Embed Size (px)

Citation preview

7/29/2019 122782016 Lithium Fundamentals Remain Strong

http://slidepdf.com/reader/full/122782016-lithium-fundamentals-remain-strong 1/7

Lithium Industry Fundamentals Remain Strong

EVENT – ROCKWOOD HOLDS INVESTOR DAY; OTHER LITHIUM INDUSTRY UPDATES

On January 15th, Rockwood Holdings (ROC-US; Not Covered) held an investor day; we listened to the webcast and wacutely interested in the leading lithium producer’s comments about the industry, particularly with respect to outlooksupply/demand, and strategy for M&A. Rockwood’s webcast presentation was certainly indicative of a continued initiativdrive further growth in their lithium business. The Company which has a 50% market share in the global lithium supply chintends to maintain that market share going forward, and thus, there is a good likelihood that the Company will puadditional lithium acquisitions. In addition to summarizing some of the key themes from the Rockwood investor day, thisalso provides an update of the landscape in the lithium industry. We summarize the key reasons why we believe there wi

further consolidation in the sector, and why other companies in addition to Rockwood may pursue acquisitions. We csome of the leading take-out candidates within our research coverage. This note summarizes the strategic attractivenethese companies, and highlights the most likely takeout candidates in the near-term.

INDUSTRY IMPACT & INVESTMENT STRATEGY; M&A CONSIDERATIONS

Our view that the outlook for supply and demand in the lithium industry remains tight was supported by the lithium segmof Rockwood’s investor day. Mainly due to the rapid growth of lithium-ion batteries, Rockwood expects total demand inindustry to grow at a rate of 10% to 15% over the next decade. This may prove low if Rockwood’s admittedly conservaprojections for pure electric vehicles (EV) turn out to be indeed conservative. A 10% CAGR in supply over the next decadbelieved to lag demand growth over the next decade, suggesting the possibility for continued strength in lithium prices.

In effect, Rockwood’s presentation espoused the virtues of both brine and hard rock projects in terms of allowing the Compto execute on its growth strategy. Immediately below, we contrast the characteristics of both hard rock and brine lithprojects. When considering both current industry conditions and the characteristics of these types of projects, we conclude

CLQ appears to be the most likely take-out candidate at the present time.

Best Hard Rock Lithium Plays – Offering Product Purity, Lower Capex Requirements, Access to North American Marke

1) Good hard rock projects are regarded by lithium end-users as having good quality, and lower amounts of certain impurthat can do harm in supply chains. 2) Lower capital requirements to put hard rock projects into production is also anoadvantage over brines, which is noteworthy considering Rockwood’s long-term growth capex budget which equates to 3.5its revenue. 3) Market presence, being the ability to locate close to customers and markets is something that the hard projects allow in certain situations. For example, Talison’s proximity to the China market attracted Rockwood partly due toaspect. With companies like Rockwood and FMC being U.S. based, the hard rock companies below may provide ROCFMC with an early mover advantage in the growing battery sector in North America, and also be in close proximitheadquarters.

Canada Lithium Corp. (CLQ-T; Spec. Buy, $1.25 target) is close to completing the construction of an open-pit lith

carbonate mine and processing plant near Val d'Or, Quebec. The company is expected to start commercial produimminently, and has essentially sold out all of its 2013 lithium carbonate production through the use of off-take agreeme

Nemaska Lithium Inc. (NMX-T; Spec Buy, $0.79 target) is a Quebec-based mine developer planning to produce lithhydroxide and lithium carbonate from a high grade hard rock deposit in the James Bay region. We expect Nemaskachieve commercial production in 2015. Next to Talison, it has the highest grading hard rock project in the world.

Critical Elements Corp. (CRE-T; Not Covered) is a Quebec-based mineral exploration company focusing on tantalithium, niobium, and rare metals. Its flagship Rose project is at the feasibility stage and has delineated a resource of 64tonnes of LCE in the Indicated category and 227,565 tonnes of LCE in the Inferred category.

