Embed Size (px)

Citation preview

1

www.hro.com

Denver Boulder Colorado Springs Dublin London Los Angeles Munich Phoenix Salt Lake City San Francisco

Update on SEC’s Proxy Disclosure Enhancements

Christine M. Daly

Martha Dugan Rehm

303-866-0486

303-866-0464

CBA Securities Subsection LuncheonFebruary 18, 2010

2

SEC’s New Corporate Governanceand Compensation Disclosure - Timing

• Proposed - 7/10/2009 (Rel. No. 33-9052)

• Adopted - 12/16/2009 (Rel. No. 33-9089)

• Effective – 2010 Proxy Season• FYE on or after 12/20/2009• File proxy statement (or Form 10-K) on or

after 2/28/2010

• Compliance and Disclosure Interpretations (CD&I’s - 12/22/2009)

3

SEC’s New Corporate Governanceand Compensation Disclosure - Rules

• Reg. S-K, Item 401 (Directors, etc.)

• Reg. S-K, Item 402 (Exec. Comp.)

• Reg. S-K, Item 407 (Corp. Gov.)

• Form 8-K (Current Reports)

• Forms N-1A, N-2 and N-3 (registered investment companies)

• CD&I’s - 1/20/2010 and 2/16/2010

4

SEC’s New Corporate Governanceand Compensation Disclosure - Areas

• Compensation practices, including risk assessment

• Director qualifications, background; diversity as factor in nominee selection

• Board leadership structure and risk oversight• Compensation table, reporting equity awards• Compensation consultant disclosure• Election results accelerated (4 bus. days)

5

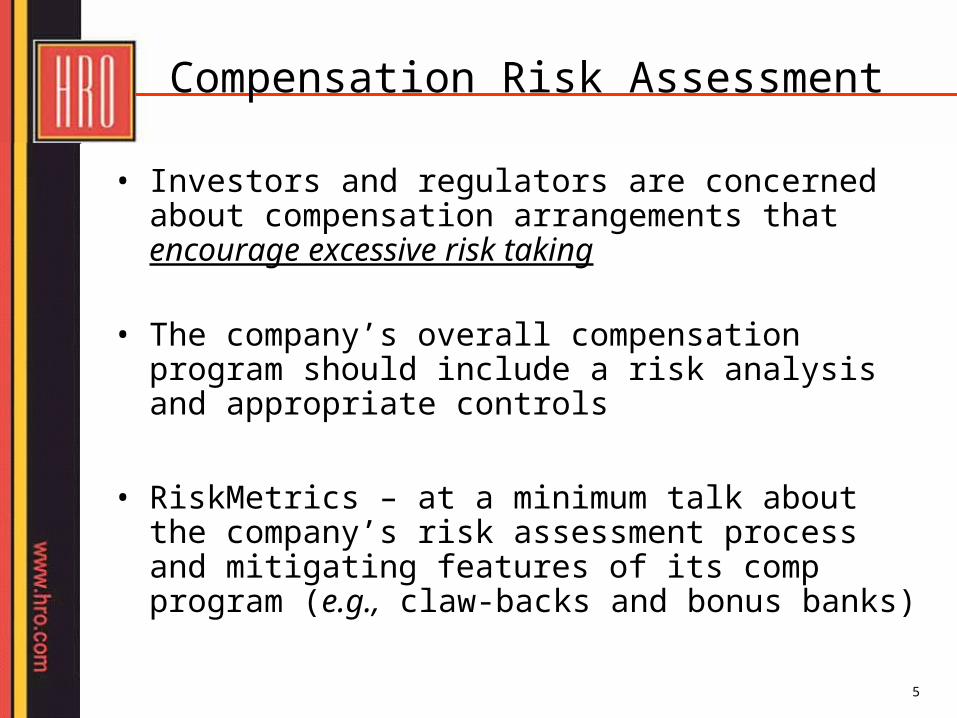

Compensation Risk Assessment

• Investors and regulators are concerned about compensation arrangements that encourage excessive risk taking

