Embed Size (px)

Citation preview

5 October 2021

Trustee Training

Hogan Lovells Pensions Team

Katie BanksPartner, London Pensions

Why are we here?

Hogan Lovells | 3

• tPR: body corporate established under ss 1-3 Pensions Act 2004

• Objectives:

• Protect members' benefits

• Reduce risk of PPF compensation being payable

• Promote understanding/good administration of work-based pension schemes

• Maximise compliance with employer duties, including auto-enrolment

• Employer sustainable growth

Trustee knowledge and understanding

Hogan Lovells | 4

• Sections 247 – 249 of the Pensions Act 2004 plus Regulator Code of Practice and guidance

• "Appropriate" knowledge and understanding of law relating to pensions and trusts

• Necessary to exercise properly the role

• Working knowledge of scheme documents:

• Trust deed and rules

• Subsequent amendments

• Scheme booklet

• Statement of investment principles

• Statement of funding principles

• Keep up to date

Trustee knowledge and understanding

Hogan Lovells | 5

• tPR identified poor governance in many small and medium size schemes

• Intends to drive up standards

• Tougher enforcement

• Clarifying expectations

• Encouraging consolidation

• Campaign launched 2017

• Specific content setting out clear standards

• Case studies on enforcement

• Tools for checking own scheme’s progress

21st Century Trusteeship

Hogan Lovells | 6

• This session is the start of the process

• Remainder of the day will add more detail

• Welcome to The Trustee toolkit (thepensionsregulator.gov.uk)

Trustee knowledge and understanding

Some basics – trusts and trustees

Hogan Lovells | 8

Basic structure of a trust

Knight(Settlor)

Best friend(Trustee)

Castle(Trust Asset)

Wife & Children(Beneficiaries)

Hogan Lovells | 9

Structure of a pension trust

Trustee

Trust fund

Employees

EmployerInvestment return

Leaver Pensioner

Transfer Beneficiaries

Ownership

Contributions

Hogan Lovells | 10

• Security

• Rights of action

• Statutory requirement

Why a trust?

Hogan Lovells | 11

Individuals as trustees

Trustee 2Trustee 1 Trustee 3

Trust fund

Deeds of Appointment/RetirementEach person is a trustee

Hogan Lovells | 12

Directors of a trust company

Director 2Director 1 Director 3

Trustee company

Trust fund

Appointed as a director form at Companies House

Memorandum and Articles of Associations

Trustee Company is the sole trustee

Hogan Lovells | 13

• Member nominated trustee/director requirements

• One third member nominated

• Nomination process and selection process

• Fit and proper person

• Ask for copies of scheme documents

• Ask for confidentiality agreements

• Ask for recent minutes

• Ask for conflicts of interest policy

• Bank mandates

• Removal, retirement of trustees

Appointment and removal of trustees and trustee directors

Hogan Lovells | 14

Pensions legal framework

Trust lawPensions

lawTax

Employment law

Trustee Acts 1925/2000Case law – fiduciary duties

PLUS• Company• Investment• Retained European law• Social security• Divorce/civil partners

Pensions Schemes Act 1993Pensions Act 1995Pensions Act 2003Pensions Act 2008Pensions Schemes Act 2015Pensions Schemes Act 2017Pensions Schemes Act 2021Associated RegulationsCase law

Finance Act 2004Income Tax (Earnings and Pensions) Act 2003 (ITEPA)Associated RegulationsHMRC Technical Manuals

TUPE transfersDiscriminationConsultation

Hogan Lovells | 15

What is "legislation"?

Written laws, not court decisions

The Pensions Act 2004

The OccupationalPensions Schemes (Scheme Funding) Regulations 2005

Passed in Parliament

High-level principles

“Statute”

Made by a Minister

Technical details

Usually “Regulations” or “Orders”

Hogan Lovells | 16

• Pension Schemes Act 1993

• Welfare Reform and Pensions Act 1999

• Pensions Act 1995

• Pensions Act 2004

• Finance Act 2004

• Pensions Act 2008

• Pension Schemes Act 2015

• Pension Schemes Act 2017

• Pension Schemes Act 2021

The main statutes

Hogan Lovells | 17

• To operate their scheme in accordance with its trust deed and rules and the law to ensure that the correct benefits are paid to beneficiaries at the right time