Matt Gowing, CFA 416.860.8675, [email protected] Jeremy Dason, Associate 416.860.6325, [email protected]

This report has been created by Analysts that are employed by Mackie Research Capital Corporation, a Canadian Investment Dealer. For further disclosures, please see last page of this

JANUARY 22,

7/29/2019 122782016 Lithium Fundamentals Remain Strong

http://slidepdf.com/reader/full/122782016-lithium-fundamentals-remain-strong 2/7

www.mackieresearch.com The MORNING CALL – Industry Update Pa

Leading Brine Lithium Plays – Potential for Larger Scale and By-Products, but Purity and Pricing is the Sacrifice

“Best in breed” brine projects may host larger lithium resources, and have typically greater production capacities than do hard rprojects. This certainly aligns with the initiative of Rockwood to be the Volume leader in the market. Aside from the fact that they situated at the low end of the global cost curve, the largest brine based lithium projects also provide the attraction of offering marbreadth. For example, the brine projects of South America and Argentina also generate potash as a saleable commodity to agricultmarkets. Some projects are also capable of producing boron and other items. One downside for the brine projects is their grea

requirement of capital to put into production. In a capital constrained market, this can impact on the ability to acquire constructfinancing. The presence of an off-take or strategic partnership may be a pre-requisite for these projects to get built. Even with thitems, the current financing environment may make the requirements of financing these projects as too onerous at the present time

Lithium Americas Corp. (LAC-T; Spec Buy, $2.45 target) is focused on developing its Cauchari-Olaroz brine projectArgentina. The project hosts one of the largest lithium resources in the world and also has the potential to produce potash aby-product. The Company has completed a feasibility study for the project and is actively engaged in discussions with sevethird parties regarding a potential off-take agreement or strategic investment. LAC has received its final construction perfrom the Argentinean province of Jujuy and we forecast LAC to enter commercial production by 2015.

Orocobre Limited (ORL-T, ORE-AU; Not Covered) is focused on its advanced-stage Salar de Olaroz lithium brine projectArgentina. The Company began construction on the project in November 2012 and is targeting to achieve commerproduction by April 2014. Orocobre entered into a JV agreement with Toyota Tsusho Corporation (TTC) whereby TTC w

fund the development of the Salar de Olaroz project.

Figure 1: Lithium Developer Comp Table

Last Updated: Oct 11, 2011

Ticker Market Last

Cap ($mm) Price ($)

Lithium Americas 1 LAC-T 75 0.97 27 6 n/a 6 1,8

Rodinia Lithium 2 RM-V 18 0.20 n/a n/a 5 5 1,0

Orocobre 3 ORL-T 158 1.53 n/a 22 n/a 22 10,9

BRINE AVERAGES 14 5 11 4,6

Canada Lithium 5 CLQ-T 317 0.93 688 319 460 188 13,6

Western Lithium 6 WLC-T 15 0.15 39 10 16 6 4

Rock Tech Lithium 7 RCK-V 3 0.04 n/a n/a 23 15

Nemaska Lithium 8 NMX-V 50 0.49 65 49 285 42 1,5

Critical Element Resources 8 CRE-V 24 0.22 n/a 35 98 26 8

Galaxy Resources 9 GXY-AU 193 0.38 n/a 524 1,675 399 9,5

Talison Lithium (Tianqi offer) # TLH-T 858 7.50 334 177 7,387 173 15,7

HARD ROCK AVERAGES 281 186 1,421 121 6,9

EV

Product

($/ton

EV/Total

Resource

($/tonne)

EV/Inferred

Resource

($/tonne)

EV/Reserve

($/tonne)

EV/M&I

Resource

($/tonne)

Source: Thomson One, Mackie Research Capital

7/29/2019 122782016 Lithium Fundamentals Remain Strong

http://slidepdf.com/reader/full/122782016-lithium-fundamentals-remain-strong 3/7

www.mackieresearch.com The MORNING CALL – Industry Update Pa

CLQ remains our top lithium pick considering a whole host of factors: Our preferred play among junior lithium companieCanada Lithium. This near-term producer is an attractive takeout candidate for a number of the lithium majors due to its favouramining jurisdiction and the de-risked nature of its flagship project. In the table below, we present the rationale for three of world’s top lithium producers to pursue an acquisition of Canada Lithium.