• The company’s overall compensation program should include a risk analysis and appropriate controls

• RiskMetrics – at a minimum talk about the company’s risk assessment process and mitigating features of its comp program (e.g., claw-backs and bonus banks)

6

Compensation Risk Assessment

Step 1: Perform a risk assessment of the company’s overall compensation policies and practices

Step 2: Include narrative disclosure where risks arising from compensation practices are reasonably likely to have a material adverse effect on the company

7

Compensation Risk Assessment

• Examples that may trigger disclosure: • business unit carries significant portion of

company’s risk profile• business unit with compensation structured

significantly different• business unit that is significantly more profitable• business unit where comp expense is a significant

percentage of the unit’s revenues• payment of bonus when goal achieved, while the

income and risk to the company extend over a significantly longer period of time

8

Compensation Risk Assessment

• What may need to be disclosed:• the general design of the program and its

implementation• the company’s risk assessment or incentive

considerations in structuring the policies and practices or in awarding or paying the comp

• mitigating factors such as claw-backs or holding period requirements

• policies regarding adjustments to comp policies and material adjustments made

• the extent to which the company monitors its comp program to determine whether its risk objectives are met

9

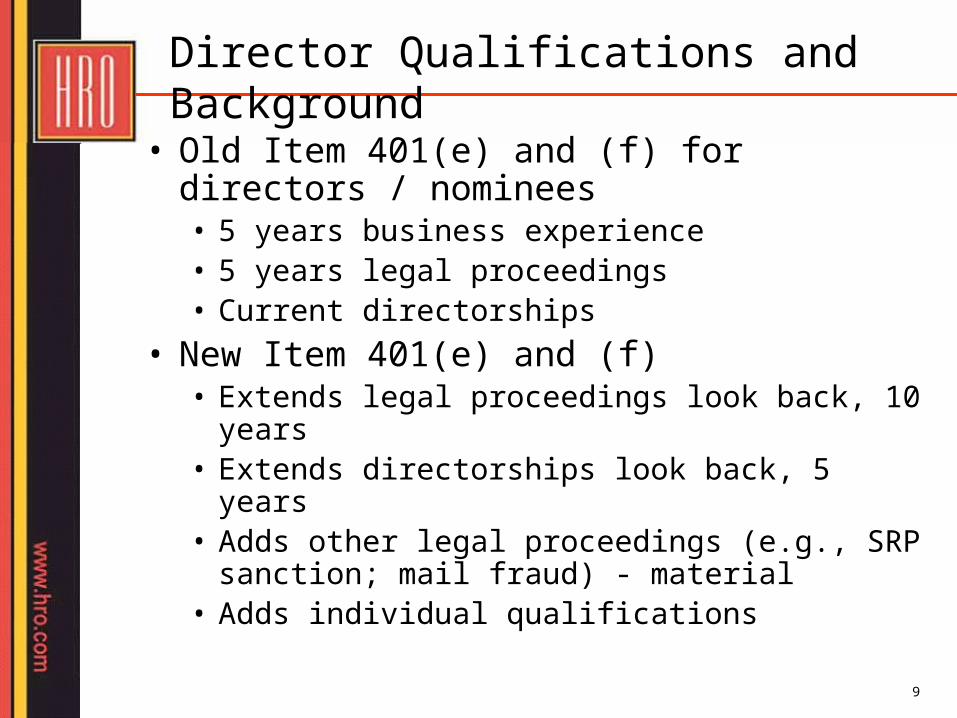

Director Qualifications and Background

• Old Item 401(e) and (f) for directors / nominees• 5 years business experience• 5 years legal proceedings• Current directorships

