FLOODING); RISKS RELATING TO THE CREDIT

WORTHINESS OR FINANCIAL CONDITION OF SUPPLIERS, REFINERS AND OTHER PARTIES WITH WHOM THE COMPANY DOES BUSINESS; INADEQUATE INSURANCE, OR INABILITY TO OBTAIN

INSURANCE, TO COVER THESE RISKS AND HAZARDS; EMPLOYEE RELATIONS; RELATIONSHIPS WITH AND CLAIMS BY LOCAL COMMUNITIES AND INDIGENOUS POPULATIONS; AVAILABILITY

AND INCREASING COSTS ASSOCIATED WITH MINING INPUTS AND LABOUR; THE SPECULATIVE NATURE OF MINERAL EXPLORATION AND DEVELOPMENT, INCLUDING THE RISKS OF

OBTAINING NECESSARY LICENSES AND PERMITS AND THE PRESENCE OF LAWS AND REGULATIONS THAT MAY IMPOSE RESTRICTIONS ON MINING, INCLUDING THOSE CURRENTLY IN

THE PROVINCE OF CHUBUT, ARGENTINA; DIMINISHING QUANTITIES OR GRADES OF MINERAL RESERVES AS PROPERTIES ARE MINED; GLOBAL FINANCIAL CONDITIONS; THE COMPANY’S

ABILITY TO COMPLETE AND SUCCESSFULLY INTEGRATE ACQUISITIONS AND TO MITIGATE OTHER BUSINESS COMBINATION RISKS; CHALLENGES TO, OR DIFFICULTY IN MAINTAINING, THE

COMPANY’S TITLE TO PROPERTIES AND CONTINUED OWNERSHIP THEREOF; THE ACTUAL RESULTS OF CURRENT EXPLORATION ACTIVITIES, CONCLUSIONS OF ECONOMIC EVALUATIONS,

AND CHANGES IN PROJECT PARAMETERS TO DEAL WITH UNANTICIPATED ECONOMIC OR OTHER FACTORS; INCREASED COMPETITION IN THE MINING INDUSTRY FOR PROPERTIES,

EQUIPMENT, QUALIFIED PERSONNEL, AND THEIR COSTS; AND THOSE FACTORS IDENTIFIED UNDER THE CAPTION “RISKS RELATED TO PAN AMERICAN’S BUSINESS” IN THE COMPANY’S

MOST RECENT FORM 40-F AND ANNUAL INFORMATION FORM FILED WITH THE UNITED STATES SECURITIES AND EXCHANGE COMMISSION AND CANADIAN PROVINCIAL SECURITIES

REGULATORY AUTHORITIES. INVESTORS ARE CAUTIONED AGAINST ATTRIBUTING UNDUE CERTAINTY OR RELIANCE ON FORWARD-LOOKING STATEMENTS. ALTHOUGH THE COMPANY

HAS ATTEMPTED TO IDENTIFY IMPORTANT FACTORS THAT COULD CAUSE ACTUAL RESULTS TO DIFFER MATERIALLY, THERE MAY BE OTHER FACTORS THAT CAUSE RESULTS NOT TO BE AS

ANTICIPATED, ESTIMATED, DESCRIBED OR INTENDED. THE COMPANY DOES NOT INTEND, AND DOES NOT ASSUME ANY OBLIGATION, TO UPDATE THESE FORWARD-LOOKING STATEMENTS

OR INFORMATION TO REFLECT CHANGES IN ASSUMPTIONS OR CHANGES IN CIRCUMSTANCES OR ANY OTHER EVENTS AFFECTING SUCH STATEMENTS OR INFORMATION, OTHER THAN AS

REQUIRED BY APPLICABLE LAW.

Our mission is to be the largest low-cost primary silver producer in the world and our strategy to

achieve this is to continuously increase our silver reserves and our low-cost silver production through

the efficient operation of our existing mines and the responsible development of our projects. In 2010,

our fifteenth consecutive year of production growth, we produced a record 24.3 million ounces of

silver and generated the highest financial returns in our history. At the same time, we earned several

awards for our commitment to the safety of our operations and the sustainable development of the

communities where we operate. Fifteen years on, Pan American Silver remains as committed as

ever, to generating solid returns for our shareholders and well-being for all of our stakeholders.

HIGHLIGHTS OF 2010PRODUCTION 2010 2009

Silver ounces 24,285,794 23,043,539

Gold ounces 89,556 100,704

Zinc tonnes 43,103 44,246

Lead tonnes 13,628 14,328

Copper tonnes 5,221 6,446

Cash costs per silver ounce1 $ 5.69 $ 5.53

Total cost per silver ounce1 $ 9.51 $ 9.57

Average silver price (London fix) $ 20.14 $ 14.67

FINANCIAL (millions except per share amount)

Sales $ 632.0 $ 454.8

Mine operating earnings2 $ 239.8 $ 126.0

Net income $ 112.6 $ 62.0

Net income per share (basic) $ 1.05 $ 0.71

Cash flow from operating activities3 $ 218.3 $ 151.7

STAKEHOLDERS

Common shares outstanding at Dec 31 (millions) 107.8 105.1

Employees and Contractors 7,068 6,729

1 Cash costs per silver ounce and total costs per silver ounce are non-GAAP measures. A reconciliation is

included in the Company’s MD&A on page 44.2 Mine operating earnings are equal to sales less cost of sales less depreciation and amortization.3 Net cash flow from operations is shown before adjustments for non-cash working capital items.

A SENIOR SILVER PRODUCER

WITH AN OUTSTANDING

GROWTH PROFILE

In 2010, Pan American Silver produced 24.3 million

ounces of silver. With seven operating mines

and two key development projects, Pan American

offers outstanding exposure to silver and a growth

profile that is second to none in its industry.

PAN AMERICAN SILVER CORP. | ANNUAL REPORT 20102

ALAMO DORADO | MEXICO

HEAD OFFICE, VANCOUVER

1 ALAMO DORADO

2 LA PRECIOSA (JV)

3 LA COLORADA

4 QUIRUVILCA

5 HUARON

6 MOROCOCHA

7 PICO MACHAY

8 SAN VICENTE

9 CALCATREU

10 NAVIDAD

11 MANANTIAL ESPEJO

CANADA

MEXICO

NORTH AMERICA

SOUTH AMERICA

PERU

BOLIVIA

ARGENTINA

MINING OPERATIONS

DEVELOPMENT PROJECTS

1

2

3

4

5

6

7

8

9

10

11

3OPERATIONS / PROJECTS MAP

CHAIRMAN’S MESSAGE

TO SHAREHOLDERS

It is again my absolute pleasure to write to our shareholders and express my delight at how well our Company is performing. We had another record year in 2010 and, quite frankly, I genuinely feel that Pan American’s future has never been more promising. This is mainly due to three things:

(1) Our exceptional financial condition. We ended 2010 with cash and near-cash holdings of $360 million, working capital of $434 million and no debt. We are generating very significant amounts of cash today and I expect we will be able to readily finance our future growth plans and our growing dividends.

(2) Our enormous Navidad silver project in Argentina.I believe that we will be able to commence Navidad’s development near the end of 2011, which will lead to a dramatic increase in our silver production from today’s level of about 24 million ounces annually to over 40 million ounces. This should position Pan American as the world’s largest primary silver mining company and allow us to deliver even greater financial returns to our shareholders. Navidad’s plus billion ounces of silver reserves and resources will profoundly increase our leverage to higher silver prices.

(3) Our extraordinary management team. We have built or done major expansions at five mines in the last seven years, on budget and on schedule. This is much easier said than done. Our record is a testament to the high quality of our operating, development, administrative and

financial teams. Pan American is blessed to have such fine men and women working to build our enterprise, and to have tremendous support of the communities and countries where we work and the outstanding service companies and contractors that assist our operations.

Pan American Silver Corp. is now one of the world’s “senior” silver producers, and is seen as a market and management leader in the silver mining industry. I hope all shareholders feel as proud as I am about this achievement, and at our having done it while:

Preserving healthy and safe working conditions for our workers,

Applying honest and ethical business practices, and,

Maintaining open and transparent reporting, and good corporate governance.

We have an excellent reputation in the mining industry and we have earned it with good practices. This alone is worth celebrating, but we have also delivered to our shareholders excellent financial returns and none better than the year just ended.

