Embed Size (px)

Citation preview

7/27/2019 14651606 a Comparative Analysis Between LIC and Private Insurance Companies

http://slidepdf.com/reader/full/14651606-a-comparative-analysis-between-lic-and-private-insurance-companies 1/65

DISSERTATION PROJECT REPORT

ON

A COMPARATIVE ANALYSIS OF LIFE INSURANCE

CORPORATION AND PRIVATE INSURANCE COMPANIES

Report submitted in partial fulfillment of the requirements for

Post Graduate in Management

PROJECT GUIDE: SUBMITTED BY:

Prof. Usha Kiran Rai Shashank Tripathi

FMS BHU MBA IV Sem (Finance)

FMS BHU

7/27/2019 14651606 a Comparative Analysis Between LIC and Private Insurance Companies

http://slidepdf.com/reader/full/14651606-a-comparative-analysis-between-lic-and-private-insurance-companies 2/65

2

CONTENTS

Ø Acknowledgement

Ø Introduction

§ Concept of Insurance

§ Global Insurance Industry

§ Performance of Indian Industry

§ Insurance sector reforms in India

§ New avenues for growth of the Insurance industry

Ø Research Methodology

§ Research Objectives

§ Research Design

§ Research Process

§ Limitations of the Study

§ Significance of the study

Ø Analysis and Interpretation

Ø Findings & Conclusions

Ø References

7/27/2019 14651606 a Comparative Analysis Between LIC and Private Insurance Companies

http://slidepdf.com/reader/full/14651606-a-comparative-analysis-between-lic-and-private-insurance-companies 3/65

3

ACKNOWLEDGEMENT

I must acknowledgemy indebtedness to various personalities, but for whom, this project

could not haveseen thelight of theday.

I amprofoundly grateful to Prof. Usha Kiran Rai, Faculty of Management Studies, BHU

who agreed to becomemy mentor and guidefor theproject and gavemetheopportunity to

work on this project. I amalso grateful, for her support and guidancethroughout this

project with valuableinformation and giving mea better insight of thethings, withoutwhich thesuccessful culmination of this project would not havebeen possible. Not only did

sheinspired methroughout theprogress of theproject, but, also motivated meto get an

insight into thefield of my work.

I would also liketo extent my immensegratitudeto Prof. A. K. Agrawal, and respected

Dean Prof. Deepak Barman, Faculty of Management Studies, BHU who allowed meto

choosethetopic for my Dissertation.

Shashank Tripathi

7/27/2019 14651606 a Comparative Analysis Between LIC and Private Insurance Companies

http://slidepdf.com/reader/full/14651606-a-comparative-analysis-between-lic-and-private-insurance-companies 4/65

4

CHAPTER 1

INTRODUCTION

7/27/2019 14651606 a Comparative Analysis Between LIC and Private Insurance Companies

http://slidepdf.com/reader/full/14651606-a-comparative-analysis-between-lic-and-private-insurance-companies 5/65

5

1. CONCEPT OF INSURANCE :

Life has always been an uncertain thing. To be secure against unpleasant possibilities,

always requires the utmost resourcefulness and foresight on the part of man. To prayor to pay for protection is the spirit of the humanity. Man has been accustomed to

pray God for protection and security from time immemorial. In modern days

Insurance Companies want him to pay for protection and security. The insurance man

says "God helps those who help themselves"; probably he is correct.

Too many people in this country are not in employment; and work for too many no

longer guarantees income security. Several millions are part-time, self employed and

low-earning workers living under pitiable circumstances where there is no security

cover against risk. Further the inherent changing employment risks, the prospect of

continual change in the work place with its attendant threats of unemployment andlow pay especially after the adoption of New Economic Policy and the imminent life

cycle risks - a new source of insecurity which includes the changing demands of

family life, separation, divorce and elderly dependents are tormenting the society.

Risk has become central to one's life. It is within this background life insurance policy

has been introduced by the insurance companies covering risks at various levels. Life

insurance coverage is against disablement or in the event of death of the insured,

economic support for the dependents. It is a measure of social security to livelihood

for the insured or dependents. This is to make the right to life meaningful, worth

living and right to livelihood a means for sustenance. Therefore, it goes without

saying that an appropriate life insurance policy within the paying capacity and means

of the insured to pay premium is one of the social security measures envisaged under

the Indian Constitution. Hence, right to social security, protection of the family,

economic empowerment to the poor and disadvantaged are integral part of the right to

life and dignity of the person guaranteed in the constitution.

Man finds his security in income (money) which enables him to buy food, clothing,

shelter and other necessities of life. A person has to earn income not only for himself

but also for his dependents, viz., wife and children. He has to provide legally for his

family needs, and so he has to keep aside something regularly for a rainy day and for

his old age. This fundamental need for security for self and dependents proved to be

the mother of invention of the institution of life insurance.

7/27/2019 14651606 a Comparative Analysis Between LIC and Private Insurance Companies

http://slidepdf.com/reader/full/14651606-a-comparative-analysis-between-lic-and-private-insurance-companies 6/65

6

What is Insurance :

The business of insurance is related to the protection of the economic values of assets. Every

asset has a value. The asset would have been created through the efforts of the owner. The

asset is valuable to the owner, because he expects to get some benefit from it. The benefit

may be an income or some thing else. It is a benefit because it meets some of his needs. In the

case of a factory or a cow, the product generated by is sold and income generated. In the caseof a motor car, it provides comfort and convenience in transportation. There is no direct

income.

Every asset is expected to last for a certain period of time during which it will perform. After

that, the benefit may not be available. There is a life-time for a machine in a factory or a cow

or a motor car. None of them will last for ever. The owner is aware of this and he can so

manage his affairs that by the end of that period or life-time, a substitute is made available.

Thus, he makes sure that the value or income is not lost. However, the asset may get lost

earlier. An accident or some other unfortunate event may destroy it or make it non-functional.

In that case, the owner and those deriving benefits from there, would be deprived of the benefit and the planned substitute would not have been ready. There is an adverse or

unpleasant situation. Insurance is a mechanism that helps to reduce the effect of such adverse

situations.

Insurance, in law and economics, is a form of risk management primarily used to hedge

against the risk of a contingent loss. Insurance is defined as the equitable transfer of the risk

of a potential loss, from one entity to another, in exchange for a premium. Insurer, in

economics, is the company that sells the insurance. Insurance rate is a factor used to

determine the amount, called the premium, to be charged for a certain amount of insurance

coverage. Risk management, the practice of appraising and controlling risk, has evolved as a

discrete field of study and practice.

Origin of Insurance

PRACTICE OF INSURANCE IN INDIA: 1818-1956

It is claimed that insurance was practiced in India even in Vedic times in one form or theother. The Sanskrit term "Yogakshema" in the Rigveda meant some kind of insurance, whichwas practiced by the Aryans in India nearly 3000 years ago. During the Mughal periodinsurance took firm roots. There are even references to the cover against war risks. Lossesdue to the passage of royal troops through farms were compensated by the State as a gesture

of goodwill.

The year 1818 is an epoch -making year in the history of our country. The first Life InsuranceCompany on India soil appears to have been started in this year. A group of Europeans

pioneered the establishment of the Oriental Life Insurance Society to afford relief to thedistressed relatives of European. The venture was not quite successful but the company wasreformed in 1829.The renewed Company also got into trouble in 1833 when Agency Houseof Calcutta, partners of the same, fell.

7/27/2019 14651606 a Comparative Analysis Between LIC and Private Insurance Companies

http://slidepdf.com/reader/full/14651606-a-comparative-analysis-between-lic-and-private-insurance-companies 7/65

7

Prince Dwarkanath Tagore was the only solvent partner & the sole responsibility for carryingon the institution developed on him. Meanwhile, early in Janury1834, the Government madeup its mind to establish a Public Insurance Company & a Committee was set up for this

purpose .A number of foreign Insurance Companies then operating in the country viewed thismove with alarm. They set up Committees of their own enquire into their individual affairs.Dwarkanath Tagore, too, had a Committee appointed to look into the affairs of the Oriental.