• New Item 401(e) and (f)• Extends legal proceedings look back, 10 years• Extends directorships look back, 5 years• Adds other legal proceedings (e.g., SRP

sanction; mail fraud) - material• Adds individual qualifications

10

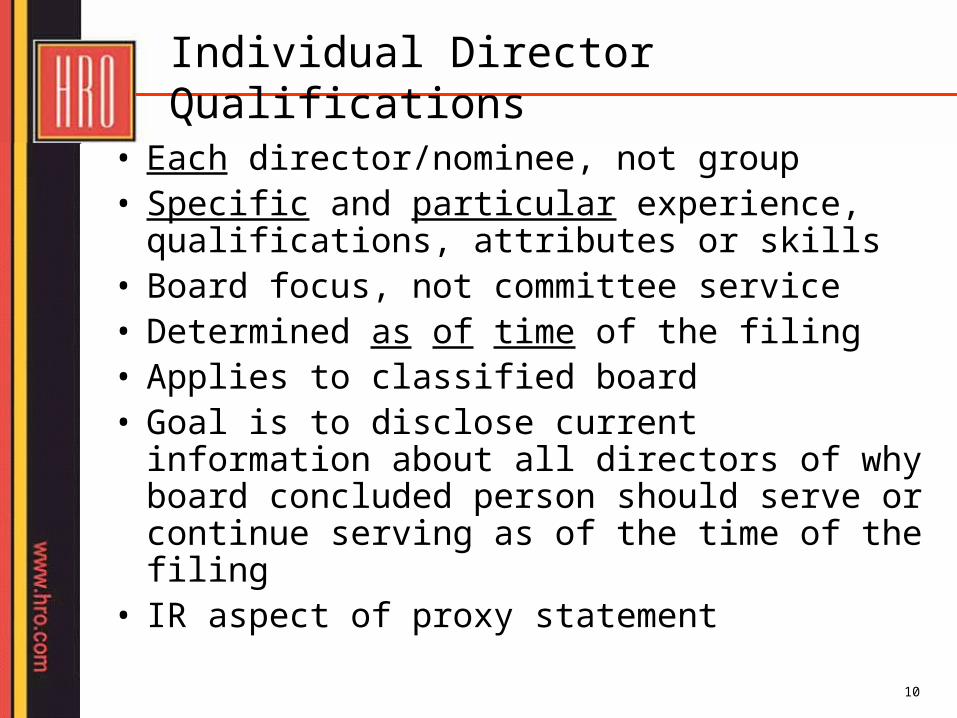

Individual Director Qualifications

• Each director/nominee, not group• Specific and particular experience,

qualifications, attributes or skills• Board focus, not committee service• Determined as of time of the filing• Applies to classified board• Goal is to disclose current information about

all directors of why board concluded person should serve or continue serving as of the time of the filing