With Navidad, we are today poised to take another great leap forward – kind of like we made in 2002 when we began an aggressive mine development program that moved us from being a one-mine company to a seven-mine company by 2009. I hope you share my excitement

“We ended 2010

with cash and

near-cash holdings

of $360 million,

working capital of

$434 million and

no debt.”

Ross J. Beaty Chairman

PAN AMERICAN SILVER CORP. | ANNUAL REPORT 20104

about this potential and will watch as we execute it. Development of Navidad will give Pan American something it has never had: a world-class, long-life and low-cost silver mine. We expect we will have the same positive experience we have had with our Manantial Espejo Mine, located like Navidad in the great silver mining country of Argentina – a country that, after all, has

“silver” embedded in its name.

Silver prices are in an amazing up trend for fundamental reasons: more demand than supply. Silver prices, like gold prices and most other commodities, are responding to secular forces – long-term weakness in the US dollar; extraordinary industrial demand growth in China; unprecedented investor demand for silver coins, bars and ETF silver bullion and new commodity asset classes that are bringing more investment funds into physical metal ownership. All of these factors are giving us robust metals markets, with none as strong as the silver market. Silver has outperformed gold in recent months and many are calling for even higher prices ahead. Our record silver production could not have been better timed to coincide with such good silver markets!

I know I speak for all our shareholders when I extend my thanks to all of Pan American’s Board of Directors for their hard work and dedication, and to our management teams and employees at all our operations and project locations for such outstanding results in 2010. By the same token I extend my thanks to our shareholders for their support – in good times like now, and in the tough

times we had to live through from 1997-2002 and during the global financial meltdown in late 2008 and early 2009. We are today laying the building blocks for our next “great leap forward” with development of Navidad and other growth projects in the coming years, and I look forward to reporting on these projects in my next message to you in 2012.

Ross J. Beaty Chairman

5CHAIRMAN’S MESSAGETO SHAREHOLDERS

LA COLORADA | MEXICO

PRESIDENT’S MESSAGE

TO SHAREHOLDERS

When Pan American Silver was created in 1994, the silver market was vastly different from what it is today. Silver demand far exceeded new mine supply, an ounce of silver sold for approximately $5 and there were only a handful of mining companies that focused on silver mining and offered real exposure to the metal. Fast forward 15 years and the face of the silver industry has changed dramatically: the number of companies focused on silver has multiplied, competition for silver deposits has intensified, silver has regained its role as a store of value and the price of silver has been on a tear, hitting new records almost daily.

Just like the silver industry, through this time Pan American has also experienced a dramatic change. From being a newcomer to the industry with just one mining operation in Peru, in just 15 years we have become the second-largest primary silver producer in the world, with seven mining operations in four different countries across Latin America and over 7,000 employees worldwide.

But we have not just grown; we have matured as an organization, forging ourselves a reputation as a well-founded and experienced mining Company that delivers on its production targets; generating solid financial returns for our shareholders and well-being for the communities where we operate. This was never more evident than in 2010, when once again we delivered on the forecasts we set at the beginning of the year and rewrote several important records.

Last year, our 15th consecutive year of production growth, we increased our annual silver production by 5% to a record 24.3 million ounces of silver at a cash cost of $5.69 per ounce, we generated record net income of approximately $113 million or $1.05 per share and our cash flow from operations increased to a record $218 million or $2.04 per share. As a consequence we ended 2010 with $360 million in the bank and our working capital reached an all-time high of $434 million.

Building on our operational and financial strength we were also able to achieve a historic milestone when we declared our first semi-annual cash dividend in February of 2010, and although it may have seemed modest at $0.025 per share, just a few months later we increased the frequency of our dividend distributions from semi-annual to quarterly, effectively doubling the total amount paid out to each of our shareholders annually.

Instituting a cash dividend was not only a way to reward your continued support; it was also an expression of confidence in our ability to carry on generating healthy financial returns without jeopardizing our future growth. Our fiscal discipline has enabled us to grow in an orderly and managed way. We are at the brink of what we expect will be the largest growth phase in our history, by a couple of orders of magnitude, and we are confident that we can continue to deliver superior financial returns, while we take on the task of responsibly developing the world class Navidad silver project in Argentina.

“Last year we

generated record

net income of

approximately

$113 million

or $1.05 per

share.”

Geoff Burns President & Chief Executive Officer

PAN AMERICAN SILVER CORP. | ANNUAL REPORT 20106

For Pan American, 2010 was also a year of awards. For the second time in their history, each of our Mexican operations (Alamo Dorado and La Colorada) received the prestigious “Casco de Plata” award as safest open cut and underground mining operations, respectively, in the country. Our Peruvian operations were distinguished with a prestigious award for our work with our local communities on sustainable development and our San Vicente mine in Bolivia was ranked 3rd in the entire country, across all business sectors for its efforts to support community-driven sustainable development programs. For me, these awards are as important as any of our other production or financial records, because they reflect our commitment to being fully fledged members of the communities where we work and sharing our good fortune with those who generate or contribute to it by working with us or hosting us.

Our objectives for 2011 are well defined. Our silver production will remain stable at between 23 to 24 million ounces, while we expect our gold production will be between 76,000 to 78,000 ounces. We do expect our cash costs to increase to the $7.00 to $7.50 per ounce range, as a direct consequence of the inflationary pressures that all companies which operate in the resource sector are facing. Given the current metal price environment we should continue to generate excellent cash flows and healthy net income quarter after quarter throughout 2011.

While we work to optimize our maturing operating asset base, we will continue with the technical work we initiated

at our two development projects. We intend to produce a Preliminary Assessment for the La Preciosa project by mid-year, and a full Feasibility Report for the Navidad project in the fourth quarter of this year. We remain confident that our policy of open and frank communication with the local communities, the provincial and federal governments and our demonstrated construction and social integration capabilities in Argentina will ultimately lead to an amendment of the mining law in Chubut, which will pave the way for the responsible development of Navidad.

I would like to close by taking this opportunity to personally thank all of our employees and contractors whose unwavering commitment to the principles of operational excellence and safety have been the single most important driver of our success. Of course, there are our shareholders whose confidence continues to push us forward, to create or find new value through exploration, innovation and simple hard work.

Geoff Burns President & Chief Executive Officer

7PRESIDENT’S MESSAGETO SHAREHOLDERS

GOBERNADOR GREGORES | ARGENTINA

SILVER IS SHINING BRIGHT

In 2010, silver performed exceedingly well. It began the year selling at US$17.17 per ounce on the London Bullion Market and finished the year at a decades-long record of $30.63 per ounce on December 31st.

The deep economic woes in the US and Europe, coupled with worldwide fears of inflation and historically low interest rates fuelled investment demand and provided strong support for the price of silver, which remained firmly above 2009’s annual average of US$14.67 per ounce throughout the first half of 2010.

The second half of the year saw a surge in silver prices after the summer, when silver broke above the US$20 per ounce mark and never looked back. Fueled by China’s seemingly insatiable appetite for industrial metals, in particular copper, silver benefited from the “contagion effect”, which focused on silver’s industrial characteristics, particularly in the fabrication of consumer electronics.

But the main driver of silver’s strong performance has been and continues to be investment demand. The incredible

amount of cash issued in recent years by the US and some European countries is finally being re-deployed to both stock markets and commodities like gold and silver. According to the CPM Group, in 2010, investors added 123 million ounces to their silver ETFs and the combined silver ETFholdings totaled almost 600 million ounces at March 11, 2011.

Silver averaged $20.16 per ounce during 2010 and so far, in 2011 silver has remained firmly above the $30 per ounce mark, repeatedly setting new single day highs.

According to Goldfields Mineral Services (GFMS), this year the silver market will be in a small surplus; however, expectations of tight fiscal policies to curb spending and reign in the sovereign debt in the US and Europe, coupled with the rising costs of energy, fuel and food, plus the recent instability in some areas of Africa and the Middle East should be very favourable for silver as it continues to be a strategic investment for those looking to preserve their wealth. In this scenario, silver and quality silver equities should enjoy another great year.

As a primary silver producer, Pan American derives most of its revenues from silver, which contributed

65% to the Company’s total sales in 2010. At current metal prices, silver will represent approximately

66% of the Company’s total revenues in 2011, while gold is expected to be the second-largest source

of revenue accounting for approximately 15% of total sales.

