Embed Size (px)

Citation preview

1

PSU Professional Development Center

Welcomes You!

Carmen SchwisowProgram ManagerTwitter@PSU_HR

www.pdx.edu/professional-development/hrProfessional Development Center

Welcome! • Thank you• Healthcare Reform in PDX HR • How the HR Certificate at Portland State can help• Introduction of Panelists & Program

www.bullardlaw.com

Federal Health Care Reform Laws

The Patient Protection and Affordable Care Act and the companion Health Care and Education Reconciliation Act will affect employee health plans and other benefits

The new laws are phased in over many years Election results and legal challenges may lead to

changes

www.bullardlaw.com

Outstanding Issues

2012 Presidential election States – delay exchange funding? Decline Medicaid

expansion funds? Challenges to contraception mandate Creation of exchanges Guidance pending from IRS/DOL/HHS

www.bullardlaw.com

Provisions Effective in 2012

Four-page (double-sided) summary of benefits Plans must give 60 days’ advance notice of

changes to summaries Penalty for noncompliance – up to $1k per

person per day W-2 reporting on cost of coverage

Women’s Health Care Services

For plan years starting on or after 8/1/12, non-grandfathered plans must include – Well-woman visits Gestational diabetes screening Contraception (subject to exception for religious

employers) Nursing support and supplies Domestic violence screening and counseling

www.bullardlaw.com

www.bullardlaw.com

Provisions Effective in 2013

FSA contributions limited to $2,500 (indexed) Medicare hospital insurance tax increased from

1.45% to 2.35% on employee share for earned income over $200k ($250k if joint)

2.9% excise tax on medical device makers; may be passed on

Employers must give notice of health insurance exchange and premium credits, effective 3/1/13

Provisions Effective in 2014

Play-or-pay mandate for employers with at least 50 FTE employees

Waiting periods limited to 90 days Non-grandfathered plans must cover clinical

trials for cancer or similar conditions Wellness programs may offer up to 30%

reward (up from current 20%)

www.bullardlaw.com

www.bullardlaw.com

Caution!

Multiple bills make for confusion – be careful where you get your information

Guidance regularly being issued by Internal Revenue Service and U.S. Departments of Labor and Health & Human Services

This is general information, not legal advice

Confidential | Planar Systems10

Chiefly competitive reasons

Hard to attract and retain employees without health coverage

There would be a huge advantage to those employers offering health coverage in attracting the best candidates

Confidential | Planar Systems11

Chiefly competitive reasons

Hard to attract and retain employees without health coverage

There would be a huge advantage to those employers offering health coverage in attracting the best candidates

Confidential | Planar Systems12

Employers also continue health coverage

Employers feel moral obligation to provide health coverage Need access to care for employees to be productive Cannot image not offering health coverage in mature industries Wage increases traded for health coverage maintenance in past

Executives demand health coverage Do not want total cost of health coverage to be imputed income now

Cadillac plan results in some imputed income in 2018

Confidential | Planar Systems13

Health Care offered in the US Bureau of Labor Statistics 2009 National Compensation Survey

