Embed Size (px)

Citation preview

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

College Accounting

11th Edition

The General Journal and

the General Ledger

ch

apte

r

3

3–1

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Learning Objectives

3–2

After you have completed this chapter, you

will be able to do the following:

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

• The process of recording business transactions in a journal is

called journalizing.

• In the journal, both the debits and the credits of the entire

transaction are recorded in one place.

• A journal is called a book of original entry because the first place

an entry is recorded is in the journal.

• A journal is a book in which business transactions are recorded as

they happen.

• Information about transactions come from source documents that

furnish proof that a transaction has taken place.

• The basic journal form is the two-column general journal.

The General Journal

3–3

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Transaction (a) – June1: J. Conner deposited

$90,000 in a bank account in the name of Conner’s

Whitewater Adventures.

3–4

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Step 1: Decide which accounts are involved.

Step 2: Classify the accounts involved.

Step 3: Decide if the accounts involved are increased

or decreased.

Step 4: Write the transactions as a debit to one account

(or accounts) and a credit to another account (or

accounts).

Step 5: Check to see if the equation is in balance.

Decide which accounts should be debited

and credited

3–5

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Analyze the Transaction Using the

T- Account Approach

i

n

c

r

e

a

s

e

3–6

Cash

increases, so

it is debited

i

n

c

r

e

a

s

e

J. Conner,

Capital

increases, so

it is credited

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Journal Entry

3–7

1: Page number 2: Date 3: Debit account title

3: Debit amount

4: Indent credit

account title

4: Credit amount

5: Indent further

explanation

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Transaction (b) – June 2: Conner’s Whitewater

Adventures bought equipment, paying cash, $38,000.

3–8

Skip a line between

entries in your homework

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

• When a business buys an asset, the asset should be

recorded at the actual cost (the agreed amount of a

transaction).

• This is called the cost principle.

• Assume in Transaction (c) that Signal Products had

been asking $7,500 for the equipment.

• The cost of the equipment to Conner’s Whitewater

Adventures is $4,320, so that is the amount recorded.

The Cost Principle

3–9

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Transaction (c) – June 3: Conner’s Whitewater

Adventures bought equipment on account from Signal

Products, $4,320.

3–10

Note that the month and year are not

repeated unless they change or a new

journal page begins

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Transaction (d) – June 4: Conner’s Whitewater

Adventures paid Signal Products, a creditor, on

account,$2,000.