40

35

30

25

20

15

10

5

0

JAN–0

6

MAR–0

6

MAY

–06

JUL–

06

SEP–06

NOW–0

6

JAN–0

7

MAR–0

7

MAY

–06

JUL–

06

SEP–06

NOV–06

JAN–0

8

MAR–0

8

MAY

–08

JUL–

08

SEP–08

NOV–08

JAN–0

9

MAR–0

9

MAY

–09

JUL–

09

SEP–09

NOV–09

JAN–1

0

MAR–1

0

MAY

–10

JUL–

10

SEP–10

NOV–10

JAN–1

1

MAR–1

1

SILVER PRICE (US$/OZ AG)

PAN AMERICAN SILVER CORP. | ANNUAL REPORT 20108

Through on-going research and the

advent of nanotechnologies, the

use of silver in new environmentally

friendlier technologies is growing

fast. Did you know silver is used in

the following applications?

MEDICINAL: silver’s antimicrobial

and bactericidal properties are put

to use in bandages and dressings

to prevent infections. With the onset

of super-bugs (antibiotic-resistant

bacteria), silver-based cleaning

agents are also used to sanitize

medical facilities and silver oxide is

also being used to treat a number of

bacterial and viral diseases.

WATER PURIFICATION: silver-

based water purifiers prevent the

buildup of bacteria and algae in

filters. Combined with oxygen, silver

is a powerful sanitizer which can

eliminate the need for chlorine in

swimming pools.

SOLAR ENERGY: environmental

concerns are driving people to look

for sources of renewable energy.

Thanks to its superior conductive

properties, silver is used in 90% of all

crystalline silicon photovoltaic cells,

the most common type of solar cell.

RECHARGEABLE BATTERIES:rechargeable lithium-ion batteries

are being replaced by silver-oxide

batteries that are safer, because

silver-zinc batteries do not contain

lithium or flammable liquids.

Also, silver micro-batteries offer

significantly more energy than

conventional batteries and are up to

95% recyclable.

THINK GREEN; THINK SILVER!

9THE SILVER MARKET

EXPLORATION

Why is it important to differentiate between Mineral Reserves and Resources? It is very important to differentiate between Mineral Resources and Mineral Reserves. Every exploration project will define first Mineral Resources, which are categorized into Inferred, Indicated and Measured Resources with increasing geological information and confidence. Mineral Resources have not proven their feasible economic extraction yet. A Mineral Reserve is the economically mineable part of a Measured or Indicated Mineral Resource demonstrated by at least a Preliminary Feasibility Study. This Study must include adequate information on mining, processing, metallurgical, economic and other relevant factors that demonstrate, at the time of reporting, that economic extraction can be justified. A Mineral Reserve includes diluting materials and allowances for losses that may occur when the material is mined. Mineral Reserves is what we extract, what generates cash flow and earnings for the company and are the base for our business.

What is the difference between brown field and green field exploration? Brown field exploration takes place in and around our producing mines on the land package surrounding the operation. It is the exploration which replaces our Reserves

mined during the year and adds Resources for future production or plant expansions. Green field exploration happens on new projects in zones where we currently don’t have an operation or any Resources. It explores for new ore bodies and if successful will ultimately prompt the construction of a new operation.

How many people are involved in Pan American’s exploration programs? We are currently employing about 70 geologists, 54 at our mine-site geology departments, or brown field exploration programs, and 16 in our green field exploration programs. In addition, we employ about 255 individuals in support functions like sampling, field assistance, diamond drilling, resource modeling, etc.

Can you summarize Pan American’s 2010 exploration results and this year’s programs?2010 was yet another successful brown field exploration year for us. We drilled over 110,000 meters at our operations and discovered 27.0 million ounces of new Proven and Probable silver Reserves, which was almost sufficient to fully replace the 28.3 million contained ounces we mined during a record production year. As of January 1st

2011, the Company had a Proven and Probable Reserves of

Michael Steinmann, Executive Vice-President Geology and Exploration speaks about Pan American’s

recent exploration success and the Company’s green field and brown field exploration programs

going forward.

Michael Steinmann Executive Vice-President Geology & Exploration

“Green field

exploration is

a way to add

value for our

shareholders”

PAN AMERICAN SILVER CORP. | ANNUAL REPORT 201010

230.8 million ounces of silver and 698,000 ounces of gold. The small Reserve decrease of 1.4% compared to last year was mainly caused by a reclassification from Reserves to Resources of about 1.9 million ounces of silver from the Pyrite Stock Piles in Peru due to the shutdown of the La Oroya smelter.

How much does Pan American spend in its exploration programs and how does this compare to other companies in the silver sector?While our Reserves are sufficient to sustain our current production levels for the next 10 years, our goal every year is obviously to keep replacing what we mine. In order to achieve this in 2011, we will spend approximately $11 million on brown field exploration, including a 108,000 meter drill program at our seven operations. Green field exploration is another way to add value for our shareholders. In 2010, we spent about $5 million on a few green field projects and in 2011 we will more than double that to about $12 million. The new properties we plan to explore are in Mexico, Peru and Argentina.

Since 2004, when it produced 11.2 million ounces of silver, Pan American has more than doubled its silver production. In fact last year the Company produced 24.3 million ounces of silver. How much of this production growth was due to exploration success? In 2004 we produced over 11 million ounces of silver and had reserves of 147.5 million ounces, supporting 10 years of production at 2004 levels. In 2010 we produced over 24 million ounces of silver and we have 230 million ounces

silver Reserves, supporting 10 years of production at current levels. Over the last 7 years we have been very successful with our brown field exploration programs. We have added a total of 169 million ounces of new silver Reserves since 2004, 21% more than what we mined in the same period. We spent a total of $46.3 million during that period for brown field exploration, which means that we added new reserves at a cost of about $27 cents per ounce, while delivering new production records year after year.

The company has seven producing mines. Which ones have the most exploration potential and how will this potential translate into their future? Our assets are covering a wide variety of types of mineralization. Epithermal low sulphidation vein deposits, skarns, mantos and limestone replacements. Most of them have proved their large exploration potential by replacing mined reserves year after year. Vein deposits like La Colorada, Manantial Espejo, Huaron, Morococha or San Vicente have characteristically long mine lifes and very large exploration potential. I believe our best exploration potential is at La Colorada, Huaron, Morococha and Manantial Espejo.

Finding new deposits to maintain or grow production is vital for the long-term success of any mining company. How competitive is the silver space? Exploration success is the base of our business and the base of any mining and exploration company, hence it is extremely competitive. It is very difficult to find good primary silver deposits as they are extremely rare. Many silver deposits in the world battle with narrow veins, deep

11EXPLORATION 11

NAVIDAD | ARGENTINA

locations, difficult metallurgy and high costs. That’s what makes Navidad such a valuable and important deposit as it has high grade ore that is amenable to low strip ratio surface mining.

Navidad is a big bet for Pan American Silver. Why is it so important and how would you describe it from a geologists’ perspective?It is very difficult to find silver deposits and large deposits are extremely rare. As a matter of fact there are only a

SILVER (MILLIONS OF OUNCES OF CONTAINED SILVER)

RESERVES Dec 31, 2009 MINED 2010 GAINED/LOST RESERVES Dec 31, 20103

Morococha (92.2%) 37.98 (3.03) 2.68 37.62

Huaron 64.23 (3.86) (1.08) 59.29

Quiruvilca 3.93 (1.47) 1.48 3.94

La Colorada 30.43 (4.21) 12.11 38.34

Alamo Dorado 30.89 (7.90) 4.17 27.17

San Vicente (95%) 28.39 (3.39) 3.05 28.04

Manantial Espejo 36.13 (4.41) 4.60 36.32

Silver Stockpiles 2 1.94 - - -

TOTAL4 233.92 (28.27) 27.01 230.72

1 For the complete breakdown of reserves and resources by property and category, please refer to pages 54 and 55 of this annual report

2 Pan American believes that Doe Run’s La Oroya smelter, the only buyer of the Pyrite Stockpiles, is unlikely to resume operations in the near future. As a result, management decided to write off the book value of that asset at

December 31, 2010 and has reclassified the 1.94 million ounces of Silver contained in the Pyrite Stockpiles from Reserves to Resources

3 Proven and Probable Mineral Reserves were estimated using appropriate cut-off grades based on assumed metal prices of Ag: $18.00/oz, Au: $1,100/oz,Pb: $1,950/tonne, Cu: $6,500/tonne, Zn: $1,950/tonne

4 Totals may not add up due to rounding

handful of deposits known with over 700 million ounces of total silver Resources and most of them are already in, or will soon be in production, creating substantial shareholder value. To my knowledge, Navidad is currently the world’s largest undeveloped silver deposit in the world. It will help to create a far larger and more profitable Pan American Silver with a very big, long-life and low-cost asset. I am also excited about our very large land holdings around Navidad, which have an incredible exploration potential to add new Resources and Reserves in the future.