• Trustees have powers to act

• Trustees owe duties when acting

• Manage conflict of interest

Role of the trustees

Hogan Lovells | 18

The four main conflicts of trustees

Trustee

Director of employer

Member of scheme

Employee

Hogan Lovells | 19

• Set down how the trustees should exercise their powers – ie what they must do

• Mainly case law (but now Pensions Acts)

• Impose a strict code of conduct on trustees

• tPR codes and guidance

Trustees' duties

Hogan Lovells | 20

• Comply with the trust deed and rules

• Act in the interests of the beneficiaries

• Balance the interests of beneficiaries

• Act prudently, conscientiously and honestly

• Not to make a profit from the trust

• Take advice where necessary

The main trustee duties

Hogan Lovells | 21

• Know your trust deed and rules

• Know formalities required for valid decision making

• Have the trust deed or rules been amended?

• Status of announcements to members

• Overriding legislation

• Interpretation

• Take advice

Comply with the trust deed and rules

Hogan Lovells | 22

• Payment of lump sum – £140,000

• Divorced, two adult children and Ms Slack

• Power to pay anyone "financially dependent" and to "relatives“

• Decision (Ombudsman and High Court)

The Wild case

Hogan Lovells | 23

Trustees must:

• Ask themselves the correct questions

• Direct themselves correctly in law (adopt the correct construction of the Rules)

• Not arrive at a perverse decision which no reasonable set of trustees would arrive at and

• Take into account all relevant – but no irrelevant – factors

Exercise of a discretionary power

Hogan Lovells | 24

Who are the beneficiaries?

• Active members

• Pensioners

• Deferred members

• Survivors

• Employer?

Act in the interests of the beneficiaries

Hogan Lovells | 25

• Does not mean treating each class the same

• Must however consider each class

• Appreciate conflicts will exist

Balance the interests of beneficiaries

Hogan Lovells | 26

• Reflects fiduciary nature of trustee

• An ordinary prudent business person

• Special skills

Act prudently, conscientiously and honestly

Hogan Lovells | 27

• Give time freely

• Do not buy or sell assets from or to the trust

• Member trustees – conflicts of interest?

Not to make a profit from the trust

| 28Hogan Lovells

• Not expected to know everything

• Specialist advisers

• Actuary

• Auditor

• Lawyer

• Investment advice

• Covenant adviser

Take advice where necessary

Hogan Lovells | 29

The buck stops with you

• Liable for breaches of trust

• Liable for breaches of legislation

• Liable for “maladministration”

Liability

| 30Hogan Lovells

Protected by:

• Exclusion clause

• Indemnity from assets of scheme (care)

• Indemnity from employer

• Trustee liability insurance

• For corporate trustees, the "corporate veil"

But …

Hogan Lovells | 31

• Comply with your powers and duties

• Take responsibility for your scheme and for decision making

• Take professional advice

• Ensure sound administration processes

• Scheme governance review

• Ask questions

Practical ways to avoid liability

Hogan Lovells | 32

• What is money laundering?

• Proceeds of Crime Act 2002

• Criminal property and terrorist financing

• Criminal offences

• Dealing with criminal property

• Failing to report ("regulated sector")

• Tipping off

• Trustees of registered pensions scheme exempt from additional registration requirement

Money laundering

Hogan Lovells | 33

• Money Laundering, Terrorist Financing and Transfer of Funds (Information on the Payer) Regulations 2017 in force 26 June 2017 (amended January 2020 to comply with the Fifth Money Laundering Directive)

• Keep records of beneficial owners

• Notify 3rd parties of status of trustee and scheme's beneficial owners

• May need to give information to HMRC

• Failure to comply is a criminal offence

Money laundering

Hogan Lovells | 34

• Guidance for members

• ScamSmart website

• Guidance for trustees on tPR website

• http://www.thepensionsregulator.gov.uk/trustees/pension-scams-trustees.aspx

• Mr N – the Police Pension Scheme (PO-12763)

• Northumbria Police Authority ordered to reinstate member's accrued benefits, totalling £135,400 plus £1,000 in damages for distress

Pension scams

Katie BanksPartner, London Pensions

Why are we here?