As a result, another company was born out of the previous one in the name of "New OrientalCompany"

In the reorganization of the "Oriental" in the year 1834, two other gentlemen were associated.One was Ramtanu Lahiri and the other Rustamjee Cowasjee. The latter was another

prominent figure of the business world. Rustamjee entered insurance business in 1828, hewas already known to the community and the Government as a wealthy Parsi merchant.Rustamjee's connection with insurance also started with "Laudable Societies", but he waslater on associated with Companies like "Sun Life Office (1834) ", New Oriental(1835),Universal Life (1835) , New Laudable (1840) , and Indian Laudable (1841) . He wasalso on the Committee of the Union Insurance Company which was formed by a group of five persons. This Company was issuing policies covering river-risks only. He was intimately

connected with the Committee of Insurance Offices in Calcutta. Rustamjee Cowasjee &Dwarkanath Tagore was probably the first Indians to join in partnership business with theEuropeans & in the field of insurance they were pioneers on this side of the country.

Apart from Calcutta, several enterprising people in Bombay started in 1823 the "BombayLife" Assurance Company. The company went into liquidation soon and could not revive. In1829, the "Madras Equitable "was formed. It finally ceased to function in 1921 due tofinancial difficulties after the First World War.

The effort to set up a public insurance company at the government level also went in vain,mainly from objection of private operators. Majority of the early attempts to form insuranceoffices were in the province of Bengal. This was due to its political & economic importanceat that time.

The contribution of Raja Ram Mohan Roy, one of the greatest social reformers of India, tothe development of life insurance is very great. He was deeply concerned about the sad plightof desperate widows and helpless orphans.

OVERSEAS INSURERS

Initially, when Life Offices were established in large numbers in Britain, some of themventured to issue sterling policies to the British residents in India. Premiums collected here

were credited to England largely for British beneficiaries. Business seems to have been brisk and profitable and was usually under short term policies. Insurance mortality tables andinsufficient mortality data of Englishmen in India made the premiums heavy-heavier than athome. Insurance was denied to the "natives" even if they wanted it- for their lives werealways considered risky and sometimes valueless. When Indian lives were accepted as a veryspecial case, the extras charged were still heavier.

Prominent amongst the companies which came to India around this period was the "MedicalInvalid and General" incorporated in London in 1841. As more areas were annexed and the

7/27/2019 14651606 a Comparative Analysis Between LIC and Private Insurance Companies

http://slidepdf.com/reader/full/14651606-a-comparative-analysis-between-lic-and-private-insurance-companies 8/65

8

ruling power, with vested interests in developing trade, took charge , the "Medical" extendedits area of operation, established large connections, absorbed the" Agra Life" and in 1835,took over the "New Oriental". P.M. Tate, the then manager of the "Medical", was a keen

businessman, widely liked, influential and shrewd. With W.F. Ferguson, who was themanager of the "New Oriental" before amalgamation, he commenced very active operationswhich were temporarily affected by the 1857 "Mutiny".

The Universal Life Insurance Company established in England in 1836 opened its IndianBranch in 1840 and enjoyed a long period of successful operations until it was taken over bythe "North British" in May 1901. Insurance exceeding Rs. 10 crores were issued in Indiaduring this period. Another English Company operating in India at that time was the ColonialLife Assurance Company. It was established in 1846 under the auspices of the Standard LifeAssurance Company. The original prospectus of this company declared its purpose as"extending to the Colonies of Great Britain and to Indian the full benefit of Life Assurance".It appointed agents with local boards which were first established on Calcutta, Bombay,Madras and Colombo. Later on this company was taken over by the "Standard Life" andmade valuable contribution to investigations into the mortality experience of assured lives inIndia. Eventually it ceased its operations in India in 1938.

It is difficult to say which was the oldest Life Policy in India, but the oldest known appears to be one sold by the Royal Insurance (which commenced business in India in 1845) on the lifewas to Cursetjee Furdonjee on 6th January 1848, no reference to any earlier policy beingavailable. In the year 1853, the Liver pool and London and Globe Insurance Companyestablished in England in 1836, commenced business in India. Sir Charles Forbes was its firstagent, succeeded by M/s. Forbes, Forbes and Campbell. It accepted only European lives andcommenced insuring Indian lives only after 1929.This too, was mainly to oblige good agentsof the Company for classes other than life business. The North British and Mercantile was thenext company to appear on the Indian scene.

It started fire insurance business in the year 1861 and life business 1864. The LondonAssurance started life business in 1864, limited principally to European lives and closeddown its life department when the Life Assurance Companies Act 1912 made submission of returns compulsory.

On 3rd December, 1870, seven earnest men of Bombay with just seven rupees for initialexpenses gave shape to a plan of offering insurance to the public without the risk of ruin andthe "Bombay Mutual Life Assurance Society" came into existence. This was followed by theOriental Life Assurance Company in1874, the Bharat in 1896 and the Empire of India in1897.

THE BIRTH OF INDIAN INSURERS

With the advent of the 20th century, the glorious renaissance of swadeshi days dawned. Atthe same time, well- to do Indians realized the potentiality of Indian Insurance business. TheSwadeshi movement of 1905-1907 gave rise to more insurance companies. The United Indiain Madras, National Indian and National Insurance in Calcutta and the Co-operativeAssurance at Lahore were established in 1906. In 1907, Hindustan Co-operative InsuranceCompany took its birth in one of the rooms of the Jorasanko House of the great poetRabindranath Tagore, in Calcutta. The Indian Mercantile (1907) was started in Bombay,

7/27/2019 14651606 a Comparative Analysis Between LIC and Private Insurance Companies

http://slidepdf.com/reader/full/14651606-a-comparative-analysis-between-lic-and-private-insurance-companies 9/65

9

General Assurance (1908) at Ajmer and the Swadeshi Life (Later Bombay Life) in Bombayin 1908.

The end of the First World War (1914-18) witnessed an influx of insurance companies inIndia. Famous Indian business houses started new insurance companies. Industrial andPrudential Bombay, Western India, Satara, were floated before the war, but by 1919,

companies like Jupiter General, New India, Vulcan Insurance Company etc. came into being.Pandit K.Santhanam with blessing of Lala Lajpat Rai and Pandit Motilal Nehru started LaxmiInsurance Co. Similarly, Andhra Insurance was started in Masulipatnam, with the initiative of stalwarts like Dr. Pattabhi Sitaramaiah. From political platforms also, national leaderssupported this cause. It is duty to every Indian to support only Indian Insurance. The keynoteof our Swaraj is in placing all our insurance with our Indian companies", said MahatmaGandhi in his message. "I hope Indians will realize the importance of patriotism only throughIndian insurance institution", stated Pandit Jawaharlal Nehru. Thus, the cause of Indianinsurance became a national issue. The pursuit to boost Indian insurance represented acrusade to extricate the Indian economy from foreign domination.

PROGRESS IN INSURANCE BUSINESS

The growth of Life Insurance in concrete terms could be said to being during the first two

decades of twentieth century when most of the major companies were founded. They grew interms of rise in the number of companies, in terms of number of policies and sum assured as

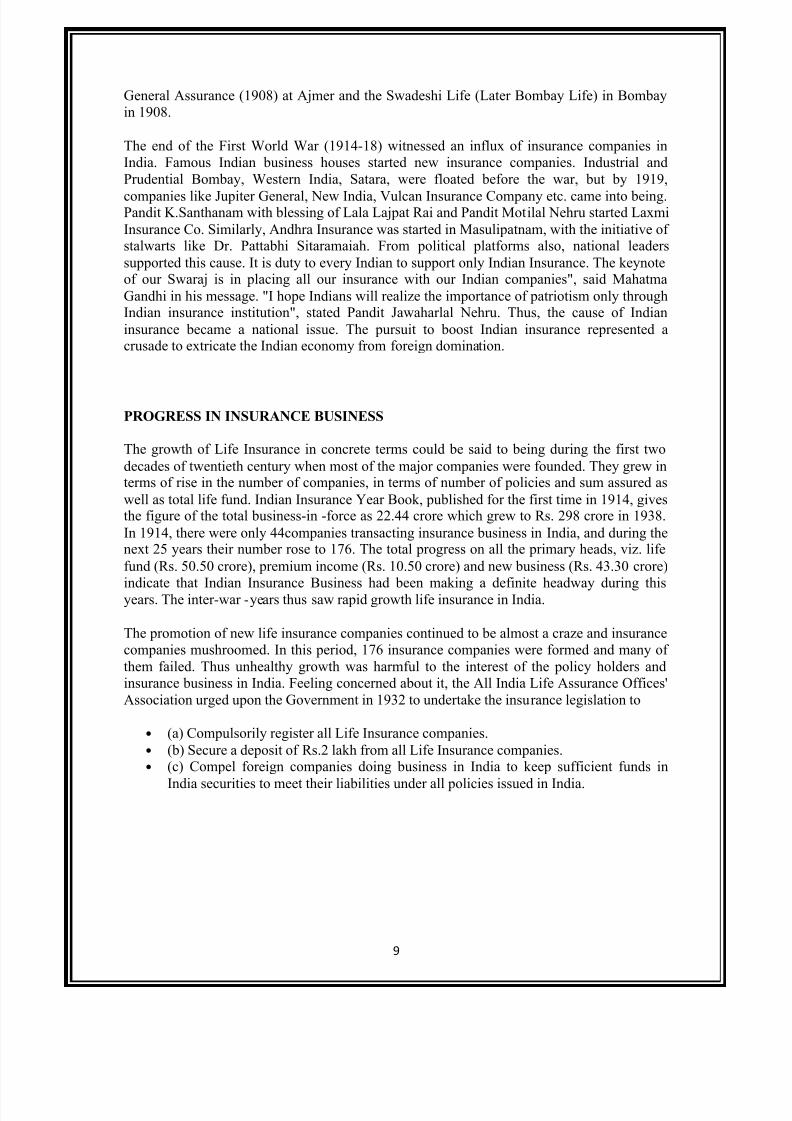

well as total life fund. Indian Insurance Year Book, published for the first time in 1914, givesthe figure of the total business-in -force as 22.44 crore which grew to Rs. 298 crore in 1938.