PAN AMERICAN SILVER CORP. | ANNUAL REPORT 201012

NAVIDAD | DRILL CORE SAMPLE

PROJECT DEVELOPMENT:

NAVIDAD

What is the history of Navidad?In Late 2002, Daniel Bussandri, a geologist working for IMA Exploration Inc., discovered untouched outcropping mineralization on a hill located in the North-central plateau of the Chubut Province while he was following-up on sample data collected the year before by Normandy Geologists. Soon he found surface exposed mineralization over what later became known as the Navidad Hill, Connector Zone, Galena Hill and Barite Hill deposits. IMA geologists conducted additional geologic mapping and surface sampling of the area until the first discovery drill hole was completed in late 2003 on Navidad Hill; a 58.4 meter intercept of ore with an average silver grade of 111 grams per tonne. Aquiline Resources Inc. successfully challenged IMA’s use of Normandy’s data in a British Columbia courtroom arguing that IMA had breached a confidentiality agreement signed as part of a Newmont sale for another project in Argentina (Newmont acquired Normandy and then withdrew work in the area). Except for the legal disruption in which Navidad was handed over to Aquiline Resources Inc. in July 2006, geologic efforts and intensive drilling continued for 6 years resulting in the current mineral Resource, which is arguably the single largest undeveloped silver Resource in the world. We

gained control over Navidad when we acquired Aquiline in January 2010.

What are Pan American’s plans for Navidad?We are committed to developing Navidad into a profitable silver mine. It has the potential to essentially double our production and profits, but it also possesses the ability to provide significant economic stimulus for the local communities in an isolated rural region that has been facing steady population declines. In 2010, we produced a Preliminary Assessment which illustrated that Navidad is unquestionably technically and economically robust enough to justify immediate development; however, there is a Provincial law in Chubut banning the use of open pit mining, which must be reformed before development can proceed. We are focused on sharing the concepts of the Project with the local and provincial residents describing the potential benefits and predicted impacts Navidad would have on the region anticipating this will persuade a reform to the current Provincial ban on open pit mining. Meanwhile we are taking full advantage of the time to optimize and enhance the project design, incorporating comments, concerns, and suggestions from the Chubut residents. The province of Chubut is fortunate to have abundant natural resources and by partnering with a responsible mine developer

Steve Busby Chief Operating Officer

Steve Busby, Chief Operating Officer, discusses the Navidad deposit, arguably the largest

undeveloped primary silver deposit in the world, and how Pan American is advancing this project

into the development stage.

“Navidad has

the potential to

essentially double

our production

and profits.”

13PROJECT DEVELOPMENT: NAVIDAD

like Pan American, it has an opportunity to improve the infrastructure, provide adequate employment opportunities, create successful businesses, and make vast improvements in basic services such as access to health care, schools, water distribution, and improved transportation networks.

Why is there a ban in Chubut on Open Pit Mining?The open pit mining ban is the result of a legislative act passed in April of 2003, aimed at stopping an open pit cyanide leach gold mine development near the picturesque town of Esquel, located 200 kilometers west of Navidad in the foothills of the Andes. The legislation was a response to severe public opposition against a gold mine project near Esquel because there was insufficient public participation in the design of the project. The initial legislation included a provision to allow zoning of the Province into areas where open pit mine developments could proceed, which has yet to be acted on. It is important to note that the Navidad Project does not require the use of cyanide for development. We believe there is significant public support growing for Navidad which will sway the legislators of Chubut to reform the open pit mining ban during 2011, specifically in the area of the Central Plateau, where Navidad is situated.

This is a significant project, larger than anything your Company has ever undertaken. Is Pan American capable of building Navidad?Yes, we are a silver mining and development company currently operating seven different mines that we had developed in four different Latin American countries. We also have two development stage projects, one in Mexico (La Preciosa) and one in Argentina (Navidad). By far the most important of these projects is Navidad. We employ over 7,000 people directly at our mines and development projects. In Argentina we employ over 800 people in Argentina, 99% of them are Argentinean, 650 in Santa Cruz, 150 in Chubut and several others elsewhere in the country, including our regional headquarters in Buenos Aires. Our reputation for excellence, both in our technical ability to develop environmentally sensitive operations, and also for our commitment to integrate with the local communities where we operate, is well known and we have been recognized with numerous awards for employee safety and sustainable development programs. We have been in Argentina since 2002 with the successful development of the Manantial Espejo mine in Santa Cruz, which has had a tremendous positive impact in the nearby community of Gobernador Gregores. Finally, we have and continue generating significant financial resources and means to secure the Project financing.

Can you briefly describe the Navidad Project and its impact?Navidad is located just south of Route 4, some 40kms west of the community of Gan Gan and 40kms east of the community of Gastre in the central plateau of Chubut. So far we have invested close to US$35 million in Navidad to better understand the deposit, to study the best and most environmentally sensitive methods to safely mine and produce silver and to complete a Preliminary Assessment describing the Project. The Assessment estimates that a total of 431 million tonnes of material could be surface mined from eight deposits to generate 89.4 million tonnes of ore, which could be treated in a 15,000 tonne per day floatation concentrator for a period of 17 years. The project would produce two concentrates: a silver-rich copper concentrate and a lead concentrate containing silver values. Production is expected to average 19.8 million ounces of silver annually at a cash cost of just over $6 per ounce during the first 5 years and 17 million ounces of silver at a cash cost of nearly $7 per ounce over the life of the mine, with estimated total silver recovered being 275.5 million ounces. We estimate that construction and commissioning activities would demand approximately 1,500 individuals between employees and contractors, which would represent approximately $167 million in direct wages. Navidad’s total capital estimate of $760 million includes approximately $450 million in local wages and benefit payments as well as locally-supplied goods and services. Once in commercial production, Navidad is expected to provide direct employment to approximately 500 employees and contractors. Mindful of the environment, it is our intention to obtain most of the water required to run the processing plant by recycling water from the tailings facility, adding a limited amount of fresh water from surface mine dewatering systems and to a lesser degree from nearby ground water wells. Technical field work carried out to date indicates that there is more than sufficient ground water at or near the Project to provide water for the life of the operation without impacting the needs of local communities and ranches. Energy for the Project could be supplied from a twin 330 KV power line that runs approximately 100 kilometers south.

Are there any unique aspects to the Navidad Project?Navidad has a very large Resource of over 630 million ounces of silver and nearly 3 billion pounds of lead in the Measured and Indicated category and over 100 million more ounces of silver and nearly 600 million pounds of lead in the Inferred category, making it the world’s largest undeveloped primary silver Resource. The mineralization outcrops to the surface and has attractive grades, ideal for surface

PAN AMERICAN SILVER CORP. | ANNUAL REPORT 201014

mining and conventional floatation processing. We have a large 10,000 hectare land position immediately surrounding the existing known deposits and feel there are significant opportunities to grow the Resources by continuing exploration in remaining untested prospective terrain. There are significant opportunities to improve silver recoveries above the levels described in our Preliminary Assessment, as there is a significant amount of silver trapped in pyrites that are not amenable to conventional floatation and off-shore concentrate sales. We are learning more about the deposits and the mineralization and we are discovering new opportunities for reducing operating costs and enhancing profitability with our increasing knowledge. Navidad is truly a rare and uniquely rich primary silver Project.

