Embed Size (px)

Citation preview

City Telecom (H.K.) LimitedDBS Vickers Pulse of Asia ConferenceSingapore

(HKEX:1137.HK / NASDAQ: CTEL)NiQ Lai, [email protected], +852 3145 606813 Jan 2010

1

2

This presentation contains forward-looking statements and information that involve risks, uncertainties and assumptions.Forward-looking statements are all statements that concern plans, objectives, goals, strategies, future events or performanceand underlying assumptions and other statements that are other than statements of historical fact, including, but not limitedto, those that are identified by the use of words such as "anticipates,'' "believes,'' "estimates,'' "expects,'' "intends,'' "plans,''"predicts,'' "projects'' and similar expressions.

Risks and uncertainties that could affect us include, without limitation: changes in technology; changes in the regulatoryenvironment in which we operate, or changes in the rules and polices that government regulators apply to our businesses;increased competition in the international services or fixed telecommunications network services; the benefits we expect toreceive from our continuing capital expenditure on our network; our ability to both maintain growth and successfullyintroduce new products and services; and the continued development and stability of the technological infrastructure we useto provide our telecommunications and Internet services.

Should one or more of such risks and uncertainties materialize, or should any underlying assumption prove incorrect, actualoutcomes may vary materially from those indicated in the applicable forward-looking statements. Any forward-lookingstatement or information contained in this presentation speaks only as of the date the statement was made.

We are not required to update any such statement or information to either reflect events orcircumstances that occur after the date the statement or information is made or to accountfor unanticipated events.

Disclaimer

US$400 million + 10 years later …

Click to watch on youtube: http://www.youtube.com/watch?v=wxuuK8r6T-s

3

Industry leading growth via market share gains. 17.7% growth to 943,000 subscription base for broadband, voice and IP-TV, majority of whom are on secured 24-month service contracts.

Turnover growth of 13.4% to HK$1,478.2 mn. EBITDA Growth of 34.4% to HK$508.1 mn.

Positive free cash flow for the third consecutive year, profit after tax up 70.0% to HK$212.8 mn and a net cash balance sheet.

FY2009 full year dividend per share up 216.7% to HK19 cents, 4.3% yield on stock price of HK$4.40 as of 8 Jan 2010.

Grew homes pass coverage by 140,000 to 1.62 mn and corporate buildings by 530 to 1,230, expanding our base for future growth.

FY09 Key Achievements

4

For the future ... Look to Japan

FTTH: +2.864 mn

DSL: -1.527 mn

CATV: +0.239 mn

12M to 2009/03

5

Agenda

How We Do ItFinancial Review

Management Outlook

6

Hong Kong’s Extreme Density

• Extremely compelling “Addressable Income per Fibre Mile”.

• US$200/Home Pass cost is <1/5th of US and European benchmarks.

Country

GDP/

Capita

(U$)

Pop

(million)

Area

(mi2)

Density

(mi2)

HK 30,755 7 428 16,380

US 46,859 302 3,717,813 80

Japan 38,559 127 145,868 640

IMF 2008 data

View from Victoria Peak

Luxury apartments in Kowloon East

7 7

End-To-End Bypass of Incumbent

End to End Network

• Brand-new fibre network completely bypassing the incumbent.

• When Alexander Graham Bell invented the telephone network system in 1876, it was not designed for computing. CTEL’s network is a computer network.

LAN Switches within

100m of end users

100 meters of Category 5e Copper Wiring

Fibre-To-The-Building

In-building Diagram

8

Can a New Generation Network cost base be structurally lower than the incumbent?

Cost per subscriber = US$1,295 / X, with X = number of subscribers:

If X = 1, cost per subscriber = US$1,295, i.e. relatively expensive.If X = 24, cost per subscriber = US$54, i.e. difficult for xDSL to match.

Above list price example is before bulk purchase discounts.

Furthermore, NGN bandwidth is symmetric at 100 Mbps which is difficult for xDSL to match on a mass scale.

Answer: It depends on network utilization.

Cisco Catalyst 2960 Router with 24 subscriber ports

List Price: US$1,295

9

22x Better Value

Only HKBN offers 80% bandwidth Guarantee of 2x money back AND

22x better vlaue.