In 1914, there were only 44companies transacting insurance business in India, and during thenext 25 years their number rose to 176. The total progress on all the primary heads, viz. life

fund (Rs. 50.50 crore), premium income (Rs. 10.50 crore) and new business (Rs. 43.30 crore)

indicate that Indian Insurance Business had been making a definite headway during thisyears. The inter-war -years thus saw rapid growth life insurance in India.

The promotion of new life insurance companies continued to be almost a craze and insurancecompanies mushroomed. In this period, 176 insurance companies were formed and many of them failed. Thus unhealthy growth was harmful to the interest of the policy holders andinsurance business in India. Feeling concerned about it, the All India Life Assurance Offices'Association urged upon the Government in 1932 to undertake the insurance legislation to

• (a) Compulsorily register all Life Insurance companies.• (b) Secure a deposit of Rs.2 lakh from all Life Insurance companies.• (c) Compel foreign companies doing business in India to keep sufficient funds in

India securities to meet their liabilities under all policies issued in India.

7/27/2019 14651606 a Comparative Analysis Between LIC and Private Insurance Companies

http://slidepdf.com/reader/full/14651606-a-comparative-analysis-between-lic-and-private-insurance-companies 10/65

10

INSURANCE ACT, 1938

The Insurance Act, 1938, was the first comprehensive legislation governing not only life butalso non- life branches of insurance to provide strict state control over insurance business. Insub- sections to dealt with provident companies, mutual offices and co-operative societies as

well.

The silent features of the Act were as follows:

• (A) Constitution of a Department of Insurance under a superintendent vested withwide powers of supervision and control over all kinds of insurance companies.

• (B) Regulation for the compulsory registration of insurance companies and for filingof returns of investment and financial conditions.

• (C) Provisions for deposit, to prevent insurers of inadequate financial resources of speculative concerns for commencing business.

• (D) Provisions that 55% of the net life fund of an Indian or non- Indian insurer shouldinvested in Indian Government and approved securities with at least 25% in Indian

Government Rupee securities.. All other companies, i.e., foreign companies mustinvest 100% of their Indian liabilities in Indian Government and approved securities,with at least 33.3% Indian Government securities.

• (E) Prohibition of rebating, restriction of commission, licensing of agents etc.Maximum rates of commission were fixed at 40% of the first premiums and 5% of therenewal premium in respect of life assurance business. The agent must be licensed, toimprove the status of the profession.

• (F) Periodical valuation of Indian Insurance business of foreign companies and the business of Indian companies.

• (G) Provision for policyholders' directors, making it possible for the representatives of policyholders to be on the Board of directors.

• (H) Standardization of policy conditions required all companies to file standard formsand tables of premium approved by an Actuary. Under this requirement, the initialdeposit for life insurance business was raised from Rs. 25000 in Governmentsecurities to Rs. 50000 in cash approved securities, which was subsequently to beraised by installments to Rs. 2 lakh within a specified time limit.

7/27/2019 14651606 a Comparative Analysis Between LIC and Private Insurance Companies

http://slidepdf.com/reader/full/14651606-a-comparative-analysis-between-lic-and-private-insurance-companies 11/65

11

GROWTH OF LIFE BUSINESS IN INDIA: 1914-1948

Sr no

1914 1930 1940 1945 1948

1 No of insurers 44 68 195 215 209

(a) Indian 44 68179(91.79)

200(93.02)

189(90.43)

(b) Non-Indian - - 16 15 20

2Total No. of

policies In force- 748997 1628381 2714000 3016000

(a) Indian -513925(68.61)

1371963(84.25)

2376000(87.55)

2791000(90.15)

(b) Non-Indian - 220703 181247 261000 234000

(c) Indian outsideIndia

- 14369 75171 77000 202000

3Total business in

force22.44 258.42 304.03 573.07 712.76

(a) Indian (Rs. Crore) 22.4484.89(32.85)

225.51(74.17)

459.43(80.17)

566.38(79.46)

(b) Non-Indian - 69.76 60.12 91.85 101.08

(c)Indian outsideIndia

- 3.77 18.4 21.79 45.3

4

Total life funds

(Rs. Crore) 6.36 20.53 62.41 107.4 150.39

Note: Figures in brackets show percentage of the total.

7/27/2019 14651606 a Comparative Analysis Between LIC and Private Insurance Companies

http://slidepdf.com/reader/full/14651606-a-comparative-analysis-between-lic-and-private-insurance-companies 12/65

12

Nationalization

THE LIFE INSURANCE CORPORATION OF INDIA: 1956

This was the first step taken towards the nationalization of life insurance business in India.On 20th January, 1956 all life insurance companies were taken over by 43 nominated

custodians. The custodians were experienced senior executives of private insurancecompanies, reporting directly to the Finance Ministry. From the word go, the complex task of running the industry on a permanent basis and continuing the services to policy holderswithout interruption were their major concerns. The actual work of integration had to awaitlegislation. The custodians managed the insurance companies till 1-09-1956, when LifeInsurance Corporation was established under the general direction and control of the Ministryof Finance.

The Ordinance provided for the transfer of the control of 154 Indian insurers, 16 non Indianinsurers and 75 provident societies. These arrangements were designed to ensure that noinconvenience whatsoever was caused to the policy holders. With the Government take over the management aimed towards the evolution of a common uniform premium rate, policyconditions and service and working procedures and above all to help promote team spirit.

The corporation, a body corporate shall consist of not more than 15 members appointed bythe Central Government, one of them being appointed by the government as chairman.

The capital of the corporation was at Rs 5 crore provided by the central government.

INSURANCE SECTOR REFORMS

In 1993, Malhotra Committee, headed by former Finance Secretary and RBI Governor R.N.Malhotra was formed to evaluate the Indian Insurance industry and recommended its future

direction.

The Malhotra committee was set up with the objective of complementing the reforms

initiated in the financial sector.

The reforms were aimed at "creating a more efficient and competitive financial systemsuitable for the requirements of the economy keeping in mind the structural changes currentlyunderway and recognizing that insurance is an important part of the over all financial systemwhere it was necessary to address the need for similar reforms...".

In 1994, the committee submitted the report and some of the key recommendations included:

(1) STRUCTURE

• Government stake in the Insurance Companies to be brought down to 50%.• Government should take over the holdings of GIC and its subsidiaries so that these

subsidiaries can act as independent corporations.• All the insurance companies should be given greater freedom to operate

7/27/2019 14651606 a Comparative Analysis Between LIC and Private Insurance Companies

http://slidepdf.com/reader/full/14651606-a-comparative-analysis-between-lic-and-private-insurance-companies 13/65

13

(2) COMPETETION

• Private Companies with minimum paid up capital of Rs.1 bn should be allowed toenter the industry.

• No Company should deal in both Life and General Insurance through a single entry.• Foreign Companies may be allowed to enter the industry in collaboration with the

domestic companies.• Postal Life Insurance should be allowed to operate in the rural market.

• Only one State Level Life Insurance Company should be allowed to operate in eachstate.

(3) REGULATORY BODY

• The Insurance Act should be changed• An Insurance Regulatory Body should be set up.• Controller of Insurance (Currently a part from the Finance Ministry)should be made

independent

(4) INVESMENTS

• Mandatory Investments of LIC Life Fund in government securities to be reduced from75% to 50%.