What are your specific plans for 2011 at Navidad?First and foremost we are focused on working to disseminate descriptions of the Project to the residents of Chubut and invite them to join us in optimizing the designs to accommodate their needs and concerns. This includes conducting numerous site visits with local residents and initiating a comprehensive communications campaign. Simultaneously we will continue efforts to prepare the Project’s Environmental Impact Assessment, and assemble a feasibility study. We are also advancing additional definition drilling and have initiated basic engineering so we could move rapidly into development once the law reforms are passed and the permits are received. Overall we are expecting to spend nearly $45 million in 2011 inclusive of the efforts of 150 local individuals assigned to Navidad. We anticipate significant improvements to the Project from the optimization studies currently underway, particularly in respect to reducing operating costs and improving metal recoveries.

15PROJECT DEVELOPMENT: NAVIDAD

SOCIAL RESPONSIBILITY

Through sustainability we try to create value for all of our stakeholders, because it is clear that our responsibility towards our host communities extends beyond the life of our operations. Our mission is to conduct our activities in an environmentally responsible manner and to help develop sustainable economic activities in the areas around operations that we influence.

Geoff Burns, President & CEO, believes, “Fundamental responsibility to and accountability for the environment are core values. We have a history of investing in new sustainable technologies to help mitigate the environmental impact of our activities. In addition, Pan American takes great pride in the productive, proactive and open relationships that have forged with the communities in the areas where we operate.”

Pan American Silver recognizes that the skills and the dedication of our employees and contractors are the most important drivers of our success. We also recognize the vital contribution they make to the economic prosperity of the communities in which we operate. As such, we offer career development opportunities through specialized training,

competitive remuneration, an engaging working environment and a supportive culture where fairness, respect, safety, and diversity are valued and practiced.

Our number one priority at all of our mines, development projects and exploration prospects is the safety of our employees. Our approach is to implement the highest safety standards possible and to undertake comprehensive and continuous safety training. We also comply with, and in most cases surpass, all applicable safety regulations and industry standards in the countries were we operate. This has allowed us to dramatically improve our safety record over the past five years.

We are committed to operating our mines and developing our new projects in an environmentally responsible manner. We take every measure practical to minimize and mitigate environmental impacts during all phases of the mining cycle, from exploration through project development, into full mining operations and ultimately to mine closure and reclamation. This is accomplished through careful engineering and design, prudent operating practices, continuous monitoring and by providing ongoing training

At Pan American Silver, we believe that sustainability is not a secondary activity but a principle that

drives us towards the ongoing improvement of our business. Sustainability is achieved by treating our

employees as we would like to be treated, by treating the environment with the respect it deserves, and

by acting as good neighbour and active member in the communities where we operate.

PAN AMERICAN SILVER CORP. | ANNUAL REPORT 201016

17SOCIAL RESPONSIBILITY

QUIRUVILCA | PERU

MEXICO:LA COLORADA MINE – 2009 “Casco

de Plata” Safety Award (Silver

Hard Hat) by the Mexican Chamber

of Mines for safest underground

operation with more than 501 workers

ALAMO DORADO MINE – 2009

“Casco de Plata” Safety Award

(Silver Hard Hat) by the Mexican

Chamber of Mines for safest open pit

operation with less than 500 workers

LA COLORADA MINE – Attained the

Clean Industry Certification

ALAMO DORADO MINE –

Successfully renewed its Socially

Responsible Business certification

PERU:The National Chamber of Mining,

Petroleoum and Energy awarded PAN

AMERICAN SILVER PERU the 2010

Sustainable Development Award for

the campaign for the improvement

of the nutritional health of the

population around the Morococha

mine

BOLIVIA:The National Chamber of Industry

awarded the SAN VICENTE MINE

the 3rd place in the category Best

CSR Community Driven Project,

for its community-driven business

development programs

PAN AMERICAN SILVER2010 AWARDS AND

RECOGNITIONS

and education for the employees and contractors who work at our facilities and our projects.

OUR PROGRAMS: 1. We recognize that water is a finite resource, essential to sustain life and a healthy environment. We are committed to ensuring that sources of water are not negatively impacted by our operations by making sure that water is used in the most efficient way possible and recycled as much as possible, that natural water courses are maintained as much as possible, and that the quality of the water that we return to the environment is consistently better than regulatory requirements.

2. We are well aware of the challenges and risks associated with climate change and are committed to reducing our Greenhouse Gas (GHG) emissions through improvements in energy efficiency and the use of renewable energy.

3. We have intensified our efforts to reduce the amount of wastes generated by our operations by continually upgrading our waste management and disposal programs. We investigate and then apply alternative procedures and technologies to reduce waste and work with local companies to increase the amount of waste that is reclaimed and reused.

4. Our community outreach programs are consistent with a “good neighbour attitude.” Our programs are born out of local contact and the information obtained by our local offices. We typically focus on education, health, infrastructure improvements and the promotion of alternative economic activities. We maintain offices with knowledgeable staff in each of our host communities to make it easy for residents to ask questions, find out more about our operations and provide feedback and suggestions. A strong local presence also ensures that we are better able to understand community issues and priorities.

The practices employed by Pan American Silver have demonstrated that care for our employees, our environment and our communities not only makes good business sense but also provides long lasting benefits to the land and its people.

Ross Beaty, Chairman of the Board, adds, “The term “sustainable mining” might seem an oxymoron to some: how can extraction of non-renewable resources ever be sustainable? But Pan American Silver Corp. is proving this can be achieved, through its dedication to community engagement, health, safety and environmental excellence, and fair-minded, transparent and collaborative management practices.”

PAN AMERICAN SILVER CORP. | ANNUAL REPORT 201018

19SOCIAL RESPONSIBILITY

MANANTIAL ESPEJO | ARGENTINA

TECHNICAL INFORMATION

MICHAEL STEINMANN, P.GEO., EXECUTIVE VP GEOLOGY & EXPLORATION, AND MARTIN WAFFORN, P.ENG., VP TECHNICAL SERIVCES, EACH OF WHOM ARE QUALIFIED PERSONS, AS THE

TERM IS DEFINED IN NATIONAL INSTRUMENT 43-101 “NI 43-101”, HAVE REVIEWED AND APPROVED THE CONTENTS OF THIS ANNUAL REPORT. TECHNICAL INFORAMATION WITH RESPECT

TO NAVIDAD IS DERIVED FROM THE NI 43-101 TECHNICAL REPORT ON THE PROPERTY PREPARED BY SNOWDEN, UNDER THE SUPERVISION OF PAMELA DE MARK, P.GEO., SR. CONSULTANT

OF SNOWDEN MINING INDUSTRY CONSULTANTS. MINERAL RESOURCE ESTIMATES FOR HOG HEAVEN AND WATERLOO ARE BASED ON HISTORICAL THIRD PARTY ESTIMATES. TECHNICAL

INFORMATION FOR THE LA PRECIOSA PROPERTY IS BASED ON PUBLICLY AVAILABLE INFORMATION PUBLISHED BY ORKO SILVER.

CAUTIONARY NOTE TO US INVESTORS CONCERNING ESTIMATES OF RESERVES AND RESOURCES

THIS ANNUAL REPORT HAS BEEN PREPARED IN ACCORDANCE WITH THE REQUIREMENTS OF CANADIAN PROVINCIAL SECURITIES LAWS, WHICH DIFFER FROM THE REQUIREMENTS OF U.S.

SECURITIES LAWS. UNLESS OTHERWISE INDICATED, ALL MINERAL RESERVE AND RESOURCE ESTIMATES INCLUDED IN THIS ANNUAL REPORT HAVE BEEN PREPARED IN ACCORDANCE

WITH CANADIAN NATIONAL INSTRUMENT 43-101 – STANDARDS OF DISCLOSURE FOR MINERAL PROJECTS (‘‘NI 43-101’’) AND THE CANADIAN INSTITUTE OF MINING, METALLURGY AND

PETROLEUM CLASSIFICATION SYSTEM. NI 43-101 IS A RULE DEVELOPED BY THE CANADIAN SECURITIES ADMINISTRATORS THAT ESTABLISHES STANDARDS FOR ALL PUBLIC DISCLOSURE

AN ISSUER MAKES OF SCIENTIFIC AND TECHNICAL INFORMATION CONCERNING MINERAL PROJECTS.

