Embed Size (px)

Citation preview

Koji Ueda (Nomura)Nazri Omar (KFH Malaysia)Qudeer Latif (Clifford Chance Dubai)Reiko Sakimura (Clifford Chance Tokyo)

Nomura Sukuk-al-IjaraCase Study

Tokyo (8 December 2010)

1

Introduction Nomura’s Perspective KFH’s Perspective and Shari’a Process Islamic Structural and Legal Issues Capital Markets Issues

I – Background and Challenges (Nomura’s Perspective)

Koji Ueda

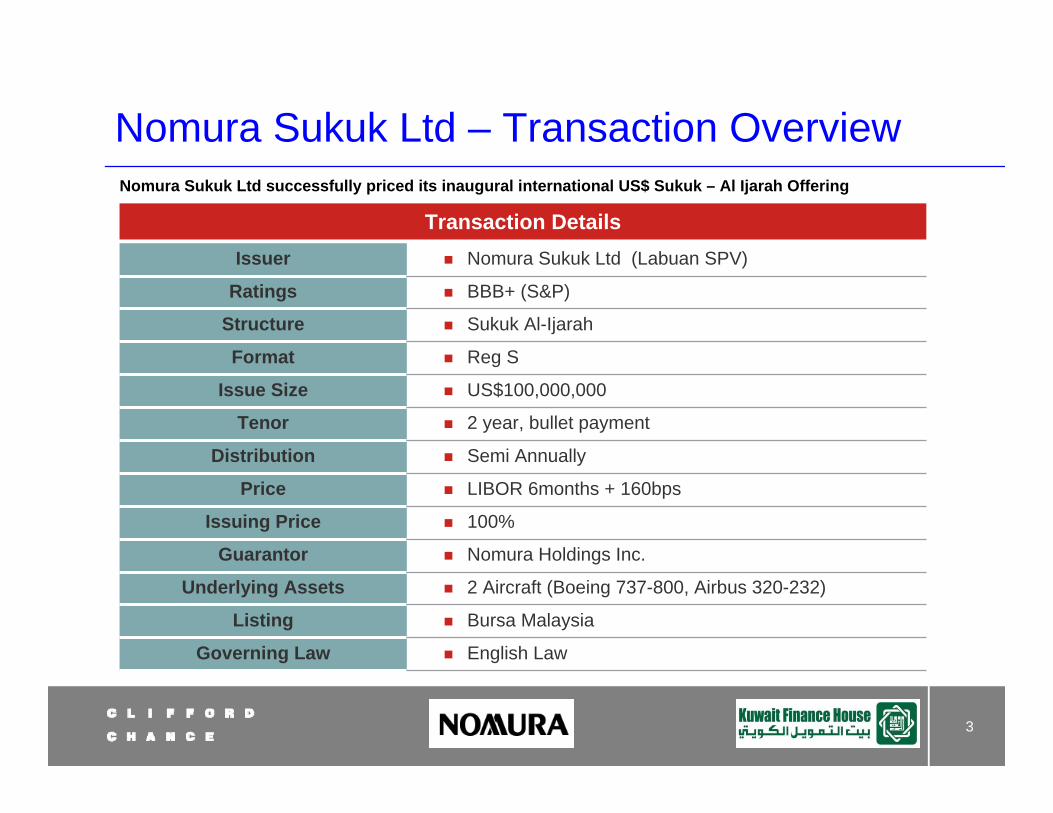

Nomura Sukuk Ltd – Transaction Overview

3

Transaction DetailsIssuer Nomura Sukuk Ltd (Labuan SPV)

Ratings BBB+ (S&P)

Structure Sukuk Al-Ijarah

Format Reg S

Issue Size US$100,000,000

Tenor 2 year, bullet payment

Distribution Semi Annually

Price LIBOR 6months + 160bps

Issuing Price 100%

Guarantor Nomura Holdings Inc.

Underlying Assets 2 Aircraft (Boeing 737-800, Airbus 320-232)

Listing Bursa Malaysia

Governing Law English Law

Nomura Sukuk Ltd successfully priced its inaugural international US$ Sukuk – Al Ijarah Offering

4

A Highly Flexible Shari’a-compliant Structure

* NBB : Lease Arrangement company which specializes in the international leasing of large equipment in Nomura Group

Funding

The underlying physical assets for the sukuk were 2 aircraft, and the transaction involved transfer of legal ownership to the Sukuk issuer

This more strictly follows Shari’a guidelines, compared with many other Sukuk Al Ijarah issuances, which usually apply a transfer of Beneficial Ownership

