Embed Size (px)

Citation preview

1. Which of the following is not a benefit of budgeting?

A. Management can plan ahead.

B. An early warning system is provided for potential problems.

C. It enables disciplinary action to be taken at every level of responsibility.

D. The coordination of activities is facilitated.

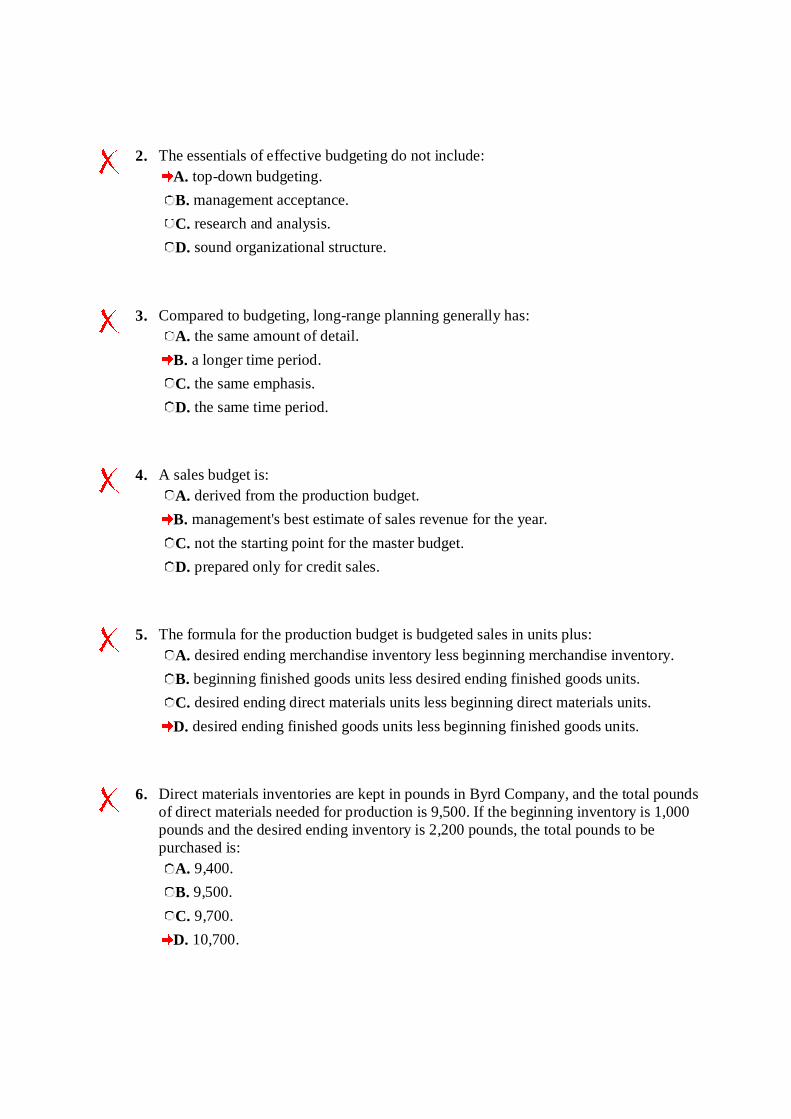

2. The essentials of effective budgeting do not include:

A. top-down budgeting.

B. management acceptance.

C. research and analysis.

D. sound organizational structure.

3. Compared to budgeting, long-range planning generally has:

A. the same amount of detail.

B. a longer time period.

C. the same emphasis.

D. the same time period.

4. A sales budget is:

A. derived from the production budget.

B. management's best estimate of sales revenue for the year.

C. not the starting point for the master budget.

D. prepared only for credit sales.

5. The formula for the production budget is budgeted sales in units plus:

A. desired ending merchandise inventory less beginning merchandise inventory.

B. beginning finished goods units less desired ending finished goods units.

C. desired ending direct materials units less beginning direct materials units.

D. desired ending finished goods units less beginning finished goods units.

6. Direct materials inventories are kept in pounds in Byrd Company, and the total pounds of direct materials needed for production is 9,500. If the beginning inventory is 1,000 pounds and the desired ending inventory is 2,200 pounds, the total pounds to be purchased is:

A. 9,400.

B. 9,500.

C. 9,700.

D. 10,700.

7. The formula for computing the direct labor budget is to multiply the direct labor cost per hour by the:

A. total required direct labor hours.

B. physical units to be produced.

C. equivalent units to be produced.

D. No correct answer is given.

8. Each of the following budgets is used in preparing the budgeted income statement except the:

A. sales budget.

B. selling and administrative budget.

C. capital expenditure budget.

D. direct labor budget.

9. Expected direct materials purchases for Read Company are $70,000 in the first quarter and $90,000 in the second quarter. Forty percent of the purchases are paid in cash as incurred, and the balance is paid in the following quarter. The budgeted cash payments for purchases in the second quarter are:

A. $96,000.

B. $90,000.

C. $78,000.

D. $72,000.

10. The budget for a merchandiser differs from a budget for a manufacturer because:

A. a merchandise purchases budget replaces the production budget.

B. the manufacturing budgets are not applicable.

C. None of the above.

D. Both (a) and (b) above.

This is the end of the test. When you have completed all the questions and reviewed your answers, press the button below to grade the test.