3–11

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

3–12

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

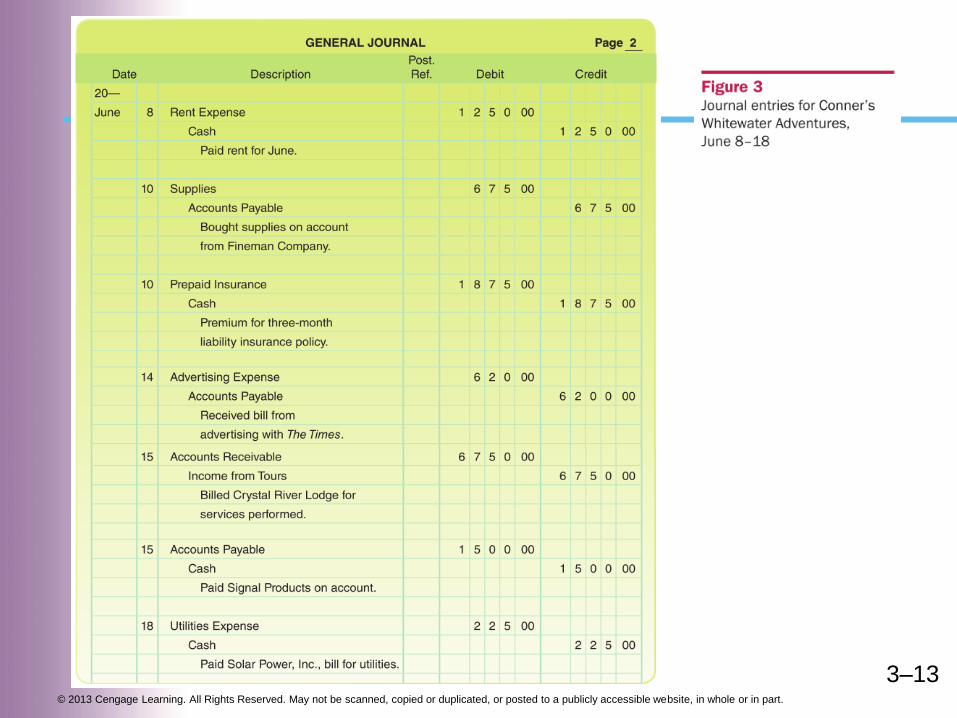

3–13

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

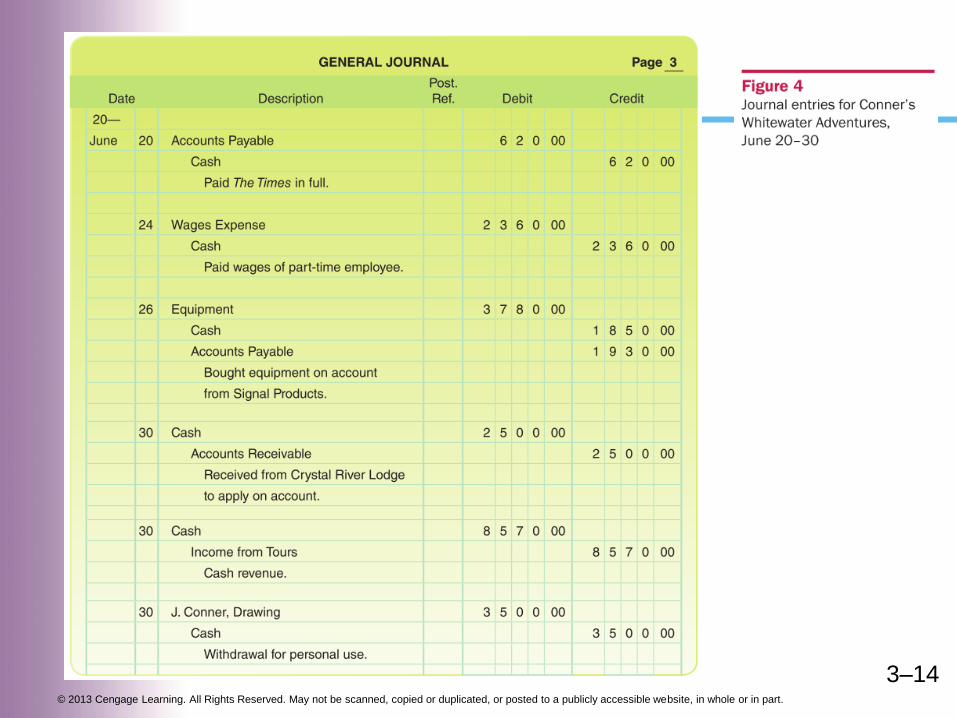

3–14

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

• The journal is the book of original entry because

each transaction must first be recorded in full in

the journal.

• The ledger account gives us a complete record of

the transactions recorded in each individual

account.

• The general ledger contains all the accounts.

• The process of transferring information from the

journal to the ledger is called posting.

Posting to the General Ledger

3–15

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

3–16

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

3–17

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

STEP 1. Write the date of the transaction in the account’s

Date column.

STEP 2. Write the amount of the transaction in the Debit

or Credit column, and enter the balance in the

Balance column under Debit or Credit.

STEP 3. Write the page number of the journal in the Post.

Ref. column of the ledger account. (This is a

cross-reference; it tells you where the amount

came from.)

STEP 4. Record the ledger account number in the Post. Ref.

column of the journal.