CANADIAN STANDARDS, INCLUDING NI 43-101, DIFFER SIGNIFICANTLY FROM THE REQUIREMENTS OF THE UNITED STATES SECURITIES AND EXCHANGE COMMISSION (THE “SEC”),

AND INFORMATION CONCERNING MINERALIZATION, DEPOSITS, MINERAL RESERVE AND RESOURCE INFORMATION CONTAINED OR REFERRED TO HEREIN MAY NOT BE COMPARABLE

TO SIMILAR INFORMATION DISCLOSED BY U.S. COMPANIES. IN PARTICULAR, AND WITHOUT LIMITING THE GENERALITY OF THE FOREGOING, THIS ANNUAL REPORT USES THE TERMS

‘‘MEASURED RESOURCES’’, ‘‘INDICATED RESOURCES’’ AND ‘‘INFERRED RESOURCES’’. U.S. INVESTORS ARE ADVISED THAT, WHILE SUCH TERMS ARE RECOGNIZED AND REQUIRED BY

CANADIAN SECURITIES LAWS, THE SEC DOES NOT RECOGNIZE THEM. UNDER U.S. STANDARDS, MINERALIZATION MAY NOT BE CLASSIFIED AS A ‘‘RESERVE’’ UNLESS THE DETERMINATION

HAS BEEN MADE THAT THE MINERALIZATION COULD BE ECONOMICALLY AND LEGALLY PRODUCED OR EXTRACTED AT THE TIME THE RESERVE DETERMINATION IS MADE. U.S. INVESTORS

ARE CAUTIONED NOT TO ASSUME THAT ANY PART OF A “MEASURED RESOURCE” OR “INDICATED RESOURCE” WILL EVER BE CONVERTED INTO A “RESERVE”. U.S. INVESTORS SHOULD

ALSO UNDERSTAND THAT “INFERRED RESOURCES” HAVE A GREAT AMOUNT OF UNCERTAINTY AS TO THEIR EXISTENCE AND GREAT UNCERTAINTY AS TO THEIR ECONOMIC AND LEGAL

FEASIBILITY. IT CANNOT BE ASSUMED THAT ALL OR ANY PART OF “INFERRED RESOURCES” EXIST, ARE ECONOMICALLY OR LEGALLY MINEABLE OR WILL EVER BE UPGRADED TO A HIGHER

CATEGORY. UNDER CANADIAN SECURITIES LAWS, ESTIMATED “INFERRED RESOURCES” MAY NOT FORM THE BASIS OF FEASIBILITY OR PRE-FEASIBILITY STUDIES EXCEPT IN RARE CASES.

DISCLOSURE OF “CONTAINED OUNCES” IN A MINERAL RESOURCE IS PERMITTED DISCLOSURE UNDER CANADIAN SECURITIES LAWS. HOWEVER, THE SEC NORMALLY ONLY PERMITS

ISSUERS TO REPORT MINERALIZATION THAT DOES NOT CONSTITUTE “RESERVES” BY SEC STANDARDS AS IN PLACE TONNAGE AND GRADE, WITHOUT REFERENCE TO UNIT MEASURES.

THE REQUIREMENTS OF NI 43-101 FOR IDENTIFICATION OF “RESERVES” ARE ALSO NOT THE SAME AS THOSE OF THE SEC, AND RESERVES REPORTED BY THE COMPANY IN COMPLIANCE

WITH NI 43-101 MAY NOT QUALIFY AS “RESERVES” UNDER SEC STANDARDS. ACCORDINGLY, INFORMATION CONCERNING MINERAL DEPOSITS SET FORTH HEREIN MAY NOT BE

COMPARABLE WITH INFORMATION MADE PUBLIC BY COMPANIES THAT REPORT IN ACCORDANCE WITH U.S. STANDARDS.

20 PAN AMERICAN SILVER CORP. | ANNUAL REPORT 2010

SANTA CRUZ | ARGENTINA

21

operating mines

propertY tYpe LoCationproVen & proBaBLe reserVes1 2010 proDUCtion2 2011 proDUCtion ForeCast3

Huaron Underground Pasco, Peru 59.29 Moz Ag 2.6 Moz Ag at cash cost of $12.35/oz

3.1 to 3.2 Moz Ag at cash cost of $11.10 to $13.00 per oz Ag

Morococha (92.2%) Underground Junin, Peru 37.62 Moz Ag

2.6Moz Ag at cash cost of $4.43

2.6 to 2.7 Moz Ag at cash costs of $4.80 to $6.60 per oz Ag

Quiruvilca Underground La Libertad, Peru3.94 Moz Ag; 18 Koz Au

1.2 Moz Ag at cash cost of $5.87/oz

1.0 to 1.1 Moz Ag at cash cost of $8.80 to $9.90 per oz Ag

Alamo Dorado Open Pit Sonora, Mexico 27.17Moz Ag; 100.52 Koz Au

6.7 Moz Ag at cash cost of $3.16/oz

4.8 to 5.1 Moz Ag at cash cost of $5.30 to $5.70 per oz Ag

La Colorada Underground Zacatecas, Mexico38.34 Moz Ag; 44.48 Koz Au

3.7 Moz Ag at cash cost of $8.59/oz

4.1 to 4.2 Moz Ag at cash cost of $7.60 to $8.50 per oz Ag

San Vicente (95%) Underground Potosi, Bolivia 28.04 Moz Ag

3.0 Moz Ag at cash cost of $8.21/oz

3.2 to 3.3 Moz Ag at cash cost of $7.60 to $8.60 per oz Ag

Manantial Espejo

Combination Open Pit & Underground Santa Cruz, Argentina

36.32 Moz Ag; 534.11 Koz Au

4.0 Moz Ag at cash cost of $1.61/oz

4.2 to 4.5 Moz Ag at cash cost of $4.80 to $5.60 per oz Ag

1 At December 31, 2010 2 Cash costs per payable ounce of silver produced net of by-product credits 3 Cash costs per ounce of Ag, net of by-product credits. Price assumptions: Au $1,320/oz, Zn $2,050/tonne, Pb $2,050/tonne, Cu $7,000/tonne

DeVeLopment projeCts

resoUrCes

propertY oWnersHip LoCation measUreD & inDiCateD inFerreD 2011 oBjeCtiVes

Navidad 100% Chubut, Argentina632.36 Moz Ag; 2,914 M pounds Pb

119 Moz Ag; 580 M pounds Pb

Invest $44.7 million for continued diamond drilling and to complete an Environmental Impact Assessment and ultimately a full Feasibility Report in Q4 2011

La Preciosa

55% Joint Venture Interest Durango, Mexico 63 Moz Ag; 92 Koz Au

72 Moz Ag; 97 Koz Ag

Invest $1 million to complete a Preliminary Assessment by mid-year 2011

Pico Machay 100% Huancavelica, Peru 265 Koz Au 446 Koz AuLimited in-fill drilling, resource model development and advance scoping study

Calcatreu 100% Rio Negro, Argentina 6.6 Moz Ag; 676 Koz Au1.8 Moz Ag; 226 Koz Au Monitor Provincial legislation evolution

properties at a gLanCe

2222

taBLe oF Contents

Management’s Discussion and Analysis 22

Introduction 23

Core Business and Strategy 24

Highlights of 2010 25

2011 Project Development Objectives 25

2011 Operating Outlook 26

2010 Operating Performance 29

Overview of 2010 Financial Results 38

Liquidity Position 40

Investments and Investment Income 41

Capital Resources 41

Financial Instruments 41

Asset Retirement Obligations 42

Contractual Commitments and Contingencies 42

general and Administrative 43

Exploration and Project Development 43

Non-gAAP Measures 44

governance and Corporate Social Responsibility 45

Risks and Uncertainties 46

Critical Accounting Policies and Estimates 49

Future Accounting Changes 50

Subsequent Events 52

Disclosure Controls and Procedures 52

Mineral Reserves and Resources 54

Management’s Responsibility for Financial Reporting 58

Auditors’ Reports 59

Consolidated Balance Sheets 61

Consolidated Statements Of Operations 62

Consolidated Statements Of Shareholders’ Equity 63

Consolidated Statements Of Cash Flows 64

Notes to Consolidated Financial Statements 65

MANAgEMENt'S DISCUSSION AND ANALYSIS 23

introDUCtionManagement’s discussion and analysis (“MD&A”) is intended to help the reader understand the signifi cant factors that have affected Pan American Silver Corp.’s and its subsidiaries’ (“Pan American” or the “Company”) performance and such factors that may affect its future performance. the MD&A should be read in conjunction with the Company’s Audited Consolidated Financial Statements for the year ended December 31, 2010 and the related notes contained therein. All amounts in this MD&A and in the consolidated fi nancial statements are expressed in United States dollars (“USD”), unless identifi ed otherwise. the Company reports its fi nancial position, results of operations and cash fl ows in accordance with Canadian generally accepted accounting principles (“Canadian gAAP”). Pan American’s signifi cant accounting policies are set out in Note 2 of the Audited Consolidated Financial Statements. Differences between Canadian and United States generally accepted accounting principles (“US gAAP”) that would have affected the Company’s reported fi nancial results are set out in Note 21 of the Audited Consolidated Financial Statements. this MD&A refers to various non-gAAP measures, such as “cash and total cost per ounce of silver”, which are used by the Company to manage and evaluate operating performance at each of the Company’s mines and are widely reported in the silver mining industry as benchmarks for performance, but do not have standardized meaning. to facilitate a better understanding of these measures as calculated by the Company, we have provided detailed descriptions and reconciliations where applicable.