Figure 2: Lithium Producers – Rationale for a Potential Takeout of CLQ

Sociedad Química y Minera de Chile S.A Rockwood Holdings Inc. FMC Corp.

SQM - NYSE ROC - NYSE FMC - NYSE

•

•

•

•

•

•

Sociedad Química y Minera de Chile S.A Rockwood Holdings Inc. FMC Corp.

SQM - NYSE ROC - NYSE FMC - NYSE

• SQM's lithium operations in Chile have been

shown to be exposed to a considerable amount

of regulatory risk. A geographical diversificationof operations could help to reduce risk from this

source.

• ROC recently had its takeout bid for Talison

Lithium trumped by China's Tianqi. ROC will

most likely be seeking to pursue additionalacquisition candidates in order to grow its

market share.

• FMC's operations in Argentina have historical

been impacted by weather related issues,

causing production to be halted intermittently.FMC may seek to geographically diversify its

operations in an effort to reduce this risk.

• ROC's lithium operations in Chile are exposed

to a considerable amount of governmentregulatory risk. A geographical diversification of

operations could help to reduce risk from this

source.

• Argentina is perceived to have increased

political risk due to the recent expropriation ofRepsol's shares in oil and gas produced YPF.

This furthers the need for FMC to diversify

geographically.

• ROC is a well-capitalized company, having

recently raised $1.25 bn in senior notes.

• FMC recently announced a decision not to

expand further in Argentina. Therefore, the

Company will most likely be looking to grow itsmarket share through acquisitions.

• ROC's corporate headquarters are located on

the U.S. east coast in close proximity to CLQ.

• FMC comments at China conference suggest

it is currently considering a lithium acquisition.

Reasons that CLQ is an attractive acquisition target for EACH of these companies:

Reasons that CLQ is an attractive acquisition target for INDIVIDUAL companies:

For well-capitalized lithium producers such as SQM, ROC, and FMC, project development is seen as a r isky endeavour. These companies seek toadd low-risk sources of cash flow for investors. CLQ has an advanced stage hard rock lithium project that has been significantly de-risked and is a

near-term producer, presenting an attractive takeout candidate.

China's Tianqi has become an increased threat due to its larger market share following the pending Talison Lithium acquisition.

CLQ's Quebec operations are in a relatively safe geopolitical environment compared to each of the above companies' current lithium operations.

Lithium production from a hard rock resource, like that found at CLQ's project, is not impacted by climatic conditions, unlike brine projects that are.

Similarly, lithium production from hard rock resources is achieved significantly faster compared to brine resources.

The lithium segments of each of the above companies have strong fundamentals relative to other business segments the companies are involved inCapital utilization would therefore be optimized with further investment in the lithium space.