• GIC and its subsidiaries are not to hold more than 5% in any company (There currentholdings to be brought down to this level over a period of time).

(5) CUSTOMER SERVICE

• LIC should pay interest on delays on payments beyond 30 days.• Insurance Companies must be encouraged to set up unit linked pension plans• Computerization of operations and updating of technology to be carried out in the

insurance industry.

The committee emphasized that in order to improve the customer service and increase thecoverage of insurance industry should opened up to competition. But at the same time, the

committee felt the need to exercise caution as any failure on the part of new players couldruin the public confidence in the industry.

Hence, it was decided to allow competition in a limited way by stipulating the minimumcapital requirement of Rs. 100 crores. The committee felt the need to provide greater autonomy to insurance companies in order to improve their performance and enable them toact as independent companies with economic motives. For this purpose, it had proposed

setting up an independent regulatory body.

7/27/2019 14651606 a Comparative Analysis Between LIC and Private Insurance Companies

http://slidepdf.com/reader/full/14651606-a-comparative-analysis-between-lic-and-private-insurance-companies 14/65

14

Liberalization :

OPENING UP OF INSURANCE SECTOR – 1999 THE INSURANCE

REGULATORY AND DEVELOPMENT AUTHORITY

Reforms in the Insurance sector were initiated with the passage of the IRDA Bill inParliament in December 1999. The IRDA since its incorporation as a statutory body in April 2000 has fastidiously stuck to its schedule of framing regulations andregistering the private sector insurance companies.

The other decision taken simultaneously to provide the supporting systems to theinsurance sector and in particular the life insurance companies was the launch of the IRDA's online service for issue and renewal of licenses to agents.

The approval of institutions for imparting training to agents has also ensured thatthe insurance companies would have a trained workforce of insurance agents in

place to sell their products, which are expected to be introduced by early next year.

Since being set up as an independent statutory body the IRDA has put in aframework of globally compatible regulations. In the private sector 14 lifeinsurance companies have been registered.

ENTRY OF PRIVATE COMPANIES

Under the IRDA Act, private companies can now operate in India's insuranceindustry. However, they must obtain a license from the IRDA before being

permitted to write business.

To have its license application considered, a domestic private company must be

registered in accordance with the Companies Act of 1956 and have approximatelyUS$ 20 million of investment capital. The specific licensing requirements thatPrivate Indian Companies must fulfill are set forth in the Registration on IndianInsurance Companies Regulations, published by the IRDA 2000.

LIFTING OF BARRIERS TO FOREIGN INVESTMENT

The IRDA Act also lifts certain barriers to foreign direct investment in Indianinsurance industry.

Global insurers are now permitted to set up and register a domestic company in

order to write business in India. However, regulations stipulate that they have acapital base of at least US $ 20 million, and their investment in such company is

capped at 26 percent. Thus, to participate in the market, they must form a jointventure with an Indian partner that is able to invest the remaining funds.

The equity investments limit is the same for global reinsures seeking to write business in India, but they are required to put up a capital of approximately US$ 45million in order to establish a domestic company.

7/27/2019 14651606 a Comparative Analysis Between LIC and Private Insurance Companies

http://slidepdf.com/reader/full/14651606-a-comparative-analysis-between-lic-and-private-insurance-companies 15/65

15

Since the IRDA first enacted these rules, 13 new life insurance companies haveentered the market.

On the other hand, no global reinsurer has established a domestic company.Instead, most of the top international reinsurance companies operate from their overseas offices by sharing the reinsurance risks picked up by the GIC. A recent

proposal has been put forward to increase foreign direct investment to 49 percent.In addition, global companies are pushing for the right to establish branch officesin India. These changes are likely to substantially increase the presence of international insurers, reinsurers, and brokers in India.

The IRDA Insurance Brokers Act in India 2002 permitted overseas insurance andreinsurance brokers to enter the market, but with the same equity cap as thatgoverning the operations of foreign insurers and reinsurers. Thus, foreign brokersmust also form a joint venture with an Indian partner in order to establish an Indian

broking house.

The 2002 IRDA legislation established four broker categories, one of which brokers must select when applying for a license:

1. Category 1A : Direct General Insurance Broker 2. Category 1B : Direct Life Insurance Broker 3. Category 2 : Reinsurance Broker 4. Category 3: Composite Broker 5. Category4: Others, for example Insurance Consultants and Risk

Management Consultants.

Each category has different solvency margins and capital adequacy ratios, and allcategories need to carry professional indemnity insurance at different minimum

levels.

In the years since market liberalization was initiated, the insurance sector haswitnessed some impressive changes. The needs of insurance and reinsurance

buyers have grown; the market is introducing new products to address these needs;and the services of brokers are now seen as critical to making informed insuranceand reinsurance decisions.

OVERVIEW OF THE CURRENT INSURANCE MARKET

In the years since the IRDA Act initiated market reforms, the insurance sector hasexperienced some remarkable changes.

The entry of a large number of Indian and Foreign private companies in lifeinsurance business has to lead greater choice in terms of products and services.Increased consumer awareness of the benefits and importance of insurance andreinsurance has generated many more buyers; and new distribution channels_ among them brokers, bank assurance, the Internet, and corporate agents_ have

provided additional ways of getting products and services to customers.

7/27/2019 14651606 a Comparative Analysis Between LIC and Private Insurance Companies

http://slidepdf.com/reader/full/14651606-a-comparative-analysis-between-lic-and-private-insurance-companies 16/65

16

Private insurance companies have to date written a small percentage of business inthis sector during the last three years, but they have ushered in a competitiveenvironment that has accelerated market growth.

State owned insurers still write the bulk of insurance business, and they have thenet worth required to underwrite large corporate risks without depending almostentirely on reinsurance support. However, their focus on restructuring is beginningto put them at a disadvantage against private competitors.

Over the next few years, the share of the market held by the public insurers isexpected to drop substantially, with private companies assuming a growing

percentage of the business written.

At present there are 15 private insurers with two standalone private players andremaining private-foreign joint venture.

Purpose and Need of Insurance :

Assets are insured, because they are likely to be destroyed through accidental occurrences.

Such possible occurrences are called perils. Fire, floods, breakdowns, lightening,

earthquakes, etc, are perils. If such perils can cause damage to the asset, we say that the asset

is exposed to that risk. Perils are the events. Risks are the consequential losses or damages.

The risk to a owner of a building, because of the peril of an earthquake, may be a few lakhs

or a few crores of rupees, depending on the cost of the building and the contents in it.

The risk only means that there is a possibility of loss or damage. The damage may or may nothappen. Insurance is done against the contingency that it may happen. There has to be an

uncertainty about the risk. Insurance is relevant only if there are uncertainties. If there is no

uncertainty about the occurrence of an event, it cannot be insured against. In the case of

human being, death is certain, but the time of death is uncertain. In the case of person who is

terminally ill, the time of death is not uncertain, though not exactly known. He cannot be

insured.

Insured does not protect the asset. It does not prevent its loss due to peril. The peril cannot be

avoided through insurance. The peril can sometimes be avoided through better safety and

damage control management. Insurance only tries to reduce the impact of the risk on the

owner of the asset and those who depend on that asset. It only compensates the losses and

that too, not fully.

Only economic consequences can be insured. If the loss is not financial, insurance may not be

possible. Example of non-economic losses are love and affection of parents, leadership of

managers, sentimental attachments to family heirlooms, innovative and creative abilities, etc.

7/27/2019 14651606 a Comparative Analysis Between LIC and Private Insurance Companies

http://slidepdf.com/reader/full/14651606-a-comparative-analysis-between-lic-and-private-insurance-companies 17/65

17

How Insurance Works?

The mechanism of insurance is very simple. People who are exposed to the same risks come

together and agree that, if any one of them suffers a loss, the others will share the loss and

make good to the person who lost. All people who send goods by ship are exposed to the

same risks, which are related to water damage, ship sinking, piracy, etc. Those owningfactories are not exposed to these risks, but they are exposed to different kinds of risks like,

fire, hailstorms, earthquake, lightning, burglary, etc. Like this, different kinds of risks can be

identified and separate groups made, including those exposed to such risks. By this method,

the heavy loss that any one of them may suffer (all of them may not suffer such losses at the

same time) is divided into bearable small losses by all. In other words, the risk is spread

among the community and the likely big impact on one is reduced to smaller manageable

impacts on all.