• IR aspect of proxy statement

11

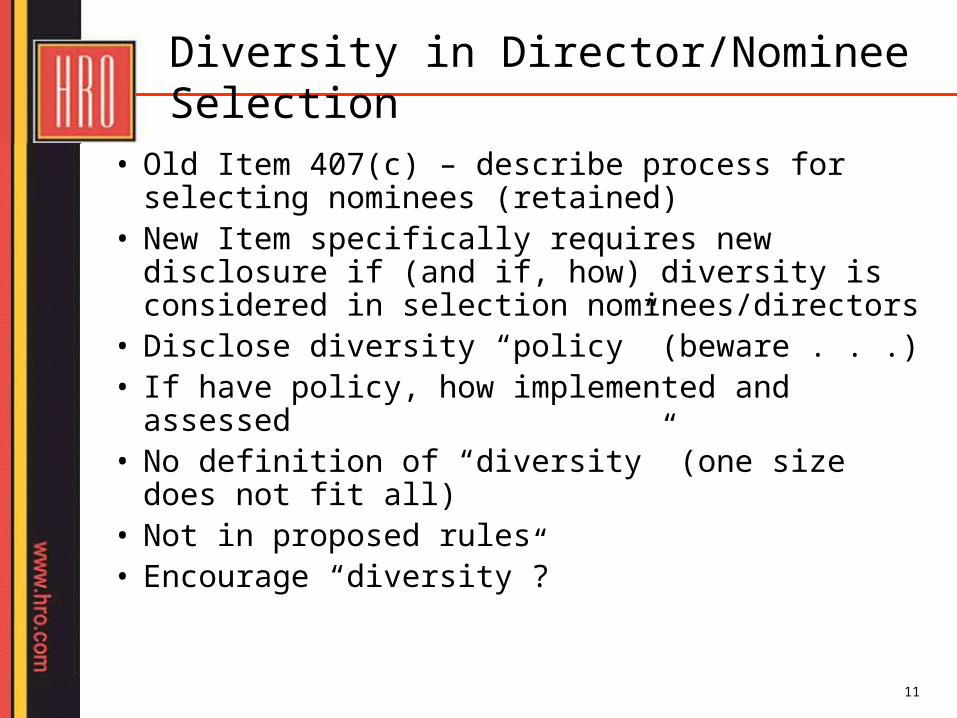

Diversity in Director/Nominee Selection

• Old Item 407(c) – describe process for selecting nominees (retained)

• New Item specifically requires new disclosure if (and if, how) diversity is considered in selection nominees/directors

• Disclose diversity “policy” (beware . . .)• If have policy, how implemented and assessed• No definition of “diversity” (one size does not

fit all)• Not in proposed rules• Encourage “diversity”?

12

Board Leadership Structure

• New Item 407(h)

• Board leadership structure• CEO/Chair combined or not• Why chosen structure is appropriate

• Lead independent director existence and role, if CEO/Chair is combined

• Goal of transparency, not to dictate structure of leadership

13

Board Role in Risk Oversight

• Disclosure of how company perceives role of board and senior management in managing material risks

• No definition of risk (but credit, liquidity, operational risks)

• Process oriented, not substantive risk disclosure• Manner in which board administers oversight• Structure of risk oversight (e.g., risk committee;

reporting relationships; information receipt)• Effect oversight function has on leadership

structure

14

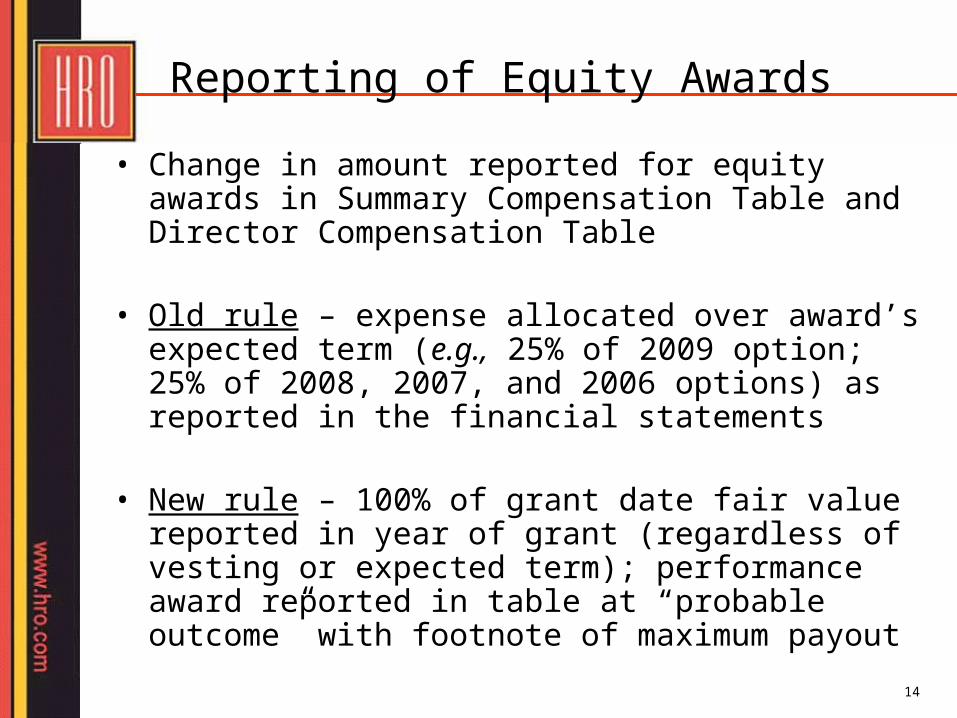

Reporting of Equity Awards

• Change in amount reported for equity awards in Summary Compensation Table and Director Compensation Table