Source: Mackie Research Capital

7/29/2019 122782016 Lithium Fundamentals Remain Strong

http://slidepdf.com/reader/full/122782016-lithium-fundamentals-remain-strong 4/7

www.mackieresearch.com The MORNING CALL – Industry Update Pa

GROWTH IN ELECTRIC VEHICLES TO POWER LITHIUM DEMAND OVER THE NEXT DECADE

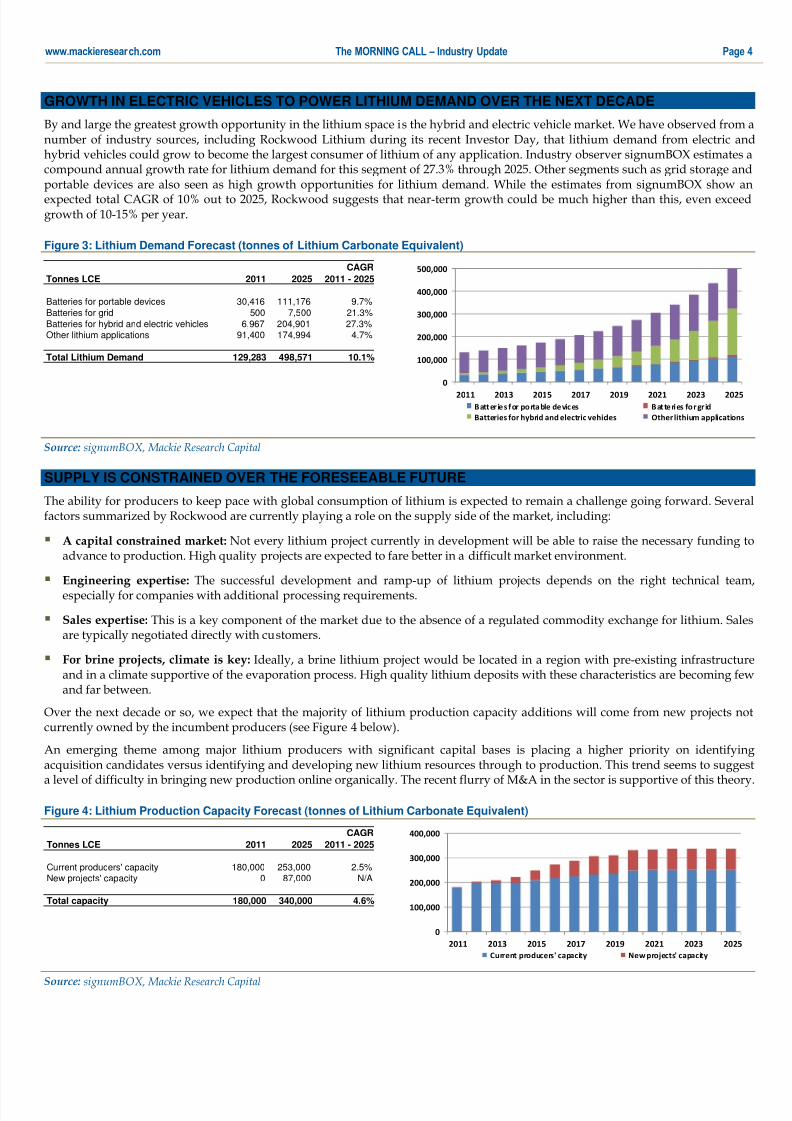

By and large the greatest growth opportunity in the lithium space is the hybrid and electric vehicle market. We have observed fronumber of industry sources, including Rockwood Lithium during its recent Investor Day, that lithium demand from electric ahybrid vehicles could grow to become the largest consumer of lithium of any application. Industry observer signumBOX estimatecompound annual growth rate for lithium demand for this segment of 27.3% through 2025. Other segments such as grid storage aportable devices are also seen as high growth opportunities for lithium demand. While the estimates from signumBOX show expected total CAGR of 10% out to 2025, Rockwood suggests that near-term growth could be much higher than this, even excegrowth of 10-15% per year.

Figure 3: Lithium Demand Forecast (tonnes of Lithium Carbonate Equivalent)

CAGR

Tonnes LCE 2011 2025 2011 - 2025

Batteries for portable devices 30,416 111,176 9.7%Batteries for grid 500 7,500 21.3%Batteries for hybrid and electric vehicles 6,967 204,901 27.3%Other lithium applications 91,400 174,994 4.7%

Total Lithium Demand 129,283 498,571 10.1%

0

100,000

200,000

300,000

400,000

500,000

2011 2013 2015 2017 2019 2021 2023 202

Batter ies for portable devices Batteries for gr id

Batteries for hybrid and electric vehicles Other lithium applicatio

Source: signumBOX, Mackie Research Capital

SUPPLY IS CONSTRAINED OVER THE FORESEEABLE FUTURE

The ability for producers to keep pace with global consumption of lithium is expected to remain a challenge going forward. Sevefactors summarized by Rockwood are currently playing a role on the supply side of the market, including:

A capital constrained market: Not every lithium project currently in development will be able to raise the necessary fundingadvance to production. High quality projects are expected to fare better in a difficult market environment.