Rebecca HowardCounsel, London Pensions

Member lifecycle 1 Joining the scheme

Hogan Lovells | 37

The Downton Abbey Pension Scheme

Hogan Lovells | 38

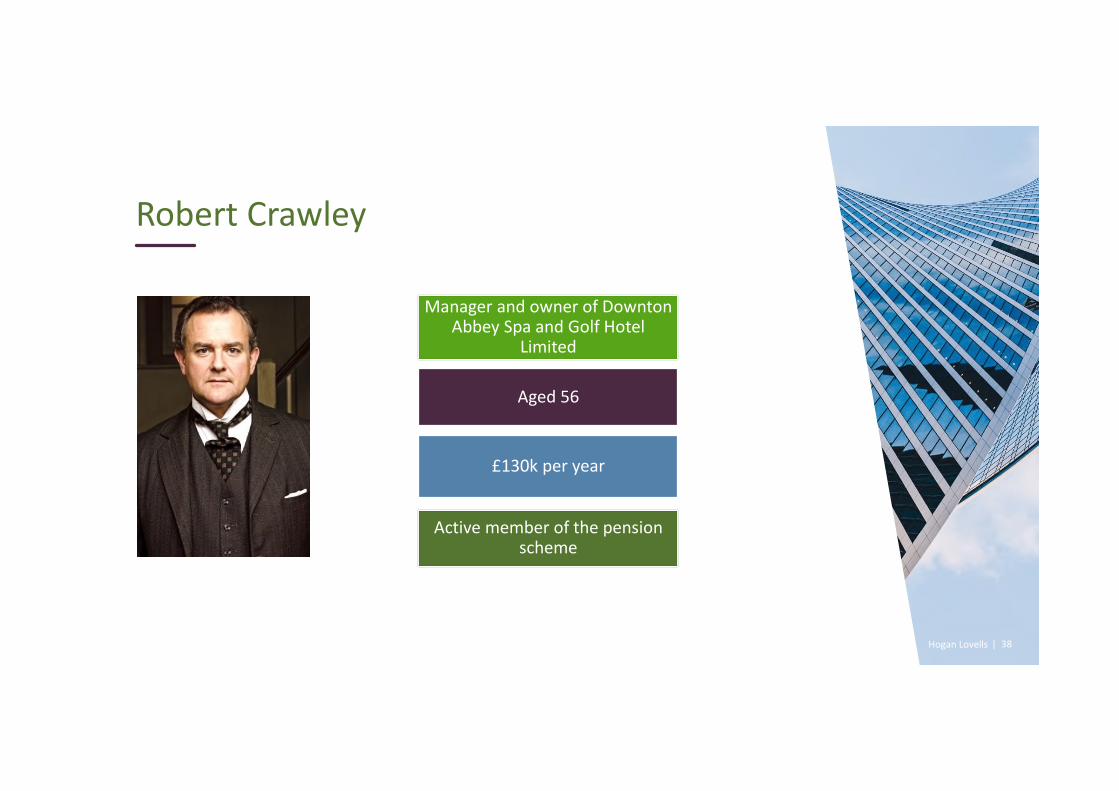

Robert Crawley

Manager and owner of Downton Abbey Spa and Golf Hotel

Limited

Aged 56

£130k per year

Active member of the pension scheme

Hogan Lovells | 39

Tom Branson

Golf cart supervisor

£20k per year

Active member of the pension

scheme

Hogan Lovells | 40

Charles Carson

Manager of sister company Downton Services Limited

£42k per year

Active member of the pension scheme

Hogan Lovells | 41

John Bates

Assistant in golf clothing shop

Aged 56

£12k per year

Not a member of the pension scheme; keeps his money under his mattress

Hogan Lovells | 42

Daisy Mason

Tea maid in cafe Aged 19

£12k per yearNot a member of

the pension scheme

Hogan Lovells | 43

Anna Bates

Stylist in spa beauty salon

Aged 41

£20k per year

Active member of the pension scheme

Hogan Lovells | 44

• Why?

• Demographic timebomb

• Widespread undersaving

• Voluntary saving has not worked

• Phased in

• Each employer has a ‘Staging Date’

• Began in October 2012

Auto-enrolment – introduction

Hogan Lovells | 45

What is auto-enrolment?

All "eligible jobholders" not in a Qualifying Scheme must be auto-enrolled

a "Worker"

between age 22 and state pension age

earning at least £10k per annum

• Worker can opt out

• Re-enrolment every 3 years

• Government relying on effects of inertia

Hogan Lovells | 46

• John Bates

• Earns more than £10k pa and is between age 22 and state pension age

• Must be auto-enrolled

• Daisy Mason

• Earns more than £10k pa but is under age 22

• Need not be auto-enrolled

Who does Downton Abbey need to auto-enrol?