Company TechnologyDownload / Upload

Speed

List Price

/Month Cost per Mbps

CTEL Fibre based FTTx 100Mbps / 100Mbps US$13 US$$0.06

IncumbentCopper based

xDSL8Mbps / 0.8 Mbps US$13 US$1.44

1010

The Brand Advantage

2008: Desell – Part II

Alexander Bell visits Broadband Hell to explain that the copper telephone line designed a 100 years ago.

http://www.youtube.com/watch?v=CJmfcFhJsWE

2007: Desell – Part I

Largest network is still providing broadband on old phone lines.

http://www.youtube.com/watch?v=BOceE7j--Oc

2009: “Awesome Speed. For Everyone”

A Lamborghini “SuperCar” experience for everyone.

http://www.youtube.com/watch?v=gj27SOjOn58

11

Wireless Broadband is a not a Substitute

HKBN Fibre Broadband Services Wireless 3.5G

HKBN bb100 Wireless 3.5G

Downlink 100 Mbps 21 Mbps

Uplink 100 Mbps 6 Mbps

Bandwidth Guarantee 80% of Advertise Bandwidth

Not Available

Cost Per Month US$13 US$69

US$/Mbps/Month US$0.06 US$2.60

12

64 content + 24 interactive channels capturing a wide range of interest.

bbNews available cross platforms @ www.youtube.comsince August 2009

bbTV - A Better Value Buffet Alternative

13

Management Mix

Mr. NiQ Lai

Chief Financial Officer and Head of Staff EngagementYears with Co: 5 years

Prior to joining CTEL in 2004, was Director and Head of Asia Telecom

Equity Research for Credit Suisse.

Bachelor of Commerce -University of Western

Australia, EMBA - Kellogg-HKUST, Fellow - CPA

Australia, Fellow - HKICPA and Member - Hong Kong Institute of Independent

Directors

Mr. Paul Cheung

Co-Founder, Vice ChairmanYears with Co: 16 years

Over 27 years experience in telecommunication and

computer industries

Diploma of Advanced Programming and Systems Concepts Design - Herzing

Institute, Canada

Mr. William Yeung

Chief Executive OfficerYears with Co: 4 years

Over 17 years experience in telecommunication

industry including 9 years at SmarTone Vodafone prior to joining CTEL

Bachelor of Arts and Master of Science in

Electronic Commerce and Internet Computing –Hong Kong University, MBA - University of Strathclyde, UK

Mr. Ricky Wong

Co-Founder, ChairmanYears with Co: 16 years

Over 20 years experience in telecommunication and

computer industries

Bachelor’s Degree in Science and EMBA - The

Chinese University of Hong Kong

14

Talent Engagement

“CXO of the Future”

� Management Trainee Program� Develop our future CEO, CFO, CTO

etc in 15-20 years time. � Requires - CFA Level 1, half

marathon, 36 management books, etc.

� 400 applicants, 3 hired in 2009.

“Talent Infinity”

� 75% of top 33 executives have or working towards a post graduate degrees, with company sponsorship of 50-100% of fees.

� These includes programs organized by Kellogg-HKUST, The Chinese University of Hong Kong, Kellogg School of Management and Michigan Ross School of Business.

15

New vertical model optimized for customer engagement BUT requires “smart” Mini-CEOs

Director of Network Development

Director of Customer Service

Director of Sales

Director of Network Maintenance

Ho

ng

Ko

ng

Isla

nd

Ko

wlo

on

East

New

Terr

ito

ries E

ast

Ko

wlo

on

West

New

Terr

ito

ries W

est

Cu

sto

mer

Exp

eri

en

ce

16

Agenda

How We Do It

Financial ReviewManagement Outlook

17

59

(4)

5

61

(18)

10

(26)

5

27

(13)

13

34

(7)(11)

41

7

20

3832

37

PCCW (31 Dec YE) CTI (31 Aug YE) i-Cable (31 Dec YE) HTHK (31 Dec YE)

1H 2007

2H 2007

1H 2008

2H 2008

1H 2009

2H 2009

Net Additions (‘000)