The structure satisfies the more stringent Shari’a requirements of Middle Eastern investor and opens the way for Nomura to tap Middle East as well as Asian Islamic investors

SPV 2(Orphan Trust)

Airline

NHINBB*

Islamic Market

SPV 1

Guarantee (SPV1’s Obligation)

100% Owner

100% Owner

Sale andLease-back

LeasePayment Sukuk

IssuanceInvestment in Sukuk

Agent Agreement

OriginalOwner SPV

Nomura Group Funding

Company

100% Funding(LOAN)

OriginalLease

Contract

Aircraft Sales

Operational Lease

Novation

Sukuk Related

Aircraft Related Flow & Contracts

Capital Relation

Funding Source (Repaid with Sukuk Funding)

5

Client Accessibility to Sukuk Al-IjarahThe order book was closed within 24 hours. With strong demands after close book, we realized secondary allocation by end of August

Final Secondary Allocation August 20101st Close Allocation July 2010

6

Transaction TimelineNomura drove all aspects of the transaction, from start to finish, and allowed Nomura Holdings Inc to complete issuance of its first Islamic issuance within a 12 week execution period.

Sukuk Timeline Underlying Asset Timeline

1st week Fixing Financing Scheme Underlying Asset DD

3rd week Documentation Start (till 11th week)

4th week Establishment of issuer SPV Establishment of Lessor SPV

8th week Lease License for Lessor SPV

10th week DD Meeting, Prospectus Circulation

11th week Price Fixing, Subscription Agreement Finalize title transference execution

12th week Closing / Settlement Legal Title Transfer

Transaction Timeline

Strong demand from Islamic investors for non-Islamic issuers, and for foreign currency (USD) Sukuk issuance. The structure allowed the issuance to be rated the same as a conventional Nomura Holdings issuance and so generated further

investor interest and pricing tension. The Nomura team, working closely with an Islamic bank (Kuwait Finance House) was a successful combination in realizing an

innovative structure which generated very strong demand from Islamic and non-Islamic investors. The Nomura now has proven structuring and execution capabilities to advise non-Islamic corporate clients on Shari’a-compliance

issuance.

Key Takeaways

II – Arranger’s Perspective and Shari’a Process

Nazri Omar

8

Investor/Issuer/Shari’a Key Requirements

Shari’a•Permissible asset

•Permissible business income

•Key Lease Terms

Issuer•Pricing competitiveness

•No impact from Tax/Accounting/business operations

Investor•Similar features to fixed income and tradeable

•Rating – certainty and timeliness of payments

Objective:to balance the requirements of all 3

stakeholders

9

Shari’a Key Requirements (1)Key Parameters Description• Permissible asset (for

tradeability of Nomura Sukuk Ijarah)

• Completed and clearly identified asset by both parties

• Tangible or intangible assets (that can be independently valued)

• Non-perishable (durable) or consumable

• Issuer has a clearly defined right of use over the asset

• Permissible business income

• Asset is used to generate Shari’a compliant business income, to avoid

• Restricted Food and beverage (ie Alchohol)

• Speculative/gambling related

• Media/Entertainment• Interest bearing activities

Nomura Case• Asset is a completed aircraft

• Legal ownership by Issuer/SPV

• Business income generated from aircraft leasing

10

Shari’a Key Requirements (2)Key Parameters Description• Lease Rental (for

Nomura Sukuk Ijarah)

• Determined at the time of contract

• Rental charged when Asset is handed over to the lessee

• Different rent can be fixed for different phases, provided amount/formula is agreed upon at the time of affecting a lease

• Lessor cannot increase the rent unilaterally

• No rental if no usufruct/right of use

• Lease Period • Period of lease must be determined in clear terms at the time of contract

• Responsibility of lessor

• bears and assumes the full risk of the leased asset

• liable to pay all expenses incurred with respect to asset

Nomura Case• Rental formula determined upfront

to cater for floating rate mechanism

• 2 year tenor for lease

• Insurance to cover total loss

• Appointment of lessee as Servicing Agent - expenses offset by lease formula

11

Investor/Issuer Key RequirementsKey Parameters Description• For Investor - Fixed

Income features• Defined tenor, with periodic

coupons, bullet maturity, and tradeable

• Rating – certainty and timeliness of payments

Nomura Case• Sukuk achieved requirements with the

following:

• Periodic coupons incorporated into lease payment

• Purchase/Sale undertaking to cater for Principal on maturity

• Rating of BBB+ with NHI guarantee on Obligor’s obligations under transaction

12

Issuer Key RequirementsKey Parameters Description• For Issuer - • Pricing competitiveness –

comparable to conventional benchmark

• No impact from Tax/Accounting/business operations – ie no different than conventional bonds