Hogan Lovells | 47

• The Occupational and Personal Pension Schemes (Disclosure of Information) Regulations 2013

• Trustees must provide information to members, prospective members and other beneficiaries

• Some information as a matter of course

• Basic information

• Annual benefit statement (DC)

• Summary funding statement (DB)

• Change to scheme

Disclosure – overview

Hogan Lovells | 48

• Some information on request

• Trust deed and rules

• Benefit statement (DB)

• Statement of Investment Principles (DB & DC),

Statement of Funding Principles (DB)

Disclosure – overview (cont)

Hogan Lovells | 49

• Basic information about the scheme

• Before an employee joins a scheme where practicable

• Within 1 month of receiving jobholder information (where auto-enrolment applies)

• Otherwise within 2 months of joining

• Usually in form of scheme booklet

• Information may be provided electronically, unless member opts out of electronic communications

Disclosure – new joiners

Rebecca HowardCounsel, London Pensions

Member lifecycle 1 Joining the scheme

Member lifecycle 2 Active membership

Jim DavisSenior associate, London Pensions

Hogan Lovells | 52

This session will cover

Types of benefit structure

State pensions and contracting out

Introduction of pension schemes and tax

• Registration with HMRC

• Tax treatment of employer and member contributions

• Authorised payments from scheme

Hogan Lovells | 53

Types of scheme/arrangement Defined benefit 1

The Downton Abbey Pension Scheme Final Salary Section

Benefit provided: 1/60th of final pensionable salary for each year of pensionable service, payable at 65

Closed to new members and to further accrual in 2010

Hogan Lovells | 54

Example: Robert Crawley's pension: defined benefit

• Normal pension age: 65

• Pensionable service (up to closure in 2010): 20 years

• Final pensionable salary: £120,000

• Robert’s pension at age 65 (as calculated in 2010): 20/60 x £120,000 = £40,000

• Plus inflation protection (“revaluation”) until he reaches 65

Hogan Lovells | 55

Types of scheme/arrangement Defined benefit 2

The DAPS Career Average Revalued Earnings (CARE) Section

Benefit provided: 1/100th of earnings in each year of pensionable service (earnings from earlier years revalued to allow for inflation)

Hogan Lovells | 56

Example: Charles Carson’s pension: CARE

2019 accrual: x £40,000 = £400pa

2020 accrual: x £42,000 = £420pa

September 2020 CPI: 0.5%

At the end of 2020, Mr Carson’s accrued annual pensions from 2019 to 2020:

£420 + £402 (£400 x 1.005) = £822

Hogan Lovells | 57

Types of scheme/arrangementDefined contribution

The DAPS Defined Contribution Section

• Benefit provided: employer contribution of 4% of earnings, employee contribution 5% of earnings (basic pay plus overtime)

• Employer contributions increase to 5% if employee contributes 6%

• Size of pot at retirement depends on contributions and investment return

Hogan Lovells | 58

State pensions – if reached state pension age before 6 April 2016

Basic State Pension (BSP)

• From State pension age

• Flat rate (single pensioner) £137.60 per week if sufficient "qualifying years"

• Protection for carers and those on State benefits

Additional State pensions (earnings-related)

• State Second Pension (S2P)

• State Earnings Related Pension (SERPS) 1978 – 2002

Hogan Lovells | 59

Contracting-out of State pensions

Instead, member accrued rights in employer's pension scheme

Before 6 April 2012, possible to contract-out into a DB or DC scheme

Before 6 April 2016 could "contract-out" of earnings-related State

pension into a DB scheme

While contracted-out, no S2P / SERPS benefits accrued

Instead, member accrued rights in employer's pension scheme

Before 6 April 2016 could "contract-out" of earnings-related State

pension into a DB scheme

While contracted-out, no S2P / SERPS benefits accrued

Hogan Lovells | 60

DB contracting-out – what was it?

Before April 1997 members built up rights to "guaranteed minimum

pensions" (GMPs)

GMP / RST rules still apply to accrued contracted-out benefits

Member and employer paid lower National Insurance contributions

(NICs)

From April 1997, member accrued benefits that met "reference scheme

test"

Hogan Lovells | 61

DC contracting-out – what was it?