Source: PCCW, i-Cable’s, HTHK Interim Annual Reports; JP Morgan HTHK report dated 12 Aug 2009; HTIL 20-F Filing. Note: PCCW reports “broadband access lines” rather than subscriptions

Broadband: Rapidly winning market share

Subscriptions(‘000)

Most Recent 6 months net unit growth

1,176

324245

306255280 260267 261

350260 250

391

227

1,237

247

1,275

279

1,302

316

1,305

PCCW (31 Dec YE) CTI (31 Aug YE) i-Cable (31 Dec YE) HTHK (31 Dec YE)

1H 2007

2H 2007

1H 2008

2H 2008

1H 2009

2H 2009

18

245.2

353.8378.0

508.1

(92.2)

28.9

125.2

212.8

FY06 FY07 FY08 FY09

EBITDA

Net Profit

948.5 950.4 953.8

683.6

163.3

647.9

396.1

547.3

421.6

221.1

FY05 FY06 FY07 FY08 FY09

Gross Debt

Gross Cash

Note: EBITDA for any period means, without duplication, net income for such period, plus the following to the extent deducted in calculating such net income: net interest expense/ (income), income taxes, depreciation and amortization expense (excluding any such non cash charge to the extent it represents an accrual of or reserve for cash charges in any future period or amortization of a prepaid cash expense that was paid in a prior period not included in the calculation).

Financial Trends

EBITDA and Net Profit Improvement

Net Cash Balance Sheet in FY2009

Positive Free Cash Flow Since FY2007

Achieved net debt free position

245.2

353.8378.0

508.1

323.0

132.3

211.7

286.7

FY06 FY07 FY08 FY09

EBITDA

Total CapexHK$ mn

19

Income Statement

FTNS turnover grew by 21.8% to HK$1,230.9 mn, representing 83.3% of total turnover.

Other income includes net gain of HK$31.4 mn on senior notes buyback and cancellation during FY2009.

Tax includes non-cash deferred taxation of HK$37.1 mn.

Note: * Core EBITDA excludes net gain of HK$31.4 mn from senior notes buyback and cancellation.

HK$ mn FY08 FY09 YoY %

Fixed Telecoms Network Services 1,011.0 1,230.9 21.8%

International Telecoms 292.0 247.3 -15.3%

Turnover 1,303.0 1,478.2 13.4%

Interest income 15.6 4.8 -69.2%

Other income, excluding interest income 9.4 36.7 290.4%

Other revenues 25.0 41.5 66.0%

Network Expenses (178.4) (175.1) -1.8%

Staff Costs (247.5) (302.3) 22.1%

Office Expenses (29.0) (33.8) 16.6%

General and Administration (138.0) (142.6) 3.3%

Advertising and Promotion (341.5) (353.0) 3.4%

Operating Cash Costs (934.4) (1,006.8) 7.7%

EBITDA 378.0 508.1 34.4%

EBITDA Margin 29.0% 34.4%

Core EBITDA* 476.7

Core EBITDA Margin 32.2%

Depreciation (210.1) (206.2) -1.9%

Operating Profit 183.5 306.7 67.1%

Finance Costs (75.1) (55.1) -26.6%

Profit Before Tax 108.4 251.6 132.1%

Tax 16.8 (38.8) -331.0%

Profit After Tax 125.2 212.8 70.0%

Earnings per Share (HK cents/share)

- Basic (HK cents/share) 19.7 32.4 64.5%

- Fully Diluted (HK cents/share) 19.0 31.8 67.4%

Dividend declared (HK cents/share) 6.0 19.0 216.7%

Total Capex 211.7 286.7 35.4%

EBITDA - Capex - net financing cost 106.7 171.1 60.4%20

During FY2009, brought back and cancelled US$68 mn (HK$527.0 mn) of senior notes at below par.

As of 31 Aug 2009, achieved net cash position of HK$57.8 mn on gross cash and cash equivalent balance of HK$221.1 mn.

Additional reserve liquidity secured with committed revolving bank facility of HK$190 mn until July 2011.