• Latest data published nationally

• 74% offered medical plan• 76% enroll

• 48% offered dental plan• 79% enroll

• 20% offered vision plan • 77% enroll

• Medical coverage offered to 88% FT ees• Medical coverage offered to 24% PT ees

• 58% PT ees enroll

Greater income, education, skills more likely to have coverage

Healthcare Changes

Challenges and Strategies from an HR Department Manager’s Perspective

Context for Employee Benefits

Financial context: While average wages and salaries have increased by 1-

3% per year recently, medical insurance has increased an average of 9-12%

Benefits constitute 40.2% of payroll costs*

HR Directors need to control costs for both the company and for employees

*US Chamber of Commerce 2004 data

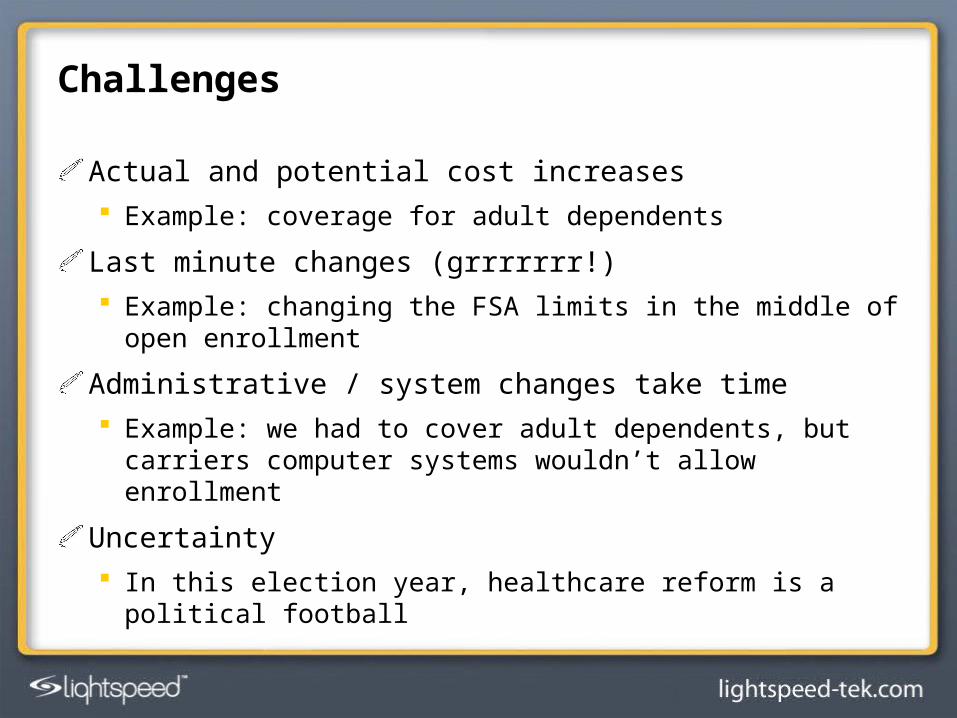

Challenges

Actual and potential cost increases Example: coverage for adult dependents

Last minute changes (grrrrrrr!) Example: changing the FSA limits in the middle of open

enrollment

Administrative / system changes take time Example: we had to cover adult dependents, but carriers

computer systems wouldn’t allow enrollment

Uncertainty In this election year, healthcare reform is a political

football

Strategies

Partner with your benefits broker and insurance carriers for information

Stay nimble… change is pretty much inevitable

Work at balancing business needs with employee needs

1818

is an Independent Licensee of the Blue Cross and Blue Shield Association.

The Regence Group

Jim Walton, Director of New Sales

Regence BlueCross

BlueShield of Oregon

Jim Walton, Director of New Sales

Regence BlueCross

BlueShield of Oregon

Exchange 2.0Fall/Winter 2012 PSU HR Presentation

Exchange 2.0Fall/Winter 2012 PSU HR Presentation

Regence

Blu

eC

ross

Blu

eShie

ld o

f O

regon

is a

n Independent

Lice

nse

e o

f th

e B

lue C

ross

and B

lue S

hie

ld A

ssoci

ati

on

© 2012. The Regence Group, all rights reserved.

19

Oregon Exchange – Structure

•Public corporation- own entity• Similar to SAIF, or OHSU

•Governance:

• Citizen Board – 9 Members• Appointed by the Governor and were confirmed by the Senate-

September 23, 2011 • At least 2 consumer members, and no more than 2 members can

have ties to insurance or health care industry

• Board makes decisions, not recommendations

20

The Oregon Health Insurance Exchange Corporation

Mission Statement

Improving the health of all Oregonians by providing health coverage options, increasing access to information, and fostering quality and value in the health care system.

21

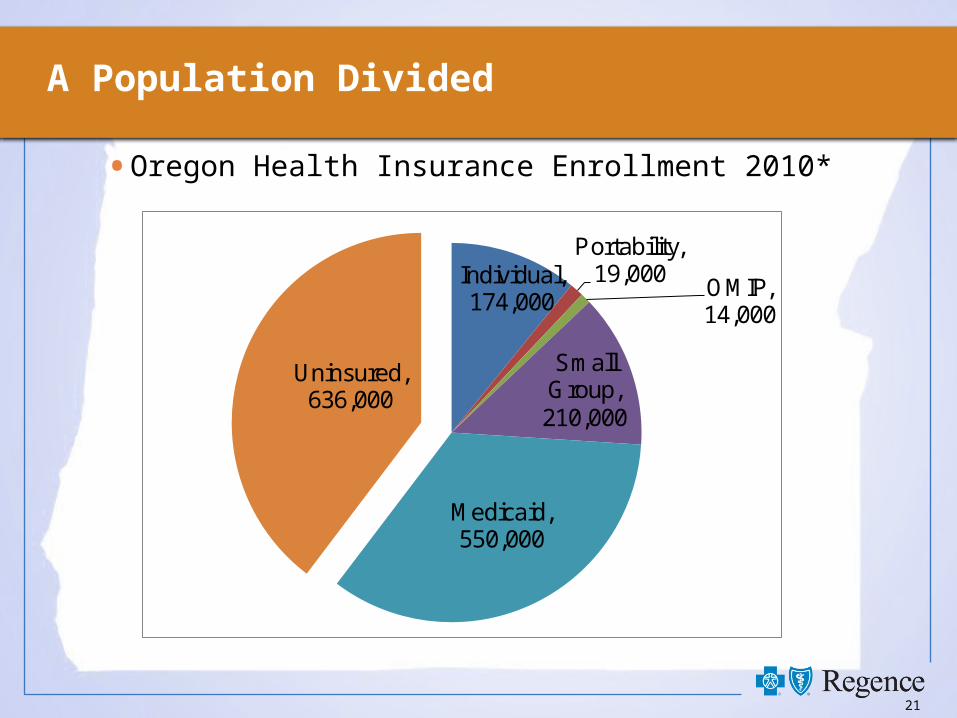

A Population Divided

• Oregon Health Insurance Enrollment 2010*

Individual, 174,000

Portability, 19,000

OMIP, 14,000

Small Group, 210,000

Medicaid, 550,000

Uninsured, 636,000

22

Individual Exchange: Tax Credits and Cost-Sharing Reductions

• Exchange and HHS determine if

individual is eligible for tax subsidy and cost share

subsidy

• Available only to individuals purchasing in Exchange• Sliding credit amount based on 133% - 400% Federal Poverty