If a Jumbo Jet with more than 350 passengers crashes, the loss would run into several crores

of rupees. No airline would be able to bear such a loss. It is unlikely that many Jumbo Jets

will crash at same time. If 100 airline companies flying Jumbo Jets, come together into an

insurance pool, whenever one of the Jumbo Jets in the pool crashes, the loss to be borne by

each airline would come down to a few lakhs of rupees. Thus, insurance is a business of

sharing.

There are certain principles, which make it possible for insurance to remain a fair

arrangement. The first is that it is difficult for any one individual to bear the consequences of

the risks that he is exposed to. It will become bearable when the community shares the

burden. The second is that the perils should occur in an accidental manner. Nobody should be

in a position to make the risk happen. In other words, none in the group should set fire to hisassets and ask others to share the costs of damage. This would be taking unfair advantage of

an arrangement put into place to protect people from risks they are exposed to. The

occurrence has to be random, accidental, and not the deliberate creation of the insured person.

The manner in which the loss is to be shared can be determined before-hand. It may be

proportional to the risk that each person is exposed to. This would be indicative of the benefit

he would receive if the peril befell him. The share could be collected from the members after

the loss has occurred or the likely shares may be collected in advance, at the time of

admission to the group. Insurance companies collect in advance and create a fund from which

the losses are paid.

The collection to be made from each person in advance is determined on assumptions. While

it may not be possible to tell beforehand, which person will suffer, it may be possible to tell,

on the basis of past experiences, how many persons, on an average, may suffer losses. The

following two examples explain the above concept of insurance:

7/27/2019 14651606 a Comparative Analysis Between LIC and Private Insurance Companies

http://slidepdf.com/reader/full/14651606-a-comparative-analysis-between-lic-and-private-insurance-companies 18/65

18

Example 1

In a village, there are 400 houses, each valued at Rs. 20000. Each year, on the average, 4

houses get burnt, resulting into a total loss of Rs. 80000. If all the 400 owners come together

and contribute Rs. 200 each, the common fund would be Rs. 80000. this is enough to pay Rs.

20000 to each of the 4 owners whose houses got burnt. Thus, the risk of 4 owners is spread

over 400 house-owners of the village.

Example 2

There are 1000 persons who are all aged 50 and are healthy. It is expected that of these, 10

persons may die during the year. If the economic value of the loss suffered by the family of

each dying person is taken to be Rs. 20000, the total loss would work out to Rs. 200000. If

each person in a group contributed Rs. 200 a year, the common fund would be Rs. 200000.

This would be enough to par Rs. 20000 to the family of each of the ten persons who die.

Thus, the risks in the case of 10 persons, are shared by 1000 persons.

Insurance of ‘Human Asset’

A human being is an income generating asset. Ones manual labour, professional skills and

business acumen are the assets. This asset also can be lost through unexpectedly early death

or through sickness and disabilities caused by accidents. Accidents may or may not happen.

Death will happen, but the timing is uncertain. If it happens around the time of one s

retirement, when it could be expected that the income will normally cease, the person

concerned could have made some other arrangements to meet the continuing needs. But if it

happens much earlier when the alternate arrangements are not in place, there can be losses to

the person and dependents. Insurance is necessary to help those dependent on the income.

A person, who may have made arrangements for his needs after his retirement, also would

need insurance. This is because the arrangements would have been made on the basis of some

expectations like, likely to live for another 15 years, or that children will look after him. If

any of these expectations do not become true, the original arrangement would become

inadequate and there could be difficulties. Living too long can be as much a problem as dying

too young. Both are risks, which need to be safeguarded against. Insurance takes care.

7/27/2019 14651606 a Comparative Analysis Between LIC and Private Insurance Companies

http://slidepdf.com/reader/full/14651606-a-comparative-analysis-between-lic-and-private-insurance-companies 19/65

19

Insurance of Intangibles :

The concept of insurance has been extended beyond the coverage of tangible assets.

Exporters run risk of losses if the importers in the other country default in payments or in

collecting the goods. They will also suffer heavily due to sudden changes in currency

exchange rates, economic policies or political disturbances in the other country. These risks

are insured. Doctors run the risk of being charged with negligence and subsequent liability

for damages. The amounts in question can be fairly large, beyond the capacity of individuals

to bear. These are insured. Thus, insurance is extended to intangibles. In some countries, the

voice of a singer or the legs of a dancer may be insured.

Types of Insurance :

Any risk that can be quantified can potentially be insured. Specific kinds of risk that maygive rise to claims are known as "perils". An insurance policy will set out in detail which

perils are covered by the policy and which are not.

Below is a (non-exhaustive) list of the many different types of insurance that exist. A single

policy may cover risks in one or more of the categories set forth below. For example, auto

insurance would typically cover both property risk (covering the risk of theft or damage to

the car) and liability risk (covering legal claims from causing an accident). A homeowner's

insurance policy in the U.S. typically includes property insurance covering damage to the

home and the owner's belongings, liability insurance covering certain legal claims against the

owner, and even a small amount of health insurance for medical expenses of guests who areinjured on the owner's property.

Automobile insurance known in the UK as motor insurance, is probably the most common

form of insurance and may cover both legal liability claims against the driver and loss of or

damage to the insured's vehicle itself. Throughout most of the United States an auto insurance

policy is required to legally operate a motor vehicle on public roads. In some jurisdictions,

bodily injury compensation for automobile accident victims has been changed to a no-fault

system, which reduces or eliminates the ability to sue for compensation but provides

automatic eligibility for benefits.

Aviation insurance insures against hull, spares, deductible, hull war and liability risks. Boiler insurance (also known as boiler and machinery insurance or equipment breakdown

insurance) insures against accidental physical damage to equipment or machinery.

Builder's risk insurance insures against the risk of physical loss or damage to property

during construction. Builder's risk insurance is typically written on an "all risk" basis

covering damage due to any cause (including the negligence of the insured) not otherwise

expressly excluded.

7/27/2019 14651606 a Comparative Analysis Between LIC and Private Insurance Companies

http://slidepdf.com/reader/full/14651606-a-comparative-analysis-between-lic-and-private-insurance-companies 20/65

20

Business insurance can be any kind of insurance that protects businesses against risks. Some

principal subtypes of business insurance are (a) the various kinds of professional liability

insurance, also called professional indemnity insurance, which are discussed below under that

name; and (b) the business owners policy (BOP), which bundles into one policy many of the

kinds of coverage that a business owner needs, in a way analogous to how homeowners

insurance bundles the coverage that a homeowner needs.

Casualty insurance insures against accidents, not necessarily tied to any specific property.

Credit insurance repays some or all of a loan back when certain things happen to the

borrower such as unemployment, disability, or death. Mortgage insurance (which see below)

is a form of credit insurance, although the name credit insurance more often is used to refer to

policies that cover other kinds of debt.

Crime insurance insures the policyholder against losses arising from the criminal acts of

third parties. For example, a company can obtain crime insurance to cover losses arising from

theft or embezzlement.

Crop insurance "Farmers use crop insurance to reduce or manage various risks associated

with growing crops. Such risks include crop loss or damage caused by weather, hail, drought,

frost damage, insects, or disease, for instance."

Defense Base Act Workers' compensation or DBA Insurance provides coverage for civilian

workers hired by the government to perform contracts outside the US and Canada. DBA is

required for all US citizens, US residents, US Green Card holders, and all employees or

subcontractors hired on overseas government contracts. Depending on the country, Foreign

Nationals must also be covered under DBA. This coverage typically includes expenses

related to medical treatment and loss of wages, as well as disability and death benefits.

Directors and officers liability insurance protects an organization (usually a corporation)

from costs associated with litigation resulting from mistakes incurred by directors and

officers for which they are liable. In the industry, it is usually called "D&O" for short.

Disability insurance policies provide financial support in the event the policyholder is

unable to work because of disabling illness or injury. It provides monthly support to help pay

such obligations as mortgages and credit cards.

o Total permanent disability insurance provides benefits when a person is permanently

disabled and can no longer work in their profession, often taken as an adjunct to life

insurance.

Errors and omissions insurance: See "Professional liability insurance" under "Liability

insurance". Expatriate insurance provides individuals and organizations operating outside of their home

country with protection for automobiles, property, health, liability and business pursuits.

Financial loss insurance protects individuals and companies against various financial risks.

For example, a business might purchase cover to protect it from loss of sales if a fire in a

factory prevented it from carrying out its business for a time. Insurance might also cover the

failure of a creditor to pay money it owes to the insured. This type of insurance is frequently

7/27/2019 14651606 a Comparative Analysis Between LIC and Private Insurance Companies

http://slidepdf.com/reader/full/14651606-a-comparative-analysis-between-lic-and-private-insurance-companies 21/65

21

referred to as "business interruption insurance." Fidelity bonds and surety bonds are included

in this category, although these products provide a benefit to a third party (the "obligee") in

the event the insured party (usually referred to as the "obligor") fails to perform its

obligations under a contract with the oblige.