Balance Sheet

HK$ mn 31-Aug-08 31-Aug-09

Goodwill 1.1 1.1

Fixed assets 1,231.4 1,302.4

Deferred tax assets 26.3 -

Long term prepayment 5.6 6.0

Long-term portion - deferred expenditure 15.4 12.8

Cash and bank balances 421.6 221.1

Restricted bank deposit 87.3 15.0

Other current assets 291.7 226.6

Current assets 800.6 462.7

Current liabilities (359.4) (377.7)

Employment of capital: 1,721.0 1,407.3

Shareholder funds 1,032.6 1,228.5

Deferred taxation 4.9 15.7

Finance lease 0.3 0.5

8.75% 2015 Senior Notes 683.2 162.6

Funds employed 1,721.0 1,407.3

Gross Debt to EBITDA (x) 1.8 0.3

Net Debt to EBITDA (x) 0.7 Net Cash

21

Increased Dividend Payout Ratio

The Board of Directors recommends a final cash dividend per share of HK16 cents, making a total dividend of HK19 cents for FY2009 (FY2008: HK6 cents).

Since achieving positive adjusted free cash flow (EBITDA-Capex-Net Finance Costs) in FY2007, we have been paying a portion of this metric as our dividend policy.

We raised the payout from around 30% in FY2008 to around 75% in FY2009 due to: - growing portion of our business with service under secured 24 months contracts, - controllable capital expenditure, and - net cash balance sheet.

Going forward, we aim to maintain dividend payout in the range of 50-75%.

Dividend per ordinary share in HK$

217% increase

0.08

0.06

0.19

FY07 FY08 FY09

22

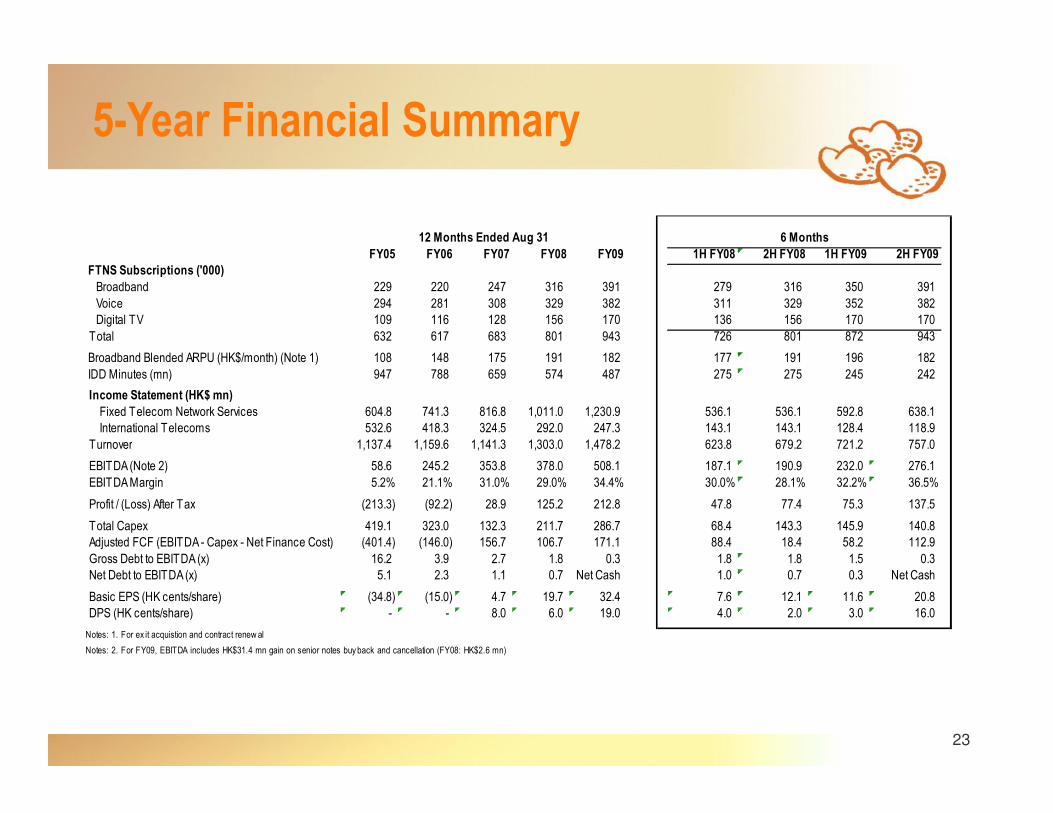

5-Year Financial Summary

FY05 FY06 FY07 FY08 FY09 1H FY08 2H FY08 1H FY09 2H FY09

FTNS Subscriptions ('000)