Grade the Test

0% (0 out of 10 correct)

1. Which of the following is not a benefit of budgeting? A. Management can plan ahead. B. An early warning system is provided for potential problems. C. It enables disciplinary action to be taken at every level of responsibility. D. The coordination of activities is facilitated.

2. The essentials of effective budgeting do not include: A. top-down budgeting. B. management acceptance. C. research and analysis. D. sound organizational structure.

3. Compared to budgeting, long-range planning generally has: A. the same amount of detail. B. a longer time period. C. the same emphasis. D. the same time period.

4. A sales budget is: A. derived from the production budget. B. management's best estimate of sales revenue for the year. C. not the starting point for the master budget. D. prepared only for credit sales.

5. The formula for the production budget is budgeted sales in units plus: A. desired ending merchandise inventory less beginning merchandise inventory. B. beginning finished goods units less desired ending finished goods units. C. desired ending direct materials units less beginning direct materials units. D. desired ending finished goods units less beginning finished goods units.

6. Direct materials inventories are kept in pounds in Byrd Company, and the total pounds of direct materials needed for production is 9,500. If the beginning inventory is 1,000 pounds and the desired ending inventory is 2,200 pounds, the total pounds to be purchased is:

A. 9,400. B. 9,500. C. 9,700. D. 10,700.

7. The formula for computing the direct labor budget is to multiply the direct labor cost per hour by the:

A. total required direct labor hours. B. physical units to be produced. C. equivalent units to be produced. D. No correct answer is given.

8. Each of the following budgets is used in preparing the budgeted income statement except the:

A. sales budget. B. selling and administrative budget. C. capital expenditure budget. D. direct labor budget.

9. Expected direct materials purchases for Read Company are $70,000 in the first quarter and $90,000 in the second quarter. Forty percent of the purchases are paid in cash as incurred, and the balance is paid in the following quarter. The budgeted cash payments for purchases in the second quarter are:

A. $96,000. B. $90,000. C. $78,000. D. $72,000.

10. The budget for a merchandiser differs from a budget for a manufacturer because: A. a merchandise purchases budget replaces the production budget. B. the manufacturing budgets are not applicable. C. None of the above. D. Both (a) and (b) above.

Retake Test

1. Budgeting facilitates the coordination of activities within the business by correlating the goals of each segment with overall company objectives.

A. True

B. False

2. The most common budget period is one month.

A. True

B. False

3. The chief accountant (controller) has responsibility for coordinating the preparation of the budget.

A. True

B. False

4. The master budget is a set of interrelated budgets that constitutes a plan of action for a specified time period.

A. True

B. False

5. The budgeted income statement is the starting point in preparing financial budgets.

A. True

B. False

6. The production budget is the first budget prepared in the master budget.

A. True

B. False

7. The direct materials budget shows both the quantity and cost of direct materials to be

purchased.

A. True

B. False

8. The financing section of a cash budget shows expected borrowings and the repayment of borrowed funds plus interest.

A. True

B. False

9. The budgeted balance sheet is developed from the budgeted balance sheet for the preceding year and the budgets for the current year.

A. True

B. False

10. A merchandiser uses a merchandise purchases budget in addition to a production budget.

A. True

B. False

11. Which of the following are correct statements about a budget?

A. It is a formal written statement of management's plans for a specified future time period.

B. It becomes an important basis for evaluating performance.

C. It promotes efficiency and serves as a deterrent to waste and inefficiency.

D. All of these options are correct statements.

12. The primary benefits of budgeting include all of the following except it:

A. requires only top management to plan ahead and formalize goals.

B. provides definite objectives for evaluating performance.

C. creates an early warning system for potential problems.

D. motivates personnel throughout the organization.

13. The most common budget period is a:

A. week.

B. month.

C. quarter.

D. year.

14. Coordinating the preparation of the budget is the responsibility of the:

A. treasurer.

B. president.

C. chief accountant.

D. budget committee.

15. Long-range planning usually encompasses a period of:

A. a quarter.

B. a year.

C. at least two years.

D. at least five years.

16. Operating budgets include all of the following except the:

A. sales budget.

B. production budget.

C. capital expenditure budget.

D. budgeted income statement.

17. Each of the other budgets in the master budget depends on the:

A. budgeted income statement.

B. cash budget.

C. production budget.

D. sales budget.

18. In the direct materials budget, the quantity of direct materials to be purchased is computed by adding direct materials required for production to:

A. desired ending direct materials.

B. beginning direct materials.

C. desired ending direct materials less beginning direct materials.

D. beginning direct materials less desired ending direct materials.

19. The direct labor budget and the manufacturing overhead budget depend on the:

A. budgeted income statement.

B. cash budget.

C. production budget.

D. sales budget.

20. The important end-product of the operating budgets is the:

A. budgeted income statement.

B. cash budget.

C. production budget.

D. budgeted balance sheet.

21. Financial budgets consist of all of the following except the:

A. cash budget.

B. capital expenditure budget.

C. budgeted income statement.

D. budgeted balance sheet.

22. The budget that is often considered to be the most important financial budget is the:

A. cash budget.

B. capital expenditure budget.

C. budgeted income statement.

D. budgeted balance sheet.

23. The cash budget contains sections for each of the following except:

A. financing.

B. cash receipts.

C. cash disbursements.

D. capital expenditures.

24. Budgets are used by all of the following except:

A. merchandisers.

B. service enterprises.

C. not-for-profit organizations.

D. All of these organizations use budgets.

25. In the merchandise purchases budget, required merchandise purchases are computed by adding:

A. budgeted sales and desired ending merchandise inventory together.

B. budgeted cost of goods sold and desired ending merchandise inventory together.

C. budgeted sales and desired ending merchandise inventory together and deducting beginning merchandise inventory.

D. budgeted cost of goods sold and desired ending merchandise inventory together and deducting beginning merchandise inventory.

This is the end of the test. When you have completed all the questions and reviewed your answers, press the button below to grade the test.

Grade the Test

0% (0 out of 25 correct)

1. Budgeting facilitates the coordination of activities within the business by correlating the goals of each segment with overall company objectives.

A. True B. False

2. The most common budget period is one month. A. True B. False

3. The chief accountant (controller) has responsibility for coordinating the preparation of the budget.

A. True B. False

4. The master budget is a set of interrelated budgets that constitutes a plan of action for a specified time period.

A. True B. False

5. The budgeted income statement is the starting point in preparing financial budgets. A. True B. False

6. The production budget is the first budget prepared in the master budget. A. True B. False

7. The direct materials budget shows both the quantity and cost of direct materials to be purchased.

A. True B. False

8. The financing section of a cash budget shows expected borrowings and the repayment of borrowed funds plus interest.

A. True B. False

9. The budgeted balance sheet is developed from the budgeted balance sheet for the preceding year and the budgets for the current year.

A. True B. False

10. A merchandiser uses a merchandise purchases budget in addition to a production budget.

A. True B. False

11. Which of the following are correct statements about a budget? A. It is a formal written statement of management's plans for a specified future

time period. B. It becomes an important basis for evaluating performance. C. It promotes efficiency and serves as a deterrent to waste and inefficiency. D. All of these options are correct statements.

12. The primary benefits of budgeting include all of the following except it: A. requires only top management to plan ahead and formalize goals. B. provides definite objectives for evaluating performance. C. creates an early warning system for potential problems. D. motivates personnel throughout the organization.

13. The most common budget period is a: A. week. B. month. C. quarter. D. year.

14. Coordinating the preparation of the budget is the responsibility of the: A. treasurer. B. president. C. chief accountant. D. budget committee.

15. Long-range planning usually encompasses a period of:

A. a quarter. B. a year. C. at least two years. D. at least five years.

16. Operating budgets include all of the following except the: A. sales budget. B. production budget. C. capital expenditure budget. D. budgeted income statement.

17. Each of the other budgets in the master budget depends on the: A. budgeted income statement. B. cash budget. C. production budget. D. sales budget.

18. In the direct materials budget, the quantity of direct materials to be purchased is computed by adding direct materials required for production to:

A. desired ending direct materials. B. beginning direct materials. C. desired ending direct materials less beginning direct materials. D. beginning direct materials less desired ending direct materials.

19. The direct labor budget and the manufacturing overhead budget depend on the: A. budgeted income statement. B. cash budget. C. production budget. D. sales budget.

20. The important end-product of the operating budgets is the: A. budgeted income statement. B. cash budget. C. production budget. D. budgeted balance sheet.

21. Financial budgets consist of all of the following except the: A. cash budget. B. capital expenditure budget. C. budgeted income statement. D. budgeted balance sheet.

22. The budget that is often considered to be the most important financial budget is the: A. cash budget. B. capital expenditure budget. C. budgeted income statement. D. budgeted balance sheet.

23. The cash budget contains sections for each of the following except: A. financing. B. cash receipts. C. cash disbursements. D. capital expenditures.

24. Budgets are used by all of the following except: A. merchandisers. B. service enterprises. C. not-for-profit organizations. D. All of these organizations use budgets.

25. In the merchandise purchases budget, required merchandise purchases are computed by adding:

A. budgeted sales and desired ending merchandise inventory together. B. budgeted cost of goods sold and desired ending merchandise inventory

together. C. budgeted sales and desired ending merchandise inventory together and

deducting beginning merchandise inventory. D. budgeted cost of goods sold and desired ending merchandise inventory together

and deducting beginning merchandise inventory.

Retake Test