Except for historical information contained in this MD&A, the following disclosures are forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995 or are future oriented fi nancial information and as such are based on an assumed set of economic conditions and courses of action. Please refer to the cautionary note regarding the risks associated with forward looking statements at the back of this MD&A and the “Risks Related to Pan American’s Business” contained in the Company’s most recent Form 40-F and Annual Information Form on fi le with the US Securities and Exchange Commission and the Canadian provincial securities regulatory authorities. Additional information about Pan American and its business activities, including its Annual Information Form, is available on SEDAR at www.sedar.com

the scientifi c or technical information in this MD&A, which includes reserve estimates for the Huaron, Morococha, Quiruvilca, Alamo Dorado, La Colorada, Manantial Espejo, and San Vicente properties were based upon information prepared by or under the supervision of Michael Steinmann, P.geo., Executive Vice President geology & Exploration and Martin g. Wafforn, P.Eng., Vice President technical Services, who are “Qualifi ed Persons” for purposes of National Instrument 43-101. Navidad Resource estimates were prepared by Pamela De Mark, P. geo. Mineral Resource estimates for Hog Heaven and Waterloo are based on historical third party estimates.

the Company’s 2011 forecast and the resultant forecast numbers contained in this MD&A include estimates of future production rates for silver and other metals and future cash and total costs of production at each of the Company’s properties, which are forward-looking estimates. these forecasts are based on the following key assumptions: (i) silver: $20.65 per ounce, gold: $1,320 per ounce, zinc: $2,050 per tonne ($0.93 per lb), lead: $2,050 per tonne ($0.93 per lb), and copper: $7,000 per tonne ($3.18 per lb); (ii) that we are able to ship and sell all of our 2011 production in the 2011 fi nancial year; (iii) the Company’s forecast production for each individual mine is achieved; (iv) there is no disruption in production, increase in costs or disruption due to, among other things: natural phenomena and hazards; technological, mechanical or operational disruptions; changes in local governments, legislation, taxation or the political or economic environment; fl uctuations in the price of silver, gold or base metals; fl uctuations in the local currencies of those countries in which the Company carries on business; unexpected work stoppages or labour disputes; fl uctuations in the price for electricity, natural gas, fuel oil, and other key supplies; or transportation disruptions.

No assurance can be given that the indicated quantities of silver and other metals will be produced, or that projected cash costs or forecast capital costs will be achieved. Expected future production, cash costs and capital costs are inherently uncertain and could materially change over time. If actual results differ from the assumptions set out above, the Company’s mineral production and cash costs may differ materially from the forecasts in this MD&A. Readers should review those matters discussed herein under the heading “Risks and Uncertainties” and are advised to read the “Cautionary Note Regarding Forward Looking statements” contained herein.

march 22, 2011

PAN AMERICAN SILVER CORP. | ANNUAL REPORt 201024

Core BUsiness anD strategYPan American engages in silver mining and related activities, including exploration, mine development, extraction, processing, refining and reclamation. the Company owns and operates silver mines located in Peru, Mexico, Argentina, and Bolivia. In addition, the Company is exploring for new silver deposits throughout South America and Mexico. the Company is listed on the toronto Stock Exchange (Symbol: PAA) and on the NASDAQ Exchange in New York (Symbol: PAAS).

Pan American was founded in 1994 with the specific intention of providing investors with the best investment opportunity to gain real exposure to silver prices. the Company's mission is to be the largest and lowest cost primary silver mining company globally. to realize this mission, Pan American’s strategy is to focus on growing its base of low cost silver production and silver reserves by constantly optimizing its production methods, and developing new silver deposits through acquisition and exploration.

to execute this strategy, Pan American has assembled a sector leading team of mining professionals with a depth of exploration, construction, operating, and financing knowledge that allows the Company to confidently advance early stage projects through construction and into operation.

Pan American is determined to conduct its business in a responsible and sustainable manner.

Being responsible for the environment in which we operate, contributing to the long-term development of our host communities and ensuring that our employees can work in a safe and secure manner are core values at Pan American. We are committed to maintaining positive relations with our employees, the local communities and the government agencies, all of whom we view as partners in our enterprise.

Pan American Silver’s priority at every operation is the safety of our employees. We believe that comprehensive and continuous training is fundamental to the safety of our employees. With our comprehensive safety training and strictly enforced safety procedures, our goal is to continually improve our safety performance and remain industry leaders in the health and safety of our workers.

In addition, the Company is committed to operating our mines and developing new projects in an environmentally responsible manner. We have developed a comprehensive environmental policy, which all operations adhere to and apply to their short and long-term plans. this policy addresses topics that include water use and recycling, waste disposition, the research and use of alternative energies, compliance with required laws, closure requirements and education initiatives. Each operation runs unique environmental programs according to its location, needs, resources and processes. We have a proactive approach to minimizing and mitigating environmental impacts during all phases of the mining cycle from exploration through project development and into full mining operations. this is accomplished by applying prudent design and operating practices, continuous monitoring and by providing training and education for the employees and contractors who work at our facilities.

the Company recognizes that the skills and dedication of our employees and contractors are important drivers of our success. We also recognize the vital contribution they make to the economic prosperity of the communities in which we operate. As such, we offer leading career development opportunities, competitive remuneration, an engaging working environment and a supportive culture where fairness, respect, safety and diversity are valued and practiced.

Pan American’s operational track record and strong financial standing has positioned the Company to take full advantage of strategic opportunities in the silver market, when and if they arise. Pan American’s silver production has grown for 15 consecutive years. At the end of 2010, Pan American had seven operating mines and also owned the world class Navidad silver development project in Argentina, and is the operator of the La Preciosa project in Mexico - a considerable portfolio of quality silver assets providing diversification of political and operational risk. Pan American also produces significant quantities of gold and base metals as by-products to its silver mining activities. the following charts reflect the geographic diversity of our silver production and the breakdown of our revenue, by metal type, for 2010:

Mexico 44%Peru 28%Argentina 16%Bolivia 12%

44%16%

12%

28%

2010 SILVER PRODUCTIONBY COUNTRY

5%4%

11%

2010 REVENUE BY METAL

Silver 65%Gold 15%Zinc 11%Copper 5%Lead 4%

65%

15%

MANAgEMENt'S DISCUSSION AND ANALYSIS 25

HigHLigHts oF 2010operationaL & projeCt DeVeLopment

record silver production Silver production was 24.3 million ounces in 2010, an increase of 5% over 2009. this new record is mainly attributable to exceptional silver production at Alamo Dorado, where 6.7 million ounces was produced compared to 5.3 million ounces in 2009.

navidad project Updatethe Company released the results of Navidad’s preliminary assessment, which defined a highly economic project that would produce an estimated average of 19.8 million ounces of silver over the first 5 years of operation, have a mine life of 17 years and generate an after-tax return of $1.2 billion at a 5% discount rate (assuming a $25 per ounce silver price).