Engineering expertise: The successful development and ramp-up of lithium projects depends on the right technical tea

especially for companies with additional processing requirements.

Sales expertise: This is a key component of the market due to the absence of a regulated commodity exchange for lithium. Saare typically negotiated directly with customers.

For brine projects, climate is key: Ideally, a brine lithium project would be located in a region with pre-existing infrastructand in a climate supportive of the evaporation process. High quality lithium deposits with these characteristics are becoming fand far between.

Over the next decade or so, we expect that the majority of lithium production capacity additions will come from new projects ncurrently owned by the incumbent producers (see Figure 4 below).

An emerging theme among major lithium producers with significant capital bases is placing a higher priority on identifyacquisition candidates versus identifying and developing new lithium resources through to production. This trend seems to sugga level of difficulty in bringing new production online organically. The recent flurry of M&A in the sector is supportive of this theo

Figure 4: Lithium Production Capacity Forecast (tonnes of Lithium Carbonate Equivalent)

CAGR

Tonnes LCE 2011 2025 2011 - 2025

Current producers' capacity 180,000 253,000 2.5%New projects' capacity 0 87,000 N/A

Total capacity 180,000 340,000 4.6%

0

100,000

200,000

300,000

400,000

2011 2013 2015 2017 2019 2021 2023 202

Current producers' capacity New projects' capacity

Source: signumBOX, Mackie Research Capital

7/29/2019 122782016 Lithium Fundamentals Remain Strong

http://slidepdf.com/reader/full/122782016-lithium-fundamentals-remain-strong 5/7

www.mackieresearch.com The MORNING CALL – Industry Update Pa

A real risk of severe under-supply in the lithium market: Figure 5 below illustrates forecasted global consumption verproduction capacity. Actual lithium production is a function of production capacity and utilization rate. In order for supply ademand to be balanced from 2011 to 2020 using signumBOX’s forecasts, capacity utilization will need to average 73% over the ndecade. On review of the Figure below, there is a chance that the lithium market may remain balanced for the next six to seven yeBeyond that however, this a real risk of a severely undersupplied market.

Figure 5: Lithium Supply & Demand Forecast (tonnes of Lithium Carbonate Equivalent)

0

100,000

200,000

300,000

400,000

500,000

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Producers' capacity Total demand Source: signumBOX, Mackie Research Capital

7/29/2019 122782016 Lithium Fundamentals Remain Strong

http://slidepdf.com/reader/full/122782016-lithium-fundamentals-remain-strong 6/7

www.mackieresearch.com The MORNING CALL – Industry Update Pa

HEALTHY PRODUCER MARGINS; LITHIUM PRICING OUTLOOK IS STABLE

Our “flat” lithium price deck may prove conservative considering recent momentum and comments from the majors: Seveincumbent producers have announced significant price increases for lithium products, including Talison Lithium which on Janu15th announced a 10-15% price increase for its technical-grade and chemical-grade lithium concentrates. We anticipate lithium prito remain stable going forward, which should translate to healthy margins for incumbent producers. Developers such as Cana

Lithium are using price assumptions below current market levels in their economic models, which could provide further upsiderobust project economics. At Rockwood’s investor day, it indicated an expectation for significant price gains in lithium hydroxand other exotic lithium compounds, while lithium carbonate pricing may be more “stable” due to the considerable pricing gahaving been achieved over the recent past.

Figure 6: Mackie Research Capital Price Forecast for Lithium

US$/tonne 2010A 2011A 2012A 2013E 2014E 2015E

Battery grade lithium carbonate price $5,184 $5,095 $6,241 $6,500 $6,500 $6,500

Battery grade lithium hydroxide price $7,750 $7,750 $8,500 $8,500 $8,500 $8,500

Lithium concentrate price $309 $311 $353 $375 $375 $375

4,000

4,500

5,000

5,500

6,000

6,500

7,000

7,500

8,000

8,500

9,000

9,500

2008 2009 2010 2011 2012 2013

Battery Grade Lithium Carbonate Price(in USD/MT; Source: Asian Metal)

Low High

Note: Historical price for lithium concentrate is based on Talison Lithium’s sales of technical-grade and chemical-grade lithium concentrates. Histor

price for lithium hydroxide is based on reports from Nemaska Lithium.