Health insurance policies will often cover the cost of private medical treatments if the

National Health Service in the UK (NHS) or other publicly-funded health programs do not

pay for them. It will often result in quicker health care where better facilities are available.

Home insurance or homeowners insurance: See "Property insurance".

Liability insurance is a very broad superset that covers legal claims against the insured.

Many types of insurance include an aspect of liability coverage. For example, a homeowner's

insurance policy will normally include liability coverage which protects the insured in the

event of a claim brought by someone who slips and falls on the property; automobile

insurance also includes an aspect of liability insurance that indemnifies against the harm that

a crashing car can cause to others' lives, health, or property. The protection offered by a

liability insurance policy is twofold: a legal defense in the event of a lawsuit commenced

against the policyholder and indemnification (payment on behalf of the insured) with respectto a settlement or court verdict. Liability policies typically cover only the negligence of the

insured, and will not apply to results of willful or intentional acts by the insured.

o Environmental liability insurance protects the insured from bodily injury, property damage

and cleanup costs as a result of the dispersal, release or escape of pollutants.

o Professional liability insurance also called professional indemnity insurance, protects

professional practitioners such as architects, lawyers, doctors, and accountants against

potential negligence claims made by their patients/clients. Professional liability insurance

may take on different names depending on the profession. For example, professional liability

insurance in reference to the medical profession may be called malpractice insurance.

Notaries public may take out errors and omissions insurance (E&O). Other potential E&O policyholders include, for example, real estate brokers, home inspectors, appraisers, and

website developers.

Life insurance provides a monetary benefit to a decedent's family or other designated

beneficiary, and may specifically provide for burial, funeral and other final expenses. Life

insurance policies often allow the option of having the proceeds paid to the beneficiary either

in a lump sum cash payment or an annuity.

o Annuities provide a stream of payments and are generally classified as insurance because

they are issued by insurance companies and regulated as insurance and require the same kinds

of actuarial and investment management expertise that life insurance requires. Annuities and pensions that pay a benefit for life are sometimes regarded as insurance against the possibility

that a retiree will outlive his or her financial resources. In that sense, they are the complement

of life insurance and, from an underwriting perspective, are the mirror image of life

insurance.

Locked funds insurance is a little-known hybrid insurance policy jointly issued by

governments and banks. It is used to protect public funds from tamper by unauthorized

parties. In special cases, a government may authorize its use in protecting semi-private funds

7/27/2019 14651606 a Comparative Analysis Between LIC and Private Insurance Companies

http://slidepdf.com/reader/full/14651606-a-comparative-analysis-between-lic-and-private-insurance-companies 22/65

22

which are liable to tamper. The terms of this type of insurance are usually very strict.

Therefore it is used only in extreme cases where maximum security of funds is required.

Marine insurance and marine cargo insurance cover the loss or damage of ships at sea or on

inland waterways, and of the cargo that may be on them. When the owner of the cargo and

the carrier are separate corporations, marine cargo insurance typically compensates the owner

of cargo for losses sustained from fire, shipwreck, etc., but excludes losses that can berecovered from the carrier or the carrier's insurance. Many marine insurance underwriters will

include "time element" coverage in such policies, which extends the indemnity to cover loss

of profit and other business expenses attributable to the delay caused by a covered loss.

Mortgage insurance insures the lender against default by the borrower.

National Insurance is the UK's version of social insurance (which see below).

No-fault insurance is a type of insurance policy (typically automobile insurance) where

insurers are indemnified by their own insurer regardless of fault in the incident.

Nuclear incident insurance covers damages resulting from an incident involving radio active

materials and is generally arranged at the national level. (For the United States, see the Price-

Anderson Nuclear Industries Indemnity Act.)

Pet insurance insures pets against accidents and illnesses - some companies cover

routine/wellness care and burial, as well.

Political risk insurance can be taken out by businesses with operations in countries in which

there is a risk that revolution or other political conditions will result in a loss.

Pollution Insurance A first-party coverage for contamination of insured property either by

external or on-site sources. Coverage for liability to third parties arising from contamination

of air, water or land due to the sudden and accidental release of hazardous materials from the

insured site. The policy usually covers the costs of cleanup and may include coverage for

releases from underground storage tanks. Intentional acts are specifically excluded

Property insurance provides protection against risks to property, such as fire, theft or

weather damage. This includes specialized forms of insurance such as fire insurance, flood

insurance, earthquake insurance, home insurance, inland marine insurance or boiler

insurance.

Purchase insurance is aimed at providing protection on the products people purchase.

Purchase insurance can cover individual purchase protection, warranties, guarantees, care

plans and even mobile phone insurance. Such insurance is normally very limited in the scope

of problems that are covered by the policy.

Retrospectively Rated Insurance is a method of establishing a premium on large commercial

accounts. The final premium is based on the insured's actual loss experience during the policyterm, sometimes subject to a minimum and maximum premium, with the final premium

determined by a formula. Under this plan, the current year's premium is based partially (or

wholly) on the current year's losses, although the premium adjustments may take months or

years beyond the current year's expiration date. The rating formula is guaranteed in the

insurance contract. Formula: retrospective premium = converted loss + basic premium × tax

multiplier. Numerous variations of this formula have been developed and are in use.

Social insurance can be many things to many people in many countries. But a summary of

7/27/2019 14651606 a Comparative Analysis Between LIC and Private Insurance Companies

http://slidepdf.com/reader/full/14651606-a-comparative-analysis-between-lic-and-private-insurance-companies 23/65

23

its essence is that it is a collection of insurance coverage (including components of life

insurance, disability income insurance, unemployment insurance, health insurance, and

others), plus retirement savings, that mandates participation by all citizens. By forcing

everyone in society to be a policyholder and pay premiums, it ensures that everyone can

become a claimant when or if he/she needs to. Along the way this inevitably becomes related

to other concepts such as the justice system and the welfare state. This is a large, complicatedtopic that engenders tremendous debate, which can be further studied in the following articles

(and others):

o Social welfare provision

o Social security

o Social safety net

o National Insurance

o Social Security (United States)

o Social Security debate (United States)

Terrorism insurance provides protection against any loss or damage caused by terrorist

activities.

Title insurance provides a guarantee that title to real property is vested in the purchaser

and/or mortgagee, free and clear of liens or encumbrances. It is usually issued in conjunction

with a search of the public records performed at the time of a real estate transaction.

Travel insurance is an insurance cover taken by those who travel abroad, which covers

certain losses such as medical expenses, lost of personal belongings, travel delay, personalliabilities, etc.

Workers' compensation insurance replaces all or part of a worker's wages lost and

accompanying medical expense incurred because of a job-related injury.

Advantages of Life Insurance :

Life insurance has no competition from any other business. Many people think that life

insurance is an investment or a means of saving. This is not a correct view. When a person

saves, the amount of funds available at any time is equal to the amount of money set aside inthe past, plus interest. This is so in a fixed deposit in the bank, in national savings certificates,

in mutual funds and all other savings instruments. If the money is invested in buying shares

and stocks, there is the risk of the money being lost in the fluctuations of the stock market.

Even if there is no loss, the available money at any time is the amount invested plus

appreciation. In life insurance, however, the fund available is not the total of the savings

already made (premiums paid), but the amount one wished to have at the end of the savings

period (which is the next 20 or 30 years). The final fund is secured from the very beginning.

7/27/2019 14651606 a Comparative Analysis Between LIC and Private Insurance Companies

http://slidepdf.com/reader/full/14651606-a-comparative-analysis-between-lic-and-private-insurance-companies 24/65

24

One is paying for it later, out of the savings. One has to pay for it only as long as one lives or

for a lesser period if so chosen. There is no other scheme which provides this kind of benefit.

Therefore life insurance has no substitute.

Even so, a comparison with other forms of savings will show that life insurance has the

following advantages.

In the event of death, the settlement is easy. The heirs can collect the moneys quicker,

because of the facility of nomination and assignment. The facility of nomination is now

available for some bank accounts.

There is a certain amount of compulsion to go though the plan of savings. In other forms, if

one changes the original plan of savings, there is no loss. In insurance, there is a loss.

Certain cannot claim the life insurance moneys. They can be protected against attachments

by courts.

There are tax benefits, both in income tax and in capital gains.