Ceased 6 April 2012

No reduction in NICs

Government paid age-related contributions to DC scheme

Benefits from Government contributions called "protected rights"

Special rules restricted what could be done with protected rights

Protected rights rules have been abolished but are still reflected in some scheme rules

Hogan Lovells | 62

6 April 2016 – all change!

Transitional protection for existing State pension rights

Reduction where member was previously contracted-out

Basic State Pension and State Second Pension replaced

New single-tier, flat-rate pension of £179.60 per week

Hogan Lovells | 63

Looking ahead ... a longer wait

• State pension age:

• State pension age equalised at 65 for men and women from November 2018

• Increasing to 68 by 2039

• Review every six years (report July 2017)

Hogan Lovells | 64

Pensions and tax: registered schemes

• May be occupational or personal schemes

• Must register with HMRC

Schemes registered under Finance Act 2004 ("Registered schemes"):

Hogan Lovells | 65

Taxation points

• Contributions going in

EXEMPT

• Fund growing

(mostly) EXEMPT

• Lump sums/pension going out

TAXED

(25% lump sum tax free; tax deducted by scheme)

Hogan Lovells | 66

Tax treatment of employer contributions

Member not taxed on employer contributions (though count towards

member’s annual allowance in DC schemes)

Deducted as an expense No limits on employer contributions

Hogan Lovells | 67

Tax treatment of member contributions

Free of income tax up to 100% of earnings (£3,600 if higher)

Subject to annual allowance

Hogan Lovells | 68

Annual allowance (AA) – restricting accrual

Exceeds accrual over annual allowance

£40,000 annual allowance (plus unused allowance for 3 previous

years)

Pension input amount in pension input period

• Member DC contributions

• Employer DC contributions

• Deemed value of DB accrual

Excess taxed at individual's marginal income tax rate

Tax relief

Hogan Lovells | 69

Annual allowance: not £40,000 for everyone

Annual allowance reduced for very high earners (broadly more than £240k pa) – tapering down to £4k pa

After taking flexible DC benefits – further tax-free DC accrual is reduced to level of “money purchase annual

allowance” - £4k

Hogan Lovells | 70

Tax relief for members' contributions –occupational schemes

Net pay arrangement – contributions from untaxed income

• Earns £20,000 pa

• Makes 5% pension contributions - £1,000, deducted from salary before tax

• Employer pays Anna's contributions direct to pension scheme

• Taxable income £19,000 (less personal allowance)

• National Insurance (employer and member) calculated on £20,000 salary

Anna Bates

Hogan Lovells | 71

Members' contributions – salary sacrifice

• Reference salary: £20,000

• Salary after salary sacrifice: £19,000

• Employer's pension contribution increased by £1,000

• National Insurance (employer and member) calculated on salary of: £19,000

Anna Bates

Hogan Lovells | 72

Paying out of the scheme – authorised payments

• Authorised member payments

• Income (pensions, annuities, drawdown payments)

• Lump sums

• Survivors' benefits

• Recognised transfers

• Payments following divorce

• Authorised employer payments

• Return of surplus

• Scheme administration payments

Hogan Lovells | 73

Unauthorised payments – charges

• Unauthorised member payments

• Member: 40% unauthorised payments charge

• Scheme administrator: 40% scheme sanction charge (15% if member has paid unauthorised payments charge)

• Scheme must report unauthorised payments annually

• Overpayments due to genuine error may be treated as authorised payments

Member lifecycle 2 Active membership

Jim DavisSenior associate, London Pensions

Any questions?

"Hogan Lovells" or the "firm" is an international legal practice that includes Hogan Lovells International LLP, Hogan LovellsUS LLP and their affiliated businesses.

The word “partner” is used to describe a partner or member of Hogan Lovells International LLP, Hogan Lovells US LLP or any of their affiliated entities or any employee or consultant with equivalent standing.. Certain individuals, who are

designated as partners, but who are not members of Hogan Lovells International LLP, do not hold qualifications equivalent to members.

For more information about Hogan Lovells, the partners and their qualifications, see www.hoganlovells.com.

Where case studies are included, results achieved do not guarantee similar outcomes for other clients. Attorney advertising. Images of people may feature current or former lawyers and employees at Hogan Lovells or models not

connected with the firm.

© Hogan Lovells 2020. All rights reserved

www.hoganlovells.com