La preciosa Updatethe Company made good progress at the La Preciosa joint-venture project, where we invested in exploration and delineation drilling, metallurgical testing and engineering activities and are well on our way to producing a preliminary assessment by mid-year 2011.

robust proven and probable silver reservesA successful exploration and resource conversion program in 2010 very nearly fully replaced reserves that were mined during the year. As at December 31, 2010, proven and probable reserves totaled 230.7 million ounces. For the complete breakdown of reserves and resources by property and category, refer to section “Mineral Reserves and Resources” contained herein.

FinanCiaL

record sales Annual sales in 2010 were a record $632.0 million, an increase of 39% over 2009 sales, driven primarily by increased quantities of silver sold, combined with higher realized prices for all metals.

record mine operating earnings Mine operating earnings in 2010 increased to $239.8 million, an increase of 90% over the prior year, as growth in sales noted above significantly outweighed increases in cost of sales and depreciation.

record operating Cash Flow Cash flow from operations was at a record $242.3 million, a 109% increase from 2009. Operating cash flow before changes in non-cash working capital was $218.3 million in 2010, a $66.7 million improvement on the comparable cash flow from 2009. the additional operating cash flow was mainly attributable to increased cash flow from Alamo Dorado and Manantial Espejo, which combined to generate $150.9 million.

record Liquidity and Working Capital position the Company had a record cash and short term investment balance of $360.5 million and a working capital position at a record $433.8 million at December 31, 2010, an increase of $167.4 million and $161.5 million, respectively, from a year ago. this was driven mostly by the record operating cash flows as described above.

pan american starts paying Dividends Pan American declared its first dividend in February 2010 and a second dividend in August 2010, both in the amount of $0.025 per common share. In November 2010 the Company announced a dividend in the amount of $0.025 per share and increased the frequency of the Company’s dividend distributions from a semi-annual to a quarterly basis.

BUsiness DeVeLopment

the aquiline transactionDuring January 2010, the Company issued further common shares and share purchase warrants (1.7 million and 0.7 million, respectively) to bring its ownership interest in Aquiline Resources Inc. from 93% to 100% by January 22, 2010. the final step of the acquisition was achieved through a Compulsory Acquisition. Please refer to Note 3 of the Audited Consolidated Financial Statements for further details.

2011 projeCt DeVeLopment oBjeCtiVesOn November 30, 2010, the Company released the results of Navidad’s Preliminary Assessment, which defined a highly economic project that would involve developing and mining the deposit through conventional surface mining methods. the Preliminary Assessment technical report was subsequently filed with the applicable regulatory authorities on January 14, 2011 and is available on SEDAR at www.sedar.com. the Company expects to complete an Environmental Impact Assessment (“EIA”) during the second quarter of 2011 and a full feasibility study in the fourth quarter. In 2011, the Company plans to invest over $40.0 million in Navidad’s continued development, including $16 million for exploration diamond drilling. the remainder will be directed towards preparation of the EIA, tailings site and geotechnical evaluation, metallurgical studies, basic engineering, preparation of the feasibility study, and community, media and government relations activities. Pan American Silver remains confident that an open and informed dialogue with the provincial government and local communities regarding open pit mining in the Central Meseta of Chubut will ultimately be resolved favorably and lead to the responsible development of Navidad. the Company intends to transform Navidad into a world-class silver mine.

During 2010 Pan American was also very active at the La Preciosa joint-venture with Orko Silver Corp. the Company is currently completing additional work to evaluate alternative extraction and development scenarios in order to maximize the project’s economics, in view of the improved metals price environment. During the first half of 2011, Pan American expects to invest $1 million at La Preciosa to complete a preliminary assessment.

Pan American’s Morococha Relocation Project will advance in 2011 with completion of the construction of the new Morococha site infrastructure, including a maintenance facility, warehouse, administration building, and employee residence. A total of $43 million is budgeted for this work in 2011, which will be partially offset by progress payments received from Minera Peru Chinalco (“Chinalco”). the purpose of this project is to move existing facilities to outside the area of Chinalco’s future toromocho open pit mine. the processing plant relocation is currently scheduled for 2013/2014, as the current concentrator is located a safe distance from the first toromocho open pit activity.

PAN AMERICAN SILVER CORP. | ANNUAL REPORt 201026

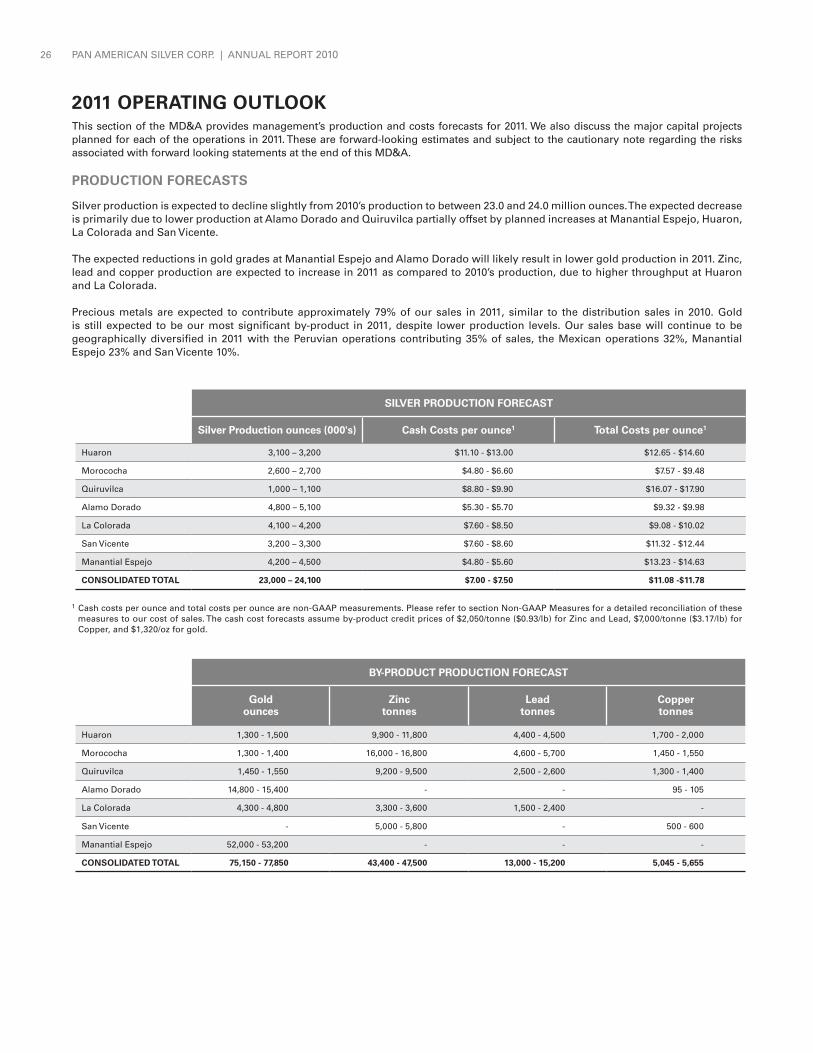

2011 operating oUtLooKthis section of the MD&A provides management’s production and costs forecasts for 2011. We also discuss the major capital projects planned for each of the operations in 2011. these are forward-looking estimates and subject to the cautionary note regarding the risks associated with forward looking statements at the end of this MD&A.

proDUCtion ForeCasts

Silver production is expected to decline slightly from 2010’s production to between 23.0 and 24.0 million ounces. the expected decrease is primarily due to lower production at Alamo Dorado and Quiruvilca partially offset by planned increases at Manantial Espejo, Huaron, La Colorada and San Vicente.

the expected reductions in gold grades at Manantial Espejo and Alamo Dorado will likely result in lower gold production in 2011. Zinc, lead and copper production are expected to increase in 2011 as compared to 2010’s production, due to higher throughput at Huaron and La Colorada.

Precious metals are expected to contribute approximately 79% of our sales in 2011, similar to the distribution sales in 2010. gold is still expected to be our most significant by-product in 2011, despite lower production levels. Our sales base will continue to be geographically diversified in 2011 with the Peruvian operations contributing 35% of sales, the Mexican operations 32%, Manantial Espejo 23% and San Vicente 10%.

siLVer proDUCtion ForeCast

silver production ounces (000's) Cash Costs per ounce1 total Costs per ounce1

Huaron 3,100 – 3,200 $11.10 - $13.00 $12.65 - $14.60

Morococha 2,600 – 2,700 $4.80 - $6.60 $7.57 - $9.48