Nomura Case• Achieved - Commercial Terms and

Conditions and Credit Risk comparable to NHI’s Bonds

• Sale Transfer from SPV1 to SPV2 and leaseback (done in Labuan, an International Business & Financial Centre (IBFC)) – viewed as a financing transaction, achieved tax neutrality

• SPV1 lease payments to SPV2 viewed as substitute to interest payments by tax/accounting

• SPV1 operates as an Operating Lease company

III – Shari’a and Legal Structure and Challenges

Qudeer Latif

14

Nomura Sukuk Structure

15

Nomura Sukuk I

US$100 million Sukuk Certificates Ijara

Shari’a compliant lease Lease rental payments “mirror” the profit payments under

the Sukuk Certificates Obligation to undertake major maintenance of leased asset

remains with lessor (SPV) Obligation to insure the leased asset remains with the

lessor (SPV) Obligation to pay any ownership taxes remains with the

lessor (SPV)

16

Nomura Sukuk II

Service Agency Agreement Lessor appoints an agent (usually the lessee ) to carry out

servicing duties pursuant to a servicing agreement Recovery of Services Agency Costs?

Acceleration of debt? Sale & Purchase Undertakings

Asset based v Asset backed What risk are investors taking?

17

Islamic Documentation

Sale and Purchase Agreement Lease Agreement Service Agency Agreement Purchase Undertaking Sale Undertaking Substitution Undertaking Replacement Undertaking Guarantee Deed

18

Ijara Sukuk - Important Considerations

Size of Sukuk issuance is restricted by the value of the assets transferred to the Lessee

Once the assets have been transferred for the purposes of a Sukuk issue, they cannot be used for any other purpose until the Sukuk issue has matured

IV – Capital Market Issues

Reiko Sakimura

20

Differences from Conventional Bonds (1)

Parties and Terms

Conventional Bonds SukukIssuer TrusteeTrustee (if any) DelegateGuarantor guarantees payment to investors

Guarantor guarantees payment to Trustee

Bonds Trust CertificatesInterest Periodic DistributionsRedemption Payment Dissolution DistributionEvents of Default Dissolution Events

21

Differences from Conventional Bonds (2)

Nomura Subsidiary

(Issuer)

Bond-holders

Promise to pay (if it had been a trust deed structure, covenant to pay would be held on trust by the trustee for the benefit of the Bondholders)

Nomura Holdings

Guarantee

Certificate-holders

Lease and undertakings held on trust for Certificateholders

NBB Ijarah Ltd

Nomura Holdings

Lease

Purchase etc. undertakings

Guarantee

Trust Assets

Delegate

Powers vested in Delegate

Nomura Sukuk Ltd (Trustee)

Nomura MTN Nomura Sukuk

22

Delegate

Enforcement Delegate can sue obligor (whether it be NBB Ijarah or

Nomura Holdings) in the name of the Trustee for unpaid amounts

– Note: no recourse to aircraft assets

Locus standi of Delegate: attorney of Trustee

Powers vested in the Delegate Convening meetings Determination of Dissolution Event Amendments, waivers etc. Delegate = attorney BUT does not hold trust assets “on

trust”

23

Similarities with Conventional Bonds (1)

Disclosure Ultimate credit = Nomura Holdings Offering Circular

disclosure Due diligence: corporate and asset Auditors’ comfort letters

Terms and Conditions Nomura Holdings’ negative pledge Dissolution Events related to Nomura Holdings

– Cross Default threshold– Grace periods– Bankruptcy/insolvency etc. events

24

Similarities with Conventional Bonds (2)

Subscription and sale Subscription Agreement

Periodic / “principal” payments to investors Agency Agreement

Clearing Euroclear and Clearstream, Luxembourg

Questions & Answers

Speakers’ contact details:Koji Ueda (Nomura, Singapore)+65 6433 [email protected]

Nazri Omar (Director, KFH Malaysia)+603 2055 [email protected]

Qudeer Latif (Partner/Head of Islamic Finance)+971 4 362 0675 [email protected]

Reiko Sakimura (Partner)+81 3 5561 [email protected]

Clifford Chance, 3rd Floor, The Exchange Building, Dubai International Financial Centre, PO Box 9380, Dubai, United Arab Emirates© Clifford Chance LLP 2006Clifford Chance Limited Liability PartnershipDoc Dubai library – 163794

Nomura Sukuk-al-Ijara