• Old rule – expense allocated over award’s expected term (e.g., 25% of 2009 option; 25% of 2008, 2007, and 2006 options) as reported in the financial statements

• New rule – 100% of grant date fair value reported in year of grant (regardless of vesting or expected term); performance award reported in table at “probable outcome” with footnote of maximum payout

15

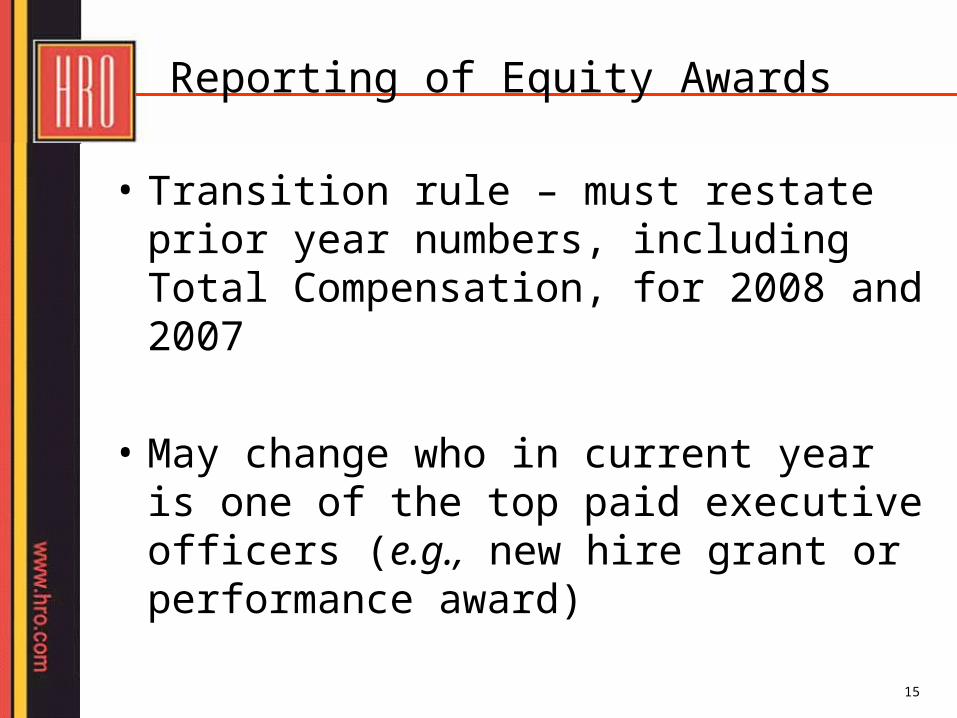

Reporting of Equity Awards

• Transition rule – must restate prior year numbers, including Total Compensation, for 2008 and 2007

• May change who in current year is one of the top paid executive officers (e.g., new hire grant or performance award)