Broadband 229 220 247 316 391 279 316 350 391

Voice 294 281 308 329 382 311 329 352 382

Digital TV 109 116 128 156 170 136 156 170 170

Total 632 617 683 801 943 726 801 872 943

Broadband Blended ARPU (HK$/month) (Note 1) 108 148 175 191 182 177 191 196 182

IDD Minutes (mn) 947 788 659 574 487 275 275 245 242

Income Statement (HK$ mn)

Fixed Telecom Network Services 604.8 741.3 816.8 1,011.0 1,230.9 536.1 536.1 592.8 638.1

International Telecoms 532.6 418.3 324.5 292.0 247.3 143.1 143.1 128.4 118.9

Turnover 1,137.4 1,159.6 1,141.3 1,303.0 1,478.2 623.8 679.2 721.2 757.0

EBITDA (Note 2) 58.6 245.2 353.8 378.0 508.1 187.1 190.9 232.0 276.1

EBITDA Margin 5.2% 21.1% 31.0% 29.0% 34.4% 30.0% 28.1% 32.2% 36.5%

Profit / (Loss) After Tax (213.3) (92.2) 28.9 125.2 212.8 47.8 77.4 75.3 137.5

Total Capex 419.1 323.0 132.3 211.7 286.7 68.4 143.3 145.9 140.8

Adjusted FCF (EBITDA - Capex - Net Finance Cost) (401.4) (146.0) 156.7 106.7 171.1 88.4 18.4 58.2 112.9

Gross Debt to EBITDA (x) 16.2 3.9 2.7 1.8 0.3 1.8 1.8 1.5 0.3

Net Debt to EBITDA (x) 5.1 2.3 1.1 0.7 Net Cash 1.0 0.7 0.3 Net Cash

Basic EPS (HK cents/share) (34.8) (15.0) 4.7 19.7 32.4 7.6 12.1 11.6 20.8

DPS (HK cents/share) - - 8.0 6.0 19.0 4.0 2.0 3.0 16.0

Notes: 1. For ex it acquistion and contract renew al

Notes: 2. For FY09, EBITDA includes HK$31.4 mn gain on senior notes buyback and cancellation (FY08: HK$2.6 mn)

6 Months12 Months Ended Aug 31

23

Since FY2007, the start of our 10-year Big Hairy Audacious Goal (BHAG) period, we have achieved accelerated growth. Broadband is particularly strong with 23.7% year-on -year growth rate to 391,000, far exceeding the industry growth rate of approximately 2.8% to 2.0 mn.

Note: *includes all registered paid and free, on-net and off-net subscriptions.

FTNS Performance - Triple Play Subscriptions

Subscription (‘000)

229 220 247316

391

294 281308

329

382109 116

128

156

170

FY05 FY06 FY07 FY08 FY09

Digital TV

Voice

Broadband

Start of 10 year BHAG period

24

During FY2009, ARPU fell by 4.7% to HK$182/month as we focused on expanding our customer base for future growth.

During FY2009, Broadband churn rate remained well below 1.0% per month.

*Note: For exit acquisition and contract renewal

Broadband ARPU Trend

Blended ARPU HK$

113

148

175

191182

FY05 FY06 FY07 FY08 FY09

25

Hong Kong Based Acquisition

1,633 Talents^

Guangzhou Based Retention

1,520 Talents^

Two-thirdreduction in

costs

Margin Expansion with transition from Acquisition to Retention

^These refer to the number of talents working in the location indicated. 26

During FY2009, grew homes pass coverage by 140,000 to 1.62 mn and corporate buildings by 530 to 1,230, expanding our base for future growth. Maintain target for Fibre network expansion to 2.0 mn homes pass and 1,800 commercial buildings by end 2011.