Source: Asian Metal, Talison Lithium, Nemaska Lithium, Mackie Research Capital

7/29/2019 122782016 Lithium Fundamentals Remain Strong

http://slidepdf.com/reader/full/122782016-lithium-fundamentals-remain-strong 7/7

www.mackieresearch.com The MORNING CALL – Industry Update Pa

RISKS TO TARGET

Canada Lithium Corp.

The company is subject to class action law suit risk, commodity price risk, risks pertaining to oversupply and substitution of lithproducts, construction risk, and financing risk as well the conventional risks associated with mining companies.

Lithium Americas Corp. The company is subject to geopolitical risk, commodity price risk, scaling risk of the process, financing risk as well the conventioexploration and development risks associated with mining companies. In terms of financing risk, the Company’s development care far greater than its current resources, and thus the Company would consider raising equity in the near future. Lithium Amercurrently has $11.5 million in cash, and zero debt. A $10 million stand-by credit facility is available from two of the Companlargest shareholders.

Nemaska Lithium Inc.

The company is subject to class action law suit risk, commodity price risk, risks pertaining to oversupply and substitution of lithproducts, construction risk, and financing risk as well the conventional risks associated with mining companies.

RELEVANT DISCLOSURES APPLICABLE TO:

Canada Lithium Corp.

1. Matt Gowing visited the operations of Canada Lithium Corp. on November 29, 2011. A chartered flight from TorontoVal D’Or, Quebec, and all transportation costs to the site were paid for by Canada Lithium Corp.

Lithium Americas Corp.

1. In January 2012, Matt Gowing visited Lithium Americas Cauchari-Olaroz site. All reasonable expenses for the trip wpaid by Mackie Research Capital Corporation.

Nemaska Lithium Corp.

1. On Thursday, June 14, Matt Gowing attended a site tour hosted by Nemaska Lithium. Transportation costs includinchartered flight from Toronto to the site were paid for by Nemaska.

ANALYST CERTIFICATION

Each analyst of Mackie Research Capital Corporation whose name appears in this report hereby certifies that (i) recommendations and opinions expressed in this research report accurately reflect the analyst’s personal views and (ii) no parthe research analyst’s compensation was or will be directly or indirectly related to the specific conclusions or recommendatiexpressed in this research report.

nformat ion about Mackie Research Capi tal Corporat ion’s Rat ing System, the dist r ibut ion of our research to cl ients and the percentage of recommendawhich are in each of our ra t ing categories is avai lable on our web si te at www.mackieresearch.com.

The informat ion contained in th is report has been drawn f rom sources bel ieved to be rel iable but i ts accuracy or completeness is not guaranteed, nproviding i t does Mackie Research Capi tal Corporat ion assume any responsibi l i ty or l iabi l i ty. Mackie Research Capi tal Corporat ion, i ts di rectors, of f icersother employees may, f rom t ime to t ime, have posi t ions in the securi t ies ment ioned herein. Contents of th is report cannot be reproduced in whole or inwi thout the express permission of Mackie Research Capi tal Corporat ion. (US Inst i tut ional Cl ients - Mackie Research USA Inc. , a whol ly owned subsidiaMackie Research Capi tal Corporat ion, accepts responsibi l i ty for the contents of th is report subject to the terms and l imi tat ions set out above. US f i rnst i tut ions receiving this report should ef fect t ransact ions in securi t ies discussed in the report through Mackie Research USA Inc. , a Broker-Dealer regis

wi th the Financial Indust ry Regulatory Author i ty (FINRA)).

Toronto 416.860.7600 - Montreal 514.399.1500 - Vancouver 604.662.1800 - Calgary 403.218.6375 - Regina 306.566.7550 - St. Albert 780.460.6460