The Posting Process

3–18

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

3–19

Date of transaction

Amount of transaction

Page number of the journal

Ledger account number

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

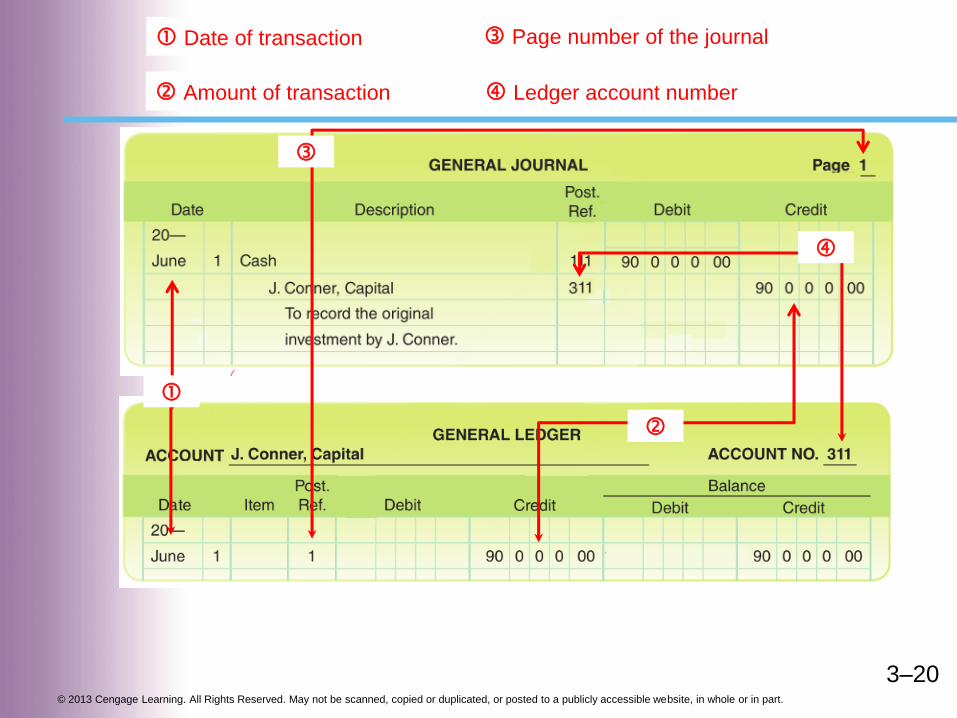

3–20

Date of transaction

Amount of transaction

Page number of the journal

Ledger account number

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

3–21

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Preparation of the Trial Balance

• The trial balance is

simply a list of accounts

that have balances.

• Even when the debit and

credit balances are equal,

other types of errors may

slip through—for

example,

1. Posting the correct debit

or credit amounts to the

incorrect account.

2. Neglecting to journalize

or post an entire

transaction.

3–27

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

3–28

STEP 1. Record the transaction of a business in a journal.

STEP 2. Post entries to the accounts in the ledger.

STEP 3. Prepare a trial balance.

Steps in the Accounting Process

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

3–29

Source Documents

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

3–30

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Manual Ruling Method

3–31

Manual Correcting Errors

Before Posting Has Taken

Place

An entry to record payment of $1,500 rent was

incorrectly debited to Salary Expense.

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Manual Ruling Method

3–32

An entry for $120 payment for office supplies was

recorded as $210.

Manual Correcting Errors Before

Posting Has Taken Place

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Manual Ruling Method

3–33

Manual Correcting Errors After

Posting Has Taken Place

An entry to record cash received for professional

fees was correctly journalized as $400. However, it

was posted as a debit to Cash and a credit to

Professional Fees for $4,000.

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

The correcting entry method

is used when incorrectly

journalized amounts have

been posted. There are two

correcting entry methods.

One-step method. Simply

make one entry that undoes

the error and provides the

correct account.

Two-step method. The first

step reverses the error made

by the original entry. The

second step includes the

correct entry.

Correcting Entry Method — Manual or Computerized

3–34

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

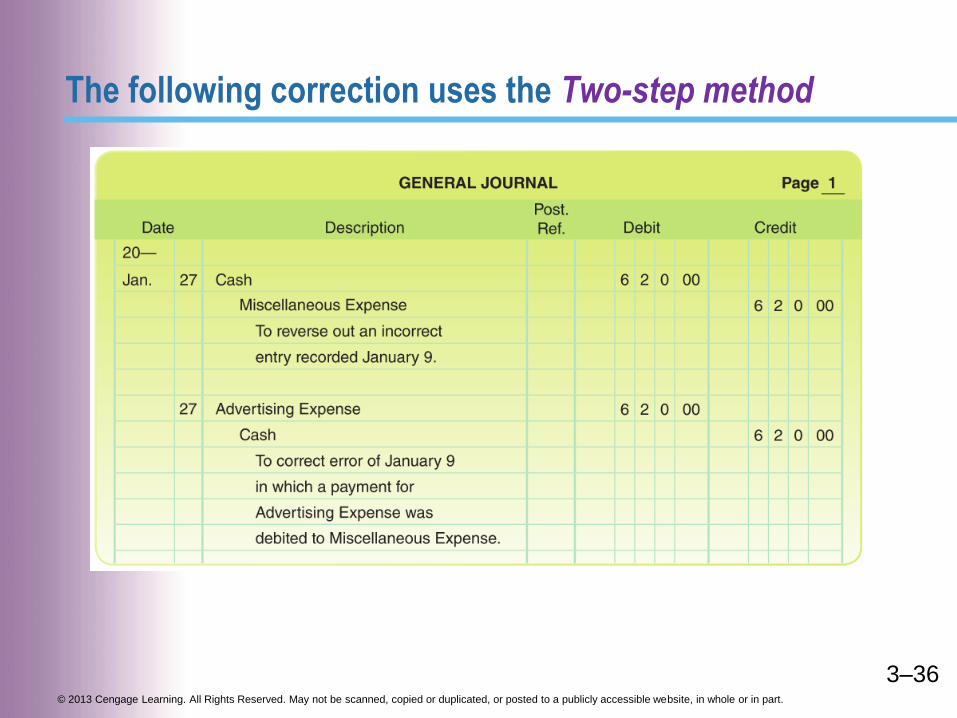

Transaction (Jan. 9) : A $620 payment for advertising was

incorrectly journalized and posted as a debit to Miscellaneous

Expense and a credit to Cash for $620. The error was discovered

on January 27. The following correction uses the one-step

method:

3–35

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

The following correction uses the Two-step method

3–36