Level (FPL)

• Not available to groups members in Exchange

• Cost Sharing Credit available up to 250% FPL• One third, one half or two thirds credit on out of pocket costs

23

Exchange Premium Limits by Income

•Up to 133% FPL: 2.0% of income

•133-150% FPL: 3.0% - 4.0% of income

•150-200% FPL: 4.0% - 6.3% of income

•200-250% FPL: 6.3% -8.05% of income

•250-300% FPL: 8.05% - 9.5% of income

•300-400% FPL: Capped to 9.5% of income

24

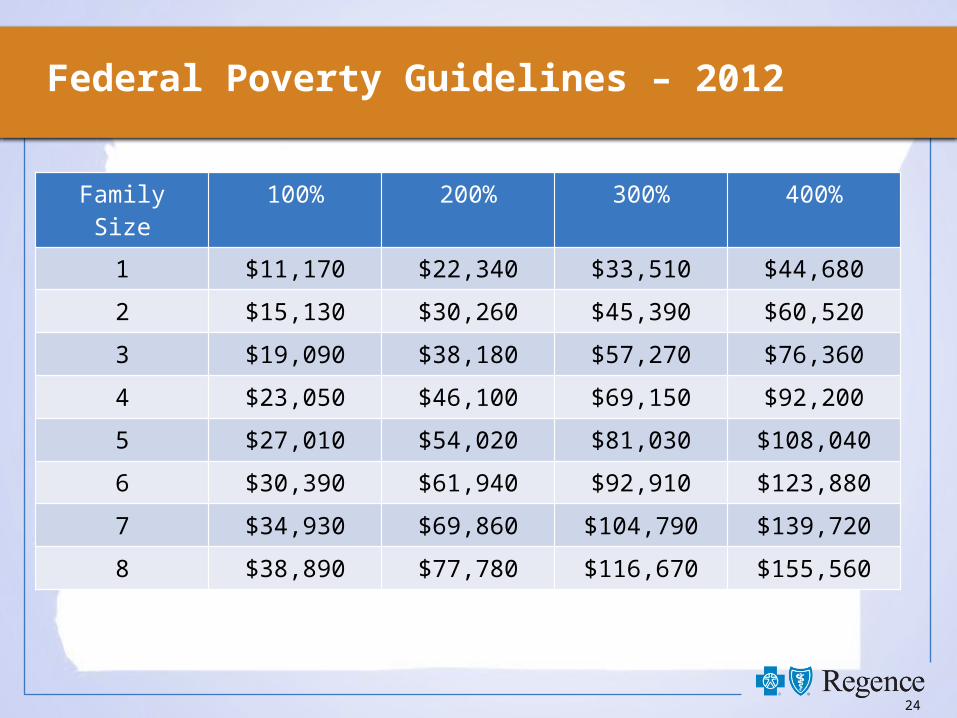

Federal Poverty Guidelines – 2012

Family Size 100% 200% 300% 400%

1 $11,170 $22,340 $33,510 $44,680

2 $15,130 $30,260 $45,390 $60,520

3 $19,090 $38,180 $57,270 $76,360

4 $23,050 $46,100 $69,150 $92,200

5 $27,010 $54,020 $81,030 $108,040

6 $30,390 $61,940 $92,910 $123,880

7 $34,930 $69,860 $104,790 $139,720

8 $38,890 $77,780 $116,670 $155,560

25

Individual Example

• Let’s do some math…Single Parent/Two Kids• $700 monthly premium. (2nd lowest Silver Plan)

• Annual income $38,180 (200% FPL)• Premium percentage is 6.0% of annual income, or $2,223.6 ($185

per month)• Advance credit is $700 (premium) – $185 (max allowed premium

percentage)= $515/month• ½ Cost Subsidy (deductibles, co pays, co-insurance, max out of

pocket)

26

Cost Sharing Subsidies

Cost Subsidy 0% 1/3 1/2 2/3

Federal Poverty Level 251%+ 201-250% 151-200% 133-150%

Actuarial Value - Possible Silver Plan Base - 70% 73% 87% 94%

Deductible - Individual $1,750 $1,750 $500 $50

Maximum out of Pocket - Individual $5,750 $4,000 $1,200 $600

Copay / Coinsuran

ce

Copay / Coinsuran

ce

Copay / Coinsuran

ce

Copay / Coinsuran

ce

Inpatient and Outpatient 30% 30% 30% 10%

Emergency Room 30% 30% 30% 10%

Preventive Visits and Services $0 $0 $0 $0

Office Visits - Primary Care $35 $35 $35 $10

Office Visits - Specialists $60 $60 $60 $25

Prescription Drug - Generic $10 $10 $10 $5

Prescription Drug - Preferred Brand 50% 50% 50% 30%Prescription Drug - Non-Preferred Brand 50% 50% 50% 50%

27

Individual Eligibility

Questions?