Marketability and liquidity are better. A life insurance policy is property and can be

transferred or mortgaged. Loans can be raised against the policy.

The following tenets help agents to believe in the benefits of life insurance. Such faith will

enhance their determination to sell and their perseverance.

Life insurance is not only the best possible way for family protection. There is no other

way.

Insurance is the only way to safeguard against the unpredictable risks of the future. It is

unavoidable.

The terms of life are hard. The terms of insurance are easy.

The value of human life is far greater than the value of property. Only insurance can

preserve it.

Life insurance is not surpassed by many other savings or investment instrument, in terms of

security, marketability, stability of value or liquidity.

Insurance, including life insurance, is essential for the conservation of many businesses, just

as it is in the preservation of homes.

Life insurance enhances the existing standards of living.

Life insurance helps people live financially solvent lives.

Life insurance perpetuates life, liberty and the persuit of happiness.

Life insurance is a way of life.

7/27/2019 14651606 a Comparative Analysis Between LIC and Private Insurance Companies

http://slidepdf.com/reader/full/14651606-a-comparative-analysis-between-lic-and-private-insurance-companies 25/65

25

The Business of Insurance :

Insurance companies are called insurers. The business of insurance is to (a) bring together

persons with common insurance interests (sharing the same risks), (b) collect the share or

contribution (called premium) from all of them, and (c) pay out compensation (called claims)

to those who suffer. The premium is determined on the same lines as indicated in the

examples above, but with some further refinements.

In India, insurance business is classified primarily as life and non-life or general. Life

insurance includes all risks related to the lives of human beings and General insurance covers

the rest. General insurance has three classifications viz., Fire (dealing with all fire related

risks), Marine (dealing with all transport related risks and ships) and Miscellaneous (dealing

with all others like liability, fidelity, motor crop, personal accident, etc.). Personal accident

and sickness insurance, which are related to human beings, is classified as non-life in India,

but is classified as life, in many other countries. What is Non-life in India is termed as

Property and Casualty in some other countries.

The premium is based on expectations of the losses. These expectations are based on studies

of occurrences in the past and the use of statistical principles. There is, in statistics, a law of

large numbers. When you toss a coin, the chance of a head or tail coming up is half. If the

coin is tossed 10 times, one cannot be sure that the head will come up 5 times. If the coin is

tossed 1 million times, the number of heads will be closer to half a million proportionately

than in the case of 10. The variation will be less as a percentage. So also, the larger the

numbers (of risks) included in the pool, the better the chances that the assumptions regarding

the probability of the risk occurring, which is the basis of premium calculation, will be

realized in practice. In order to be amenable to statistical predictions, insurers have to insure

large numbers of risks. Larger the spread of business better is the experience in relation to

expectations.

The business of insurance is nothing but one of sharing. It spreads losses of an individual

over the group of individuals who are exposed to similar risks. People who suffer loss get

relief because their loss is made good. People who do not suffer loss are relieved because

they were spared the loss.

The insurer is in the position of a trustee as it is managing the common fund, for and on

behalf of the community of policyholders. It has to ensure that nobody is allowed to take

undue advantage of the arrangement. That means that the management of the insurance

business requires care to prevent entry (into the group) of people whose risks are not of thesame kind as well as paying claims on losses that are not accidental. The decision to allow

entry is the process of underwriting of risk. Underwriting includes assessing the risk, which

means, making an evaluation of how much is the exposure to risk. The premium to be

charged depends on this assessment of the risk. Both underwriting and claim settlements have

to be done with great care.

7/27/2019 14651606 a Comparative Analysis Between LIC and Private Insurance Companies

http://slidepdf.com/reader/full/14651606-a-comparative-analysis-between-lic-and-private-insurance-companies 26/65

26

Criticism of Insurance Companies :

Some people believe that modern insurance companies are money-making businesses which

have little interest in insurance. They argue that the purpose of insurance is to spread risk so

the reluctance of insurance companies to take on high-risk cases (e.g. houses in areas subject

to flooding, or young drivers) runs counter to the principle of insurance.

Other criticisms include:

Insurance policies contain too many exclusion clauses. For example, some house insurance

policies do not cover damage to garden walls.

Most insurance companies now use call centre and staff attempt to answer questions by

reading from a script. It is difficult to speak to anybody with expert knowledge.

Role of Insurance in Economic Development :

For economic development, investments are necessary. Investments are made out of savings.A life insurance company is a major instrument for the mobilization of savings of people,

particularly from the middle and lower income groups. These savings are channeled into

investments for economic growth.

As on 31.3.2002, the total investments of the LIC exceeded Rs. 245000 crores, of which more

than Rs. 130000 crores were directly in Government (both State and Centre) related

securities, more than Rs. 12000 crores in the State Electricity Boards, nearly Rs. 20000 crores

in housing loans and Rs. 4000 crores in water supply and sewerage systems. Other

investments included road transport, setting up industrial estates and directly financing

industry. Investments in the corporate sector (shares, debentures and term loans) exceeded

Rs. 30000 crores. These directly affect the lives of the people and their economic well-being.

A life insurance company will have large funds. These amounts are collected by way of

premiums. Every premium represents a risk that is covered by that premium. In effect,

therefore, these vast amounts represent pooling of risks. The funds are collected and held in

trust for the benefit of the policyholders. The management of life insurance companies are

required to keep this aspects in mind and make all its decisions in ways that benefit the

community. This applies also to its investments. That is why successful insurance companies

would not be found investing in speculative ventures. Their investments, as in the case of the

LIC, benefit the society at large.

Apart from investments, business and trade benefit through insurance. Without insurance,

trade and commerce will find it difficult to face the impact to major perils like fire,

earthquake, floods, etc. Financiers, like banks, collapse if the factory, financed by it, is

reduces to ashes by terrible fire. Insurers cover also the loss to financiers, if their debtors

default.

7/27/2019 14651606 a Comparative Analysis Between LIC and Private Insurance Companies

http://slidepdf.com/reader/full/14651606-a-comparative-analysis-between-lic-and-private-insurance-companies 27/65

27

2. GLOBAL INSURANCE INDUSTRY :

The global insurance industry is one of the largest sectors of finance. It ranges from

consumer to corporate and industrial insurance, and even reinsurance, or insurance of

insurance.

The major insurance markets of the world are obviously the US, Europe, Japan, and SouthKorea. Emerging markets are found throughout Asia, specifically in India and China, and arealso in Latin America.

With the internet and other forms of high-speed communication, companies and individualsare now able to purchase insurance and related financial products from almost anywhere inthe world. Increasing affluence, especially in developing countries, and a risingunderstanding of the need to protect wealth and human capital has led to significant growth inthe insurance industry.

Given the evolving and growing socio-economic conditions worldwide, insurance companiesare increasingly reaching out across borders and are offering more competitive andcustomized products than ever before.

Over the past ten years, global insurance premiums have risen by more than 50%, withannual growth rates ranging between 2 and 10%.In 2004, global insurance premiumsamounted to $3.3 trillion.

The majority of insurance comes from developed nations such as most of Europe, the US,and Japan. In 2004, premiums in North American amounted to $1,217 billion, while theEuropean Union generated $1,198 billion, and Japan produced $492 billion. The UK amounted to $295 billion.

The four biggest generators of insurance premiums comprised almost two-thirds of premiumsfor 2004, the US and Japan amount to half, while they only make up 7% of the world s

population.

In contrast, the emerging markets that make up 85% of the worlds population produced only10% of the premiums.