Budgeted annual capital expenditure of HK$300-350 mn per year for FY2010-11 and maintain “CAPEX level below EBITDA” policy.

Capital Expenditure

HK$ mn419.1

323.0

132.3

211.7

286.7

FY05 FY06 FY07 FY08 FY09

27

Agenda

How We Do It

Financial Review

Management Outlook

28

Our Passion

Vivid Description“My children will say, “Dad I

love you as my Father””

Big Hairy Audacious Goal (BHAG)

“Be the largest IP provider in Hong Kong

by 2016”

Core Value“To experience the emotion of competition, winning and

crushing competition”

29

Member Get Member: “AWESOME SPEED. FOR EVERYONE”

100Mbps broadband at HK$99/monthInterview with CEO can be viewed at http://www.youtube.com/watch?v=IZqhiziKzZ0

3,000 Talent Town-Hall Meetings

30

Member Get Member:“Turn One Happy Customer into Two.”

Existing Happy Customer(with Bigger Smile!)

bb100 @ HK$99/month+

Note: + Foundation for Value Added Services Upsell, e.g. bbDrive package @ HK$20/month, Voice @ HK$20-40/month, bbTV @ HK$40-70/month, etc.

New Happy Customerbb100 @ HK$99/month+

Existing Happy Customer HK$182/month

31

It’s a Huge Market for CTEL

2008

5% of US$3.6 billion revenue market share

today

2016

BHAG: Hong Kong’s largest IP Service

Provider

PCCW - TSS62%

PCCW - Now TV8%

Hutchison - Fixed9%

Wharf T&T6%

i-Cable7%

Hong Kong Broadband Network

5%

New World3%

3232

Accelerate our broadband growth from 391,000 subscriptions as of 31 August 2009 to exceed 500,000 subscriptions by 31 August 2010

mild revenue growth,

flat core EBITDA of HK$478 million, and

Capital Expenditure at HK$300-350 mn.

Big, Hairy & Audacious Goal (BHAG)

“To be the largest IP provider in Hong Kong by 2016”

Company Vision Statement set in November 2006

FY2010 Guidance

With objective firmly set on achieving our BHAG, we have the following outlook for FY2010:

33

For the four months to 31 Dec 2009 (1st four months of FY2010):

added net 52,000 broadband subscriptions which compares with our full financial year 2010 target of adding net 110,000.

net additions of 13,000/month far exceeds normal versus industry growth of 5,100/month, i.e. HKBN grabbing customers from other broadband providers on mass.

1 Millionth Milestone Achieved in Dec 2009

34

Fixed Telecom Network Services Subscriptions

31 Aug 08 31 Aug 09 31 Dec 09 Broadband 316,000 391,000 443,000

Voice 329,000 382,000 403,000 TV 156,000 170,000 158,000

Total 801,000 943,000 1,004,000

In Dec 2010, filed an application for Free TV license (FTV):

FTV is a incremental HK$210 million (capex and opex) investment to existing IP-TV operations, which has been running for 6 years.

Existing advertising revenues of FTV market estimated at HK$3.7 billion with 75% dominance by TVB.

As our FTV will be delivered by Fibre rather than traditional over the air, this expansion helps to monetize our Fibre investment

Free TV Application

35

Stock Valuation Metrics

1137.HK and CTEL 12 months Stock Price Chart

36

Units SEHK Shares NASDAQ ADR

Stock code 1137.HK CTEL

Currency HK$ US$

Price, 8 Jan 2010 4.40 11.65

ADR Premium / (Discount) NA 2.60%

Average daily stock turnover

(3 months) 000 2,138 63

Number of issued shares millions 680 34

Market Cap millions 2,991 396

Less: Net Debt \ (Net Cash) millions 58 7

Enterprise Value millions 3,049 403

FY2009 DPS 0.19 0.49

Dividend Yield 4.3% 4.2%

FY2009 EBITDA millions 508 66

EV/EBITDA x 6.0 6.2

FY2009 Profit after Tax millions 213 27

Price to Earnings (P/E) x 14.1 14.4

::: END :::

Investor Engagement ContactMr. NiQ Lai

CFO and Head of Talent Engagement Telephone: +852 3145 6068

Email: [email protected]

37