16

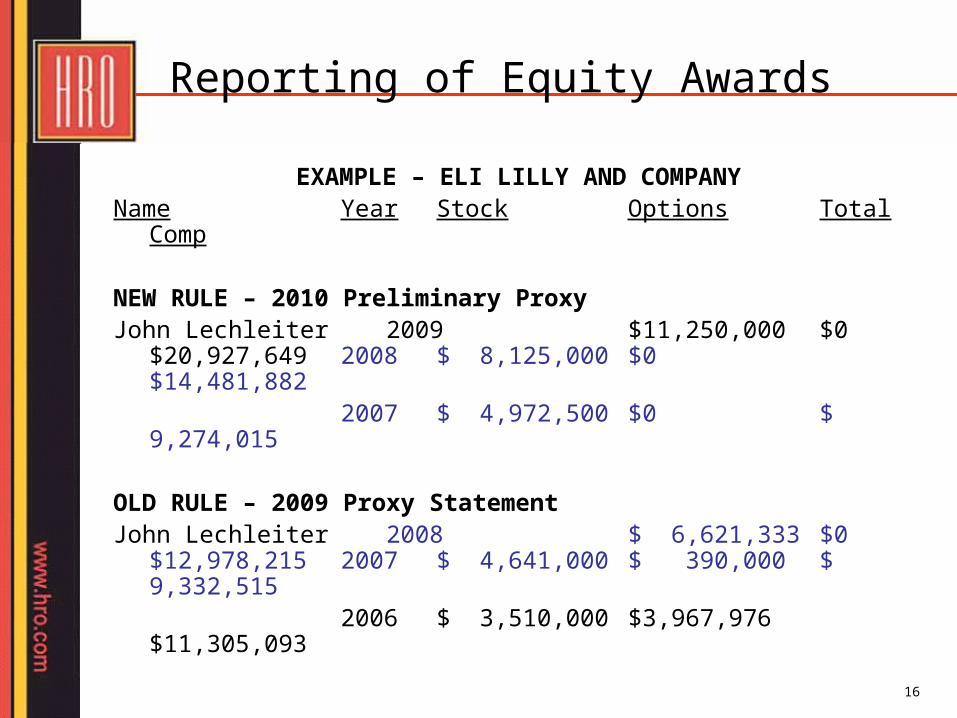

Reporting of Equity Awards

EXAMPLE – ELI LILLY AND COMPANYName Year Stock Options Total

Comp

NEW RULE – 2010 Preliminary ProxyJohn Lechleiter 2009 $11,250,000 $0

$20,927,649 2008 $ 8,125,000 $0$14,481,882

2007 $ 4,972,500 $0 $ 9,274,015

OLD RULE – 2009 Proxy StatementJohn Lechleiter 2008 $ 6,621,333 $0

$12,978,215 2007 $ 4,641,000 $ 390,000 $ 9,332,515

2006 $ 3,510,000 $3,967,976$11,305,093

17

Compensation Consultant

• Disclose fees paid to compensation consultant and potential conflicts of interest

• Where board or comp committee has engaged its own consultant and the consultant received more than $120,000 during the fye, disclose:

• fees paid for board and non-board services• whether decision to engage consultant (or its

affiliates) for additional services to the company was made or recommended by management

• whether board or committee approved the other services provided to the company

18

SEC Comments

• Trends in SEC comments:• Peer group and benchmarking (“competitive;”

describe how peers selected and data is used; disclose where actual payments fell in range)

• Performance targets (disclose any material performance targets; identify the specific targets; disclose actual results)

• Compensation Discussion and Analysis (shorten background and process-oriented information; include “how” and “why”)

• SEC change in position – will require amendment of filings if material deficiency (instead of “futures” comment)

19

Director Elections - Impact

• Broker non-votes (NYSE Rule 452)

• Direct proxy accessby shareholders (proposed rule 14a-11)

• Proxy disclosure enhancements(adopted 12/16/2009)

• Accelerated results – Form 8-K within 4 business days

• Proxy advisory firms more active

20

Broker Non-Votes

• No broker discretionary voting in director elections

• Primary effect – lower retail vote turnout

• Ensure that proxy includes a “routine” proposal (e.g., ratify auditors) so broker votes count for quorum

• Analyze impact s/h base and state law

• Review and modify description of “vote required” and “how votes are counted”

21

Update on SEC’s Proxy Disclosure Enhancements

CBA Securities Subsection LuncheonFebruary 18, 2010