The leading global insurance companies are:

• Zurich Financial Services,• AXA•

Berkshire Hathaway/ Berkshire Hathaway Re• Allianz• Aviva• ING Group• Munich RE Group• American International Group (AIG)• Nippon Life Insurance• Assicurazioni Generali

7/27/2019 14651606 a Comparative Analysis Between LIC and Private Insurance Companies

http://slidepdf.com/reader/full/14651606-a-comparative-analysis-between-lic-and-private-insurance-companies 28/65

28

GLOBAL LIFE INSURANCE DENSITY :

Continent/Country 2001** 2002** 2003** 2004** 2005** 2006**

North America 1508.6 1563.8 1565.7 1617.2 1686.3 1731.8

United States 1602 1662.6 1657.5 1692.5 1753.2 1789.5

Canada 675.9 657.3 722.9 926.1 1071.9 1204.1

Latin America 26.3 29.1 30 37.2 42.0 51.3

Brazil 10.8 27.2 35.8 45.9 56.8 72.5

Mexico 53.2 59.2 41.3 50.2 49.9 62.9Uruguay 21.5 17.8 15.4 N/A 15.5 16.6

Argentina 68.8 19.7 24.2 34.5 35.4 43.8

Panama 39.3 44.6 42.4 50.6 47.2 51.2

Chile 122.1 103.5 138.3 164.5 174.9 176

Colombia 11.5 12.5 12.4 14.3 16.8 20.5

Europe 573.2 620.4 726.9 848.1 911.8 1119.6

United kingdom 2567.9 2679.4 2617.1 3190.4 3287.1 5139.6

Switzerland 2715.7 3099.7 3431.8 3275.1 3078.1 3111.8

Netherlands 1345 1296.1 1561.7 1936.5 1954.2 2071.6

France 1268.2 1349.5 1767.9 2150.2 2474.6 2922.5

Belgium 1155 1323.6 2004.8 2291.2 2988.7 2427.7

Sweden 1356 1232.2 1602.3 1764.3 2105.2 2214.6

Denmark 1364.4 1574.9 2037.5 2310.5 2489.9 2840.8

Germany 674.3 736.7 930.4 1021.3 1042.1 1136.1

Italy 720.8 904.9 1238.3 1417.2 1449.8 1492.8

Austria 632 648.7 811 955.3 1095.1 1104.6

Portugal 302.9 418.6 611.4 768.1 1113.7 1131.5

Spain 491 588 488.6 571.9 615.8 651.0

Poland 48.7 50.7 59.9 73.3 101.9 150.5

Russia 33.2 23.1 33.9 24.8 6.3 4.0

Croatia 25.3 33.2 46.3 58.7 70.9 81.8

Hungary 59.3 76.7 99.1 117.3 148.2 192.3

Greece 108.9 116 152.1 177.9 213.1 256.7

Bulgaria 5 9.9 5.5 8.2 11.1 13.2

Ukraine 0.1 0.1 0.3 0.6 1.3 1.9

Turkey 5.5 6.5 8.4 12 12.7 13.1

Asia 125 128.1 140.1 147.2 149.6 154.6

South Korea 763.4 821.9 873.6 1006.8 1210.6 1480.0

Japan 2806.4 2783.9 3002.9 3044 2956.3 2829.3Tiwan 760.9 925.1 1050.1 1494.6 1699.1 1800.0

Hongkong 1249.7 1237.9 1483.9 1884.3 2213.2 2456

Israel 525.2 459.3 460.8 467.4 510.2 532.6

Malaysia 129.5 118.7 139.8 167.3 188 189.2

Singapore 713.2 730.1 1300.2 1483.9 1591.4 1616.5

Thailand 34.1 42.1 52 50.8 54.6 60

India 9.1 11.7 12.9 15.7 18.3 33.2

China 12.2 19.5 25.1 27.3 30.5 34.1

Phillipines 6.6 8.7 8.6 9.4 10.6 13.1

UAE 56.3 74 72.5 59.7 74.7 89.8Srilanka 4.3 4.5 5.3 6.2 6.9 8.5

Indonesia 3.6 5.2 6.4 7.5 10.5 12.5

Oman 13.6 14.8 13.8 14.2 17.3 14.3

Vietnam 2.1 3.8 4.1 7.3 6.1 6.1

Iran 1.1 1.5 1.7 2.3 2.2 2.6

Kuwait 30.3 36.8 36.9 39.1 35.7 40.9

Pakistan 1.2 1 1.1 1.5 1.9 2.3

Saudia Arabia 0.6 1.7 1.7 2.1 0.7 0.8

Africa 22.4 21.5 26.1 30.3 30.7 38.3

South Africa 377.2 360.5 476.5 545.5 558.3 695.6

Mauritius 95.3 103.7 119.1 133.1 136.1 N/A

Zimbabwe 12.4 7.8 21.4 N/A N/A N/A

Morocco 9.4 12.2 12 10.6 11.7 14.7

Kenya 2.9 3 3.4 3.7 4.5 5.3

Nigeria 0.5 0.5 0.6 0.7 0.5 0.8

Egypt 2.7 2.4 2.7 3.1 4 4.7

Algeria 0.4 0.5 0.5 0.8 0.9 1.2

Oceania 697.5 668.7 750.7 851 885 896.3Australia 1040.3 1010.4 1129.3 1285.1 1366.7 1389

New Zealand 198.4 211.1 272 318 219.7 215

World 235 247.3 267.1 291.5 299.5 330.6

Source: Swiss Re, Sigma volumes

* Insurance density is measured as ratio of premium to total population

** Data relates to calender

years Figure in US$

www.indiainsuranceresearc

h.com

7/27/2019 14651606 a Comparative Analysis Between LIC and Private Insurance Companies

http://slidepdf.com/reader/full/14651606-a-comparative-analysis-between-lic-and-private-insurance-companies 29/65

29

3. PERFORMANCE OF INDIAN INSURANCE INDUSTRY :

Performance up to October 2006

The performance growth rate that was 22.8 percent as at September 2006 has moved

up to 23.3 percent at the end of October 2006, an improvement of significance. Thetotal premium at the end of October is Rs.14,628 crore as against Rs.11,855 crore.The established players have added Rs.807 crore at a growth rate of 8.3 percent withthe new players adding Rs.1966 crore at a growth rate of 62 percent. Here again,ICICI Lombard has achieved an accretion of Rs.887 crore; whereas the total accretionof all the established players is Rs 807 crores, a truly impressive record. New Indiawith Rs.286 crore, closely followed by Oriental with Rs.277 crore are the major contributors for the established players. Reliance, a late starter in the race for

premium acquisition has recorded an accretion of Rs.357 crore as against a meager last year renewal of Rs.89 crore. The growth path is now led by several players: witheight out of the twelve players having achieved accretions in excess of Rs.100 croreand more at the end of October 2006. With the imminent detariffing around the corner

in January 2007, the next two months should witness even more fierce battles for supremacy of the market turf. A few of the new players are inching towards breakinginto the big league premium players of yesteryears and this may happen sooner than

one thought. Interesting and challenging times are certainly ahead for all the players.

Premiums Rise 163.68% over October, 2006

Individual premium:

The life insurance industry underwrote Individual Single Premium of Rs.1336610.10lakh for the period ended October, 2006 of which the private insurers garnered

Rs.118242.78 lakh and LIC garnered Rs.1218367.32 lakh. The correspondingnumbers for the previous year were Rs.443296.40 lakh for the industry, with privateinsurers underwriting Rs.64530.68 lakh and LIC Rs.378765.72 lakh. The Individual

Non-Single Premium underwritten during April-October, 2006 was Rs.1771903.71lakh of which the private insurers underwrote Rs.536863.16 lakh and LICRs.1235040.55 lakh. The corresponding numbers for the previous year wereRs.743586.24 lakh, Rs.260432.63 lakh and Rs.483153.61 lakh respectively.

Group premium:

The industry underwrote Group Single Premium of Rs.467348.58 lakh of which the private insurers underwrote Rs.30147.74 lakh and LIC Rs.437200.84 lakh. The livescovered being 7678192, 456696 and 7221496 respectively. The correspondingnumbers for the previous year were Rs.171382.70 lakh with private insurersunderwriting Rs.17261.98 lakh and LIC Rs.154120.72 lakh and the lives covered

being 8547743, 397721 and 8150022 respectively. The Group Non-Single Premiumunderwritten during April-October, 2006 was Rs.53221.05 lakh which wasunderwritten entirely by the private insurers, covering 2366084 lives. Thecorresponding numbers for the previous year were Rs. 18031.15 lakh and covering1277400 lives.

7/27/2019 14651606 a Comparative Analysis Between LIC and Private Insurance Companies

http://slidepdf.com/reader/full/14651606-a-comparative-analysis-between-lic-and-private-insurance-companies 30/65

30

Segment-wise segregation:

A further segregation of the premium underwritten during the period indicates thatLife, Annuity, Pension and Health contributed Rs.2329869.52 lakh (64.24%),Rs.74006.48 lakh (2.04%), Rs.1221904.91 lakh (33.69%) and Rs.897.90 lakh (0.02%)respectively. In respect of LIC, the break up of life, annuity and pension categories

was Rs.1677831.45 lakh (58.04%), Rs.69437.82 lakh (2.40%) and Rs.1143339.44lakh (39.55%) respectively. In case of the private insurers, Rs.652038.07 lakh(88.58%), Rs.4568.66 lakh (0.62%), Rs.78565.47 lakh (10.67%) and Rs.897.90 lakh(0.12%) respectively was underwritten in the four segments.

Unit linked and conventional premium: